One by one, quietly and without public notice, central banks around the world are repatriating their gold reserves. From New Delhi to Belgrade, Frankfurt to Paris, institutions are arriving at similar conclusions independently. The trust that once supported the postwar reserve architecture is beginning to show visible cracks.

Introduction

The last time France withdrew its gold from American custody was in 1965. Under Charles de Gaulle, who viewed the Bretton Woods system as granting the United States an “exorbitant privilege,” France dispatched a warship to New York to exchange dollars for gold—directly challenging US monetary supremacy.

Six years later, President Richard Nixon ended the dollar’s convertibility into gold, effectively dismantling the Bretton Woods gold standard. Six decades on, France has again quietly reduced its gold holdings stored at the New York Federal Reserve. This time, instead of geopolitical confrontation, the move is executed through discreet financial transfers, driven by a €12.8 billion arbitrage opportunity.

Despite the change in method, the underlying motivation appears familiar: persistent skepticism toward dollar-centric financial systems and a renewed emphasis on monetary sovereignty. While history does not repeat exactly, developments in gold markets often echo earlier patterns with notable precision.

The Silent Return

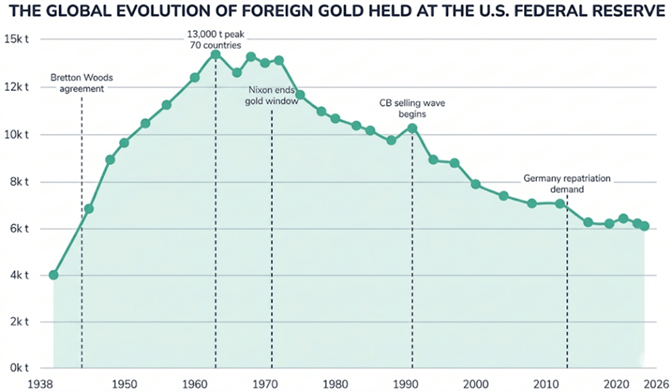

For much of the postwar period, the physical location of gold reserves was rarely questioned. Many central banks—particularly in Europe and the developing world—kept their gold in custodial vaults such as the Federal Reserve Bank of New York and the Bank of England, assuming these locations were neutral, liquid, and politically secure. That long-standing assumption is now weakening.

Recent data supports this shift. The World Gold Council’s Central Bank Gold Reserves Survey 2025, based on responses from 73 institutions, shows that 59% of central banks now store at least part of their gold domestically, up from 41% in 2024 and 50% in 2020. Since 1972, approximately 6,900 tonnes of gold have been repatriated to national vaults.

This marks an 18-percentage-point increase in just five years, with most of the change occurring in the past year alone. The same survey also found that 95% of central banks expect global gold reserves to rise further over the next 12 months, indicating a broadly shared expectation of continued accumulation among monetary authorities.

The driver behind this shift is increasingly evident. The 2022 freezing of around $300 billion in Russian foreign currency reserves sent a powerful message: assets held abroad may not remain fully under the owner’s control in times of geopolitical stress. An updated 2025 Invesco survey of central banks shows that the share storing gold domestically has increased by 18 percentage points since that episode—suggesting a striking alignment between the event and changing reserve behavior.

Gold has traditionally been regarded as the ultimate safe-haven asset, but recent developments revealed a less discussed vulnerability: what was once framed as market risk has increasingly become jurisdictional and counterparty risk. In other words, even physical reserves held in trusted foreign vaults depend on political continuity and legal access—risks that were previously underappreciated.

