Markets are increasingly betting that the conflict with Iran has come to an end. Yet even if that assumption holds, the economic repercussions are likely to persist for months—if not years.

While global attention tends to center on the immediate spectacle of war—airstrikes, blockades, and sanctions—the most disruptive consequences often emerge more slowly. In the Persian Gulf, the true impact is delayed, carried across the world through disrupted shipping routes and declining exports of oil, natural gas, and key agricultural inputs. Because of these lags, the global economy is only beginning to absorb the shock from reduced supply.

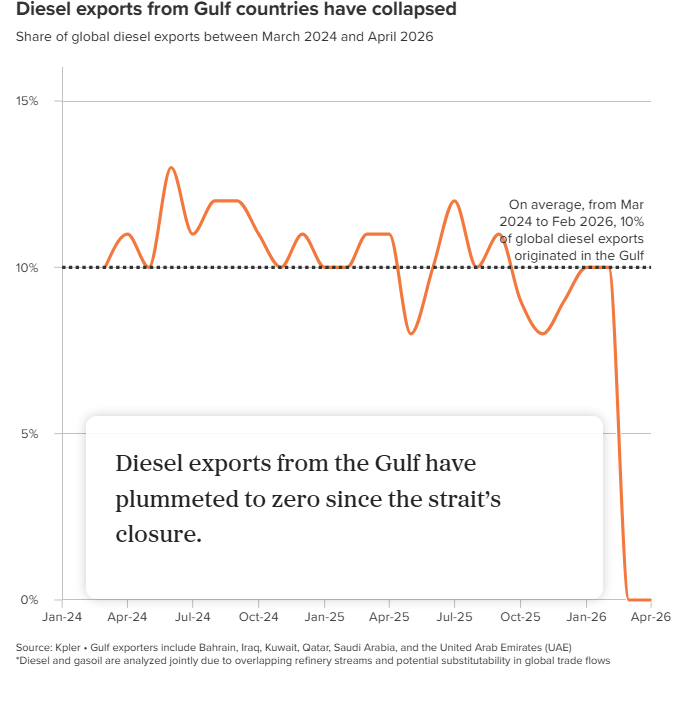

As Comfort Ero of the International Crisis Group observes, wars expose the fragile systems that quietly sustain everyday life. Strategic chokepoints like the Strait of Hormuz—normally overlooked—suddenly become critical when they falter.

Oil shipments from the Gulf typically take between 30 and 45 days to reach major markets. That delay means supply disruptions don’t show up immediately. Instead, countries draw down existing inventories while incoming supply gradually shrinks. By the time shortages become visible, the disruption has already been building for weeks.

Recent data underscores this dynamic. OPEC output plunged by 27% in March, signaling the first wave of global supply strain. Even under a sustained ceasefire, a rapid recovery appears unlikely. Industry leaders estimate it could take months for production in the region to return to normal levels.

At the same time, the easing of military tensions may create a false sense of stability. Beneath the surface, the economic damage continues to accumulate. Supply chain pressures are only now intensifying. Companies are beginning to feel the strain—illustrated by manufacturers halting orders due to shortages tied to disruptions in the energy supply chain.

The agricultural sector offers another clear example. With planting season nearing its end, rising fertilizer and fuel costs are forcing farmers to make difficult choices: cut back production or absorb significant financial losses. Many are already reporting deteriorating financial conditions.

Although limited shipping activity has resumed through the Strait of Hormuz, it remains uncertain how quickly normal export levels can be restored. Even if the passage reopens soon, the broader damage—to infrastructure, refining capacity, and logistics networks—will take far longer to repair, ensuring that the war’s economic aftershocks continue well into the future.

Oil isn’t the only export under threat. The Persian Gulf also supplies large volumes of natural gas liquids, ammonia, urea, and other petrochemical inputs that are vital to global fertilizer production. Prolonged disruptions to these flows could ripple through agricultural supply chains worldwide.

Even a short delay in shipments can trigger cascading effects—tightening fertilizer supplies, reducing crop yields, and driving up food prices months down the line.

In this sense, the war’s impact on oil and fertilizer inputs resembles a slow-building shockwave. For now, the global economy is cushioned by existing inventories and shipments made before the conflict. But as those buffers wear thin, declining exports from the Gulf are likely to place increasing strain on energy markets, food production, and overall economic stability.

The most significant consequences are not in the past—they are only starting to surface.

Leave a comment