Western retail gold investors often fear rising interest rates because they mistakenly view the Federal Reserve as the ultimate force behind bond market movements. In reality, long-term interest rates are largely shaped by market dynamics, and the Fed’s influence may be far less significant than many assume.

From a broader perspective, extremely high interest rates coupled with persistent inflation could become one of the strongest catalysts for a major rally in gold prices. Investors should at least consider the possibility of a future environment where market-driven forces push yields dramatically higher, potentially coinciding with a substantial rise in gold.

Historical examples show that governments often react to inflation rather than control it. In countries that experienced severe inflationary pressures, interest rates were forced sharply higher as policymakers struggled to restore stability. Some analysts argue that similar risks, although on a much smaller scale today, are not being fully reflected in U.S. financial markets.

A key concern is the growing burden of government debt. If Treasury yields were to rise significantly, interest expenses could consume an increasingly large share of federal revenues, placing additional strain on public finances. Critics argue that markets may be underestimating this risk.

Quantitative easing (QE) proved effective during periods of disinflation and financial stress, largely supporting asset prices and market liquidity. However, in an environment where inflation remains elevated, renewed large-scale monetary stimulus could have very different consequences, potentially intensifying inflationary pressures felt by households.

Throughout history, societies have often focused on entertainment and short-term distractions during periods of economic uncertainty rather than preparing for potential financial upheaval. Advocates of gold believe the current environment presents a similar lesson: maintaining exposure to hard assets may offer protection against the long-term risks associated with inflation, debt accumulation, and currency debasement.

The long-running battle between gold and fiat currencies can be viewed as a contest between financial discipline and governments burdened by chronic overspending, rising debt levels, and an increasing reliance on monetary expansion.

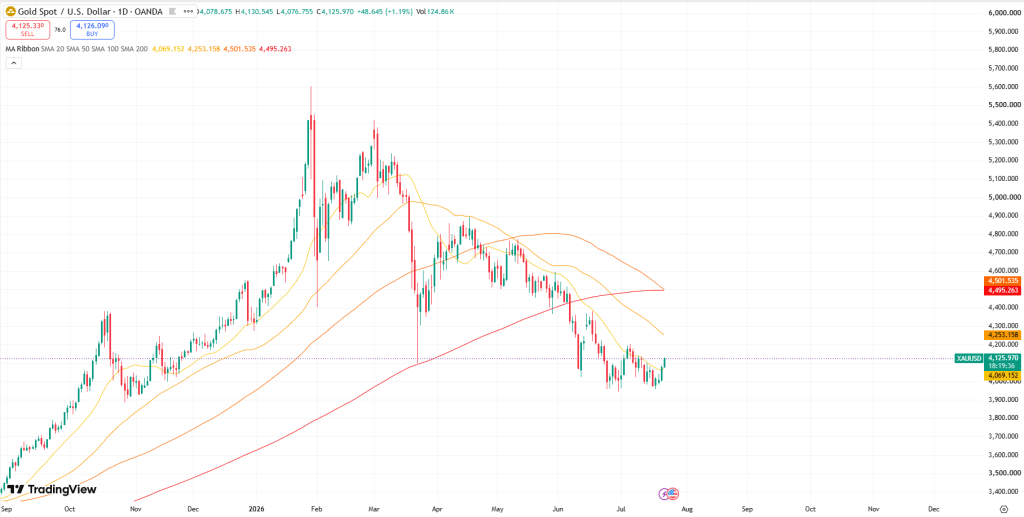

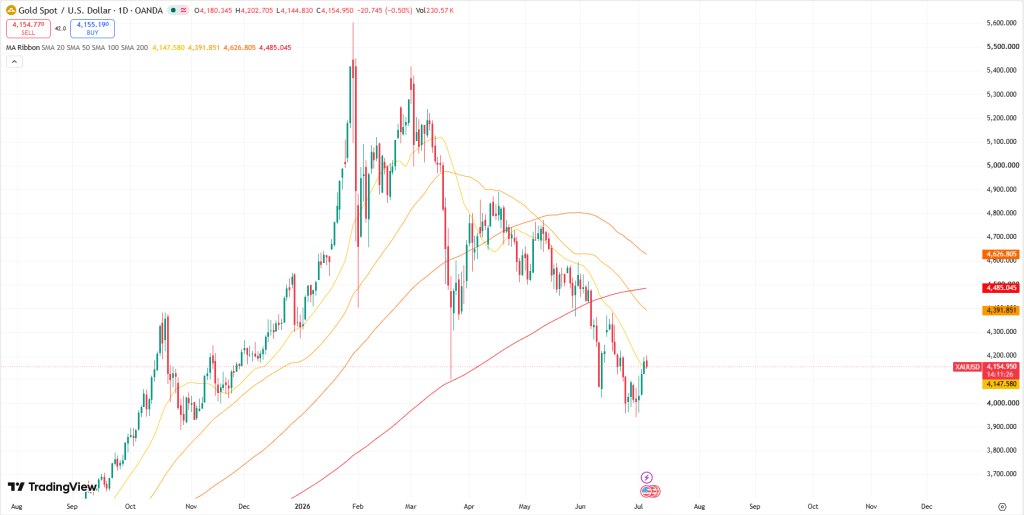

Gold Spot ($GOLD – Daily Chart)

Gold’s recent price action has produced a notable technical breakout, a development that many market participants see as an important bullish signal.

Investors have been encouraged to pay close attention to gold’s retreat toward the psychologically significant $4,000 level. From recent highs, this represents roughly a 30% correction, creating what some analysts consider a rare long-term accumulation opportunity.

The broader $3,900–$4,100 range is increasingly being viewed as a high-conviction buying zone for investors seeking strategic exposure to the precious metal.

From a technical perspective, gold has broken above a key downward trendline, suggesting that bearish momentum may be fading. If the breakout is sustained, the next major target could be the higher resistance trendline near $4,400, implying further upside potential in the weeks ahead.

Gold and Silver Outlook

Looking at the weekly gold chart, several outcomes remain possible, and a scenario involving substantially higher prices cannot be ruled out. Some analysts argue that gold reaching $9,000 is conceivable even in an environment where interest rates rise toward 9%, particularly if inflation remains elevated or accelerates further.

Historical examples such as Venezuela and Zimbabwe demonstrate that governments can continue operating despite extremely high interest rates, largely because inflation was even higher. In such environments, nominal rates rise in response to inflationary pressures rather than acting as a constraint on them.

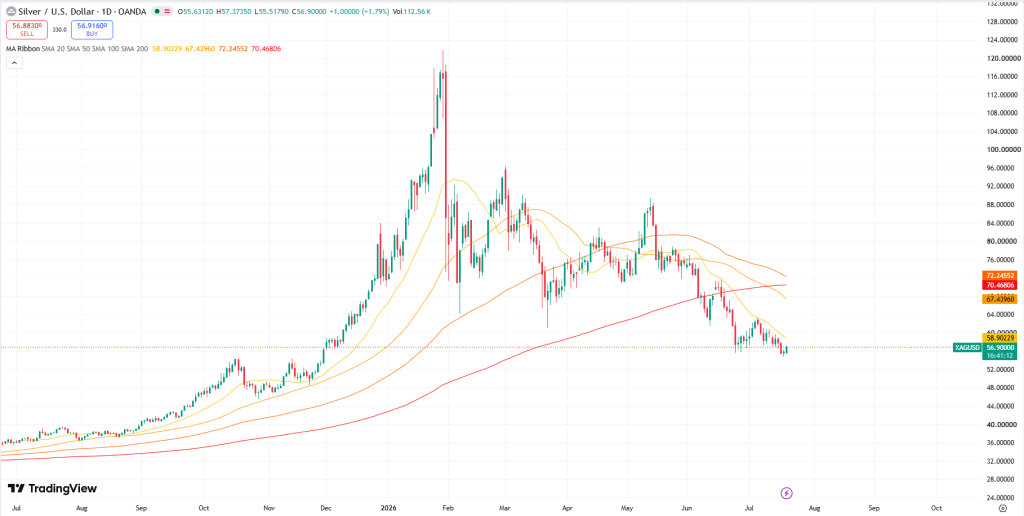

Silver Spot ($SILVER – Daily Chart)

Silver’s technical picture also appears increasingly constructive. Investors who accumulated the metal during the recent pullback—particularly as gold traded within the $3,900–$4,100 accumulation zone—are now seeing the market move in their favor.

The latest breakout signals strengthening bullish momentum, with silver appearing poised for a rapid advance. If current trends continue, the metal could target the $80 level, while an extension of the rally may open the door to prices approaching $90 over the longer term.

Overall, both precious metals continue to attract attention as investors seek potential protection against inflation, currency debasement, and mounting sovereign debt concerns.

Mining stocks are also beginning to show renewed strength. A review of the CDNX Index suggests that momentum is building across the junior resource sector, with technical indicators increasingly aligning in favor of the bulls.

From a chart perspective, the index appears to have entered a more constructive phase, as key signals—including trend direction, price structure, and momentum measures—have turned positive. In other words, the technical backdrop has improved significantly, leading some analysts to conclude that all major technical indicators are now flashing green for the CDNX.

If precious metals continue their advance, the improving technical outlook could position junior mining shares to benefit from increased investor interest and capital flows into the sector.

Gold mining stocks are presenting an increasingly attractive technical setup, according to some market analysts. The latest chart of the GDX Gold Miners ETF highlights several key accumulation zones that have historically offered favorable risk-reward opportunities for investors.

With gold, silver, and mining equities having already completed what appears to be a three-wave corrective decline, the sector may now be positioned for a much larger advance. Supporters of the bullish case argue that investors who accumulated positions during gold’s pullback into the $3,900–$4,100 range have already secured attractive entry points, while momentum-focused investors may now be receiving confirmation as prices begin to trend higher.

If the rally in precious metals continues to strengthen, GDX could potentially challenge—and in an especially bullish scenario, surpass—its previous all-time highs. Such a move would likely be supported by rising gold prices, improving sentiment, and increased capital flows into mining shares.

