Oil prices climbed in Asian trading on Wednesday, extending the previous session’s gains after severe cold weather disrupted U.S. production, signaling tighter supply conditions.

Crude was also supported by a weaker dollar, which slid to near a four-year low this week, while markets continued to monitor heightened tensions between the United States and Iran following comments from President Donald Trump that a second armada was heading to the Middle East.

Brent futures for March edged up 0.1% to $67.66 a barrel, hovering near a four-month high, while U.S. West Texas Intermediate futures rose 0.2% to $62.53 a barrel by 20:49 ET (01:49 GMT).

Oil prices jump as U.S. snowstorm disrupts supply

Oil’s advance this week was largely fueled by a powerful winter storm sweeping across the United States, which disrupted crude output in several producing regions.

Exports from the U.S. Gulf Coast were also brought to a standstill, as heavy snowfall and sub-zero temperatures blanketed large parts of the country. According to Reuters estimates, roughly 2 million barrels per day of production were affected over the weekend.

These supply interruptions have prompted traders to brace for sharp drawdowns in U.S. crude inventories in the weeks ahead, signaling tighter supply conditions in the world’s largest oil-consuming market.

API data points to declining U.S. inventories

Figures from the American Petroleum Institute released late Tuesday showed an unexpected decline in U.S. crude inventories last week. Stockpiles fell by roughly 250,000 barrels, according to the API, defying expectations for a 1.45 million-barrel build.

The API report often foreshadows a similar trend in the official inventory data, which is scheduled for release later on Wednesday.

Oil gains on softer dollar ahead of Fed rate call

A weaker dollar also lent support to oil prices, as declines in the greenback tend to boost demand for commodities priced in the U.S. currency.

The dollar index fell to near a four-year low on Tuesday, weighed down by investor concerns over U.S. economic uncertainty, the impending Federal Reserve interest rate decision, and intermittent trade and geopolitical policy moves under President Donald Trump.

The Fed is broadly expected to keep interest rates unchanged at the end of its meeting later in the day, with markets focused on signals from Chair Jerome Powell regarding the policy outlook for the year ahead.

Oil prices were largely flat in Asian trade on Thursday as U.S. President Donald Trump eased tariff threats related to Greenland. Market participants also weighed an increase in U.S. crude inventories alongside recent supply disruptions. At 22:07 ET (03:07 GMT), March Brent futures inched up 0.1% to $65.31 a barrel, while WTI crude rose 0.2% to $60.74. Both benchmarks have posted modest gains over the past two sessions, underpinned by supply concerns after OPEC+ member Kazakhstan suspended production at the Tengiz and Korolev oilfields on Sunday.

Trump retreats from tariff threats against Greenland

Market sentiment improved after President Trump unexpectedly softened his position on Greenland on Wednesday, stepping back from threats to impose tariffs on European countries as leverage to annex the Danish territory. He ruled out the use of force and indicated that a framework for a potential deal was emerging, easing concerns over a sharp escalation in U.S.–EU tensions that could have pressured global growth and energy demand. The de-escalation supported broader risk appetite, although oil markets remained cautious amid mixed supply and demand signals.

U.S. crude inventories increase again, API data shows

The American Petroleum Institute (API) reported that U.S. crude stockpiles increased by 3.04 million barrels in the week ending Jan. 16, following a build of more than 5 million barrels the previous week. Gasoline inventories surged by 6.21 million barrels, signaling weaker demand, while distillate stocks—including diesel and heating oil—slipped by 33,000 barrels.

On the demand front, oil prices drew some support after the International Energy Agency raised its forecast for global oil demand growth in 2026 on Wednesday. Despite the upward revision, the IEA continues to expect the oil market to remain in a substantial surplus through 2026.

WTI crude prices edged lower to around $59.25 in early European trading on Tuesday.

Tensions surrounding Iran have eased in recent days following earlier speculation about a potential U.S. attack.

Market attention is now turning to developments around Greenland after President Trump threatened to escalate tariffs on eight European countries.

West Texas Intermediate (WTI), the U.S. crude oil benchmark, was trading near $59.25 during early European hours on Tuesday. Prices edged lower as concerns over supply disruptions from Iran eased, while traders continued to assess the implications of the U.S. push to take control of Greenland.

There were no signs of escalating tensions in Iran over the weekend, although Supreme Leader Ayatollah Ali Khamenei said that 5,000 people were killed in anti-government protests this month, according to Reuters. The easing of tensions has reduced the risk of a potential U.S. attack that could disrupt supplies from a major OPEC producer, weighing on WTI prices.

Traders are turning their focus to the Greenland crisis after U.S. President Donald Trump said on Saturday that Washington would impose an additional 10% import tariff from February 1 on goods from Denmark, Norway, Sweden, France, Germany, the Netherlands, Finland and the United Kingdom until the U.S. is permitted to purchase Greenland.

Trump is expected to discuss Greenland at the World Economic Forum in Davos, Switzerland, on Wednesday, while European Union leaders are set to hold an emergency summit in Brussels on Thursday. Concerns that tensions could escalate into a broader U.S.–EU trade war have weighed on market sentiment and may add selling pressure to oil prices.

“With fears around Iran easing in recent days following rumors of a U.S. attack, market attention has shifted to the Greenland issue and the potential depth of any fallout between the U.S. and Europe, as an expanded trade conflict could weigh on demand,” said Janiv Shah, an analyst at Rystad.

Meanwhile, the American Petroleum Institute’s (API) crude inventory report is due later on Tuesday. A larger-than-expected draw could signal stronger demand and support WTI prices, while a bigger-than-forecast build would point to weaker demand or oversupply, potentially pressuring prices lower.

