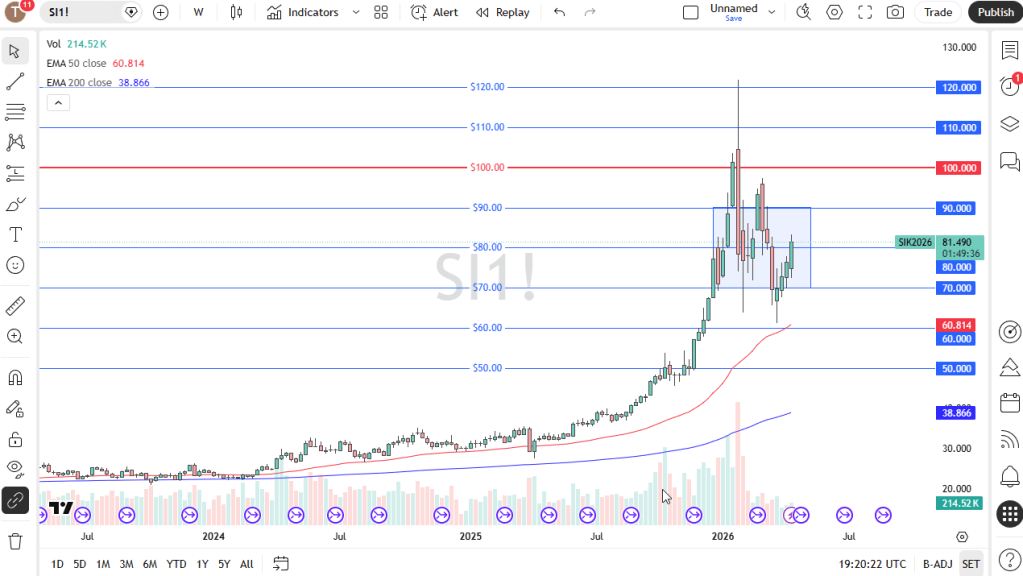

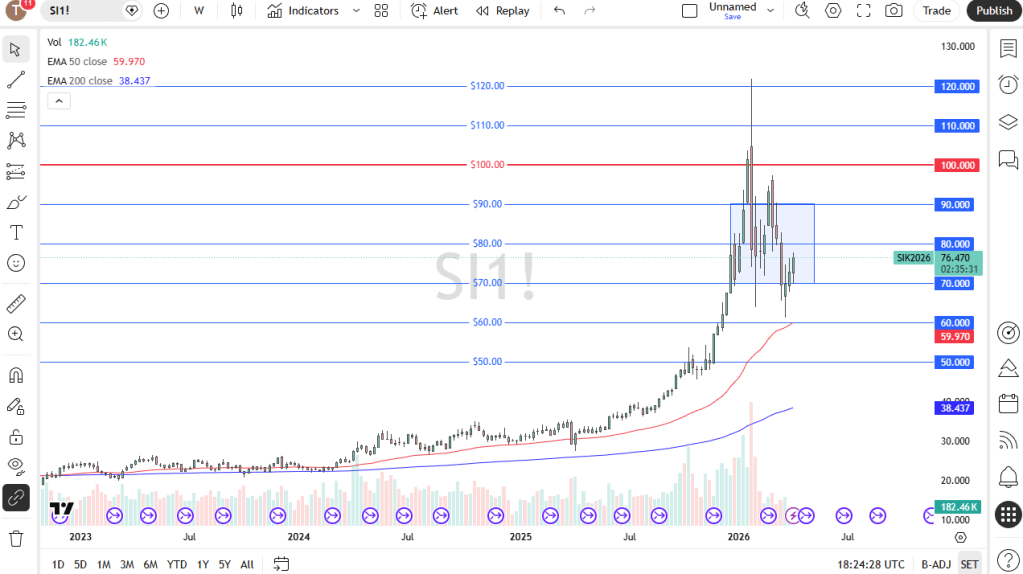

Silver advanced over the week but continued to struggle to break decisively above the key $60 level. This major psychological resistance remains a focal point for traders, with selling pressure re-emerging as prices approach the area.

Meanwhile, the $55 region continues to provide solid support, helping to limit downside moves. Despite the recent gains, silver remains challenged by the higher interest-rate environment, which continues to weigh on the precious metals market.

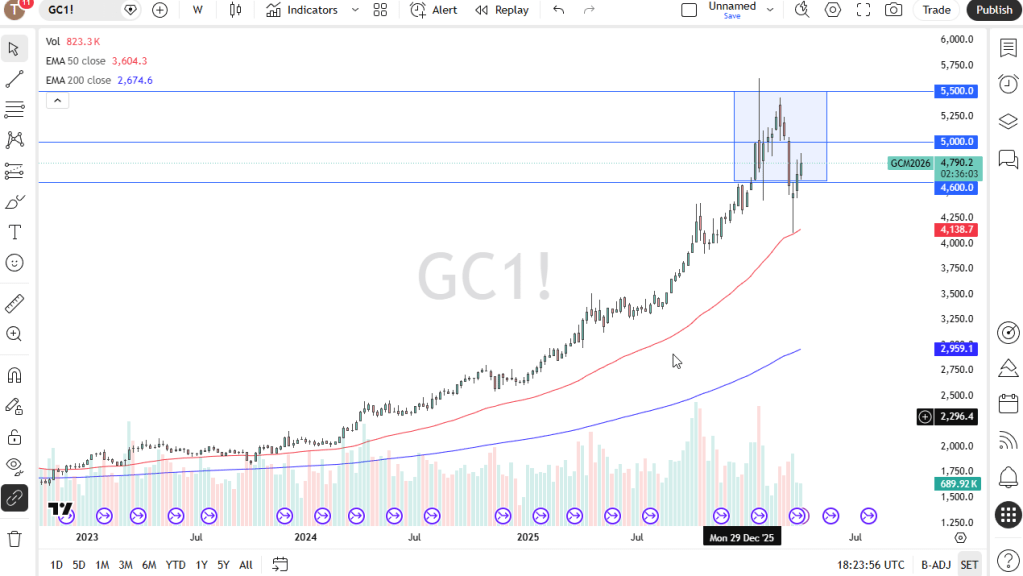

Gold

Gold followed a similar pattern, climbing toward the $4,200 area before retreating from a level that has repeatedly acted as a significant resistance zone. The pullback highlights the market’s ongoing struggle to establish sustained momentum above this threshold.

On the downside, the $4,000 mark remains a key psychological support level, with additional buying interest emerging around $3,900. Overall, gold continues to trade in a volatile and uneven manner, with price action heavily influenced by developments in the Middle East. Geopolitical headlines are likely to remain a major driver of market sentiment, affecting not only gold but also interest-rate expectations, which continue to play a crucial role in shaping global financial markets.

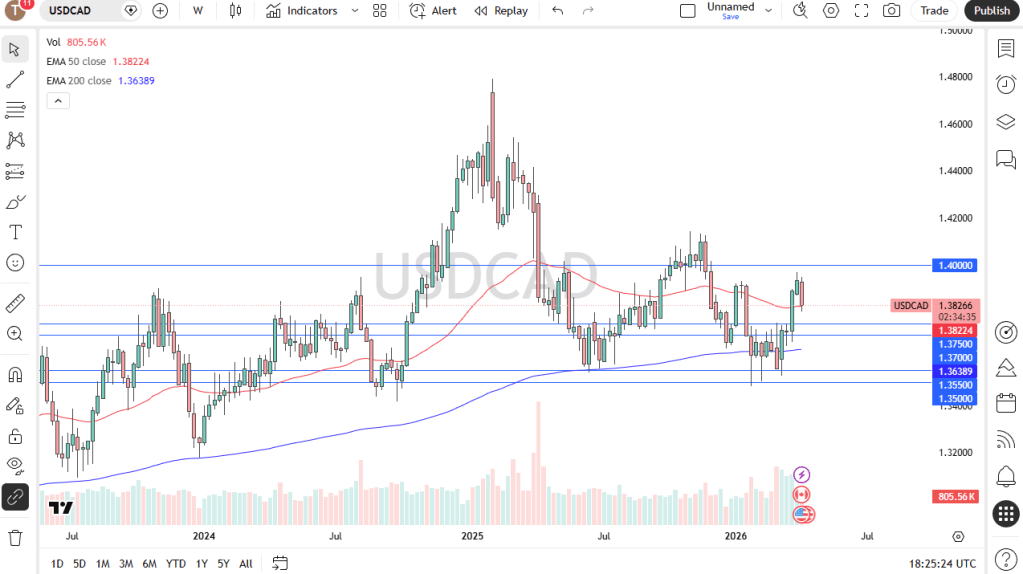

USD/CAD

The U.S. dollar strengthened against the Canadian dollar over the week, even as oil prices surged. This divergence is not particularly surprising, as elevated market uncertainty has boosted demand for the U.S. dollar, while rising U.S. interest rates continue to support the currency. The positive interest-rate differential remains an important factor attracting buyers to the pair.

Although USD/CAD experienced a pullback in recent weeks after an extended bullish run, the correction appears to have helped ease overbought conditions. With the market showing signs of stabilizing, the pair may be positioned to resume its broader uptrend, with the 1.4150 area emerging as a key upside target.

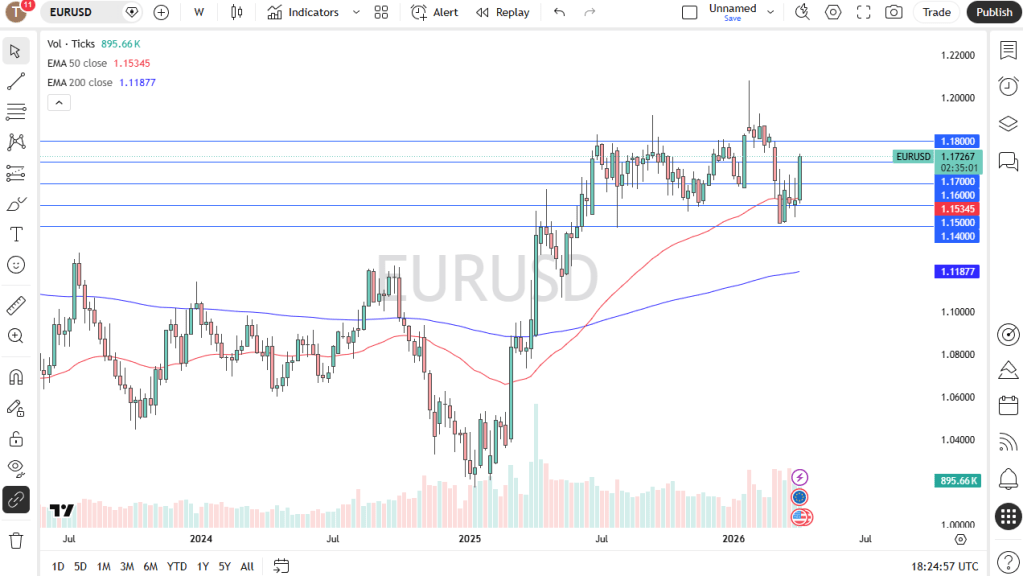

EUR/USD

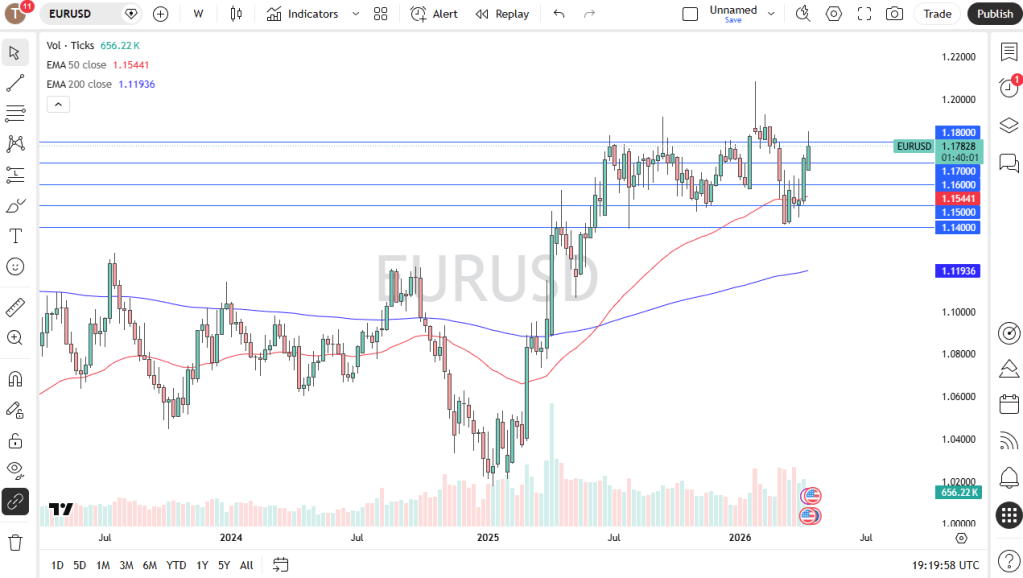

The euro weakened against the U.S. dollar during the week, with the 1.1400 level continuing to serve as a crucial support zone. This area has attracted significant market attention, having acted as a key consolidation level over the past year.

Looking ahead, the outlook for the pair remains heavily influenced by monetary policy expectations. Elevated U.S. interest rates continue to provide strong support for the dollar, reinforcing its appeal relative to other major currencies. As a result, interest-rate dynamics are likely to remain a primary driver of EUR/USD price action in the near term.

USD/JPY

The U.S. dollar remained firmly supported against the Japanese yen, as the yen continues to struggle amid the wide interest-rate gap between Japan and the United States. The pair’s broader trend remains bullish, with underlying fundamentals continuing to favor the U.S. dollar.

While a short-term correction cannot be ruled out after the recent advance, any pullback is likely to be viewed as a buying opportunity by market participants. The substantial interest-rate differential between the two economies continues to attract demand for the pair, reinforcing the longer-term upward outlook for USD/JPY.

GBP/USD

The British pound declined over the week, but the broader market structure remains largely unchanged. GBP/USD continues to trade within a well-established consolidation range between 1.3150 and 1.3700, suggesting that the recent weakness is part of ongoing sideways price action rather than the start of a new trend.

As the pair remains range-bound, it is likely to continue attracting traders who favor consolidation and mean-reversion strategies. Compared with other major currencies, the pound has shown relative resilience against the U.S. dollar, supported in part by the Bank of England’s comparatively hawkish policy stance, which has helped limit downside pressure on sterling.

Bitcoin (BTC/USD)

Bitcoin continues to experience choppy and unpredictable price action, with market sentiment largely driven by shifts in overall risk appetite. As investors weigh macroeconomic conditions and broader financial market trends, volatility is likely to remain elevated.

Despite the recent fluctuations, the $60,000 level appears to be establishing itself as a significant support zone. From a technical perspective, the latest weekly candlestick resembles a shooting star, following two consecutive hammer formations. This combination suggests a market lacking clear directional conviction, increasing the likelihood of continued sideways trading as participants wait for a stronger catalyst to determine the next major move.

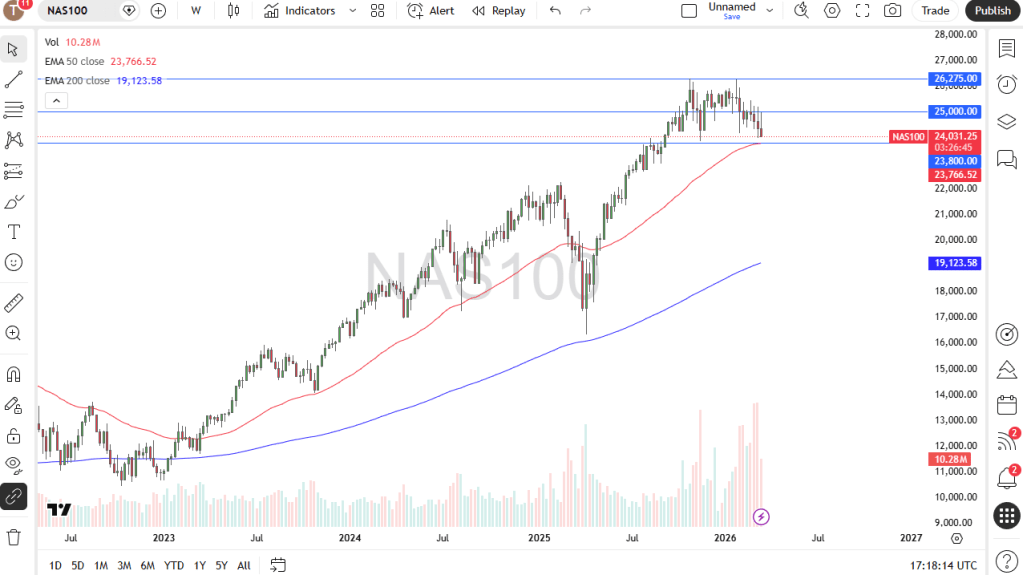

Nasdaq 100

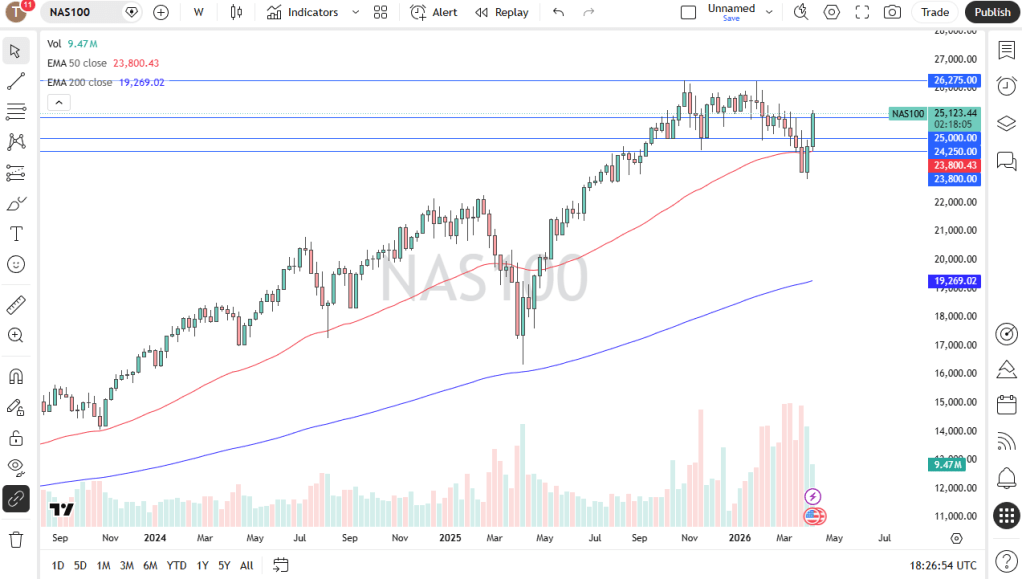

The Nasdaq 100 attempted to move higher during the week but quickly surrendered its gains as investor caution remained elevated. Ongoing geopolitical uncertainty and concerns about the economic outlook continue to weigh on sentiment, limiting the index’s ability to sustain upward momentum.

From a technical standpoint, the index appears vulnerable to a deeper correction if selling pressure persists. However, a decisive break above the high of the latest weekly candlestick would signal renewed bullish strength and could improve the near-term outlook. For now, persistent tensions in the Middle East and expectations of higher interest rates remain key headwinds, making it difficult for growth-oriented assets such as the Nasdaq 100 to stage a strong and sustained rally.

Many investors focus heavily on domestic markets, particularly in the United States, where stocks account for roughly 65% of global equity market capitalization. However, this still leaves about 35% of the world’s investable equity opportunities outside the U.S. A portfolio concentrated solely in one country may miss significant growth potential and expose investors to unnecessary concentration risk.

