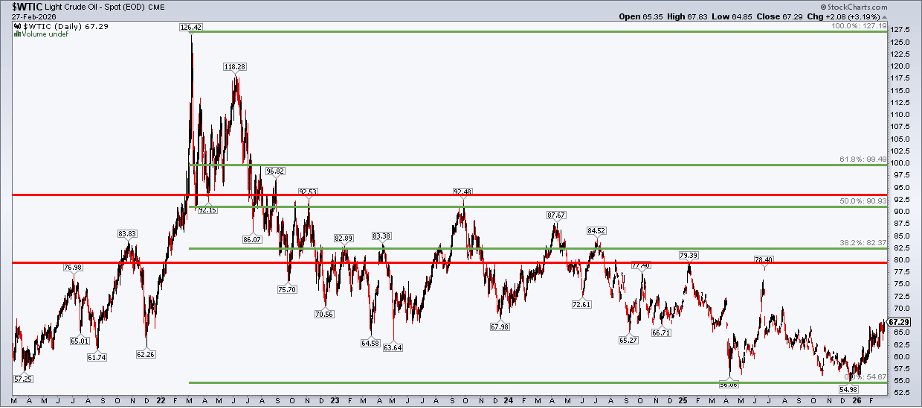

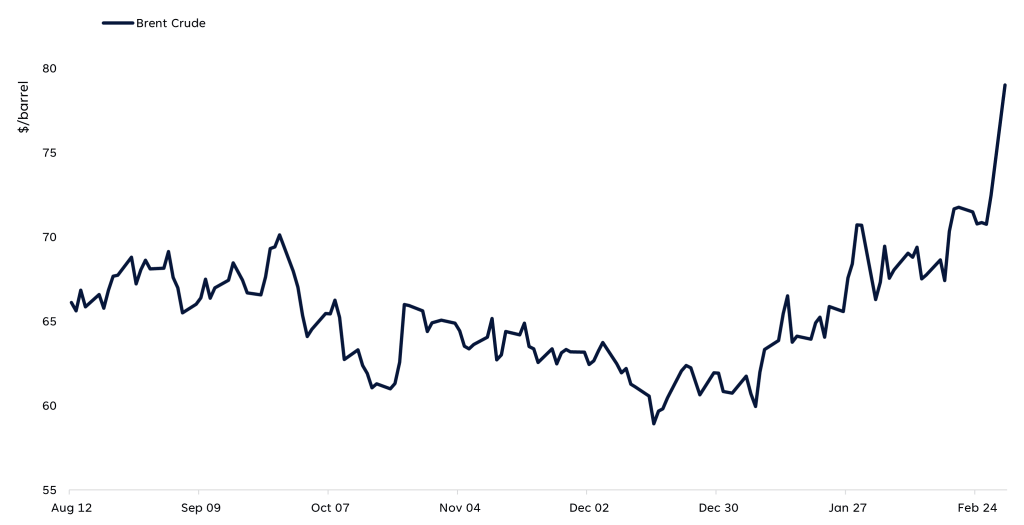

Crude oil prices continued their sharp decline on Thursday, with West Texas Intermediate (WTI) dropping nearly 3% to around $74.52 per barrel and Brent crude losing 2.7% to trade near $77.40. Both benchmarks fell to their lowest levels since early March as markets reacted to the newly signed US-Iran peace agreement and the partial reopening of the Strait of Hormuz. These developments have significantly reduced the geopolitical risk premium that had supported oil prices for months, reversing one of the largest supply-driven rallies in recent years. As tanker traffic resumes through the world’s most critical oil transit route, downward pressure on crude prices remains dominant.

The magnitude of the pullback has been remarkable. Since reaching a four-month peak in April, oil prices have fallen by roughly 38%. At the height of the US-Iran conflict, the effective closure of the Strait of Hormuz disrupted a substantial portion of global seaborne oil flows, driving Brent crude to levels not seen since the 2022 energy crisis. More than 11 million barrels per day of Middle Eastern production were temporarily removed from the market, inventories tightened sharply, and prices surged into triple-digit territory. With the ceasefire now in place and shipping activity gradually returning, traders are rapidly adjusting expectations to reflect the prospect of recovering supply.

