Gold attracts renewed buying interest during Tuesday’s Asian session, although its upside remains limited. Persistent inflation concerns continue to reinforce expectations that the Federal Reserve will keep interest rates elevated, providing support for the US Dollar and reducing the appeal of the non-yielding precious metal. At the same time, lingering geopolitical tensions between the United States and Iran are underpinning demand for the greenback, prompting traders to remain cautious about chasing further gains in gold.

Gold (XAU/USD) extends its rebound during Tuesday’s European session, climbing to its highest level in four days around the $4,075 area as the US Dollar eases amid renewed hopes for diplomacy between Washington and Tehran.

The precious metal draws support after US Secretary of State Marco Rubio stated on Sunday that the United States remains willing to engage in negotiations with Iran despite the recent exchange of military strikes. The remarks have tempered demand for the US Dollar by encouraging optimism that the conflict could eventually be resolved through diplomatic channels.

However, Gold’s upside remains constrained as investors continue to price in the inflationary risks stemming from rising energy costs. Disruptions to oil shipments through the Strait of Hormuz, combined with Yemen’s Iran-backed Houthi movement announcing a maritime blockade targeting Saudi Arabia, have reinforced expectations of tighter global crude supplies. Higher oil prices could fuel inflation and strengthen the case for the Federal Reserve to maintain restrictive monetary policy for longer.

Market expectations continue to reflect that view. According to the CME FedWatch Tool, traders see roughly an 83% chance that the Fed will raise interest rates before the end of the year. The prospect of higher US borrowing costs supports the US Dollar and limits demand for non-yielding assets such as Gold.

Meanwhile, geopolitical tensions remain elevated despite the diplomatic signals. The United States has reportedly carried out a tenth consecutive night of strikes on Iranian targets, with the White House indicating that military operations will continue until President Donald Trump decides otherwise. Iran has responded with retaliatory attacks against US military facilities and allied infrastructure across the Gulf, keeping concerns over a broader regional conflict firmly in focus.

With geopolitical risks continuing to underpin the US Dollar’s safe-haven appeal and expectations for prolonged Fed tightening remaining intact, traders may prefer to wait for stronger confirmation before concluding that Gold has established a near-term bottom, particularly in the absence of major US economic data releases on Tuesday.

Gold H4 Chart

Gold continues to trade with a positive intraday tone after breaking above the 23.6% Fibonacci retracement of the decline from the July peak and pushing through a short-term descending trendline. This technical breakout strengthens the bullish outlook, while momentum indicators also show improving conditions. Both the Moving Average Convergence Divergence (MACD) and the Relative Strength Index (RSI) are pointing higher, indicating that selling pressure is gradually easing.

Even so, the broader near-term outlook remains cautious as long as XAU/USD stays below the 100-period Simple Moving Average (SMA) on the 4-hour chart and several key Fibonacci resistance levels. Any continued advance is therefore likely to encounter resistance first near the 38.2% Fibonacci retracement at $4,052.78, followed by the 100-period SMA at $4,067.29 and the 50.0% retracement at $4,081.40.

If bullish momentum extends beyond those levels, the 61.8% Fibonacci retracement at $4,110.01 could provide a more formidable resistance zone. On the downside, initial support is located around $4,017, where the 23.6% Fibonacci level aligns with the recently broken trendline. A stronger support base sits near $3,960.14, the key Fibonacci anchor, where buyers may step back in should the current pullback deepen.

The US Dollar Index trades lower against its major counterparts as markets scale back expectations for a more hawkish Federal Reserve.

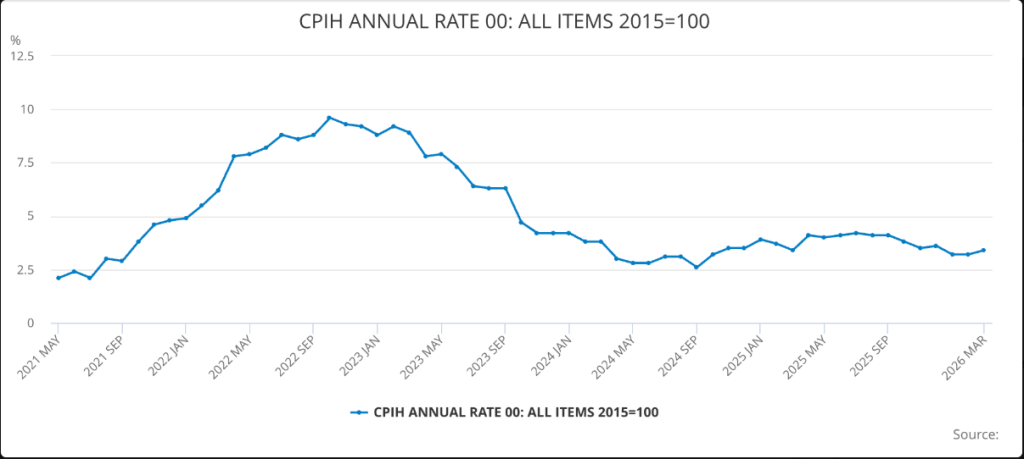

US inflation softened in June, with both headline and core CPI easing to 3.5% and 2.6% year-over-year, respectively.

Fed Chair Kevin Warsh reiterated that the central bank remains firmly committed to bringing inflation under control, emphasizing zero tolerance for persistently elevated price pressures.