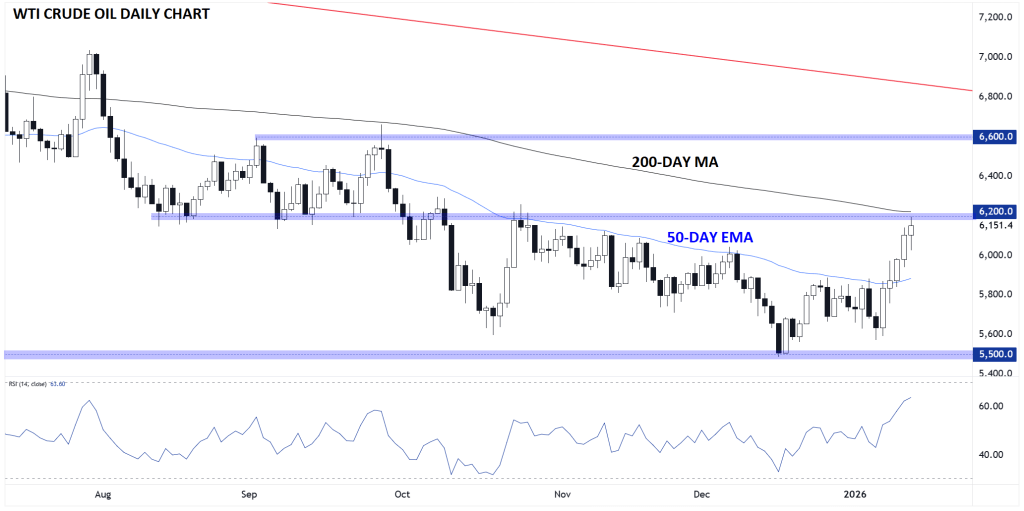

Oil prices are rising sharply, as WTI nears $62 and Brent crude moves up toward $66 per barrel. These increases highlight the market’s responsiveness to geopolitical tensions, despite no actual disruptions in supply. The question remains: where will prices go from here?

Main Highlights of WTI Crude Oil

WTI Crude Oil prices are sharply rising amid concerns that ongoing protests in Iran might escalate and impact production or disrupt the Strait of Hormuz.

However, this upward pressure is balanced by underlying fundamentals and a global surplus.

The current price around $62 is a crucial threshold: surpassing this resistance level could pave the way for a rally toward the six-month highs near $66.

In today’s trading environment, it can be difficult for market participants to isolate the key drivers of price action on a day‑to‑day basis. Beyond enduring themes like economic growth trajectories, inflation trends, the expansion of AI infrastructure, and sovereign debt pressures, fresh geopolitical tensions seem to emerge almost daily.

Amid simmering issues in places like Venezuela — and speculation about other potential flashpoints — Iran has become the dominant focus for energy markets. Nationwide protests there, sparked by severe economic strains and a collapsing currency, have raised serious questions about stability in one of the world’s most influential oil‑producing countries.

Although these demonstrations have not yet led to direct disruptions in oil output, the unrest has prompted traders to price in a growing geopolitical risk premium. Concerns about possible escalation — including the risk of broader conflict or disruption to key infrastructure such as the Strait of Hormuz, through which a large share of global seaborne oil exports transit — are contributing to recent volatility in crude prices.

As a reminder, Iran remains a key influence on global energy markets due to both its oil production capacity and its control over the Strait of Hormuz — a vital maritime chokepoint through which nearly 20 million barrels per day of crude and petroleum products transit, representing a large share of seaborne global oil flows. Any actual or perceived threat to exports or shipping through this route can have outsized impacts on pricing and risk sentiment.

Against this backdrop, oil prices have recently climbed, with Brent trading in the mid‑$60s and WTI previously approaching the $62 per barrel area, as traders price in geopolitical risk tied to the unrest in Iran. This reflects markets’ sensitivity to potential escalations, even though there have been no confirmed widespread production outages to date.

However, this upside is balanced by broader market fundamentals. Global oil inventories remain substantial, and additional output from other producers — including resumed Venezuelan exports and lingering oversupply concerns — continues to temper the rally. This backdrop helps explain why prices have fluctuated and, at times, pulled back when geopolitical anxieties ease.

Looking ahead, the future direction of crude prices is likely to hinge on developments in Iran’s domestic unrest and whether tensions translate into actual disruptions in oil production or interference with key export infrastructure such as the Strait of Hormuz. So far, most of the price appreciation has been driven by risk premium and sentiment rather than physical losses of barrels.

If broader instability were to disrupt supply routes or exports, markets could respond with a more pronounced and sustained price surge, particularly given the strategic importance of Middle East exports to the global oil system. However, short‑term moves are also currently influenced by macro factors such as inventory data and demand signals, as well as comments from policymakers that can quickly recalibrate risk perceptions.

Technical Analysis of Crude Oil: Daily Chart for WTI

Looking at the technicals, WTI Crude Oil is on a five-day winning streak, climbing from the lower end of its three-month trading range between $55 and $62 up to the upper boundary. Chart-wise, the current price level is a crucial threshold: a break above the $62 resistance — which also aligns with the 200-day moving average — could open the door for further gains toward the six-month highs around $66, where it would face resistance from the longer-term bearish trend line drawn from the second half of 2023’s peak.

Conversely, if indications emerge that the protests are easing and stability is being restored in Iran, the geopolitical risk premium currently weighing on crude prices may diminish. This could trigger a reversal, causing prices to retreat below the $60 mark. Regardless of the outcome, oil traders should closely monitor developments in Iran in the days ahead.

WTI crude slipped to around $60.70 during Wednesday’s Asian trading session, pressured by significant increases in U.S. crude stockpiles. Meanwhile, President Trump assured Iranian protesters that support is forthcoming.

West Texas Intermediate (WTI), the U.S. crude oil benchmark, was trading near $60.70 during Wednesday’s Asian session, as prices edged lower amid rising supply pressures. WTI has been pressured by Venezuela restarting oil exports and the latest American Petroleum Institute (API) report showing a large build in U.S. crude inventories, while traders await the official Energy Information Administration (EIA) stockpile figures later in the day.

According to Reuters and industry sources, Venezuela has begun reversing recent production cuts made under its previous U.S. oil embargo, allowing crude exports to resume. Two supertankers carrying roughly 1.8 million barrels each departed Venezuelan waters, potentially marking the first shipments under a 50‑million‑barrel supply arrangement with Washington, following U.S. control of the country’s exports after political developments.

U.S. crude inventories saw a significant increase last week, with the American Petroleum Institute (API) reporting a build of 5.27 million barrels for the week ending January 9. This contrasts sharply with the previous week’s drawdown of 2.8 million barrels and defies market expectations, which had forecasted a 2 million barrel decline.

