Is Bitcoin’s legendary boom-and-bust cycle truly breaking down, or are traders simply misinterpreting recent price action? After rallying to around $126,000 and then plunging nearly 50% within months, Bitcoin is putting one of its most enduring narratives—the four-year cycle—under serious scrutiny.

From 2024 to 2025, claims that “the four-year cycle is dead” spread widely across crypto circles as Bitcoin repeatedly set new all-time highs, peaking near $126,000 in October. Prominent voices like Bitwise’s Matt Hougan and ARK Invest’s Cathie Wood supported this view, pointing to shifting market dynamics such as spot BTC ETFs, evolving regulation, and increasing institutional and government participation.

Yet after the roughly 50% correction over the past six months, many who dismissed the cycle have reversed course, once again favoring the traditional pattern. Still, the question remains: what if the original argument—that the cycle is changing—was right all along?

The four-year cycle, explained

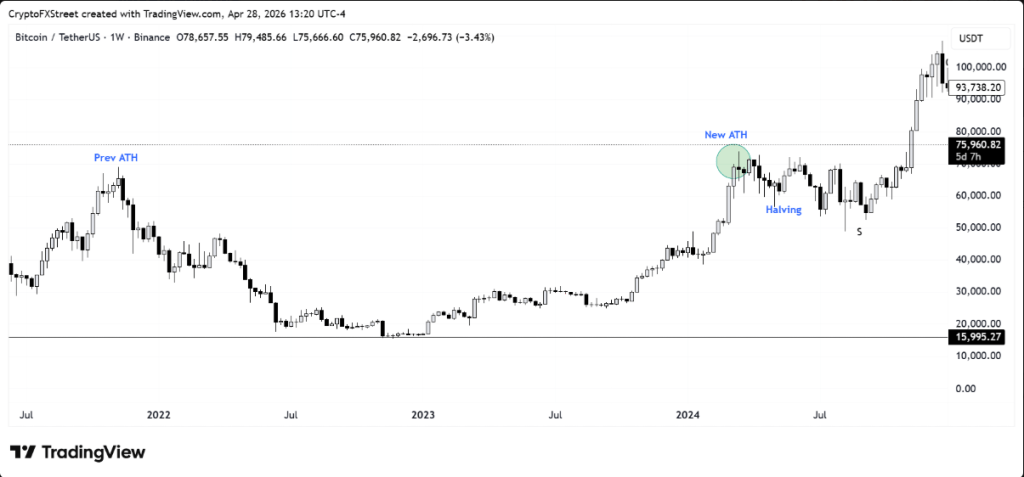

Bitcoin has historically moved in a repeating four-year rhythm, closely tied to its halving events. These cycles typically feature major bull market peaks and deep bear market bottoms spaced about four years apart. This pattern can be seen in Bitcoin’s record highs in November 2013, December 2017, November 2021, and October 2025—each occurring in the period following a halving.

A halving cuts the rate of new Bitcoin issuance by 50% roughly every four years, tightening supply and often fueling upward price momentum.

On the downside, Bitcoin has also followed a consistent pattern of steep corrections, with bear market lows marked by drawdowns of around 80% from prior highs—seen in January 2015, December 2018, and November 2022.

