Gold attracts renewed buying interest during Tuesday’s Asian session, although its upside remains limited. Persistent inflation concerns continue to reinforce expectations that the Federal Reserve will keep interest rates elevated, providing support for the US Dollar and reducing the appeal of the non-yielding precious metal. At the same time, lingering geopolitical tensions between the United States and Iran are underpinning demand for the greenback, prompting traders to remain cautious about chasing further gains in gold.

Gold (XAU/USD) extends its rebound during Tuesday’s European session, climbing to its highest level in four days around the $4,075 area as the US Dollar eases amid renewed hopes for diplomacy between Washington and Tehran.

The precious metal draws support after US Secretary of State Marco Rubio stated on Sunday that the United States remains willing to engage in negotiations with Iran despite the recent exchange of military strikes. The remarks have tempered demand for the US Dollar by encouraging optimism that the conflict could eventually be resolved through diplomatic channels.

However, Gold’s upside remains constrained as investors continue to price in the inflationary risks stemming from rising energy costs. Disruptions to oil shipments through the Strait of Hormuz, combined with Yemen’s Iran-backed Houthi movement announcing a maritime blockade targeting Saudi Arabia, have reinforced expectations of tighter global crude supplies. Higher oil prices could fuel inflation and strengthen the case for the Federal Reserve to maintain restrictive monetary policy for longer.

Market expectations continue to reflect that view. According to the CME FedWatch Tool, traders see roughly an 83% chance that the Fed will raise interest rates before the end of the year. The prospect of higher US borrowing costs supports the US Dollar and limits demand for non-yielding assets such as Gold.

Meanwhile, geopolitical tensions remain elevated despite the diplomatic signals. The United States has reportedly carried out a tenth consecutive night of strikes on Iranian targets, with the White House indicating that military operations will continue until President Donald Trump decides otherwise. Iran has responded with retaliatory attacks against US military facilities and allied infrastructure across the Gulf, keeping concerns over a broader regional conflict firmly in focus.

With geopolitical risks continuing to underpin the US Dollar’s safe-haven appeal and expectations for prolonged Fed tightening remaining intact, traders may prefer to wait for stronger confirmation before concluding that Gold has established a near-term bottom, particularly in the absence of major US economic data releases on Tuesday.

Gold H4 Chart

Gold continues to trade with a positive intraday tone after breaking above the 23.6% Fibonacci retracement of the decline from the July peak and pushing through a short-term descending trendline. This technical breakout strengthens the bullish outlook, while momentum indicators also show improving conditions. Both the Moving Average Convergence Divergence (MACD) and the Relative Strength Index (RSI) are pointing higher, indicating that selling pressure is gradually easing.

Even so, the broader near-term outlook remains cautious as long as XAU/USD stays below the 100-period Simple Moving Average (SMA) on the 4-hour chart and several key Fibonacci resistance levels. Any continued advance is therefore likely to encounter resistance first near the 38.2% Fibonacci retracement at $4,052.78, followed by the 100-period SMA at $4,067.29 and the 50.0% retracement at $4,081.40.

If bullish momentum extends beyond those levels, the 61.8% Fibonacci retracement at $4,110.01 could provide a more formidable resistance zone. On the downside, initial support is located around $4,017, where the 23.6% Fibonacci level aligns with the recently broken trendline. A stronger support base sits near $3,960.14, the key Fibonacci anchor, where buyers may step back in should the current pullback deepen.

Major currency pairs traded within familiar ranges early Tuesday as investors avoided making aggressive moves while monitoring developments in the Middle East. Attention now turns to Germany and the Eurozone’s ZEW Economic Sentiment surveys, while the US economic calendar remains light for the remainder of the day.

After Monday’s volatile session, crude oil prices eased modestly, with West Texas Intermediate (WTI) slipping around 0.5% to trade near $82 per barrel. Oil initially retreated after reports suggested mediators had proposed a 10-day ceasefire between the United States and Iran to revive diplomatic negotiations. However, hostilities continued to escalate.

US President Donald Trump warned that Iran would face consequences following the deaths of American service members, while US forces carried out strikes for a tenth consecutive day, targeting areas near Sirik, Bandar Abbas, Qeshm Island, Chabahar, and Konarak. Iran responded with attacks on US assets across the Gulf, keeping geopolitical tensions elevated.

Oil Supported by Ongoing Geopolitical Risks

Despite signs of diplomatic engagement, analysts remain cautious. Deutsche Bank noted that Iran acknowledged receiving proposals from international mediators, but escalating rhetoric from both Yemen’s Houthi movement and President Trump helped push Brent crude to settle 1.27% higher at $89.22 per barrel.

OCBC warned that any broader escalation could revive concerns over a prolonged disruption to global oil supplies, potentially lifting crude prices back above $100 per barrel. Such a scenario could increase market volatility, weaken demand for carry trades, and reinforce demand for the US Dollar as investors seek safe-haven assets.

Fed Faces Fresh Inflation Concerns

The US Dollar Index (DXY) extended Monday’s gains by more than 0.2%, although it traded sideways just below the 101.00 level during Tuesday’s European session.

According to Commerzbank’s Volkmar Baur, persistently high energy prices could make it increasingly difficult for the Federal Reserve to avoid raising interest rates. While policymakers typically focus on core inflation, sustained increases in oil prices risk feeding into broader inflation through second-round effects, complicating the Fed’s policy outlook.

Sterling Softens Despite Stable Labor Market

UK labor market data showed the ILO unemployment rate remained unchanged at 4.9% in the three months to May. Meanwhile, average earnings excluding bonuses increased 4.3% year-over-year, below expectations of 4.5%.

The softer wage growth limited Sterling’s recovery, although GBP/USD edged slightly higher to around 1.3450 after three consecutive daily declines. Investors now await Wednesday’s UK inflation report.

New Zealand Dollar Outperforms After Inflation Surprise

New Zealand’s second-quarter inflation accelerated more than expected, with the annual Consumer Price Index (CPI) rising to 4.1%, up from 3.1% in the previous quarter and exceeding forecasts of 4.0%.

The stronger inflation reading boosted expectations that the Reserve Bank of New Zealand could maintain a restrictive policy stance, lifting NZD/USD above 0.5850, its strongest level since early June.

Euro, Canadian Dollar and Yen Hold Steady

EUR/USD traded quietly around 1.1420 after posting modest losses on Monday.

USD/CAD remained above 1.4050 despite Canadian inflation slowing to 2.8% in June from 3.2% previously. The Canadian Dollar also faced pressure after the White House announced that President Trump would impose 50% tariffs on most Canadian imports, citing what Washington described as discriminatory treatment of US automobiles, alcohol, and dairy products.

Meanwhile, USD/JPY held near 162.50. Japanese Prime Minister Sanae Takaichi stated that the government would continue balancing economic support with fiscal sustainability while working to preserve market confidence.

Oil Still Matters: Ranking the World’s Top 10 Producers

Oil has been pronounced obsolete countless times, yet global consumption still exceeds 100 million barrels per day.

Beyond fueling airplanes, trucks, and cargo ships, petroleum serves as a key ingredient in plastics, fertilizers, chemicals, pharmaceuticals, and thousands of everyday products that consumers rarely connect to crude oil.

According to OPEC projections, worldwide oil demand is expected to rise to 113.3 million barrels per day by 2030 and 124.1 million by 2050, with non-OECD nations driving most of the increase. Despite the global push toward alternative energy, oil is set to remain a cornerstone of the world economy for decades.

Below is a ranking of the world’s 10 largest oil-producing nations based on the latest data from the U.S. Energy Information Administration (EIA), reflecting 2025 production levels.

10. Kuwait | 2.6 Million Barrels Per Day

Although Kuwait ranks last on this list, it remains one of the richest countries in terms of oil reserves. The nation holds an estimated 101.5 billion barrels of crude, enough to sustain current production levels for roughly 100 years, while also benefiting from some of the lowest extraction costs globally.

Production, however, has fallen below its traditional pace of around 3 million barrels per day. Through the state-owned Kuwait Petroleum Corporation, the oil sector remains the backbone of the economy, generating approximately 90% of government revenues and export earnings.

Kuwait highlights an important reality: possessing vast reserves is not the same as maximizing their economic value.

9. Brazil | 3.8 Million Barrels Per Day

Brazil has emerged as one of the most compelling offshore oil success stories in recent decades. Its massive pre-salt reserves, buried beneath deep Atlantic waters and thick salt formations, require advanced technology and significant capital investment to develop.

Those investments are yielding results. Petrobras recently reported record output of 1.1 million barrels per day from the Búzios field alone, which now accounts for roughly one-third of the company’s Brazilian production.