The US Dollar (USD) weakens against its major peers as investors scale back expectations for further Federal Reserve (Fed) rate hikes this year after softer-than-anticipated US inflation data for June. The US Dollar Index (DXY), which tracks the Greenback against a basket of six major currencies, is trading around 100.80, down roughly 0.12% on the day.

Data released by the US Bureau of Labor Statistics (BLS) on Tuesday showed headline Consumer Price Index (CPI) inflation eased to 3.5% year-over-year in June from 4.2% in May, coming in below the market forecast of 3.8%. Meanwhile, core CPI, which strips out food and energy prices, rose 2.6% annually, undershooting both the 2.8% consensus estimate and May’s 2.9% reading.

Following the inflation report, market expectations for another Fed rate increase this month dropped sharply. According to the CME FedWatch Tool, the probability of a rate hike has fallen to 16.6%, down from 41.7% a day earlier.

Despite the softer inflation figures, Fed Chair Kevin Warsh maintained a firm stance on price stability during his congressional testimony on Tuesday, stressing that policymakers have “no tolerance for persistently elevated inflation.” He added that if monetary policy remains on the right path, the inflation surge seen over the past five years will eventually become a thing of the past.

Market participants now await the release of June’s US Producer Price Index (PPI), scheduled for 12:30 GMT, for additional insight into wholesale inflation trends and the Fed’s policy outlook.

Meanwhile, rising tensions between the United States and Iran could continue to support demand for the Greenback, as investors seek the safety of the world’s reserve currency amid growing geopolitical uncertainty.

Gold drifts lower as the market’s initial response to Tuesday’s softer-than-expected US inflation data loses momentum. Persistently high oil prices continue to fuel expectations of at least one additional Federal Reserve rate hike, weighing on the non-yielding metal. Meanwhile, escalating tensions between the US and Iran could boost demand for the safe-haven US Dollar, adding further downside pressure to XAU/USD.

Gold (XAU/USD) comes under renewed selling pressure after failing to sustain gains above the $4,100 level in the previous session, though it continues to hold above the key $4,000 psychological support during Wednesday’s Asian trading hours. While softer-than-expected US Consumer Price Index (CPI) data initially weighed on the US Dollar (USD), persistent concerns over energy-driven inflation continue to dominate sentiment. Escalating tensions between the US and Iran, along with the closure of the Strait of Hormuz, have kept crude oil prices elevated, reinforcing inflation fears. Meanwhile, Federal Reserve (Fed) Chair Kevin Warsh reaffirmed the central bank’s commitment to restoring price stability during his first congressional testimony, signaling that another rate hike remains possible before year-end. The hawkish tone largely offsets the impact of a weaker USD and limits demand for the non-yielding precious metal.

Data released by the US Bureau of Labor Statistics showed headline CPI fell by 0.4% in June, marking the steepest monthly decline since April 2020 and falling short of expectations for a 0.1% decrease. Core CPI, which excludes food and energy prices, was unchanged during the month, well below the expected 0.3% increase. On an annual basis, headline inflation eased to 3.5%, while core inflation slowed to 2.6%, both undershooting market forecasts. The softer inflation figures briefly dragged the USD to its weakest level in nearly four weeks as traders pared back expectations for additional Fed tightening. However, the Greenback quickly recovered after Warsh emphasized that the Fed remains firmly committed to combating inflation and highlighted the resilience of the US economy.

At the same time, crude oil prices have climbed to their highest level in nearly a month, increasing concerns that higher energy costs could reignite inflationary pressures and justify further monetary tightening. Reflecting this outlook, the CME FedWatch Tool indicates that markets continue to price in the possibility of one additional Fed rate hike, potentially in September or December. Geopolitical tensions also continue to underpin the USD’s safe-haven appeal. The US carried out another wave of airstrikes on Iranian targets, while Tehran responded by attacking US military facilities across Gulf nations. In addition, President Donald Trump warned that Washington could target Iranian bridges and power infrastructure if Tehran refuses to resume nuclear negotiations.

Overall, the prevailing fundamental backdrop remains supportive of the US Dollar and suggests that downside risks for Gold persist. Investors now await the release of the US Producer Price Index (PPI) and the second day of Fed Chair Kevin Warsh’s congressional testimony for fresh clues on the interest rate outlook. Meanwhile, any new developments in the Middle East conflict are likely to remain a key driver of market sentiment and could trigger heightened volatility across financial markets, particularly in Gold.

Technical Analysis

From a technical perspective, Gold continues to trade within a descending parallel channel and remains firmly below the 200-day Simple Moving Average (SMA), indicating that the broader trend remains tilted to the downside despite the recent recovery. The Moving Average Convergence Divergence (MACD) has crossed into positive territory and continues to improve, signaling a modest pickup in bullish momentum, while the Relative Strength Index (RSI) hovers near the neutral 40.80 mark, suggesting limited buying conviction.

The upper boundary of the descending channel, located around $4,140.69, represents the first significant resistance level. A sustained break above this barrier would be required to weaken the prevailing bearish outlook and open the door for additional gains. On the downside, immediate support is seen near the channel’s lower boundary at $3,718.03. A decisive rebound from this level would be needed to indicate that bearish momentum is fading and that sellers are beginning to lose control of the short-term trend.