The broader investment thesis remains centered on concerns over expanding government debt, persistent inflation risks, and currency debasement. From this perspective, advocates of precious metals view gold as a long-term store of value and a potential hedge against fiscal and monetary instability, making it an important component of a diversified portfolio.

President Trump warned that any Houthi attempts to disrupt critical Saudi oil export routes would be met with retaliatory military action.

An attack on a Kuwaiti oil tanker has underscored the persistent security risks facing key shipping lanes in the Persian Gulf.

Strikes targeting Black Sea export terminals threaten the main corridor responsible for transporting most of Kazakhstan’s crude oil exports.

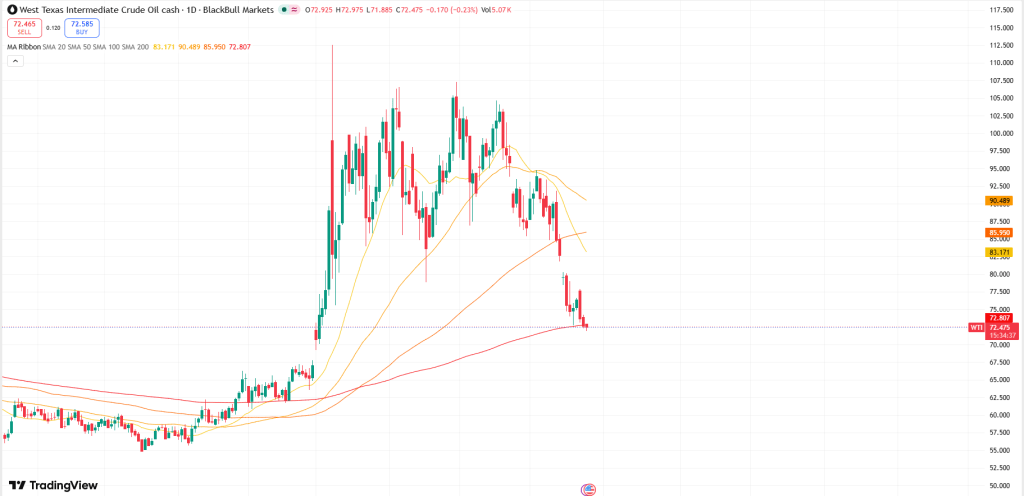

WTI crude oil extended its rally for a second straight session, trading near $84.60 per barrel during Wednesday’s Asian session as growing supply concerns across several major export routes supported prices. The latest gains reflect rising geopolitical risks that now extend beyond the Middle East, raising fears of potential disruptions to global energy flows.

In the United States, President Donald Trump downplayed the prospects of near-term negotiations with Iran and warned that further military action remains possible. He also pledged a swift response if Iran-backed Houthi forces follow through on threats to target commercial vessels operating in the Red Sea.

The Red Sea has become an increasingly important export route for Saudi Arabia during the regional conflict. By diverting part of its crude shipments through pipelines to Red Sea ports, the kingdom has reduced its dependence on the strategically sensitive Strait of Hormuz. Nevertheless, maritime security concerns remain elevated, highlighted by a recent attack on a Kuwaiti tanker transporting oil products through the Gulf region.

Meanwhile, supply risks are not limited to the Middle East. Market participants are also watching repeated drone strikes targeting the Caspian Pipeline Consortium terminal on Russia’s Black Sea coast. The facility serves as a crucial export gateway for Kazakhstan, handling most of the country’s crude oil shipments to international markets, making any disruption a potential threat to global supply.

Gold surged to a two-week high above the $4,100 mark during Wednesday’s Asian trading session. The precious metal found support from optimism that diplomatic initiatives could help ease geopolitical tensions. However, persistent concerns over energy-related inflation continue to strengthen expectations that the Federal Reserve may maintain a hawkish stance on interest rates. Higher rate-hike expectations, coupled with escalating US-Iran tensions, could provide support for the US Dollar and potentially limit further gains in gold prices.

Fundamental Analysis

The US Dollar (USD) traded with a stronger tone on Tuesday, but Gold also advanced, an unusual combination that highlighted rising market uncertainty. The precious metal moved further away from the key $4,000 level and hovered near an intraday high of $4,084, reflecting strong demand for safe-haven assets. Notably, Gold appeared to be outperforming the USD, a rare occurrence during periods of heightened risk aversion.

Investor concerns intensified after US President Donald Trump threatened to impose sweeping 50% tariffs on a range of Canadian goods, accusing Ottawa of maintaining unfair trade practices against American products. Although some market participants viewed the threat as a negotiating tactic, the announcement reinforced worries that trade tensions could contribute to longer-lasting inflationary pressures.

As the US trading session progressed, Gold, the US Dollar, and Wall Street equities all moved higher simultaneously—an uncommon market dynamic. The gains came despite fresh comments from President Trump indicating a willingness to escalate military action against Iran while signaling that negotiations with Tehran were no longer a priority, adding another layer of geopolitical uncertainty to global markets.

Technical Analysis

While recent price action has improved, it may be premature to confirm a sustained bullish breakout in XAU/USD. On the four-hour chart, gold maintains a constructive tone, trading above both the 100-period SMA at $4,067.46 and the 20-period SMA at $4,017.34. However, the 200-period SMA at $4,133.13 continues to act as a significant resistance barrier. Supporting the near-term bullish outlook, the RSI is trending higher around 61, while the Momentum indicator remains firmly positive, signaling strengthening upside pressure.

The broader daily chart presents a more cautious picture. Gold remains well below the 100-day and 200-day SMAs, located at $4,510.85 and $4,495.98 respectively, indicating that the longer-term trend remains under pressure. The metal is holding just above the 20-day SMA at $4,062.64, which provides immediate support and suggests consolidation rather than a confirmed trend reversal. Momentum indicators remain mixed, with the RSI near 46 and the 14-day Momentum indicator still below its midpoint, reflecting only a modest improvement in underlying sentiment.

From a technical perspective, initial support is found around the confluence of the 100-period SMA at $4,067.46 and the 20-day SMA at $4,062.64. A deeper pullback could target the 20-period SMA near $4,017.34. On the upside, the primary resistance remains the 200-period SMA at $4,133.13. A decisive break above this level would strengthen the bullish case and could pave the way for a move toward the $4,200 region.

Gold attracts renewed buying interest during Tuesday’s Asian session, although its upside remains limited. Persistent inflation concerns continue to reinforce expectations that the Federal Reserve will keep interest rates elevated, providing support for the US Dollar and reducing the appeal of the non-yielding precious metal. At the same time, lingering geopolitical tensions between the United States and Iran are underpinning demand for the greenback, prompting traders to remain cautious about chasing further gains in gold.

Gold (XAU/USD) extends its rebound during Tuesday’s European session, climbing to its highest level in four days around the $4,075 area as the US Dollar eases amid renewed hopes for diplomacy between Washington and Tehran.

The precious metal draws support after US Secretary of State Marco Rubio stated on Sunday that the United States remains willing to engage in negotiations with Iran despite the recent exchange of military strikes. The remarks have tempered demand for the US Dollar by encouraging optimism that the conflict could eventually be resolved through diplomatic channels.

However, Gold’s upside remains constrained as investors continue to price in the inflationary risks stemming from rising energy costs. Disruptions to oil shipments through the Strait of Hormuz, combined with Yemen’s Iran-backed Houthi movement announcing a maritime blockade targeting Saudi Arabia, have reinforced expectations of tighter global crude supplies. Higher oil prices could fuel inflation and strengthen the case for the Federal Reserve to maintain restrictive monetary policy for longer.

Market expectations continue to reflect that view. According to the CME FedWatch Tool, traders see roughly an 83% chance that the Fed will raise interest rates before the end of the year. The prospect of higher US borrowing costs supports the US Dollar and limits demand for non-yielding assets such as Gold.

Meanwhile, geopolitical tensions remain elevated despite the diplomatic signals. The United States has reportedly carried out a tenth consecutive night of strikes on Iranian targets, with the White House indicating that military operations will continue until President Donald Trump decides otherwise. Iran has responded with retaliatory attacks against US military facilities and allied infrastructure across the Gulf, keeping concerns over a broader regional conflict firmly in focus.

With geopolitical risks continuing to underpin the US Dollar’s safe-haven appeal and expectations for prolonged Fed tightening remaining intact, traders may prefer to wait for stronger confirmation before concluding that Gold has established a near-term bottom, particularly in the absence of major US economic data releases on Tuesday.

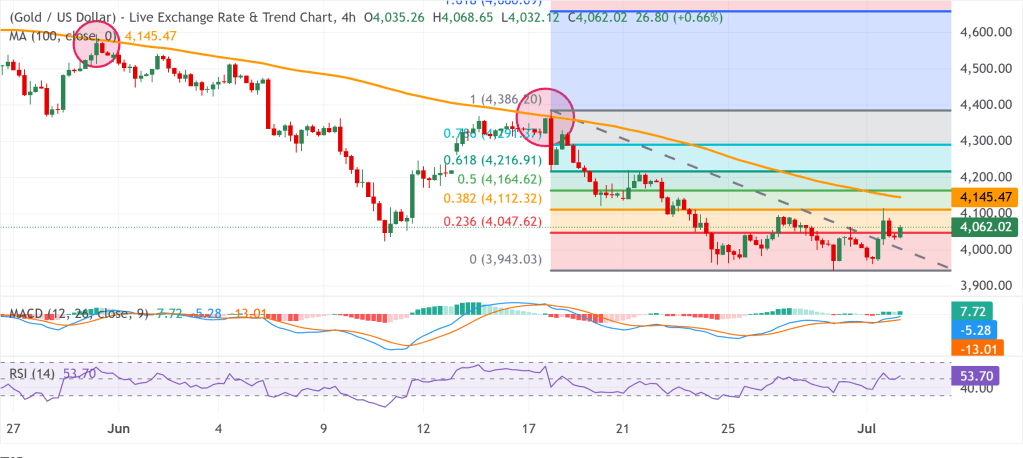

Gold H4 Chart

Gold continues to trade with a positive intraday tone after breaking above the 23.6% Fibonacci retracement of the decline from the July peak and pushing through a short-term descending trendline. This technical breakout strengthens the bullish outlook, while momentum indicators also show improving conditions. Both the Moving Average Convergence Divergence (MACD) and the Relative Strength Index (RSI) are pointing higher, indicating that selling pressure is gradually easing.