The Myth of Automatic Global Diversification

Some investors believe they already have international exposure because large U.S. companies generate a substantial portion of their revenue overseas. However, owning multinational U.S. corporations is not the same as investing directly in foreign markets. International investments provide exposure to different economies, regulatory systems, currencies, and political environments that domestic stocks cannot fully replicate.

Another concern is concentration risk within major U.S. indices. The largest companies now account for an increasingly large share of benchmark indexes, meaning investors may be more exposed to a handful of mega-cap stocks than they realize.

Four Ways to Improve Global Diversification

1. Gain Growth Exposure Through Emerging Markets

Emerging economies such as India, Brazil, Indonesia, and China offer access to expanding populations, rising consumer demand, and faster economic growth. Exchange-traded funds (ETFs) focused on these regions can enhance portfolio growth potential while adding geographic and currency diversification.

2. Add Stability with Developed International Markets

Countries including Japan, Canada, Australia, and those in Western Europe host many established companies with strong balance sheets and dividend-paying histories. Developed-market equities often behave differently from U.S. stocks, helping reduce portfolio volatility during periods of market stress.

3. Diversify Income Through International Bonds

International fixed-income investments can provide exposure to different interest-rate cycles and monetary policies. They also introduce foreign-currency exposure, helping reduce reliance on the U.S. dollar while potentially offering attractive yields.

4. Invest in Global Real Estate and Infrastructure

Global infrastructure assets such as utilities, transportation networks, and renewable energy projects can provide stable, defensive returns. International real estate investments further diversify a portfolio by accessing property markets whose cycles may differ from those in the United States.

Bottom Line

A well-diversified portfolio extends beyond national borders. While the U.S. remains one of the world’s most important investment destinations, relying exclusively on domestic assets can create concentration risks and limit long-term opportunities. By incorporating emerging markets, developed international equities, global bonds, and overseas real assets, investors can build a more balanced portfolio positioned to benefit from growth across the global economy.

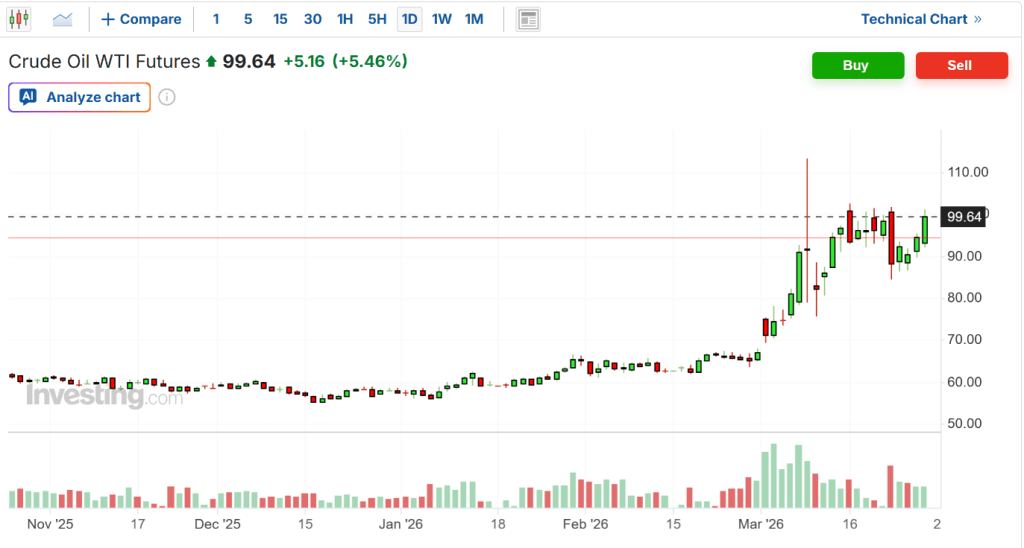

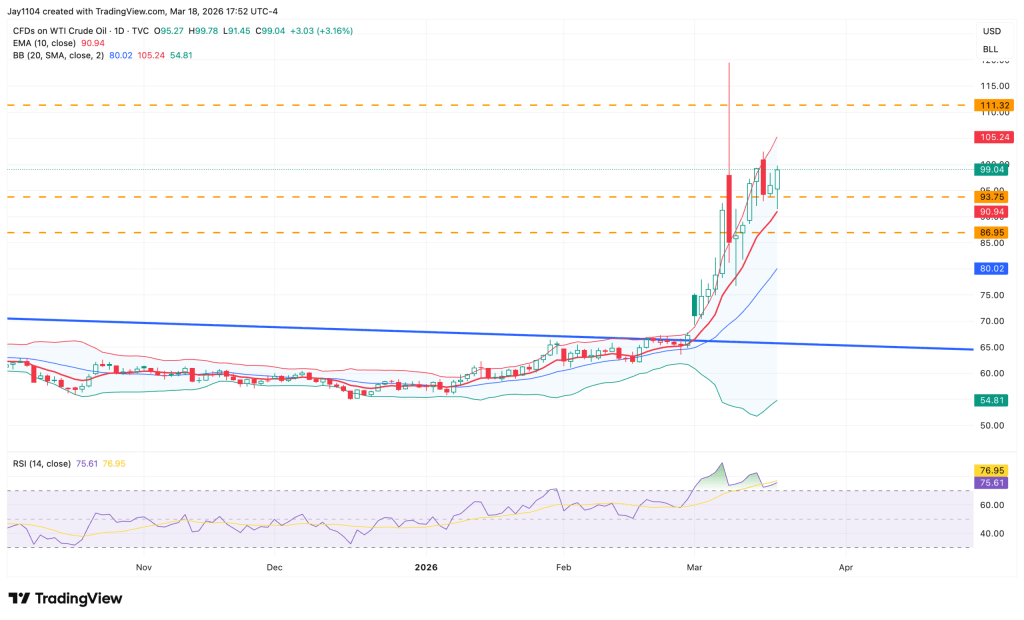

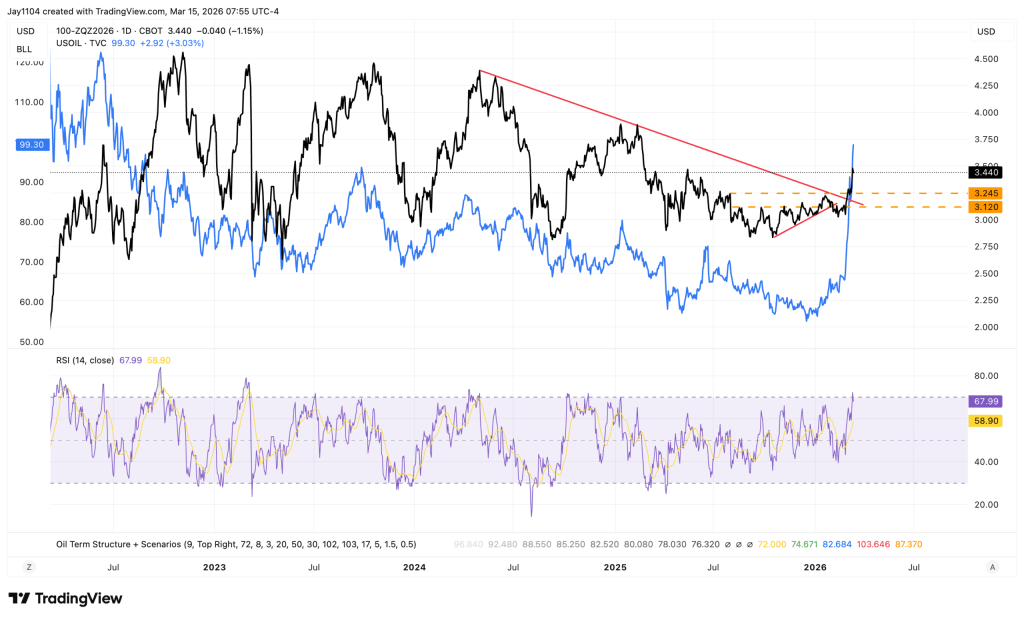

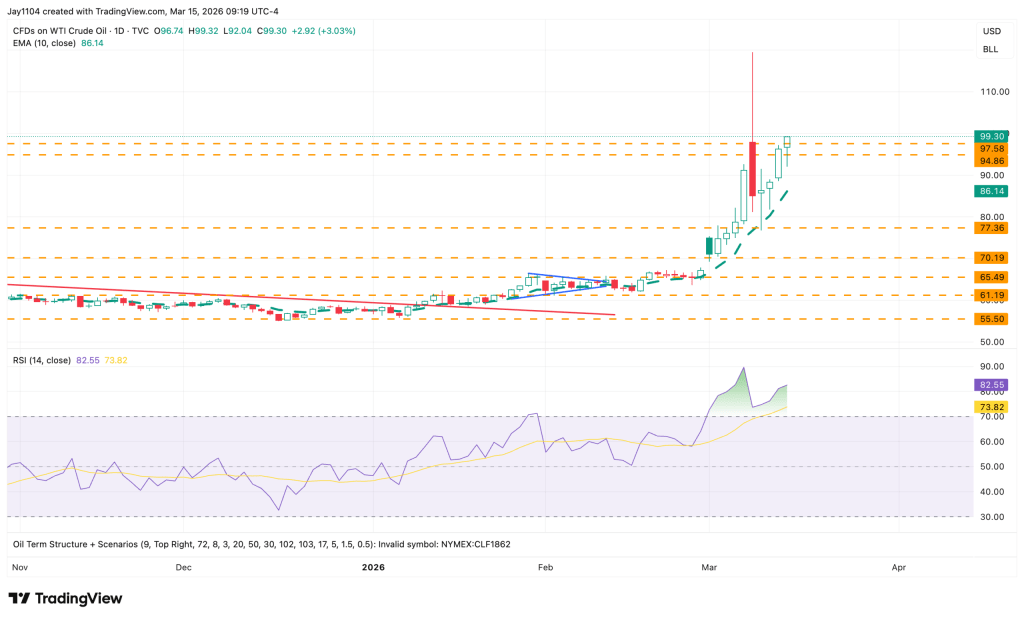

Light Sweet Crude posted strong gains over the past week, a move largely driven by persistent geopolitical tensions in the Middle East that continue to fuel concerns over potential supply disruptions.

The market appears firmly positioned to challenge the $85 per barrel mark. Any near-term weakness or corrective pullbacks are likely to attract fresh buying interest, particularly from short-term traders looking to capitalize on the prevailing bullish momentum.

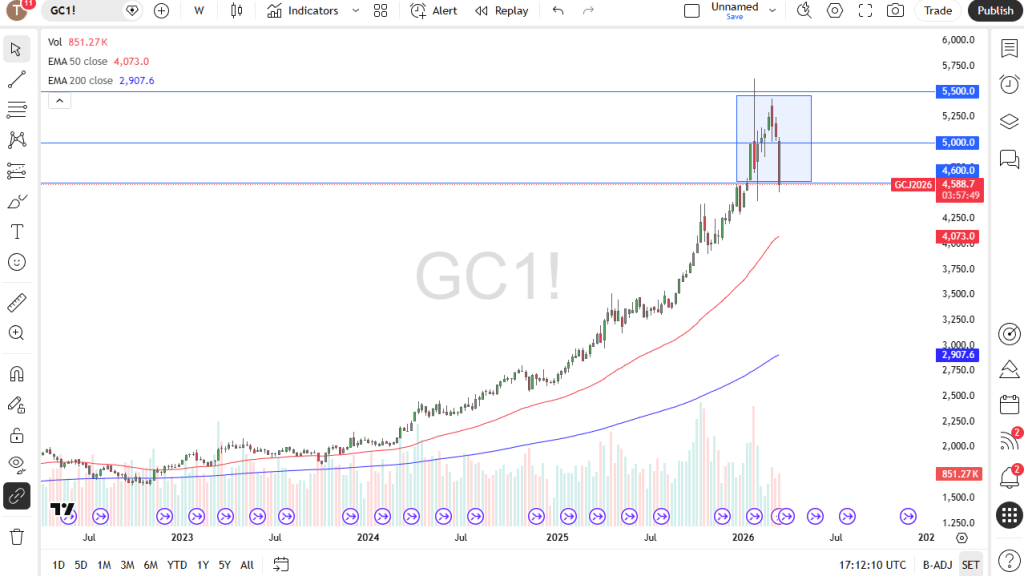

Gold

Gold retreated below the $4,000 threshold once again during the week, remaining under pressure as investors continue to assess the interest rate outlook. Persistent concerns that elevated borrowing costs could reduce the appeal of non-yielding assets such as gold have weighed on market sentiment.

The $4,000 level remains a key technical support zone. A sustained hold above this area could help stabilize prices, while a decisive break lower may open the door to additional downside pressure.

Silver

Silver came under heavy selling pressure during the week, dropping to a fresh low before attempting a modest recovery heading into Friday’s session. Despite the rebound, the broader technical outlook remains weak, with rallies likely to encounter renewed selling interest as bearish sentiment continues to dominate the market.

The $50 level remains a significant support zone that has influenced price action on several occasions in the past. Given the current downward momentum, a move toward this area cannot be ruled out. Rising interest rates continue to undermine the appeal of non-yielding assets, leaving silver vulnerable to further declines and offering little incentive for bullish positioning at this stage.

CAC 40

The CAC 40 experienced volatile and range-bound trading throughout the week. However, following the sharp decline seen in the previous week, the recent consolidation can be viewed as a constructive sign that the market may be stabilizing. A decisive break above the 8,400 level could pave the way for further gains toward 8,500.

A sustained move beyond 8,500 would strengthen the bullish outlook and potentially trigger a broader upward advance. On the downside, the 8,000 area continues to provide significant support, and as long as the index remains above this level, the longer-term uptrend is likely to stay intact.

Natural Gas

Natural gas prices edged lower over the past week, extending the prevailing bearish trend. The weakness is largely consistent with seasonal demand patterns, as this period of the year typically experiences softer consumption. Under these conditions, short-term rebounds are likely to be viewed as selling opportunities rather than the start of a sustained recovery.

Market sentiment remains tilted to the downside, with traders likely to sell into rallies that show signs of losing momentum. A break below this week’s low could accelerate selling pressure and expose the $2.50 level as the next significant downside target. Given that the market is currently focused on the August contract, a substantial upward move appears unlikely unless an intense and widespread heatwave significantly boosts energy demand across the United States.

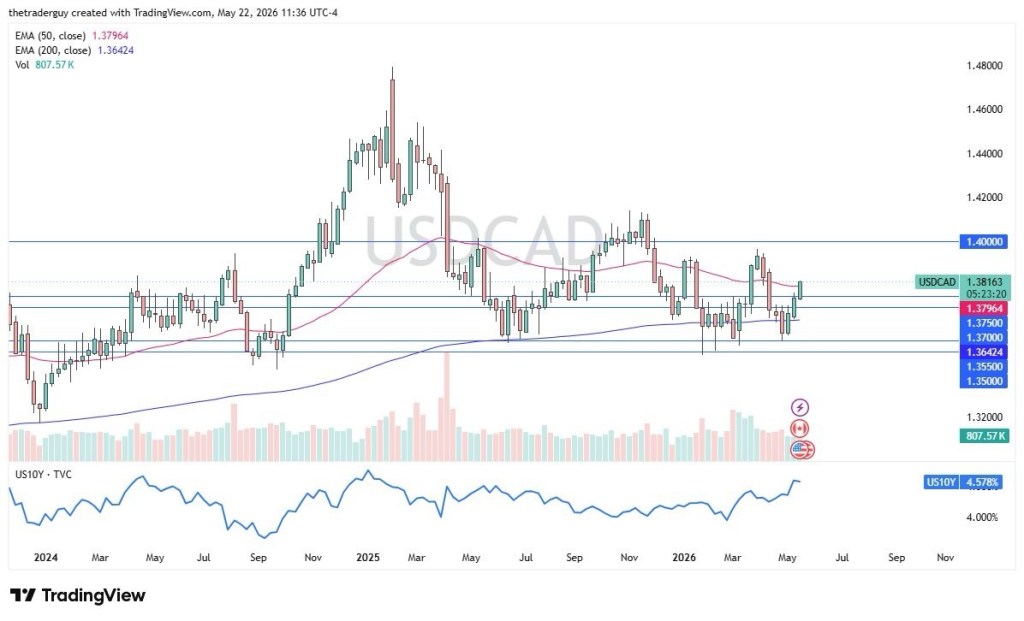

USD/CAD

The US dollar came under significant pressure against the Canadian dollar during the week, with the 1.40 level providing a measure of support heading into the weekend. Strength in crude oil prices has contributed to the Canadian dollar’s resilience, as rising energy prices generally benefit Canada’s commodity-linked currency.

The 1.40 area is likely to remain a closely watched support zone, making next week’s price action particularly important for determining the pair’s near-term direction. Recent movements have been influenced by a combination of factors, including ongoing geopolitical tensions in the Middle East, softer-than-expected US CPI and PPI data, and stronger-than-forecast Canadian employment figures released the previous week. Together, these developments have increased pressure on the US dollar while providing support for the Canadian currency.

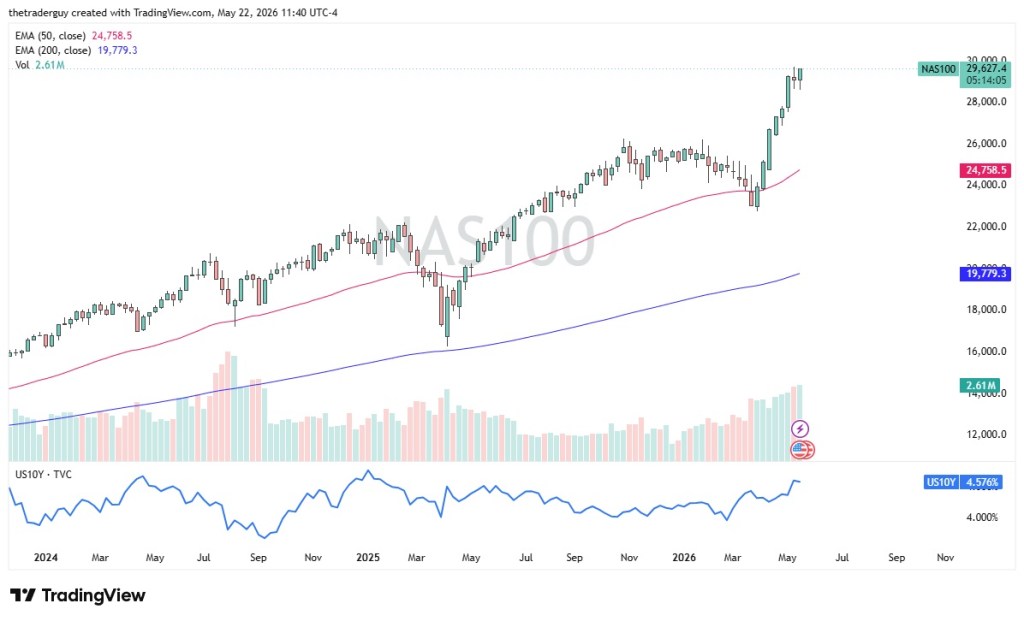

NASDAQ 100

The Nasdaq 100 declined during the week, revisiting the 28,500 level, a region that has repeatedly acted as an important support zone. The market’s ability to hold above this area is likely to attract attention from investors looking for value opportunities and could help sustain the broader consolidation pattern.

If buyers successfully defend the 28,500 support level, the index may stage a rebound and continue trading within its established range. Under current conditions, the broader outlook still favors a move back toward the 30,000 mark over time. However, a significant deterioration in geopolitical conditions, particularly in the Middle East, could undermine risk sentiment and challenge the bullish scenario.

EUR/USD

The EUR/USD pair continued to hover around the key 1.14 level throughout the week. This area, which previously served as a major support zone, remains an important reference point for traders. Although the euro managed to recover modestly earlier in the week, higher US interest rates have continued to limit upside momentum and provide underlying support for the US dollar.