As production expands, Brazil has become a major crude exporter and continues to offer investors exposure to highly productive fields with substantial growth potential.

8. United Arab Emirates | 3.8 Million Barrels Per Day

The UAE matched Brazil’s output at roughly 3.8 million barrels per day in 2025 but entered 2026 with a more aggressive production strategy.

Following its departure from OPEC in May, the country boosted output to a record 4.1 million barrels per day by June, signaling a desire to prioritize national production goals over cartel quotas.

Serving key Asian markets such as China, India, and Japan, the UAE has also invested heavily in refining, storage, port infrastructure, and pipeline networks. In periods of supply disruption, especially around the Strait of Hormuz, that logistical flexibility becomes a major strategic advantage.

7. Iran | 4.1 Million Barrels Per Day

Iran’s energy sector has long been shaped by geopolitics. Despite holding the world’s fourth-largest proven oil reserves and second-largest natural gas reserves, sanctions, conflict, and limited foreign investment have prevented the country from reaching its full production potential.

Output once exceeded 6 million barrels per day during the 1970s. Today, much of Iran’s oil trade relies on Chinese demand and a complex network of intermediaries designed to navigate sanctions.

Iran remains a critical player because any disruption to its exports can have an outsized effect on oil prices, particularly when tensions threaten traffic through the Strait of Hormuz, one of the world’s most important energy chokepoints.

6. China | 4.3 Million Barrels Per Day

While China is widely recognized as the world’s largest crude importer, it is also a significant producer.

Driven by energy-security concerns, Beijing has encouraged state-owned producers to boost domestic output. As a result, production climbed from approximately 3.8 million barrels per day in 2020 to a record 4.3 million in 2025.

PetroChina remains the country’s largest producer, while offshore specialist CNOOC has delivered notable growth. Increased exploration spending and new discoveries have also expanded reserve estimates.

Even so, China still imported roughly 11.55 million barrels per day in 2025. Aging fields and rising development costs suggest domestic production may be approaching practical limits, leaving imports as a crucial component of the nation’s energy strategy.

5. Iraq | 4.4 Million Barrels Per Day

Iraq possesses around 145 billion barrels of proven reserves, ranking among the largest resource holders globally.

Its oil fields are both extensive and relatively inexpensive to operate, giving the country the potential to produce far more crude than current levels suggest.

The challenge lies in infrastructure and export reliability. Roughly 93% of Iraqi crude exports pass through terminals near Basra on the Persian Gulf. Any disruption in the Strait of Hormuz can quickly create bottlenecks, forcing storage facilities to fill and production to slow.

Despite enormous geological advantages, logistical constraints and political challenges continue to limit Iraq’s full potential.

4. Canada | 5 Million Barrels Per Day

Canada stands as the only non-U.S. nation in the top five located entirely within North America, a valuable advantage amid growing geopolitical uncertainty.

Most Canadian production comes from Alberta’s oil sands, where heavy bitumen is either mined or extracted using steam-assisted recovery techniques.

Although oil sands projects require substantial upfront investment, they offer exceptionally long production lives and relatively low decline rates compared with shale wells.

Canada set another production record in 2025, with crude and equivalent output averaging 5.35 million barrels per day under broader regulatory measurements. Alberta alone contributed nearly 84% of national production.

3. Saudi Arabia | 9.6 Million Barrels Per Day

Saudi Arabia remains the most influential nation in the global oil market despite no longer holding the top production spot.

Output rose to approximately 9.6 million barrels per day in 2025 as OPEC+ gradually relaxed voluntary supply cuts.

Saudi Aramco oversees more than 260 billion barrels of proven reserves and operates some of the largest and lowest-cost oil fields ever discovered. More importantly, Saudi Arabia maintains significant spare production capacity that can be activated relatively quickly.

While most producers pump at maximum capacity, Saudi Arabia often has the ability to increase or decrease output strategically, giving it extraordinary influence over global oil prices.

2. Russia | 9.9 Million Barrels Per Day

Despite sanctions, production restraints, and the ongoing conflict in Ukraine, Russia remained the world’s second-largest oil producer in 2025 with roughly 9.9 million barrels per day.

The country has successfully redirected much of its crude exports toward Asia, with China and India becoming its dominant buyers.

However, the long-term outlook is more uncertain. Mature fields require increasing investment, while sanctions continue to limit access to advanced Western technology and financing.

Russia remains an energy giant, but sustaining current production levels could become increasingly challenging over time.

1. United States | 13.6 Million Barrels Per Day

The United States did more than lead the rankings in 2025—it achieved the highest crude oil production ever recorded by any country.

U.S. crude and condensate output averaged a record 13.6 million barrels per day, roughly 40% higher than production from either Russia or Saudi Arabia. Monthly production reached an all-time high of 13.93 million barrels per day in April.

At the center of this achievement is the Permian Basin in Texas and New Mexico, which produced approximately 6.6 million barrels per day and accounted for nearly half of total U.S. output.

Technological advances in horizontal drilling and hydraulic fracturing, combined with private mineral ownership, deep capital markets, and a competitive oil-services industry, transformed the United States into a global energy powerhouse.

Today, the country is also a major exporter of crude oil, gasoline, diesel, and refined petroleum products, strengthening both its trade position and domestic economy.

Why Oil Still Matters

Across much of the world, oil production is dominated by governments and state-owned enterprises. In contrast, private investment and publicly traded companies play a far greater role in North America.

Understanding where global oil supplies originate—and the economics behind bringing those barrels to market—can help investors better navigate future commodity cycles. Despite rapid growth in renewable energy, oil remains one of the most important resources underpinning modern civilization and the global economy.

The global oil market is losing many of its key shock absorbers as inventories remain tight, shipments through the Strait of Hormuz face ongoing disruptions, and spare supply continues to shrink, increasing the likelihood of stronger oil prices.

One factor that has kept prices from climbing further is China’s sharp decline in crude oil imports. However, analysts believe that support may soon disappear, with the world’s largest oil importer expected to return to the market after drawing down its existing stockpiles.

Should disruptions in the Strait of Hormuz continue while Chinese buying accelerates, market analysts warn that global oil supplies could tighten considerably. The resulting imbalance between supply and demand may place the greatest upward pressure on crude prices in the latter part of the year.

The oil market could soon lose the key supply and demand buffers that have prevented crude prices from surging despite the massive disruption to shipments through the Strait of Hormuz.

A temporary U.S.-Iran memorandum of understanding had allowed Middle Eastern producers to accelerate exports of crude that had accumulated in Gulf storage over the previous four months. That opportunity has now effectively ended as hostilities resumed and the ceasefire collapsed.

At the same time, crude and refined fuel inventories across major consuming regions, including the United States, have fallen to critically low levels. Much of the oil released through the largest coordinated strategic stock drawdown in history has already reached refiners, leaving few reserves available to cushion further supply shocks.

Another important stabilizing factor may also be fading. China, whose reduced crude imports have helped moderate global demand in recent months, is expected to return to the market soon. If that happens, one of the largest forces restraining oil prices during the March-to-June period could disappear.

China’s Demand May Be Reawakening

China cut crude imports to their lowest level in a decade during June, extending three months of unusually weak buying as elevated prices and constrained Middle Eastern supplies discouraged purchases. Compared with its 2025 average, imports are estimated to have declined by roughly 4.4 million barrels per day.

Official customs figures showed June crude imports totaled 29.27 million metric tons, or about 7.12 million barrels per day—down 41.3% from the same month a year earlier and marking the weakest monthly import level since October 2016.

The country’s large commercial and strategic reserves, accumulated before the conflict with Iran intensified, allowed Beijing to sharply reduce imports while still meeting domestic demand. Those stockpiles have acted as a major buffer for the global market, helping prevent prices from soaring despite the disruption of more than 10 million barrels per day of oil flows through the Strait of Hormuz.

As the world’s largest crude importer, China entered the supply crisis better prepared than any other major consumer. Analysts estimate it built reserves of between 1.2 billion and 1.3 billion barrels before the conflict began, although the true size of those inventories remains uncertain because official data are limited.

Recent estimates suggest China began drawing on those reserves in May and continued doing so through June. According to the International Energy Agency (IEA), inventories declined by roughly 41 million barrels last month.

While Goldman Sachs believes China still holds ample reserves and faces no immediate pressure to increase purchases, analysts expect the turning point may be approaching. Lower official selling prices from Gulf producers for July and August could encourage Chinese refiners to step up imports in the coming months.

Since the Middle East conflict escalated in February, China’s restrained buying has effectively acted as the global oil market’s swing demand factor. If imports recover, that important demand buffer could disappear.