Even so, the broader near-term outlook remains cautious as long as XAU/USD stays below the 100-period Simple Moving Average (SMA) on the 4-hour chart and several key Fibonacci resistance levels. Any continued advance is therefore likely to encounter resistance first near the 38.2% Fibonacci retracement at $4,052.78, followed by the 100-period SMA at $4,067.29 and the 50.0% retracement at $4,081.40.

If bullish momentum extends beyond those levels, the 61.8% Fibonacci retracement at $4,110.01 could provide a more formidable resistance zone. On the downside, initial support is located around $4,017, where the 23.6% Fibonacci level aligns with the recently broken trendline. A stronger support base sits near $3,960.14, the key Fibonacci anchor, where buyers may step back in should the current pullback deepen.

Major currency pairs traded within familiar ranges early Tuesday as investors avoided making aggressive moves while monitoring developments in the Middle East. Attention now turns to Germany and the Eurozone’s ZEW Economic Sentiment surveys, while the US economic calendar remains light for the remainder of the day.

After Monday’s volatile session, crude oil prices eased modestly, with West Texas Intermediate (WTI) slipping around 0.5% to trade near $82 per barrel. Oil initially retreated after reports suggested mediators had proposed a 10-day ceasefire between the United States and Iran to revive diplomatic negotiations. However, hostilities continued to escalate.

US President Donald Trump warned that Iran would face consequences following the deaths of American service members, while US forces carried out strikes for a tenth consecutive day, targeting areas near Sirik, Bandar Abbas, Qeshm Island, Chabahar, and Konarak. Iran responded with attacks on US assets across the Gulf, keeping geopolitical tensions elevated.

Oil Supported by Ongoing Geopolitical Risks

Despite signs of diplomatic engagement, analysts remain cautious. Deutsche Bank noted that Iran acknowledged receiving proposals from international mediators, but escalating rhetoric from both Yemen’s Houthi movement and President Trump helped push Brent crude to settle 1.27% higher at $89.22 per barrel.

OCBC warned that any broader escalation could revive concerns over a prolonged disruption to global oil supplies, potentially lifting crude prices back above $100 per barrel. Such a scenario could increase market volatility, weaken demand for carry trades, and reinforce demand for the US Dollar as investors seek safe-haven assets.

Fed Faces Fresh Inflation Concerns

The US Dollar Index (DXY) extended Monday’s gains by more than 0.2%, although it traded sideways just below the 101.00 level during Tuesday’s European session.

According to Commerzbank’s Volkmar Baur, persistently high energy prices could make it increasingly difficult for the Federal Reserve to avoid raising interest rates. While policymakers typically focus on core inflation, sustained increases in oil prices risk feeding into broader inflation through second-round effects, complicating the Fed’s policy outlook.

Sterling Softens Despite Stable Labor Market

UK labor market data showed the ILO unemployment rate remained unchanged at 4.9% in the three months to May. Meanwhile, average earnings excluding bonuses increased 4.3% year-over-year, below expectations of 4.5%.

The softer wage growth limited Sterling’s recovery, although GBP/USD edged slightly higher to around 1.3450 after three consecutive daily declines. Investors now await Wednesday’s UK inflation report.

New Zealand Dollar Outperforms After Inflation Surprise

New Zealand’s second-quarter inflation accelerated more than expected, with the annual Consumer Price Index (CPI) rising to 4.1%, up from 3.1% in the previous quarter and exceeding forecasts of 4.0%.

The stronger inflation reading boosted expectations that the Reserve Bank of New Zealand could maintain a restrictive policy stance, lifting NZD/USD above 0.5850, its strongest level since early June.

Euro, Canadian Dollar and Yen Hold Steady

EUR/USD traded quietly around 1.1420 after posting modest losses on Monday.

USD/CAD remained above 1.4050 despite Canadian inflation slowing to 2.8% in June from 3.2% previously. The Canadian Dollar also faced pressure after the White House announced that President Trump would impose 50% tariffs on most Canadian imports, citing what Washington described as discriminatory treatment of US automobiles, alcohol, and dairy products.

Meanwhile, USD/JPY held near 162.50. Japanese Prime Minister Sanae Takaichi stated that the government would continue balancing economic support with fiscal sustainability while working to preserve market confidence.

Oil Still Matters: Ranking the World’s Top 10 Producers

Oil has been pronounced obsolete countless times, yet global consumption still exceeds 100 million barrels per day.

Beyond fueling airplanes, trucks, and cargo ships, petroleum serves as a key ingredient in plastics, fertilizers, chemicals, pharmaceuticals, and thousands of everyday products that consumers rarely connect to crude oil.

According to OPEC projections, worldwide oil demand is expected to rise to 113.3 million barrels per day by 2030 and 124.1 million by 2050, with non-OECD nations driving most of the increase. Despite the global push toward alternative energy, oil is set to remain a cornerstone of the world economy for decades.

Below is a ranking of the world’s 10 largest oil-producing nations based on the latest data from the U.S. Energy Information Administration (EIA), reflecting 2025 production levels.

10. Kuwait | 2.6 Million Barrels Per Day

Although Kuwait ranks last on this list, it remains one of the richest countries in terms of oil reserves. The nation holds an estimated 101.5 billion barrels of crude, enough to sustain current production levels for roughly 100 years, while also benefiting from some of the lowest extraction costs globally.

Production, however, has fallen below its traditional pace of around 3 million barrels per day. Through the state-owned Kuwait Petroleum Corporation, the oil sector remains the backbone of the economy, generating approximately 90% of government revenues and export earnings.

Kuwait highlights an important reality: possessing vast reserves is not the same as maximizing their economic value.

9. Brazil | 3.8 Million Barrels Per Day

Brazil has emerged as one of the most compelling offshore oil success stories in recent decades. Its massive pre-salt reserves, buried beneath deep Atlantic waters and thick salt formations, require advanced technology and significant capital investment to develop.

Those investments are yielding results. Petrobras recently reported record output of 1.1 million barrels per day from the Búzios field alone, which now accounts for roughly one-third of the company’s Brazilian production.

As production expands, Brazil has become a major crude exporter and continues to offer investors exposure to highly productive fields with substantial growth potential.

8. United Arab Emirates | 3.8 Million Barrels Per Day

The UAE matched Brazil’s output at roughly 3.8 million barrels per day in 2025 but entered 2026 with a more aggressive production strategy.

Following its departure from OPEC in May, the country boosted output to a record 4.1 million barrels per day by June, signaling a desire to prioritize national production goals over cartel quotas.

Serving key Asian markets such as China, India, and Japan, the UAE has also invested heavily in refining, storage, port infrastructure, and pipeline networks. In periods of supply disruption, especially around the Strait of Hormuz, that logistical flexibility becomes a major strategic advantage.

7. Iran | 4.1 Million Barrels Per Day

Iran’s energy sector has long been shaped by geopolitics. Despite holding the world’s fourth-largest proven oil reserves and second-largest natural gas reserves, sanctions, conflict, and limited foreign investment have prevented the country from reaching its full production potential.

Output once exceeded 6 million barrels per day during the 1970s. Today, much of Iran’s oil trade relies on Chinese demand and a complex network of intermediaries designed to navigate sanctions.

Iran remains a critical player because any disruption to its exports can have an outsized effect on oil prices, particularly when tensions threaten traffic through the Strait of Hormuz, one of the world’s most important energy chokepoints.

6. China | 4.3 Million Barrels Per Day

While China is widely recognized as the world’s largest crude importer, it is also a significant producer.

Driven by energy-security concerns, Beijing has encouraged state-owned producers to boost domestic output. As a result, production climbed from approximately 3.8 million barrels per day in 2020 to a record 4.3 million in 2025.

PetroChina remains the country’s largest producer, while offshore specialist CNOOC has delivered notable growth. Increased exploration spending and new discoveries have also expanded reserve estimates.

Even so, China still imported roughly 11.55 million barrels per day in 2025. Aging fields and rising development costs suggest domestic production may be approaching practical limits, leaving imports as a crucial component of the nation’s energy strategy.

5. Iraq | 4.4 Million Barrels Per Day

Iraq possesses around 145 billion barrels of proven reserves, ranking among the largest resource holders globally.

Its oil fields are both extensive and relatively inexpensive to operate, giving the country the potential to produce far more crude than current levels suggest.

The challenge lies in infrastructure and export reliability. Roughly 93% of Iraqi crude exports pass through terminals near Basra on the Persian Gulf. Any disruption in the Strait of Hormuz can quickly create bottlenecks, forcing storage facilities to fill and production to slow.

Despite enormous geological advantages, logistical constraints and political challenges continue to limit Iraq’s full potential.

4. Canada | 5 Million Barrels Per Day

Canada stands as the only non-U.S. nation in the top five located entirely within North America, a valuable advantage amid growing geopolitical uncertainty.

Most Canadian production comes from Alberta’s oil sands, where heavy bitumen is either mined or extracted using steam-assisted recovery techniques.

Although oil sands projects require substantial upfront investment, they offer exceptionally long production lives and relatively low decline rates compared with shale wells.

Canada set another production record in 2025, with crude and equivalent output averaging 5.35 million barrels per day under broader regulatory measurements. Alberta alone contributed nearly 84% of national production.

3. Saudi Arabia | 9.6 Million Barrels Per Day

Saudi Arabia remains the most influential nation in the global oil market despite no longer holding the top production spot.

Output rose to approximately 9.6 million barrels per day in 2025 as OPEC+ gradually relaxed voluntary supply cuts.

Saudi Aramco oversees more than 260 billion barrels of proven reserves and operates some of the largest and lowest-cost oil fields ever discovered. More importantly, Saudi Arabia maintains significant spare production capacity that can be activated relatively quickly.