The broader bias remains cautious, with rallies likely to face resistance if buying momentum begins to fade. Given the current interest rate dynamics and ongoing demand for the dollar, traders may prefer a short-term trading approach, looking to capitalize on brief upward corrections while remaining alert to signs of renewed weakness in the pair.

U.S. stocks ended Tuesday in positive territory, with the S&P 500 gaining 0.38%. The advance, however, appeared to stem largely from a sharp drop in implied volatility rather than a meaningful shift in market fundamentals. The one-day VIX slid four points to finish at 10.5 after climbing to nearly 15 on July 13.

The earlier spike in volatility was fueled by investor uncertainty ahead of the latest Consumer Price Index (CPI) data and Kevin Warsh’s testimony before the House. Once those events passed and the one-day VIX retreated rapidly following the opening bell, equities lost momentum and spent most of the session moving sideways. With implied volatility now back near subdued levels, the boost it provided to stocks appears to have largely run its course.

Treasury yields declined after the latest CPI report showed softer-than-expected inflation in both the headline and core readings, easing concerns over immediate price pressures. The move was most pronounced at the short end of the curve, with the 2-year Treasury yield dropping eight basis points to close near 4.20%.

Despite the encouraging inflation data, Fed Chair Kevin Warsh struck a more hawkish tone during his testimony before the House on Tuesday. He emphasized that inflation remains above the Federal Reserve’s target and suggested that additional policy tightening may still be necessary. His remarks raised doubts about whether financial markets have fully accounted for the possibility of further interest rate increases.

Although the 2-year yield retreated to 4.20%, it continues to hold above a key support level after breaking through previous resistance. From a technical standpoint, the yield could still climb toward the 4.35%–4.40% range. If inflation proves more persistent than expected, the Federal Reserve may ultimately need to resume rate hikes to complete its inflation-fighting efforts.

Despite the softer-than-expected CPI data, the Japanese yen showed little sign of gaining meaningful traction. The currency strengthened by only 0.12% on the day, leaving USD/JPY to settle near 162.25.

The broader outlook for the yen remains fragile, with few developments so far convincing investors to reverse their bearish stance. As a result, the prevailing trend continues to favor further weakness in the Japanese currency.

From a technical perspective, USD/JPY has been trading closely along its 10-day and 20-day simple moving averages, indicating that bullish momentum remains intact. A decisive break above the 162.50 level could pave the way for a move toward 166, a price not seen since the mid-1980s.

Nvidia’s nearly 4% gain on Tuesday stood in sharp contrast to signals coming from the credit market. The company’s five-year credit default swap (CDS) spread widened to 60.6 basis points, up from roughly 42 basis points on June 22 and above 60 basis points by July 14. Over the same period, Nvidia’s shares rebounded from a June 26 low near $192 to approximately $211.

Under normal market conditions, rising CDS spreads—which reflect increasing perceived credit risk—tend to coincide with weaker equity performance. The divergence between Nvidia’s strengthening share price and widening CDS spreads suggests a disconnect that may not persist. Either the CDS spread will narrow as credit concerns fade, or the stock could eventually adjust lower to reflect the caution being signaled by the credit market.

One possible explanation is that credit investors are pricing in risks that equity investors have yet to fully acknowledge. If that assessment proves accurate, Nvidia’s recent rally may struggle to sustain its momentum as broader market concerns begin to filter into the stock price.

In our previous report, we outlined the $5.5 trillion AI capex supercycle and highlighted three critical bottlenecks that could ultimately determine how much value the ecosystem captures.

The capital is already flowing. The key question now is which supply constraint becomes the limiting factor first. As the industry shifts from training large models to deploying autonomous AI agents, all three bottlenecks are being fundamentally reshaped.

Memory is emerging as the first major pressure point, and Micron’s latest earnings delivered a clear signal of just how rapidly demand is accelerating.

This Week’s TechEdge

CPUs: the most overlooked growth inflection

Memory: the new battleground and what Micron’s results reveal

Networking: our highest-conviction opportunity

The Bottom Line: key implications for investors

The traditional hardware equation is changing. AI training was primarily a GPU-driven story, with large clusters of GPUs supported by relatively few CPUs.

Agentic AI introduces a different dynamic. Like human workers, AI agents require dedicated compute resources, their own memory footprint, and continuous communication with other systems. This reverses the hardware ratios that defined the training era and channels significantly greater demand toward infrastructure categories that were previously secondary considerations.

We believe the agentic AI era could generate roughly three times the hardware spending of the training era over the next two to three years.

CPUs: The Most Overlooked Inflection Point

As AI agents become more prevalent, infrastructure requirements move closer to a one-to-one CPU-to-GPU ratio, since each agent requires orchestration, task management, and system coordination.

We project the CPU market could expand from approximately $35–40 billion today to more than $200 billion by 2030. That outlook exceeds AMD’s estimate of roughly $120 billion and is well above the current Wall Street consensus of around $170 billion.

To put the scale into perspective, Cloudflare estimates that supporting 100 million knowledge workers in the United States would require roughly 10 million CPUs, with global demand potentially approaching one billion CPUs. AMD, Arm, and Intel have all pointed to this emerging trend, and 2025 appears to mark the beginning of the transition. While related stocks have already responded, we believe current valuations reflect only the early stages of a much larger growth cycle.

Memory: The Battleground — What Micron’s Results Revealed

This quarter, the memory story moved beyond theory and into reality.

Micron delivered strong results across every major segment, with the upside driven primarily by pricing rather than volume growth. The most striking figure was adjusted gross margin, which surged to nearly 80%—an extraordinary level for a business that has historically generated margins of 30–50% during favorable cycles and often slipped into negative cash flow during downturns.

Memory pricing has climbed roughly sevenfold from the cycle trough, creating a powerful earnings tailwind for Micron. Those higher prices are flowing directly into the company’s profits while simultaneously increasing infrastructure costs for hyperscalers and AI leaders such as NVIDIA, Alphabet, and Microsoft.

The takeaway is clear: memory is no longer just a supporting component in the AI stack. It is becoming one of the most critical constraints in the industry, with pricing power increasingly concentrated among the companies capable of supplying it.

The forces driving this trend are structural rather than cyclical.

Agentic AI is creating a second, distinct source of memory demand alongside high-bandwidth memory (HBM). While AI training workloads require HBM, autonomous agents also rely heavily on conventional DRAM and NAND—the same memory technologies found in everyday PCs and enterprise systems.

At the same time, manufacturing capacity is becoming increasingly constrained. Producing HBM consumes significantly more resources, with each HBM wafer requiring the equivalent of three to four conventional DRAM wafers. As memory manufacturers shift capacity toward HBM production, the supply available for traditional memory products tightens just as demand for those products is accelerating.

The result is a convergence of two demand streams that historically moved independently, now competing for the same limited supply base. According to Micron’s management, there is still no clear timeline for when supply—particularly in HBM—will fully catch up with demand. We believe these constraints could persist through 2028, extending the favorable pricing environment for memory suppliers and reinforcing memory’s position as one of the most critical bottlenecks in the AI infrastructure stack.

Perhaps the most significant development is not technological, but contractual.

Micron announced 16 strategic customer agreements with fixed-price structures, each spanning roughly three years and representing a combined minimum value of approximately $100 billion through 2030.

Historically, memory has been sold largely on the spot market, a key reason the sector has long traded at a valuation discount due to its cyclical nature. The emergence of multi-year, fixed-price agreements has the potential to reduce earnings volatility, soften future downturns, and support the case for a structural re-rating of memory companies.

That said, we are not prepared to fully underwrite that thesis yet. The real test will come when these businesses generate strong cash flows through an entire down cycle—something that remains unproven. These agreements also carry execution risk. If AI infrastructure investment slows, customers could scale back commitments, while increasing competition from Chinese memory producers remains a meaningful long-term consideration.

For that reason, we continue to favor the picks-and-shovels approach. Companies such as KLA, Lam Research, and Applied Materials supply the critical tools required to expand manufacturing capacity, allowing them to benefit from industry growth without taking direct exposure to memory price cycles.

One emerging catalyst deserves close attention. Micron has highlighted humanoid robotics as a potential second wave of demand growth. These systems could require roughly ten times the memory capacity of today’s AI deployments, creating an additional demand engine that may extend the current cycle well into the next decade.

Networking: Our Highest-Conviction Opportunity

As AI agents become more prevalent, the volume of machine-to-machine communication is set to increase dramatically. Every interaction, task delegation, and data exchange generates network traffic that must be moved efficiently across increasingly complex infrastructure.

The debate is often framed as a choice between copper and optical connectivity, but we believe that view is overly simplistic. Both technologies will play important roles at different performance, distance, and cost thresholds. Rather than betting on a single transmission medium, we prefer technology-agnostic infrastructure providers such as Astera Labs and Credo Technology Group, whose products enable faster and more efficient data movement regardless of the underlying architecture.

Signs of strain are already emerging across the ecosystem. Lead times for certain optical networking products have reportedly extended to as much as 12 months, while fiber pricing has risen approximately 50% since the start of the year. These pressures reflect a market struggling to keep pace with accelerating AI infrastructure demand.

Industry forecasts suggest the optical networking market could ultimately exceed $150 billion in value—roughly nine times its current size. While networking has already outperformed both memory suppliers and hyperscale cloud providers during this cycle, we continue to see the greatest potential for upward earnings revisions in this segment, alongside semiconductor capital-equipment companies.

As AI workloads evolve from model training to large-scale deployment of autonomous agents, networking is increasingly becoming a mission-critical layer of the infrastructure stack. In our view, this remains one of the most compelling opportunities across the AI value chain.

The Bottom Line: What This Means for Investors

The AI opportunity is no longer defined by who has the most capital to deploy—it is increasingly determined by who controls the most constrained resources.

CPUs are entering a major growth inflection and, in our view, remain underappreciated by the market. As AI agents proliferate, demand for orchestration, coordination, and general-purpose compute is set to rise sharply, creating a powerful tailwind for the CPU ecosystem.

Memory has moved from a future thesis to a present reality. Pricing power is already reshaping industry economics, and the market has begun to reflect that shift. However, much of the near-term optimism is now embedded in valuations. Whether memory suppliers deserve a sustained re-rating will ultimately depend on their ability to generate durable cash flows through the next downturn. Until that is proven, we prefer exposure through semiconductor equipment providers rather than the memory manufacturers themselves.

Networking remains our highest-conviction investment theme. As AI systems become increasingly agent-driven, the volume of data moving between machines will grow exponentially, making connectivity infrastructure one of the most critical—and scarce—components of the AI stack. We continue to see the strongest potential for earnings upside in this segment.

The broader takeaway is straightforward: in the agentic era, value accrues to the owners of scarcity. For years, GPUs were the primary bottleneck. Today, the constraints are shifting toward compute orchestration, memory capacity, and network infrastructure. Investors who identify these emerging choke points early will be best positioned to capture the next phase of AI-driven growth.

Although Livermore is not always mentioned in the same breath as renowned investors such as Warren Buffett and Peter Lynch, the lessons he left behind remain remarkably valuable. Notably, many of his principles differ significantly from the investment philosophies championed by Buffett and Lynch.

This contrast largely stems from their differing approaches. Buffett and Lynch are known for their focus on fundamental analysis and long-term value investing, whereas Livermore relied heavily on technical analysis and possessed a deep understanding of market psychology, including both his own behavioral tendencies and those of other investors.

While there is much to learn from the great figures of the investment world, it is important to recognize that no single strategy guarantees success. Every investment approach—whether conservative or aggressive—has its limitations. Livermore’s own career illustrates this reality; despite achieving extraordinary trading success, he ultimately died in financial hardship. Nevertheless, his insights into investor behavior and market dynamics remain highly relevant. With that perspective in mind, we now turn to the next 11 lessons.

Rule 1: Never Sell a Stock Simply Because It Appears Expensive

Rule 1 is essentially the opposite of Rule 10: never avoid a stock merely because it has already risen significantly from previous levels. A company that seems overvalued by traditional metrics may continue to appreciate if its business fundamentals remain strong and investor demand persists.

Valuation measures can help estimate long-term return potential, but they are often poor tools for market timing. Investors should evaluate stocks using multiple metrics rather than relying solely on commonly cited ratios such as P/E. Measures like the PEG ratio and forward P/E can provide additional perspective. A stock’s price alone should never be the sole reason for selling.

History offers many examples. Companies such as Amazon and Apple appeared expensive at various points in their growth cycles, yet continued delivering substantial gains. Selling high-quality businesses solely because they have appreciated can be a costly mistake.

Rule 2: Buy When a Stock Breaks Out After a Healthy Consolidation

Livermore believed investors should enter positions when a stock reaches a new high following a normal and orderly pullback. Such consolidations often indicate that selling pressure has been absorbed and buyers are regaining control of the trend.

A healthy correction differs significantly from a breakdown. The former represents a pause within an existing trend, while the latter may signal a genuine reversal. Distinguishing between these two scenarios is one of the most important skills in technical analysis. According to Livermore, a breakout following orderly consolidation often provides one of the lowest-risk opportunities to join a strong uptrend.

Rule 3: Never Average Down on Losing Positions

Averaging down remains one of the most common—and potentially damaging—investing habits. The reasoning often sounds logical: if a stock was attractive at $50, it should be even more attractive at $40.

In reality, a declining stock may be signaling that the original investment thesis is flawed or that the timing was wrong. Adding more capital to a losing position does not fix the problem; it increases exposure to it. Livermore viewed averaging down as one of the most destructive behaviors a trader can adopt because small losses can quickly become major ones.

Rule 4: Human Nature Is the Investor’s Greatest Enemy

Long before behavioral finance became an established discipline, Livermore recognized that investors frequently act irrationally.

Psychological biases influence nearly every investment decision. Loss aversion encourages investors to hold losing positions for too long. Overconfidence can lead to excessive risk-taking. Anchoring causes people to focus on their purchase price rather than a stock’s current value. Recency bias tempts investors to assume recent trends will continue indefinitely.

While these tendencies cannot be completely eliminated, recognizing them allows investors to build processes and disciplines that help reduce their influence.

Rule 5: Eliminate Wishful Thinking

Wishful thinking begins when hope replaces objective analysis. It occurs when investors stop asking what the market is communicating and instead focus on what they want to happen.

A useful exercise is to periodically evaluate every holding by asking: “If I did not already own this stock, would I buy it today based on the current information and price?” If the answer is no, it may be worth reconsidering the position. Successful investing requires evidence-based decisions, not emotional attachment.

Rule 6: Major Market Moves Require Time

The largest gains in financial markets typically come from trends that develop over months or even years. These trends rarely emerge overnight and often take considerable time to reach their full potential.

Impatience is a common reason investors fail to capture the majority of a trend’s returns. Identifying a strong trend is important, but having the discipline to remain invested while the trend unfolds is equally critical. Often, the biggest profits come not from finding opportunities, but from holding them long enough.

Rule 7: Do Not Obsess Over Every Explanation for Price Movements

Financial news outlets provide explanations for virtually every market move. However, many of these narratives are created after the fact to justify what has already occurred.

Markets frequently move for reasons that are impossible to identify with certainty. Constantly searching for explanations can lead investors toward poor conclusions and unnecessary trading decisions. Livermore believed that price action itself often provides more reliable information than the stories constructed around it. Observing what the market is doing can be more valuable than speculating about why it is doing it.

Rule 8: Following a Few Stocks Is Easier Than Following Many

Diversification has benefits, but excessive diversification can dilute both attention and conviction. When investors own dozens of positions, it becomes increasingly difficult to monitor each one effectively.

Livermore preferred focusing on a relatively small number of leading companies within strong sectors. By concentrating on businesses he understood well, he believed investors could make better decisions and respond more effectively to changing market conditions.

There is an important distinction between diversification as a risk-management tool and diversification as a substitute for thorough research. Owning fewer, well-understood investments may often be more effective than spreading capital across a large number of positions without sufficient analysis.

Rule 9: If You Cannot Profit from Market Leaders, You Are Unlikely to Profit from the Market Overall

In every market cycle, a relatively small group of stocks attracts the majority of investor capital. The growing popularity of passive investing has only reinforced this phenomenon.

If investors struggle to identify and benefit from these leading stocks, generating strong returns from secondary or lagging companies becomes increasingly difficult. For example, investors who avoid high-performing sectors such as technology in favor of weaker-performing areas may miss the primary engines of market gains. This principle underscores the importance of understanding sector leadership and monitoring shifts in market momentum.

Rule 10: Today’s Leaders May Not Be Tomorrow’s Leaders

Market leadership is never permanent. Sectors and investment factors rotate over time, often in dramatic fashion.

History provides countless examples. The “Nifty Fifty” stocks that dominated the early 1970s later fell out of favor. Technology stocks led the market during the late 1990s but underperformed for much of the following decade. Likewise, energy stocks struggled between 2014 and 2020 before becoming some of the market’s strongest performers in 2021 and 2022.

Investors who remain attached to yesterday’s winners risk underperforming in future market environments. Rather than focusing solely on what has worked in the past, successful investors continually evaluate which sectors and themes are most likely to benefit from changing economic and market conditions.

Rule 11: Do Not Let One Stock or Event Shape Your Entire Market View

A single data point does not establish a trend.

One company’s disappointing earnings report does not necessarily indicate weakness across an entire industry. Similarly, one stronger-than-expected inflation reading does not automatically signal the end of a broader disinflationary trend. Even a single bank failure does not guarantee a systemic financial crisis.

Markets are complex systems influenced by numerous variables. Investors often make costly mistakes when they draw sweeping conclusions from isolated events. Effective analysis requires examining a broad range of evidence and identifying consistent patterns before forming a strong bullish or bearish outlook.

Rule 12: Be Skeptical of Tips and “Inside Information”

While the sources of investment advice have evolved since Livermore’s time, the underlying principle remains unchanged.

In Livermore’s era, stock tips were commonly exchanged through personal networks and social gatherings. Today, they spread through social media, online forums, financial influencers, and subscription trading services. Yet the reality remains the same: if a truly exceptional investment opportunity were widely known, its advantage would quickly disappear.

People promoting “guaranteed winners” are often either misinformed, motivated by self-interest, or both. More importantly, investors should avoid relying entirely on someone else’s judgment. External research can be valuable, but investment decisions should ultimately be based on an analytical framework that the investor understands and can evaluate independently.

One of the most effective ways to strengthen investment decisions is to actively study viewpoints that challenge your own assumptions.

Summary

Jesse Livermore experienced extraordinary success and devastating setbacks throughout his career, building and losing multiple fortunes. Personal struggles, including depression and the changing regulatory landscape following the establishment of the U.S. Securities and Exchange Commission in 1934, weighed heavily on him. In 1940, he tragically ended his life, leaving behind a note describing himself as a failure. History, however, remembers him very differently.

What makes Livermore’s legacy remarkable is the enduring relevance of his principles. The markets he traded were vastly different from those of today. Technology, communication systems, market structure, and regulations have all undergone profound transformation. Yet the behavioral tendencies and market dynamics he identified remain strikingly familiar.

More than a century later, Livermore’s lessons on discipline, psychology, trend-following, risk management, and independent thinking continue to offer valuable guidance for investors navigating modern financial markets.

