Gold’s behavior during the recent U.S.-Iran conflict has defied both historical precedent and conventional market logic. Instead of rising when geopolitical tensions escalated and falling when tensions eased, gold has often done the opposite. However, several factors suggest this unusual pattern is likely temporary. If Iran continues to keep the strategically vital Strait of Hormuz closed, the near-term outlook for gold could become increasingly bullish.

Since the conflict began in late February, many of gold’s largest daily price swings have been driven by war-related headlines. Surprisingly, gold frequently sold off following military escalations and rallied on reports hinting at diplomatic progress. For example, gold fell sharply after Israeli strikes targeted Iran’s South Pars gas field, yet surged when reports emerged that the U.S. might accept an end to the conflict without reopening the Strait of Hormuz.

This “war-is-bearish, peace-is-bullish” relationship has become so pronounced that traders can often infer major geopolitical developments simply by observing gold’s overnight price action. A strong rally has typically signaled optimism about a peace agreement, while a steep decline has often coincided with military escalation.

Historically, gold has behaved very differently. Rising geopolitical risks have traditionally fueled safe-haven demand, attracting capital seeking protection from uncertainty. Following Russia’s invasion of Ukraine in 2022, for instance, gold climbed roughly 7.5% within two weeks. Yet despite the potentially larger economic consequences of the Iran conflict, gold has experienced a significant decline since the war began.

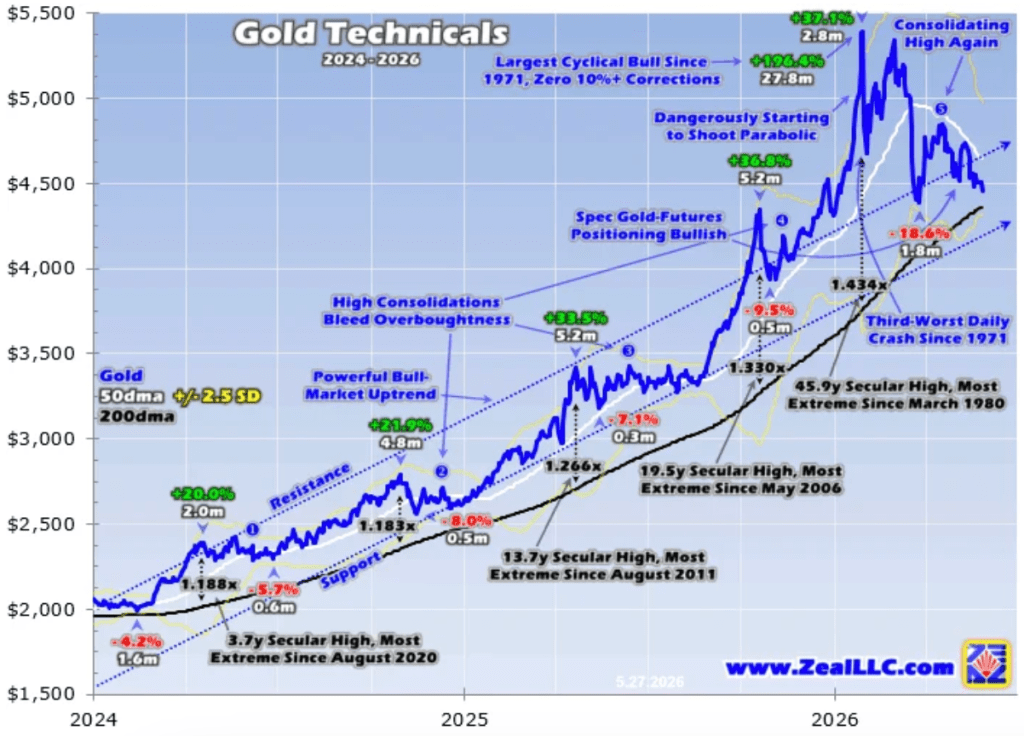

One explanation is that gold entered the conflict after an extraordinary multi-year bull market. By early 2026, gold had already posted one of the strongest cyclical advances in modern history, leaving the market extremely overbought and vulnerable to a major correction. Some of the initial weakness may therefore have reflected a natural rebalancing process rather than a response to geopolitical developments.

However, that explanation alone does not fully account for gold’s continued inverse reaction to war news. Analysts have increasingly pointed to another factor: gold has become a source of emergency liquidity for countries facing severe economic stress from soaring energy prices.

The closure of the Strait of Hormuz has disrupted a critical artery of global trade. Roughly one-fifth of the world’s oil and liquefied natural gas supplies pass through the Strait, along with significant volumes of fertilizers, sulfur, helium, aluminum, and other industrial materials. As energy prices surged, import-dependent nations faced mounting pressure on their currencies, trade balances, and inflation rates.