While most producers pump at maximum capacity, Saudi Arabia often has the ability to increase or decrease output strategically, giving it extraordinary influence over global oil prices.

2. Russia | 9.9 Million Barrels Per Day

Despite sanctions, production restraints, and the ongoing conflict in Ukraine, Russia remained the world’s second-largest oil producer in 2025 with roughly 9.9 million barrels per day.

The country has successfully redirected much of its crude exports toward Asia, with China and India becoming its dominant buyers.

However, the long-term outlook is more uncertain. Mature fields require increasing investment, while sanctions continue to limit access to advanced Western technology and financing.

Russia remains an energy giant, but sustaining current production levels could become increasingly challenging over time.

1. United States | 13.6 Million Barrels Per Day

The United States did more than lead the rankings in 2025—it achieved the highest crude oil production ever recorded by any country.

U.S. crude and condensate output averaged a record 13.6 million barrels per day, roughly 40% higher than production from either Russia or Saudi Arabia. Monthly production reached an all-time high of 13.93 million barrels per day in April.

At the center of this achievement is the Permian Basin in Texas and New Mexico, which produced approximately 6.6 million barrels per day and accounted for nearly half of total U.S. output.

Technological advances in horizontal drilling and hydraulic fracturing, combined with private mineral ownership, deep capital markets, and a competitive oil-services industry, transformed the United States into a global energy powerhouse.

Today, the country is also a major exporter of crude oil, gasoline, diesel, and refined petroleum products, strengthening both its trade position and domestic economy.

Why Oil Still Matters

Across much of the world, oil production is dominated by governments and state-owned enterprises. In contrast, private investment and publicly traded companies play a far greater role in North America.

Understanding where global oil supplies originate—and the economics behind bringing those barrels to market—can help investors better navigate future commodity cycles. Despite rapid growth in renewable energy, oil remains one of the most important resources underpinning modern civilization and the global economy.

Silver remains under pressure as escalating US-Iran tensions drive oil prices higher, stoking inflation concerns and reinforcing expectations of further Fed tightening.

Overnight US military strikes on Iran led Tehran to declare the ceasefire void, raising the risk of significant disruptions to global energy supply routes.

Cleveland Fed President Beth Hammack reiterated on Friday that inflationary pressures continue to persist.

Silver prices (XAG/USD) extended their advance for a second straight session, trading near $56.80 per troy ounce during Monday’s Asian session. Despite the recent rebound, the precious metal may encounter headwinds as escalating tensions between the United States and Iran continue to push crude oil prices higher, reviving inflation concerns and strengthening expectations that the Federal Reserve could tighten monetary policy further.

The US has carried out a ninth consecutive night of strikes against Iranian-linked targets. In response, Tehran announced that the ceasefire arrangement between the two countries is effectively over, raising concerns about potential disruptions to key energy transit routes across the Middle East.

Regional tensions intensified further after Iran launched a new barrage of ballistic missiles and one-way attack drones targeting locations in Bahrain, Jordan, Kuwait, and Iraq, triggering air raid warnings across parts of the Gulf. At the same time, the US military confirmed the death of another service member, bringing the total to three casualties within two days.

The conflict has increasingly affected civilian infrastructure, with reports of damage to bridges, utility networks, and port facilities. Adding to concerns over energy security, Kuwait Petroleum Corp. stated that one of its oil installations was struck by an Iranian attack over the weekend.

Although investors largely expect the Federal Reserve to leave interest rates unchanged at its next policy meeting, market expectations for tighter monetary policy have increased. According to CME FedWatch data, traders are now pricing in a 61.4% chance of a rate hike in September, reflecting growing concerns that higher energy prices could reignite inflationary pressures.

Hammack highlights widespread inflation risks, supporting a hawkish Fed outlook

Cleveland Fed President Beth Hammack delivered a notably hawkish message, earning a 7.2/10 FXS SpeechTracker score, comfortably above the historical average of 6.6/10. Her remarks reflected growing concern that inflationary pressures remain entrenched across the economy. By stressing calls from businesses for stronger measures to contain rising prices and noting that many households continue to struggle financially despite solid economic growth and resilient consumer spending, Hammack underscored the disconnect between healthy economic activity and increasing cost-of-living challenges.

She also pointed to several sources of inflation pressure, including elevated energy costs, supply-chain constraints, rising insurance expenses, and growing demand linked to AI infrastructure and data-center investments. By identifying persistent inflation as the primary risk facing policymakers, Hammack’s comments reinforced expectations that the Federal Reserve may maintain a restrictive policy stance for longer, providing underlying support for the US Dollar.

Meanwhile, the FXS Fed Sentiment Index climbed 2.06 points to 128.64, signaling that overall Fed communication remains firmly tilted toward tightening and well above the neutral threshold of 100. Combined with Hammack’s above-average hawkish score, the increase suggests that policymakers continue to prioritize inflation control over concerns about economic growth, a backdrop that generally favors the Dollar against lower-yielding currencies.

Light Sweet Crude posted strong gains over the past week, a move largely driven by persistent geopolitical tensions in the Middle East that continue to fuel concerns over potential supply disruptions.

The market appears firmly positioned to challenge the $85 per barrel mark. Any near-term weakness or corrective pullbacks are likely to attract fresh buying interest, particularly from short-term traders looking to capitalize on the prevailing bullish momentum.

Gold

Gold retreated below the $4,000 threshold once again during the week, remaining under pressure as investors continue to assess the interest rate outlook. Persistent concerns that elevated borrowing costs could reduce the appeal of non-yielding assets such as gold have weighed on market sentiment.

The $4,000 level remains a key technical support zone. A sustained hold above this area could help stabilize prices, while a decisive break lower may open the door to additional downside pressure.

Silver

Silver came under heavy selling pressure during the week, dropping to a fresh low before attempting a modest recovery heading into Friday’s session. Despite the rebound, the broader technical outlook remains weak, with rallies likely to encounter renewed selling interest as bearish sentiment continues to dominate the market.

The $50 level remains a significant support zone that has influenced price action on several occasions in the past. Given the current downward momentum, a move toward this area cannot be ruled out. Rising interest rates continue to undermine the appeal of non-yielding assets, leaving silver vulnerable to further declines and offering little incentive for bullish positioning at this stage.

CAC 40

The CAC 40 experienced volatile and range-bound trading throughout the week. However, following the sharp decline seen in the previous week, the recent consolidation can be viewed as a constructive sign that the market may be stabilizing. A decisive break above the 8,400 level could pave the way for further gains toward 8,500.

A sustained move beyond 8,500 would strengthen the bullish outlook and potentially trigger a broader upward advance. On the downside, the 8,000 area continues to provide significant support, and as long as the index remains above this level, the longer-term uptrend is likely to stay intact.

Natural Gas

Natural gas prices edged lower over the past week, extending the prevailing bearish trend. The weakness is largely consistent with seasonal demand patterns, as this period of the year typically experiences softer consumption. Under these conditions, short-term rebounds are likely to be viewed as selling opportunities rather than the start of a sustained recovery.

Market sentiment remains tilted to the downside, with traders likely to sell into rallies that show signs of losing momentum. A break below this week’s low could accelerate selling pressure and expose the $2.50 level as the next significant downside target. Given that the market is currently focused on the August contract, a substantial upward move appears unlikely unless an intense and widespread heatwave significantly boosts energy demand across the United States.

USD/CAD

The US dollar came under significant pressure against the Canadian dollar during the week, with the 1.40 level providing a measure of support heading into the weekend. Strength in crude oil prices has contributed to the Canadian dollar’s resilience, as rising energy prices generally benefit Canada’s commodity-linked currency.

The 1.40 area is likely to remain a closely watched support zone, making next week’s price action particularly important for determining the pair’s near-term direction. Recent movements have been influenced by a combination of factors, including ongoing geopolitical tensions in the Middle East, softer-than-expected US CPI and PPI data, and stronger-than-forecast Canadian employment figures released the previous week. Together, these developments have increased pressure on the US dollar while providing support for the Canadian currency.

NASDAQ 100

The Nasdaq 100 declined during the week, revisiting the 28,500 level, a region that has repeatedly acted as an important support zone. The market’s ability to hold above this area is likely to attract attention from investors looking for value opportunities and could help sustain the broader consolidation pattern.

If buyers successfully defend the 28,500 support level, the index may stage a rebound and continue trading within its established range. Under current conditions, the broader outlook still favors a move back toward the 30,000 mark over time. However, a significant deterioration in geopolitical conditions, particularly in the Middle East, could undermine risk sentiment and challenge the bullish scenario.

EUR/USD

The EUR/USD pair continued to hover around the key 1.14 level throughout the week. This area, which previously served as a major support zone, remains an important reference point for traders. Although the euro managed to recover modestly earlier in the week, higher US interest rates have continued to limit upside momentum and provide underlying support for the US dollar.

The broader bias remains cautious, with rallies likely to face resistance if buying momentum begins to fade. Given the current interest rate dynamics and ongoing demand for the dollar, traders may prefer a short-term trading approach, looking to capitalize on brief upward corrections while remaining alert to signs of renewed weakness in the pair.

The global oil market is losing many of its key shock absorbers as inventories remain tight, shipments through the Strait of Hormuz face ongoing disruptions, and spare supply continues to shrink, increasing the likelihood of stronger oil prices.

One factor that has kept prices from climbing further is China’s sharp decline in crude oil imports. However, analysts believe that support may soon disappear, with the world’s largest oil importer expected to return to the market after drawing down its existing stockpiles.

Should disruptions in the Strait of Hormuz continue while Chinese buying accelerates, market analysts warn that global oil supplies could tighten considerably. The resulting imbalance between supply and demand may place the greatest upward pressure on crude prices in the latter part of the year.

The oil market could soon lose the key supply and demand buffers that have prevented crude prices from surging despite the massive disruption to shipments through the Strait of Hormuz.

A temporary U.S.-Iran memorandum of understanding had allowed Middle Eastern producers to accelerate exports of crude that had accumulated in Gulf storage over the previous four months. That opportunity has now effectively ended as hostilities resumed and the ceasefire collapsed.

