Key Insights

- International investors and governments increased their holdings of U.S. Treasury securities to an all-time high of $9.49 trillion in February 2026, with holdings rising $587 billion year-over-year and nearly $200 billion in a single month.

- Central banks continued accumulating gold, adding 244 tonnes during the first quarter of 2026 and extending a buying streak that has lasted 17 months. However, because gold is traded globally in U.S. dollars, this trend still reinforces the dollar’s central role in the financial system.

- The United Arab Emirates’ decision to withdraw from OPEC/OPEC+ came shortly after U.S. officials endorsed a potential emergency dollar liquidity arrangement for Abu Dhabi, highlighting the strategic influence of dollar-based financial support.

- U.S. sanctions efforts against Iran have successfully frozen $344 million worth of cryptocurrency assets, illustrating how digital financial infrastructure linked to the dollar can strengthen U.S. economic enforcement power.

- Overall, evidence from Treasury market demand, rising foreign capital inflows, and expanding digital-dollar adoption suggests that predictions of the dollar’s decline are not supported by current data.

For years, predictions of the US dollar’s decline have dominated headlines, and those claims have only grown louder. Critics argue that BRICS nations are creating a viable alternative to the dollar, China is reducing its holdings of US Treasuries, gold is poised to replace the dollar as the world’s primary reserve asset, and the US government is struggling to attract buyers for its mounting debt—so much so that it is allegedly using dollar swap lines with Gulf nations as an indirect liquidity support mechanism.

While these arguments make for a compelling narrative, the underlying data tells a different story. Despite the persistent warnings from dollar skeptics, there is little evidence to suggest that the dollar’s dominant role in the global financial system is meaningfully eroding.

The dollar’s dominance is far from disappearing. If anything, the developments seen in late April 2026 provided one of the strongest pieces of evidence in years that its position in the global financial system remains firmly intact.

Theory vs. Reality

For years, I’ve argued that the “dollar collapse” narrative mistakenly equates inflation with currency debasement. Those are not the same thing. A currency cannot realistically be considered debased when global demand for it continues to intensify. We’ve explored this rebasement perspective before in our discussions of the dollar’s global funding system and in The Dollar’s Death Is Greatly Exaggerated. The latest figures only strengthen the case that the U.S. dollar remains firmly dominant.

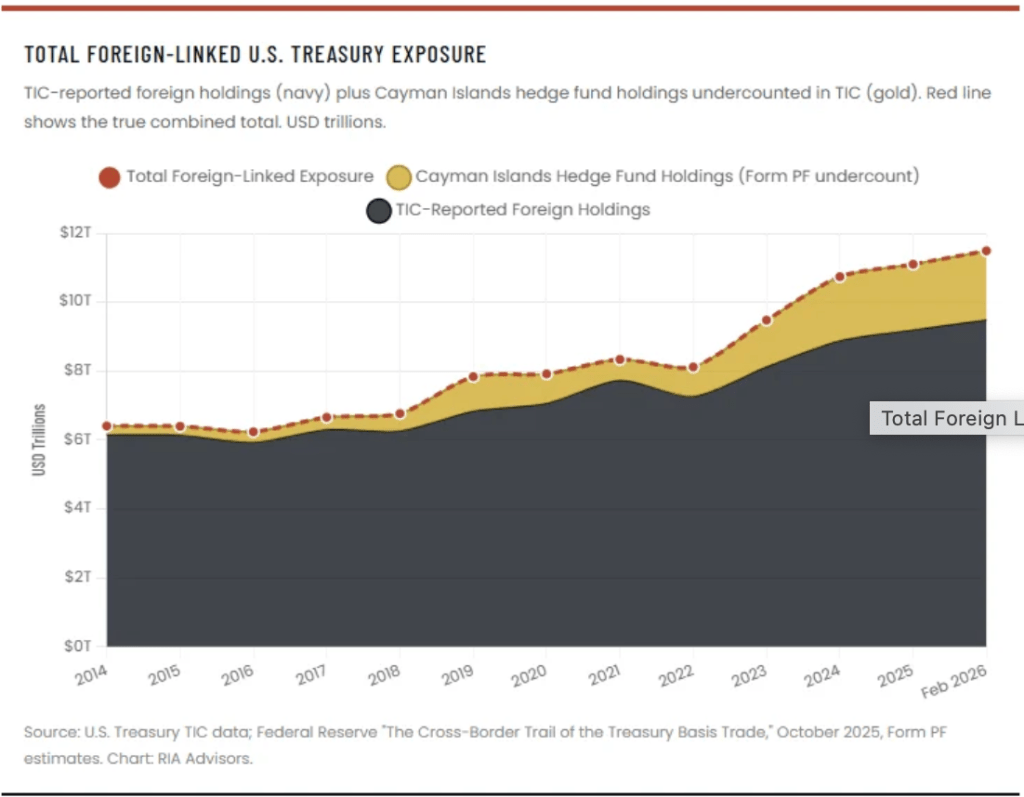

The most recent Treasury International Capital (TIC) report from the U.S. Treasury, released on April 15 and covering February 2026 activity, showed foreign investors purchased $101 billion of long-term U.S. securities in a single month. Total net TIC inflows reached $184.5 billion, while foreign investors also increased their Treasury bill holdings by another $91.6 billion. As a result, foreign ownership of U.S. Treasuries climbed to a record $9.49 trillion in February, rising by $198 billion during the month and by $587 billion over the previous year.