Shrinking Inventories Raise Risks

A rebound in Chinese demand could coincide with continuing uncertainty surrounding the Strait of Hormuz, where shipping activity remains well below the pace seen during the brief period following the U.S.-Iran agreement.

Any renewed disruption to tanker traffic would further delay the recovery of Middle Eastern exports and tighten global supplies of both crude oil and refined fuels.

According to Energy Aspects founder Amrita Sen, slower vessel movements through the Strait, combined with renewed U.S. restrictions on Iranian oil exports and rapidly declining inventories, are laying the groundwork for higher oil prices if current conditions persist.

Sen estimates that global oil inventories have fallen by roughly 600–700 million barrels since the crisis began. She warned that if the current situation extends into the end of this month or early next month, the market may face its greatest pressure later in the third quarter or early in the fourth quarter.

Speaking separately to the Financial Times, Sen said that nearly all excess commercial inventories have now been exhausted, leaving only government-held strategic reserves as a meaningful emergency backstop. As a result, confidence that oil flows through the Strait of Hormuz will remain uninterrupted is increasingly being tested.

GBP/USD slips toward 1.3470 during Friday’s Asian session.

The US carried out a sixth consecutive day of strikes against Iran, fueling geopolitical tensions.

Markets continue to increase expectations for additional Bank of England rate hikes this year.

The GBP/USD pair remains under modest pressure, slipping to around 1.3470 during Friday’s Asian session as heightened geopolitical tensions in the Middle East dampen investor risk appetite and lend support to the US Dollar. Market participants are also awaiting the preliminary University of Michigan Consumer Sentiment Index for July, due later in the day.

Risk aversion intensified after the United States launched a sixth consecutive day of military strikes against Iran. Authorities in Bandar Abbas reported damage to civilian infrastructure, including electricity facilities and a railway station, adding to concerns over a widening regional conflict.

The US Central Command (CENTCOM) stated that the latest operations were aimed at further weakening Iran’s military capabilities and confirmed that naval forces had boarded a vessel as part of efforts to enforce the blockade around the strategic waterway. Earlier this week, President Donald Trump warned that Iranian bridges and power infrastructure could become targets unless Tehran returned to negotiations. The escalating conflict has increased demand for traditional safe-haven assets, providing additional support for the US Dollar against Sterling.

Meanwhile, recent US inflation figures have offered mixed signals. Consumer price inflation eased in June, while producer prices also declined, reinforcing expectations that inflationary pressures are moderating. Even so, traders continue to assign roughly a 55% probability to a Federal Reserve interest rate hike in September, according to the CME FedWatch Tool.

In the UK, Bank of England Governor Andrew Bailey acknowledged concerns over the renewed hostilities between the US and Iran but said the conflict has not materially altered the country’s inflation outlook. Markets continue to expect the BoE to raise interest rates at its November meeting, with another increase largely priced in by April 2027, according to Reuters.

WTI edges higher during the Asian session, although buying interest remains limited. Escalating tensions between the US and Iran continue to underpin geopolitical risk premiums, while fears of supply disruptions across key shipping routes lend further support to crude prices.

West Texas Intermediate (WTI), the US benchmark for crude oil, trades modestly higher during Friday’s Asian session but continues to move within a well-established multi-day trading range. The commodity is hovering near $79.35, up roughly 0.5% on the day and close to Tuesday’s one-month peak, leaving it on course for a second consecutive weekly gain as investors remain focused on the possibility of further escalation between the United States and Iran.

Market sentiment remains supported after the US military conducted a sixth straight night of airstrikes against Iran on Thursday, including a strike on an empty oil tanker bound for Kharg Island as part of its renewed naval blockade of Iranian ports. In response, Iran launched attacks on US military positions across the region, intensifying concerns that the conflict could evolve into a broader confrontation. These developments have kept geopolitical risk premiums elevated and continue to provide underlying support for crude prices.

Additional concerns emerged after authorities in Bandar Abbas reported damage to civilian infrastructure, including electricity facilities and a railway station. Iran’s Islamic Revolutionary Guard Corps has also warned of expanding military operations by targeting more regional energy transport routes. Adding to supply concerns, Reuters reported that Tehran has instructed Yemen’s Houthi movement to prepare for the possible closure of the Red Sea oil corridor, creating another potential threat to global energy flows.

At the same time, declining shipping activity through the Strait of Hormuz has reinforced fears of tighter oil supplies, strengthening the case for further upside in crude prices. Even so, traders may prefer to wait for a decisive breakout above the current consolidation range before committing to fresh bullish positions. Nevertheless, the broader fundamental backdrop continues to favor buyers, suggesting that any near-term pullback is likely to attract renewed demand and remain relatively limited.

Gold prices fell to around $3,995 during Tuesday’s early Asian trading session.

The decline followed President Trump’s decision to reinstate the Iran port blockade and his pledge to impose a 20% levy on cargo transiting the Strait of Hormuz.

Investors are now awaiting the release of the US June Consumer Price Index (CPI), which is expected to be the key market catalyst later on Tuesday.

Gold prices (XAU/USD) continued to trade under pressure, hovering around $3,995 during Tuesday’s early Asian session. The precious metal remained on the defensive as escalating tensions between the United States and Iran reinforced concerns over persistent inflation. Investors are now focused on the release of the US June Consumer Price Index (CPI) and testimony from Federal Reserve Chair Kevin Warsh, both scheduled for later on Tuesday.

According to Bloomberg, US President Donald Trump reinstated the blockade on Iranian vessels passing through the Strait of Hormuz and announced a 20% fee on all other cargo transiting the strategic waterway. Trump also pledged to intensify military action against Iran, stating that the US would continue launching heavy strikes over the coming days.

The renewed blockade raises the risk of retaliation from Tehran, potentially increasing attacks on commercial shipping in the Strait of Hormuz. Such disruptions could fuel higher energy prices, adding to inflationary pressures and reinforcing expectations that the Federal Reserve will keep interest rates elevated for longer. Although gold typically benefits from heightened geopolitical uncertainty, its appeal is often limited in a high-interest-rate environment because it does not generate yield.

Market participants are also awaiting the latest US inflation figures for further policy clues. Economists expect the headline CPI to decline 0.1% month-over-month in June, while core CPI is forecast to increase 0.3% over the same period. If inflation comes in below expectations, the US Dollar could weaken, providing short-term support for dollar-denominated gold prices.

Gold extends its losses, falling more than 1% toward the $4,050 level during Monday’s Asian session as escalating tensions between the United States and Iran boost demand for the safe-haven US Dollar. At the same time, concerns that higher Crude Oil prices could fuel inflation are reinforcing expectations of a Federal Reserve rate hike in 2026, strengthening the Greenback further and adding pressure on the non-yielding precious metal.

Fundamental Analysis

Gold remains under heavy selling pressure at the beginning of the week as the US Dollar strengthens, supported by a sharp rebound in Oil prices and renewed inflation concerns that reinforce expectations of a hawkish stance from the Federal Reserve.

The move follows a fresh escalation of tensions in the Middle East after the United States launched additional strikes against Iran on Sunday. In response, Iran reportedly targeted US facilities across Gulf states and reiterated the closure of the strategically important Strait of Hormuz.

Rising inflation worries have also contributed to Gold’s weakness after the Fed highlighted increasing price pressures in its semi-annual Monetary Policy Report released on Friday. The central bank noted that inflation accelerated further this spring, driven by the combined effects of tariffs, higher energy costs linked to the conflict, and continued investment in artificial intelligence infrastructure.

Market participants remain cautious ahead of Tuesday’s release of the US Consumer Price Index (CPI) report and Federal Reserve Chair Kevin Warsh’s first semi-annual testimony before Congress.

For now, traders are expected to keep a close eye on developments surrounding the US-Iran conflict and fluctuations in Oil prices for fresh market direction. From a technical perspective, the bearish outlook for Gold remains intact, with downside risks continuing to dominate the near-term picture.

