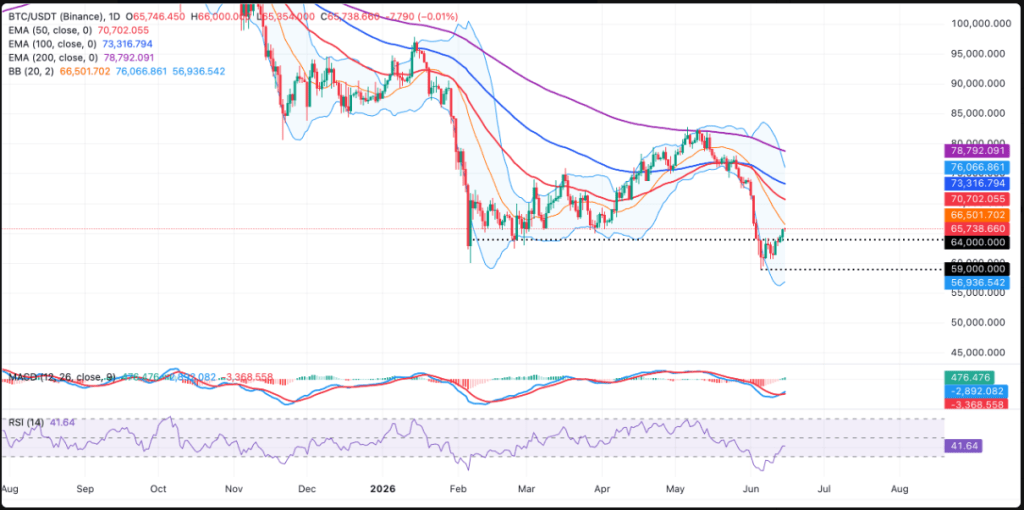

Bitcoin Breaks Below $60,000 as Bearish Structure Deepens

Bitcoin has slipped below the $60,000 threshold, reinforcing a deterioration in near-term market structure. BTC traded around $60,128 on Monday, briefly touching $59,748—its weakest level since October 2024. The move caps a month-long decline that has fully unwound the spring rally.

June opened near $73,674 and briefly topped at $74,092 before reversing sharply to a monthly low of $58,115, ending the month down ~18.4%. The key issue is not just the break of $60,000, but the loss of trend integrity: short-term moving averages are rolling over, and dip-buying has largely faded.

Despite strength in broader equities—particularly the Nasdaq, driven by AI-related momentum and easing geopolitical concerns—Bitcoin has failed to participate.

This divergence suggests BTC is currently behaving less like a macro hedge and more like a high-beta liquidity-sensitive risk asset competing for speculative flows. Capital rotation appears to be favoring AI infrastructure, large-cap tech, and IPO narratives, draining marginal demand from crypto.

Above 100-month EMA: $40,322 (long-term trend still intact)

Price action confirms sustained downside pressure, with weekly losses near 4.5% and monthly drawdown ~18%, alongside declining trend structure across shorter timeframes.

The market remains technically weak, though still within a cyclical correction rather than a structural breakdown.

Institutional Flows: ETF Demand Reversal Becomes Central Risk

A major shift has emerged in institutional positioning:

~ $5.96B net outflows from US spot Bitcoin ETFs over the past 30 days

Including a peak monthly redemption of ~$2.43B

Multiple large single-day withdrawals ($400–500M+), including a $1.26B outlier

Roughly $3.4B exited in a single week at peak stress

Given ETFs have become a dominant marginal price driver, this reversal materially weakens demand elasticity. Brief inflow days have not yet signaled trend reversal.

Sustained inflows would be required to stabilize price action; continued outflows would reinforce downside momentum.

Corporate Demand Weakens: Strategy Flywheel Under Pressure

The corporate accumulation narrative is also deteriorating.

Strategy, the largest corporate Bitcoin holder (~847,000 BTC), is now under pressure as BTC trades below its average cost basis. Its equity drawdown has reduced its premium-to-NAV, weakening its ability to raise capital for further accumulation.

More importantly, the firm has expanded financial flexibility to include potential Bitcoin sales for liquidity and buybacks—marking a meaningful shift away from its previous purely accumulation-driven stance.

Even if accumulation continues, the reflexive “buy-the-premium” flywheel that previously amplified demand is clearly impaired.

Derivatives markets have undergone a sharp deleveraging:

Open interest down ~19%

Majority of liquidations from long positions

Multi-billion-dollar cascading liquidation events during breakdown

This reset improves structural stability but removes a key source of reflexive upside (forced shorts and leverage expansion). Recovery now depends on genuine spot demand rather than positioning-driven flows.

Technical Structure: Bearish Alignment Across Timeframes

Bitcoin’s technical setup is aligned bearish across multiple horizons.

Price remains below all major short- and medium-term moving averages, including:

20-month EMA: $79,979

50-month EMA: $65,631 (critical level)

A sustained reclaim of $65,631 would materially weaken the bearish structure. Until then, rallies are corrective within a broader downtrend.

Shorter-term indicators reinforce weakness:

50-day MA (~$70,238) trending lower and acting as resistance

200-day MA rolling over

Most intraday averages flattening or declining above price

Price is also compressing between roughly $59,000–$61,000, suggesting volatility expansion risk rather than immediate resolution.

Key Levels: Downside Risk Remains Active

Critical support: $58,115

Break would confirm continuation of downtrend

Downside targets:

$55,000: secondary structural support

$48,000: deeper cycle retracement zone

The rising 100-month EMA (~$40,322) defines the long-term structural floor, consistent with a cyclical correction rather than full regime failure.

As long as $58,115 holds, rebound scenarios remain valid—but fragile.

Upside Structure: Heavy Resistance Cluster

Key resistance levels:

$62,500: initial supply zone

$64,178–$67,180: dense resistance cluster

$65,631: 50-month EMA (key structural pivot)

A reclaim of $65,631 would be the first meaningful signal of structural repair and open a path toward $70,000. Failure to reclaim it keeps rallies within corrective territory.

Momentum & Sentiment: Oversold, Not Reversed

Momentum remains weak across timeframes:

RSI: deeply depressed, near oversold on daily

MACD: negative with no confirmed bullish crossover

Breadth: broadly bearish across indicators

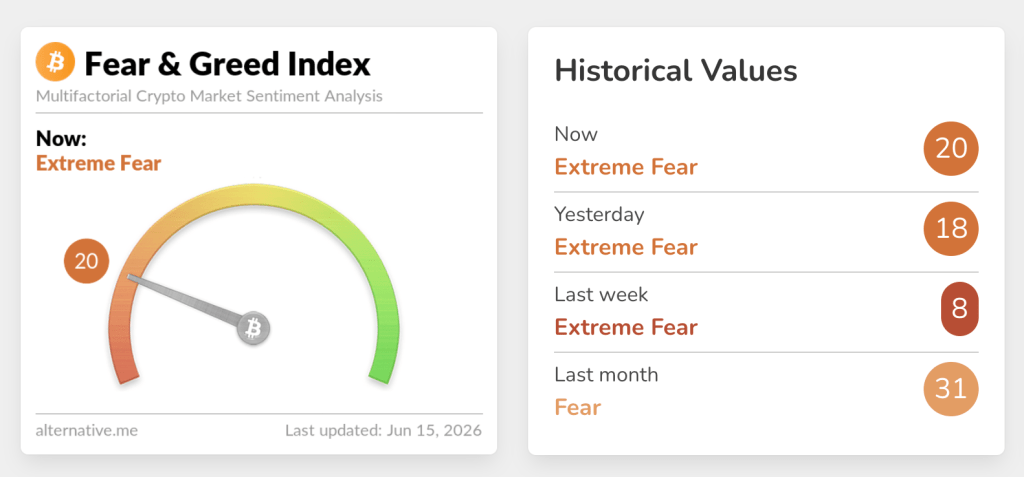

Sentiment sits at “Extreme Fear” (~18 on Fear & Greed Index), historically consistent with late-stage stress but not a timing signal on its own.

The core tension remains unresolved: sentiment is washed out, but price has not confirmed reversal.

Bottom Line

Bitcoin is in a structurally corrective phase driven by three reinforcing forces:

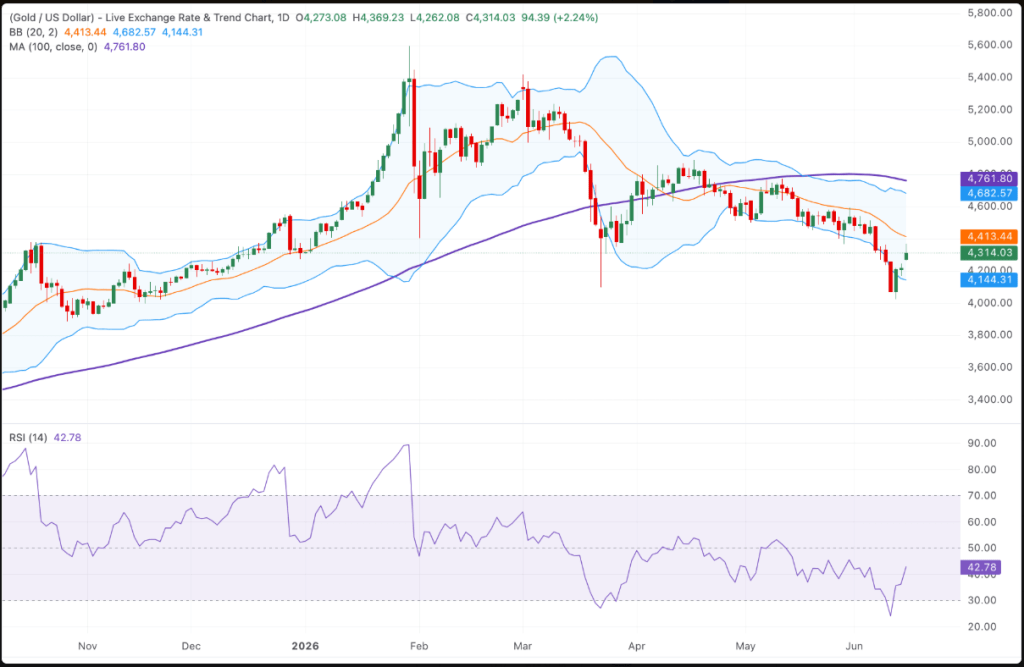

Gold fell 12% in June, prompting questions over whether further downside is likely, while USD/JPY remains in focus amid intervention concerns.

Gold has rebounded above the 4,000 level but is still set to record a 12% monthly loss in June—its steepest decline since October 2008. The drop reflects a broader market shift away from geopolitical risk premiums and back toward concerns over elevated U.S. interest rates.