However, the outlook remains far from straightforward. Global inventories are still under pressure after months of heavy drawdowns, and restoring Iranian and regional oil production could take considerably longer than current market pricing suggests. In addition, uncertainty surrounding the ceasefire persists, as unresolved nuclear negotiations and warnings from President Trump about potential renewed military action continue to pose risks. As US markets head into the Juneteenth holiday closure, crude oil finds itself caught between two opposing forces: the bearish impact of reopening supply routes and the supportive influence of tight inventories and lingering geopolitical uncertainty. The key question is whether returning production will outweigh supply tightness, or whether a slower recovery process will help stabilize prices before any meaningful surplus emerges.

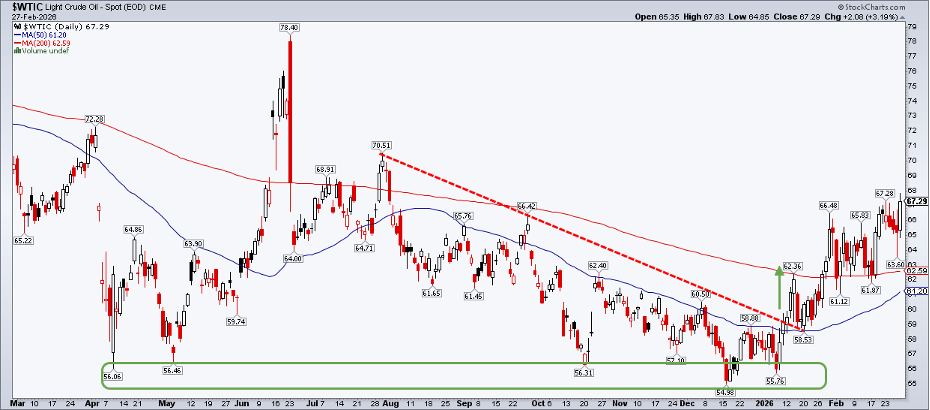

Current Oil Market Levels: WTI, Brent, and the 38% Retreat From April Peaks

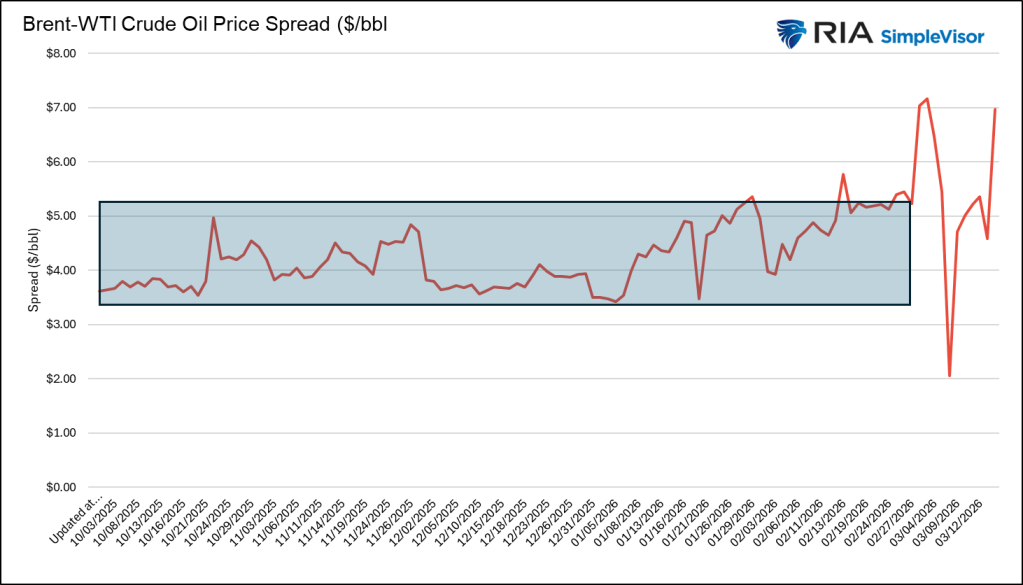

Recent price action underscores the scale of the oil market’s reversal. On Thursday, West Texas Intermediate (WTI) slipped nearly 3% to approximately $74.52 per barrel, while Brent crude declined around 2.7% to $77.40. Both benchmarks reached their lowest levels since early March, extending losses as optimism surrounding the US-Iran peace agreement strengthened throughout the week. At the same time, the premium between Brent and WTI has narrowed from the elevated levels recorded during the peak of shipping disruptions.

The sharp decline illustrates the unwinding of a substantial geopolitical risk premium. During the height of the conflict, when the Strait of Hormuz was effectively closed and more than 11 million barrels per day of Middle Eastern production were offline, Brent surged into triple-digit territory, reaching its highest levels since the 2022 energy crisis. WTI also rallied dramatically, climbing from below $60 earlier in the year to nearly $100. April marked the peak of that fear-driven advance. Since then, expectations of a diplomatic resolution have steadily gained traction, triggering a roughly 38% correction as the market reassesses the likelihood of supply returning.