At the same time, crude and refined fuel inventories across major consuming regions, including the United States, have fallen to critically low levels. Much of the oil released through the largest coordinated strategic stock drawdown in history has already reached refiners, leaving few reserves available to cushion further supply shocks.

Another important stabilizing factor may also be fading. China, whose reduced crude imports have helped moderate global demand in recent months, is expected to return to the market soon. If that happens, one of the largest forces restraining oil prices during the March-to-June period could disappear.

China’s Demand May Be Reawakening

China cut crude imports to their lowest level in a decade during June, extending three months of unusually weak buying as elevated prices and constrained Middle Eastern supplies discouraged purchases. Compared with its 2025 average, imports are estimated to have declined by roughly 4.4 million barrels per day.

Official customs figures showed June crude imports totaled 29.27 million metric tons, or about 7.12 million barrels per day—down 41.3% from the same month a year earlier and marking the weakest monthly import level since October 2016.

The country’s large commercial and strategic reserves, accumulated before the conflict with Iran intensified, allowed Beijing to sharply reduce imports while still meeting domestic demand. Those stockpiles have acted as a major buffer for the global market, helping prevent prices from soaring despite the disruption of more than 10 million barrels per day of oil flows through the Strait of Hormuz.

As the world’s largest crude importer, China entered the supply crisis better prepared than any other major consumer. Analysts estimate it built reserves of between 1.2 billion and 1.3 billion barrels before the conflict began, although the true size of those inventories remains uncertain because official data are limited.

Recent estimates suggest China began drawing on those reserves in May and continued doing so through June. According to the International Energy Agency (IEA), inventories declined by roughly 41 million barrels last month.

While Goldman Sachs believes China still holds ample reserves and faces no immediate pressure to increase purchases, analysts expect the turning point may be approaching. Lower official selling prices from Gulf producers for July and August could encourage Chinese refiners to step up imports in the coming months.

Since the Middle East conflict escalated in February, China’s restrained buying has effectively acted as the global oil market’s swing demand factor. If imports recover, that important demand buffer could disappear.

Shrinking Inventories Raise Risks

A rebound in Chinese demand could coincide with continuing uncertainty surrounding the Strait of Hormuz, where shipping activity remains well below the pace seen during the brief period following the U.S.-Iran agreement.

Any renewed disruption to tanker traffic would further delay the recovery of Middle Eastern exports and tighten global supplies of both crude oil and refined fuels.

According to Energy Aspects founder Amrita Sen, slower vessel movements through the Strait, combined with renewed U.S. restrictions on Iranian oil exports and rapidly declining inventories, are laying the groundwork for higher oil prices if current conditions persist.

Sen estimates that global oil inventories have fallen by roughly 600–700 million barrels since the crisis began. She warned that if the current situation extends into the end of this month or early next month, the market may face its greatest pressure later in the third quarter or early in the fourth quarter.

Speaking separately to the Financial Times, Sen said that nearly all excess commercial inventories have now been exhausted, leaving only government-held strategic reserves as a meaningful emergency backstop. As a result, confidence that oil flows through the Strait of Hormuz will remain uninterrupted is increasingly being tested.

Gold’s $4,000 Test Signals Interest Rates Are Overriding Safe-Haven Demand

Gold futures dropped to $4,008.80, down $43.00 (1.06%), after opening at $4,068.90, slightly above Wednesday’s close. Spot gold weakened even further, falling to $4,010.33 by 11:03 EDT, a daily loss of $57.22. After trading near $4,041 early in the session, bullion came under steady selling pressure throughout the day.

Gold’s recent performance reflects a sharp reversal in momentum. Prices have declined 5.25% over the past month, although they remain 20.89% higher than a year ago. Since reaching $4,121.05 on July 10, the metal has steadily retreated, ending that week around $4,100 before sliding to $4,013.64 on July 13 as it tested the $4,000 level. Today’s move marks yet another return to that critical support, with the June low resting at $4,002.

The repeated tests of $4,000 suggest the market’s focus has shifted. Rather than responding primarily to geopolitical uncertainty, gold is increasingly trading in line with interest rate expectations. Rising tensions between the United States and Iran have lifted oil prices, reinforcing inflation concerns and increasing expectations that the Federal Reserve could keep monetary policy tighter for longer. Higher real yields raise the opportunity cost of holding non-yielding assets such as gold, limiting the metal’s appeal despite heightened geopolitical risks.

The broader precious metals market reflects the same trend. Silver fell to $56.90, while August Comex silver futures declined more than 3% to $57.095. Platinum slipped to $1,656.30, and palladium dropped to $1,295.75, highlighting broad-based selling across the sector as markets reassessed the outlook for inflation and interest rates.

Although softer-than-expected U.S. inflation data briefly supported gold by reducing expectations of an imminent Fed rate hike, the relief proved short-lived. As oil prices surged on renewed Middle East tensions, inflation concerns quickly resurfaced, sending gold back toward $4,000. The swift reversal from a CPI-driven rally to an oil-driven selloff illustrates the dominant theme shaping the 2026 gold market: interest rate expectations now carry more weight than traditional safe-haven demand.

War Is Hurting Gold Through Oil, Not Supporting It as a Safe Haven

The current weakness in gold reflects a market driven more by interest rate expectations than traditional safe-haven demand. The transmission mechanism is straightforward: military escalation raises concerns over crude oil supply, pushing energy prices higher. More expensive oil feeds into headline inflation, strengthening the case for the Federal Reserve to keep interest rates elevated—or tighten further. Higher real yields increase the opportunity cost of holding non-yielding assets like gold, encouraging institutional investors to reduce exposure.

Rather than acting as a catalyst for safe-haven buying, geopolitical tensions are being interpreted primarily through their impact on inflation and monetary policy.

That dynamic explains why gold has continued to decline despite intensifying conflict in the Gulf. Investors are viewing the risk surrounding the Strait of Hormuz as an interest-rate story: higher oil prices support higher bond yields and a firmer U.S. dollar, reducing gold’s appeal. The conflict itself remains significant, but the market is responding through the inflation channel instead of the traditional flight-to-safety narrative.

Oil prices continue to reinforce that view. Brent crude trades around $84.63, up 6.39% over the past month and 21.74% from a year ago, while WTI crude remains above $80 after rallying more than 11% in three sessions. Recent U.S. strikes on Iranian targets and Iran’s retaliation against American military bases across the Gulf have heightened concerns over energy supplies.

The sequence of events also helps explain the sharp swings in sentiment. A Memorandum of Understanding signed by Iran and the United States on June 17 had raised hopes for improved relations, including the easing of sanctions on Iranian oil exports and reduced disruption around the Strait of Hormuz. Those expectations unraveled on July 6, when attacks on commercial shipping prompted military retaliation, placing the agreement under severe strain.

The contrast with earlier in the year is notable. Gold rallied during the February escalation but has fallen during the July conflict because the macro backdrop has changed. Earlier, geopolitical risks boosted demand for defensive assets. Today, the same risks are reinforcing expectations of tighter monetary policy, fundamentally altering the market’s response.

A reversal remains possible but would likely require either a prolonged disruption to shipping through the Strait of Hormuz that sparks a genuine flight to safety or a deterioration in global growth severe enough to drive bond yields lower. Reports that Tehran remains open to renewed negotiations reduce the likelihood of either scenario in the near term, leaving interest rate expectations as the dominant force weighing on bullion.

Gold Has Fallen 28% From Its Record High

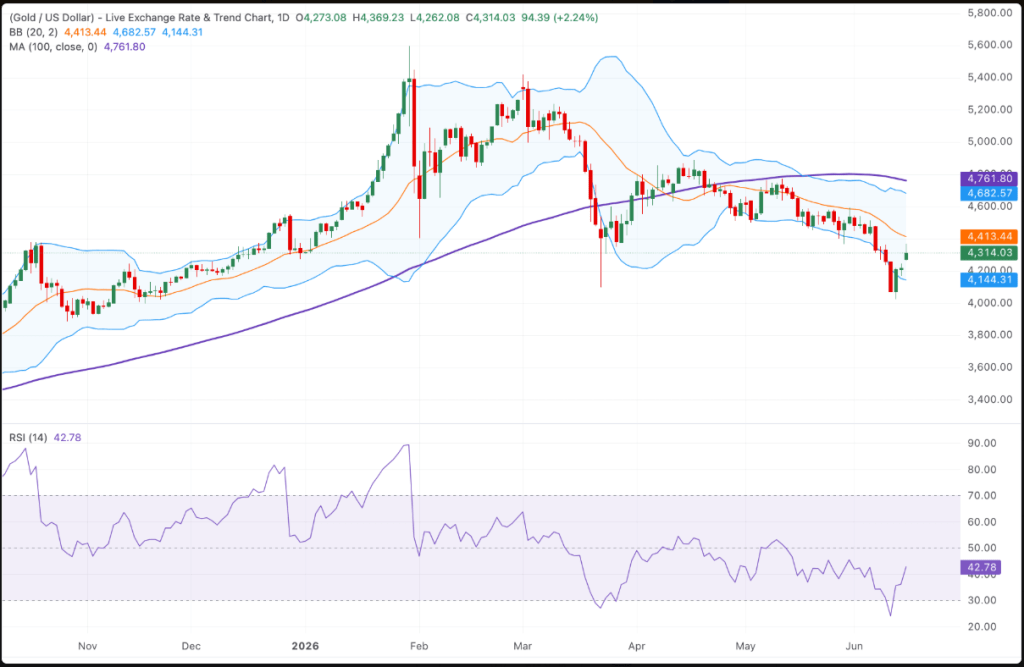

Gold has retreated dramatically from its January 29 record of $5,589 per ounce to approximately $4,008.80, a decline of 28.3%, or $1,580, in less than six months.

The rally earlier this year was extraordinary. Gold surged above $5,000 for the first time, briefly touched $5,595 intraday, and established multiple all-time highs before suffering a historic reversal. After peaking in late January, prices traded sideways through much of the first quarter before breaking sharply lower in March. A modest rebound in April eventually gave way to another steady decline toward the $4,000 area, with June’s low at $4,002.