The metal is also heading for its first quarterly loss since 2024 and its largest three-month drop since Q2 2013.

The selloff has been driven by rising expectations that the Federal Reserve will continue tightening policy. After a hawkish FOMC meeting and persistently high Core PCE inflation at 3.4%, markets are now pricing in more than a 60% chance of a 25-basis-point rate hike in September, with up to three hikes still seen as possible this year.

These expectations have pushed the U.S. dollar to a 13-month high, while higher real yields have increased the opportunity cost of holding non-yielding assets like gold.

Together, a stronger dollar, rising real yields, and a hawkish Fed stance continue to pressure gold prices.

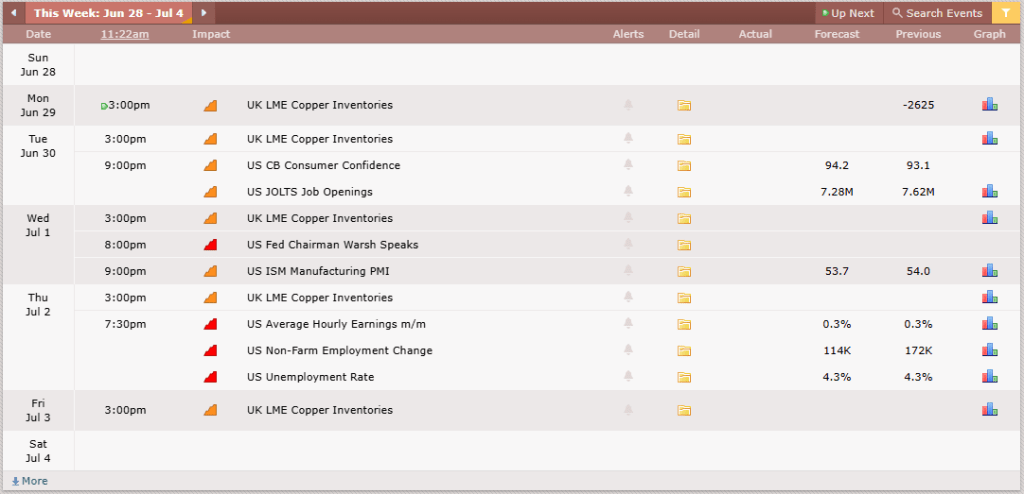

Market attention now shifts to Fed Chair Kevin Walsh’s remarks at the ECB Sintra Forum and Thursday’s U.S. non-farm payrolls report, which could offer further clues on the rate outlook and gold’s direction.

For a sustained recovery, gold would likely need lower real yields, a weaker dollar, or a reversal in hawkish Fed expectations—none of which currently appear imminent.

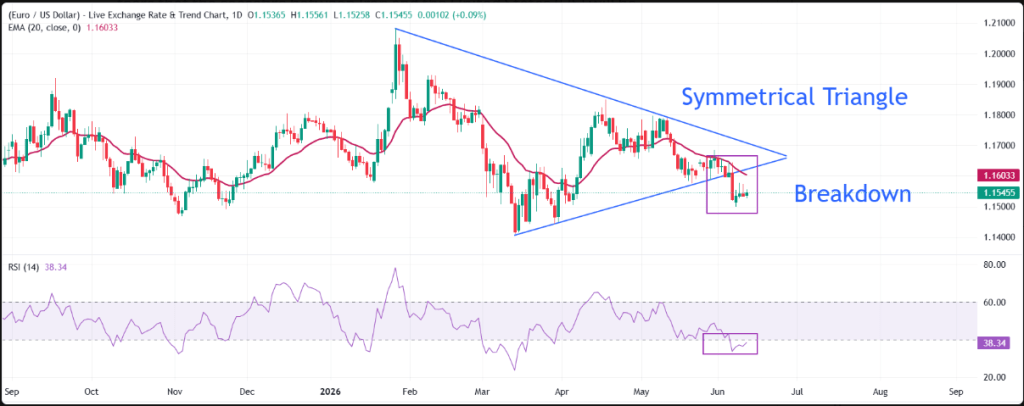

Gold Forecast – Technical Analysis

Gold has broken down from its symmetrical triangle formation and slipped below the 200-day simple moving average, hitting a low of 3,942—its weakest level since November.

The 50-day SMA has now crossed beneath the 200-day SMA, confirming a bearish “death cross” signal. Alongside an RSI reading below 50, technical indicators continue to point toward downside momentum.

On the downside, sellers may target 3,930—the November low—followed by 3,800. A break beneath that level could open the door toward the psychological support zone around 3,500.

On the upside, any recovery would first need to reclaim 4,100, which aligns with this week’s high and the March low. Beyond that, resistance is seen near a declining trendline around 4,300, followed by horizontal resistance at 4,350. A sustained move above this zone would bring the 200-day SMA near 4,500 back into focus.

USD/JPY

USD/JPY has surged to a 40-year high above 162, heightening concerns that Japanese authorities may intervene to support the yen.

The currency has weakened to levels last seen in 1986, increasing speculation that Tokyo could step into the market in the near term, even as the U.S. dollar has eased slightly from its 13-month peak.

The yen is down 2% in the second quarter, marking its fourth consecutive quarterly decline and the longest losing streak in four years, as the wide interest rate gap between the U.S. and Japan continues to weigh on the currency.

Finance Minister Satsuki Katayama has reiterated that authorities are prepared to act at any time if necessary. Historically, interventions have often occurred during periods of thin liquidity, and with a holiday-shortened trading week, conditions could be conducive to action.

The key market debate is increasingly shifting from whether intervention will occur to when it might happen. However, unless any intervention is supported by a narrowing U.S.-Japan yield differential, its impact is likely to be short-lived.

Previous interventions in late February and early May briefly strengthened the yen, but USD/JPY resumed its uptrend as markets quickly re-priced U.S. rate expectations. In that context, intervention has often been faded, as underlying macro forces remain unchanged.

The carry trade continues to be supported by the persistent yield advantage in the U.S., keeping upward pressure on USD/JPY.

Recent hawkish Federal Reserve signals and sticky Core PCE inflation at 3.4%, a three-year high, have led markets to price in around a 60% chance of a 25-basis-point rate hike in September, with expectations of up to three hikes this year.

Looking ahead, attention turns to Federal Reserve Chair Kevin Walsh’s remarks at the ECB Sintra Forum, alongside Thursday’s U.S. non-farm payrolls report. Ahead of that, U.S. consumer confidence and JOLTS job openings data will also be closely watched for further clues on the interest rate outlook.

USD/JPY Forecast – Technical Analysis

USD/JPY has broken above the upper boundary of its rising wedge pattern, extending gains to a new 40-year high at 162.40 and effectively invalidating the prior bearish reversal setup.

Momentum indicators show the RSI in overbought territory across multiple timeframes, suggesting the pair may pause for consolidation before attempting further upside.

On the bullish side, buyers are now eyeing a move toward 165, with the longer-term projection extending to 170 if momentum persists.

On the downside, initial support is seen at 160.20, followed by the key psychological level at 160.00. A break below that zone would expose the 50-day SMA near 159.50, with deeper support at 157.90, where the rising trendline aligns with horizontal support.

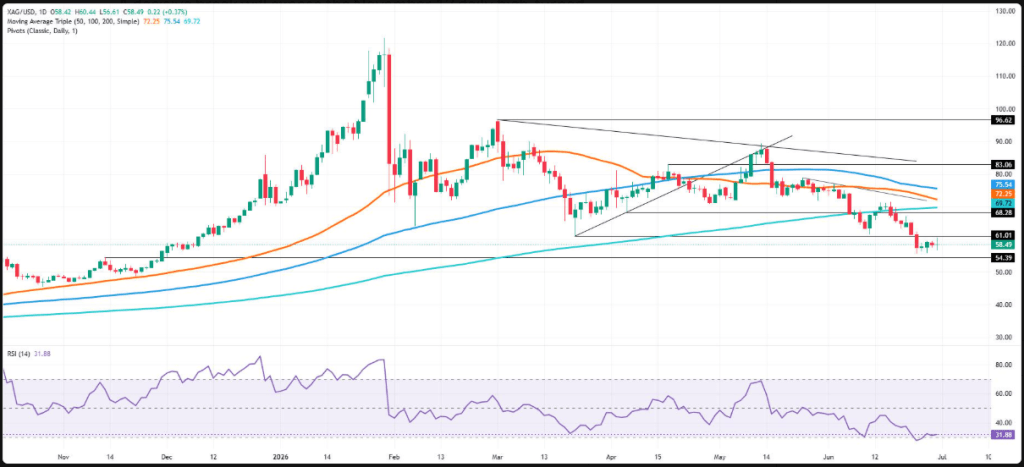

Silver remains trapped below the $60 mark, with the broader bearish trend still firmly in place.

The RSI is approaching oversold levels, indicating that sellers continue to dominate market sentiment.

A decisive break beneath $56.61 could pave the way for a retest of the year-to-date low and the key $55.00 support zone.

Silver prices climbed more than 1.5% on Tuesday despite rising US Treasury yields and a resilient US Dollar. Ongoing concerns over the stability of the fragile ceasefire agreement between the United States and Iran helped support the precious metal, with XAG/USD trading around $58.73, above its opening level.

Technical Outlook

Silver continues to trade in a consolidation phase below the $60.00 threshold, struggling to break above either the psychological resistance at $60.00 or move decisively away from its year-to-date low of $55.63.

Technical momentum remains tilted to the downside, as reflected by the Relative Strength Index (RSI), which is approaching oversold territory and suggests bearish pressure remains dominant.

Should sellers regain control, a break below the intraday low at $56.61 could trigger further losses. The next downside targets lie at the YTD low of $55.63 and the key $55.00 support level. A sustained move beneath these levels could open the door to the November 13 former resistance-turned-support at $54.39, with the psychological $50.00 mark emerging as a longer-term downside objective.

Conversely, a bullish reversal would require buyers to reclaim the March 23 swing low, now acting as resistance, at $61.01. If that barrier is overcome, attention would shift to the 200-day Simple Moving Average near $69.72, followed by the significant $70.00 level.

Gold prices remain steady near $4,015 during Wednesday’s early Asian trading session as investors monitor ongoing US-Iran negotiations. Market sentiment was influenced after US envoy Steve Witkoff and Jared Kushner met with Qatar’s prime minister on Tuesday to discuss diplomatic efforts between Washington and Tehran.