AUD/USD comes under renewed selling pressure on Wednesday as a combination of factors continues to support the US Dollar. Ongoing uncertainty surrounding Iran and growing expectations of further Fed rate hikes remain key tailwinds for the greenback. Meanwhile, the pair shows little reaction to China’s RatingDog Manufacturing PMI, which came in broadly in line with expectations.

AUD/USD failed to build on Tuesday’s rebound from the 0.6865 area, its lowest level in three months, and came under renewed selling pressure during Wednesday’s Asian session. The pair slipped back below 0.6900 and showed little reaction to China’s latest private manufacturing PMI data.

China’s RatingDog Manufacturing PMI eased to 51.7 in June from 52.2 in May, reinforcing concerns about slowing economic momentum. Combined with Tuesday’s official PMI figures, which highlighted weak domestic demand and subdued consumer spending, the data weighed on the Australian Dollar, which is often viewed as a proxy for China’s economic health. A modest recovery in the US Dollar further added to the pair’s downside pressure.

The Greenback continued to benefit from its safe-haven appeal amid uncertainty surrounding US-Iran negotiations and growing expectations that the Federal Reserve may need to raise interest rates further. Although US officials arrived in Qatar to discuss the implementation of a preliminary peace agreement, Iran’s reluctance to engage with US envoys has cast doubt on the prospects for a lasting resolution, keeping geopolitical risks elevated.

At the same time, stronger-than-expected US labor market data supported the USD. The JOLTS report showed job openings climbed to a two-year high of 7.594 million in May, underscoring continued labor market resilience. Combined with concerns that renewed tensions in the Middle East could reignite inflationary pressures, the data strengthened market expectations for additional Fed tightening.

Investors now await remarks from Fed Chairman Kevin Warsh at the ECB Forum in Sintra, alongside key US data releases including the ADP employment report and ISM Manufacturing PMI. Attention will then turn to Thursday’s closely watched Nonfarm Payrolls report, which could provide the next major catalyst for AUD/USD.

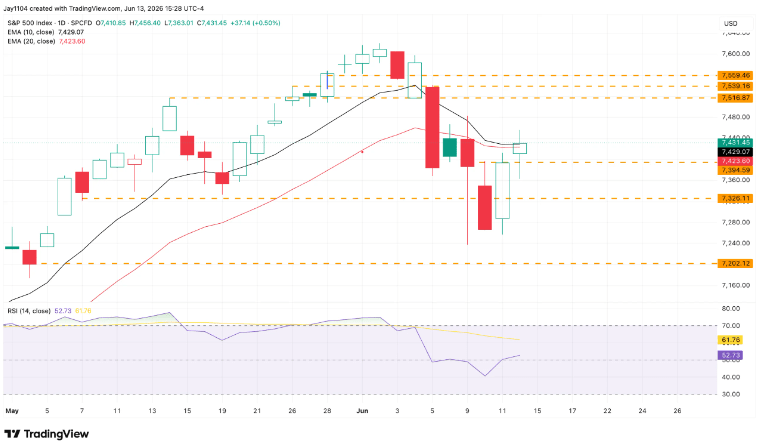

The market had a shaky start to the week but managed to stage a respectable recovery following last week’s sharp selloff. Most of the rebound came on Thursday after reports suggested that the US and Iran could be moving closer to another agreement, a development that has resurfaced repeatedly since March. Whether a deal is ultimately finalized or not, investors continue to react positively whenever such headlines emerge, and that response itself remains significant. By Friday’s close, the S&P 500 had edged slightly above where it finished the previous week.

However, the index remains capped by its 10-day and 20-day exponential moving averages, both of which are currently acting as resistance. Additional technical barriers sit just above these levels, suggesting that the market still faces challenges before a more convincing upside breakout can occur.

From a positioning perspective, the market has drifted back into slightly positive gamma, meaning dealer hedging is once again acting as a stabilizer rather than a source of amplification. However, the signal is still relatively weak. If we see another pullback next week, that setup could quickly shift back into negative gamma, where hedging flows would start to reinforce price moves and potentially accelerate downside — a dynamic that helped fuel Thursday’s rebound.

In a positive gamma environment, price action tends to gravitate toward “pinning” rather than trending. With monthly options expiring on Thursday the 18th (and markets closed on Friday the 19th for the holiday), and a meaningful amount of gamma set to roll off into expiry, conditions point toward a potentially quieter, more range-bound week ahead.

The key event next week is the Fed meeting on Wednesday, and there’s a risk the market may be caught leaning the wrong way if the tone comes in more hawkish than expected.

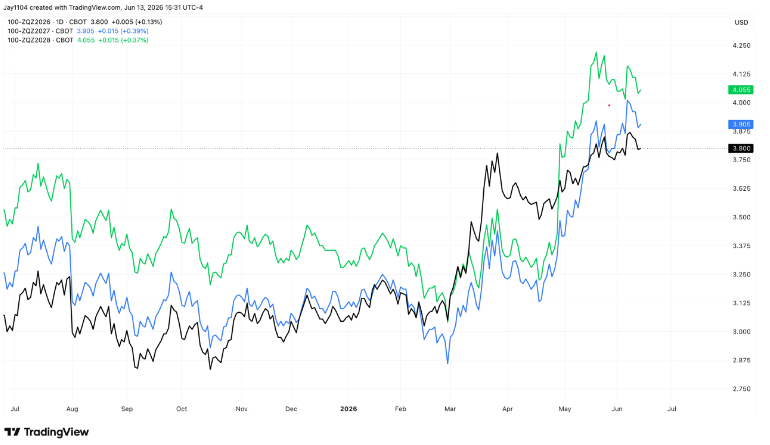

It helps to put the starting point in context. At the March meeting under Chair Powell, the FOMC’s dot plot showed a median policy rate of about 3.4% for 2026, with the easing cycle flattening out near 3.1% into early 2027.