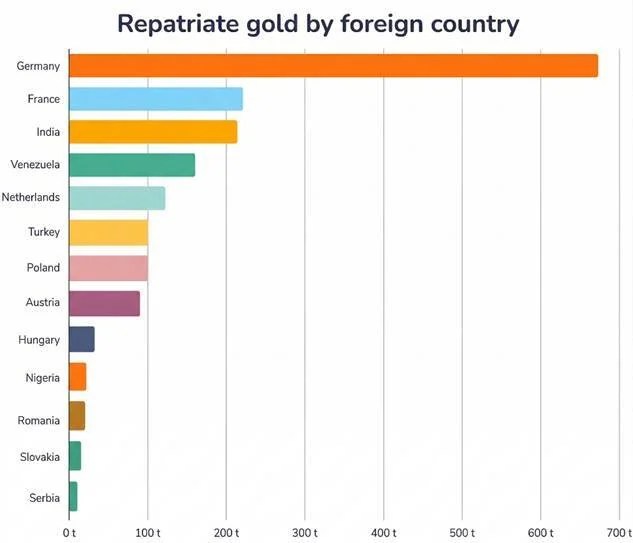

The reaction has been broad-based and measured in substantial volumes. Bloomberg reports that India has repatriated roughly 280 tonnes of gold over the past four years, including a notable transfer from the Bank of England in 2024. In July 2025, it was also reported that Serbia brought back its entire gold holdings—worth about $6 billion—into domestic storage, deliberately avoiding reliance on established international custodial centers.

Other countries, including Poland, Turkey, and Nigeria, have followed similar paths. While much of this movement has been led by emerging markets, the trend is gradually extending into parts of Western Europe as well, pointing to a broader structural rethinking of where ultimate financial security resides.

The pace of accumulation further strengthens this trend. According to World Gold Council data, central banks purchased more than 1,000 tonnes of gold annually in 2022, 2023, and 2024—an unprecedented sustained buying cycle in modern history. Although this pace eased to 863 tonnes in 2025, it still remained exceptionally high by historical standards.

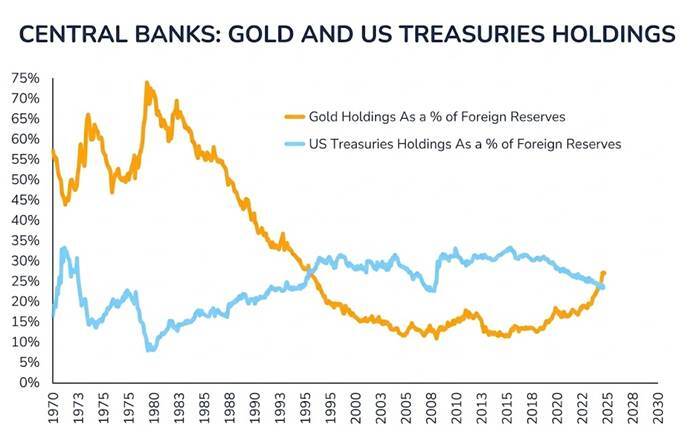

By early 2026, total gold held by central banks worldwide was estimated at around $4 trillion, overtaking, for the first time, the roughly $3.9 trillion in US Treasury securities held by the same institutions. According to the World Gold Council and Visual Capitalist, this shift reflects a meaningful rebalancing of global reserve preferences, with potential long-term implications for the international monetary system.

France’s Banque de France offers a particularly illustrative case. Between July 2025 and January 2026, it carried out a discreet program involving 129 tonnes of gold stored at the New York Federal Reserve—about 5% of its total 2,437-tonne holdings—executed through 26 separate transactions. However, this was not a straightforward physical repatriation.

Instead of transporting older bars across the Atlantic, the central bank sold legacy-format gold in New York and replaced it with modern London Good Delivery bars held in Paris. The result was effectively a swap in form rather than a logistical relocation.

As reported by La Tribune, the financial outcome was striking: a combined €12.8 billion gain—€11 billion in 2025 and €1.8 billion in 2026—achieved without physically moving the metal. While often described in the press as repatriation, the operation was more accurately a form of quality arbitrage that incidentally increased domestic holdings.