Even that record figure understates the true scale of foreign demand. It excludes Treasury exposure held through U.S.-based hedge funds and the Cayman Islands basis trade. According to Federal Reserve estimates, these channels account for roughly an additional $1.5 trillion of effective foreign demand. When those positions are included, total foreign-linked exposure to U.S. Treasuries approaches $11 trillion, underscoring the continued global appetite for dollar-denominated assets.

Looking beyond the total amount of debt outstanding, the flow data paints the same picture. Indirect bidders—widely viewed as a gauge of foreign demand—have consistently accounted for more than 70% of successful bids in recent Treasury auctions. Meanwhile, bid-to-cover ratios for both 10-year and 30-year Treasury sales have remained above 2.5 through multiple market cycles, signaling robust investor appetite.

If the world were genuinely abandoning the dollar, the evidence would look very different: weaker auction participation, higher yields caused by poorly received offerings, and a rising term premium as investors demanded greater compensation to absorb excess supply. Yet the data points in the opposite direction. Despite the U.S. running approximately $2.5 trillion in deficits over the past year, global investors have continued to absorb the resulting Treasury issuance with little difficulty.

Far from resembling a rush for the exits, these trends suggest exceptionally strong demand. In fact, they point to one of the most powerful and persistent periods of global demand for U.S. government debt ever recorded.

How Central Bank Gold Purchases Strengthen the Dollar’s Position

This is where many dollar-collapse narratives begin to break down. Gold advocates often make a fundamental mistake by treating central bank gold accumulation as proof that the world is abandoning the U.S. dollar. The reality is more nuanced.

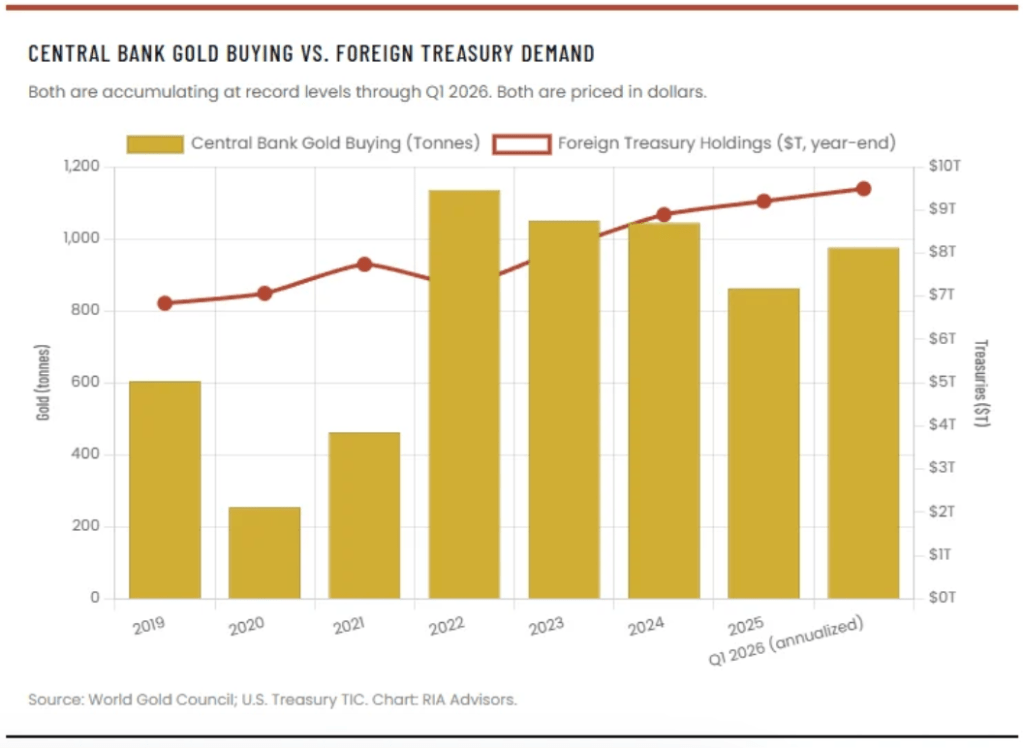

There is no dispute that central banks have been aggressively increasing their gold reserves. According to the World Gold Council’s Q1 2026 Gold Demand Trends report, released on April 29, official-sector institutions purchased a net 244 tonnes of gold during the first quarter alone, a 3% increase from the same period a year earlier. That marked the seventeenth consecutive month of net central bank buying, despite gold prices surpassing $5,400 per ounce in January. Physical gold demand reached 474 tonnes during the quarter, making it the second-strongest first quarter on record. Looking ahead, the World Gold Council expects central banks to purchase approximately 850 tonnes of gold throughout 2026, broadly matching 2025 levels and extending a multi-year trend of substantial accumulation.