Despite the correction, the longer-term picture remains relatively resilient. Gold is down roughly 7% year-to-date but still trades nearly 21% above year-ago levels and remains about $578 above its 2025 year-end close of $3,431. In that context, the decline represents a significant retracement of an exceptionally rapid rally rather than the complete breakdown of the longer-term bullish trend.

However, the technical landscape has changed. Analysts previously viewed the $4,550 region—formed by late-December highs and early-2026 support—as a major floor. That level failed during March’s selloff and now sits roughly $460 above current prices, removing an important layer of technical support.

Heavy Liquidation Intensified the Selloff

The decline was amplified by two major liquidation waves rather than a gradual reassessment of gold’s long-term value.

The first came immediately after January’s record highs, when gold plunged nearly $1,200 in just two trading sessions, marking its steepest two-day decline since 1983. The second occurred in March, when prices fell roughly 13%, producing the worst monthly decline since 2009. In both cases, rising interest-rate expectations linked to higher energy prices overshadowed gold’s traditional role as a defensive asset.

Despite the sharp correction, Wall Street remains broadly constructive. A Reuters survey of analysts projects a 2026 median gold price of $4,746.50 per ounce, the highest consensus forecast since the poll began in 2012. With gold currently near $4,009, prices remain roughly 15.6% below that consensus estimate.

Liquidity dynamics also played an important role. During periods of market stress, institutional investors often sell their most liquid holdings to meet margin calls or raise cash quickly. Gold’s liquidity makes it a frequent source of funding, creating a paradox in which a traditional safe-haven asset can come under heavy selling pressure precisely when uncertainty rises.

That behavior was evident on March 4, when the SPDR Gold Shares (GLD) experienced approximately $2.91 billion in net outflows in a single session—the largest daily withdrawal in more than a decade. Combined with profit-taking from investors who benefited from gold’s rapid rise earlier in the year, those outflows accelerated the correction. As momentum traders exited, ownership shifted toward longer-term investors whose buying tends to be steadier but less aggressive, leaving the market without the speculative demand that previously fueled the rally.

Rising Real Yields Continue to Undermine Gold

The surge in U.S. Treasury yields has become one of the primary headwinds for gold. The 10-year Treasury yield climbed to 4.60% on Thursday, approaching the two-month high of 4.62% reached on July 13, as investors increasingly positioned for another Federal Reserve rate hike.

The key driver is real yields—bond yields adjusted for inflation expectations—rather than nominal interest rates alone. As expectations for tighter monetary policy increase, real yields rise, making income-generating assets more attractive relative to gold, which offers no yield. Conversely, when markets anticipate fewer rate hikes or eventual easing, real yields typically decline, improving gold’s relative appeal.

That dynamic briefly supported bullion after June’s softer inflation data. Consumer prices fell 0.4% month over month, the largest monthly decline since April 2020, while annual CPI eased to 3.5% and core inflation held at 2.6%. Producer prices also slipped 0.3%, marking their first monthly decline in nearly a year as energy costs retreated. Gold initially benefited from the weaker inflation readings.

However, the rally proved short-lived as stronger economic data quickly shifted attention back to the Fed. Retail sales remained resilient despite lower fuel prices, while initial jobless claims fell to 208,000, a two-month low, reinforcing confidence in the labor market. Those developments strengthened expectations that the Federal Reserve could still tighten policy later this year. Interest-rate futures currently imply roughly a 44% probability of a September rate hike, down from 50% a day earlier but still keeping additional tightening firmly on the table.

A stronger U.S. dollar has added further pressure. Supported by higher Treasury yields and a resilient U.S. economy, the Dollar Index remains near 100.49. Earlier in 2026, a weaker dollar helped propel gold to its record high of $5,589, but the recent rebound in the greenback has reversed that tailwind.

History, however, offers a note of caution. Gold has often performed well after Federal Reserve rate increases, averaging gains in the month following a 25-basis-point hike during several previous tightening cycles. The decisive factor is not the hike itself but whether tighter policy ultimately slows economic growth enough to push yields lower.

A More Hawkish Federal Reserve Has Increased Uncertainty

Since taking office as Federal Reserve Chair in May 2026, Kevin Warsh has adopted a notably less predictable communication strategy. During congressional testimony in mid-July, he followed a June Federal Open Market Committee meeting that left rates unchanged but shifted the policy outlook in a more hawkish direction.

One notable feature of the June meeting was Warsh’s decision not to publish his own interest-rate projection in the Fed’s dot plot. Combined with the removal of explicit forward guidance, the move increased uncertainty around future monetary policy and made it more difficult for markets to anticipate the Fed’s reaction function.

Markets currently expect the July 28–29 FOMC meeting to end with rates unchanged, assigning roughly a 90% probability to a hold. Nevertheless, investors continue to see September as a realistic opportunity for another rate increase.

The broader policy backdrop also remains restrictive. The World Gold Council (WGC) expects at least one Federal Reserve rate hike in 2026 while anticipating additional tightening by the Bank of England, Bank of Japan, and European Central Bank. Simultaneous tightening across several major central banks reduces the currency-diversification advantages that previously supported gold.

The macroeconomic outlook remains relatively stable, with global growth projected around 2.9%, U.S. growth near 2.1%, U.S. inflation peaking around 3.9%, and global inflation averaging 4.3% during 2026. Under those conditions, elevated real yields continue to reduce the incentive to hold gold.

The primary upside risk for bullion would be a sharper-than-expected economic slowdown. According to Bank of America’s June fund manager survey, 58% of respondents expect stagflation. Should tighter monetary policy significantly weaken growth, declining yields could eventually restore support for gold.

The World Gold Council Sees Gold Near Fair Value

The World Gold Council’sMid-Year Outlook 2026, titled Point Break, values gold using a framework based on real yields, inflation expectations, the U.S. dollar, and central-bank demand. Under its baseline macroeconomic scenario, the model estimates fair value near $4,100 per ounce, with a tolerance range of roughly ±5%, implying a second-half trading band between $3,895 and $4,305.

With gold trading around $4,008.80, prices remain comfortably within that projected range. The implication is that current valuations broadly reflect consensus expectations of one additional Fed rate hike and inflation peaking near 3.9%, suggesting the market is neither significantly overvalued nor deeply undervalued.

That assessment limits both bullish and bearish arguments. It weakens expectations of a sharp collapse because the WGC’s framework identifies fundamental support near $3,895, but it also challenges forecasts of a rapid return to $5,200–6,000 unless the macroeconomic outlook changes substantially.

Future price direction will largely depend on shifts in economic growth, geopolitical developments, and the U.S. dollar. The WGC notes that while geopolitical tensions drove much of gold’s volatility during the first half of the year, currency movements could become an equally important variable in the months ahead.

Central-Bank Buying Provides Support—but Not Momentum

Central banks continue to accumulate gold despite the recent correction. The People’s Bank of China (PBoC) purchased 15 tonnes in June—its largest monthly acquisition since October 2023—marking the 20th consecutive month of reserve accumulation. China’s official gold holdings have now reached 2,346 tonnes, representing roughly 9% of its total foreign-exchange reserves.

Worldwide, central banks acquired an estimated 244 tonnes during the first quarter of 2026, with countries such as Poland also continuing to expand their holdings.

While these purchases provide an important source of structural demand, they have not prevented prices from falling. Central banks typically allocate reserves based on long-term diversification strategies rather than short-term market movements. As a result, they tend to absorb supply steadily instead of aggressively chasing prices higher.

The scale of recent buying also illustrates its limitations. China’s 15-tonne purchase represents roughly 482,000 ounces, equivalent to approximately $1.9 billion at current prices. By comparison, the SPDR Gold Shares (GLD) experienced $2.91 billion in outflows in a single trading session during March. One day of ETF liquidation outweighed an entire month of China’s purchases.

Many longer-term bullish forecasts assume central-bank buying will remain robust, with total official-sector purchases exceeding 800 tonnes in 2026. Even if that pace is achieved, however, official demand is more likely to establish a long-term price floor than trigger another powerful rally.

The broader structural arguments for gold—including reserve diversification, fiscal expansion, de-dollarization, and limited mine-supply growth—remain intact. What has weakened is private investment demand. Because marginal private buyers typically determine short-term price movements, their retreat has had a much larger impact on prices than continued sovereign accumulation.

WTI edges higher during the Asian session, although buying interest remains limited. Escalating tensions between the US and Iran continue to underpin geopolitical risk premiums, while fears of supply disruptions across key shipping routes lend further support to crude prices.