Since then, markets have moved meaningfully higher in their rate expectations. Fed funds futures are now pricing roughly 3.80% for 2026, 3.90% for 2027, and about 4.05% for 2028. In effect, that shift has largely erased the earlier assumption of continued rate cuts and instead leans toward a more restrictive long-run stance, even introducing a subtle tilt toward the possibility of hikes.

Against that backdrop, the focus will be on whether the Fed updates its messaging to match this repricing. A key risk is a removal of any remaining easing bias, along with a rhetorical shift away from emphasizing labor market softness and back toward inflation persistence.

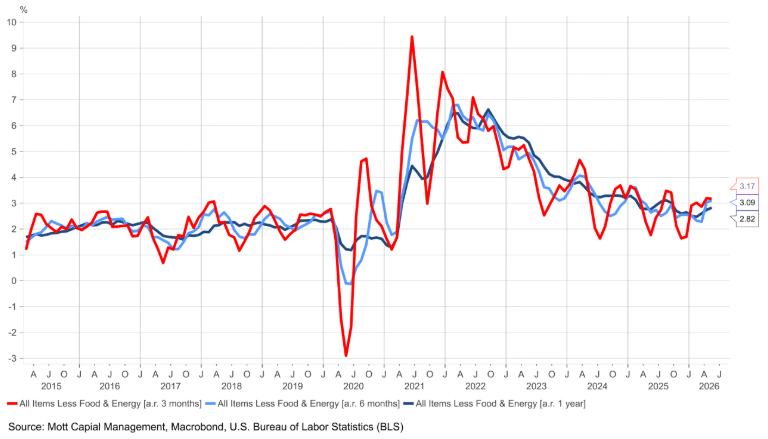

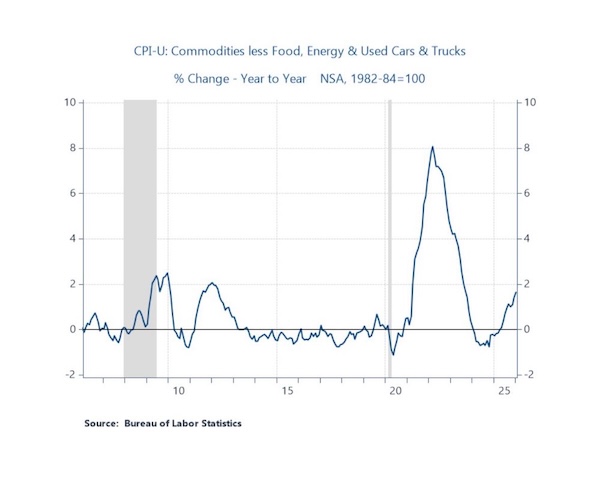

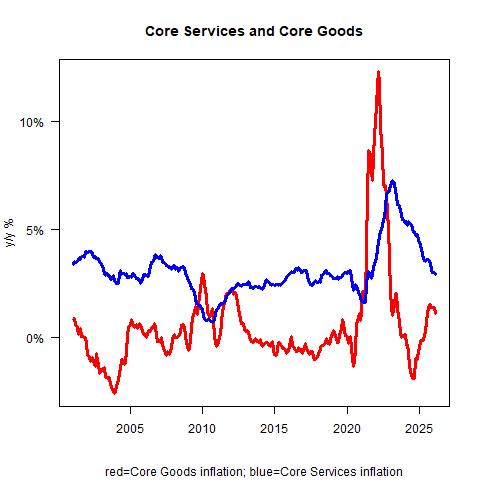

Inflation has also become more interesting lately because it’s no longer just an energy-driven story.

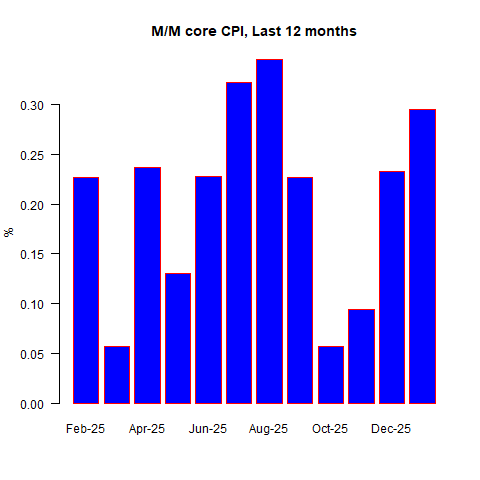

Core CPI, which strips out food and energy, is running at roughly 3.1%–3.2% on a three- and six-month annualized basis, and about 2.8% year over year. That implies the headline annual figure may continue edging higher unless monthly momentum clearly cools in the near term.