The trend is both genuine and important. However, interpreting it as evidence of a mass exodus from the dollar is a leap that the data does not support. Central banks are adding gold primarily as a reserve diversifier and geopolitical hedge, not as a replacement for the dollar-based financial system. Gold can store value, but it cannot replicate the liquidity, collateral function, settlement infrastructure, or global financing role provided by U.S. Treasury securities and dollar-denominated markets.

In other words, rising gold reserves and continued dollar dominance are not mutually exclusive. Central banks can accumulate gold while still relying heavily on dollars for trade settlement, reserve management, cross-border financing, and international liquidity. The growth of official gold holdings reflects diversification at the margin—not a practical abandonment of the world’s primary reserve currency.

A key point often overlooked in de-dollarization debates is that gold itself remains deeply embedded within the dollar-based financial architecture. Gold may be a reserve asset, but it is still primarily valued through a dollar lens. The London Bullion Market Association (LBMA) benchmark—the global standard used to value central bank gold holdings—is quoted in U.S. dollars per ounce. Whether it is the People’s Bank of China, the National Bank of Poland, or the Reserve Bank of India increasing its gold reserves, those holdings are ultimately measured, reported, and assessed in dollar terms.

The same principle applies when central banks use gold as a source of liquidity. Whether through swaps, repurchase agreements, or outright sales, transactions are typically priced against dollar benchmarks. Gold and dollars are therefore not competing monetary systems operating independently of one another. Rather, gold functions as a reserve asset within a broader framework that is still largely organized around the U.S. dollar.

This distinction fundamentally changes how central bank gold purchases should be interpreted. If a central bank reallocates 5% of its reserves from U.S. Treasuries into gold, that does not constitute an exit from the dollar system. It is simply a portfolio adjustment within a reserve structure where assets continue to be valued and compared using dollar-based metrics. The same logic applies to gold swaps conducted through the Bank for International Settlements, yuan-denominated contracts traded on the Shanghai Gold Exchange, and even the large gold accumulation programs undertaken by Central Bank of the Russian Federation before sanctions. Regardless of the transaction venue or currency of quotation, reserve managers still evaluate those positions against their dollar-equivalent value.

Viewed through that lens, growing gold reserves do not necessarily undermine dollar dominance. In many respects, they reinforce it by relying on the dollar as the world’s primary unit of account for reserve wealth.