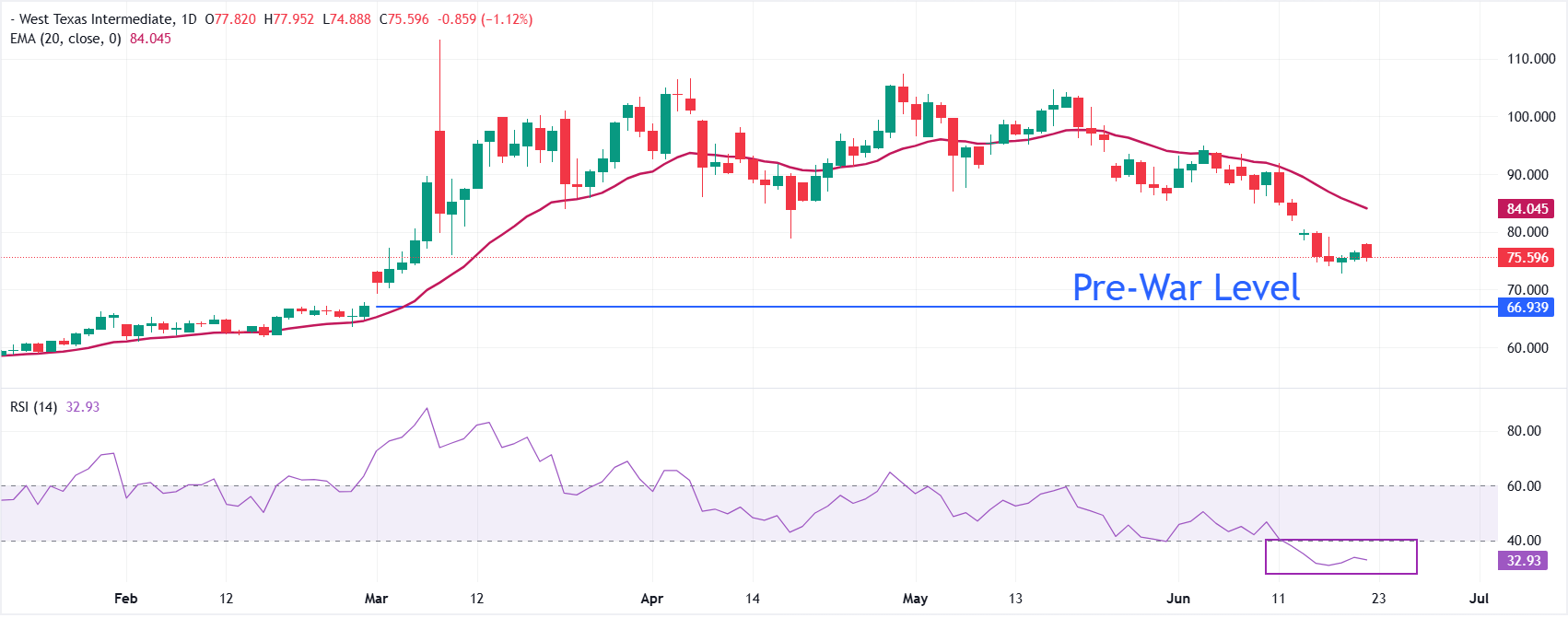

West Texas Intermediate (WTI), the US benchmark for crude oil, trades modestly higher during Friday’s Asian session but continues to move within a well-established multi-day trading range. The commodity is hovering near $79.35, up roughly 0.5% on the day and close to Tuesday’s one-month peak, leaving it on course for a second consecutive weekly gain as investors remain focused on the possibility of further escalation between the United States and Iran.

Market sentiment remains supported after the US military conducted a sixth straight night of airstrikes against Iran on Thursday, including a strike on an empty oil tanker bound for Kharg Island as part of its renewed naval blockade of Iranian ports. In response, Iran launched attacks on US military positions across the region, intensifying concerns that the conflict could evolve into a broader confrontation. These developments have kept geopolitical risk premiums elevated and continue to provide underlying support for crude prices.

Additional concerns emerged after authorities in Bandar Abbas reported damage to civilian infrastructure, including electricity facilities and a railway station. Iran’s Islamic Revolutionary Guard Corps has also warned of expanding military operations by targeting more regional energy transport routes. Adding to supply concerns, Reuters reported that Tehran has instructed Yemen’s Houthi movement to prepare for the possible closure of the Red Sea oil corridor, creating another potential threat to global energy flows.

At the same time, declining shipping activity through the Strait of Hormuz has reinforced fears of tighter oil supplies, strengthening the case for further upside in crude prices. Even so, traders may prefer to wait for a decisive breakout above the current consolidation range before committing to fresh bullish positions. Nevertheless, the broader fundamental backdrop continues to favor buyers, suggesting that any near-term pullback is likely to attract renewed demand and remain relatively limited.

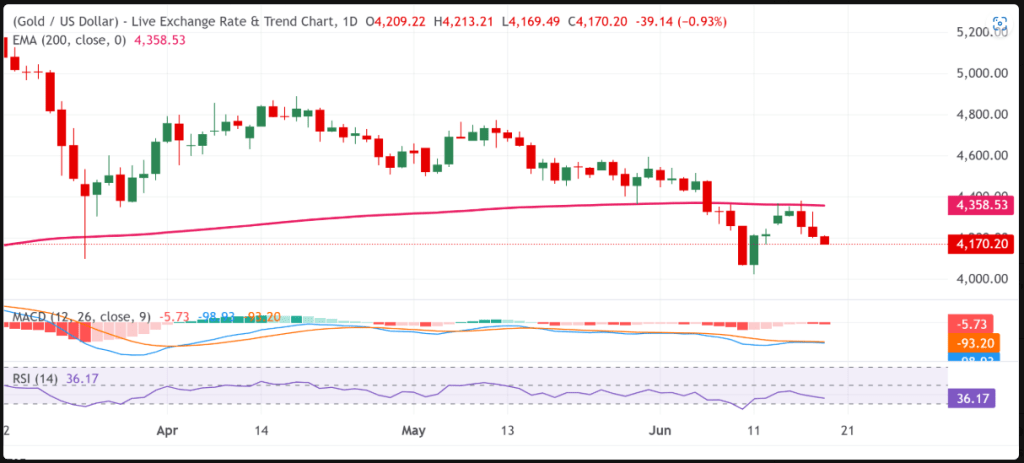

Gold prices fell to around $3,975 during Friday’s early Asian trading session. The decline came after Iran reportedly urged the Houthis to block the Red Sea gateway if the US targeted its power network, intensifying Middle East tensions. The escalating geopolitical conflict strengthened expectations that the Federal Reserve could raise interest rates later this year, putting additional pressure on the precious metal.

Gold prices remained under pressure, slipping toward an eight-month low near $3,975 in early Asian trading on Friday. The precious metal continued to weaken as escalating tensions in the Middle East fueled inflation concerns and strengthened expectations that US interest rates could remain higher for longer.

According to Reuters, Iran has instructed Yemen’s Houthi movement to prepare to block the Red Sea shipping route if the United States targets Iranian power infrastructure. The warning followed US President Donald Trump’s threat earlier this week to strike Iran’s power network.

Any disruption to the Red Sea would significantly worsen the global energy crisis already intensified by Iran’s closure of the Strait of Hormuz. Such a scenario could drive crude oil prices even higher, increasing inflationary pressures and encouraging major central banks to keep monetary policy restrictive. Higher interest rates typically reduce the attractiveness of non-yielding assets such as gold.

The renewed geopolitical tensions have overshadowed recent signs of easing US inflation. Data released earlier this week showed that both the Consumer Price Index (CPI) and Producer Price Index (PPI) cooled in June, suggesting inflationary pressures had moderated.

Despite the softer inflation readings, market participants now see roughly a 55% probability that the Federal Reserve will raise interest rates at its September meeting, according to the CME FedWatch Tool, adding further downside pressure to gold.

Gold attracts fresh selling pressure on Thursday as energy-led inflation concerns revive expectations of additional Fed rate hikes.

Escalating tensions between the US and Iran underpin demand for the safe-haven US Dollar, weighing on the precious metal.

The technical outlook remains bearish, suggesting the path of least resistance is tilted toward further downside.

Gold (XAU/USD) came under renewed selling pressure during Thursday’s Asian session, retreating toward the $4,025 area near the previous day’s swing low. Although recent US inflation data pointed to easing price pressures, elevated crude oil prices continue to fuel expectations that the Federal Reserve could still raise interest rates later this year. The prospect of tighter monetary policy lends support to the US Dollar (USD) and weighs on non-yielding Gold.

Data released by the US Bureau of Labor Statistics showed that the Producer Price Index (PPI) unexpectedly fell 0.3% in June following a revised 0.6% increase in May, while annual producer inflation slowed to 5.5% from 6.0%. The report followed a sharp decline in the Consumer Price Index (CPI), reinforcing signs that inflation pressures are moderating. As a result, traders reduced expectations for an imminent Fed rate hike, sending the USD to its weakest level since June 18 and helping Gold recover on Wednesday.

However, persistent energy-driven inflation risks continue to cloud the outlook. Crude oil prices remain near one-month highs as escalating US-Iran tensions and ongoing disruptions in the Strait of Hormuz raise concerns about global energy supplies. The US launched another wave of airstrikes against Iranian military targets on Wednesday, prompting retaliatory drone and missile attacks by Iran on US-linked facilities across the region. President Donald Trump also warned that additional Iranian infrastructure could be targeted if hostilities intensify.

Meanwhile, Iran’s Islamic Revolutionary Guard Corps threatened to broaden the conflict by targeting key regional energy routes, including shipping lanes near the Bab el-Mandeb Strait through its Houthi allies in Yemen. These developments continue to support oil prices, rekindling inflation concerns and strengthening the argument for at least one 25-basis-point Fed rate hike in 2026. Consequently, USD weakness may remain limited, while the broader outlook for Gold continues to favor further downside.

Gold Daily Chart

Gold remains under bearish pressure as XAU/USD continues to trade below its 200-day Simple Moving Average (SMA) and within a well-defined descending channel. While momentum indicators show signs of stabilization, they have yet to signal a meaningful bullish reversal. The Moving Average Convergence Divergence (MACD) remains slightly positive at 9.43, while the Relative Strength Index (RSI) hovers near 40.77, suggesting weak buying interest rather than a sustained recovery.

A confirmed break and daily close below the key psychological support at $4,000 could trigger a fresh wave of selling. Such a move would bring the June year-to-date low around $3,943–$3,942 into focus. Further downside pressure could then drive Gold toward the channel’s lower boundary near $3,675.71, a major structural support level. A decisive violation of this zone would strengthen the broader bearish outlook and open the door to deeper losses.

On the upside, immediate resistance is located near $4,093.63, corresponding to the upper boundary of the descending channel. Any recovery attempt is likely to encounter renewed selling interest in this region. A sustained breakout above this barrier would improve the technical picture and pave the way for a move toward the 200-day SMA around $4,495.94, which remains the next major resistance level.

Silver remains under pressure as escalating US-Iran tensions in the Strait of Hormuz drive oil prices higher, raising concerns that the Federal Reserve may keep interest rates elevated for longer. Softer-than-expected June CPI and PPI data have helped ease near-term rate-hike concerns. Meanwhile, markets have reduced the probability of a September Fed rate increase to 44%, although the impact of recent military developments has yet to be fully reflected in asset prices.