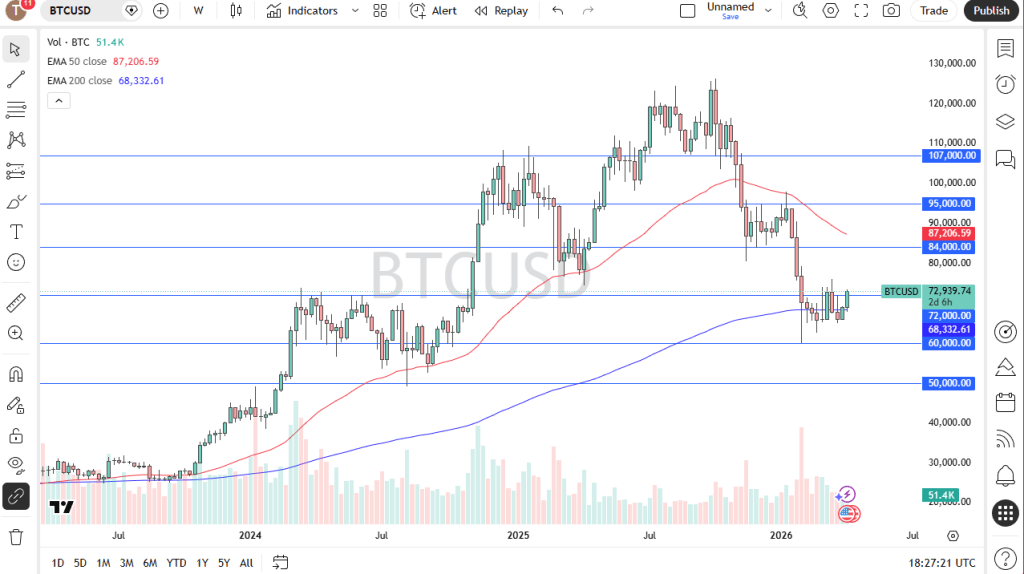

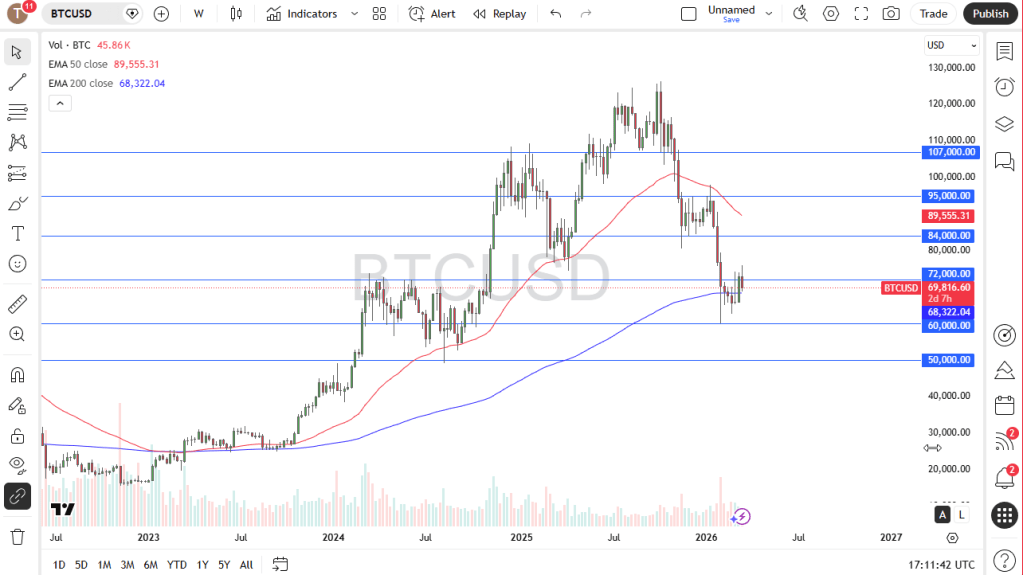

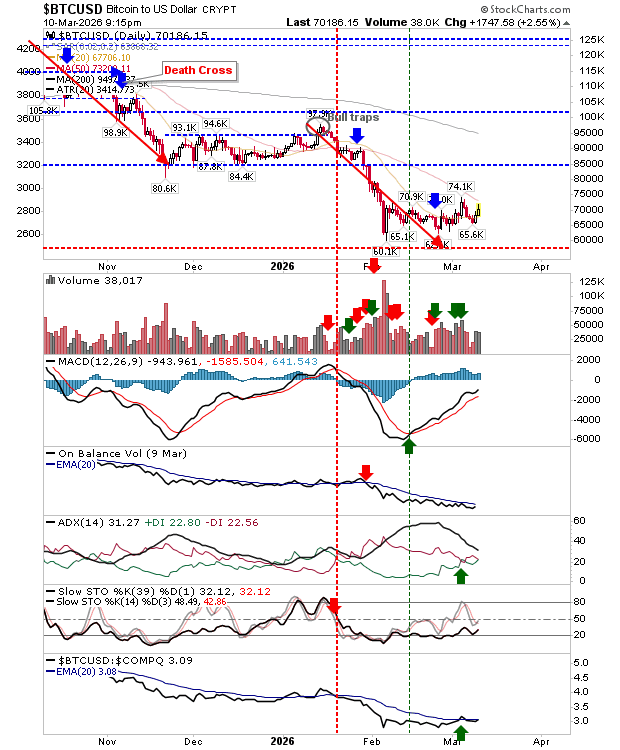

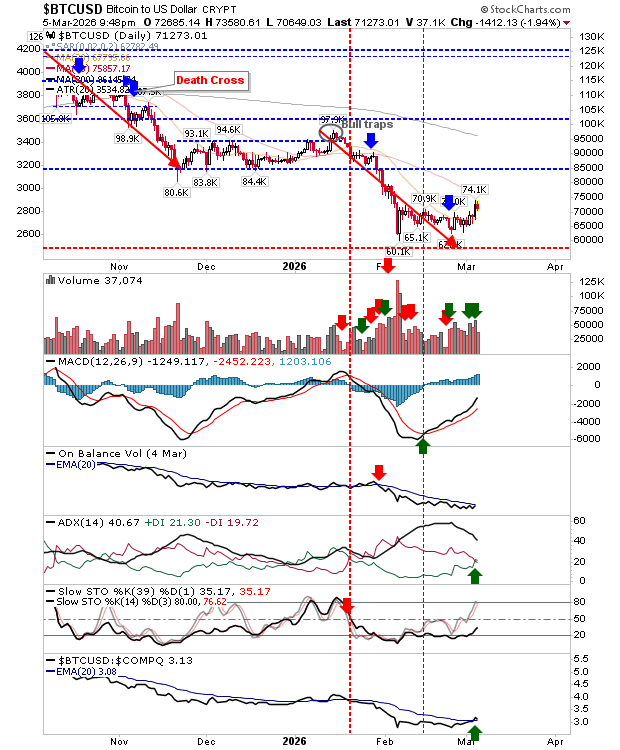

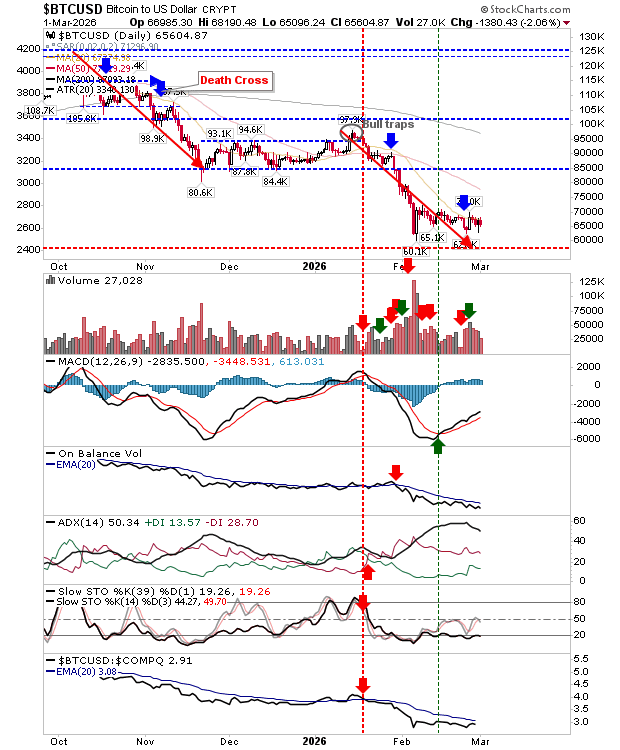

Bitcoin showed a modest recovery over the week, finding support around the $60,000 level and signaling a potential stabilization after its recent decline. However, caution remains warranted, as the cryptocurrency has experienced significant downward pressure and market sentiment is still fragile.

Looking ahead, any upward movement is likely to face resistance from sellers until Bitcoin can establish itself firmly above the $65,000 mark. On the downside, a break below the low of the current weekly candle could trigger renewed bearish momentum, increasing the likelihood of a move toward the $50,000 level.

EUR/USD

EUR/USD traded within a relatively narrow range throughout the week, with the 1.14 level continuing to serve as an important support zone for market participants. Sentiment shifted slightly following a weaker-than-expected U.S. Non-Farm Payrolls report, which prompted investors to scale back expectations of further interest rate hikes by the Federal Reserve.

Despite this development, the broader outlook remains uncertain. A break below the previous week’s low could accelerate bearish momentum and pave the way for a decline toward the 1.12 level. On the upside, any recovery attempts should be approached cautiously until the pair can convincingly move above 1.15, ideally supported by a daily close above that threshold.

NZD/USD

NZD/USD posted solid gains for most of the week, although the pair began to lose momentum on Friday, suggesting that bullish sentiment may be fading. If the U.S. dollar strengthens broadly in the coming sessions, the New Zealand dollar could be among the currencies most vulnerable to a reversal.

The pair has remained trapped within a long-standing trading range, while New Zealand’s monetary policy outlook differs from that of several other major economies. The central bank has maintained a relatively less hawkish stance, which could limit the kiwi’s upside potential. Given these factors, bearish opportunities may emerge if further signs of weakness develop. Additionally, Friday’s price action resembles a shooting star candlestick pattern, often viewed as a warning of potential downside pressure, making it a technical signal worth monitoring closely.

USD/CAD

USD/CAD traded largely sideways throughout the week, reflecting a period of consolidation after recent moves. While the pair may appear somewhat stretched in the short term, price action is likely to remain volatile given the close economic relationship between the United States and Canada.

Although the latest U.S. employment data came in weaker than expected, broader fundamentals continue to support the U.S. dollar. At the same time, concerns over the Canadian economy’s performance may limit the Canadian dollar’s strength. As a result, any near-term pullback in USD/CAD could present buying opportunities, particularly if the pair declines toward the key 1.40 support area, where demand may re-emerge.

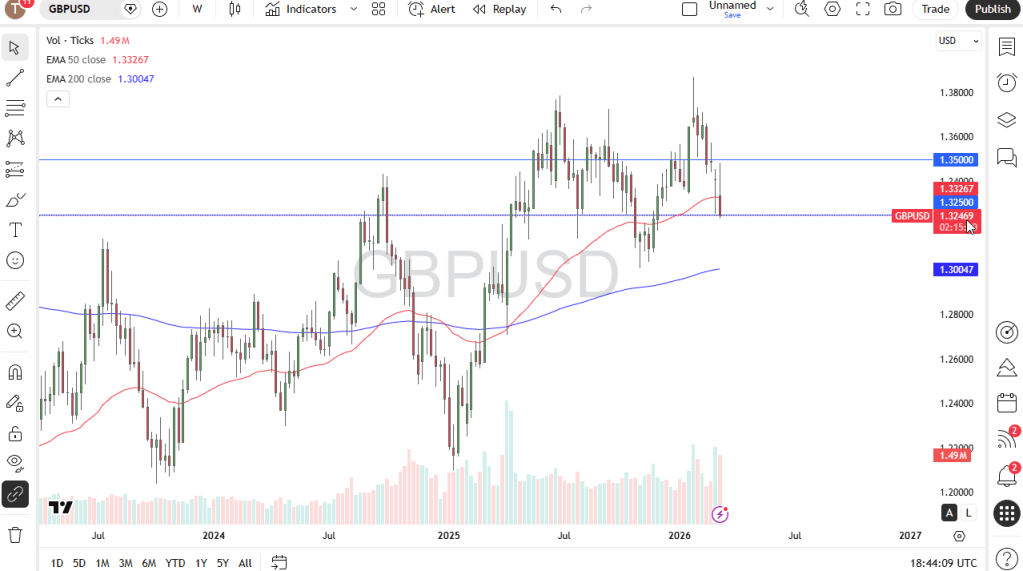

GBP/USD

GBP/USD delivered a strong performance during the week, advancing above the 1.33 level and testing the 50-week Exponential Moving Average (EMA). A decisive break above this week’s high, near 1.34, could reinforce bullish momentum and pave the way for a move toward the 1.35 area.

The pair has spent an extended period trading within a range, making the recent recovery a relatively natural development. The British pound has also demonstrated greater resilience against the U.S. dollar compared with several other major currencies. Should the U.S. dollar come under renewed selling pressure, sterling could emerge as one of the primary beneficiaries. Conversely, even if the dollar regains strength, the current market structure offers little incentive for a bearish outlook on GBP/USD, as the pair continues to show underlying support and positive momentum.

Silver

Silver experienced considerable volatility throughout the week, with price action remaining choppy and directionless. The $60 level continues to act as a key psychological resistance zone, creating a significant hurdle for any sustained upward movement.

Despite periodic rebounds, the broader technical picture remains cautious following the recent formation of a new swing low. This suggests that rallies may continue to face selling pressure, particularly if bullish momentum begins to fade. From a technical perspective, the 50-week Exponential Moving Average (EMA), currently near $64.36, represents an important resistance area and may serve as the primary upside barrier in the near term. Until silver can break convincingly above this level, the market is likely to remain vulnerable to further downside pressure.

Gold

Gold has shown signs of improvement over the past several weeks, with prices recovering and attempting to build a stronger foundation. The market is now approaching the 50-week Exponential Moving Average (EMA), a key technical level that could determine the next major move. A successful breakout above this resistance may strengthen bullish momentum and open the door for a rally toward the $4,400 level.

On the downside, a decline below the $3,900 support zone would likely weaken the outlook and increase the risk of a deeper correction toward $3,500. Overall, gold appears to be in the process of establishing a long-term bottom, although confirmation is still needed. Traders should continue to monitor the performance of the U.S. dollar, as further dollar weakness could provide additional support for gold prices and enhance the prospects for a sustained recovery.

The Nasdaq 100

The Nasdaq 100 advanced for most of the week, continuing to reflect the market’s underlying strength. However, trading activity was shortened due to the market closure on Friday, which slightly distorts the weekly candlestick. Additionally, Thursday’s session was heavily influenced by the release of the U.S. Non-Farm Payrolls report. While the data came in weaker than expected, the impact does not appear severe enough to significantly alter the broader market outlook.

Looking ahead, the index may enter a period of consolidation following its substantial gains over the past several months. Rather than expecting an immediate continuation of the rally, a sideways trading phase could help absorb recent gains and establish a stronger foundation for future advances. Within this context, short-term pullbacks may present attractive buying opportunities, as the longer-term trend remains constructive and investor sentiment continues to favor equities.

Gold started the previous week with a noticeable gap lower, highlighting the market’s ongoing uncertainty and elevated volatility. Price fluctuations are likely to remain significant in the near term as traders continue to react to various external factors.

The $4,000 level remains a key support zone. As long as gold stays above this threshold, short-term pullbacks could present buying opportunities. However, a decisive break below $4,000 may trigger a deeper correction, potentially sending prices toward the $3,500 area.

On the upside, a move above the 50-week EMA would strengthen the bullish outlook and could pave the way for a rally toward $4,600. That said, gold continues to be influenced by a range of macroeconomic and geopolitical developments, making its direction less predictable.

For now, the most likely scenario may be a period of consolidation, with prices trading within a broad range while the market searches for its next major catalyst.

EUR/CHF

The euro declined notably against the Swiss franc over the past week, yet the 0.92 level continues to serve as an important support area. A rebound from this zone would not be surprising, as the pair appears to be searching for enough momentum to resume a move higher, potentially targeting a break above 0.93.

In the near term, buying on a bounce remains an attractive strategy, especially if support at 0.92 continues to hold. However, if the pair falls decisively below this level, downside pressure could intensify, opening the door for a move toward 0.91.

Overall, EUR/CHF may remain range-bound in the short run, with traders closely watching whether support at 0.92 can sustain another upward attempt.

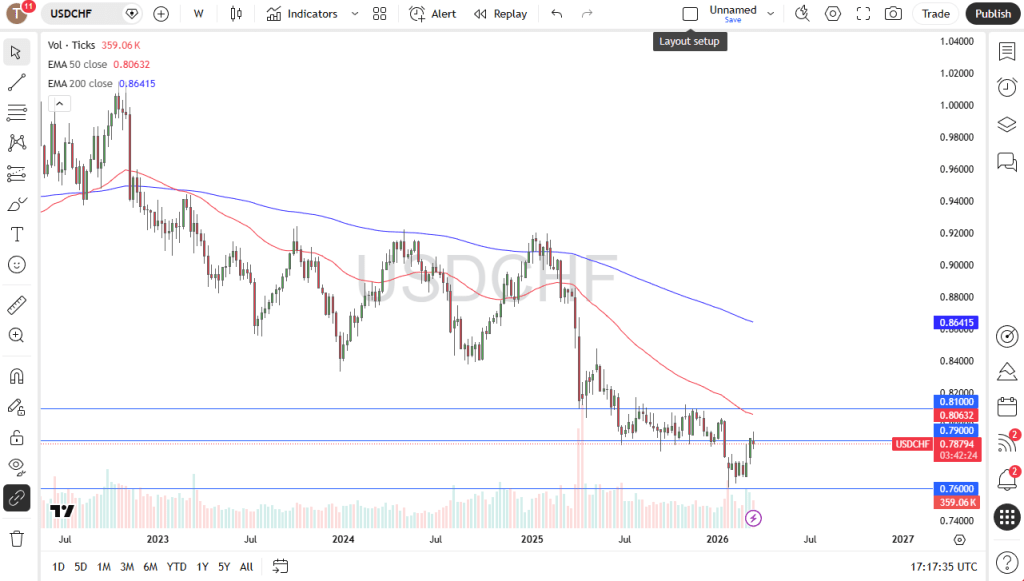

USD/CHF

The U.S. dollar posted gains against the Swiss franc during the week, but a significant portion of those advances was later erased. This price action suggests that the pair may be due for a corrective pullback after its recent rally.

The 0.80 level stands out as a key area to watch. A retreat toward this support zone could provide a potential buying opportunity if the market shows signs of stabilization and renewed bullish momentum. Traders may look for a bounce from this level as confirmation of a possible continuation higher.

On the upside, a breakout above the high of the current weekly candlestick would strengthen the bullish outlook and could lead to a test of the 0.82 level.

Overall, the short-term bias remains cautiously positive, although a pullback toward support may be needed before the next leg higher can develop.