Technical Analysis

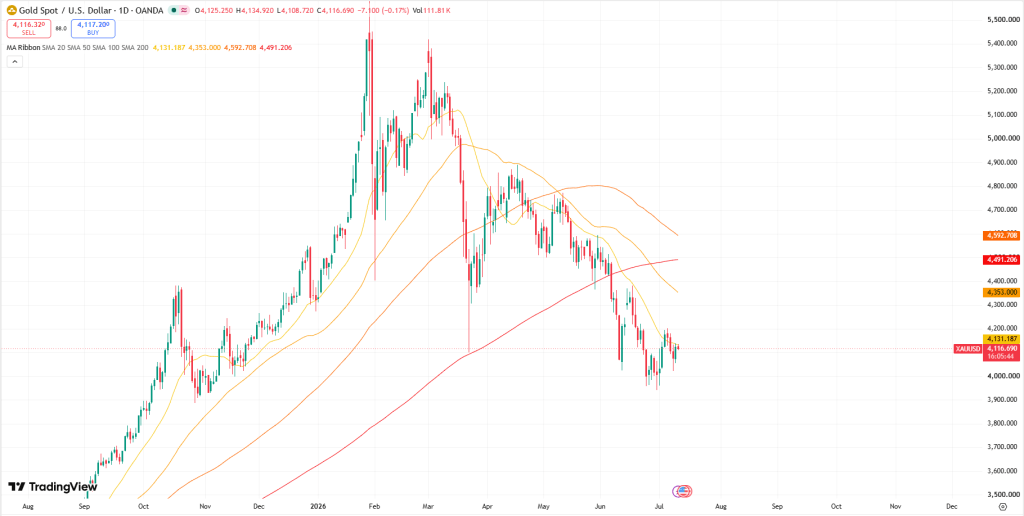

On the daily timeframe, Gold (XAU/USD) is trading near $4,069, maintaining a bearish short-term bias as it remains below both the 21-day SMA at $4,128 and the 50-day SMA at $4,344. The longer-term technical outlook also continues to favor sellers, with the 200-day SMA at $4,495 and the 100-day SMA at $4,583 positioned well above current market levels. Meanwhile, the RSI near 41 suggests bearish momentum is still present, although selling pressure appears to be moderating rather than reaching oversold territory.

On the upside, the first resistance zone is located around the 21-day SMA at $4,128. A sustained move higher could then target the 50-day SMA near $4,344, followed by the 200-day SMA around $4,495 and the 100-day SMA near $4,583. With no significant moving-average support levels immediately beneath the current price, any rebound attempt remains fragile while Gold continues to trade below this cluster of resistance levels. Unless buyers can regain control above the 21-day SMA, the broader risk profile remains tilted toward further downside pressure.

Escalating tensions between the US and Iran drove oil prices higher, reigniting inflation worries and dampening investor sentiment.

A stronger US Dollar continues to weigh on EUR/USD, with geopolitical uncertainty taking precedence over economic fundamentals.

Investors are looking ahead to the Fed minutes for policy clues, although developments in the Middle East remain the primary catalyst for market direction.

After a turbulent first half of the year marked by the US-Israel conflict with Iran and President Trump’s frequent policy reversals, investors were hoping for a quieter period as the summer holiday season approached. Instead, geopolitical tensions appear to be resurfacing.

Oil prices have climbed sharply over the past few sessions, recovering to levels last seen before the conflict. While Trump may later attempt to ease market concerns with softer rhetoric, the immediate reaction has been a renewed focus on geopolitical risks.

My view is that Trump is unlikely to favor a major escalation, which could limit the magnitude of any oil rally compared with the dramatic price swings witnessed during the peak of the conflict earlier this year. However, his recent remarks have undeniably heightened concerns over potential supply disruptions from Iran and the broader Middle East. In particular, markets are once again watching the possibility of Tehran restricting traffic through the Strait of Hormuz, a critical global energy chokepoint.

The coming days should provide greater clarity on how the situation develops, but for now, there is a growing risk that markets could find themselves facing a familiar geopolitical backdrop once again.

Fed Minutes Likely to Take a Back Seat as Geopolitical Risks Return

Markets initially appeared to shrug off the renewed tensions between the US and Iran earlier this week, but sentiment has shifted noticeably. As geopolitical concerns intensify, investors are likely to pay less attention to incoming macroeconomic data. While the minutes from the Federal Reserve’s June meeting are due later today and are expected to reaffirm a hawkish policy stance, supporting the US Dollar, the market’s primary focus has returned to oil prices and their implications for inflation and interest-rate expectations.

Investor sentiment deteriorated after President Trump’s remarks at the NATO summit unsettled financial markets, prompting a broad risk-off move that weighed on European equities and US stock futures. Addressing reporters, Trump stated that the memorandum of understanding with Iran was no longer valid and referred to Iranian leaders in highly critical terms, signaling a tougher stance toward Tehran.

The change in rhetoric has significantly reduced hopes for renewed diplomatic engagement. Only a few days ago, expectations were growing that both Washington and Tehran would maintain restraint ahead of another round of negotiations. Instead, concerns over renewed confrontation have resurfaced, placing geopolitical risks back at the forefront of market attention.

Euro Lacks Clear Catalysts Amid Mixed Fundamental Signals

The euro continues to face a challenging outlook as conflicting economic and geopolitical factors shape market sentiment. On the positive side, Germany’s industrial production data surprised to the upside, with output increasing by 0.9% in May, supported by stronger activity in the automotive and construction sectors.

The data suggests that Europe’s industrial economy has remained relatively resilient despite recent geopolitical uncertainty. However, the renewed escalation of tensions in the Middle East threatens to push energy costs higher once again, potentially weighing on economic growth across the region. At the same time, investors remain divided over the European Central Bank’s policy path, with expectations for a September rate hike no longer representing the market’s base-case scenario.

Nevertheless, ECB policymakers are unlikely to signal an end to the inflation fight while geopolitical risks remain elevated. Underlying price pressures continue to run above desired levels, prompting officials to maintain a cautious and data-dependent stance. Comments from senior ECB members this week may reinforce that message, providing intermittent support for the euro. Even so, such support could prove limited as the US Dollar continues to benefit from safe-haven demand and expectations that US interest rates will remain elevated for longer.

EUR/USD Technical Analysis

From a technical standpoint, EUR/USD remains trapped in a consolidation phase, although the near-term bias appears to favor the downside. The pair is currently hovering around the key 1.1400 support zone. A sustained break below this level could open the door for a deeper pullback toward the 1.1300 region.

On the upside, resistance is initially seen near 1.1450. If buyers manage to push the pair above this barrier, attention would shift to the psychological 1.1500 level, followed by the next major resistance around 1.1575.

At present, a stronger bullish move in EUR/USD would likely require a meaningful change in expectations surrounding Federal Reserve policy or a notable weakening in US economic conditions. With neither scenario appearing likely in the near term, investors continue to favor the US Dollar, supported by its yield advantage and renewed geopolitical concerns stemming from rising US-Iran tensions, which have also helped sustain higher oil prices.

WTI is trading within a narrow range as investors remain cautious amid conflicting signals from the US and Iran.

Ongoing exchanges of fire between the US and Iran continue to fuel geopolitical concerns, providing underlying support for crude oil prices.

However, market anxiety has eased after US President Donald Trump stated that Iran is willing to negotiate a deal, limiting further gains in WTI.

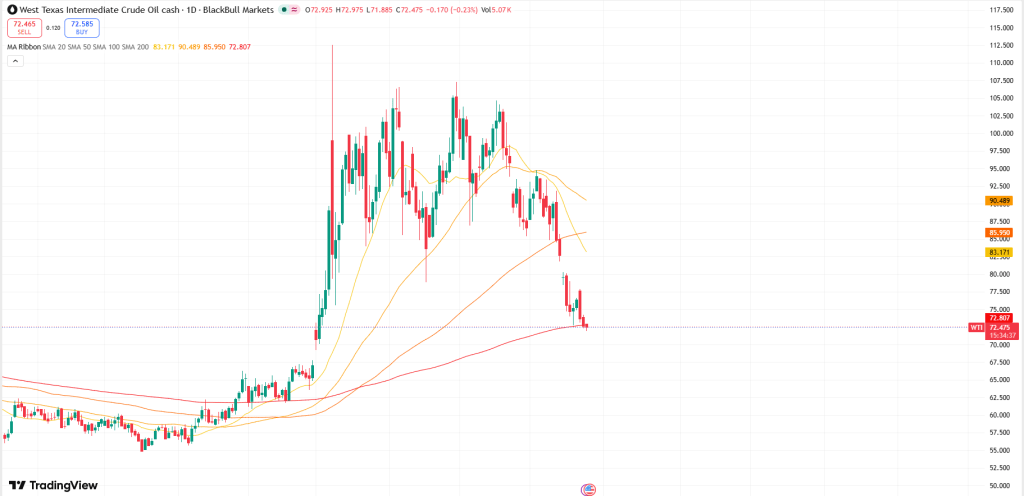

West Texas Intermediate (WTI), the US benchmark for crude oil, remains stable during Friday’s Asian trading session after recovering from the previous day’s decline. Mixed signals from Washington and Tehran have encouraged traders to stay on the sidelines, with prices hovering near $71.75 and showing little change on the day as markets await fresh developments in the Middle East.