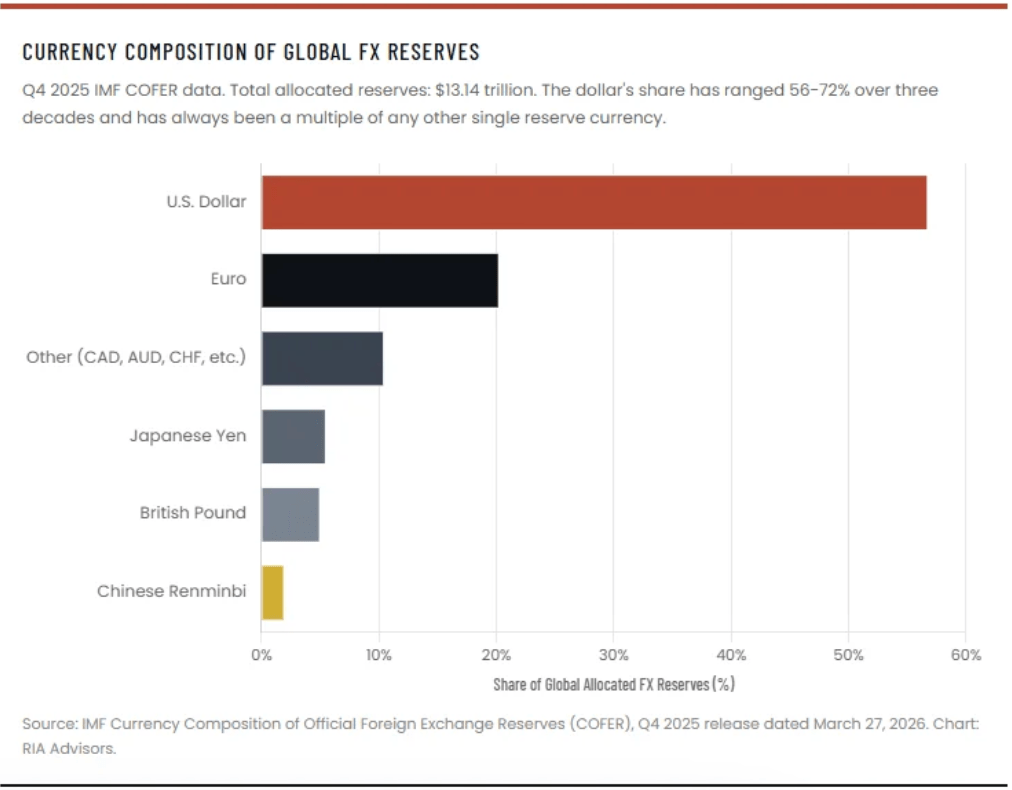

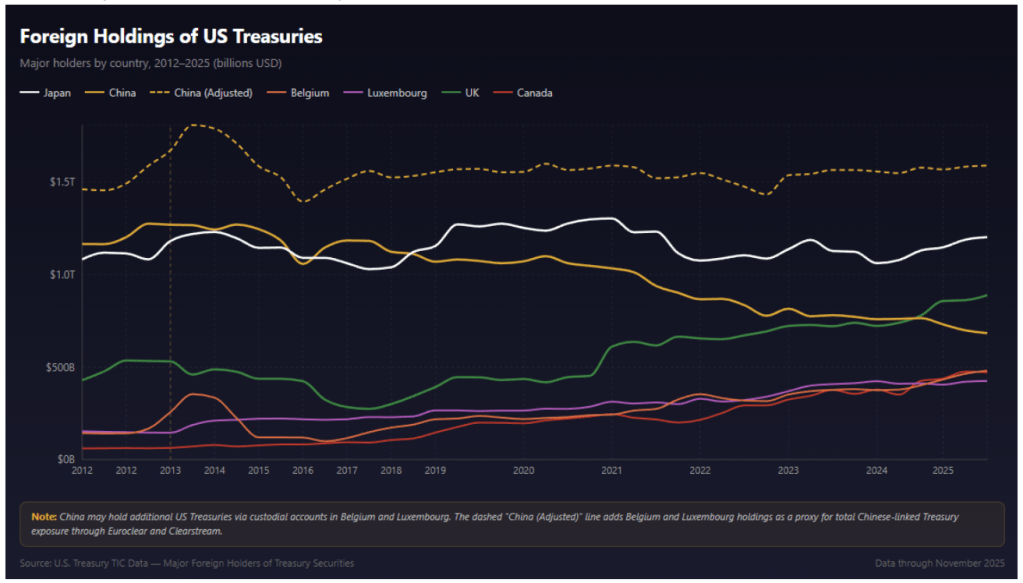

The same surveys frequently cited as evidence of de-dollarization illustrate this nuance. While many central banks expect the dollar’s share of reserves to gradually decline over the coming years, actual reserve data tells a more measured story. According to the IMF’s COFER statistics for the fourth quarter of 2025, the U.S. dollar accounted for roughly 56.8% of allocated global foreign-exchange reserves. Although lower than the levels seen decades ago, that share remained broadly stable, with much of the quarter-to-quarter movement attributable to exchange-rate fluctuations rather than aggressive reserve liquidation.

At the end of 2025, total global foreign-exchange reserves stood above $13 trillion. Within that pool, the dollar remained by far the dominant reserve currency, holding a share that exceeded the combined weight of every major competitor except the euro. The euro represented roughly one-fifth of allocated reserves, while the Japanese yen and British pound each accounted for about 5%. Despite persistent discussion of its rise, the Chinese yuan continued to represent only a small fraction of global reserve holdings.

The broader takeaway is that reserve diversification and de-dollarization are not synonymous. Central banks may seek greater exposure to gold or other currencies, but the available data still points to a global reserve system in which the dollar remains the primary benchmark, funding currency, and store of international liquidity.

Bessent’s Dollar Swap Strategy Expands Dollar Dominance

Recent discussions surrounding potential new dollar swap lines have provided another example of how U.S. policymakers are working to reinforce, rather than merely defend, the dollar’s global position.

Treasury Secretary Scott Bessent has recently floated the idea of extending dollar swap arrangements to key partners in the Persian Gulf and Asia, with the United Arab Emirates frequently mentioned as a leading candidate. Critics have interpreted the proposal as an emergency measure designed to prevent foreign holders from selling U.S. Treasuries amid geopolitical tensions in the Middle East. However, that interpretation overlooks the broader strategic objective.