Traders are also turning their attention to key US labor market data due later this week, with the ADP Employment Change report and the closely watched Nonfarm Payrolls (NFP) release expected to provide fresh clues on the Federal Reserve’s policy outlook and the near-term direction of gold prices.

Gold prices (XAU/USD) remained largely unchanged near the $4,015 level during Wednesday’s early Asian session as investors assessed the outlook for potential US-Iran negotiations in Doha. Market participants remained cautious after conflicting statements from Washington and Tehran highlighted the uncertain nature of the temporary peace agreement reached earlier this month.

According to CNBC, US President Donald Trump stated on Tuesday that discussions between the two nations would take place in Qatar, adding that Iran had requested a meeting following the recent exchange of US airstrikes. However, an Iranian Foreign Ministry spokesperson reportedly rejected claims that talks were scheduled in the coming days.

US representatives Jared Kushner and Steve Witkoff arrived in Doha on Tuesday, where they were expected to meet with Qatar’s prime minister to discuss regional developments and ongoing diplomatic efforts involving Iran. Despite these engagements, no direct high-level talks between US and Iranian officials have been confirmed.

Progress toward a lasting diplomatic resolution could enhance demand for Gold as investors seek safe-haven assets amid geopolitical developments. Conversely, continued uncertainty surrounding the negotiations may fuel concerns about inflation and monetary policy, potentially increasing expectations for tighter interest rates. While Gold is widely viewed as a hedge against inflation, its lack of yield can make it less attractive in a higher-rate environment.

Attention now shifts to key US labor market releases, including the ADP employment report on Wednesday and the Nonfarm Payrolls (NFP) report on Thursday. Stronger-than-expected employment figures could reinforce expectations that the Federal Reserve will keep interest rates elevated for longer, supporting the US Dollar and potentially limiting upside momentum in Gold prices.

AUD/USD comes under renewed selling pressure on Wednesday as a combination of factors continues to support the US Dollar. Ongoing uncertainty surrounding Iran and growing expectations of further Fed rate hikes remain key tailwinds for the greenback. Meanwhile, the pair shows little reaction to China’s RatingDog Manufacturing PMI, which came in broadly in line with expectations.

AUD/USD failed to build on Tuesday’s rebound from the 0.6865 area, its lowest level in three months, and came under renewed selling pressure during Wednesday’s Asian session. The pair slipped back below 0.6900 and showed little reaction to China’s latest private manufacturing PMI data.

China’s RatingDog Manufacturing PMI eased to 51.7 in June from 52.2 in May, reinforcing concerns about slowing economic momentum. Combined with Tuesday’s official PMI figures, which highlighted weak domestic demand and subdued consumer spending, the data weighed on the Australian Dollar, which is often viewed as a proxy for China’s economic health. A modest recovery in the US Dollar further added to the pair’s downside pressure.

The Greenback continued to benefit from its safe-haven appeal amid uncertainty surrounding US-Iran negotiations and growing expectations that the Federal Reserve may need to raise interest rates further. Although US officials arrived in Qatar to discuss the implementation of a preliminary peace agreement, Iran’s reluctance to engage with US envoys has cast doubt on the prospects for a lasting resolution, keeping geopolitical risks elevated.

At the same time, stronger-than-expected US labor market data supported the USD. The JOLTS report showed job openings climbed to a two-year high of 7.594 million in May, underscoring continued labor market resilience. Combined with concerns that renewed tensions in the Middle East could reignite inflationary pressures, the data strengthened market expectations for additional Fed tightening.

Investors now await remarks from Fed Chairman Kevin Warsh at the ECB Forum in Sintra, alongside key US data releases including the ADP employment report and ISM Manufacturing PMI. Attention will then turn to Thursday’s closely watched Nonfarm Payrolls report, which could provide the next major catalyst for AUD/USD.

USD/JPY rallies to a fresh four-decade peak on Tuesday amid broad Yen weakness.

The widening US-Japan yield gap continues to weigh on the JPY and underpin the pair.

Renewed demand for the US Dollar, fueled by Iran-related tensions and expectations of further Fed tightening, adds to the upside momentum.

The USD/JPY pair extends its powerful rally above the key 162.00 mark, reaching a new 40-year high during Tuesday’s Asian trading session. Nonetheless, concerns over potential intervention from Japanese authorities continue to limit additional gains.

Japanese Finance Minister Satsuki Katayama and US Treasury Secretary Scott Bessent recently agreed to coordinate on currency matters if required. In addition, Chief Cabinet Secretary Minoru Kihara reiterated last week that the government stands ready to respond to excessive foreign-exchange fluctuations. At the same time, traders remain cautious about adding fresh bearish positions on the Japanese Yen (JPY) following the Bank of Japan’s (BoJ) increasingly hawkish tone.

Minutes from the BoJ’s June policy meeting revealed that officials discussed rising inflation risks, with some members advocating a faster pace of rate hikes toward neutral levels. Growing evidence of stronger inflationary pressures in Japan further supports expectations for additional policy normalization. Even so, Japanese interest rates remain significantly below those in the US, preserving the attractiveness of carry trades that continue to weigh on the Yen.

On the other hand, uncertainty surrounding US-Iran diplomacy and expectations of further Federal Reserve (Fed) tightening are helping the US Dollar (USD) stabilize after its recent retreat from a 13-month peak, providing additional support for USD/JPY. While US President Donald Trump stated that Iran had sought talks with Washington in Qatar, Iranian officials denied that any negotiations with the US are planned in the near future.

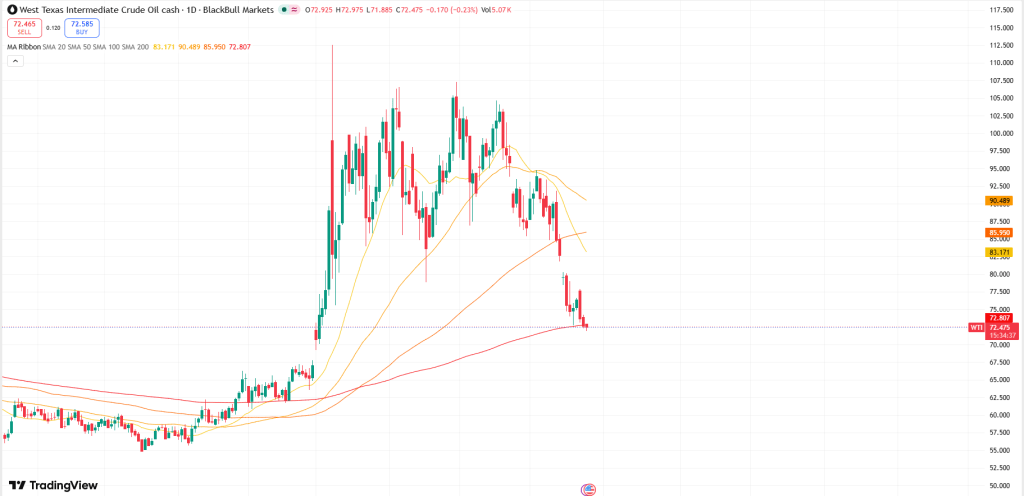

WTI extends losses as conflicting reports on potential US-Iran peace talks fuel uncertainty over the Middle East outlook. President Trump said US and Iranian officials would meet in Doha on Tuesday, but Tehran denied that any talks with Washington had been scheduled. Meanwhile, although vessel traffic has slowed and several ships were damaged following weekend hostilities, tanker operators continue to navigate the strategically important waterway.

West Texas Intermediate (WTI) crude oil surrendered part of its recent advance, slipping toward $70.10 per barrel during Tuesday’s Asian session. The decline followed a mix of conflicting geopolitical developments in the Middle East and uncertainty surrounding potential diplomatic engagement between the United States and Iran.

According to CNBC, US President Donald Trump said Washington and Tehran were set to resume peace talks in Doha, Qatar, on Tuesday after a weekend marked by renewed tensions. Iran, however, swiftly rejected the claim, insisting that no meetings with US officials were planned at any level. Iranian authorities stressed that their priority remains implementing the existing memorandum of understanding rather than pursuing a final settlement.

Further clouding the outlook, Tehran reiterated its intention to monitor shipping activity through the strategically important Strait of Hormuz, even if Oman chooses not to take part. Under the temporary arrangement currently in place, Iran has agreed not to levy transit fees for 60 days, although it has suggested such charges could be introduced afterward. The idea has been strongly opposed by the US, European nations, and Gulf Arab countries.

Despite a slowdown in maritime traffic and damage to two vessels following weekend clashes, tanker operators and crews have continued to navigate the crucial shipping corridor, helping to ease immediate concerns over major supply disruptions.

Bitcoin remains under pressure near the $60,000 mark as weak buyer conviction, persistent selling activity, and cautious positioning in derivatives markets continue to cap recovery attempts.

Meanwhile, Strategy has approved a Bitcoin monetization program that permits the sale of up to $1.25 billion worth of BTC, aiming to enhance liquidity and strengthen its financial flexibility.

According to Bitget analyst Lacie Zhang, the initiative helps alleviate funding concerns but also signals a notable departure from Strategy’s longstanding approach of continuously accumulating Bitcoin.

Bitcoin hovers near $60K as weak demand caps recovery; Strategy approves BTC sales program

Bitcoin (BTC) traded around $60,000 on Monday, attempting to stabilize after last week’s sharp decline. Despite finding support near $58,000, the cryptocurrency has struggled to stage a convincing rebound, with analysts pointing to weak buyer conviction and a broadly defensive market environment.

According to Glassnode, Bitcoin remains stuck near recent lows as buyers have yet to show the confidence needed to drive a sustained recovery. While trading activity has increased, spot markets continue to record net selling pressure, suggesting liquidity is still being used for distribution rather than accumulation.

The cautious mood is also evident in derivatives markets, where traders are scaling back leverage and increasing downside protection. Elevated options skew indicates stronger demand for hedging against further losses, while institutional appetite remains subdued. US spot Bitcoin ETFs have slipped into aggregate unrealized losses and continue to experience net outflows, highlighting limited interest from large investors despite higher trading volumes.

Meanwhile, Strategy unveiled a new Digital Credit Capital Framework aimed at strengthening liquidity and supporting its preferred securities. The company reported a cash reserve of $2.55 billion as of June 28 and authorized a $1 billion repurchase program for its Digital Credit Securities.

As part of the initiative, Strategy’s board approved a Bitcoin monetization program that allows the sale of up to $1.25 billion worth of BTC. The proceeds may be used to bolster cash reserves, fund dividend and interest payments, and support share repurchase programs.