Despite the growing stockpiles, ongoing geopolitical tensions in Iran—a key oil producer—could provide support for WTI prices. U.S. President Donald Trump canceled all planned meetings with Iranian officials and pledged assistance to protesters amid reports of a severe crackdown by Iranian security forces, which has resulted in hundreds of deaths. Trump has repeatedly warned that the U.S. would intervene if the Iranian government continues to target demonstrators.

Most Asian currencies weakened on Tuesday, with the Japanese yen falling to a one-year low, as higher oil prices fueled by unrest in Iran pressured the region. Meanwhile, new political and trade developments in the United States dampened investor sentiment.

The U.S. Dollar Index, which tracks the greenback against a basket of major currencies, rose 0.1% after a slight decline in the previous session. Dollar Index futures were also up 0.1% as of 03:36 GMT.

Japan’s currency drops to a one-year low following news of a possible snap election

The yen was the worst-performing currency, as USD/JPY climbed 0.4% to 158.76, its highest level since January 2025. The currency came under pressure after reports suggested that Prime Minister Sanae Takaichi could call a snap election as early as February. Investors speculated that a potential election win would strengthen her mandate for expansionary fiscal policies, further weighing on the yen.

Markets focus on Trump’s tariff threat, unrest in Iran, and higher oil prices

Risk appetite across Asia stayed cautious following U.S. President Donald Trump’s announcement of a 25% tariff on goods from countries “doing business” with Iran, though specifics on timing and coverage remain unclear.

Meanwhile, oil prices rose further amid deadly anti-government protests in Iran, sparking concerns over potential supply disruptions. The unrest has also led to warnings of possible military intervention from Trump, heightening geopolitical risk premiums.

MUFG analysts noted that Asian currencies may have been negatively affected by recent rises in oil prices, driven by events in both Venezuela and Iran.

They added that, aside from China, countries like Turkey, the United Arab Emirates, and to a lesser extent Russia and India, maintain some trade connections with Iran.

In Asia, the South Korean won (USD/KRW) rose 0.4%, marking its seventh consecutive gain. The Indian rupee (USD/INR) increased slightly by 0.1%, while the Singapore dollar (USD/SGD) remained stable. In China, the onshore yuan (USD/CNY) showed little movement, whereas the offshore yuan (USD/CNH) edged up 0.1%. The Australian dollar (AUD/USD) traded mostly flat.

Concerns over Fed independence trigger risk-averse sentiment

The Trump administration has launched a criminal probe into Federal Reserve Chair Jerome Powell regarding his testimony about renovation activities at the central bank’s headquarters, raising concerns about the Fed’s independence.

In response, Powell issued a statement affirming the Fed’s autonomy and assuring that policy decisions will remain based solely on economic data and the central bank’s mandate. Several former Fed chairs and senior officials have publicly expressed their support for Powell.

“It’s a wait-and-see situation as markets attempt to gauge the actual impact of these developments,” noted analysts from ING in a recent report.

Despite a softer U.S. dollar, Asian currencies found it difficult to gain, as investors remained focused on broader U.S. political risks, trade uncertainties, and rising oil prices.

Focus is also shifting to upcoming U.S. economic reports and any indications from the Federal Reserve, as market participants reevaluate interest rate forecasts amid increased political scrutiny of the central bank.

WTI prices rise amid growing supply concerns linked to escalating unrest in Iran.

President Trump has warned Tehran against using force on protesters, while Iran has warned the U.S. and Israel against any intervention.

However, oil price gains may be capped due to anticipated resumption of Venezuelan exports and forecasts of a potential market oversupply.

West Texas Intermediate (WTI) crude extended its gains for a third consecutive session, trading around $59.10 per barrel during Asian hours on Monday. The rise in oil prices is driven by growing supply concerns amid escalating protests in Iran. As OPEC’s fourth-largest producer, exporting nearly 2 million barrels per day, any conflict escalation poses a significant risk to global supply.

The unrest, now in its third week and having reportedly resulted in hundreds of casualties, has prompted Iranian authorities to signal a harsher crackdown. Meanwhile, U.S. President Donald Trump warned Tehran against using force on protesters and suggested possible intervention if the situation worsens, while Iranian officials cautioned against any U.S. or Israeli involvement.

Oil price gains may be restrained by expectations that Venezuelan crude exports could resume following political changes in the country, with the U.S. poised to receive or manage up to 50 million barrels of sanctioned oil under a new arrangement with interim authorities. This potential influx of supply has tempered some of the upside from geopolitical risk.

However, uncertainty remains over the timing and scale of Venezuelan shipments, as shifting U.S. policy and the logistics of restarting exports from dilapidated ports and vessels cloud the outlook for actual flows.

Meanwhile, traders are watching for possible supply disruptions from Russia amid ongoing Ukraine attacks on energy infrastructure and the prospect of tougher U.S. sanctions on Russian energy exports — factors that could add upward pressure on prices if they materially reduce output.

Oil prices remained mostly steady during Asian trading on Monday as investors balanced concerns over potential supply disruptions due to escalating unrest in Iran against the likelihood of more Venezuelan crude returning to the market.

As of 22:23 ET (03:23 GMT), March Brent crude futures rose slightly by 0.1% to $63.39 per barrel, while West Texas Intermediate (WTI) futures also increased by 0.1% to $59.15 per barrel. Both benchmarks had gained over 3% last week amid heightened geopolitical tensions.

Iran’s lethal protests raise fears of oil supply disruption

Markets have been closely monitoring Iran, a major oil producer in the Middle East, where widespread anti-government protests have escalated in recent days. According to rights organizations, over 500 people have died amid the unrest.

Iranian authorities have warned that U.S. military bases in the region would be targeted if Washington intervenes in support of the protesters. This threat has intensified concerns about a wider regional conflict that could disrupt oil shipments passing through the Strait of Hormuz, a critical artery for global energy supplies.

U.S. President Donald Trump adopted a tougher stance on Iran last week, declaring that the U.S. would not remain passive if Iranian forces continue harsh crackdowns on demonstrators.

“Iran, as the fourth-largest OPEC member, produces about 3.2 million barrels per day of crude oil, which represents a significant supply risk for the market,” ING analysts noted in a recent report.

Resumption of Venezuelan oil exports limits upside in oil prices

However, gains were limited by news from Venezuela, where U.S. officials indicated they might ease restrictions on the country’s oil sector. U.S. Treasury Secretary Scott Bessent said additional sanctions could be lifted as early as next week to help facilitate the sale of Venezuelan crude and support oil exports.