Bessent’s own comments suggest a different motivation. He has emphasized that swap lines help maintain stability in dollar funding markets and reduce the risk of disorderly asset sales during periods of stress. More importantly, he has argued that expanding swap-line networks can strengthen international dollar usage and create additional dollar funding hubs across strategically important regions.

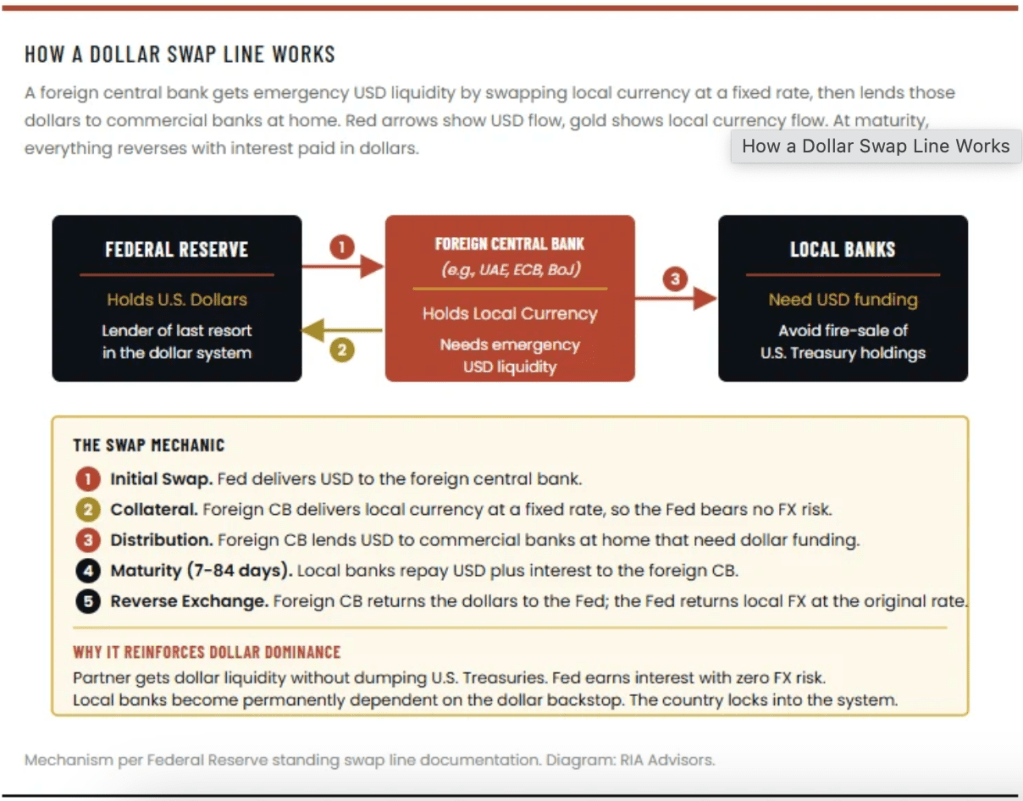

At its core, this approach is about infrastructure. Dollar swap lines are one of the most powerful tools available for extending the reach of the global dollar system. During the 2008 financial crisis, swap lines were deployed primarily as a defensive measure, providing dollar liquidity to foreign central banks and preventing disruptions in global funding markets. The emerging strategy seeks to use the same mechanism more proactively by deepening the dollar’s presence in regions where competing financial architectures have been gaining attention.

The logic is straightforward. When a central bank receives permanent or highly reliable access to dollar liquidity through a swap arrangement, its domestic financial institutions gain confidence that dollars will remain available during periods of market stress. That assurance strengthens incentives to continue conducting trade, financing, and reserve management activities in dollars rather than investing heavily in alternative systems.

From a network perspective, every new swap line effectively creates another node within the global dollar ecosystem. Countries connected to these facilities become more deeply integrated into dollar funding markets, increasing the currency’s utility and reinforcing its network effects. This dynamic helps explain why existing swap-line arrangements among the United States, the European Central Bank, Japan, United Kingdom, Canada, and Switzerland have remained central pillars of the international monetary system since the global financial crisis.

Viewed through this lens, proposed Gulf and Asian swap lines are less about preventing a collapse in Treasury demand and more about extending the geographical footprint of the dollar system. Rather than signaling weakness, they represent an effort to strengthen the institutional infrastructure that underpins the dollar’s reserve-currency status and global liquidity role.

The broader implication is that dollar dominance is sustained not only by the size of the U.S. economy or the Treasury market, but also by the network of financial relationships that make dollars readily available around the world. Swap lines are one of the clearest examples of how that network continues to expand.