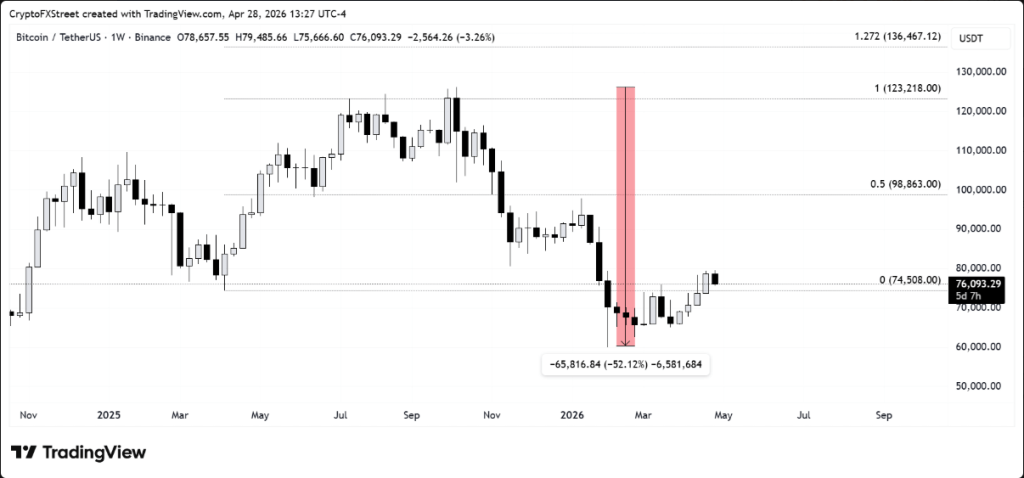

More recently, Bitcoin appears to be echoing this behavior, dropping about 50% from its $126,000 peak in October to around $63,000 by February. However, this could be one of the final instances where the market adheres so closely to the traditional four-year cycle.

Why calling the death of the four-year cycle in 2024 may have been premature

One of the main arguments for declaring the cycle “dead” was Bitcoin reaching a new all-time high before the April 2024 halving. This early surge was largely driven by strong inflows into newly launched spot BTC ETFs, which boosted demand ahead of schedule.

In previous cycles, Bitcoin typically set fresh record highs 16–18 months after a halving—not before it. So this unusual timing led many to believe that the traditional pattern had broken.

However, rather than signaling the end of the cycle, this shift may simply reflect front-loaded demand. The ETFs and rising institutional participation could have pulled forward the bullish phase, compressing or reshaping the cycle instead of eliminating it altogether.

Some argued that the arrival of traditional finance (TradFi) players via ETFs introduced entirely new market dynamics, since these participants don’t behave like native crypto investors. While there’s some truth to that, the argument overlooks a core driver of price action: supply and demand.

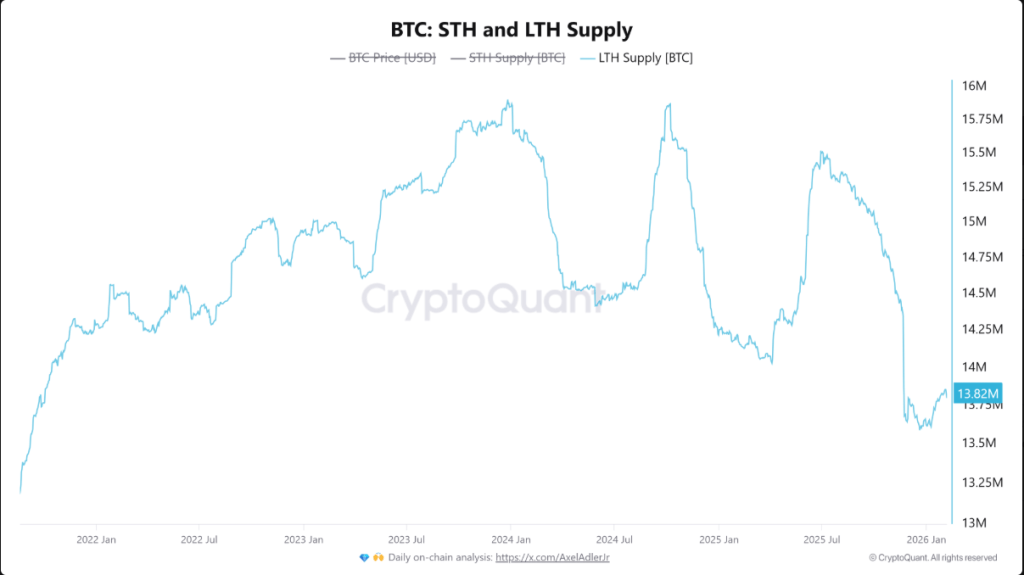

By the time ETF investors entered in January 2024, Bitcoin had already gone through about a year of bear market consolidation. During that phase, native crypto participants—long-time cycle followers, including whales and retail investors—had accumulated significant amounts of BTC, effectively becoming long-term holders (LTHs).