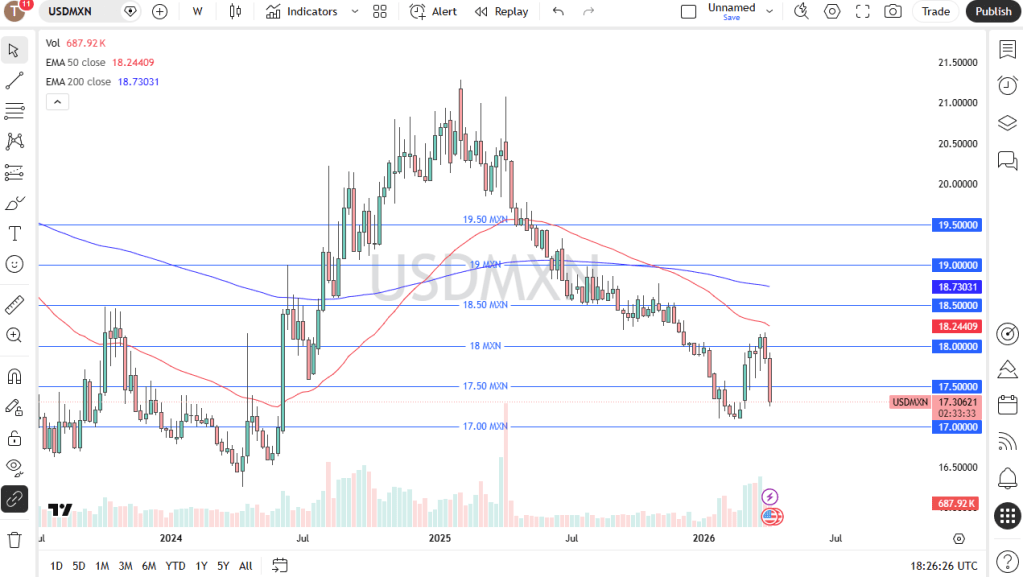

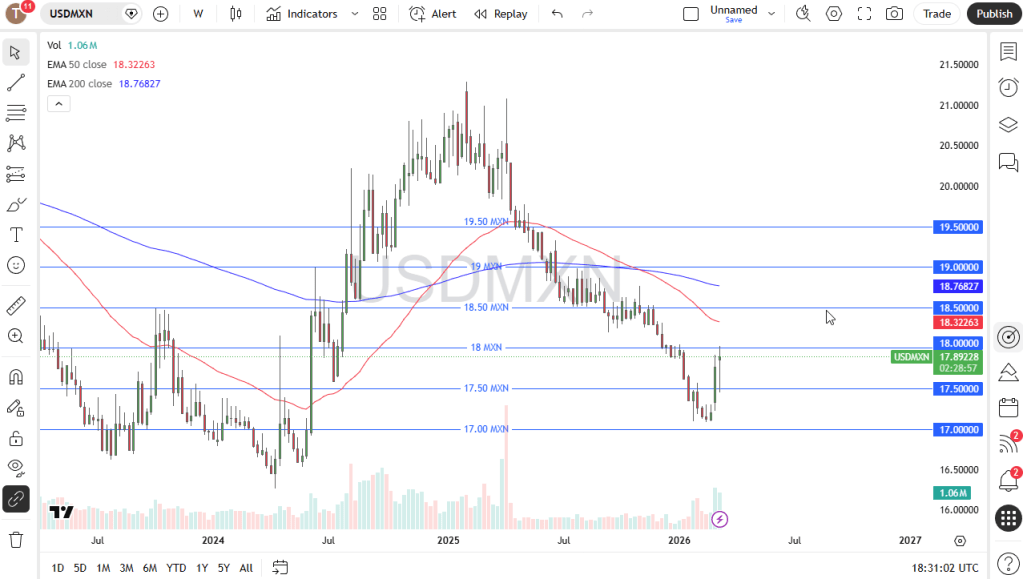

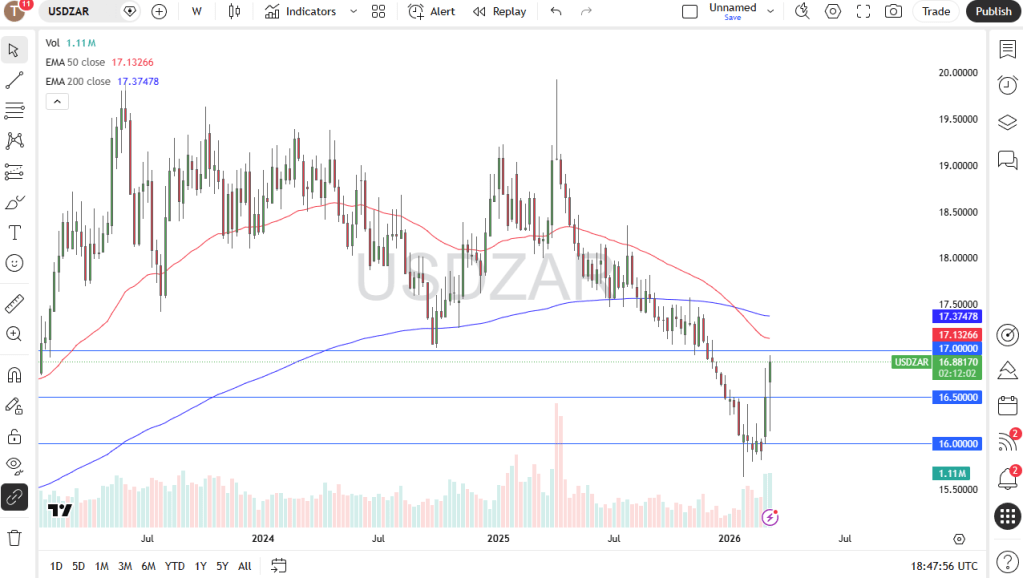

USD/MXN

The U.S. dollar advanced against the Mexican peso during the week, but the 17.50 level once again proved to be a strong area of resistance. The subsequent pullback from those highs is not particularly surprising and suggests that the pair may continue trading within its established consolidation range.

Looking ahead, USD/MXN is likely to remain volatile and range-bound as traders assess the next directional catalyst. While occasional swings above or below recent levels are possible, the broader price action continues to favor consolidation rather than the start of a sustained trend.

Even if the U.S. dollar manages to break decisively higher against the Mexican peso, the move may not offer an attractive trading opportunity given the pair’s tendency to remain choppy and unpredictable. For now, traders may be better served by focusing on short-term range dynamics rather than chasing a potential breakout.

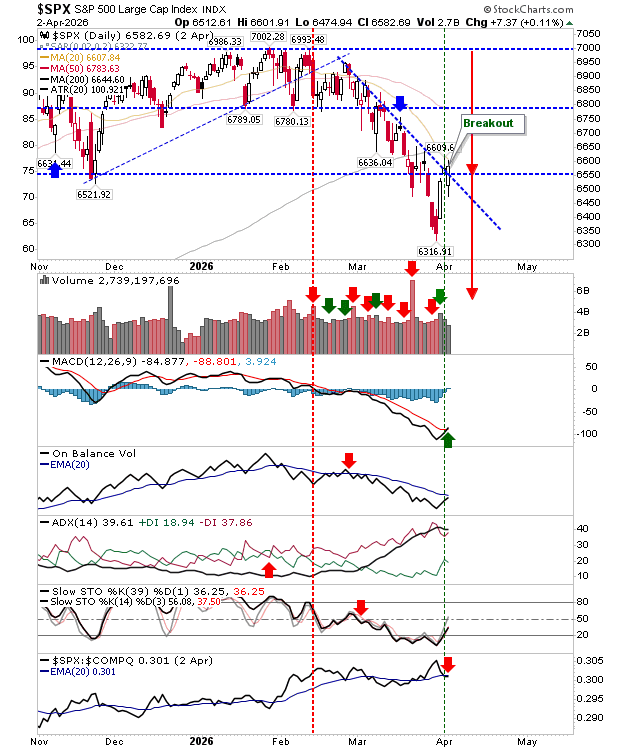

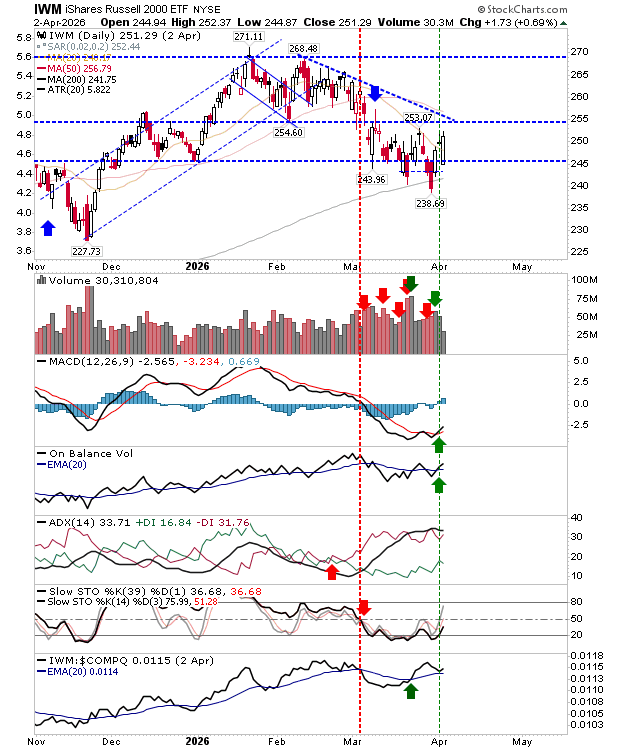

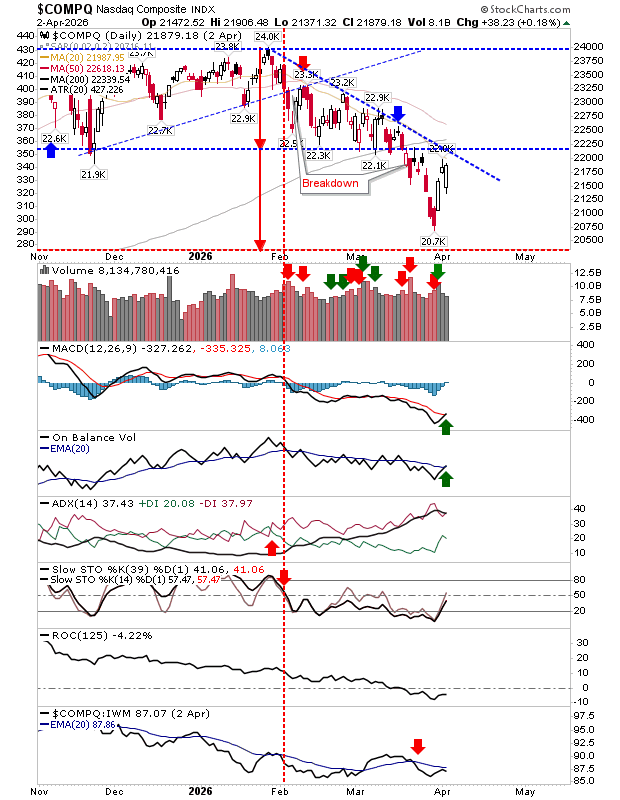

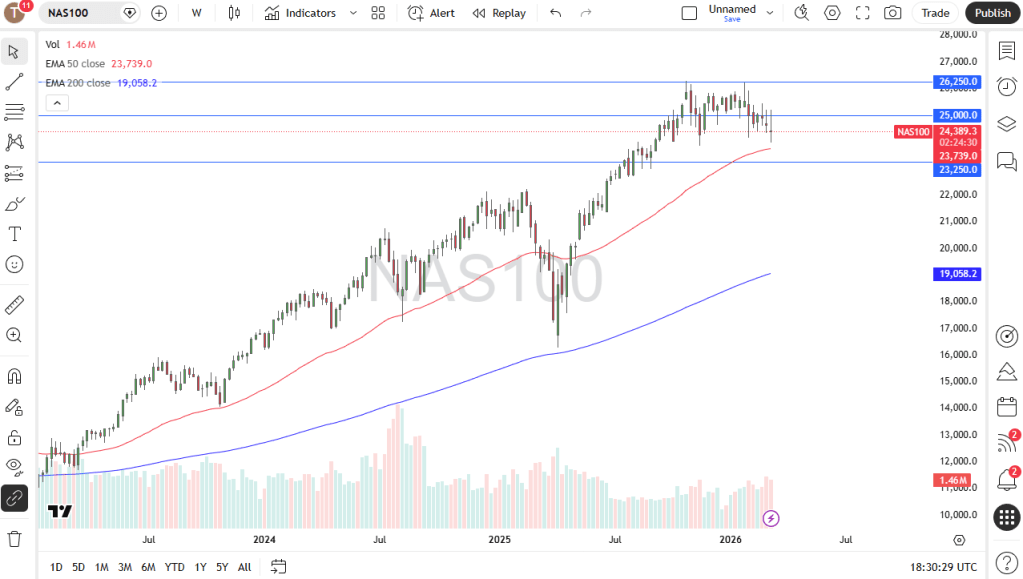

Nasdaq 100

The Nasdaq 100 moved lower throughout the week, but the broader picture suggests that the index is simply consolidating after an extended rally. Recent weakness appears to be a healthy pause as the market works off some of the excess optimism and overbought conditions that developed earlier.

Despite the pullback, the longer-term outlook remains constructive. Buyers are likely to re-emerge over time, although current market conditions do not necessarily justify taking large positions. The index may continue to trade within a range while investors assess economic data, corporate earnings, and monetary policy expectations.

Short-term declines could present attractive buying opportunities, particularly if prices approach the 28,500 level, which may act as a significant support area. For now, the focus remains on identifying value during pullbacks rather than betting against the broader uptrend.

Overall, the bias remains cautiously bullish, with dip-buying favored over short-selling.

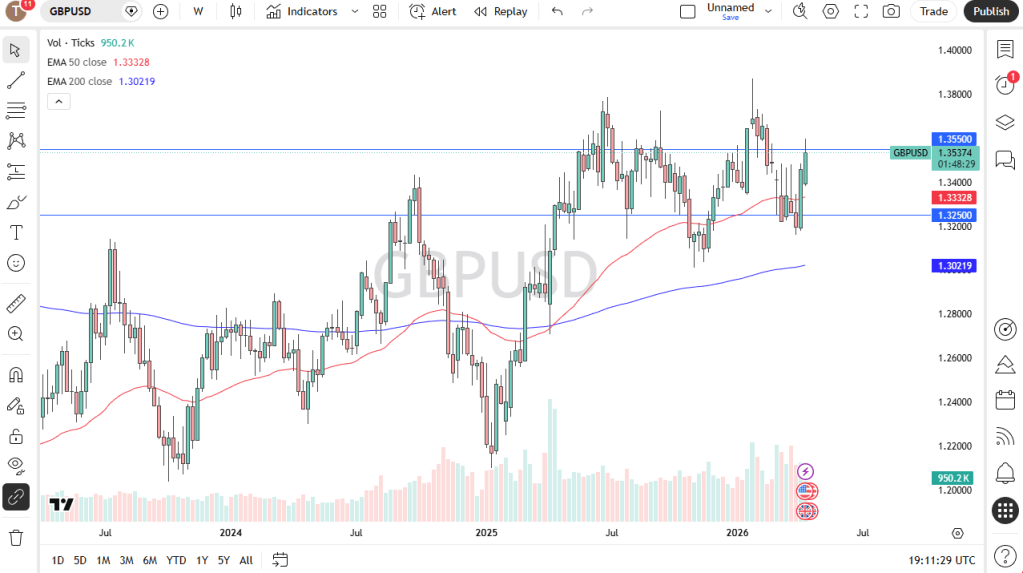

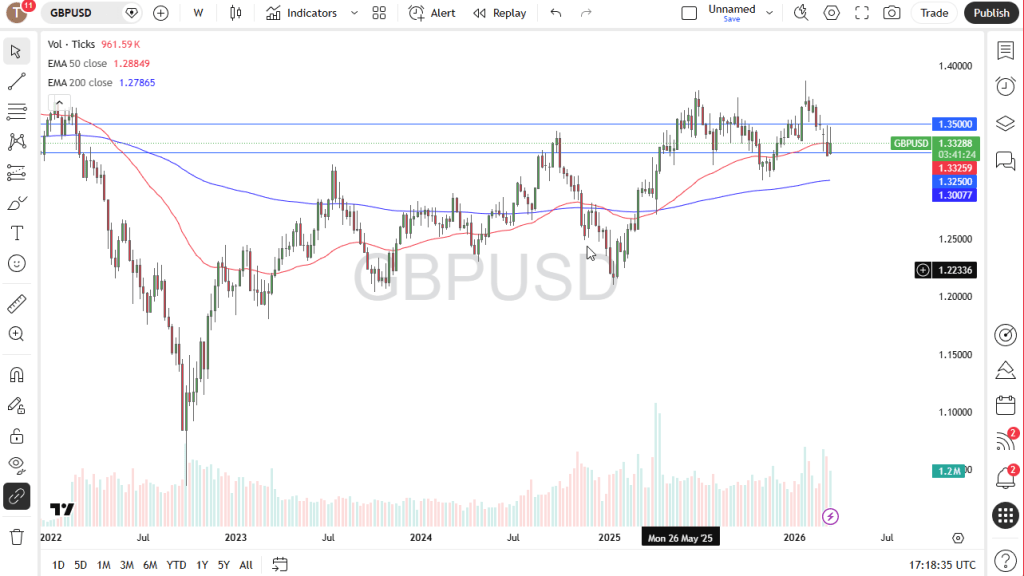

GBP/USD

The British pound posted a modest recovery against the U.S. dollar during the week, with the 1.32 level continuing to establish itself as an important support zone. The market’s ability to hold above this area suggests that buyers remain active and willing to defend the pair on pullbacks.

On the upside, the 1.33 level remains a key resistance barrier. A successful move above this threshold would strengthen bullish sentiment and could pave the way for a further advance toward the 1.35 level.

In the near term, GBP/USD is likely to remain range-bound between support at 1.32 and resistance at 1.33 as traders wait for a stronger catalyst. However, a breakout above the upper boundary of this range could signal the start of a more sustained upward move.

Overall, the outlook remains cautiously positive, with the potential for additional gains if buyers can push the pair decisively above 1.33.

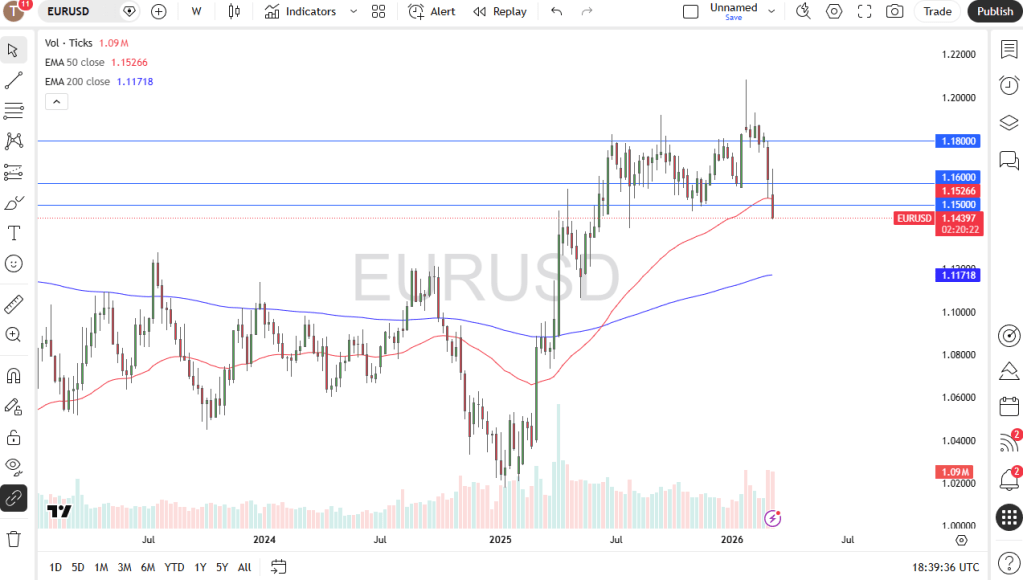

EUR/USD

The euro experienced a notable decline against the U.S. dollar during the week but managed to recover and return to the 1.14 area. This level has served as a major short-term support zone for much of the past year, making current price action particularly important for determining the pair’s next direction.

After briefly breaking below 1.14, the market has rebounded to retest this key level. Traders will be watching closely to see whether it acts as resistance following the breakdown or if buyers can regain control and push the pair higher.

A sustained move above 1.1450 would improve the bullish outlook and could encourage additional buying interest in the euro. However, there is also a strong possibility that EUR/USD remains anchored around the 1.14 level while the market searches for a clearer catalyst.

Ultimately, the pair’s direction may depend less on euro-specific factors and more on the broader performance of the U.S. dollar. As a result, developments in U.S. economic data, interest rate expectations, and overall dollar sentiment are likely to play a decisive role in shaping EUR/USD’s next major move.