More importantly, this strategy is no longer merely theoretical. Advocates argue that Treasury Secretary Scott Bessent has already demonstrated the model in practice through a swap facility extended to Argentina in 2025. The objective was straightforward: provide dollar liquidity to a strategic partner during a period of political uncertainty, stabilize financial conditions, and reinforce that country’s integration into the global dollar system. The reported repayment of the facility within a relatively short period strengthened the case that such arrangements can function as effective tools of financial diplomacy rather than permanent rescue programs.

Under this framework, swap lines serve as an incentive mechanism. They offer trusted partners access to the world’s deepest pool of liquidity and strengthen their ties to dollar-based funding markets. Proposed arrangements with Gulf states and Asian economies can therefore be viewed as efforts to expand the geographic reach of the dollar network rather than emergency measures aimed at defending Treasury demand.

At the same time, the United States retains a second source of influence: its ability to enforce financial restrictions through sanctions, regulatory oversight, and control of key financial infrastructure. In this interpretation, dollar dominance is supported by both incentives and enforcement. Countries gain significant benefits from participating in the dollar system, but they are also aware of the costs associated with operating outside it.

Recent actions targeting Iranian financial networks illustrate this point. Through sanctions programs administered by the Office of Foreign Assets Control and other agencies, the U.S. government continues to demonstrate its capacity to restrict access to international financial channels and freeze assets connected to sanctioned entities. These measures highlight the extent to which global finance remains intertwined with institutions, payment systems, and compliance frameworks linked to the dollar.

The implications extend beyond traditional banking. Cryptocurrencies and stablecoins are often portrayed as alternatives to the existing monetary order, but many of the largest digital-asset ecosystems remain dependent on regulated exchanges, custodians, issuers, and financial intermediaries. As a result, authorities can frequently exercise influence through compliance requirements and enforcement actions, limiting the extent to which these networks operate entirely outside government oversight.

From this perspective, dollar dominance is reinforced through two complementary forces. The first is attraction: deep capital markets, abundant liquidity, reserve-currency status, swap-line access, and the global demand for U.S. Treasury securities. The second is enforcement: sanctions authority, asset freezes, financial blacklists, and regulatory reach. Together, these mechanisms create powerful incentives for governments, banks, and reserve managers to remain connected to the dollar ecosystem.

This does not mean that countries are abandoning efforts to diversify reserves or reduce specific vulnerabilities. Many continue to increase gold holdings, explore alternative payment arrangements, and spread custodial risk across jurisdictions. However, diversification is not the same as disengagement. For many reserve managers, the calculation remains that participation in the dollar-centered financial system offers benefits and stability that are difficult to replicate elsewhere, even as they seek greater flexibility around the margins.

The UAE’s Exit and the De-Dollarization Debate

Supporters of the dollar-dominance thesis point to recent developments in the Gulf as evidence that financial influence often matters as much as formal reserve statistics. In their view, the reported decision by the United Arab Emirates to distance itself from the traditional OPEC framework came at a strategically significant moment, coinciding with discussions about closer financial cooperation with Washington.

The argument focuses on sequence and incentives. During a period of heightened regional uncertainty and financial stress, U.S. policymakers discussed expanding dollar liquidity support to key partners. At the same time, senior UAE officials engaged with representatives from the U.S. Treasury, the International Monetary Fund, and the Federal Reserve System. Proponents of this interpretation argue that access to dollar liquidity, security cooperation, and deeper integration into U.S.-led financial networks created powerful incentives for closer alignment with the dollar-based system.

From that perspective, swap lines are not simply emergency funding mechanisms. They are strategic tools that deepen economic ties and strengthen the network effects that support the dollar’s global role. The broader claim is that countries offered reliable access to dollar liquidity have fewer incentives to build alternative financial architectures around competing currencies.

As a result, advocates argue that this episode weakens the long-running “petroyuan” narrative. Rather than seeing a major Gulf economy move toward a yuan-centered energy pricing system, they see another example of a strategically important state reinforcing its links to the dollar ecosystem.

Counterargument: Does De-Dollarization Still Matter?

The strongest de-dollarization case remains a serious one. Following the freezing of roughly $300 billion of Russian reserves in 2022, many governments concluded that reserve assets held within Western financial systems carried political and geopolitical risks. This prompted efforts to diversify reserve management practices, expand local-currency trade arrangements, accumulate gold, and explore alternatives to traditional dollar settlement networks.

Examples frequently cited include growing cooperation among BRICS members, increased bilateral trade settlement between China and Russia, and shifts in custodial arrangements for foreign-exchange reserves. These developments are real and reflect an ongoing desire among some countries to reduce exposure to potential sanctions risk.

However, supporters of the dollar-dominance view argue that these changes have largely occurred within the existing financial architecture rather than outside it. Moving Treasury holdings from direct custody in the United States to institutions such as Euroclear changes where assets are held, but not necessarily what assets are held. Likewise, increasing bilateral trade settlement in yuan or other currencies does not automatically create a viable alternative to the broader dollar-based system.