The speed of the selloff highlights how heavily oil prices had become dependent on geopolitical concerns rather than underlying supply-and-demand fundamentals. Once traders began pricing in the restoration of disrupted barrels, the risk premium rapidly evaporated. With crude now trading at three-month lows and even below levels seen before the conflict’s most severe phase, market participants are evaluating how much downside remains. The answer will largely depend on whether returning supply outweighs the ongoing effects of historically tight inventories. As a result, both WTI and Brent are attempting to establish a new equilibrium in a post-conflict environment, a process likely to remain volatile as developments surrounding Hormuz and regional production recovery continue to unfold.

The Agreement That Triggered the Selloff

The primary catalyst behind oil’s sharp decline has been the interim peace agreement signed by President Trump and Iran’s leadership, aimed at ending months of hostilities in the Middle East. According to US officials, the memorandum of understanding is already in effect and extends the current ceasefire while creating a framework for reopening the Strait of Hormuz and ending the US naval blockade. Under the arrangement, Iran will permit vessels to transit the waterway without fees for 60 days, while the United States begins lifting restrictions, with the broader objective of fully restoring maritime traffic and easing sanctions on Iranian oil exports.

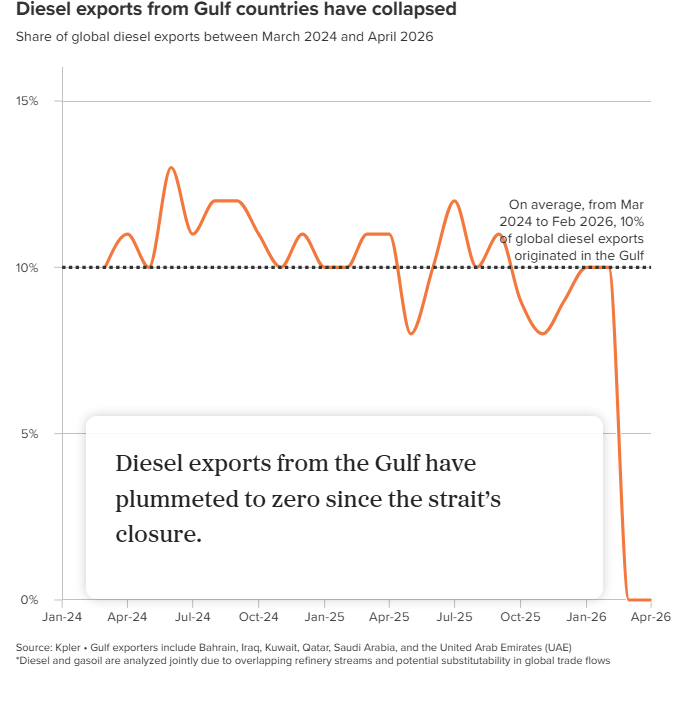

The deal marks a major shift after months of severe disruption. Since the conflict erupted in late February, oil flows through one of the world’s most critical energy corridors had been heavily constrained. The prolonged closure of Hormuz forced Gulf producers to curtail output as storage capacity tightened and export routes became inaccessible. By facilitating the reopening of the strait, the agreement paves the way for suspended production and exports to gradually return to the market.