Geopolitical concerns returned to the forefront this week after the US launched a new round of military strikes against Iran in response to attacks on commercial vessels transiting the Strait of Hormuz. Tehran retaliated by targeting regional US allies and striking American military facilities in Bahrain and Kuwait. Adding to the tensions, US President Donald Trump announced on Wednesday that the ceasefire was effectively over, helping drive crude prices higher earlier in the week.

However, sentiment improved on Thursday after Trump stated that Iran had reached out seeking negotiations to prevent further escalation. A White House official also reaffirmed Washington’s commitment to the existing memorandum of understanding with Tehran. These developments, combined with OPEC+’s decision to raise production targets once again, may limit upside momentum in oil prices and prompt traders to remain cautious about initiating new bullish positions.

Meanwhile, the latest report from the US Energy Information Administration (EIA) showed an unexpected increase in crude inventories for the week ending July 3, marking the first stockpile build in eleven weeks. Commercial crude inventories climbed by 2.998 million barrels, well above market expectations. The larger-than-forecast increase could continue to weigh on prices, although WTI remains on track to post a modest weekly gain and potentially end a four-week losing streak.

Gold prices edge higher toward the $4,120 mark during Friday’s early Asian trading session. The precious metal finds support after US officials indicated that Washington remains committed to its memorandum of understanding (MOU) with Iran, despite President Trump’s statement that the agreement is “over.” However, expectations that the Federal Reserve will maintain a hawkish policy stance could limit further gains in Gold.

Gold prices rebounded to around $4,120 during Friday’s early Asian session as investors assessed the risk of renewed conflict in the Middle East. Demand for the safe-haven metal strengthened amid persistent geopolitical uncertainty surrounding the US-Iran situation.

The White House indicated that it remains committed to the memorandum of understanding (MOU) with Iran, despite President Donald Trump’s recent statement that the framework agreement aimed at ending the conflict was “over” following Iranian attacks on vessels in the Strait of Hormuz and neighboring countries.

Nevertheless, tensions remain elevated. Trump warned that military action would intensify if Iran launched further attacks on shipping in the strait. On Thursday, Iran reportedly targeted US military bases in Bahrain, Kuwait, and Qatar, while Jordan intercepted eight missiles fired by Tehran, according to Axios.

Rising hostilities between the US and Iran have fueled concerns over potential disruptions to global oil supplies. Higher crude oil prices could increase inflationary pressures, potentially prompting the Federal Reserve to keep interest rates elevated for a longer period, which may limit Gold’s upside.

Meanwhile, minutes from the Fed’s June policy meeting—the first chaired by Kevin Warsh—revealed significant disagreement among policymakers regarding the future path of interest rates. While many officials suggested that the federal funds rate could end the year within or slightly below its current range, others argued that rates may need to remain above current levels, reflecting continued uncertainty over the inflation outlook.

WTI crude extends its advance as renewed geopolitical tensions in the Strait of Hormuz raise concerns over potential supply disruptions. Iran reportedly launched at least two missiles at commercial vessels passing through the key maritime chokepoint on Monday, bolstering risk premiums in the oil market. However, gains may be tempered after Saudi Aramco reduced the price of its Arab Light crude for Asian customers by $11, bringing it to a $1.50 discount to the regional benchmark.

West Texas Intermediate (WTI) crude oil edged higher to around $69.20 per barrel during Tuesday’s Asian session, recovering part of the previous day’s decline as renewed tensions in the Strait of Hormuz provided short-term support to prices.

Market sentiment improved after a Bloomberg report, citing a US official, indicated that Iran launched at least two missiles at commercial vessels navigating the crucial shipping corridor late Monday. Although two ships suffered significant damage, no fatalities were reported. Meanwhile, the UK Maritime Trade Operations (UKMTO) said a southbound tanker was hit by an unidentified projectile on its port side, triggering a fire onboard.

However, the upside in crude prices remained limited, with WTI hovering near a four-month low amid growing signs of ample global supply. Easing some immediate concerns over disruptions, maritime traffic through the Strait of Hormuz has begun to normalize. Data showed that at least eight Japan-linked vessels, including five supertankers capable of carrying roughly two million barrels of crude each, successfully transited the waterway via routes close to Iran.

Further weighing on the market, Saudi Aramco slashed the official selling price of its benchmark Arab Light crude for Asian customers by $11 per barrel, leaving it at a $1.50 discount to the regional benchmark. The rare and aggressive price cut—previously seen only during the oil market downturns of 2015 and 2020—underscores weakening demand conditions. The move came shortly after OPEC+ agreed over the weekend to increase production quotas for next month, reinforcing expectations of a more oversupplied global oil market and limiting the scope for sustained gains in WTI.

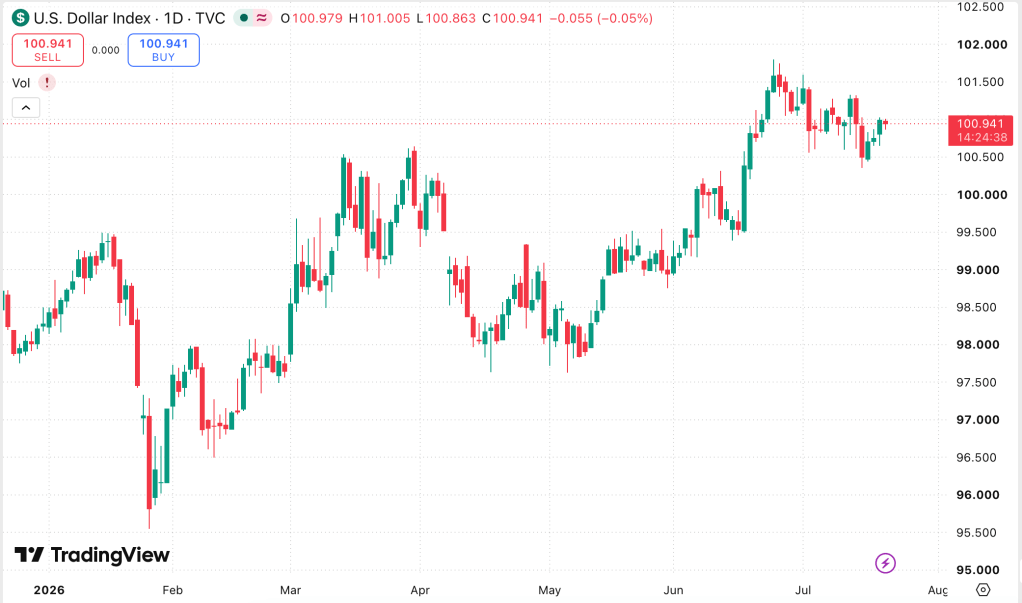

The U.S. Dollar Index remains below 101.00 as easing expectations of Fed rate hikes offset concerns over Hormuz-related risks.

The U.S. Dollar Index (DXY) continues to trade sideways on Tuesday, lacking sufficient momentum to break out of its recent range.

Fresh tensions in the Strait of Hormuz provide support for the safe-haven U.S. dollar, helping limit downside pressure.

However, fading expectations of additional Federal Reserve rate hikes keep bullish sentiment in check and restrict further gains in the greenback.

The U.S. Dollar Index (DXY) remained range-bound below 101.00 on Tuesday, extending its consolidation for a third consecutive session as geopolitical risks and monetary policy expectations pulled the dollar in opposite directions.

Renewed tensions between the U.S. and Iran, particularly in the strategically vital Strait of Hormuz, provided support for the safe-haven greenback. Reports of an oil tanker being struck in the waterway and Iran’s efforts to strengthen its control over the strait have raised concerns over the durability of the 60-day ceasefire agreement. The resulting uptick in crude oil prices has revived inflation worries, lending additional support to the U.S. dollar.

However, upside momentum remains limited as expectations for further Federal Reserve tightening continue to fade. Following June’s softer-than-expected Nonfarm Payrolls report, markets scaled back their outlook for Fed rate increases in 2026 from two hikes to between zero and one, reducing support for the dollar.

Adding to the cautious tone, the U.S. ISM Services PMI eased to 54.0 in June from 54.5 previously, meeting forecasts but offering little incentive for fresh USD buying. As a result, traders remain hesitant to extend the dollar’s rebound from the 97.40–97.45 support zone seen earlier this year.

Attention now turns to Wednesday’s FOMC Minutes, which could provide clearer guidance on the Fed’s policy outlook and determine the DXY’s next directional move.

US Dollar: Investor positioning continues to provide solid support into year-end – NBC

According to analysts Stéfane Marion and Kyle Dahms of National Bank of Canada, the US Dollar remains near its 2026 peak, supported by persistent inflation in the United States and a widening interest-rate advantage over other major economies. While these factors are likely to keep the greenback well supported in the near term, the analysts are increasingly cautious about the sustainability of the rally beyond the third quarter.