President Donald Trump also revealed plans for Venezuela to turn over up to 30 – 50 million barrels of previously sanctioned oil to the United States.

Despite the prospects of renewed output, major oil companies are cautious about re-entering the Venezuelan market without substantial legal and political reforms. ExxonMobil has described the country as “uninvestable” without major changes, and analysts note that firms whose assets were nationalised previously may be reluctant to return without adequate compensation.

Reflecting on the start of this century, the first striking observation is our national shortsightedness. After surviving Y2K and the dot-com crash in 2000, our leaders assumed the path ahead would be smooth sailing from year one onward.

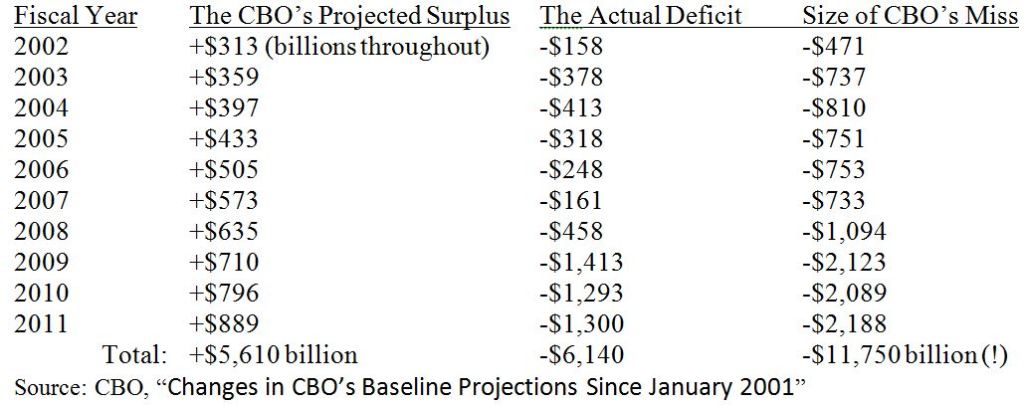

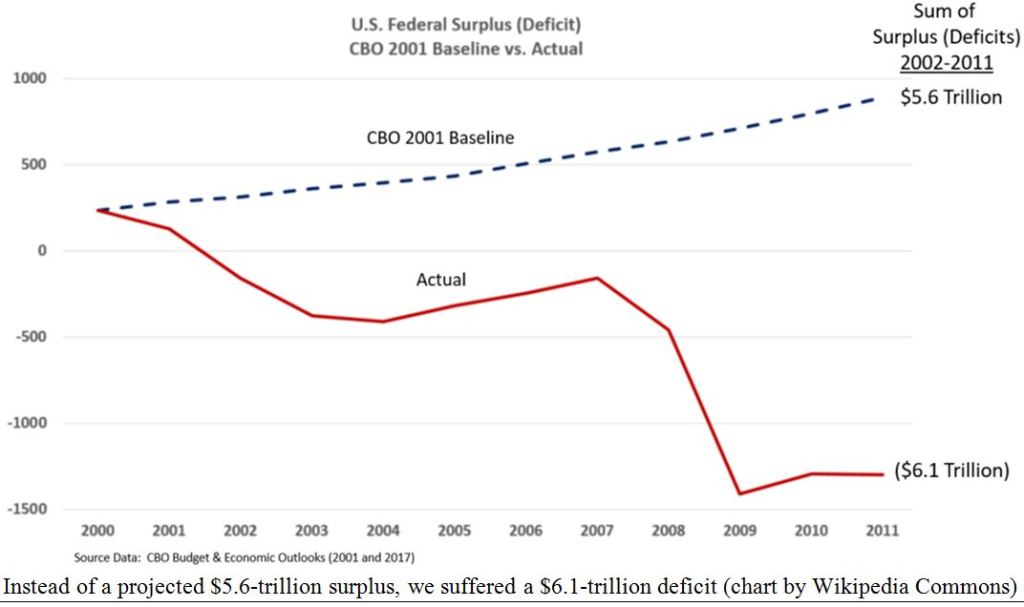

However, reality proved otherwise, beginning with a series of black swan events, notably the attacks on the World Trade Center and Pentagon on September 11. While such events are inherently unpredictable, it’s remarkable that the Congressional Budget Office (CBO) economists confidently forecasted in 2001 a future of continuous budget surpluses, anticipating the complete elimination of national debt by 2011.

For reasons unknown, the CBO issues 10-year federal spending and revenue projections, despite having no solid factual or practical foundation to accurately forecast beyond a year or two—akin to trying to predict the weather a year in advance.

The January 2001 CBO report highlights this myopia. Their projections simply extended current trends indefinitely without grounding in reality. Under this unrealistic mandate, the CBO projected a cumulative surplus of $5.6 trillion for 2002–2011.

In reality, deficits over that decade totaled $6.1 trillion—a swing of $11.7 trillion. It would have been much simpler to just flip a plus sign to a minus. The projections failed to account for the soaring costs of Bush’s “War on Terror” post-9/11, which led to prolonged wars in Afghanistan and Iraq, the bursting of the real estate bubble, and massive TARP bailouts to rescue large banks.

In short, this is a summary of CBO’s flawed foresight:

The first takeaway from this bleak forecast is that the CBO economists assumed deficits would increase in a smooth, predictable fashion—almost as if they were drawing a straight line with minor fluctuations, rather than reflecting the unpredictable realities of economic growth.

A second point is that the 2003 Bush tax cuts were not the main driver of the deficits. In fact, annual deficits dropped significantly—from $413 billion in fiscal year 2004 (which began October 1, 2003) to just $161 billion in fiscal year 2007. This means the deficit shrank by more than half during the four years following the tax cuts and before the 2007 real estate crash.

