- Geopolitical tensions involving Iran, fresh U.S. retail sales figures, and a surge in Q1 earnings reports are set to drive market sentiment in the coming week.

- Tesla stands out as a potential buy, supported by improving turnaround momentum and closely watched forward guidance that could reshape investor expectations.

- In contrast, Intel appears vulnerable after a strong recent rally, with downside risks emerging from stretched valuations and potential profit-taking.

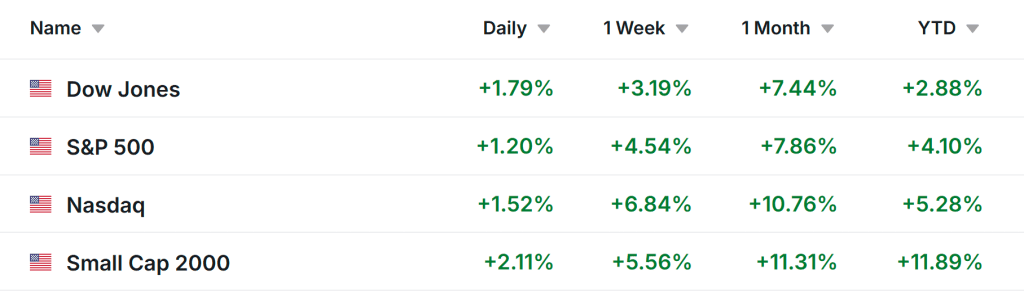

U.S. equities surged on Friday after investors welcomed Iran’s move to reopen the Strait of Hormuz. The S&P 500 and Nasdaq Composite each notched their third consecutive record close, while the blue-chip Dow Jones Industrial Average posted its strongest finish since late February.

For the week, the S&P 500 climbed 4.5%, the Dow Jones Industrial Average advanced 3.2%, the tech-heavy Nasdaq Composite surged 6.8%, and the small-cap Russell 2000 gained 5.6%.

Looking ahead, market focus will once again center on developments in the Middle East and movements in oil prices, after Iran stated on Saturday that the Strait of Hormuz is now “under strict control” by its forces—marking a sharp shift from Friday’s stance.

Potential direct talks between the U.S. and Iran may take place in Pakistan on Monday, although Tehran indicated that no official date has been confirmed. Meanwhile, the current two-week ceasefire is set to expire on Wednesday.

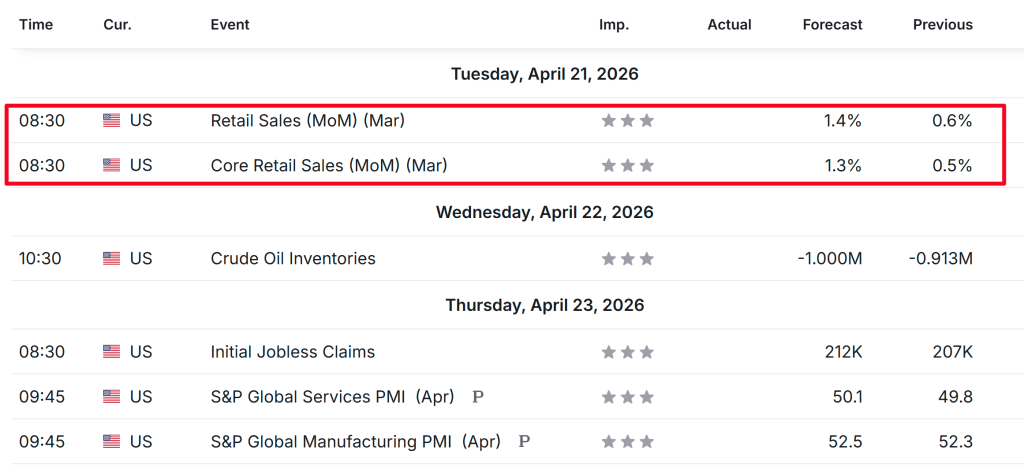

On the economic front, attention will also turn to U.S. data releases, including retail sales, initial jobless claims, and consumer sentiment, in what is expected to be a relatively quiet week for macroeconomic indicators.