According to Bitget Wallet analyst Lacie Zhang, the move helps ease concerns over Strategy’s liquidity position but also represents a significant shift from the company’s longstanding Bitcoin accumulation strategy. She noted that expanding cash reserves to $2.55 billion extends the firm’s liquidity runway and could improve investor confidence, particularly among holders of its preferred securities.

Strategy currently holds approximately 847,000 BTC, and its MSTR shares rose 12.6% following the announcement, snapping a nine-session losing streak. At the time of writing, Bitcoin was trading near $60,450, up 1.6% over the previous 24 hours.

As markets gradually move beyond pressures from energy inflation, geopolitical tensions, and persistent central bank tightness, a new potential source of volatility is emerging in the Pacific: El Niño.

Introduction

Earlier this month, the National Oceanic and Atmospheric Administration confirmed that El Niño conditions have developed across the Pacific Ocean. Early projections indicate this could evolve into one of the strongest events in decades, with impacts extending well beyond weather patterns.

El Niño is a recurring climate phenomenon that appears every few years when trade winds across the tropical Pacific weaken. As a result, warm surface waters that are usually pushed toward Asia and Oceania shift back toward the Americas. This disrupts global weather systems, often causing heavier rainfall in parts of the Americas while bringing hotter, drier conditions to regions such as South and Southeast Asia, Australia, and Southern Africa. These shifts can lead to droughts, heatwaves, or excessive rainfall, all of which can damage crop yields, disrupt planting cycles, and strain global food supply chains. Following a period where inflation has been driven largely by energy costs, food-related shocks may become the next major inflationary pressure.

A Strong El Niño Is Taking Shape

Research on El Niño’s macroeconomic effects consistently highlights its influence on commodity markets, particularly agriculture. The main transmission channel is through food prices, with multiple studies suggesting a clear link between ENSO cycles and commodity inflation.

Federal Reserve research estimates that nearly 20% of fluctuations in commodity-price inflation can be attributed to ENSO patterns. In a typical El Niño event, real commodity inflation may rise by around 3% over a six- to twelve-month horizon, with agricultural commodities experiencing the most significant impact. Studies by Cashin, Mohaddes, and Raissi further suggest global non-energy commodity prices can increase by approximately 5%, with effects lasting six to sixteen months.

Weather disruptions reduce crop yields, degrade quality, and delay transportation, tightening physical supply conditions. Agricultural prices tend to respond first, and rising input costs eventually feed through to broader food inflation. This can also weaken local currencies, increase imported inflation, and reduce central banks’ flexibility to lower interest rates.

Two key patterns stand out.

First, the growth effects differ significantly across countries. Economies such as Australia, India, Indonesia, Chile, parts of Southern Africa, and the Andean region typically experience negative output shocks when El Niño disrupts rainfall and agricultural activity. In contrast, the United States and some European economies may see a smaller negative impact or even modest gains. In South America, particularly Brazil and Argentina, segments of the soybean supply chain can benefit from increased rainfall conditions.

Second, inflation responses are uneven across regions. The effect is most pronounced in countries where food accounts for a large share of the consumer price index and where exchange rate pass-through is strong. In these economies, rising food and energy costs can push up inflation expectations, weaken domestic currencies, and intensify imported inflation pressures. As a result, central banks—especially in emerging markets that rely on commodity imports—often face limited scope to reduce interest rates.

The euro area is relatively insulated. Research from Banco de España suggests that El Niño episodes have historically lowered euro-area inflation by about 0.3 percentage points after one year. This is mainly due to composition effects and the Common Agricultural Policy, which helps buffer the transmission of global food price shocks to European consumers.

The Commodity Shock

Commodity markets typically move ahead of official inflation data, as agricultural prices are driven by expectations that can shift rapidly with changes in rainfall, temperature, and harvest conditions. This year, weather-related risks are emerging on top of already elevated input costs. Farmers continue to face high fertiliser and diesel expenses following prolonged energy-market stress and geopolitical disruptions. The World Bank projects global commodity prices to rise by about 16% in 2026—the first annual increase since 2022—driven mainly by energy and fertiliser costs. While agricultural prices are expected to decline under baseline assumptions, El Niño represents a clear upside risk to that outlook.

Historically, El Niño episodes have tended to support soft commodity prices. Products such as cocoa, coffee, sugar, palm oil, cotton, and rice are highly sensitive to rainfall patterns in tropical regions. However, the actual price response varies depending on inventory levels, regional weather conditions, and substitution effects across crops.

Cocoa is particularly vulnerable. Ivory Coast and Ghana together account for roughly half of global cocoa production. Strong El Niño events have often reduced output in these regions, either through drought conditions or through a combination of excessive rainfall followed by disease pressure. The most recent cycle illustrated this clearly: heavy rains initially increased disease risk for cocoa trees, followed by extreme heat and dry Harmattan winds that further damaged already weakened crops. As a result, cocoa prices surged dramatically in 2024, at one point approaching or exceeding USD 12,000 per metric ton, making it one of the most volatile commodity stories of the year.

Palm oil and cotton also carry significant exposure to weather conditions in Asia, particularly in Indonesia, Malaysia, and India. Any weakness in the monsoon season can quickly alter supply expectations for these crops.

Coffee exposure is mainly concentrated in robusta production, with Vietnam and Indonesia accounting for around half of global supply. El Niño typically brings hotter and drier conditions during key growing stages. Arabica behaves differently: Brazil may initially benefit from reduced frost risk, but later-season heat and dryness can still threaten yields.

Sugar is somewhat more resilient. A weaker monsoon in India and Thailand can support prices, although India may offset part of the production loss by diverting ethanol feedstock back into sugar output.

Rice is highly sensitive to monsoon performance. A weak rainy season across Asia can quickly reduce output expectations and heighten food security concerns, especially in countries where rice is a dietary staple.

Corn is influenced more by regional weather patterns than El Niño alone. While dryness in some regions can support prices, the overall signal is mixed because other growing areas may experience favorable conditions.

Soybeans present a more complex picture. While El Niño can create stress in certain regions, improved rainfall in Brazil and Argentina may offset losses elsewhere, making price effects less straightforward compared with crops like rice or palm oil.

Natural gas stands out as the main exception. A milder winter in the Northern Hemisphere typically reduces heating demand and puts downward pressure on prices. However, in 2026 this seasonal weakness may be partially offset by broader energy-market tensions linked to geopolitical risks in the Strait of Hormuz.

Looking ahead, the Indian monsoon is a key near-term catalyst. Rainfall between June and September will be critical for cotton, sugar, rice, and palm oil markets. A normal monsoon would likely contain much of the El Niño-related risk, while a significant shortfall would reintroduce strong upside price pressure.

Finally, there is a mismatch in timing between futures and physical markets. Weather forecasts are still influenced by the “spring predictability barrier,” a period when El Niño models are less reliable before summer data becomes clearer. As a result, futures markets may begin pricing in 2026–27 weather risks well in advance, while physical markets remain anchored to current inventories, crop conditions, and near-term supply-demand fundamentals.

Implications for Financial Markets

In equity markets, potential beneficiaries typically include fertiliser manufacturers, agricultural input suppliers, and commodity-exporting firms. In contrast, companies involved in food processing, beverages, and other downstream users of agricultural commodities may face margin compression due to rising input costs. The insurance and reinsurance sectors could also come under pressure from increased claims linked to extreme weather events such as floods, droughts, and wildfires. While overall equity performance may be dampened by supply-chain disruptions and agricultural volatility, the impact is likely to differ significantly across regions and sectors.

From a foreign exchange and emerging markets perspective, countries that rely heavily on food imports and have high inflation pass-through tend to be most vulnerable. These economies may experience currency depreciation and tighter monetary policy conditions. On the other hand, commodity-exporting nations could benefit from improved terms of trade. Overall, a strong El Niño event would create meaningful cross-asset implications, favoring selective exposure to commodities, inflation hedges, and careful allocation across duration, emerging market assets, and sector positioning. Close monitoring of updates from agencies such as NOAA, the WMO, and commodity price signals will be important for positioning decisions.

Conclusion

Even a severe El Niño is considered a secondary risk compared to the current energy-driven shock originating from the Strait of Hormuz, which remains the dominant force shaping commodity and inflation dynamics. Its importance lies in its role as an additional upside risk to food inflation and emerging market pressure.

The most important near-term variable to watch is the Indian monsoon through September, which will act as a key turning point. A normal monsoon would help contain much of the weather-related risk, while a significant shortfall could transform the current uncertainty into a clearer and more tradable disruption in soft commodity markets.

Gold erased part of its two-day recovery from seven-month lows as sellers returned ahead of the key US Nonfarm Payrolls report. A firmer US Dollar, supported by renewed Middle East tensions and expectations that the Federal Reserve will keep rates higher for longer, continued to weigh on the precious metal. With the daily RSI remaining bearish and a Death Cross still in effect, gold retains a negative technical outlook and remains vulnerable to selling pressure on rallies.

XAU/USD Technical Overview

On the daily chart, XAU/USD is trading around $4,068.30, extending its decline and remaining firmly below key short- and medium-term moving averages, which keeps the near-term outlook bearish. Gold is currently trading beneath the 21-day SMA at $4,240.86, the 50-day SMA at $4,453.85, and the 200-day SMA at $4,479.26. Meanwhile, the 100-day SMA at $4,674.59 remains significantly higher, highlighting strong overhead resistance and reinforcing the broader downtrend. The 14-day Relative Strength Index (RSI) hovers near 36, signaling ongoing bearish momentum while still staying above oversold territory.

Adding to the negative outlook, gold confirmed a bearish Death Cross on Friday after the 50-day SMA closed below the 200-day SMA on a weekly basis, a technical signal often associated with prolonged downside risks.

On the upside, immediate resistance is located at the 21-day SMA near $4,240.86, followed by the 50-day SMA at $4,453.85 and the 200-day SMA at $4,479.26. Together, these levels form a significant resistance zone that buyers would need to overcome to improve the technical outlook. A decisive move above this cluster could pave the way toward the 100-day SMA around $4,674.59. Until then, gold remains exposed to further weakness, with market participants closely monitoring for the emergence of fresh support levels below the current $4,068 area.

Fundamental Analysis Summary

Gold bears are regaining control as the US Dollar (USD) continues to head toward its strongest monthly performance in nearly a year. This comes amid renewed uncertainty surrounding the ceasefire between the United States and Iran, as well as doubts over whether peace talks will resume.

Over the weekend, both sides exchanged strikes and accused each other of violating the ceasefire before eventually agreeing to stop retaliatory attacks and hold negotiations in Qatar on Tuesday.