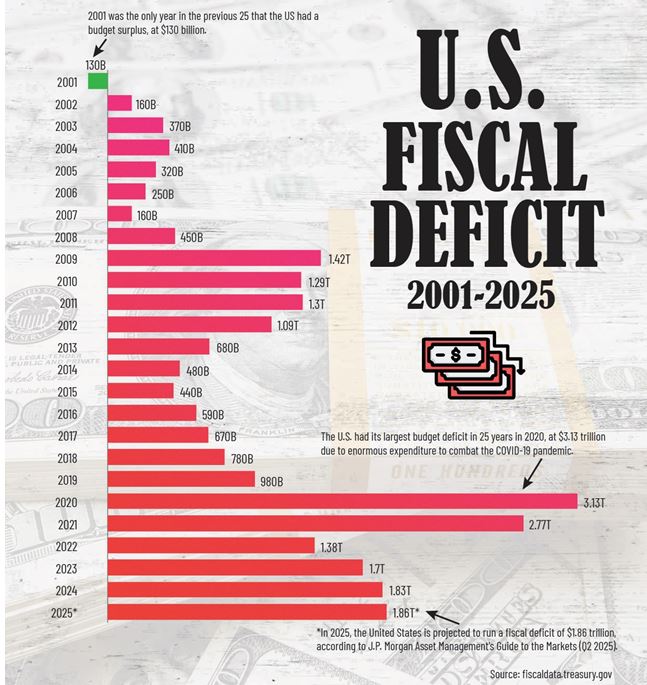

While much of this now feels like distant history, the ongoing wars and the Federal Reserve’s drastic response to the 2008 financial crisis—keeping interest rates near zero for eight years, essentially through the entire Obama administration—contributed to massive deficits that have persisted through to today, especially in the five years following the COVID-19 pandemic.

Since 2001, U.S. federal deficits have averaged about $1 billion annually, but that figure has surged to over $2 trillion per year since 2020, according to the U.S. Treasury.

Today, the total federal deficit stands at $38 trillion, which amounts to roughly $110,000 owed per American—far from the anticipated surpluses once projected.

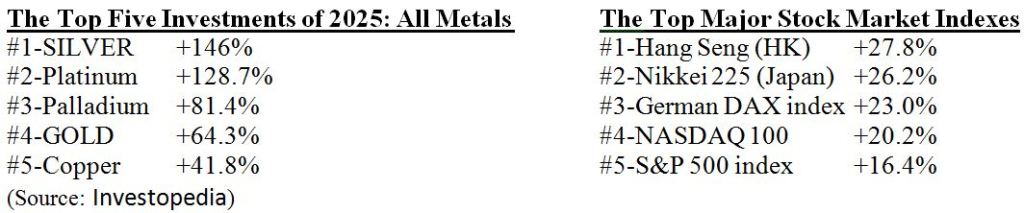

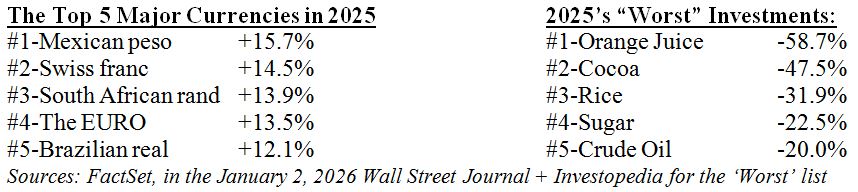

Following a Challenging 2000–2009, Markets Surged in the First Quarter

What about the markets? After nearly a “lost decade” lasting nine years from March 2000 to March 2009, all major market indexes have experienced remarkable growth—particularly gold relative to the U.S. dollar.

By March 9, 2009, three of the four major indexes—the S&P 500, NASDAQ, and Russell 2000—had fallen by 50% since the decade began (while the Dow was down 40%), but they bounced back strongly from 2009 through 2025:

Over the same 25-year period, the Consumer Price Index (CPI) increased by 83%, which means the real market gains were somewhat diminished.

The U.S. dollar performed even worse, losing about 10% in value overall (and 8% against the euro), while gold and silver surged more than 15 times in value:

The first-quarter returns were decent, but the strong performance of gold and silver signals that the dollar—and the CBO’s deficit forecasts—cannot be relied on in the long run. In fact, President Trump has set a goal for 2026 to deliberately weaken the dollar against the Chinese yuan to “help” exporters boost overseas sales. Much of the talk about the dominance of the “King Dollar” is just rhetoric. In reality, many politicians aim to devalue their currencies to encourage trade, turning paper money into a “race to the bottom,” while gold quietly holds its value, watching from the sidelines.

This brings us to the 2025 summary—a major victory for precious metals as the dollar dropped by 10%.

2025 Brought Massive Gains for Precious Metals

The year 2025 exemplified the key trends seen over the past 25 years—while the stock market continued to climb, gold and silver surged even faster. Although inflation is easing, gold today serves less as an inflation hedge and more as a safeguard against crises, a hedge against the dollar, and increasingly, a hedge against cryptocurrency volatility.

In 2025, the U.S. Dollar Index (DXY) dropped by 10%, allowing major global currencies to gain between 5% and 15%. Meanwhile, the poorest-performing investments of 2025 brought good news for consumers through lower food and energy prices:

So, if 2026 mirrors the gains of 2025, it will surely be a rewarding year for most investors.

TASIILAQ, GREENLAND — For decades, oil executives have eyed the Arctic as a potential source for vast petroleum reserves. U.S. government studies estimate that the region north of the Arctic Circle may contain up to 90 billion barrels of oil and nearly 1,700 trillion cubic feet of natural gas.

The amount of oil alone could meet global demand for almost three years if all other drilling activities worldwide stopped immediately.

At the heart of these ambitions lies Greenland, where some of the planet’s most extreme conditions safeguard vast reserves that have attracted prospectors hoping to find another giant oil field like Alaska’s Prudhoe Bay.

One company, March GL—set to be renamed Greenland Energy Company upon going public this year—is aiming to become a major player in the industry by tapping into billions of barrels of oil located on Jameson Land, a peninsula on Greenland’s eastern coast. This oil has the potential to significantly impact U.S. and European markets by introducing a large new supply, which could help reduce Europe’s reliance on Russian oil, currently constrained by strict sanctions due to the ongoing war in Ukraine.

In late October, Yahoo Finance joined March GL CEO and experienced oilman Robert Price, along with the company’s lead petroleum engineer, in the town of Tasiilaq on Greenland’s eastern coast. There, March GL’s contractors were preparing to store a range of heavy machinery for the winter season.