The core challenge for de-dollarization remains scale. A reserve currency must provide deep and liquid capital markets, a large supply of high-quality collateral, broad convertibility, legal protections, and global acceptance. While alternatives have made incremental gains, none have yet matched the combination of liquidity, market depth, and network effects that support the dollar.

As a result, the debate today is less about whether diversification is occurring—it clearly is—and more about whether diversification at the margins is sufficient to fundamentally reshape the global monetary system. Thus far, the evidence suggests gradual evolution rather than a rapid displacement of the dollar’s central role.

The key mistake in many de-dollarization arguments is treating diversification as if it were abandonment. Those are not the same thing. Foreign reserve managers are increasingly diversifying where they hold assets and expanding allocations to gold, but neither trend necessarily implies a departure from the dollar-centered financial system.

In practice, many central banks are pursuing two parallel objectives. First, they are reducing custodial concentration by spreading reserve assets across multiple jurisdictions and institutions. Second, they are increasing gold holdings as a hedge against geopolitical and financial uncertainty. Yet these adjustments leave the dollar largely intact as the world’s primary unit of account, dominant settlement currency, and leading reserve asset. Reserve composition may be evolving at the margins, but the underlying structure of the system remains remarkably stable.

The dollar’s influence is also expanding through channels that traditional reserve statistics often fail to capture. One of the most important developments is the rapid growth of dollar-denominated digital assets across emerging markets. In regions such as Latin America, Africa, and Southeast Asia, stablecoins have become increasingly popular as tools for savings, payments, and access to dollar exposure where local currencies face inflation or volatility.

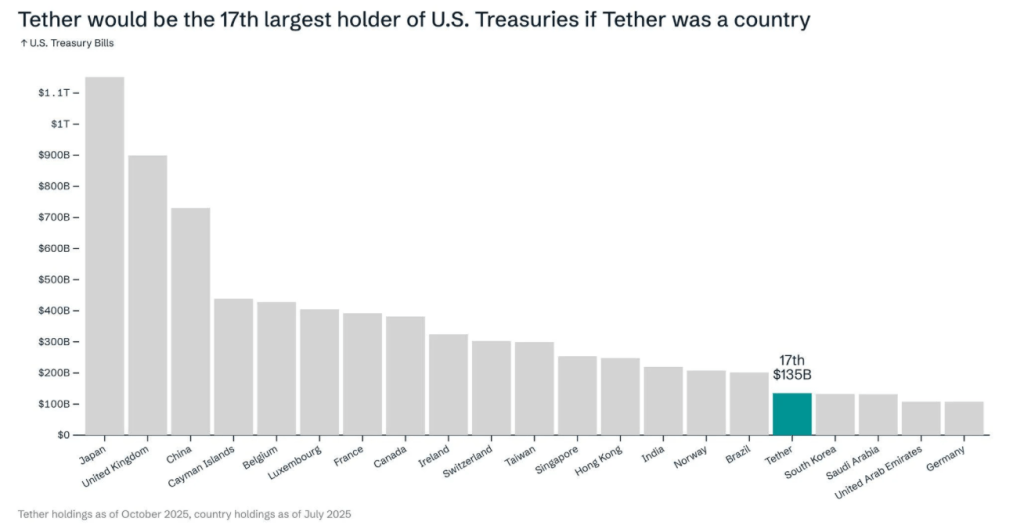

A notable example is Tether, the issuer of the USDT stablecoin. According to the company’s first-quarter 2026 attestation, it held approximately $141 billion in direct and indirect exposure to U.S. Treasury securities as of March 31, supported by total assets of roughly $191.8 billion against liabilities of $183.5 billion. The company also reported a reserve surplus exceeding $8 billion and more than $1 billion in quarterly profit.

These figures are significant because they illustrate how digital-dollar adoption can generate additional demand for U.S. government debt. Stablecoin issuers typically back their tokens with highly liquid dollar assets, including Treasury bills and other short-term government securities. As stablecoin usage grows internationally, so does the indirect demand for dollar-denominated reserves.

Viewed through this lens, digital finance may be reinforcing rather than weakening the dollar’s global position. Instead of replacing the dollar, many of the most widely used digital assets effectively extend the reach of dollar liquidity into markets that previously had limited access to traditional banking infrastructure.

The broader implication is that the future of dollar dominance may not depend solely on central-bank reserve allocations. Increasingly, it may also be shaped by private-sector demand for digital dollars, cross-border payment networks, and new forms of dollar-based financial infrastructure that continue to expand the currency’s global footprint.

The dollar’s reach is increasingly extending beyond traditional banking and central-bank reserves into the digital economy. Supporters of the dollar-dominance thesis argue that this trend is particularly visible in emerging markets, where dollar-linked stablecoins are becoming a preferred vehicle for savings, payments, and wealth preservation.