Despite emerging optimism around diplomatic talks and a pullback in oil prices, markets remain cautious and continue to favor the US dollar—the world’s reserve currency—over gold.

At the same time, gold is also under pressure from rising expectations of further US Federal Reserve interest rate hikes, with markets pricing in at least two increases before year-end.

Looking ahead, attention will shift beyond geopolitics to US Nonfarm Payrolls (NFP) data due Thursday, a key indicator of labor market strength and a major signal for the Fed’s policy direction.

Since gold typically performs better in lower interest rate environments, upcoming Fed guidance is expected to play a crucial role in shaping bullion’s trajectory.

Earlier in the week, traders will also closely monitor the European Central Bank’s annual forum in Sintra, Portugal. A highlight will be Wednesday’s policy panel featuring Fed Chair Kevin Warsh, following his unexpectedly hawkish tone at the beginning of the month.

Ask a trader what they expect to earn from their next trade, and the answer usually comes quickly. Ask how much they are prepared to lose, and the response often takes much longer. That hesitation reveals a common mistake.

Most Traders Focus on Potential Gains

Many traders enter a position thinking primarily about profits. They imagine the trade working out before it has even begun. The possible reward becomes the center of attention, while the potential loss is treated as a secondary concern.

The problem appears when the market moves against them. Emotions take over, discipline fades, and hope replaces strategy. A loss that could have been controlled grows larger because no clear exit plan was established beforehand.

Start With the Risk

Before calculating possible profits, determine the maximum amount you are willing to lose. Know where your stop belongs, how much capital is exposed, and whether your account can comfortably absorb the loss.

No trader is right all the time. Losses are an unavoidable part of trading. What separates experienced traders from inexperienced ones is that professionals decide in advance how much a losing trade will cost. Their losses are controlled, expected, and manageable.

Clarity Reduces Emotional Trading

Understanding your downside risk is not pessimistic—it is practical. When you know the worst-case scenario, you can make decisions more objectively.

Many trading mistakes stem from uncertainty. Traders move stop-loss orders, close winning positions too early, or hold losing trades too long because they do not have a clearly defined risk level. Once that level is established, it becomes much easier to follow the plan rather than react emotionally to market fluctuations.

Protecting Capital Comes First

Risk management is also supported by simple mathematics. A 50% loss requires a 100% gain just to break even. The larger the drawdown, the harder recovery becomes.

Without capital, there is no opportunity to participate in future trades. Preserving your account is not merely part of a trading strategy—it is the foundation of one.

Professionals Think Differently

Professional traders rarely begin by discussing potential profits. Instead, they focus on position size, stop placement, exposure limits, and the price level that would invalidate their trade idea.

Once risk is controlled, profits can take care of themselves. Professionals think in terms of hundreds or thousands of trades, while amateurs often become emotionally attached to the outcome of a single position.

Define the Loss Before Entering

Before placing any trade, imagine the market moving against you. Determine your exit point, calculate the dollar amount at risk, and make sure the loss is small enough that you can continue trading confidently tomorrow.

If the potential loss feels uncomfortable, the position size is likely too large.

Risk Before Reward

Successful trading begins with protecting the downside. Focus on risk first and reward second. Traders who consistently manage risk give themselves the opportunity to stay in the game long enough to benefit from future winning opportunities.

In the long run, survival is what makes success possible.

WTI crude oil prices slid to around $69.60 during early Asian trading on Monday as optimism grew over a potential diplomatic breakthrough between the US and Iran. Market sentiment improved after reports indicated that both countries were moving back toward negotiations aimed at ending the conflict, with Axios reporting that US and Iranian officials are scheduled to meet in Qatar on Tuesday.

WTI crude oil retreated to around $69.60 during early Asian trading on Monday as easing geopolitical tensions weighed on prices. The decline followed reports that the United States and Iran had agreed to suspend military strikes and resume negotiations, with officials from both countries expected to meet in Qatar on Tuesday.

According to Axios, citing unnamed US officials, Washington and Tehran have agreed to halt more than three days of retaliatory attacks in and around the Strait of Hormuz and continue technical discussions aimed at de-escalating the conflict. The move marks a shift from the weekend, when talks were reportedly suspended after US strikes on Iranian military targets in response to Tehran’s attacks on shipping vessels in the strategic waterway.

Meanwhile, Iran’s Islamic Revolutionary Guard Corps (IRGC) claimed responsibility for attacks on eight US military sites in Kuwait and Bahrain, describing them as retaliation for recent American strikes on Iranian facilities.

Market participants will remain focused on the outcome of the upcoming US-Iran talks. Any diplomatic progress could help secure oil flows through the Strait of Hormuz, a critical route that handles roughly one-fifth of global oil shipments, potentially putting further pressure on crude prices. Conversely, renewed hostilities could reignite concerns over supply disruptions and support higher oil prices.

Investors are also awaiting the latest weekly crude inventory data from the American Petroleum Institute (API) on Tuesday. A larger-than-expected decline in stockpiles would signal stronger demand and could provide support for WTI, while an unexpected inventory build may point to weaker consumption or excess supply, weighing on prices.

Gold slips toward $4,050 as uncertainty surrounds US-Iran talks.

Gold slips toward $4,060 in Monday’s Asian trading session as uncertainty surrounding US-Iran relations weighs on market sentiment. A US official indicated that both countries will “stand down for now,” easing immediate geopolitical concerns. Investors are now turning their attention to the upcoming US Nonfarm Payrolls report on Thursday for further clues on the Federal Reserve’s policy outlook.

Gold prices (XAU/USD) edged lower to around $4,060 during Monday’s Asian session as investors weighed ongoing uncertainty surrounding US-Iran relations and growing expectations that the Federal Reserve could raise interest rates later this year.

According to reports, the United States and Iran have agreed to temporarily halt hostilities and are scheduled to meet in Doha, Qatar, on Tuesday to discuss the dispute over the Strait of Hormuz. US officials indicated that both sides would “stand down for now” after recent military exchanges near the strategically important waterway.

Despite the diplomatic efforts, geopolitical risks remain elevated. Iranian Foreign Minister Abbas Araghchi stressed that responsibility for the Strait of Hormuz rests solely with Tehran, while another Iranian official warned that attempts to bypass Iran’s preferred shipping route could trigger further tensions and escalation. Renewed instability in the Middle East could fuel inflation concerns and strengthen expectations for tighter monetary policy, reducing the appeal of non-yielding assets such as gold.

Meanwhile, market participants are increasingly betting on a Federal Reserve rate hike, with the CME FedWatch Tool indicating nearly a 59.7% probability of an increase as early as September 2026. Investors are now focused on Thursday’s US Nonfarm Payrolls (NFP) report, which is expected to show that 114,000 jobs were added in June while the unemployment rate remained steady at 4.3%. Strong labor market data could reinforce the case for higher interest rates and add further pressure on gold prices.

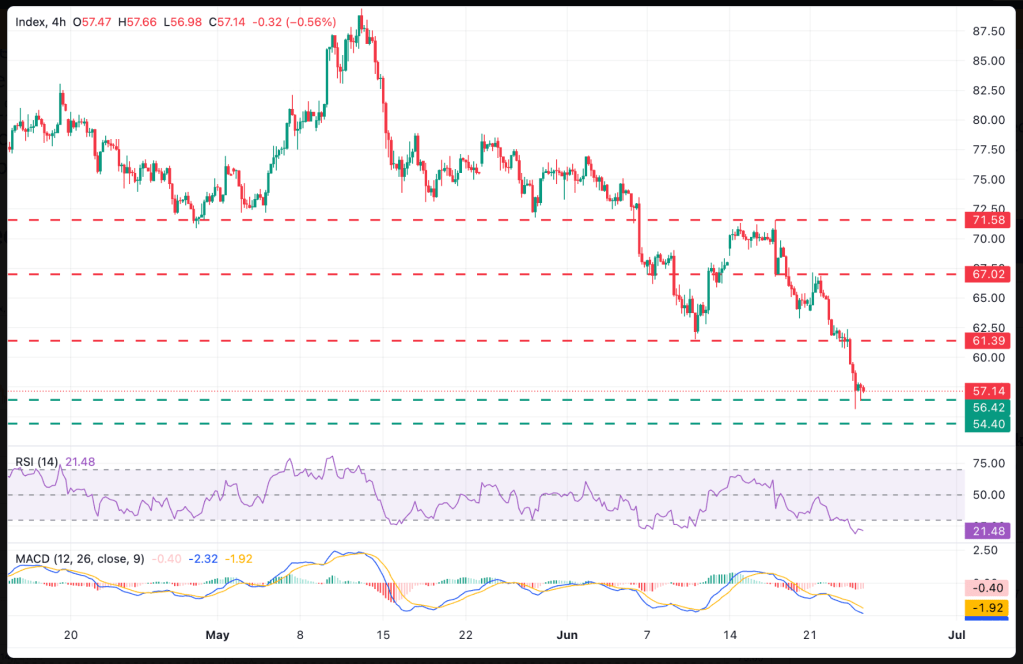

Silver remains below $59.00 as renewed Strait of Hormuz tensions support safe-haven demand.

Silver (XAG/USD) remains under pressure below $59.00 as renewed US-Iran tensions over the Strait of Hormuz fuel concerns about higher oil prices and rising inflation. However, losses are limited after Washington and Tehran agreed to pause hostilities ahead of peace talks scheduled in Doha later this week. Meanwhile, persistent expectations of a hawkish Federal Reserve continue to weigh on the non-yielding precious metal, keeping silver prices subdued.

Silver (XAG/USD) retreats to around $58.80 during Monday’s Asian session, snapping a two-day winning streak as renewed tensions between the United States and Iran in the Strait of Hormuz boost oil prices and reignite inflation concerns. Market sentiment remains sensitive to developments in the Middle East amid fears that escalating geopolitical risks could disrupt global energy supplies.

Despite the renewed clashes, downside pressure on silver is somewhat limited after Washington and Tehran agreed to suspend attacks ahead of peace talks in Doha this week. The diplomatic breakthrough follows several days of retaliatory strikes triggered by an incident involving a cargo vessel, with both sides accusing each other of breaching the June 17 ceasefire. Officials from the US and Iran are expected to meet in Qatar on Tuesday in an effort to de-escalate tensions.

Meanwhile, silver continues to face headwinds from persistent expectations of tighter US monetary policy. According to the CME FedWatch Tool, markets are pricing in a 59.7% probability of a Federal Reserve rate hike in September 2026. Investors are now focused on this week’s US labor market data, particularly Thursday’s Nonfarm Payrolls report. Economists expect the US economy to add 114,000 jobs in June, while the unemployment rate is projected to remain unchanged at 4.3%. Strong employment figures could reinforce the Fed’s hawkish stance and further weigh on non-yielding assets such as silver.