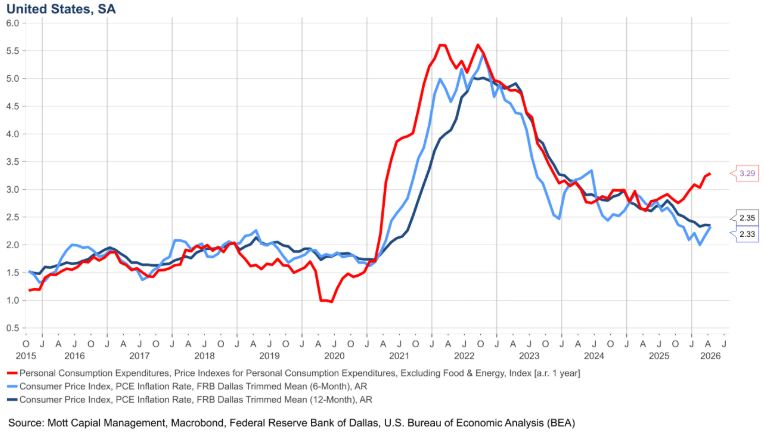

Core PCE — the Fed’s preferred inflation measure — is showing a similar pattern. It’s tracking around 3.8% on a three- and six-month basis and about 3.3% year over year, reinforcing the idea that underlying inflation remains sticky even without the volatility from energy prices.

Even measures designed to strip out outliers are now pointing in the same direction. Trimmed mean PCE — an alternative inflation gauge that excludes the most extreme monthly price moves and has been highlighted by figures such as Kevin Warsh — is running around 2.3%. Meanwhile, the Cleveland Fed’s trimmed mean CPI sits closer to 2.9%.

The historical context matters here. In 2021, trimmed-mean measures lagged the acceleration in inflation, while core PCE moved higher earlier and ultimately peaked first. In contrast, during 2019–2020, relying on trimmed-mean data alone would not have justified the rate cuts that eventually came.

The current setup suggests this is not purely an energy-driven story. If inflation were mainly about oil, it would be harder to explain why core measures are still elevated on both three- and six-month annualized bases, especially given that oil’s move only really began in March.

A key contributor appears to be goods inflation. After previously running negative, goods prices have swung back to roughly 4.4% year over year, and that reversal is now feeding through into broader inflation readings.

At the same time, the labor market is starting to show signs of turning. The ratio of job openings to unemployed workers has moved back above one and has been trending with higher highs and higher lows since December. Broader indicators — including payroll data, ADP figures, and Revelio Labs — are broadly aligned, suggesting the labor market likely bottomed out in late autumn and is now gradually firming.

That shift gives the Fed more flexibility to pivot its attention away from employment concerns and back toward inflation. Against that backdrop, it wouldn’t be surprising if the updated dot plot on Wednesday reflects a slightly lower unemployment path alongside higher inflation projections for both this year and next.

On equities, the semiconductor complex still hasn’t fully reset. Implied volatility across the group remains near the upper end of its one-year range, and positioning in options is still skewed toward calls. Even after Broadcom and NVIDIA pulled back following Broadcom’s results, names like Micron have kept overall volatility elevated.

At the same time, dispersion remains wide — the gap between single-stock volatility and index-level volatility is still pronounced — and implied correlations are still low. In other words, single-stock volatility is elevated while index volatility remains relatively contained, and that relationship hasn’t fully normalized despite the sharp selloff over the past couple of weeks.

Gold prices fell toward $4,235 during early Asian trading on Wednesday as renewed US-Iran tensions boosted market uncertainty. Fresh US strikes on Iran, following the downing of a helicopter, intensified fears of a prolonged conflict. Meanwhile, investors are closely watching the US May CPI inflation report due later Wednesday for further market direction.

Gold prices extended losses to around $4,235, the lowest level since March 23, during Wednesday’s early Asian session. The decline in XAU/USD comes amid renewed Middle East tensions and growing expectations that the Federal Reserve could raise interest rates later this year. Investors are now awaiting the release of the US May CPI inflation report for fresh market direction.

According to Reuters, the US launched strikes on Iran after US President Donald Trump claimed that Tehran had shot down a US Apache helicopter in the Strait of Hormuz. Earlier on Tuesday, Trump said the US and Iran were close to reaching an agreement, although little concrete progress has emerged since a fragile ceasefire began in early April.

Ongoing uncertainty surrounding a potential peace deal between Washington and Tehran continues to fuel inflation concerns and support expectations for higher interest rates. While Gold is traditionally viewed as a safe-haven asset during geopolitical instability, elevated interest rates reduce the appeal of the non-yielding metal.

Meanwhile, stronger-than-expected US May employment data have reinforced market expectations of a possible Fed rate hike this year. Traders are now focused on the upcoming US CPI report. Headline inflation is forecast to rise 4.2% year-over-year in May, up from 3.8% previously, while core CPI is expected to increase 2.9% YoY compared with 2.8% in April.

Any signs of stronger-than-expected inflation could strengthen the US Dollar and add further downside pressure on Gold prices in the near term.

“The prevailing inflation fears, data strength, Fed hike probability increasing, and break of 200-day moving average have led to a heavy skew negative,” said Ryan McKay, senior commodity strategist at TD Securities.

Silver prices declined sharply to around $72.40 as Federal Reserve officials reiterated concerns about persistent inflationary pressures.

Fed official Schmid noted that policymakers may need to either maintain interest rates at elevated levels for longer or consider further rate hikes to keep inflation under control.