Investors have responded by aggressively removing the geopolitical premium embedded in crude prices. As confidence grows that oil shipments can once again move freely through Hormuz, fears of prolonged supply shortages are fading. Although the agreement remains temporary and key issues—particularly negotiations surrounding Iran’s nuclear program—have yet to be resolved, the reopening of the strait has convinced many traders that the most severe phase of the supply disruption has passed. That shift in sentiment has fueled the rapid decline that has pushed oil prices to their lowest levels in three months.

Hormuz Reopens: Shipping Flows Signal a Return of Supply

One of the clearest signs of easing tensions in the Middle East is the revival of maritime traffic through the Strait of Hormuz. Government officials reported that more than 12 million barrels of crude oil have already passed through the waterway, marking the highest volume since the conflict began. They also noted that Iran has refrained from targeting commercial vessels for several consecutive days, adhering to the terms of the ceasefire agreement. Saudi crude tankers, LNG carriers, and fuel shipments have resumed departures from Gulf ports, providing tangible evidence that the reopening is progressing beyond diplomatic commitments and into operational reality.

The importance of this development cannot be overstated. Prior to the conflict, the Strait of Hormuz handled roughly 14 million barrels of crude oil per day, along with approximately 6 million barrels of refined petroleum products, making it the world’s most critical energy transit corridor. The prolonged disruption of this route removed a significant portion of global supply from international markets, fueling the sharp rally in oil prices. As traffic gradually normalizes, confidence is growing that those lost volumes will return. Every successful transit through the strait strengthens market belief that the ceasefire is holding and that supply chains are being restored.

The faster-than-expected return of shipping activity has become the primary driver behind this week’s sharp selloff in crude prices. Markets had largely anticipated a prolonged disruption, and the rapid reopening has forced traders to reassess supply expectations. The movement of more than 12 million barrels through the corridor serves as concrete evidence that the bottleneck is easing, while the absence of attacks on commercial shipping reinforces confidence in the agreement. Although risks remain—particularly given the temporary nature of the ceasefire and the 60-day implementation window—the restoration of physical oil flows has emerged as the dominant bearish factor. As long as vessels continue to navigate Hormuz without disruption, pressure on crude prices is likely to persist.

Returning Production: Saudi Arabia, the UAE, and Iraq Prepare to Ramp Up

The reopening of Hormuz also creates a pathway for major Gulf producers to restore output that was suspended during the conflict. Saudi Arabia, the United Arab Emirates, and Iraq collectively curtailed millions of barrels per day as export routes became constrained and storage facilities approached capacity limits. At the peak of the crisis, more than 11 million barrels per day of regional production were effectively removed from the market. Even a partial recovery of these volumes would significantly increase global oil supply.

How quickly this production returns will play a crucial role in determining future price movements. During the closure, producers were forced to either store unsold crude or shut in wells as inventories accumulated. With shipping routes reopening, they can gradually reduce storage levels, resume exports, and reactivate idle production. Some facilities may be able to restart relatively quickly, while others could require additional time before reaching normal operating levels. Given the substantial revenue losses incurred during the disruption, Gulf producers have strong incentives to accelerate the recovery process wherever possible.