Gold started the previous week with a noticeable gap lower, highlighting the market’s ongoing uncertainty and elevated volatility. Price fluctuations are likely to remain significant in the near term as traders continue to react to various external factors.

The $4,000 level remains a key support zone. As long as gold stays above this threshold, short-term pullbacks could present buying opportunities. However, a decisive break below $4,000 may trigger a deeper correction, potentially sending prices toward the $3,500 area.

On the upside, a move above the 50-week EMA would strengthen the bullish outlook and could pave the way for a rally toward $4,600. That said, gold continues to be influenced by a range of macroeconomic and geopolitical developments, making its direction less predictable.

For now, the most likely scenario may be a period of consolidation, with prices trading within a broad range while the market searches for its next major catalyst.

EUR/CHF

The euro declined notably against the Swiss franc over the past week, yet the 0.92 level continues to serve as an important support area. A rebound from this zone would not be surprising, as the pair appears to be searching for enough momentum to resume a move higher, potentially targeting a break above 0.93.

In the near term, buying on a bounce remains an attractive strategy, especially if support at 0.92 continues to hold. However, if the pair falls decisively below this level, downside pressure could intensify, opening the door for a move toward 0.91.

Overall, EUR/CHF may remain range-bound in the short run, with traders closely watching whether support at 0.92 can sustain another upward attempt.

USD/CHF

The U.S. dollar posted gains against the Swiss franc during the week, but a significant portion of those advances was later erased. This price action suggests that the pair may be due for a corrective pullback after its recent rally.

The 0.80 level stands out as a key area to watch. A retreat toward this support zone could provide a potential buying opportunity if the market shows signs of stabilization and renewed bullish momentum. Traders may look for a bounce from this level as confirmation of a possible continuation higher.

On the upside, a breakout above the high of the current weekly candlestick would strengthen the bullish outlook and could lead to a test of the 0.82 level.

Overall, the short-term bias remains cautiously positive, although a pullback toward support may be needed before the next leg higher can develop.

USD/MXN

The U.S. dollar advanced against the Mexican peso during the week, but the 17.50 level once again proved to be a strong area of resistance. The subsequent pullback from those highs is not particularly surprising and suggests that the pair may continue trading within its established consolidation range.

Looking ahead, USD/MXN is likely to remain volatile and range-bound as traders assess the next directional catalyst. While occasional swings above or below recent levels are possible, the broader price action continues to favor consolidation rather than the start of a sustained trend.

Even if the U.S. dollar manages to break decisively higher against the Mexican peso, the move may not offer an attractive trading opportunity given the pair’s tendency to remain choppy and unpredictable. For now, traders may be better served by focusing on short-term range dynamics rather than chasing a potential breakout.

Nasdaq 100

The Nasdaq 100 moved lower throughout the week, but the broader picture suggests that the index is simply consolidating after an extended rally. Recent weakness appears to be a healthy pause as the market works off some of the excess optimism and overbought conditions that developed earlier.

Despite the pullback, the longer-term outlook remains constructive. Buyers are likely to re-emerge over time, although current market conditions do not necessarily justify taking large positions. The index may continue to trade within a range while investors assess economic data, corporate earnings, and monetary policy expectations.

Short-term declines could present attractive buying opportunities, particularly if prices approach the 28,500 level, which may act as a significant support area. For now, the focus remains on identifying value during pullbacks rather than betting against the broader uptrend.

Overall, the bias remains cautiously bullish, with dip-buying favored over short-selling.

GBP/USD

The British pound posted a modest recovery against the U.S. dollar during the week, with the 1.32 level continuing to establish itself as an important support zone. The market’s ability to hold above this area suggests that buyers remain active and willing to defend the pair on pullbacks.

On the upside, the 1.33 level remains a key resistance barrier. A successful move above this threshold would strengthen bullish sentiment and could pave the way for a further advance toward the 1.35 level.

In the near term, GBP/USD is likely to remain range-bound between support at 1.32 and resistance at 1.33 as traders wait for a stronger catalyst. However, a breakout above the upper boundary of this range could signal the start of a more sustained upward move.

Overall, the outlook remains cautiously positive, with the potential for additional gains if buyers can push the pair decisively above 1.33.

EUR/USD

The euro experienced a notable decline against the U.S. dollar during the week but managed to recover and return to the 1.14 area. This level has served as a major short-term support zone for much of the past year, making current price action particularly important for determining the pair’s next direction.

After briefly breaking below 1.14, the market has rebounded to retest this key level. Traders will be watching closely to see whether it acts as resistance following the breakdown or if buyers can regain control and push the pair higher.

A sustained move above 1.1450 would improve the bullish outlook and could encourage additional buying interest in the euro. However, there is also a strong possibility that EUR/USD remains anchored around the 1.14 level while the market searches for a clearer catalyst.

Ultimately, the pair’s direction may depend less on euro-specific factors and more on the broader performance of the U.S. dollar. As a result, developments in U.S. economic data, interest rate expectations, and overall dollar sentiment are likely to play a decisive role in shaping EUR/USD’s next major move.

USD/JPY

The U.S. dollar continued its gradual advance against the Japanese yen during the week, maintaining the bullish momentum established by recent breakouts. As a result, USD/JPY remains one of the key currency pairs to watch in the current market environment.

The 162.00 level represents an important resistance zone. A decisive break above this threshold could signal the continuation of the broader uptrend and open the door to further gains for the U.S. dollar.

While Japanese authorities have recently intervened in the currency market to support the yen, the underlying fundamentals still appear favorable for USD/JPY. In particular, the significant interest rate differential between the United States and Japan continues to attract investors toward the pair.

Short-term pullbacks may therefore present buying opportunities, especially if prices retrace toward the key 160.00 level, which is likely to act as an important support area. As long as this zone holds, the overall bullish bias remains intact.

Overall, the outlook continues to favor the upside, with traders closely monitoring whether USD/JPY can break through 162.00 and extend its recent rally.

Bitcoin’s historically dependable four-year halving cycle indicates that the current bear market could persist through Q3 before a more sustainable bottom is established. But how do valuation metrics, central bank policy, liquidity growth, market sentiment, and institutional participation factor into the outlook?

Key Bitcoin Takeaways

The well-established four-year halving cycle points to continued downside pressure through Q3 before Bitcoin potentially forms a lasting market bottom.

Near-term momentum for Q3 still leans bearish, though the outlook for Q4 is becoming increasingly constructive as valuations remain relatively subdued and long-term holders continue to show resilience.

Long-term investors may still need to remain patient until price action provides clearer confirmation of a more bullish trend heading into the lead-up to the 2028 halving cycle.

Bitcoin H1 2026 Review

In our previous Bitcoin outlook, we noted that “Bitcoin remains in a downtrend from the October 2025 peak” and that “there is still no clear evidence the current decline has ended.” Despite several recovery attempts — including a rebound above $80K in mid-May — that assessment has largely held true. The main question facing crypto traders now is not whether the downtrend exists, but when and at what level it may finally bottom out.

Below, we revisit our quarterly outlook for the world’s largest cryptocurrency and examine the key fundamental and technical forces likely to influence Bitcoin over the months ahead.

Bitcoin Q3 2026 Outlook

From a broader market-cycle perspective, analysts continue to focus on Bitcoin’s historically reliable four-year cycle linked to the Bitcoin Halving. While past performance does not guarantee future results, the cycle has consistently helped identify major market tops and bottoms over time.

For newer market participants, the Bitcoin Halving refers to the event where mining rewards are reduced by half. This slows the pace of new Bitcoin issuance, tightening supply growth over time. Reduced supply inflation has historically strengthened Bitcoin’s scarcity narrative and increased its appeal among long-term investors. Following the April 2024 halving, Bitcoin’s annual supply growth rate fell below 1% — less than half the estimated annual supply growth of gold.

One of the most widely followed long-term cycle charts — sometimes nicknamed “The Only Bitcoin Chart You’ll Ever Need™” — illustrates how previous halvings often marked the shift from the yellow post-bottom recovery phase into the green full-scale bull market phase, eventually followed by the red bear-market reset phase as optimism fades and sentiment resets.

Projecting a similar cycle forward from the April 2024 halving suggests that Bitcoin likely peaked near the beginning of Q4 2025, with a more durable long-term bottom potentially not arriving until closer to the start of Q4 2026.

Beyond the four-year cycle, Bitcoin’s broader fundamental and technical outlook remains mixed, with several competing forces shaping the market environment.

From a macroeconomic standpoint, the monetary policy landscape appears to be shifting once again, as an increasing number of central banks lean toward higher interest rates while managing the ongoing effects of geopolitical disruptions. Although most global central banks have still been easing policy in recent months, the broader trend may be starting to reverse. Major institutions such as the European Central Bank, Bank of Japan, and Federal Reserve are all signaling a growing bias toward additional tightening, potentially pressuring other central banks around the world to follow suit.

Looking ahead, the growing focus on the risk of renewed inflation could become a meaningful headwind for Bitcoin during the second half of the year, particularly as governments around the world continue to maintain relatively accommodative fiscal policies.

At the same time, the expansion of fiat liquidity within the global financial system has moderated in recent months. The so-called “M2” money supply — a broad measure tracked by central banks that includes physical cash, checking deposits, savings accounts, and other short-term savings instruments such as certificates of deposit (CDs) — continues to increase overall, but at a slower pace. Year-over-year M2 growth has cooled to around 6%, down from levels near 12% seen earlier this year.

One of the core narratives underpinning Bitcoin’s long-term appeal is its role as “hard money” — a potential hedge against the debasement of fiat currencies. As long as the global money supply continues to expand over time, that narrative may continue to provide underlying support for Bitcoin prices.

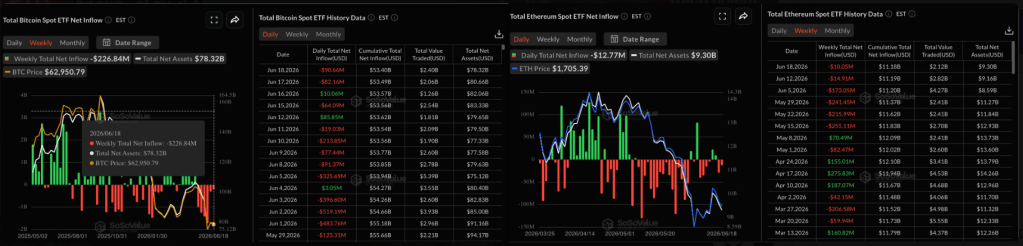

Beyond the broader macro backdrop, another major driver of Bitcoin’s rise in recent years has been sustained accumulation from both large financial institutions and retail investors. Alongside the growing number of companies adding Bitcoin to their corporate treasuries, institutional participation through traditional finance channels has also expanded significantly. In particular, spot Bitcoin ETFs have attracted substantial demand from “TradFi” investors, with cumulative inflows approaching $53 billion. However, those inflows have largely plateaued since mid-2025, suggesting institutional momentum has slowed for now.