The End of the American Vault Illusion

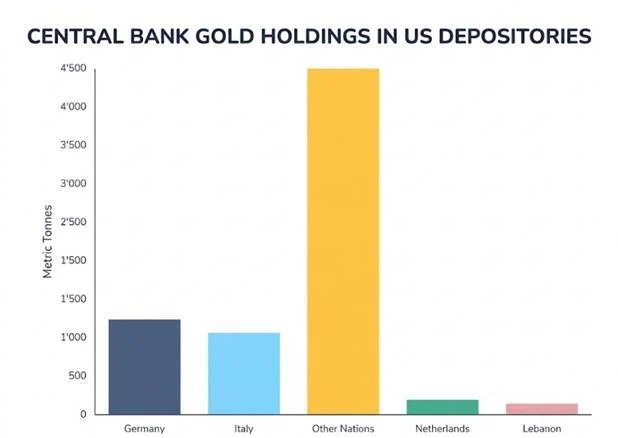

Germany’s case underscores the strategic significance of this shift more clearly than France’s quieter financial maneuvers. The Bundesbank continues to hold 1,236 tonnes of gold at the Federal Reserve Bank of New York—around 36.6% of its total 3,378-tonne reserves—and this remains the largest single foreign gold position stored at the NY Fed.

Between 2013 and 2017, Germany conducted the largest gold repatriation operation in modern history, withdrawing 674 tonnes from both New York and Paris. This process was framed at the time as a technical modernization of reserve management rather than a strategic pivot.

For context, the New York Federal Reserve currently stores roughly 6,331 tonnes of foreign sovereign gold. Germany alone accounts for nearly one-fifth of all foreign-held gold in its vaults in lower Manhattan, highlighting how concentrated global trust once was in a single custodial hub.

From 2013 to 2021, Germany repatriated about 300 tonnes from New York and 283 tonnes from Paris, completing what was widely regarded as a normalization of storage practices. The remaining 1,236 tonnes were, at the time, still considered securely and appropriately held abroad.

What has changed since then is not necessarily the security of the vault itself, but the perception of what “secure custody” means in a more fragmented geopolitical environment.

This ruling is increasingly subject to political debate. In January 2026, former senior Bundesbank official Emanuel Mönch warned that, amid heightened geopolitical uncertainty, concentrating large volumes of gold in the United States poses risks. He argued that the Bundesbank should consider further repatriation as a way to enhance strategic autonomy. His position echoes a widening political consensus in Germany, spanning parties from the AfD to figures within the Greens and FDP.

Despite this, the Bundesbank has not changed its official policy. It continues to regard New York as a safe and dependable storage hub, and no additional repatriation initiative is currently planned. Nevertheless, the divergence between institutional continuity and mounting political pressure is becoming more pronounced.

At a deeper level, the issue is structural. For many years, the rationale for keeping gold in New York rested on three foundations: liquidity, given the ability to quickly trade or mobilize gold in the world’s largest market; network advantages, driven by the scale and efficiency of the LBMA and New York Federal Reserve gold markets; and political confidence, based on the assumption that US custody would not be used as a geopolitical lever.

Each of these pillars has since been weakened to some extent. The 2022 sanctions episode demonstrated that the US and its allies are willing to deploy financial infrastructure as an instrument of geopolitical pressure. A more transactional approach in US foreign policy has further reinforced such concerns. At the same time, improvements in European gold markets and LBMA access have reduced the liquidity advantages of storing reserves in New York, making domestic storage increasingly viable without significant market disadvantage.

The Overlooked Gold Catalyst Markets Still Haven’t Factored In

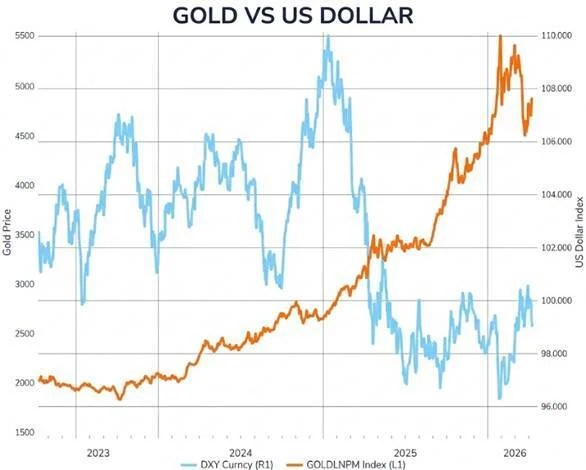

Investment banks are largely aligned on a continued rise in gold prices, though their forecasts differ, reflecting varying views on how quickly central bank behavior is shifting.