The prospect of returning supply remains the central reason behind the market’s bearish repricing. Traders are increasingly factoring in the return of millions of barrels per day that were previously unavailable, shifting expectations from severe scarcity toward the possibility of future oversupply. This helps explain why crude prices have fallen not only from their conflict-driven highs but also below some pre-crisis levels. However, the timing of the recovery remains critical. A rapid production restart would reinforce downward pressure on prices, while a slower-than-expected return could allow tight inventories to provide support. Ultimately, the interaction between recovering supply and depleted stockpiles will shape the next phase of the oil market, making production trends in Saudi Arabia, the UAE, and Iraq key indicators for investors to watch.

How Quickly Can Oil Production Recover?

One of the most important questions facing the oil market is how quickly physical supply can return compared with the pace at which prices have already adjusted. While crude prices have plunged on expectations of renewed supply, industry experts warn that restoring Iranian production and refining operations may take considerably longer than markets currently assume. Damage to infrastructure, the need to clear mines and secure shipping routes around the Strait of Hormuz, and the technical complexity involved in restarting oil fields and refineries all suggest that recovery will likely be gradual rather than immediate.

Most official projections reflect this more measured outlook. Energy analysts generally expect shipping activity through Hormuz to normalize in stages, with tanker traffic gradually increasing and production levels recovering over an extended period. Trade flows and regional output may not fully return to pre-conflict conditions until well into next year. In several Gulf countries, prolonged production shut-ins and operational challenges could further delay the restoration of output. Forecasts vary widely, with some financial institutions expecting a relatively quick recovery in maritime traffic, while others believe the process could take months before reaching full capacity.

The disconnect between market pricing and physical recovery remains a key source of uncertainty. If supply returns more slowly than traders currently anticipate, tight inventories could remain in place longer, providing support for oil prices and potentially triggering periodic rebounds. On the other hand, a faster-than-expected recovery would reinforce the current bearish outlook by accelerating the return of supply to the market. As a result, investors will closely monitor tanker movements, production data, and refinery activity for clues about the pace of normalization. The possibility of a slow recovery remains one of the strongest arguments against an extended decline in crude prices.

Inventory Constraints: Cushing, OECD Stocks, and the Global Drawdown

Despite the bearish implications of reopening supply routes, the oil market continues to face an important counterbalance: exceptionally tight inventories. Months of supply disruptions forced countries and companies to rely heavily on stored crude, resulting in significant stockpile reductions across major consuming regions. At Cushing, Oklahoma—the delivery hub for WTI futures—inventory levels have fallen to roughly 20 million barrels, highlighting the strain placed on available supplies. Recent US data also showed a decline of more than 8 million barrels in crude inventories within a single week, reinforcing evidence of ongoing stock depletion.

The global inventory situation appears even more restrictive. Analysts project that OECD inventories could decline to approximately 50 days of forward demand coverage by year-end, potentially marking the lowest level in more than twenty years. During the second quarter, limited oil flows through Hormuz forced the market to draw heavily from existing stockpiles to satisfy consumption needs. As a result, inventories were depleted at a rapid pace and are unlikely to return to pre-conflict levels anytime soon, even with shipping routes gradually reopening.

These depleted inventories provide a meaningful source of support for oil prices. Before the market can experience a true oversupply, much of the returning production will likely be absorbed by the need to rebuild stockpiles. Thin inventory buffers also leave the market vulnerable to renewed price spikes if any disruptions occur during the recovery process. Consequently, the oil market remains caught between two competing forces: the bearish impact of returning supply and the bullish influence of historically low inventories. While the reopening of Hormuz has triggered a sharp selloff, the need to replenish depleted stocks suggests that the path lower may be uneven, with periods of support emerging as market participants assess the scale of future restocking demand.

The IEA’s Surplus Warning Meets OPEC’s Skepticism

Adding to the bearish outlook for crude oil is the International Energy Agency’s warning that global markets could face a significant supply surplus in the years ahead. According to the agency’s latest projections, oil production is expected to expand substantially while demand growth remains comparatively modest. As shipping activity through the Strait of Hormuz normalizes and Gulf producers restore previously curtailed output, the resulting increase in supply could outpace consumption growth, creating downward pressure on prices.