Meanwhile, investors remain focused on the upcoming US Nonfarm Payrolls (NFP) report for May, which could provide fresh clues about the labor market and the future path of monetary policy.

Silver prices (XAG/USD) fell nearly 2% to around $72.40 during Friday’s Asian session, coming under heavy selling pressure after several Federal Open Market Committee (FOMC) officials highlighted persistent inflation risks and suggested that policymakers may need to either maintain current interest rates for an extended period or raise them further.

Higher interest rates from the Federal Reserve (Fed) are generally unfavorable for non-yielding assets such as Silver, as they increase the opportunity cost of holding precious metals.

Speaking at the Bank of Kansas City Economic Forum on Thursday, Kansas City Fed President Jeffrey Schmid emphasized that inflation remains the primary threat to the economy. He noted that policymakers are debating whether to keep rates unchanged for longer or tighten monetary policy further to bring inflation back toward the Fed’s target.

Market participants are now turning their attention to the US Nonfarm Payrolls (NFP) report for May, scheduled for release at 12:30 GMT. Economists expect the US economy to have added 85,000 jobs during the month, down from 115,000 in April. The unemployment rate is forecast to remain steady at 4.3%, while annual Average Hourly Earnings—a key gauge of wage inflation—are projected to slow to 3.4% from the previous 3.6%.

A stronger-than-expected employment report could reinforce expectations that the Fed will maintain a hawkish stance this year. However, weaker labor-market data may have only a limited effect on policy expectations, as Fed officials appear increasingly focused on addressing elevated inflation pressures.

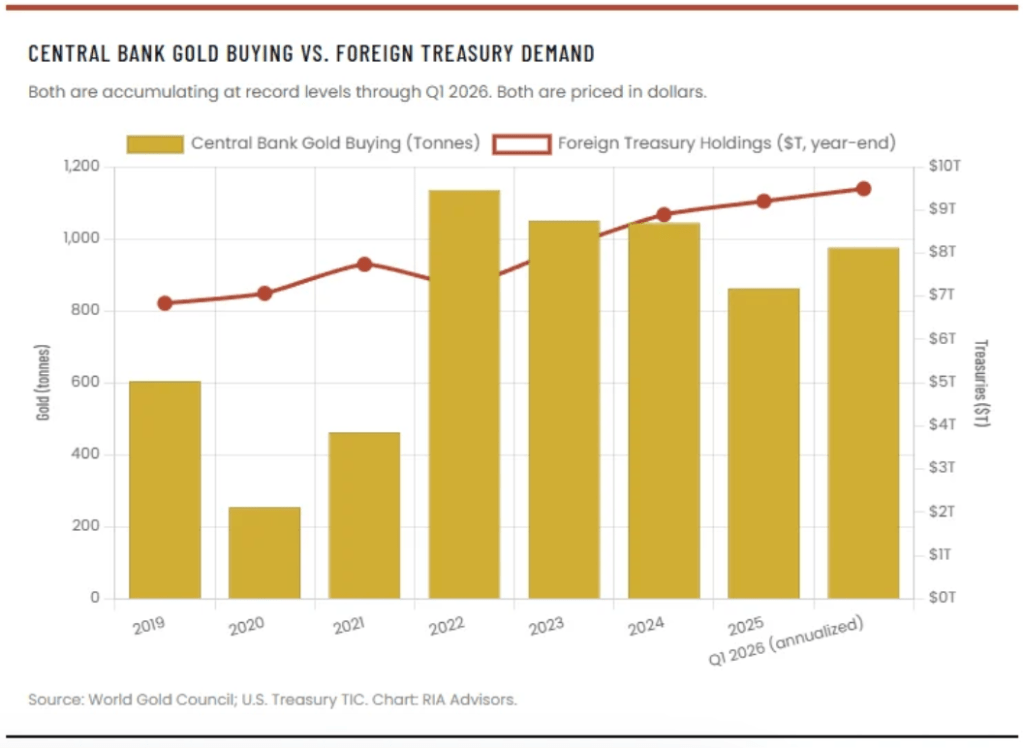

International investors and governments increased their holdings of U.S. Treasury securities to an all-time high of $9.49 trillion in February 2026, with holdings rising $587 billion year-over-year and nearly $200 billion in a single month.

Central banks continued accumulating gold, adding 244 tonnes during the first quarter of 2026 and extending a buying streak that has lasted 17 months. However, because gold is traded globally in U.S. dollars, this trend still reinforces the dollar’s central role in the financial system.

The United Arab Emirates’ decision to withdraw from OPEC/OPEC+ came shortly after U.S. officials endorsed a potential emergency dollar liquidity arrangement for Abu Dhabi, highlighting the strategic influence of dollar-based financial support.

U.S. sanctions efforts against Iran have successfully frozen $344 million worth of cryptocurrency assets, illustrating how digital financial infrastructure linked to the dollar can strengthen U.S. economic enforcement power.

Overall, evidence from Treasury market demand, rising foreign capital inflows, and expanding digital-dollar adoption suggests that predictions of the dollar’s decline are not supported by current data.

For years, predictions of the US dollar’s decline have dominated headlines, and those claims have only grown louder. Critics argue that BRICS nations are creating a viable alternative to the dollar, China is reducing its holdings of US Treasuries, gold is poised to replace the dollar as the world’s primary reserve asset, and the US government is struggling to attract buyers for its mounting debt—so much so that it is allegedly using dollar swap lines with Gulf nations as an indirect liquidity support mechanism.