Broadly speaking, renewed buying activity in Bitcoin ETFs would likely provide support for the cryptocurrency, while a transition toward sustained outflows or coordinated selling could create additional downward pressure.

From a valuation standpoint, one closely watched indicator is the MVRV (Market Value to Realized Value) Z-score, which compares Bitcoin’s current market price with the average price at which coins last moved on-chain. The metric has now declined to around 0.3 — much closer to the historical bear-market bottom zone near 0.0 than the overheated peak above 3.0 seen earlier in the cycle. This suggests that Bitcoin’s valuation has become significantly less stretched, even if broader market conditions remain uncertain.

In another sign that Bitcoin is gradually maturing as an investment vehicle — and arguably emerging as a distinct asset class — this valuation metric has become noticeably less volatile over time. For example, the latest cycle peak failed to rise above 4, well below the extreme readings between 7 and 10 seen in prior cycles. As a result, the indicator may also avoid falling as deeply below zero as previous bear-market bottoms in the -0.3 to -0.6 range would imply. Whether the MVRV Z-score continues to serve as a reliable long-term valuation gauge remains to be seen.

Another important factor to monitor is the behavior of long-term holders. As highlighted in previous outlooks, investors who have held Bitcoin for more than a year are generally not seeking short-term profits. Instead, they tend to be committed long-term participants — often referred to as “HODLers” — who are less likely to sell unless they are sitting on exceptionally large gains.

As the chart below illustrates, the share of Bitcoin held for at least one year has declined from record highs above 70% to below 59%. However, the metric now appears to be stabilizing and gradually trending higher again as long-term holders continue to withstand the worst phase of the bear market. Because this indicator naturally evolves slowly, it may not shift dramatically in the near term. Still, any renewed wave of selling from longer-term holders could counterbalance ETF inflows during the second half of the year.

Taking all of these factors into account, the near-term outlook for Bitcoin in Q3 remains tilted to the downside. Growth in global money supply and Bitcoin ETF inflows has slowed, central banks are increasingly adopting a more hawkish stance, and the historically reliable four-year cycle continues to point toward additional short-term weakness.

That said, the outlook for Q4 is beginning to appear more constructive. Valuation metrics have cooled considerably, long-term holders continue to show resilience, and the four-year cycle itself is approaching what could become a major cyclical bottom.

Naturally, the scenarios outlined in this report may not unfold exactly as expected — and in some cases, the market may have already priced in these risks and opportunities. As always, traders and investors should approach Bitcoin and other crypto assets with caution while closely monitoring both macroeconomic conditions and crypto-specific indicators as the year progresses.

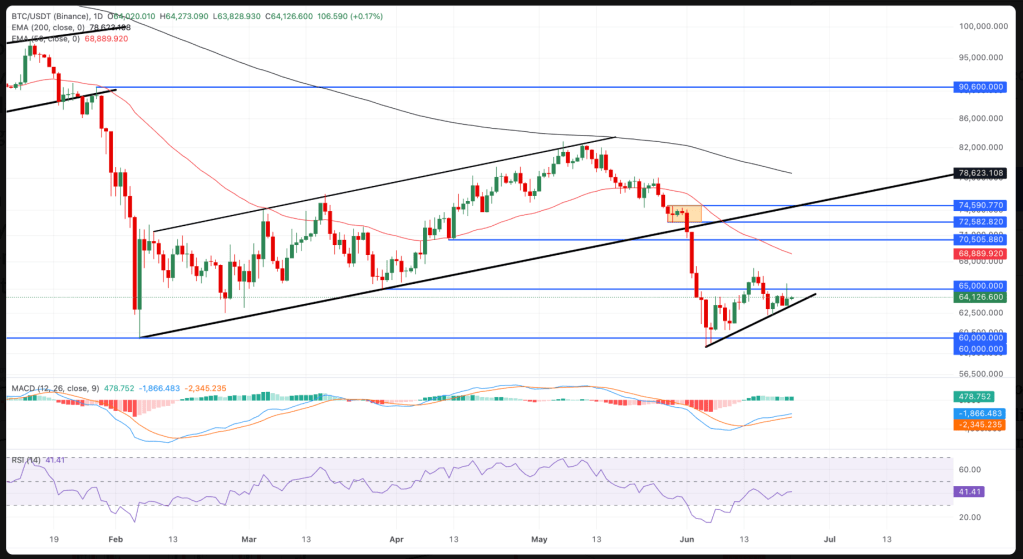

Bitcoin Technical Analysis

Looking at the longer-term chart, Bitcoin remains firmly in a downtrend from the October 2025 peak. Since topping out, the cryptocurrency has continued to form a pattern of lower highs and lower lows, interrupted only by periodic consolidation phases and short-lived relief rallies.

As we highlighted three months ago, there is still little technical evidence suggesting that the broader downtrend has ended. If Bitcoin breaks below the year-to-date lows around $60K, the next major support zone begins in the mid-$50K area. Such a move would imply an approximate 60% decline from the cycle peak, consistent with the pattern of progressively smaller bear-market drawdowns seen as Bitcoin has matured over time — roughly -93%, -86%, -84%, and -78% during the 2011, 2014, 2018, and 2022 bear markets, respectively.

On the upside, bulls would likely need to reclaim former support-turned-resistance near the $66K region before confidence in a longer-term trend reversal can improve meaningfully. Beyond that, the May high near $83K remains the next major hurdle. Until those levels are decisively broken, long-term investors may continue to benefit from patience while waiting for clearer confirmation of a more sustainable bullish trend heading into the 2028 halving cycle.

The past few sessions have delivered what traders both welcome and dislike—sharp moves followed by equally sharp uncertainty.

The dollar is still advancing into key resistance levels, while precious metals are attempting to stabilize after hitting several downside targets outlined earlier this week. The positive takeaway is that many of those projected scenarios have unfolded as expected. The key question now is whether this marks the beginning of a reversal or merely a pause before further declines.

As always, today’s daily closes are likely to provide clearer signals than intraday fluctuations.

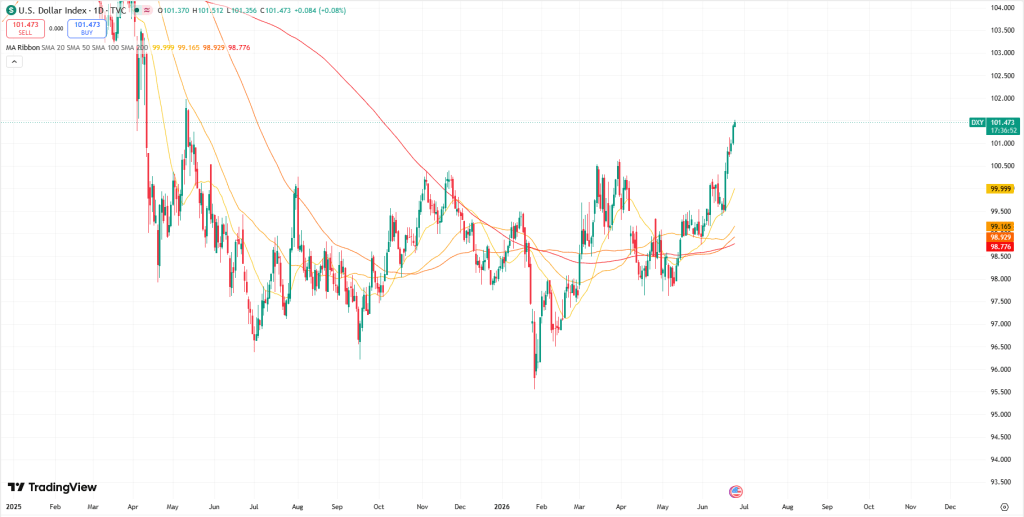

Dollar Index (DX.F)

Let’s begin with a brief recap before moving into today’s update. On Tuesday, we noted:

“(…) If buyers manage to close the day above the upper boundary of the channel, the breakout would open the door toward (at least) the next resistance zone near 101.39–101.59 (…)”

From today’s perspective, the market has largely followed that roadmap. Sustained trading above the upper boundary of the rising channel allowed the Dollar Index to extend gains into the 101.39–101.59 resistance area during yesterday’s session.

So, what comes next?

Early warning signals are beginning to emerge. Momentum indicators are now displaying negative divergences relative to price, hinting that the recent breakout may soon face its first meaningful test.

However, bulls still retain the benefit of the doubt for now.

As long as price continues to close above the prior channel resistance, buyers remain in control and may still target the next upside zone around 101.74–101.81, where the 138.2% Fibonacci extension aligns with the May 2025 intraday high.

On the downside, if sellers step in and push the market to a daily close back below this key support area, the breakout would be invalidated. In that case, initial downside risk would shift toward a retest of the former breakout zone near 100.50–100.53.

Platinum (PL.F)

Before moving into today’s update, let’s revisit Tuesday’s comment:

“(…) If buyers fail to reclaim 1665 by today’s close (meaning they cannot hold the bullish gap from June 12), the odds of a move toward the 1600 region increase significantly, particularly if the dollar continues to strengthen. (…)”

Looking at the latest chart, platinum unfolded largely in line with the bearish scenario, testing both the support zone and the lower boundary of the declining orange channel.

What stands out now is the emergence of bullish divergences on daily momentum indicators. In other words, momentum is no longer fully confirming the recent decline — a pattern that is also beginning to appear in gold and silver.

Does this mean a reversal is underway?

Possibly.

But the technical picture has not confirmed it yet.

The key concern for bulls is that platinum still trades below both the June 11 low and the March low, while yesterday’s bearish gap between 1651 and 1662 continues to serve as a significant resistance zone.

For buyers, the objective is straightforward: close the gap. A daily close above 1662 would represent the first meaningful indication that bullish momentum is returning.

Until that happens, any rebound should be viewed primarily as a retest of previous breakdown levels rather than confirmation of a fresh uptrend.

Palladium (PL.F)

We begin today by revisiting Tuesday’s observation:

“(…) Price has now fallen below the lower boundary of the June 12 bullish gap.