The implications of this supply-demand imbalance are substantial. A market that only recently grappled with severe shortages could quickly transition into one characterized by abundant supply. The conflict itself has also weakened demand in some regions, as elevated energy costs and economic disruptions weighed on consumption, particularly across Asia, where many economies depend heavily on Middle Eastern oil imports. If demand recovery remains sluggish while production rebounds aggressively, conditions for a sustained oversupply could emerge.

However, not all market participants agree with the IEA’s assessment. OPEC officials and several industry observers have challenged the surplus narrative, arguing that the pace of supply recovery may be slower than anticipated and that depleted inventories will continue to absorb a portion of the returning barrels. The divergence between those expecting a glut and those emphasizing tight stock levels highlights the uncertainty currently facing the market. While the IEA’s warning has contributed to recent price weakness, its realization ultimately depends on supply recovering more rapidly than demand—a scenario that remains far from guaranteed. The debate between surplus risks and inventory-driven support is likely to remain a key driver of oil prices during the second half of the year.

Banks Cut Oil Price Forecasts

The rapid improvement in geopolitical conditions has triggered a broad reassessment among major financial institutions, with most revisions pointing toward lower oil prices. Investment banks that had previously incorporated a prolonged closure of Hormuz into their forecasts have quickly reduced their expectations following the breakthrough in US-Iran negotiations. The return of regional supply and the reopening of a critical shipping corridor have significantly reduced the scarcity premium that previously supported elevated forecasts.

Updated projections now point to Brent crude averaging around $80 per barrel during the fourth quarter, compared with earlier estimates that frequently exceeded $90 per barrel. Several institutions have also lowered their outlooks for the following year. These revised forecasts reflect expectations that tanker traffic through Hormuz will steadily recover over the coming months, easing supply constraints and reducing market tightness. Importantly, the adjustments extend beyond spot prices and have reshaped expectations across the entire forward curve.

The scale of these revisions illustrates how quickly market sentiment has shifted. Only weeks ago, many analysts were raising their forecasts based on assumptions that the disruption in Hormuz would persist through the summer, with some expecting Brent to trade above $100 per barrel for an extended period. The unexpectedly rapid progress toward a ceasefire has rendered those assumptions obsolete. The transition from increasingly bullish forecasts to widespread downgrades underscores the extent to which geopolitical developments have dictated market direction. While the revised outlook favors lower prices in the near term, institutions continue to acknowledge significant risks tied to the durability of the agreement and the pace at which supply ultimately returns.

The Trump Factor: Why Geopolitical Risk Has Not Disappeared

Despite the recent de-escalation, one of the biggest uncertainties facing the oil market remains the fragile nature of the agreement itself. President Trump has repeatedly emphasized that the memorandum should be viewed as an interim arrangement rather than a permanent settlement, warning that military action could resume if Iran fails to meet its commitments. While the agreement extends the ceasefire for 60 days and establishes a framework for broader negotiations, unresolved issues—including discussions surrounding Iran’s nuclear program—continue to pose risks to long-term stability.

Recent market reactions demonstrate how sensitive crude prices remain to geopolitical developments. Earlier in the week, oil prices briefly surged more than 1.5% after comments suggesting that military operations could restart if negotiations deteriorate. This response highlighted that a portion of the geopolitical risk premium remains embedded in the market and can quickly re-emerge whenever tensions escalate. The temporary nature of the agreement ensures that the coming weeks will be heavily influenced by headlines and diplomatic developments.

For oil traders, this remains the primary upside risk to an otherwise bearish narrative. The reopening of Hormuz and the prospect of returning supply support lower prices, but any breakdown in negotiations could rapidly reverse sentiment and trigger a renewed rally. Market participants must therefore balance improving fundamentals against the possibility of renewed conflict—a risk that remains difficult to quantify. As long as the ceasefire remains conditional and negotiations continue, crude prices are likely to remain highly sensitive to developments in US-Iran relations, leaving room for significant volatility despite the broader downward trend.

")

")

")

")

")

")