While these arguments make for a compelling narrative, the underlying data tells a different story. Despite the persistent warnings from dollar skeptics, there is little evidence to suggest that the dollar’s dominant role in the global financial system is meaningfully eroding.

The dollar’s dominance is far from disappearing. If anything, the developments seen in late April 2026 provided one of the strongest pieces of evidence in years that its position in the global financial system remains firmly intact.

Theory vs. Reality

For years, I’ve argued that the “dollar collapse” narrative mistakenly equates inflation with currency debasement. Those are not the same thing. A currency cannot realistically be considered debased when global demand for it continues to intensify. We’ve explored this rebasement perspective before in our discussions of the dollar’s global funding system and in The Dollar’s Death Is Greatly Exaggerated. The latest figures only strengthen the case that the U.S. dollar remains firmly dominant.

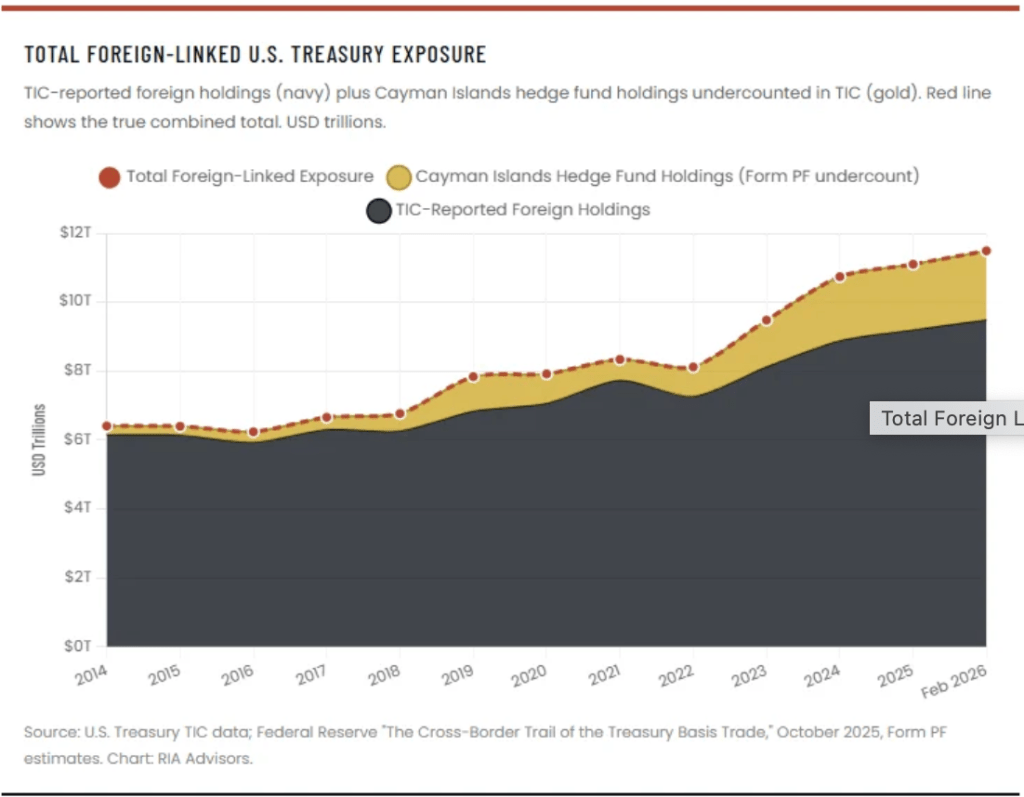

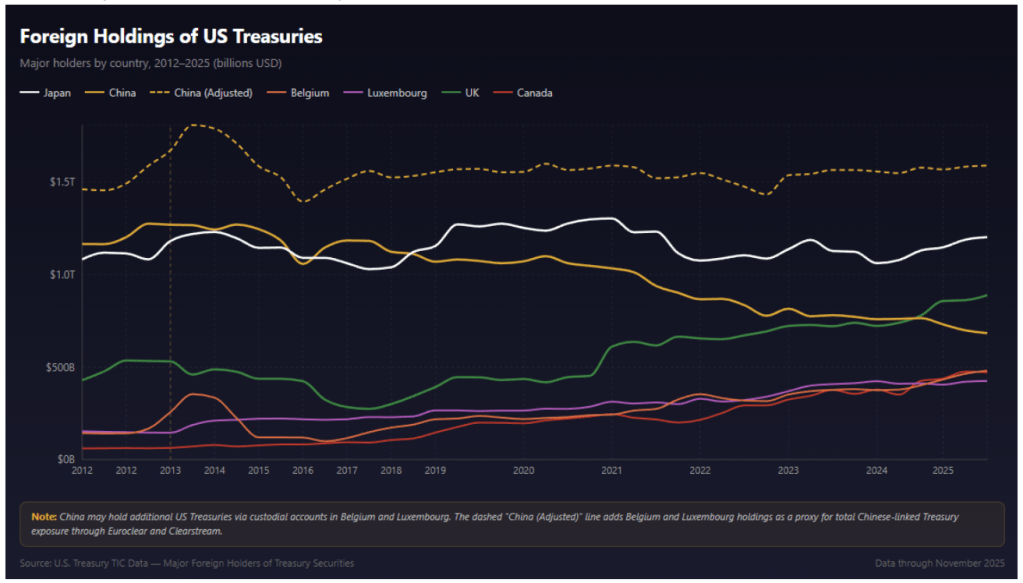

The most recent Treasury International Capital (TIC) report from the U.S. Treasury, released on April 15 and covering February 2026 activity, showed foreign investors purchased $101 billion of long-term U.S. securities in a single month. Total net TIC inflows reached $184.5 billion, while foreign investors also increased their Treasury bill holdings by another $91.6 billion. As a result, foreign ownership of U.S. Treasuries climbed to a record $9.49 trillion in February, rising by $198 billion during the month and by $587 billion over the previous year.