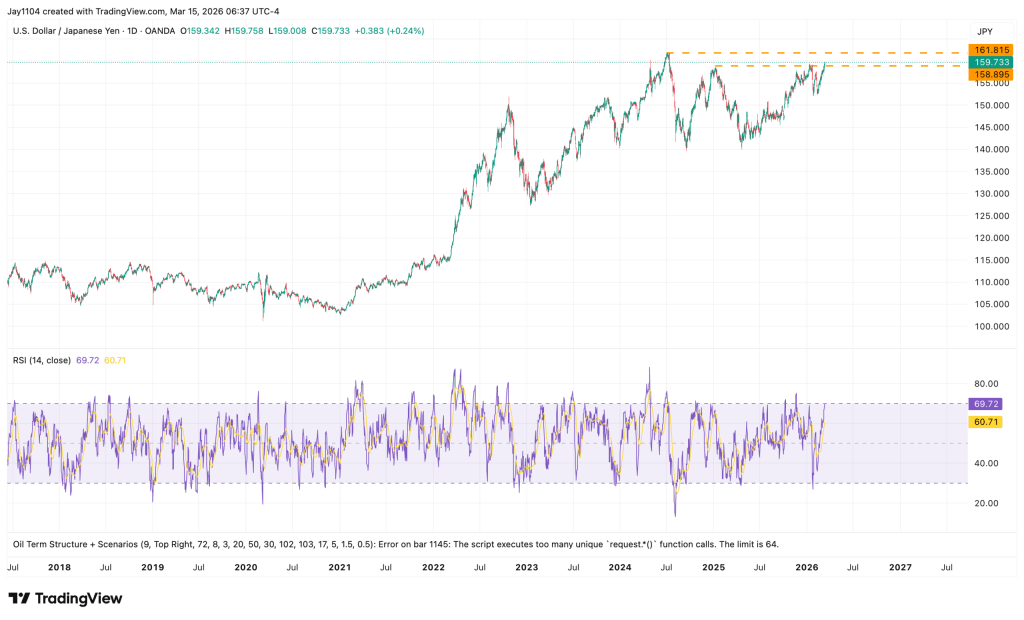

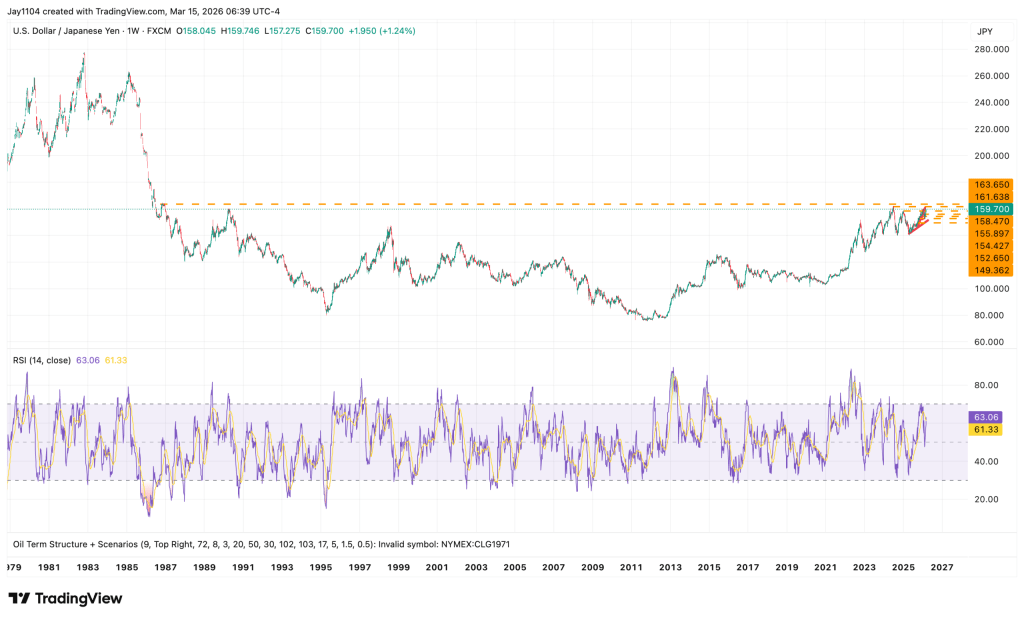

USD/JPY

The U.S. dollar continued its gradual advance against the Japanese yen during the week, maintaining the bullish momentum established by recent breakouts. As a result, USD/JPY remains one of the key currency pairs to watch in the current market environment.

The 162.00 level represents an important resistance zone. A decisive break above this threshold could signal the continuation of the broader uptrend and open the door to further gains for the U.S. dollar.

While Japanese authorities have recently intervened in the currency market to support the yen, the underlying fundamentals still appear favorable for USD/JPY. In particular, the significant interest rate differential between the United States and Japan continues to attract investors toward the pair.

Short-term pullbacks may therefore present buying opportunities, especially if prices retrace toward the key 160.00 level, which is likely to act as an important support area. As long as this zone holds, the overall bullish bias remains intact.

Overall, the outlook continues to favor the upside, with traders closely monitoring whether USD/JPY can break through 162.00 and extend its recent rally.

The US dollar strengthened against the Japanese yen for most of the week, extending the broader bullish trend that has dominated the pair in recent months. As long as this momentum remains intact, traders are likely to view pullbacks as buying opportunities rather than signs of a reversal.

The ¥160 level may provide initial support in the near term. If the pair falls below that threshold, additional support could emerge around ¥158, where buyers may step in once again.

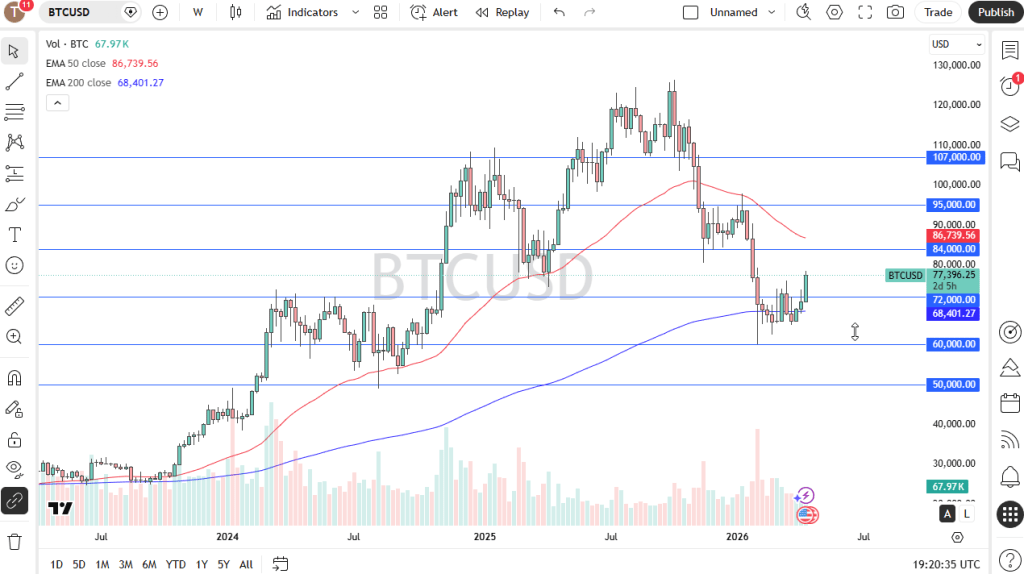

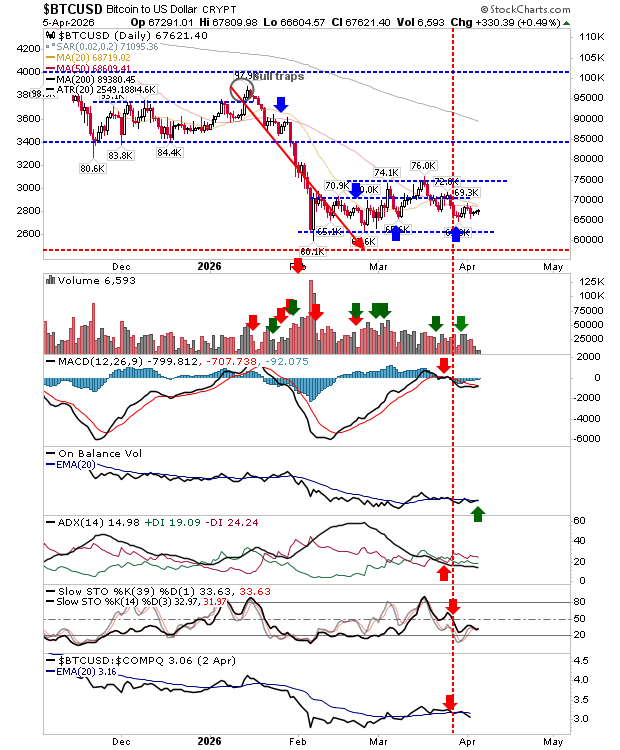

Bitcoin

Bitcoin moved lower during the week, but the cryptocurrency continues to find support around the key $60,000 level. This area remains an important technical floor for the market, and traders will be closely watching whether buyers can defend it in the coming sessions.

A decisive break below $60,000 could trigger additional selling pressure, potentially opening the door for a decline toward the $50,000 level, which represents the next major support zone.

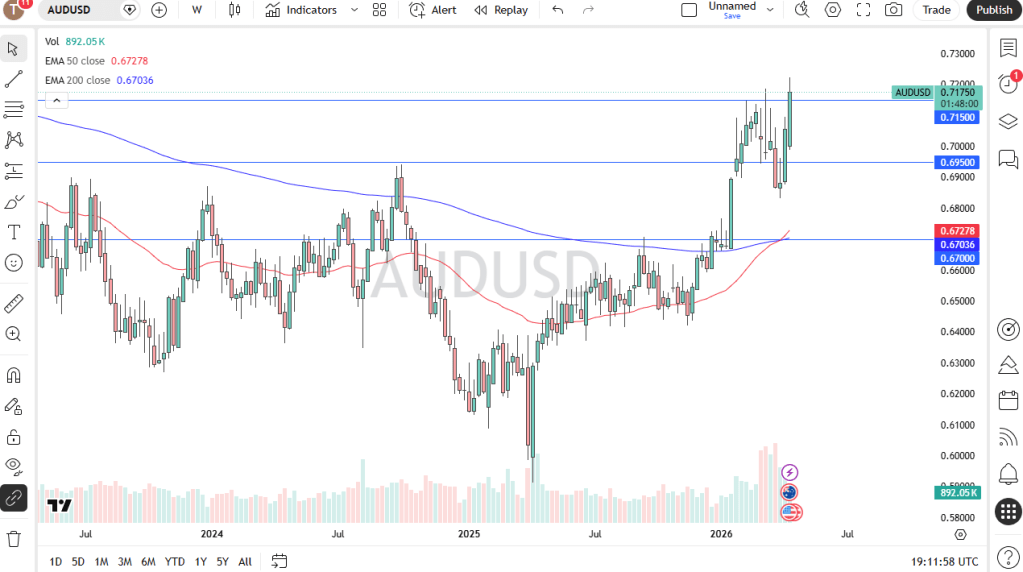

AUD/USD

The Australian dollar attempted to move higher during the week but struggled to maintain its gains, with the market retreating and signaling a degree of underlying weakness. Despite the pullback, the pair remains confined within a well-defined trading range.

The 0.6950 level continues to serve as a key support zone, while 0.7150 remains a significant resistance area. As long as these boundaries hold, AUD/USD is likely to remain range-bound, with traders looking for opportunities at the extremes of the range.

USD/MXN

The US dollar advanced against the Mexican peso during the week, but the pair continues to encounter strong resistance around the 17.50 level. This area has repeatedly attracted selling interest and remains a key barrier for further upside momentum.

A sustained break above 17.50 could signal a shift in market sentiment and pave the way for a move toward the 18.00 peso level, which would become the next major upside target.

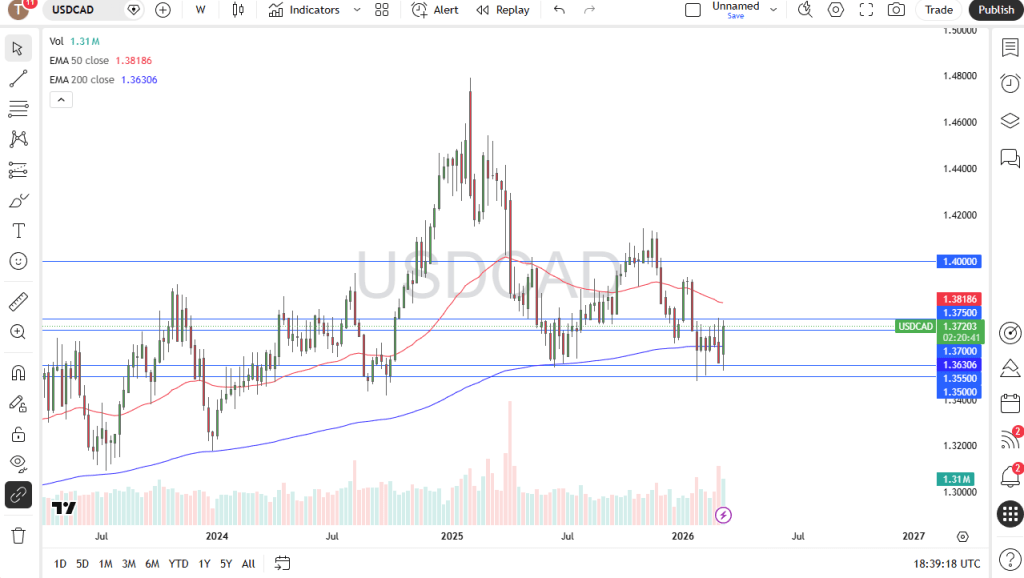

USD/CAD

The US dollar strengthened significantly against the Canadian dollar during the week, supported by growing concerns that the Canadian economy is losing momentum. Signs of slowing economic activity and increasing recession risks have weighed on the Canadian dollar, helping to drive USD/CAD higher.

As economic conditions in Canada remain challenging, the US dollar could continue to benefit from its relative strength, particularly if investors favor safer and higher-yielding assets.

Nasdaq 100

The Nasdaq 100 posted solid gains over the course of the week, reflecting the strong bullish sentiment that continues to support the technology-heavy index. Although the market opened with a gap higher on Monday, prices later pulled back to fill that gap before resuming their upward trajectory.

The successful rebound following the gap fill suggests that buyers remain firmly in control, reinforcing the positive outlook for the index.

Gold

Gold spent most of the week under pressure, although the broader market remained relatively stable as prices continued to hold above the critical $4,000 support level. This area has become a key battleground between buyers and sellers and is likely to determine the next major directional move.

A sustained break below $4,000 could signal a significant shift in market sentiment and potentially mark the beginning of a new bearish phase. For now, however, buyers appear willing to defend this important support zone.

Silver

Silver continued to trade in a volatile and directionless manner during the week, with prices hovering around the 50-week Exponential Moving Average (EMA). Similar to gold, the metal appears to be stuck in a broad consolidation phase, lacking the momentum needed to establish a sustained trend.

The market is currently positioned between two major technical levels: $60 on the downside and $70 on the upside. These boundaries have become the primary areas to watch for the next significant breakout.

The market had a shaky start to the week but managed to stage a respectable recovery following last week’s sharp selloff. Most of the rebound came on Thursday after reports suggested that the US and Iran could be moving closer to another agreement, a development that has resurfaced repeatedly since March. Whether a deal is ultimately finalized or not, investors continue to react positively whenever such headlines emerge, and that response itself remains significant. By Friday’s close, the S&P 500 had edged slightly above where it finished the previous week.

However, the index remains capped by its 10-day and 20-day exponential moving averages, both of which are currently acting as resistance. Additional technical barriers sit just above these levels, suggesting that the market still faces challenges before a more convincing upside breakout can occur.

From a positioning perspective, the market has drifted back into slightly positive gamma, meaning dealer hedging is once again acting as a stabilizer rather than a source of amplification. However, the signal is still relatively weak. If we see another pullback next week, that setup could quickly shift back into negative gamma, where hedging flows would start to reinforce price moves and potentially accelerate downside — a dynamic that helped fuel Thursday’s rebound.

In a positive gamma environment, price action tends to gravitate toward “pinning” rather than trending. With monthly options expiring on Thursday the 18th (and markets closed on Friday the 19th for the holiday), and a meaningful amount of gamma set to roll off into expiry, conditions point toward a potentially quieter, more range-bound week ahead.

The key event next week is the Fed meeting on Wednesday, and there’s a risk the market may be caught leaning the wrong way if the tone comes in more hawkish than expected.

It helps to put the starting point in context. At the March meeting under Chair Powell, the FOMC’s dot plot showed a median policy rate of about 3.4% for 2026, with the easing cycle flattening out near 3.1% into early 2027.

Since then, markets have moved meaningfully higher in their rate expectations. Fed funds futures are now pricing roughly 3.80% for 2026, 3.90% for 2027, and about 4.05% for 2028. In effect, that shift has largely erased the earlier assumption of continued rate cuts and instead leans toward a more restrictive long-run stance, even introducing a subtle tilt toward the possibility of hikes.

Against that backdrop, the focus will be on whether the Fed updates its messaging to match this repricing. A key risk is a removal of any remaining easing bias, along with a rhetorical shift away from emphasizing labor market softness and back toward inflation persistence.

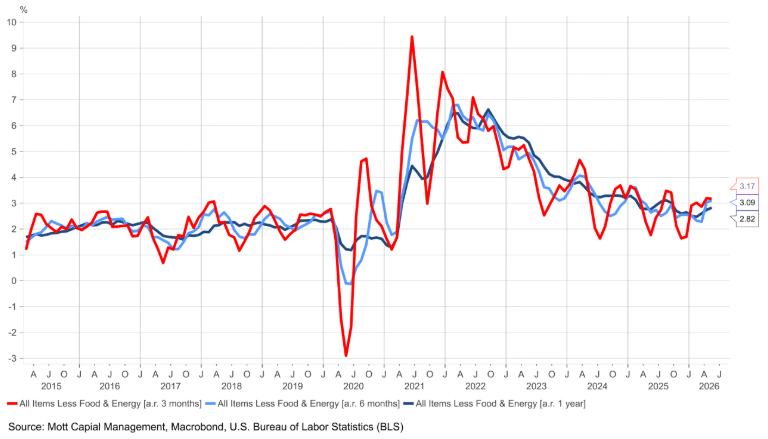

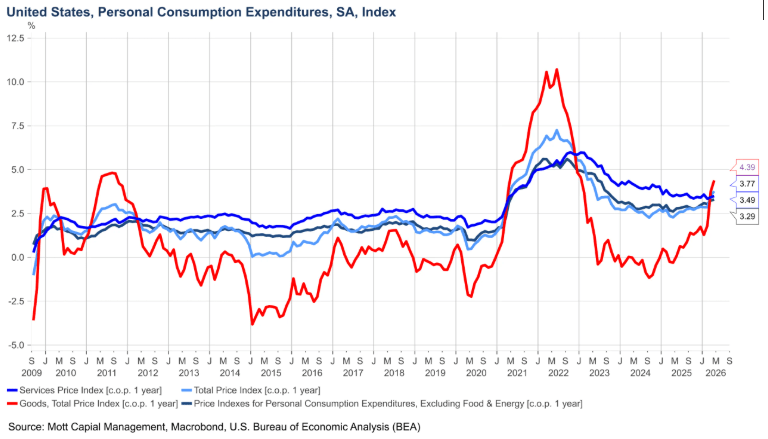

Inflation has also become more interesting lately because it’s no longer just an energy-driven story.

Core CPI, which strips out food and energy, is running at roughly 3.1%–3.2% on a three- and six-month annualized basis, and about 2.8% year over year. That implies the headline annual figure may continue edging higher unless monthly momentum clearly cools in the near term.