That is not a development buyers wanted to see.

Why?

Because a sustained break below that gap would place the previously discussed double-bottom formation under serious pressure.

(…) The market could soon shift its focus toward another leg lower. (…)”

From today’s perspective, palladium has largely followed that bearish scenario.

Tuesday’s close below the lower boundary of the June 12 gap triggered another bearish gap during yesterday’s Asian session between 1238 and 1243. That move pushed prices beneath the June 8 and June 10 lows, effectively invalidating the developing double-bottom pattern.

However, bears encountered an obstacle.

Price reached a support zone defined by the 88.6% Fibonacci retracement and a green support line drawn from previous lows — an area that has successfully contained selling pressure over the past two sessions.

As a result, today’s Asian session opened with a modest bullish gap between 1174.90 and 1182, giving bulls an opportunity to attempt a recovery move.

The key level to monitor now is 1201.

Why does it matter?

Because without a daily close above that threshold, today’s rebound should still be viewed as little more than a retest of yesterday’s breakdown.

Even if buyers manage to reclaim 1201, they would still face the overhead bearish gap, which continues to represent a major obstacle to any broader recovery attempt.

Similar to gold, silver, and platinum, some indicators are beginning to show bullish divergences. However, at this stage, those divergences should be treated as early warnings rather than confirmed reversal signals.

Today’s Key Takeaways

For the Dollar:

Keep an eye on the 101.39–101.59 resistance area

A break above 101.59 could pave the way toward the 101.74–101.81 zone

Bearish divergences are beginning to build and deserve attention

A daily close back below former channel resistance would raise the risk of a larger pullback

A move below 100.50–100.53 would strengthen the case for a deeper corrective decline

For Platinum:

Watch the 1651–1662 resistance range closely

A daily close above 1662 would provide the first meaningful bullish confirmation

As long as price remains below 1662, rallies should be treated cautiously and sellers maintain the upper hand

Bullish divergences are emerging, but confirmation is still lacking

The next major support area is located near 1542

For Palladium:

1201 remains the key resistance level

A daily close above 1201 would improve the near-term technical outlook

Failure to reclaim 1201 would keep the current rebound classified as a breakdown retest

Additional downside risk remains on the table until buyers provide stronger confirmation

Final Thoughts

This week continues to reinforce a lesson we’ve emphasized repeatedly in the Lab:

Technical clues are important — but confirmation is what truly matters.

Bullish divergences are beginning to appear across several precious metals markets. That development is worth monitoring, but until price action confirms those signals through breakouts and daily closes above critical resistance levels, they should be viewed as potential setups rather than actionable evidence.

And in trading, that distinction can make all the difference.

Stay disciplined, respect the technical levels, and allow confirmation — not anticipation — to guide the decision-making process.

U.S. benchmark crude oil prices dropped below $70 per barrel on Wednesday, hitting their lowest point since the conflict with Iran erupted on Feb. 28. The decline is expected to reduce pressure on headline inflation in the months ahead. However, the key issue now is whether the bond market will also adjust by pricing in lower inflation expectations, as uncertainty surrounding the Federal Reserve’s interest-rate path remains unresolved.

Oil prices were pressured by a preliminary agreement aimed at ending the conflict with Iran, while shipping activity through the Strait of Hormuz has started to recover gradually. Even so, energy transport volumes are still significantly below levels seen before the war. “What shippers are looking for is consistency over days and weeks,” said Matthew Wright, a freight analyst at Kpler, a firm specializing in global shipping analysis.

The oil market is currently reflecting expectations of continued progress toward stability and a gradual recovery in global energy exports over the coming weeks and months. “Traders are pricing in a return to normality,” said Francis Osborne, head of oil analysis at Argus Media, a firm that monitors global oil prices. “They are not taking into account the risks further down the road, which still remain very real.”

Despite ongoing uncertainty surrounding the Middle East, U.S. Treasury yields have started to retreat, though the decline has been uneven across maturities. The 30-year Treasury yield — typically the most sensitive to inflation expectations — dropped sharply yesterday to 4.84%, its lowest level in several months. Meanwhile, the benchmark 10-year yield also moved lower, reversing much of the increase seen over the past month.

One key exception is the policy-sensitive 2-year Treasury yield. Although it edged lower yesterday, it remained near 4.16%, close to the recent high reached only days earlier. This suggests that investors are not yet fully convinced that inflation pressures have disappeared or that further Federal Reserve rate hikes are off the table.

Torsten Slok argues that lower oil prices could ultimately become inflationary, writing:

“The narrative in markets is changing from ‘lower oil prices mean lower inflation’ to ‘lower oil prices mean more demand in an already overheating economy, which means higher inflation.’ Driven by the strong April CPI, hot May non-farm payrolls, and a hawkish Fed, the market narrative now suggests that the reopening of the Strait of Hormuz will further overheat the economy, forcing the Fed to raise interest rates soon.”

Whether Slok’s view proves correct will take time to assess, as geopolitical tensions and broader macroeconomic uncertainty continue to cloud the outlook. In the near term, however, inflation pressures are still expected to ease somewhat.

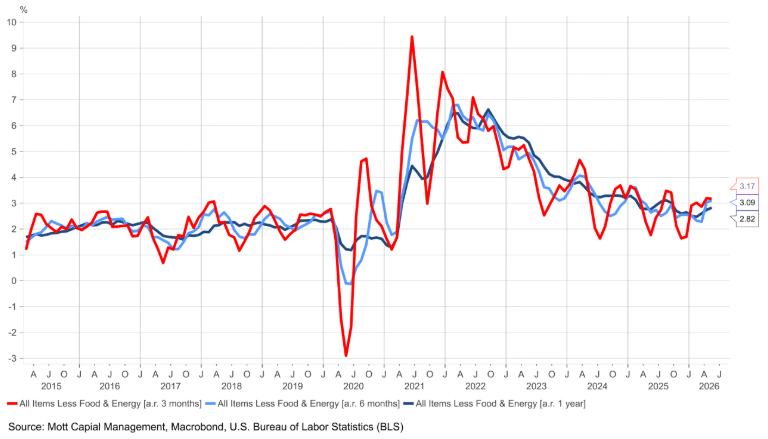

The Federal Reserve Bank of Cleveland’s inflation nowcast points to a modest slowdown in year-over-year CPI after several months of elevated readings. Meanwhile, Core CPI — which has remained relatively stable throughout the conflict, rising only slightly — is projected to increase 2.9% in the latest monthly update compared with a year earlier.

Fed funds futures markets are now assigning higher odds of near-term tightening, pricing in a 34% probability of a 25-basis-point rate hike at the next FOMC meeting on July 29, with expectations rising to around 67% in favor of further tightening by September.

Morningstar expects any near-term inflation persistence to gradually fade over time. The firm notes: “We expect inflation to fall in the coming years. Receding energy prices will be reflected in a negative impulse to inflation in 2027. The tariff impact should also cease going forward. Moreover, wage growth has slowed considerably, which should help push services inflation back to normal. Housing inflation also continues to trend down.”

Still, while the longer-term outlook points toward easing inflationary pressure, that horizon remains distant. In the immediate term, markets are taking comfort in signs of cooling prices, though uncertainty around the Federal Reserve’s policy path suggests that current stability may not last.

USD/CAD weakens as the oil-sensitive Canadian Dollar draws support from higher crude prices.

Oil prices advanced after an attack on a vessel near Oman disrupted UN evacuations through the Strait of Hormuz, reviving concerns over global energy supplies.

Meanwhile, the US Dollar could remain supported by rising expectations of a Federal Reserve rate hike, which continue to bolster demand for the Greenback.

USD/CAD extends its decline for a second straight session, hovering near 1.4200 during Friday’s Asian trading hours. The pair comes under pressure as the commodity-linked Canadian Dollar gains support from stronger crude oil prices. Canada, one of the world’s largest net oil exporters, relies heavily on petroleum exports as a key source of foreign exchange revenue.

Oil prices climbed after a suspected projectile strike on a cargo vessel near Oman forced the United Nations to suspend evacuation operations through the strategically important Strait of Hormuz, reigniting concerns over global energy supply disruptions.

Geopolitical tensions escalated further late Thursday after two US officials claimed Iranian forces had opened fire on the vessel while it was transiting the strait. Iranian authorities later warned that ships operating outside designated Hormuz routes could no longer be assured safe passage.

However, losses in USD/CAD may remain capped as the US Dollar continues to draw support from increasing expectations of another Federal Reserve rate hike. CME FedWatch data currently shows markets pricing in a 63.4% chance of a rate increase at the Fed’s September 15–16 meeting.

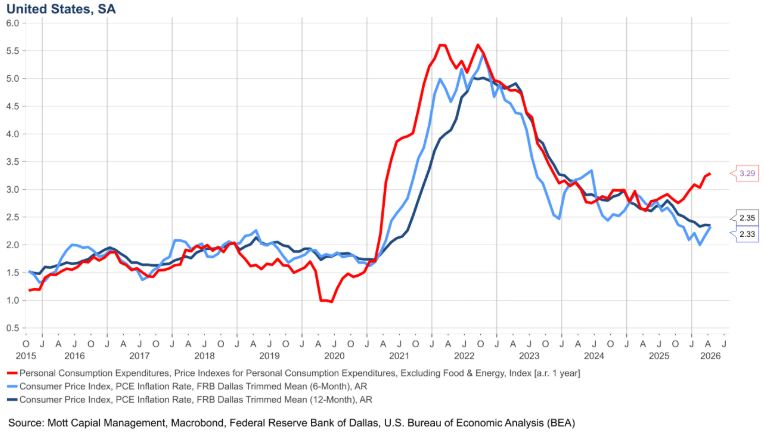

The hawkish outlook has been reinforced by stronger inflation readings. The headline Personal Consumption Expenditures (PCE) Price Index accelerated to 4.1% year-over-year in May from 3.3% previously, marking the first time in three years that the gauge has risen above 4.0%. The surge was largely driven by higher energy costs linked to Middle East tensions, keeping expectations for additional tightening alive.

Meanwhile, the Fed’s preferred inflation measure, the core PCE index, edged higher to 3.4% annually from 3.3%, its strongest pace since October 2023, underscoring persistent inflation pressures that continue to underpin the Greenback.

The United States Dollar Index remains supported as expectations for a Federal Reserve rate hike continue to build. Markets are now pricing in a 63.4% chance of a rate increase in September, according to the CME Group FedWatch tool. Meanwhile, US PCE inflation accelerated to 4.1% in May amid oil supply concerns linked to tensions in the Middle East, reinforcing expectations that the Fed could keep tightening policy.