The Senate Banking Committee is set to hold a confirmation hearing on Tuesday for Kevin Warsh regarding his nomination as Federal Reserve chair.

At the same time, earnings season is moving into full swing, with several major companies scheduled to report results in the week ahead, including Tesla, Intel, IBM, Boeing, GE Aerospace, UnitedHealth, AT&T, American Express, and United Airlines.

Regardless of how the broader market unfolds, the focus below highlights one stock that appears poised to attract buying interest and another that could face renewed downside pressure. Note that this outlook is strictly short-term, covering the trading week from Monday, April 20 through Friday, April 24.

Stock to watch for buying: Tesla

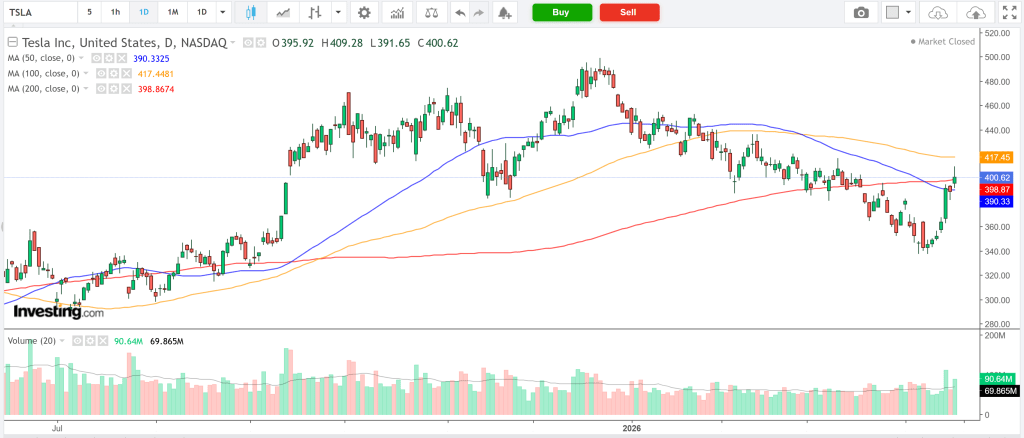

Tesla heads into its Q1 2026 earnings with strong momentum. After breaking a prolonged losing streak, the stock posted its best weekly gain since last May and is now trading close to the $400 level ahead of the announcement.

Options markets are pricing in a move of around 6% following the earnings release—significant, though not unusual for Tesla. If results meet or exceed expectations, accompanied by positive forward guidance and convincing updates on long-term autonomy and product development, the stock could see an even larger upside move as investor sentiment shifts.

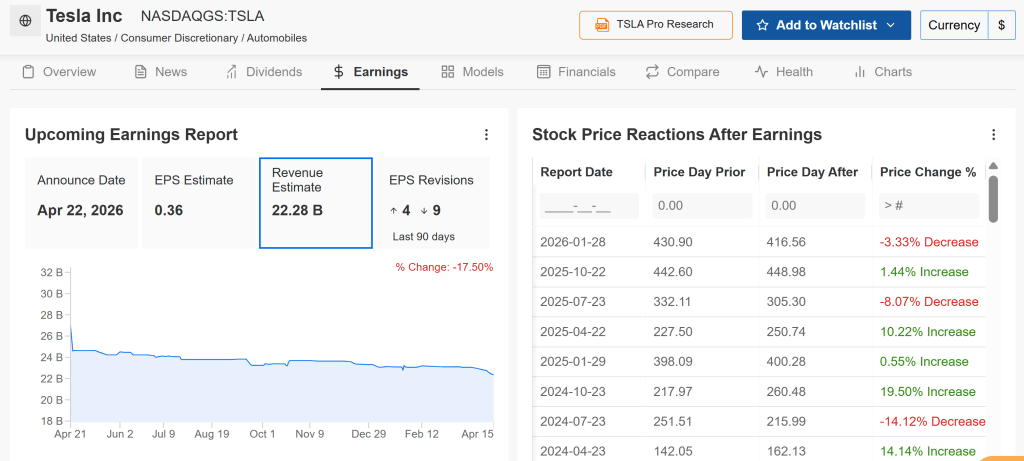

Wall Street forecasts adjusted earnings of $0.36 per share, marking an approximate 33% year-over-year increase from a weaker Q1 2025. Revenue is expected to rise 15% to $22.28 billion.