The dollar has strengthened against all major currencies over the past month as markets reassessed the outlook for US interest rates, reinforcing the currency’s yield advantage. However, NBC argues that expectations for imminent Federal Reserve tightening may be overdone.

June’s labor-market data painted a softer picture than headline sentiment suggests. Nonfarm payrolls increased by just 57,000, missing market expectations, while previous months’ figures were revised lower by a combined 74,000 jobs. Meanwhile, the household survey showed a decline of 507,000 employed workers and a notable drop in full-time employment, pointing to underlying weakness in the labor market.

NBC notes that speculative positioning has become increasingly skewed toward a stronger dollar, indicating that much of the bullish narrative may already be priced in. As a result, the USD could become more vulnerable to weaker inflation readings, further signs of labor-market cooling, or any scaling back of expectations for future Fed rate hikes.

The bank therefore expects the US Dollar to remain supported in the short term, but warns that slowing job growth and crowded market positioning make it difficult to justify extending the recent rally far beyond Q3. This view aligns with the gap between the Federal Reserve’s projections and private-sector forecasts: while roughly half of FOMC members still anticipate higher rates this year, only a small minority of economists expect additional tightening. NBC shares that skepticism, arguing that although inflation remains elevated enough to discourage rate cuts, labor-market conditions are soft enough to allow policymakers to remain patient before considering further hikes.

NBC’s broad USD index forecast reflects this outlook, with the index expected to gradually ease from 120.8 currently to 115.9 by Q2 2027, signaling a moderation rather than a reversal of dollar strength.

Gold buyers have become more cautious as concerns surrounding the Strait of Hormuz boost safe-haven demand for the US dollar. However, expectations that the Federal Reserve is unlikely to resume rate hikes limit the dollar’s upside, helping to underpin gold prices. In addition, the technical outlook remains constructive, suggesting that any pullback could attract fresh buying interest and keep the broader bullish trend intact.

Gold (XAU/USD) came under renewed selling pressure after climbing above the $4,200 level during the Asian session, reaching its highest point in two weeks. The decline appears to interrupt a three-day rally as investors shift toward the US dollar, which is benefiting from safe-haven demand amid ongoing tensions surrounding the Strait of Hormuz. Nevertheless, expectations that the Federal Reserve is unlikely to raise interest rates further continue to limit the dollar’s upside potential. At the same time, sustained purchases by central banks are providing underlying support for the precious metal.

Although the interim agreement between the United States and Iran remains in place, concerns over the Strait of Hormuz continue to linger. Iran has indicated plans to impose new service charges on vessels transiting the strategically important waterway, a proposal opposed by Washington. These developments have kept geopolitical risks elevated, boosting demand for the US dollar and weighing on gold prices at the start of the week.

On the monetary policy front, market participants have scaled back expectations for additional Fed rate hikes following weaker-than-expected US employment data released last Thursday, which pointed to a moderation in labor market strength. Furthermore, lower inflationary pressures resulting from the recent decline in crude oil prices could give the Fed more flexibility to maintain a patient policy stance. As a result, expectations for prolonged restrictive monetary policy have eased, limiting further gains in the US dollar and helping to cushion gold from deeper losses.

Support for gold also continues to come from central bank demand. A recent survey by the World Gold Council showed that central banks increasingly view gold as a safeguard against financial instability, inflation, and geopolitical uncertainty, with nearly 90% of respondents expecting global gold reserves to grow over the coming year. In addition, data from the European Central Bank revealed that gold has surpassed US Treasury holdings in global reserve allocations. China’s central bank further reinforced this trend by adding 320,000 ounces of gold to its reserves in May, marking the nineteenth consecutive month of accumulation.

Looking ahead, investors will closely monitor the release of the US ISM Services PMI and comments from key Federal Open Market Committee officials. These events could influence demand for the US dollar and provide fresh direction for gold prices. However, the broader fundamental backdrop remains supportive of the precious metal, suggesting that any near-term pullbacks are likely to attract buyers and that the overall bullish outlook remains intact.

Gold H4 Chart

Gold remains close to an important technical support zone around $4,150–$4,145, where the 100-period Simple Moving Average (SMA) on the four-hour chart is currently located. The bullish breakout above this moving average on Friday, followed by a move beyond the 23.6% Fibonacci retracement of the April–June decline, provided a strong signal that buyers were regaining control of the market.

Momentum indicators continue to support a constructive outlook. The Relative Strength Index (RSI) remains elevated near 63, while the Moving Average Convergence Divergence (MACD) stays in positive territory, suggesting that the broader upward momentum remains intact despite the recent period of consolidation below the latest highs.

As a result, any decline below the 23.6% Fibonacci retracement level at approximately $4,164 is likely to attract buying interest around the 100-period SMA near $4,147. This area should serve as an important support floor. However, a decisive break beneath this zone could open the door for a deeper correction toward the major support region around $3,940.

On the upside, immediate resistance is located near the 38.2% Fibonacci retracement level at $4,302. A sustained move above this barrier could target the 50% retracement level around $4,415, followed by the 61.8% retracement near $4,527. Beyond that, the 78.6% Fibonacci level at approximately $4,686 marks the next major bullish objective, ahead of a potential retest of the April peak around $4,889.

Energy – Brent Forward Curve Signals Improving Supply Conditions

The oil market is heading for a fourth straight weekly decline as traffic through the Strait of Hormuz continues to recover. Rising crude flows are placing increasing pressure on the front end of the ICE Brent forward curve, which has been shifting deeper into contango—a market structure often associated with ample near-term supply. The return of disrupted barrels, combined with ongoing releases from strategic petroleum reserves, has improved supply availability. However, lower outright prices and a contango market structure may begin attracting additional buying interest.

In the ARA hub, data from Insight Global showed total refined product inventories declined by 22,000 tonnes week-on-week to 4.53 million tonnes. The decrease was mainly driven by lighter products, with gasoline and naphtha stocks dropping by 75,000 tonnes and 26,000 tonnes, respectively. Meanwhile, middle distillates posted gains, as jet fuel inventories increased by 66,000 tonnes and gasoil stocks rose by 16,000 tonnes.

Singapore’s refined product inventories also moved lower, falling by 1.73 million barrels to 40.45 million barrels. Although stock levels remain below the five-year average of 45.32 million barrels, they have recovered significantly from early-June lows of 34.41 million barrels. Declines were recorded across all major categories, with light products, middle distillates, and residual fuels decreasing by 665,000 barrels, 420,000 barrels, and 648,000 barrels, respectively.

In the natural gas market, front-month Henry Hub futures came under pressure after U.S. storage data showed a larger-than-expected build. Gas inventories increased by 87 billion cubic feet last week, surpassing both market expectations of 84 bcf and the five-year average increase of 64 bcf. Nevertheless, persistent heatwaves across parts of the United States are expected to support gas demand for electricity generation as cooling requirements remain elevated.

Metals – Aluminium Retreats as Supply Concerns Ease

LME aluminium prices weakened again, with three-month contracts slipping toward $3,000 per tonne as traders continued to remove the geopolitical risk premium that had accumulated during the Middle East conflict.

Market sentiment was dampened by an update from Emirates Global Aluminium (EGA), which announced that approximately 7% of production pots at its Al Taweelah smelter have been restarted. The progress highlights a gradual recovery in output following missile and drone attacks that disrupted operations earlier this year.

The development strengthened expectations that supply interruptions in the Gulf region will be temporary. Earlier fears of production losses and shipping disruptions through the Strait of Hormuz had fueled a strong rally in aluminium prices. However, improving production levels and easing geopolitical tensions have significantly enhanced the supply outlook.

Although a large share of Al Taweelah’s capacity remains offline and a complete recovery is still some distance away, the latest progress indicates that lost supply is steadily returning to the market, helping to alleviate concerns about aluminium availability.

Precious Metals – Gold Advances on Softer U.S. Economic Data

Gold posted strong gains after weaker-than-expected U.S. employment figures reduced concerns that the Federal Reserve might need to tighten monetary policy further this year. The softer labor market data pushed both Treasury yields and the U.S. dollar lower, increasing the attractiveness of non-yielding assets such as gold.

The rally extended gains already supported by less hawkish remarks from Fed Chair Kevin Warsh earlier in the week. Investors are increasingly reassessing the trajectory of U.S. monetary policy, with upcoming economic releases likely to play a crucial role in determining whether labor market weakness persists. Continued moderation in economic activity could lessen pressure on the Fed to raise rates, providing further support for gold prices.