Price had planned to transport the earthmoving equipment by barge to Jameson Land, where the company intends to build a three-mile road from the coast to its inland drilling site for the initial wells. However, rough seas along the island’s eastern coast prevented the tugboat assigned to move the equipment from making the trip. By late autumn, the ice-free window for such a journey was closing too fast to wait for a replacement vessel.

As a result, March GL’s team will keep much of the machinery in Tasiilaq until spring or summer, when thawing ice will allow movement. This delay underscores the challenging and unpredictable operating conditions in Greenland.

Since that trip, the challenges around Price’s ambitions in Greenland have only grown more complex.

After Venezuelan leader Nicolás Maduro was captured and removed from power in early January, President Trump intensified his focus on Greenland. At a Jan. 4 press briefing, Trump said the United States “needs Greenland” to secure its national security interests in the Arctic, drawing strong criticism from both the Greenlandic and Danish governments.

At a White House meeting with more than a dozen major oil executives, Trump insisted that owning Greenland would be essential for defense, saying that defending leased territory is not the same as defending territory the U.S. owns. He added that the U.S. would take action on Greenland “whether they like it or not.”

In a Jan. 6 briefing to Congress, Secretary of State Marco Rubio confirmed that the U.S. was actively pursuing the option of purchasing Greenland from Denmark, and Louisiana Governor Jeff Landry—who Trump named as a special envoy to Greenland—said he intends to work toward making the territory part of the United States.

These moves have heightened diplomatic tensions, with Greenland’s leaders and Denmark pushing back against U.S. efforts and stressing that the island’s future should be decided by its people and legal processes.

Meanwhile, China and Russia have been expanding their military and maritime activities across the Arctic, putting pressure on the U.S. and Europe to boost their own defense readiness and elevating Greenland’s strategic importance. In January, a subsidiary of Russia’s state nuclear corporation shared a video on Telegram showing an icebreaker navigating the “Northern Sea Route,” which passes near Greenland and offers a significantly faster shipping route between Europe and Asia compared to the Suez Canal.

If March GL succeeds, Price’s company could establish a significant American energy foothold in the High North at a time when territorial control has become a top priority for the White House. That, however, was not originally part of Price’s plan.

Oil companies seeking to take part in newly approved exports of Venezuelan crude to the United States after the removal of President Nicolás Maduro are holding urgent talks to secure tankers and organize operations to safely transfer oil from ships and deteriorating Venezuelan ports, according to four sources familiar with the matter.

Trading firms and energy companies such as Chevron, Vitol, and Trafigura are vying for U.S. government contracts to export Venezuelan crude, the sources said, after President Donald Trump announced that Venezuela could deliver up to 50 million barrels of previously sanctioned oil to the United States.

Trafigura told the White House in a meeting on Friday that its first vessel is expected to load within the coming week.

After months under a U.S. blockade, Venezuela has been storing crude aboard tankers and has nearly exhausted its onshore storage capacity. Many of these vessels are aging, poorly maintained, and subject to sanctions. Due to insurance and liability restrictions, other ships cannot directly interact with sanctioned tankers—even if U.S. licenses are granted—sources added.

Onshore storage facilities have also suffered years of neglect, creating additional risks for companies attempting to load the oil.

Shipping firms including Maersk Tankers and American Eagle Tankers are among those seeking to expand ship-to-ship transfer operations in Venezuela, according to three of the sources.

According to one source, Maersk Tankers could reuse the ship-to-shore-to-ship logistics model it previously employed in Venezuela’s Amuay Bay. The company already operates in nearby Aruba and Curaçao, whose waters are frequently used for transferring Venezuelan oil. However, while such transfers are feasible in Aruba and at U.S. ports, they come at a higher cost.

In a statement, Maersk said its presence in Venezuela remains limited, with only 17 employees in the country. The company confirmed that all staff are safe and accounted for, and that there have been no changes to its ocean services. Operations are continuing with only minor delays, and the situation is being closely monitored.

Another shipping source noted that transfer operations will be further complicated by a shortage of smaller vessels needed to move oil from storage tankers to piers, where it can then be transferred to other ships, as well as by poorly maintained machinery and equipment.

American Eagle Tankers (AET), which already facilitates Chevron’s shipments of Venezuelan crude to the United States, is being contacted by potential customers seeking to expand its capacity in the region, two sources said.

Neither AET nor Chevron immediately responded to requests for comment.

Sources added that while exports could potentially return to the roughly 500,000 barrels per day that Venezuela shipped to the United States before sanctions—allowing stockpiles to be drawn down within 90 to 120 days—reaching that level will be difficult if crude must be sourced from both offshore tankers and onshore storage facilities.

Companies are also fiercely competing for loading slots at Venezuela’s main Jose oil terminal, where both capacity and operating speed are constrained. Chevron, a major joint-venture partner in the country, is working aggressively to maintain its preferential access to Venezuelan terminals while preparing its vessel fleet, according to one source.

Meanwhile, oil firms including Chevron, Vitol, and Trafigura are already securing supplies of much-needed naphtha, a Venezuelan industry source said. Naphtha is commonly blended with heavy Venezuelan crude to reduce its density, making it easier to transport and refine.

Oil prices advanced during Asian trading on Friday, extending the previous session’s rebound as investors focused on possible supply disruptions in Russia and Iran amid geopolitical risks.

At the same time, fears of an immediate rise in Venezuelan oil output subsided after the U.S. Senate approved a measure requiring congressional authorization for further military action by President Trump.

Analysts said oil production in the country is unlikely to increase sharply in the near term, even with U.S. intervention.

Brent crude futures for March rose 0.7% to $62.44 a barrel, while WTI futures gained 0.7% to $58.03 by 21:04 ET (02:04 GMT). Both benchmarks rebounded to levels seen before last week’s U.S. military action in Venezuela after posting more than 4% gains on Thursday.

Oil prices were supported by positive inflation data from China, the world’s top oil importer, signaling a tentative economic recovery. However, gains were limited as traders remained cautious ahead of key U.S. nonfarm payrolls data that could affect interest rate expectations.

Markets focus on potential supply disruptions in Russia and Iran

Concerns about possible supply disruptions in Russia and the Middle East lent support to oil prices this week.

The conflict between Russia and Ukraine showed little sign of resolution, with ongoing military actions. A drone strike on a tanker headed to Russia in the Black Sea heightened fears of further interruptions to Russian crude supplies.