However, the spotlight will be on guidance and strategic commentary from CEO Elon Musk. Investors will closely watch developments in key areas such as the robotaxi initiative, Cybercab production plans, and the rollout timeline for Full Self-Driving technology.

Markets are also paying attention to any updates related to a potential SpaceX IPO and how it might connect to Tesla’s broader ecosystem. Positive signals on this front could further boost bullish sentiment.

As Tesla continues to be valued more as an AI and robotics company rather than purely an EV manufacturer, strong earnings or encouraging autonomy-related updates could drive additional upside.

Trade Setup:

- Entry: ~$401

- Target: $436 (+8.7%)

- Stop-loss: $387 (-3.5%)

Stock to consider selling: Intel

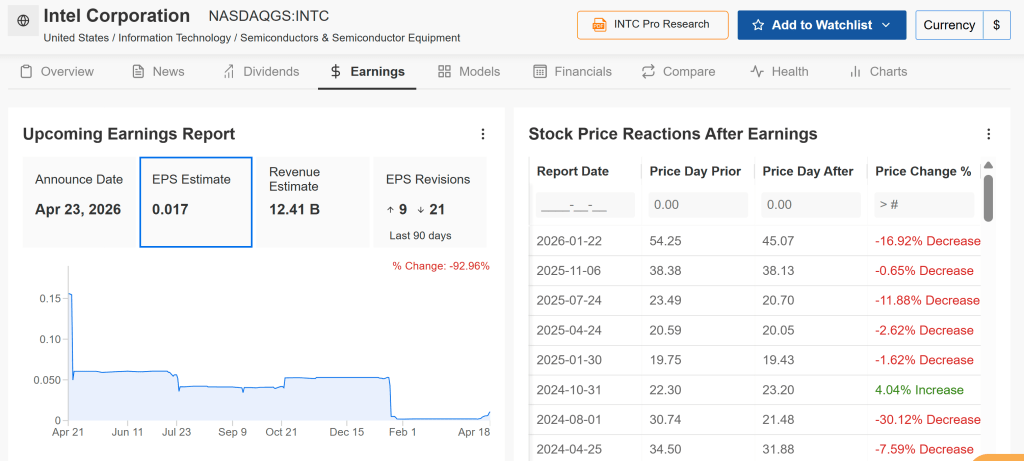

Intel is heading into a more difficult earnings setup, making it a potential sell or avoid candidate this week. The company is scheduled to report Q1 results on Thursday at 4:00 PM ET, with options markets implying a sizable post-earnings move of around ±9%.

Wall Street expects adjusted earnings per share of roughly $0.02, representing a steep 87% decline compared to the same period last year. Revenue is projected to slip 2% to about $12.4 billion, pressured by ongoing softness in the PC market and continued losses in its foundry segment.

Looking forward, Intel is likely to guide revenue in the $11.7–$12.7 billion range. Despite its widely discussed turnaround strategy, tangible progress remains limited. The foundry business continues to burn cash while facing intense competition from TSMC and Samsung. Meanwhile, its GPU and AI accelerator products have yet to gain meaningful traction in the market.

Although INTC shares have surged about 85% year-to-date in 2026, this strong rally leaves the stock exposed to profit-taking, especially if earnings or guidance disappoint.

From a technical perspective, the RSI stands at an elevated 79.05, signaling overbought conditions. Additionally, declining volume during recent price increases suggests weakening buying momentum as the stock nears resistance in the $70.33–$72.33 range (upper Bollinger Band).

Given the likelihood of underwhelming results and cautious guidance, Intel may present a classic “sell-the-news” scenario. Investors could consider trimming positions ahead of the earnings release.

Trade Setup:

- Entry: ~$68.50

- Target: $59.13 (+13.7%)

- Stop-loss: $71.38 (-4.2%)

Leave a comment