Central banks also remained significant buyers of gold in May, purchasing a net 41 tonnes according to the World Gold Council. Poland led acquisitions with 18 tonnes, bringing its purchases for the year to 64 tonnes. China continued its long-running accumulation strategy, adding 10 tonnes and extending its buying streak to 20 consecutive months. Uzbekistan and Kazakhstan increased their reserves by 9 tonnes and 7 tonnes, respectively.

In contrast, Russia was a net seller, reducing its gold holdings by 6 tonnes during May and bringing year-to-date sales to 34 tonnes. Turkey also trimmed reserves by 3 tonnes, resulting in total sales of 81 tonnes so far this year. Despite these sales, robust demand from central banks continues to provide a strong underlying foundation for the gold market.

Silver is poised for a strong rebound amid a softer Fed outlook, easing inflation concerns, and weaker oil prices.

Silver gains momentum as signs of a slowing US labor market prompt investors to reassess the path of interest rates.

According to the CME FedWatch tool, the probability of a September rate hike fell to 52% from 66% following the latest data release.

Silver prices extended gains for a fourth straight session on Friday, with XAG/USD trading near $62.60 per troy ounce during Asian trading hours. A softer inflation outlook, weaker oil prices, and a less aggressive Federal Reserve are providing strong support for the non-yielding metal’s recovery.

Silver is attracting renewed buying interest as signs of a slowing US labor market prompt investors to sharply reassess the outlook for interest rates. The shift in sentiment followed Thursday’s June Nonfarm Payrolls (NFP) report, which showed the US economy added only 57,000 jobs, well below expectations of 110,000. Although the unemployment rate unexpectedly edged down to 4.2% from 4.3% in May, the weak hiring figures reinforced concerns about broader economic cooling.

In response, traders pared back expectations for tighter monetary policy. Data from the CME FedWatch tool showed the probability of a September rate hike falling to 52%, compared with 66% before the jobs report.

Additional support came from recent comments by Federal Reserve Chair Kevin Warsh at the ECB Sintra Conference, where he reiterated the Fed’s commitment to its 2% inflation target while noting that inflation pressures and expectations have eased in recent weeks.

Silver is also benefiting from declining energy prices, which are helping reduce inflationary pressures. Crude oil prices have weakened as shipping activity through the Strait of Hormuz continues to normalize following progress in US-Iran diplomatic negotiations in Doha. The easing geopolitical tensions have reduced the risk premium that had previously supported energy markets.

WTI crude continues to trade lower below the $68.00 level as investors remain optimistic that diplomatic negotiations will bring an end to the conflict between the United States and Iran. Reports from Qatari mediators indicate that talks held in Doha this week have made meaningful progress, easing concerns over potential supply disruptions. Adding to the bearish pressure, Reuters reported that OPEC+ is considering raising output by 188,000 barrels per day in August, further improving the global supply outlook.

Crude oil prices continued to move lower on Thursday as signs of progress in diplomatic efforts between the United States and Iran reduced concerns about potential supply disruptions. West Texas Intermediate (WTI), the US benchmark crude grade, slipped below the $68.00 mark and was trading around $67.80 at the time of writing, its lowest level since the conflict began in February.

According to Qatar’s Foreign Ministry, indirect negotiations held in Doha earlier this week produced encouraging results. Officials stated that both sides made headway on matters related to the memorandum that ended hostilities in June and were building on discussions initiated during a recent summit in Switzerland.

Uncertainty Remains Despite Diplomatic Progress

While reports suggest the talks are moving in a constructive direction, key details remain limited. US President Donald Trump said the negotiations yielded progress regarding potential restrictions on Iran’s nuclear program, adding that efforts toward denuclearization were advancing positively. However, US Vice President JD Vance indicated that nuclear-related issues would likely be addressed in future discussions.

Meanwhile, Iran’s Deputy Foreign Minister Kazem Gharibabadi stated that both parties had agreed to establish a communication mechanism to monitor and report any violations of the existing memorandum of understanding.

A major source of uncertainty remains the Strait of Hormuz. Although shipping activity through the vital waterway has increased since the ceasefire, traffic levels remain well below pre-conflict norms, suggesting that full normalization has yet to occur.

On the supply side, oil prices also came under pressure after reports that the OPEC+ alliance is considering raising production quotas by 188,000 barrels per day in August. Expectations of additional supply entering the market have further weighed on crude prices, reinforcing the bearish sentiment driven by easing geopolitical risks.

AUD/USD comes under renewed selling pressure on Wednesday as a combination of factors continues to support the US Dollar. Ongoing uncertainty surrounding Iran and growing expectations of further Fed rate hikes remain key tailwinds for the greenback. Meanwhile, the pair shows little reaction to China’s RatingDog Manufacturing PMI, which came in broadly in line with expectations.

AUD/USD failed to build on Tuesday’s rebound from the 0.6865 area, its lowest level in three months, and came under renewed selling pressure during Wednesday’s Asian session. The pair slipped back below 0.6900 and showed little reaction to China’s latest private manufacturing PMI data.

China’s RatingDog Manufacturing PMI eased to 51.7 in June from 52.2 in May, reinforcing concerns about slowing economic momentum. Combined with Tuesday’s official PMI figures, which highlighted weak domestic demand and subdued consumer spending, the data weighed on the Australian Dollar, which is often viewed as a proxy for China’s economic health. A modest recovery in the US Dollar further added to the pair’s downside pressure.

The Greenback continued to benefit from its safe-haven appeal amid uncertainty surrounding US-Iran negotiations and growing expectations that the Federal Reserve may need to raise interest rates further. Although US officials arrived in Qatar to discuss the implementation of a preliminary peace agreement, Iran’s reluctance to engage with US envoys has cast doubt on the prospects for a lasting resolution, keeping geopolitical risks elevated.

At the same time, stronger-than-expected US labor market data supported the USD. The JOLTS report showed job openings climbed to a two-year high of 7.594 million in May, underscoring continued labor market resilience. Combined with concerns that renewed tensions in the Middle East could reignite inflationary pressures, the data strengthened market expectations for additional Fed tightening.

Investors now await remarks from Fed Chairman Kevin Warsh at the ECB Forum in Sintra, alongside key US data releases including the ADP employment report and ISM Manufacturing PMI. Attention will then turn to Thursday’s closely watched Nonfarm Payrolls report, which could provide the next major catalyst for AUD/USD.

As markets gradually move beyond pressures from energy inflation, geopolitical tensions, and persistent central bank tightness, a new potential source of volatility is emerging in the Pacific: El Niño.

Introduction

Earlier this month, the National Oceanic and Atmospheric Administration confirmed that El Niño conditions have developed across the Pacific Ocean. Early projections indicate this could evolve into one of the strongest events in decades, with impacts extending well beyond weather patterns.

El Niño is a recurring climate phenomenon that appears every few years when trade winds across the tropical Pacific weaken. As a result, warm surface waters that are usually pushed toward Asia and Oceania shift back toward the Americas. This disrupts global weather systems, often causing heavier rainfall in parts of the Americas while bringing hotter, drier conditions to regions such as South and Southeast Asia, Australia, and Southern Africa. These shifts can lead to droughts, heatwaves, or excessive rainfall, all of which can damage crop yields, disrupt planting cycles, and strain global food supply chains. Following a period where inflation has been driven largely by energy costs, food-related shocks may become the next major inflationary pressure.

A Strong El Niño Is Taking Shape

Research on El Niño’s macroeconomic effects consistently highlights its influence on commodity markets, particularly agriculture. The main transmission channel is through food prices, with multiple studies suggesting a clear link between ENSO cycles and commodity inflation.

Federal Reserve research estimates that nearly 20% of fluctuations in commodity-price inflation can be attributed to ENSO patterns. In a typical El Niño event, real commodity inflation may rise by around 3% over a six- to twelve-month horizon, with agricultural commodities experiencing the most significant impact. Studies by Cashin, Mohaddes, and Raissi further suggest global non-energy commodity prices can increase by approximately 5%, with effects lasting six to sixteen months.

Weather disruptions reduce crop yields, degrade quality, and delay transportation, tightening physical supply conditions. Agricultural prices tend to respond first, and rising input costs eventually feed through to broader food inflation. This can also weaken local currencies, increase imported inflation, and reduce central banks’ flexibility to lower interest rates.

Two key patterns stand out.

First, the growth effects differ significantly across countries. Economies such as Australia, India, Indonesia, Chile, parts of Southern Africa, and the Andean region typically experience negative output shocks when El Niño disrupts rainfall and agricultural activity. In contrast, the United States and some European economies may see a smaller negative impact or even modest gains. In South America, particularly Brazil and Argentina, segments of the soybean supply chain can benefit from increased rainfall conditions.