Compounding these concerns, reports indicated that U.S. President Donald Trump plans to endorse a bipartisan bill imposing even tougher restrictions on countries trading with Russia, aiming to increase pressure on Moscow to seek a ceasefire.

Meanwhile, Iraq’s government approved a move to nationalize operations at the West Qurna 2 oilfield—one of the world’s largest—in an effort to avoid supply disruptions stemming from U.S. sanctions on Russia.

In Iran, escalating nationwide anti-government protests have raised worries about potential impacts on oil production. The government responded with a countrywide internet blackout as demonstrations spread across major cities protesting the Nezam regime.

Market concerns over Venezuelan oil supply ease

Oil prices benefited from easing worries that a U.S. intervention in Venezuela would lead to a significant near-term surge in global crude supply.

Earlier this week, Trump stated that Caracas could deliver up to $3 billion worth of oil to the U.S. and indicated plans for long-term U.S. influence over the country.

However, Congress has advanced legislation that may restrict U.S. military involvement in Venezuela.

Many analysts noted that while U.S. involvement could eventually help boost Venezuelan oil production, persistent political turmoil and deteriorated infrastructure make any near‑term surge in output unlikely.

Oil prices initially plunged after the U.S. detained Venezuelan President Nicolás Maduro and signaled control over the country’s oil industry, but prices had fully recovered by Friday as markets judged immediate changes to supply to be limited.

Still, crude prices were experiencing their steepest annual decline in five years in 2025, weighed down by concerns over a widening supply glut and sluggish demand growth—an outlook echoed by major global institutions forecasting continued oversupply into 2026.

Oil prices climbed during Asian trading on Thursday, regaining some losses after sharp declines triggered by worries over rising Venezuelan crude supplies.

Additionally, stronger-than-anticipated weekly declines in U.S. oil inventories supported the price recovery. Ongoing conflict between Russia and Ukraine also contributed to maintaining a risk premium in the market.

March Brent crude futures increased by 0.7% to reach $60.38 per barrel, while West Texas Intermediate (WTI) futures also gained 0.7%, settling at $56.28 per barrel as of 20:25 ET (01:25 GMT). Both benchmarks had fallen more than 1% over the previous two sessions.

Attention turns to US – Venezuela oil agreement after Trump highlights up to $3 billion in planned crude sales

Oil markets are closely watching the impact of a new agreement between the U.S. and Venezuela on global oil supplies.

U.S. President Donald Trump announced on Tuesday that Venezuela will deliver between 30 million and 50 million barrels of oil to the U.S., valued at up to $3 billion, shortly after U.S. forces detained Venezuelan President Nicolás Maduro.

Trump also appeared to encourage multiple U.S. oil companies to expand production activities in Venezuela, with Chevron Corp (NYSE: CVX) leading these efforts. According to Reuters, Chevron is negotiating to broaden its license to operate in the country.

Currently, Chevron is the only major U.S. oil company active in Venezuela, benefiting from special government exemptions that shield it from stringent sanctions imposed on the nation.

Markets are worried that a significant rise in Venezuelan oil output could further swell global supplies, adding to prevailing fears of an oil glut in 2026. Traders are already pricing in ample supply conditions, with expectations that any additional barrels from Venezuela might weigh on crude prices.

However, analysts caution that any meaningful increase in Venezuelan production is unlikely to happen quickly, given the country’s deep political instability and the extensive investment needed to rebuild its dilapidated oil infrastructure after recent upheavals.

A Financial Times report also noted that U.S. oil firms are seeking strong legal and financial guarantees from the U.S. government before committing to major investments in Venezuela’s oil sector, reflecting industry hesitancy amid uncertain policy and market conditions.

U.S. crude stockpiles decline beyond forecasts

Government data released Wednesday revealed that U.S. oil inventories fell by 3.8 million barrels in the week ending January 2, significantly exceeding expectations of a 1.2 million barrel decline.

This reduction was almost double the 1.9 million barrel draw reported the previous week, bolstering confidence that demand remains robust in the world’s largest fuel consumer.

Attention this week centers on several key U.S. economic reports, especially the December nonfarm payrolls data set to be released on Friday, which is expected to influence interest rate forecasts.

Oil prices tumbled in Asian trading on Wednesday after U.S. President Donald Trump said Venezuela would deliver tens of millions of barrels of crude to the United States, a development expected to significantly increase global supply. Prices were already under pressure earlier in the week, as Washington’s takeover of Venezuela fueled expectations of a broad easing of sanctions on the country’s oil sector—potentially releasing tens of millions of barrels back onto the market.

Despite elevated geopolitical risks adding a modest risk premium, oil prices stayed under pressure as markets grew increasingly concerned about a potential supply glut in 2026. Crude was already on track for its steepest annual decline in five years in 2025. Brent futures for March slid 1% to $60.11 a barrel at 20:13 ET (01:13 GMT), while U.S. benchmark WTI dropped 1.1% to $56.29 a barrel.

Venezuela to send 30–50 million barrels of crude to the United States, Trump says

In a post on social media, Trump said Venezuela would transfer between 30 and 50 million barrels of oil to the United States, with Washington planning to sell the crude at prevailing market prices. He added that the proceeds from the sales would be managed by him as U.S. president, stating that the funds would be used to serve the interests of both Venezuela and the United States.

The announcement follows just days after U.S. forces detained Venezuelan President Nicolas Maduro, when Trump said Washington was taking control of the country and planned to open up its oil sector. Oil prices initially fell after Maduro’s capture, as markets anticipated that a potential easing of U.S. sanctions on Venezuela could unleash large volumes of crude onto global markets. Trump’s actions since then suggest that this outcome is increasingly likely.

However, analysts cautioned that any reopening of Venezuela’s energy industry could take longer than expected, citing risks of political instability and the constraints of the nation’s aging infrastructure. Data from maritime analytics firm Kpler also indicated that a near-term increase in Venezuelan output is unlikely due to limited domestic storage capacity.

Russia-Ukraine ceasefire draws attention as U.S. backs security guarantees for Kyiv

Oil markets were also tracking any fresh developments in talks on a Russia–Ukraine ceasefire after the United States on Tuesday endorsed a largely European-led coalition that pledged to provide security guarantees for Kyiv.