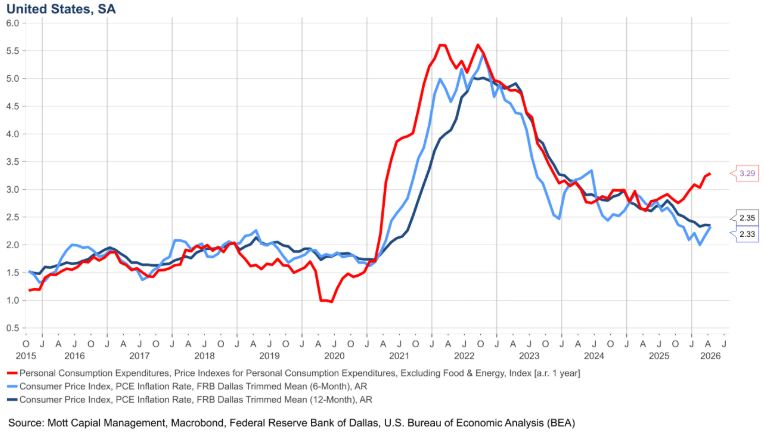

Core PCE — the Fed’s preferred inflation measure — is showing a similar pattern. It’s tracking around 3.8% on a three- and six-month basis and about 3.3% year over year, reinforcing the idea that underlying inflation remains sticky even without the volatility from energy prices.

Even measures designed to strip out outliers are now pointing in the same direction. Trimmed mean PCE — an alternative inflation gauge that excludes the most extreme monthly price moves and has been highlighted by figures such as Kevin Warsh — is running around 2.3%. Meanwhile, the Cleveland Fed’s trimmed mean CPI sits closer to 2.9%.

The historical context matters here. In 2021, trimmed-mean measures lagged the acceleration in inflation, while core PCE moved higher earlier and ultimately peaked first. In contrast, during 2019–2020, relying on trimmed-mean data alone would not have justified the rate cuts that eventually came.

The current setup suggests this is not purely an energy-driven story. If inflation were mainly about oil, it would be harder to explain why core measures are still elevated on both three- and six-month annualized bases, especially given that oil’s move only really began in March.

A key contributor appears to be goods inflation. After previously running negative, goods prices have swung back to roughly 4.4% year over year, and that reversal is now feeding through into broader inflation readings.

At the same time, the labor market is starting to show signs of turning. The ratio of job openings to unemployed workers has moved back above one and has been trending with higher highs and higher lows since December. Broader indicators — including payroll data, ADP figures, and Revelio Labs — are broadly aligned, suggesting the labor market likely bottomed out in late autumn and is now gradually firming.

That shift gives the Fed more flexibility to pivot its attention away from employment concerns and back toward inflation. Against that backdrop, it wouldn’t be surprising if the updated dot plot on Wednesday reflects a slightly lower unemployment path alongside higher inflation projections for both this year and next.

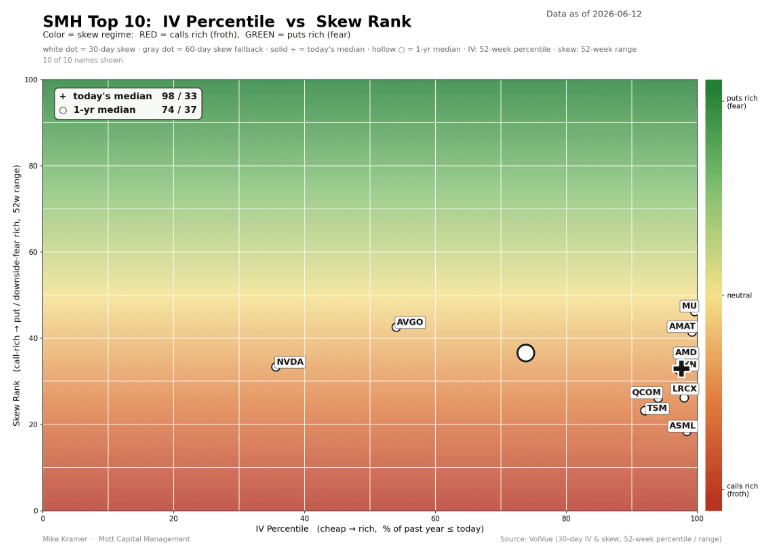

On equities, the semiconductor complex still hasn’t fully reset. Implied volatility across the group remains near the upper end of its one-year range, and positioning in options is still skewed toward calls. Even after Broadcom and NVIDIA pulled back following Broadcom’s results, names like Micron have kept overall volatility elevated.

At the same time, dispersion remains wide — the gap between single-stock volatility and index-level volatility is still pronounced — and implied correlations are still low. In other words, single-stock volatility is elevated while index volatility remains relatively contained, and that relationship hasn’t fully normalized despite the sharp selloff over the past couple of weeks.

“Space: the final frontier…” is the iconic opening narration of the long-running sci-fi series Star Trek, celebrating humanity’s drive to explore the unknown and venture beyond familiar boundaries.

On Friday, Elon Musk achieved a milestone that would have seemed equally futuristic: becoming the world’s first trillionaire. The IPO of SpaceX was a resounding success, raising $75 billion, with the stock surging 19% on its first day of trading. Despite being the largest IPO on record, it represented only a small fraction of the roughly $74 trillion market capitalization of the Wilshire 5000.

While congratulating Musk on this remarkable accomplishment, we would offer a few suggestions. First, the case for establishing a human presence on Mars remains debatable, given the immense costs and limited practical benefits currently on offer. Second, locating data centers beneath the ocean may prove more efficient than placing them in orbit, as installation, maintenance, and repairs would be significantly easier to manage. Orbital facilities would also face ongoing risks from space debris.

Finally, we would suggest that Tesla consider expanding its lineup with a hybrid vehicle, a move that could help strengthen demand and broaden its customer base.

Fueling the enthusiasm surrounding SpaceX’s blockbuster debut on Friday was growing optimism that the United States and Iran could soon reach a memorandum of understanding (MOU). Whether the agreement ultimately delivers meaningful progress remains uncertain, and skeptics may view it as a potential “memorandum of misunderstanding.” Even so, the prospect of easing geopolitical tensions helped push Brent crude prices lower, with the global benchmark settling at $87.33 per barrel on Friday. Iranian officials, however, indicated today that they would not be ready to sign the agreement on Sunday as previously anticipated.

Additional downward pressure on oil prices came from reports that the US military is escorting vessels carrying roughly 7 million barrels per day of crude oil and refined fuel products through the Strait of Hormuz. According to Chris Wright, the operation is intended to ensure the uninterrupted flow of energy supplies through one of the world’s most critical maritime chokepoints. This development has eased concerns about potential supply disruptions and contributed to the recent decline in crude prices.

The prospect of easing tensions in the Middle East also provided a modest boost to Wall Street on Friday, helping both the S&P 500 and Nasdaq edge higher. Importantly, each index found support at its respective 50-day moving average, reinforcing the resilience of the broader uptrend.

The market’s powerful advance continues to be driven by what might be called fabulous earnings momentum (FEMO). Analysts have become increasingly optimistic about corporate profitability, with consensus forecasts for long-term earnings growth (LTEG) climbing to an annualized 24.0% over the next five years during the week ending June 12.

That figure marks a new record high and stands at roughly double the historical average since 1985. Such expectations reflect extraordinary confidence in the earnings outlook, fueled by themes such as artificial intelligence, automation, and productivity gains.

Yet there is also reason for caution. Sustaining earnings growth at that pace for five consecutive years would be an exceptional achievement by historical standards. In that sense, the forecast may prove almost as ambitious as Elon Musk’s vision of establishing a human colony on Mars. Investors are currently pricing in a remarkably optimistic future, one that leaves little room for disappointment if corporate earnings fail to keep pace with expectations.

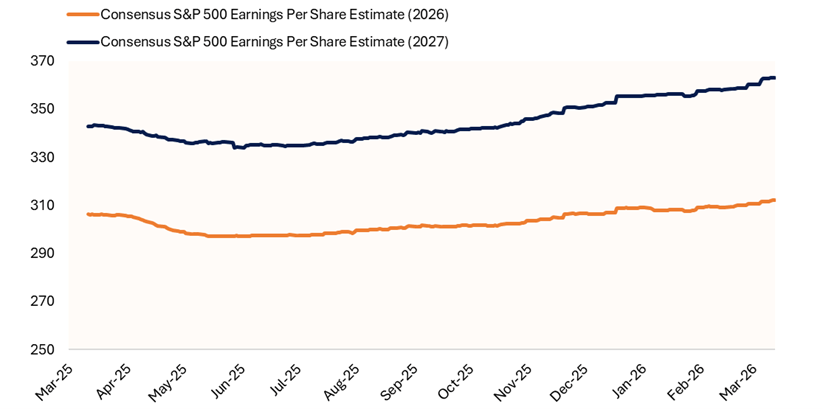

A more grounded measure of the market’s earnings outlook is the S&P 500 forward earnings per share (EPS), which climbed to another record high last week. The forward EPS estimate now stands at $366.92, representing a time-weighted blend of analysts’ current consensus forecasts for 2026 EPS of $340.39 and 2027 EPS of $397.87.

While these projections are less ambitious than the market’s lofty long-term earnings growth expectations, they still imply a notably strong profit outlook for corporate America. Indeed, the consensus forecasts remain well above our own estimates of $330 for 2026 and $375 for 2027, suggesting that Wall Street analysts continue to anticipate robust earnings expansion over the next two years.

The gap between consensus estimates and more conservative forecasts highlights the degree of optimism currently embedded in equity valuations. As long as earnings continue to surprise to the upside, investors may remain willing to support elevated stock prices. However, the higher expectations rise, the greater the risk of disappointment if corporate profit growth fails to match the market’s bullish assumptions.

In any case, fabulous earnings momentum (FEMO) is no longer confined to large-cap stocks. The trend is spreading across the broader market, with forward earnings estimates for the S&P 500, S&P MidCap 400, and S&P SmallCap 600 all surging to fresh record highs in recent weeks.

This broad-based improvement in earnings expectations is an encouraging sign for equity bulls, as it suggests that profit growth is expanding beyond a handful of mega-cap companies. Instead, analysts are becoming increasingly optimistic about the earnings prospects of mid-sized and smaller firms as well, indicating a healthier and more inclusive corporate profit cycle.

The widening participation in earnings growth helps reinforce the market’s resilience and provides a stronger fundamental foundation for the ongoing rally. However, it also means that elevated expectations are becoming embedded across a larger segment of the market. As a result, companies will need to continue delivering robust results to justify current valuations and sustain investor enthusiasm in the months ahead.

Despite our Fabulous Earnings Momentum (FEMO) thesis remaining intact, we have maintained since June 3 that the market was vulnerable to a “June Swoon”—a temporary pullback that could ultimately create an attractive buying opportunity. Arguably, that correction may have already occurred on June 5, when the S&P 500 dropped 2.6% following a much stronger-than-expected May employment report.

The surprisingly robust labor data raised the possibility that the Federal Open Market Committee could adopt a more hawkish tone at its upcoming meeting on Wednesday, a scenario we have viewed as a contrarian risk since early May. Strong economic data tends to reduce the urgency for monetary easing and can lead investors to reassess interest-rate expectations.

The pullback has been particularly noticeable among the Magnificent Seven, which have underperformed the rest of the market so far this month. In contrast, the remaining members of the S&P 500—the so-called “Impressive 493”—have held up relatively well.

One explanation may be portfolio rebalancing. Investors looking to participate in the highly anticipated SpaceX IPO may have funded purchases by taking profits in large-cap technology names that had delivered substantial gains. Another possibility is growing concern that corporate customers are becoming more disciplined with artificial intelligence spending. If businesses begin tightening AI budgets, suppliers of AI infrastructure and services could face increased pricing pressure, particularly in the market for AI computing and token-based services.

As a result, while enthusiasm for AI remains strong, investors appear to be questioning whether the extraordinary growth expectations embedded in leading technology stocks can continue to be met at the same pace.

So, has the June Swoon already run its course now that the highly anticipated SpaceX IPO has been successfully completed? There are several reasons to believe that may be the case.

A potential memorandum of understanding between the United States and Iran could provide an additional tailwind for equities by easing geopolitical tensions and putting further downward pressure on oil prices. Lower energy costs would help improve the inflation outlook, potentially creating a more supportive backdrop for risk assets.

Such a development could also strengthen the position of the more dovish members of the Federal Open Market Committee, giving them greater scope to argue against a more restrictive policy stance. Falling oil prices and reduced inflation risks would lessen the need for additional tightening measures.

That said, we continue to lean toward the view that the FOMC may signal a modest hawkish shift in Wednesday’s policy statement. However, recent geopolitical and market developments have increased the likelihood that policymakers adopt a more neutral tone instead.

If that proves to be the case, the recent pullback could ultimately be remembered as a brief correction rather than the start of a deeper downturn. Combined with strong earnings momentum, easing energy prices, and improving investor sentiment, a neutral Fed stance could provide the foundation for the broader bull market to resume its advance toward fresh record highs.

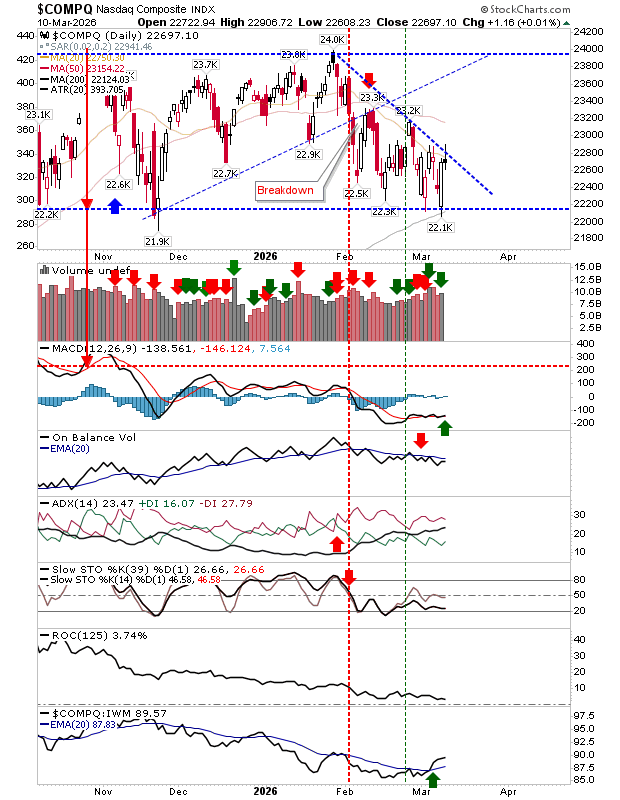

The NASDAQ 100 has experienced choppy price action this week as traders continue searching for clearer market direction. Despite the short-term uncertainty, the broader outlook remains bullish. However, ongoing geopolitical developments and headline-driven volatility could create additional risks, making it prudent to remain cautious rather than aggressively increasing exposure at current levels.

While the index continues to trade within a longer-term uptrend, investors may be wary heading into the weekend due to the possibility of unexpected developments in the Middle East that could impact market sentiment. Even so, the overall technical picture remains constructive, and any meaningful pullback is likely to be viewed as a buying opportunity, with traders looking to capitalize on potential rebounds within the prevailing bullish trend.

Gold

The gold market came under notable selling pressure at the start of the week, declining sharply and briefly testing the key $4,000 support level. This area remains a critical technical zone and is likely to attract close attention from traders in the coming sessions.

Gold prices continue to be heavily influenced by interest rate expectations. Recently, bond yields have edged lower as market participants speculate that the United States and Iran may be moving closer to a diplomatic agreement, reducing some geopolitical uncertainty and affecting demand for safe-haven assets.

From a longer-term perspective, the outlook for gold remains bullish. However, volatility is expected to remain elevated, and traders should be prepared for significant price swings. A sustained break below the $4,000 support level could trigger a deeper correction and lead to a more pronounced sell-off, making this a crucial level to monitor.

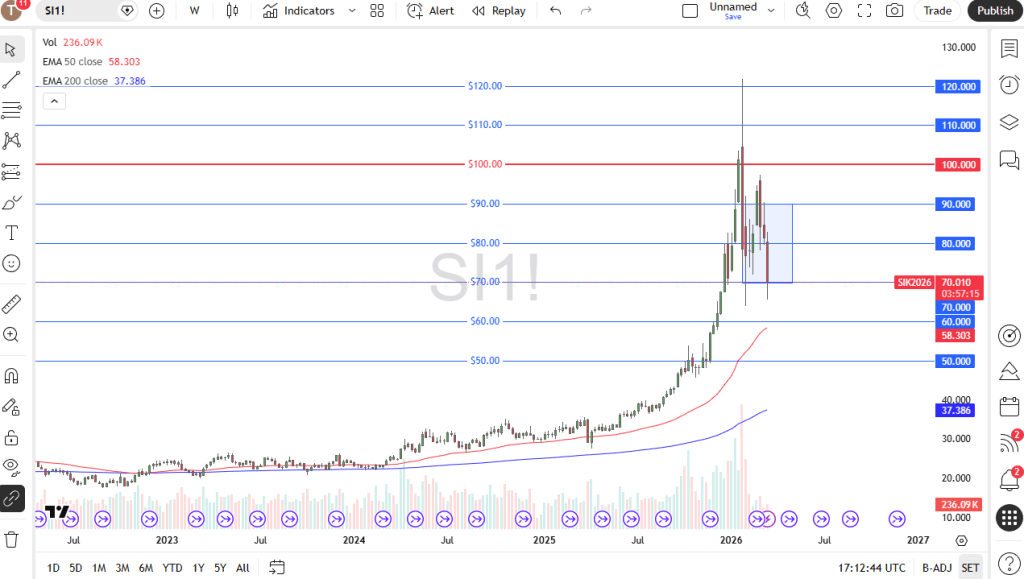

Silver

The silver market experienced volatile and uneven trading throughout the week, with price action remaining relatively noisy. Despite the fluctuations, the $60 level appears to be emerging as an important support zone and could serve as a near-term floor for the market.

On the weekly chart, the current candlestick is beginning to resemble a hammer pattern, which is often viewed as a potential bullish signal. It is also worth noting that much of the recent upward momentum was driven by Friday’s gap higher, suggesting that short-covering activity ahead of the weekend may have contributed significantly to the rally.

Looking ahead, a decisive break above the $70 level could signal a continuation of bullish momentum. If that resistance is cleared, silver may have the potential to advance another $10 relatively quickly as buyers regain control of the market.