Goldman Sachs has lifted its 2026–2027 outlook to $4,000–$5,400, pointing to sustained demand from emerging-market central banks. J.P. Morgan Private Bank is even more bullish, projecting $6,000–$6,300, attributing the upside to accelerating diversification away from the US dollar. UBS takes a more moderate stance at around $4,200, but similarly highlights a global trend of reducing dollar exposure.

Taken together, the wide forecast range of roughly $3,100 to $6,300 is less a sign of disagreement about direction and more about uncertainty over timing—particularly the speed of gold repatriation and reserve reallocation. The common thread across all projections is a shared conviction in a longer-term bullish trend, driven by evolving central bank strategies. Early 2026 pricing behavior already appears to be reinforcing this growing institutional confidence in gold.

Gold repatriation does not change the total global supply; it simply reallocates where and how gold is held and accessed. For example, when the Banque de France substituted New York-held ingots with London Good Delivery bars in Paris, global central bank reserves remained unchanged, with only a shift in classification and location. The London Bullion Market Association (LBMA), which clears roughly $30 billion in gold transactions daily, operates on the assumption that institutional gold is readily accessible regardless of storage location.

As the pool of immediately available gold tightens, borrowing costs tend to increase, price spreads widen, and physical gold can trade at a premium to paper claims. This reflects a scarcity of deliverable metal that is not captured in conventional supply-flow data and is often underrepresented in market models—highlighting that distribution can matter as much as total stock.

If Germany were to pursue a similar repatriation of its 1,236 tonnes held at the New York Fed, the effects on the physical market would be more pronounced. Such a move would require sourcing, refining to current delivery standards, and physically transporting the gold, generating real demand pressure within the LBMA system, even though global central bank holdings would remain unchanged.

This scenario is not currently priced in by markets. While the German repatriation debate remains largely political and the Bundesbank has given no indication of imminent action, the underlying drivers that prompted France’s earlier decision—bar standard considerations, proximity to European counterparties, and a geopolitical preference for domestic custody—are similarly relevant to Germany.

Understanding the De-Dollarisation Trend

Gold repatriation is frequently framed as a symbolic geopolitical gesture, but its implications are more tangible. When central banks repatriate gold, they also reduce their dependence on the dollar-based financial system, including its clearing mechanisms, custodial arrangements, and settlement infrastructure. Each tonne of gold brought back reduces exposure to dollar-linked channels and potential sanctions risk.

This shift is already becoming measurable. By early 2026, the value of gold held by central banks exceeded their holdings of US Treasuries—approximately $4 trillion compared with $3.9 trillion. This signals a gradual but persistent move away from the US dollar’s role as the dominant reserve asset. Unlike traditional currency diversification, this transition is difficult to capture fully in official statistics, yet it is ongoing, accelerating, and still not fully reflected in market pricing.

Historically, gold prices have tended to decline when the US dollar strengthens and real interest rates rise. However, this relationship has weakened since 2022, as central banks have emerged as significant buyers driven more by geopolitical considerations than by traditional market indicators such as yields or currency movements. This introduces a form of demand that is relatively insensitive to price.

Consequently, conventional gold valuation models are becoming less reliable and often understate price levels. This shift also helps explain why institutions such as Goldman Sachs, J.P. Morgan, and UBS are projecting significantly higher gold prices than would have been considered plausible prior to 2022. In effect, the pricing dynamics of gold have evolved, while many existing models have yet to fully adjust.

Conclusion

The structural argument for gold repatriation is compelling, but it is not without inconsistencies. Recent conflicts in the Middle East have added further complexity, at times pressuring both gold and the US dollar simultaneously and disrupting traditional market correlations. Central banks also do not act as a single coordinated group—some are accumulating gold, others are repatriating it, while some are still selling under financial or policy constraints.

Although data from the World Gold Council, analyst price targets, and observable repatriation flows support the broader trend, the pace is uneven and motivations vary significantly across institutions. Gold continues to function as a form of monetary insurance, but its behavior and underlying drivers are more nuanced and less linear than the prevailing narrative often implies.

Leave a comment