Recent growth in USDT circulation illustrates the scale of that demand. As the supply of dollar-pegged stablecoins continues to expand, issuers accumulate larger holdings of U.S. Treasury securities and other dollar-denominated assets to back those tokens. In effect, every new digital dollar created generates additional demand for the underlying dollar-based financial infrastructure.

The trend is especially pronounced across parts of Latin America, Africa, and Southeast Asia, where concerns about local currency volatility have encouraged users to hold digital dollars instead of local cash balances. Some industry reports have described this phenomenon as “digital dollarization”—a process in which individuals gain access to dollar exposure through blockchain networks rather than through traditional bank accounts.

From a monetary perspective, this is an important distinction. Many observers originally viewed cryptocurrencies as potential competitors to the dollar. Yet the fastest-growing segment of the digital asset market has often been dollar-backed stablecoins rather than non-sovereign alternatives. As a result, blockchain adoption in many regions has expanded demand for dollar-linked assets rather than displaced them.

Regulatory developments further reinforce this dynamic. The implementation of stablecoin legislation and enhanced compliance requirements has increasingly tied major issuers to the existing financial system. Requirements that reserves be backed by high-quality liquid assets—primarily short-term U.S. government securities—strengthen the connection between stablecoin growth and Treasury demand.

At the same time, regulatory oversight gives authorities greater visibility and enforcement capability within digital-dollar networks. Compliance obligations imposed on issuers, exchanges, and custodians allow regulators to block, freeze, or restrict assets associated with sanctioned entities when required by law. This means that large portions of the stablecoin ecosystem operate not outside the traditional financial system, but as an extension of it.

Viewed through this lens, digital dollars may represent one of the newest channels through which dollar dominance is being reinforced. Rather than creating a parallel monetary order, stablecoins are increasingly embedding dollar liquidity, Treasury demand, and regulatory reach into global digital payments networks.

The broader takeaway is that the future of dollar dominance may depend not only on central banks and sovereign reserves, but also on millions of individuals and businesses choosing to hold digital representations of dollars. If that trend continues, the dollar’s influence could become even more deeply integrated into everyday economic activity around the world.

What This Means for Investors

If the dollar-dominance thesis is correct, the investment implications extend across bonds, equities, gold, and digital-finance infrastructure.

First, persistent foreign demand for U.S. Treasuries suggests ongoing support for the long end of the yield curve, even amid large federal deficits. Strong international demand can help absorb increased issuance and potentially moderate upward pressure on long-term interest rates. From that perspective, duration exposure may offer more value than many deficit-focused forecasts imply.

Second, central-bank gold accumulation appears to be creating a stronger structural foundation for gold prices than existed in previous cycles. That does not necessarily make gold a substitute for fiat currencies. Rather, it reinforces gold’s role as a portfolio diversifier, inflation hedge, and geopolitical-risk buffer. Investors may benefit from maintaining strategic gold exposure, but the argument is increasingly about diversification rather than preparing for the collapse of the monetary system.

Third, the expansion of digital-dollar infrastructure is creating new investment opportunities across payments, custody, and financial technology. Companies such as CRCL, COIN, V, MA, JPM, and BK operate at the intersection of traditional finance and emerging digital-dollar networks, positioning them to benefit if stablecoin adoption continues to grow globally.

The contrarian takeaway is that many investors who positioned heavily for an imminent dollar collapse may have missed some of the strongest-performing asset classes of the past several years. U.S. equities continued to attract capital, Treasury securities remained central to global reserve portfolios, and the broader dollar-based financial system proved more resilient than many critics anticipated.

This does not mean investors should ignore risks. Fiscal deficits, rising debt-service costs, geopolitical tensions, sanctions-related fragmentation, and potential competition from future central bank digital currencies all deserve close attention. These factors could influence the dollar’s long-term trajectory and should remain part of any serious macroeconomic analysis.

However, the evidence presented by proponents of the dollar-dominance view points to a different conclusion than the popular collapse narrative. Foreign demand for Treasuries remains robust. Central banks continue to buy gold while largely operating within a dollar-priced reserve framework. Swap lines are being used to deepen dollar liquidity networks. Stablecoins and digital-dollar platforms are expanding dollar access across emerging markets.

Taken together, these trends suggest that the dollar is not disappearing from the global financial system. Rather, it is adapting to new technologies, new payment channels, and new geopolitical realities while retaining many of the advantages that have supported its dominance for decades.

For investors, the practical lesson is not necessarily to bet exclusively on the dollar, but to recognize that many of the world’s most important financial markets, reserve assets, payment networks, and digital-finance platforms remain deeply connected to the dollar ecosystem. Understanding that infrastructure may prove more valuable than betting on its imminent collapse.

Leave a comment