The U.S. commitment was made at a Paris summit aimed at reassuring Ukraine in the event of a truce with Moscow. Washington also said it was prepared to help monitor and verify any ceasefire should an agreement be reached. However, Russia has so far shown limited willingness to engage in a ceasefire, with fighting between the two sides continuing as the war moves toward its fifth consecutive year.

Even so, any prospective ceasefire between Russia and Ukraine could ultimately lead to a rollback of U.S. sanctions on Moscow, allowing additional Russian oil to return to the market. Such a development would also reduce the geopolitical risk premium embedded in crude prices.

U.S. President Donald Trump said on Tuesday night that Venezuela’s interim government would transfer tens of millions of barrels of oil to the United States, with the proceeds from sales to be managed by Washington. In a social media post, Trump said Caracas would hand over between “30 and 50 million barrels of high-quality, sanctioned oil,” which would be sold at market prices. He added that the revenue would be overseen by him as president to ensure it benefits both the Venezuelan and U.S. people, and noted that he had directed Energy Secretary Chris Wright to implement the plan immediately.

The proposed arrangement could redirect Venezuelan oil exports away from China while helping state-run PDVSA avoid deeper production cuts, following reports that Washington and Caracas were in talks over a supply agreement. The announcement comes days after U.S. forces captured President Nicolas Maduro, heightening political uncertainty in Venezuela. Maduro’s vice president, Delcy Rodriguez, was sworn in as interim leader this week and has signaled her willingness to cooperate with Washington.

Trump said the United States would oversee Venezuela until a permanent leader is elected and would also assume control of the country’s aging oil sector. Following the announcement, oil prices fell, as a U.S. takeover could bring large volumes of crude to market and boost supply. March Brent futures dropped 2%.

The removal of Venezuela’s current leadership would likely signal a sharp shift in Washington’s stated objectives—from a focus on counter-narcotics pressure to a far more ambitious agenda: unlocking one of the world’s largest oil reserves and reopening the country to U.S. energy companies.

“The oil business in Venezuela has been a bust—a total bust—for a long period of time,” U.S. President Donald Trump told reporters on Saturday.

“We’re going to have our very large United States oil companies—the biggest anywhere in the world—go in, spend billions of dollars, fix the badly broken oil infrastructure, and start making money for the country.”

The central question for Trump’s administration is whether political change alone would be sufficient to revive an industry hollowed out by decades of mismanagement, corruption, and chronic underinvestment.

On paper, Venezuela’s oil potential is vast. Government figures put proven reserves at more than 300 billion barrels, the largest in the world, consisting largely of heavy crude prized by refiners along the U.S. Gulf Coast and in parts of Asia.

Analysts note that this heavy crude complements U.S. shale production, which is typically lighter and less suited to certain refinery configurations. In theory, Venezuela’s reserves could once again play a meaningful role in global energy markets.

In practice, however, the obstacles are formidable. Venezuela currently produces less than one million barrels per day—a fraction of its output two decades ago. Infrastructure has deteriorated severely, skilled workers have fled the country, and oil fields, pipelines, ports, and refineries would require massive capital investment merely to restore reliable operations.

Even under optimistic scenarios, years of rebuilding would be required before production could rise meaningfully. Market conditions add another layer of complexity: global oil supplies remain ample, and prices below $60 a barrel reduce the incentive for large-scale, high-risk investment abroad.

U.S. producers must therefore weigh whether capital is better deployed in stable domestic basins rather than in a country with a long history of expropriation and contract disputes.

Legal and institutional reform would also be indispensable. Venezuela would need to overhaul laws governing private investment, restructure roughly $160 billion in sovereign and quasi-sovereign debt, and resolve outstanding arbitration claims stemming from past nationalizations.

Without clear property rights and predictable regulatory frameworks, international oil companies are unlikely to commit billions of dollars, regardless of political change.

Security and governance challenges remain unresolved as well. Removing a leader does not automatically produce stability, and companies will wait to see whether a transitional government can maintain order, protect assets, and establish credible authority across the country.

The scale of reconstruction required extends far beyond oil extraction, encompassing financing, currency stabilization, and the rebuilding of core state institutions.

In that sense, unlocking Venezuela’s oil is ultimately less a question of geology than of politics, economics, and time.

OPEC+ delegates indicated that the group is expected to keep oil production steady at their upcoming meeting on Sunday, despite ongoing political tensions between key members Saudi Arabia and the UAE, as well as the recent U.S. capture of Venezuela’s president.

The Sunday meeting involves eight OPEC+ members—Saudi Arabia, Russia, the UAE, Kazakhstan, Kuwait, Iraq, Algeria, and Oman—who together produce about half of the world’s oil supply. This session follows a challenging 2025, during which oil prices plunged over 18%, marking their steepest annual decline since 2020 amid concerns over oversupply.

From April to December 2025, these eight members raised oil output targets by roughly 2.9 million barrels per day, representing nearly 3% of global oil demand. They agreed in November to pause further output increases for January through March 2026.

According to three OPEC+ sources, Sunday’s meeting is unlikely to alter this policy.

OPEC Faces Multiple Crises Amid Market and Political Challenges

Tensions between Saudi Arabia and the UAE escalated last month over a decade-long conflict in Yemen, when a UAE-aligned group seized territory from the Saudi-backed government. This crisis sparked the biggest rift in decades between the former close allies, exposing years of divergence on key issues.

Historically, OPEC has managed to navigate serious internal disputes—such as during the Iran–Iraq War—by prioritizing market stability over political conflicts. However, the group now faces multiple challenges. Russian oil exports remain under pressure from U.S. sanctions related to the Ukraine war, while Iran grapples with widespread protests and threats of U.S. intervention.

These overlapping crises put OPEC’s cohesion and its ability to manage the global oil market to a critical test.

On Saturday, the United States reportedly captured Venezuelan President Nicolás Maduro. U.S. President Donald Trump announced that Washington would assume control of the country until a transition to a new administration can be arranged, though he did not specify how this process would be carried out.

Venezuela holds the world’s largest proven oil reserves, surpassing even those of OPEC’s leader, Saudi Arabia. However, its oil production has sharply declined over the years due to chronic mismanagement and international sanctions.

Analysts caution that a significant increase in crude output is unlikely in the near future, even if U.S. oil majors follow through on the multibillion-dollar investments promised by President Trump.