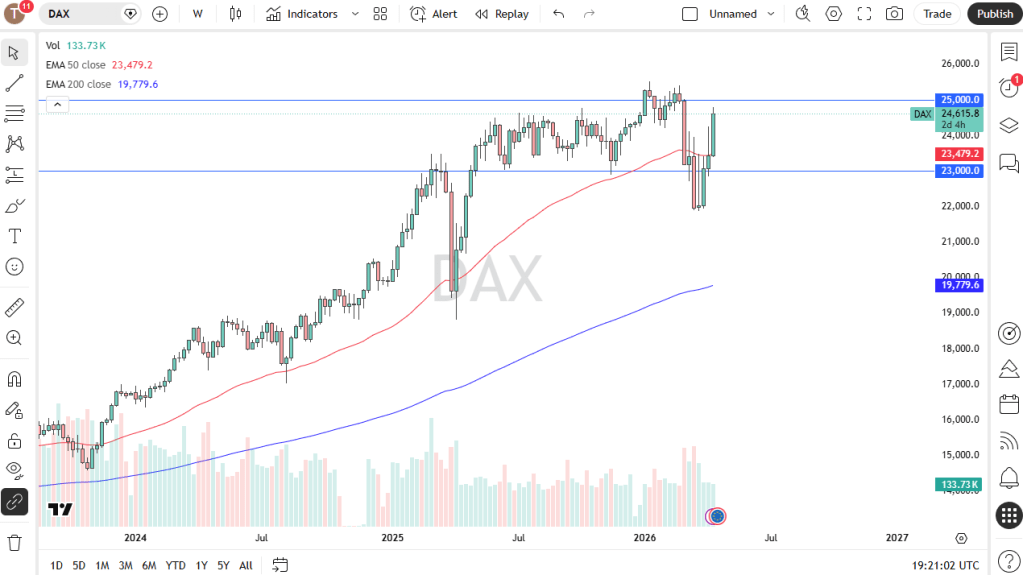

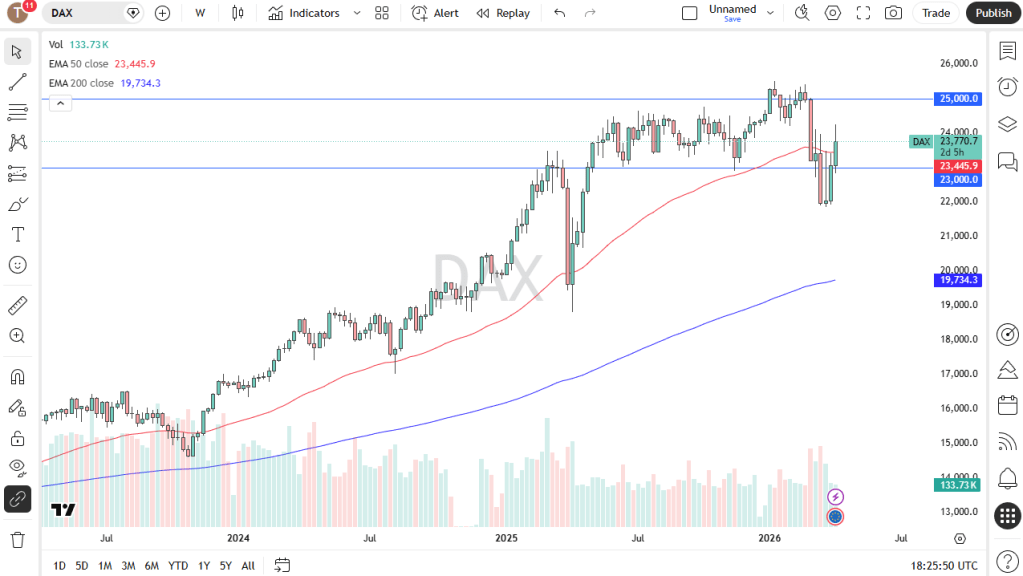

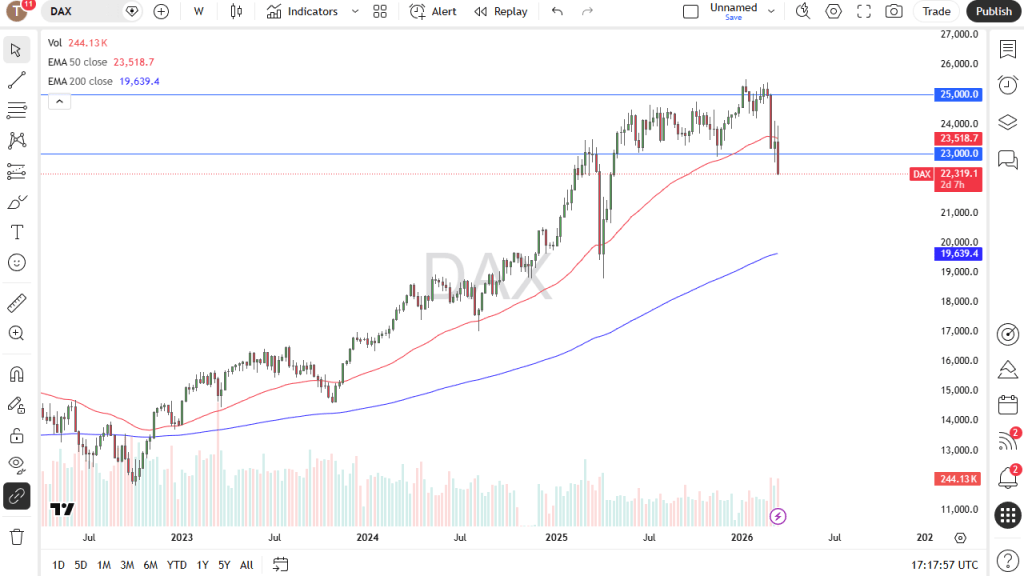

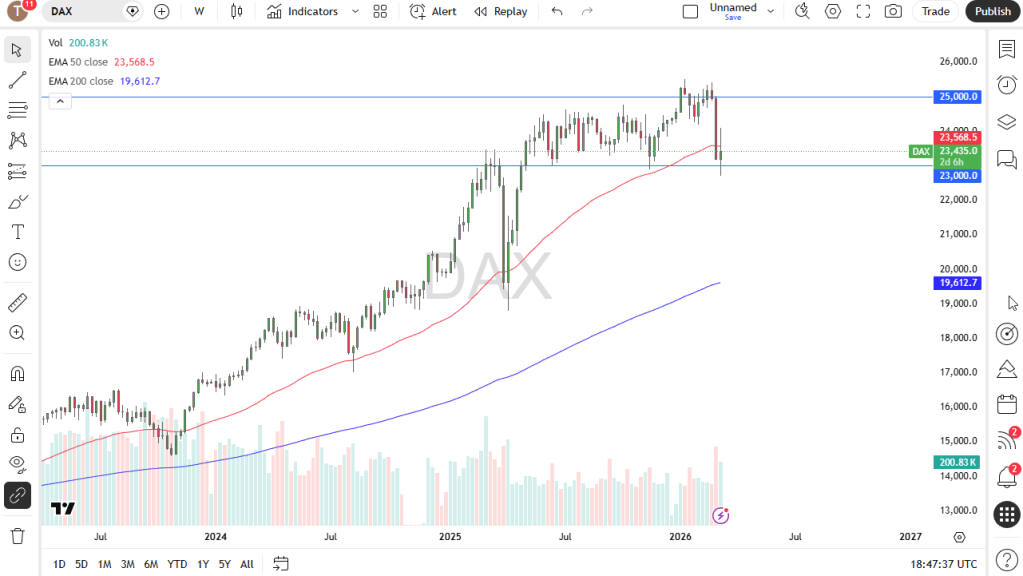

DAX

Germany’s DAX index declined during the week, testing the important €24,000 support level before rebounding and showing renewed signs of strength. The recovery suggests that buyers remain active at lower levels, helping to stabilize the market after the recent pullback.

At present, the index appears to be trading within a broad consolidation range, with support near €24,000 and resistance around €25,000–€25,250. This upper zone continues to act as a significant barrier, limiting further upside progress in the short term.

The overall outlook remains moderately bullish, but expectations for explosive gains are limited. Instead, the DAX continues to favor a “buy-the-dip” approach, with traders likely viewing pullbacks as opportunities to enter long positions. Before a more substantial upward move can develop, the market may need additional time to build momentum and establish a stronger foundation above current levels.

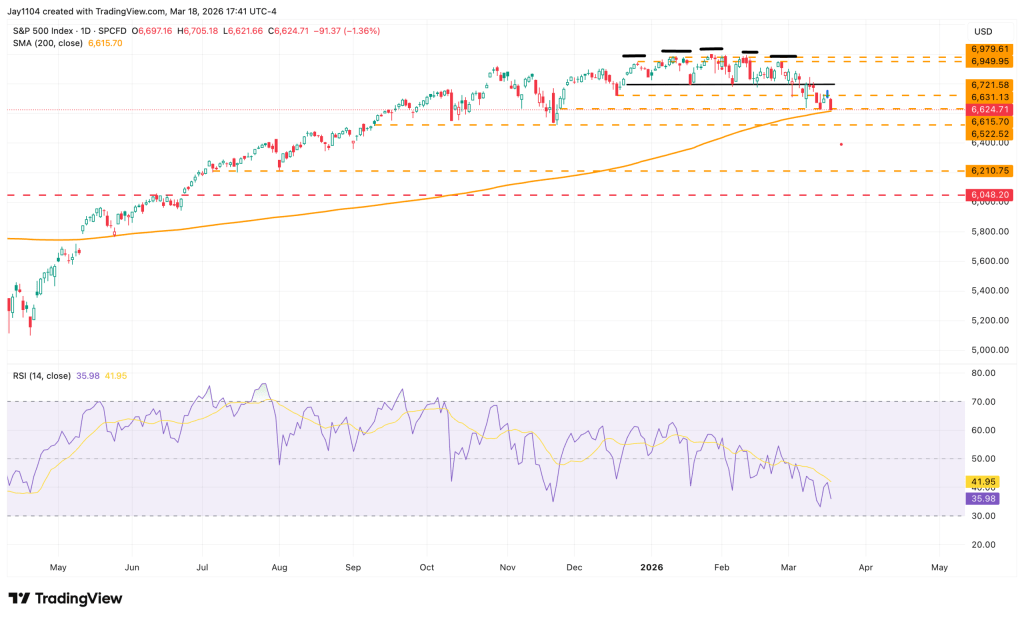

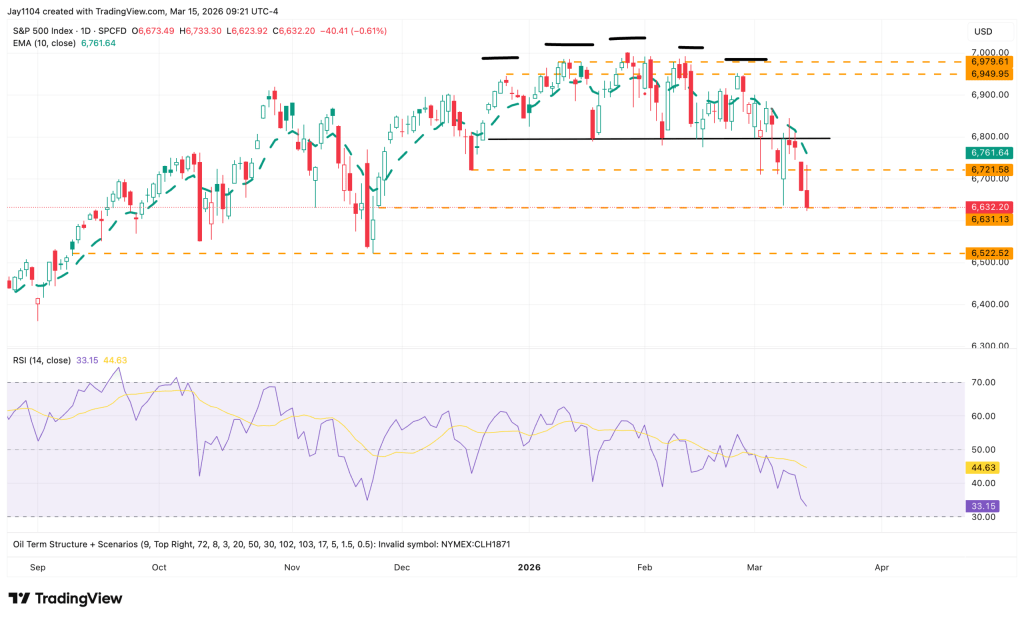

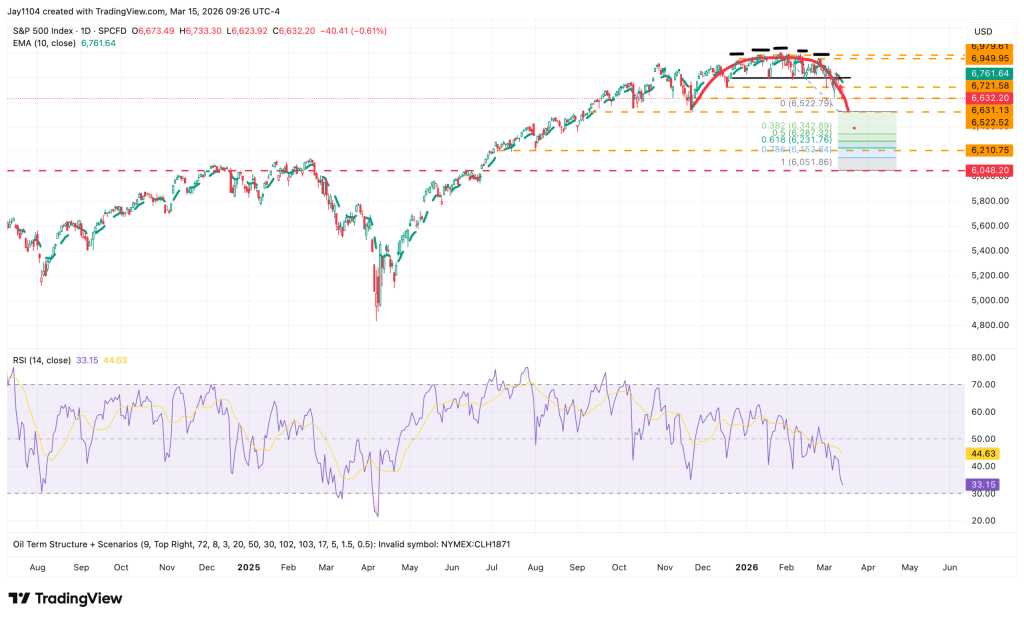

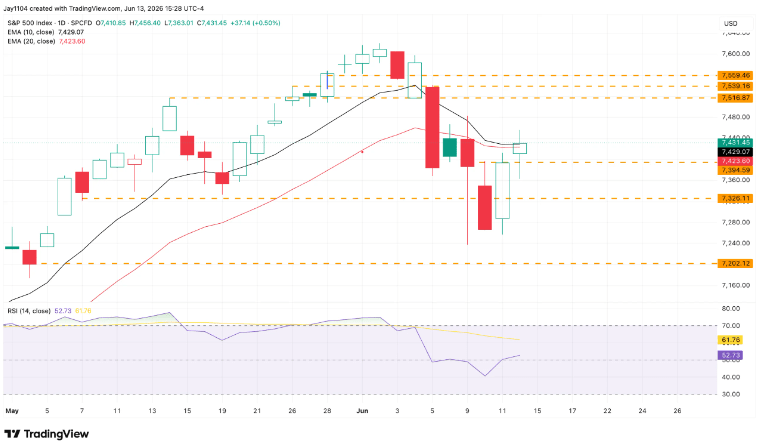

S&P 500

The S&P 500 posted modest losses during the week, but the 7,300 level continues to provide strong support, a pattern that has been observed on several occasions in recent months. Buyers have consistently stepped in around this area, helping to maintain the broader bullish structure of the market.

On the upside, the 7,500 level remains an important resistance zone. However, a decisive breakout above 7,600 could serve as a catalyst for a stronger bullish move, potentially opening the door to a fresh leg higher in the ongoing uptrend.

The preferred strategy remains buying on pullbacks, although traders should be prepared for increased volatility. Seasonal summer trading conditions, concerns surrounding the bond market, and ongoing geopolitical tensions in the Middle East could contribute to choppy price action in the near term. Nevertheless, the overall outlook remains constructive. The market is still firmly in an uptrend, and while momentum has slowed somewhat, the underlying bullish trend remains intact.

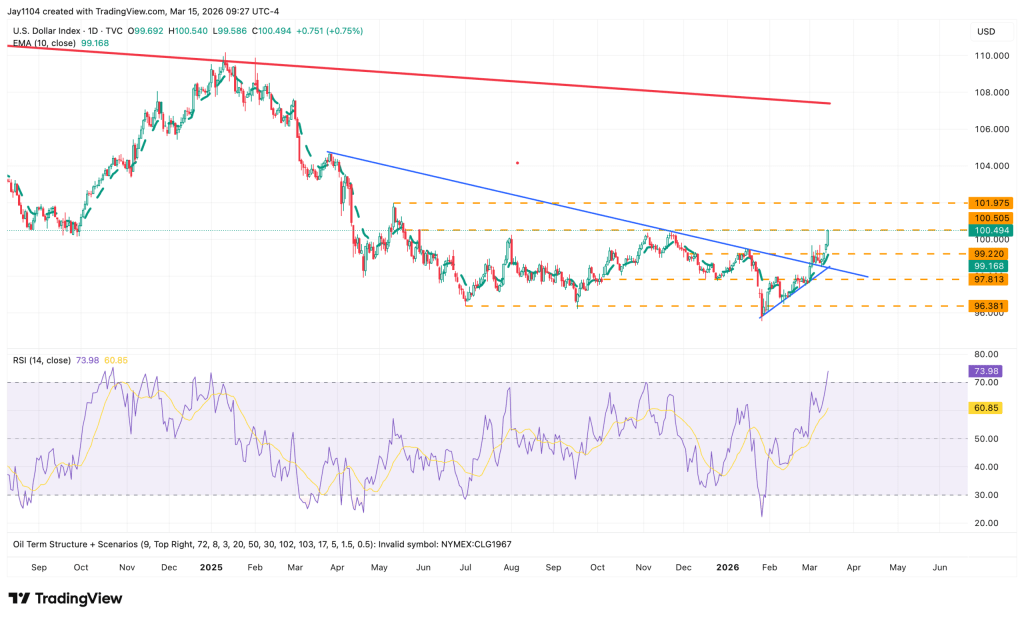

EUR/USD

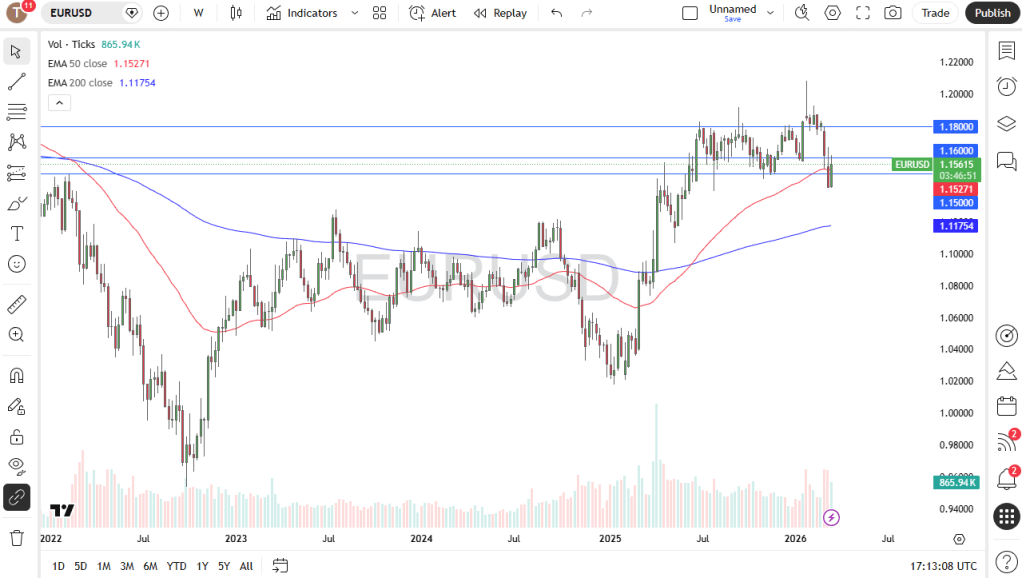

The euro strengthened against the U.S. dollar during the week, but the broader market structure remains largely range-bound. Despite the recent rally, EUR/USD appears to be trapped within a well-established trading range that has been in place since July 2025, with the 1.16 level serving as a key equilibrium or “fair value” area.

Given the current price dynamics, the pair may continue gravitating toward the middle of this range, with the 1.1600–1.1650 zone likely acting as an important area for traders to reassess market direction. Whether the euro can sustain further gains from there remains uncertain and will depend on broader macroeconomic developments.

One key indicator to monitor is the U.S. 10-year Treasury yield. Rising yields typically support the U.S. dollar by increasing the attractiveness of dollar-denominated assets. As a result, if Treasury yields begin moving higher, EUR/USD could come under renewed selling pressure and potentially reverse some of its recent gains. Overall, the pair continues to trade without a clear long-term directional bias, favoring a range-trading environment for now.

USD/JPY

The U.S. dollar traded largely sideways against the Japanese yen during the week, as the market continued to test a major resistance area near a swing high dating back to 1990. Although USD/JPY briefly moved above this level in 2024, the breakout lacked sustained momentum, leaving traders focused on whether a more decisive move higher can develop.