Sticking to the traditional cycle playbook, many of these holders maintained their positions, taking only partial profits, until around Q3 2025. This timing aligned with their expectations of a cycle peak. As a result, LTHs began distributing more heavily leading up to the final top on October 10.

In the months afterward, their holdings dropped sharply, with LTH supply falling to around 13.6 million BTC by December—the lowest level since 2021.

On the surface, the heavy distribution by long-term holders—combined with Bitcoin’s roughly 50% price drop—seemed to validate the familiar four-year cycle. However, it may instead signal a turning point, marking the beginning of that cycle’s breakdown and the rise of a new market structure.

Four-year cycle relevance may diminish over time

The current market reset suggests a gradual shift in Bitcoin ownership—from traditional cycle-driven participants to institutional players such as ETF investors and corporate treasuries like Strategy.

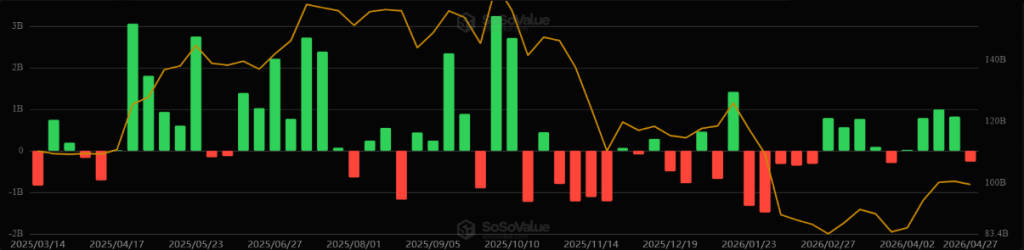

In just the past two months, US spot BTC ETFs have recorded net inflows of about $3.75 billion, while Strategy alone has accumulated over 100,000 BTC since the start of the year. The entrance of major financial institutions—highlighted by Morgan Stanley’s Bitcoin ETF launch in April—further signals that larger, more traditional players are taking a growing role in the market.

If this trend continues, and many crypto-native investors remain on the sidelines, the influence of the classic four-year cycle could steadily weaken. Price behavior already hints at this shift: the recent ~50% decline from Bitcoin’s all-time high is notably milder than the historical average of around 80% in past bear markets. If Bitcoin holds above $60,000, this would mark the shallowest drawdown in its history.

At the same time, halvings may carry less weight going forward. As Bitcoin’s total supply approaches its 21 million cap—with over 20 million already in circulation—the impact of reduced issuance naturally diminishes due to the law of diminishing returns.

As the market matures and institutional participation deepens, these structural changes could accelerate, pushing crypto-native investors to adapt their strategies to a new, less cycle-dependent environment.

Still, there’s room for error

To play devil’s advocate for the four-year cycle, recent behavior from ETF investors suggests the pattern may not be entirely gone.

Many ETF participants appeared to follow a familiar cycle-driven approach last year: strong inflows helped push Bitcoin to new all-time highs, but were later followed by significant outflows as investors rushed to lock in profits or limit losses after the October leverage flush.

This behavior mirrors the classic boom-and-bust rhythm seen in previous cycles, indicating that even newer institutional players may still be influenced—at least partially—by the same psychological and market forces that have historically shaped Bitcoin’s price action.

ETF investors, having now experienced a full boom-and-bust phase, may start factoring the four-year cycle into their strategies—potentially reinforcing it as a self-fulfilling pattern, much like crypto-native investors have done in the past.

At the same time, the true motivation behind ETF demand remains unclear. Unlike corporate holders such as Strategy, which openly embrace a long-term HODL approach, ETF investors represent a broad and diverse group with varying objectives.

Some may be drawn to Bitcoin as a store of value, others may be actively trading the familiar four-year cycle, and some—particularly hedge funds—could be exploiting arbitrage opportunities like the basis trade. This diversity makes it difficult to predict how their collective behavior will shape future market cycles.

So, is the four-year cycle dead?

A more balanced view is that Bitcoin’s cycle may weaken structurally, but still persist behaviorally. Going forward, price dynamics will likely depend less on halvings and more on how institutional capital chooses to act.

Leave a comment