Turkey provides one of the clearest examples. Faced with a collapsing currency and soaring import costs, its central bank reportedly sold substantial amounts of gold reserves to stabilize financial conditions. This large-scale liquidation injected considerable supply into the market, contributing to gold’s sharp decline even as geopolitical risks intensified.

The situation gave rise to the “emerging-market piggy bank” thesis: countries struggling with higher energy costs may be forced to sell reserve assets—including gold—to fund imports, support their currencies, or subsidize domestic energy prices. Gold’s decline, therefore, may reflect forced selling rather than a lack of safe-haven demand.

India has faced similar pressures. As one of the world’s largest gold consumers and a major energy importer, it has experienced currency weakness and rising costs linked to the Strait closure. In response, Indian authorities significantly increased import duties on gold and silver, aiming to curb demand and reduce pressure on the country’s balance of payments. Concerns over weaker Indian gold demand further weighed on prices.

Taken together, Turkey’s reserve liquidations and India’s restrictions on gold imports appear to explain much of gold’s counterintuitive reaction to the conflict. These unusual circumstances have temporarily overwhelmed the metal’s traditional safe-haven role. As a result, gold’s recent tendency to fall on bad geopolitical news may be less a new market paradigm and more a short-lived anomaly driven by extraordinary economic stress in energy-importing nations.

Why Gold’s Unusual War Trade May Not Last

It is easy to understand why sentiment toward gold has turned increasingly negative in recent months. However, that does not necessarily mean gold will continue reacting negatively to escalating conflict. Like many popular market narratives, the current view appears overstated, and key data already challenges one of its central assumptions: central banks are not abandoning gold.

Following reports that Turkey sold large amounts of gold reserves to support its currency, many analysts expected global central-bank demand to collapse. Yet data from the World Gold Council showed otherwise. First-quarter 2026 central-bank purchases totaled 243.7 tonnes, virtually unchanged from the average pace of recent years. Turkey’s sales appear to have been a temporary liquidity measure rather than a structural shift away from gold.

Concerns about India’s higher gold import tariffs have also fueled bearish sentiment. While the new taxes could reduce Indian gold demand by roughly 25% this year, the potential shortfall represents only a small fraction of total global investment demand. Demand from other regions could easily offset much of that decline, particularly if inflation pressures intensify worldwide.

The larger issue is the ongoing disruption caused by the closure of the Strait of Hormuz. Prior to the conflict, roughly one-fifth of global oil consumption flowed through this critical shipping route. Although governments and companies have relied on strategic reserves and stored inventories to soften the blow, those buffers are steadily shrinking. As stockpiles decline, energy markets could face renewed supply pressures and significantly higher prices.

Iran appears to recognize that keeping the Strait effectively disrupted may be its strongest strategic leverage. By maintaining uncertainty around commercial shipping, it can continue exerting economic pressure without direct military escalation. The longer these disruptions persist, the greater the inflationary impact on the global economy.

Higher oil prices would raise transportation costs across virtually every industry, while fertilizer shortages and rising agricultural expenses could push food prices higher. Combined with weather-related challenges affecting crop production, inflationary pressures may become increasingly difficult to ignore.

Such an environment would likely strain economic growth, weaken corporate profits, and challenge elevated stock-market valuations. Rising inflation could also push bond yields higher, creating a more favorable backdrop for gold as a portfolio diversifier and inflation hedge.

Despite gold’s strong long-term performance, American investors remain significantly underexposed. The combined value of gold held through major U.S. gold ETFs represents only a tiny fraction of the value of the U.S. stock market. Even modest shifts in portfolio allocations toward gold could generate substantial new demand.

Meanwhile, gold futures positioning suggests speculative investors have plenty of room to increase exposure. After several months of consolidation, much of the excess enthusiasm that characterized gold’s record rally has been worked off, leaving the market in a healthier technical position.

As a result, the conditions for another upward leg in gold may be falling into place. While seasonal weakness could persist through early summer, rising inflation, tighter energy markets, and growing pressure on traditional financial assets could eventually reignite investor demand.

Bottom Line

Gold’s recent tendency to fall on worsening war news is likely an anomaly rather than a lasting trend. Much of the weakness can be traced to exceptional events such as Turkey’s reserve sales and concerns over India’s import restrictions. Yet global central-bank demand remains resilient, and the economic consequences of prolonged energy disruptions could ultimately strengthen the investment case for gold.

If inflation accelerates as energy and food prices rise, investors may once again turn to gold for protection and diversification. Given how little gold many stock investors currently own, even a modest reallocation of capital could provide meaningful support for prices in the months ahead.

Leave a comment