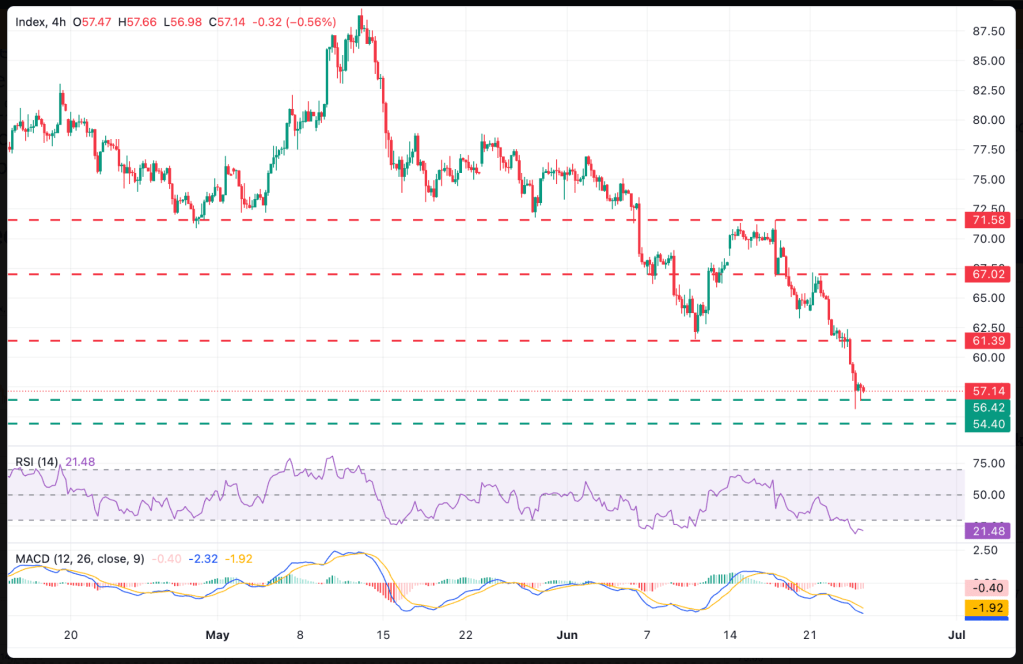

Silver (XAG/USD) extends its decline for a second consecutive session, trading near $57.00 per troy ounce during Thursday’s Asian session. The precious metal remains under pressure as escalating tensions between the United States and Iran drive oil prices higher, raising inflation risks and reinforcing expectations that the Federal Reserve could maintain elevated interest rates for longer.

According to reports, the US Central Command (CENTCOM) launched additional operations aimed at keeping the Strait of Hormuz open, a critical route for global energy supplies. In a significant escalation, US forces reportedly targeted an oil tanker in the strategic waterway, heightening concerns over further disruptions to oil markets. Meanwhile, President Donald Trump declined to provide a timeline for potential future actions against Iranian infrastructure, adding to geopolitical uncertainty.

Despite these developments, investors are also weighing softer US inflation data. Consumer inflation eased to 3.5% year-over-year in June from 4.2% in May, coming in below the consensus forecast of 3.8%. The weaker CPI reading initially reduced expectations of an imminent Fed rate increase.

Producer inflation data reinforced the disinflationary trend. The annual PPI rate slowed to 5.5% in June from 6.0% previously, missing expectations of 6.2%, while monthly PPI fell 0.3% after a 0.6% rise in May, outperforming forecasts for a flat reading.

As a result, market expectations for a September Fed rate hike eased, with implied odds declining to roughly 44% from 50% a day earlier. However, analysts note that June inflation figures do not yet reflect the economic consequences of the renewed US-Iran conflict, leaving markets cautious about the potential inflationary effects of the latest military escalation.

For the first time in the current market cycle, a silver producer has disclosed concrete figures showing a forced reduction in output, with the decline stemming from China’s mine-safety crackdown rather than changes in silver prices.

Silver is currently trading around $58 an ounce after falling below its early-July low. The metal has dropped about 18% from its year-end 2025 close near $71 and remains roughly 52% below the record high of $121.62 reached on January 29. Even so, silver is still more than 50% higher than it was a year ago. With gold hovering near $4,000 an ounce, the gold-to-silver ratio stands at approximately 69. The recent two-month pullback has largely been driven by macroeconomic forces, including a stronger US dollar and the Federal Reserve’s hawkish stance, while renewed US-Iran tensions have fueled oil prices and inflation concerns, rather than any major shift in silver market fundamentals.

Beneath the recent price weakness, however, the long-term supply outlook remains largely intact. According to Metals Focus and the Silver Institute, the global silver market is expected to record its sixth consecutive annual supply deficit in 2026, with demand projected to exceed production by 46.3 million ounces. A key pillar of the bullish outlook has been the limited ability of silver supply to respond to higher prices. Around three-quarters of global silver production comes as a byproduct of mining for copper, lead, zinc, and gold, making it difficult to significantly increase output simply because silver prices rise. This week provided one of the clearest real-world examples of that constraint, as China’s safety-related mining restrictions forced measurable production cuts despite elevated silver prices.

Silvercorp’s Production Cuts

On June 29, Canadian-listed Silvercorp Metals announced that a tightening mine-safety campaign in China would significantly reduce its production during the July-to-September quarter. Output from its Ying mining district is expected to decline by 40% to 50%, while production at the GC mine is projected to fall by around 50%. Overall, the company estimates a quarterly production decline of 10% to 15%. Based on Silvercorp’s latest annual production of approximately 6.3 million ounces from Ying and 0.5 million ounces from GC, the reductions could remove an estimated 0.9 million to 1.1 million ounces of silver from supply during the affected period.

The significance lies less in the company itself than in the cause of the disruption. The production cuts were not driven by weaker prices or operational decisions but by stricter government safety regulations. Following a fatal coal mine accident in Shanxi Province in late May, Chinese authorities expanded the country’s long-established “Six Major Safety Systems” requirements to cover all underground non-coal mines. The new rules are supported by a nationwide real-time monitoring network overseeing more than one million safety sensors.

For Silvercorp, meeting the updated standards will require roughly $5.5 million in certified safety-system installations over about 50 days, along with an additional $6 million for facility and equipment upgrades. The nearly $11.5 million investment is aimed solely at maintaining regulatory compliance and keeping mines operational, rather than increasing production capacity, effectively raising the cost of every ounce of silver the company continues to produce.

While Silvercorp is only one mining company, the regulations affecting its operations apply to every underground metal mine in China. As a result, the same safety enforcement that forced Silvercorp to scale back production could eventually reduce China’s overall silver output by several million additional ounces, although no confirmed figures beyond Silvercorp’s estimates are available yet. Given China’s position as one of the world’s largest silver producers and an even more significant refining hub, the broader regulatory trend carries greater importance than the impact on any single miner.

What It Means for Silver Investors

The immediate impact should be viewed in perspective. Silvercorp’s estimated production loss of 0.9 million to 1.1 million ounces is relatively modest compared with the roughly 846.6 million ounces of silver mined globally in 2025, representing only slightly more than one-tenth of one percent of annual supply. On its own, the reduction is far too small to meaningfully alter the global supply-demand balance. As such, portraying it as the catalyst for an immediate supply shortage would overstate its significance.

What makes this development significant is not the scale of the production cut but the underlying mechanism. One of the strongest arguments supporting silver’s long-term outlook is that mine supply cannot quickly respond to higher prices. That theory faced a real-world test as silver surged to record highs in early 2026. Instead of increasing, however, production moved in the opposite direction. Supply contracted for reasons unrelated to market prices, as regulatory safety measures forced mines to reduce output. In this case, even substantially higher silver prices could neither prevent the shutdowns nor restore the lost production. If supply continues to tighten under regulatory pressure while remaining largely unresponsive to stronger prices, the industry’s ability to offset the market’s projected sixth consecutive annual deficit becomes even more limited.

The broader significance, therefore, lies in what this episode demonstrates rather than in the number of ounces affected. In Issue #19, I highlighted the growing divergence between a replenished silver inventory in New York and persistently elevated physical premiums in Shanghai, suggesting that Western markets appear well supplied while buyers in Asia continue paying a premium for physical metal. Silvercorp’s production cut adds to that narrative, reinforcing the view that underlying physical tightness may be greater than paper prices imply. While this development does not point to any specific price target, it strengthens the long-term investment case for silver by providing tangible evidence that global mine supply remains structurally constrained and cannot be expanded quickly, even during periods of elevated prices.

Gold drifts lower as the market’s initial response to Tuesday’s softer-than-expected US inflation data loses momentum. Persistently high oil prices continue to fuel expectations of at least one additional Federal Reserve rate hike, weighing on the non-yielding metal. Meanwhile, escalating tensions between the US and Iran could boost demand for the safe-haven US Dollar, adding further downside pressure to XAU/USD.

Gold (XAU/USD) comes under renewed selling pressure after failing to sustain gains above the $4,100 level in the previous session, though it continues to hold above the key $4,000 psychological support during Wednesday’s Asian trading hours. While softer-than-expected US Consumer Price Index (CPI) data initially weighed on the US Dollar (USD), persistent concerns over energy-driven inflation continue to dominate sentiment. Escalating tensions between the US and Iran, along with the closure of the Strait of Hormuz, have kept crude oil prices elevated, reinforcing inflation fears. Meanwhile, Federal Reserve (Fed) Chair Kevin Warsh reaffirmed the central bank’s commitment to restoring price stability during his first congressional testimony, signaling that another rate hike remains possible before year-end. The hawkish tone largely offsets the impact of a weaker USD and limits demand for the non-yielding precious metal.

Data released by the US Bureau of Labor Statistics showed headline CPI fell by 0.4% in June, marking the steepest monthly decline since April 2020 and falling short of expectations for a 0.1% decrease. Core CPI, which excludes food and energy prices, was unchanged during the month, well below the expected 0.3% increase. On an annual basis, headline inflation eased to 3.5%, while core inflation slowed to 2.6%, both undershooting market forecasts. The softer inflation figures briefly dragged the USD to its weakest level in nearly four weeks as traders pared back expectations for additional Fed tightening. However, the Greenback quickly recovered after Warsh emphasized that the Fed remains firmly committed to combating inflation and highlighted the resilience of the US economy.