Second, inflation responses are uneven across regions. The effect is most pronounced in countries where food accounts for a large share of the consumer price index and where exchange rate pass-through is strong. In these economies, rising food and energy costs can push up inflation expectations, weaken domestic currencies, and intensify imported inflation pressures. As a result, central banks—especially in emerging markets that rely on commodity imports—often face limited scope to reduce interest rates.

The euro area is relatively insulated. Research from Banco de España suggests that El Niño episodes have historically lowered euro-area inflation by about 0.3 percentage points after one year. This is mainly due to composition effects and the Common Agricultural Policy, which helps buffer the transmission of global food price shocks to European consumers.

The Commodity Shock

Commodity markets typically move ahead of official inflation data, as agricultural prices are driven by expectations that can shift rapidly with changes in rainfall, temperature, and harvest conditions. This year, weather-related risks are emerging on top of already elevated input costs. Farmers continue to face high fertiliser and diesel expenses following prolonged energy-market stress and geopolitical disruptions. The World Bank projects global commodity prices to rise by about 16% in 2026—the first annual increase since 2022—driven mainly by energy and fertiliser costs. While agricultural prices are expected to decline under baseline assumptions, El Niño represents a clear upside risk to that outlook.

Historically, El Niño episodes have tended to support soft commodity prices. Products such as cocoa, coffee, sugar, palm oil, cotton, and rice are highly sensitive to rainfall patterns in tropical regions. However, the actual price response varies depending on inventory levels, regional weather conditions, and substitution effects across crops.

Cocoa is particularly vulnerable. Ivory Coast and Ghana together account for roughly half of global cocoa production. Strong El Niño events have often reduced output in these regions, either through drought conditions or through a combination of excessive rainfall followed by disease pressure. The most recent cycle illustrated this clearly: heavy rains initially increased disease risk for cocoa trees, followed by extreme heat and dry Harmattan winds that further damaged already weakened crops. As a result, cocoa prices surged dramatically in 2024, at one point approaching or exceeding USD 12,000 per metric ton, making it one of the most volatile commodity stories of the year.

Palm oil and cotton also carry significant exposure to weather conditions in Asia, particularly in Indonesia, Malaysia, and India. Any weakness in the monsoon season can quickly alter supply expectations for these crops.

Coffee exposure is mainly concentrated in robusta production, with Vietnam and Indonesia accounting for around half of global supply. El Niño typically brings hotter and drier conditions during key growing stages. Arabica behaves differently: Brazil may initially benefit from reduced frost risk, but later-season heat and dryness can still threaten yields.

Sugar is somewhat more resilient. A weaker monsoon in India and Thailand can support prices, although India may offset part of the production loss by diverting ethanol feedstock back into sugar output.

Rice is highly sensitive to monsoon performance. A weak rainy season across Asia can quickly reduce output expectations and heighten food security concerns, especially in countries where rice is a dietary staple.

Corn is influenced more by regional weather patterns than El Niño alone. While dryness in some regions can support prices, the overall signal is mixed because other growing areas may experience favorable conditions.

Soybeans present a more complex picture. While El Niño can create stress in certain regions, improved rainfall in Brazil and Argentina may offset losses elsewhere, making price effects less straightforward compared with crops like rice or palm oil.

Natural gas stands out as the main exception. A milder winter in the Northern Hemisphere typically reduces heating demand and puts downward pressure on prices. However, in 2026 this seasonal weakness may be partially offset by broader energy-market tensions linked to geopolitical risks in the Strait of Hormuz.

Looking ahead, the Indian monsoon is a key near-term catalyst. Rainfall between June and September will be critical for cotton, sugar, rice, and palm oil markets. A normal monsoon would likely contain much of the El Niño-related risk, while a significant shortfall would reintroduce strong upside price pressure.

Finally, there is a mismatch in timing between futures and physical markets. Weather forecasts are still influenced by the “spring predictability barrier,” a period when El Niño models are less reliable before summer data becomes clearer. As a result, futures markets may begin pricing in 2026–27 weather risks well in advance, while physical markets remain anchored to current inventories, crop conditions, and near-term supply-demand fundamentals.

Implications for Financial Markets

In equity markets, potential beneficiaries typically include fertiliser manufacturers, agricultural input suppliers, and commodity-exporting firms. In contrast, companies involved in food processing, beverages, and other downstream users of agricultural commodities may face margin compression due to rising input costs. The insurance and reinsurance sectors could also come under pressure from increased claims linked to extreme weather events such as floods, droughts, and wildfires. While overall equity performance may be dampened by supply-chain disruptions and agricultural volatility, the impact is likely to differ significantly across regions and sectors.

From a foreign exchange and emerging markets perspective, countries that rely heavily on food imports and have high inflation pass-through tend to be most vulnerable. These economies may experience currency depreciation and tighter monetary policy conditions. On the other hand, commodity-exporting nations could benefit from improved terms of trade. Overall, a strong El Niño event would create meaningful cross-asset implications, favoring selective exposure to commodities, inflation hedges, and careful allocation across duration, emerging market assets, and sector positioning. Close monitoring of updates from agencies such as NOAA, the WMO, and commodity price signals will be important for positioning decisions.

Conclusion

Even a severe El Niño is considered a secondary risk compared to the current energy-driven shock originating from the Strait of Hormuz, which remains the dominant force shaping commodity and inflation dynamics. Its importance lies in its role as an additional upside risk to food inflation and emerging market pressure.

The most important near-term variable to watch is the Indian monsoon through September, which will act as a key turning point. A normal monsoon would help contain much of the weather-related risk, while a significant shortfall could transform the current uncertainty into a clearer and more tradable disruption in soft commodity markets.

WTI crude oil prices slid to around $69.60 during early Asian trading on Monday as optimism grew over a potential diplomatic breakthrough between the US and Iran. Market sentiment improved after reports indicated that both countries were moving back toward negotiations aimed at ending the conflict, with Axios reporting that US and Iranian officials are scheduled to meet in Qatar on Tuesday.

WTI crude oil retreated to around $69.60 during early Asian trading on Monday as easing geopolitical tensions weighed on prices. The decline followed reports that the United States and Iran had agreed to suspend military strikes and resume negotiations, with officials from both countries expected to meet in Qatar on Tuesday.

According to Axios, citing unnamed US officials, Washington and Tehran have agreed to halt more than three days of retaliatory attacks in and around the Strait of Hormuz and continue technical discussions aimed at de-escalating the conflict. The move marks a shift from the weekend, when talks were reportedly suspended after US strikes on Iranian military targets in response to Tehran’s attacks on shipping vessels in the strategic waterway.

Meanwhile, Iran’s Islamic Revolutionary Guard Corps (IRGC) claimed responsibility for attacks on eight US military sites in Kuwait and Bahrain, describing them as retaliation for recent American strikes on Iranian facilities.

Market participants will remain focused on the outcome of the upcoming US-Iran talks. Any diplomatic progress could help secure oil flows through the Strait of Hormuz, a critical route that handles roughly one-fifth of global oil shipments, potentially putting further pressure on crude prices. Conversely, renewed hostilities could reignite concerns over supply disruptions and support higher oil prices.

Investors are also awaiting the latest weekly crude inventory data from the American Petroleum Institute (API) on Tuesday. A larger-than-expected decline in stockpiles would signal stronger demand and could provide support for WTI, while an unexpected inventory build may point to weaker consumption or excess supply, weighing on prices.

USD/CAD weakens as the oil-sensitive Canadian Dollar draws support from higher crude prices.

Oil prices advanced after an attack on a vessel near Oman disrupted UN evacuations through the Strait of Hormuz, reviving concerns over global energy supplies.

Meanwhile, the US Dollar could remain supported by rising expectations of a Federal Reserve rate hike, which continue to bolster demand for the Greenback.

USD/CAD extends its decline for a second straight session, hovering near 1.4200 during Friday’s Asian trading hours. The pair comes under pressure as the commodity-linked Canadian Dollar gains support from stronger crude oil prices. Canada, one of the world’s largest net oil exporters, relies heavily on petroleum exports as a key source of foreign exchange revenue.

Oil prices climbed after a suspected projectile strike on a cargo vessel near Oman forced the United Nations to suspend evacuation operations through the strategically important Strait of Hormuz, reigniting concerns over global energy supply disruptions.

Geopolitical tensions escalated further late Thursday after two US officials claimed Iranian forces had opened fire on the vessel while it was transiting the strait. Iranian authorities later warned that ships operating outside designated Hormuz routes could no longer be assured safe passage.

However, losses in USD/CAD may remain capped as the US Dollar continues to draw support from increasing expectations of another Federal Reserve rate hike. CME FedWatch data currently shows markets pricing in a 63.4% chance of a rate increase at the Fed’s September 15–16 meeting.