Even that record figure understates the true scale of foreign demand. It excludes Treasury exposure held through U.S.-based hedge funds and the Cayman Islands basis trade. According to Federal Reserve estimates, these channels account for roughly an additional $1.5 trillion of effective foreign demand. When those positions are included, total foreign-linked exposure to U.S. Treasuries approaches $11 trillion, underscoring the continued global appetite for dollar-denominated assets.

Looking beyond the total amount of debt outstanding, the flow data paints the same picture. Indirect bidders—widely viewed as a gauge of foreign demand—have consistently accounted for more than 70% of successful bids in recent Treasury auctions. Meanwhile, bid-to-cover ratios for both 10-year and 30-year Treasury sales have remained above 2.5 through multiple market cycles, signaling robust investor appetite.

If the world were genuinely abandoning the dollar, the evidence would look very different: weaker auction participation, higher yields caused by poorly received offerings, and a rising term premium as investors demanded greater compensation to absorb excess supply. Yet the data points in the opposite direction. Despite the U.S. running approximately $2.5 trillion in deficits over the past year, global investors have continued to absorb the resulting Treasury issuance with little difficulty.

Far from resembling a rush for the exits, these trends suggest exceptionally strong demand. In fact, they point to one of the most powerful and persistent periods of global demand for U.S. government debt ever recorded.

How Central Bank Gold Purchases Strengthen the Dollar’s Position

This is where many dollar-collapse narratives begin to break down. Gold advocates often make a fundamental mistake by treating central bank gold accumulation as proof that the world is abandoning the U.S. dollar. The reality is more nuanced.

There is no dispute that central banks have been aggressively increasing their gold reserves. According to the World Gold Council’s Q1 2026 Gold Demand Trends report, released on April 29, official-sector institutions purchased a net 244 tonnes of gold during the first quarter alone, a 3% increase from the same period a year earlier. That marked the seventeenth consecutive month of net central bank buying, despite gold prices surpassing $5,400 per ounce in January. Physical gold demand reached 474 tonnes during the quarter, making it the second-strongest first quarter on record. Looking ahead, the World Gold Council expects central banks to purchase approximately 850 tonnes of gold throughout 2026, broadly matching 2025 levels and extending a multi-year trend of substantial accumulation.

The trend is both genuine and important. However, interpreting it as evidence of a mass exodus from the dollar is a leap that the data does not support. Central banks are adding gold primarily as a reserve diversifier and geopolitical hedge, not as a replacement for the dollar-based financial system. Gold can store value, but it cannot replicate the liquidity, collateral function, settlement infrastructure, or global financing role provided by U.S. Treasury securities and dollar-denominated markets.

In other words, rising gold reserves and continued dollar dominance are not mutually exclusive. Central banks can accumulate gold while still relying heavily on dollars for trade settlement, reserve management, cross-border financing, and international liquidity. The growth of official gold holdings reflects diversification at the margin—not a practical abandonment of the world’s primary reserve currency.

A key point often overlooked in de-dollarization debates is that gold itself remains deeply embedded within the dollar-based financial architecture. Gold may be a reserve asset, but it is still primarily valued through a dollar lens. The London Bullion Market Association (LBMA) benchmark—the global standard used to value central bank gold holdings—is quoted in U.S. dollars per ounce. Whether it is the People’s Bank of China, the National Bank of Poland, or the Reserve Bank of India increasing its gold reserves, those holdings are ultimately measured, reported, and assessed in dollar terms.

The same principle applies when central banks use gold as a source of liquidity. Whether through swaps, repurchase agreements, or outright sales, transactions are typically priced against dollar benchmarks. Gold and dollars are therefore not competing monetary systems operating independently of one another. Rather, gold functions as a reserve asset within a broader framework that is still largely organized around the U.S. dollar.

This distinction fundamentally changes how central bank gold purchases should be interpreted. If a central bank reallocates 5% of its reserves from U.S. Treasuries into gold, that does not constitute an exit from the dollar system. It is simply a portfolio adjustment within a reserve structure where assets continue to be valued and compared using dollar-based metrics. The same logic applies to gold swaps conducted through the Bank for International Settlements, yuan-denominated contracts traded on the Shanghai Gold Exchange, and even the large gold accumulation programs undertaken by Central Bank of the Russian Federation before sanctions. Regardless of the transaction venue or currency of quotation, reserve managers still evaluate those positions against their dollar-equivalent value.

Viewed through that lens, growing gold reserves do not necessarily undermine dollar dominance. In many respects, they reinforce it by relying on the dollar as the world’s primary unit of account for reserve wealth.

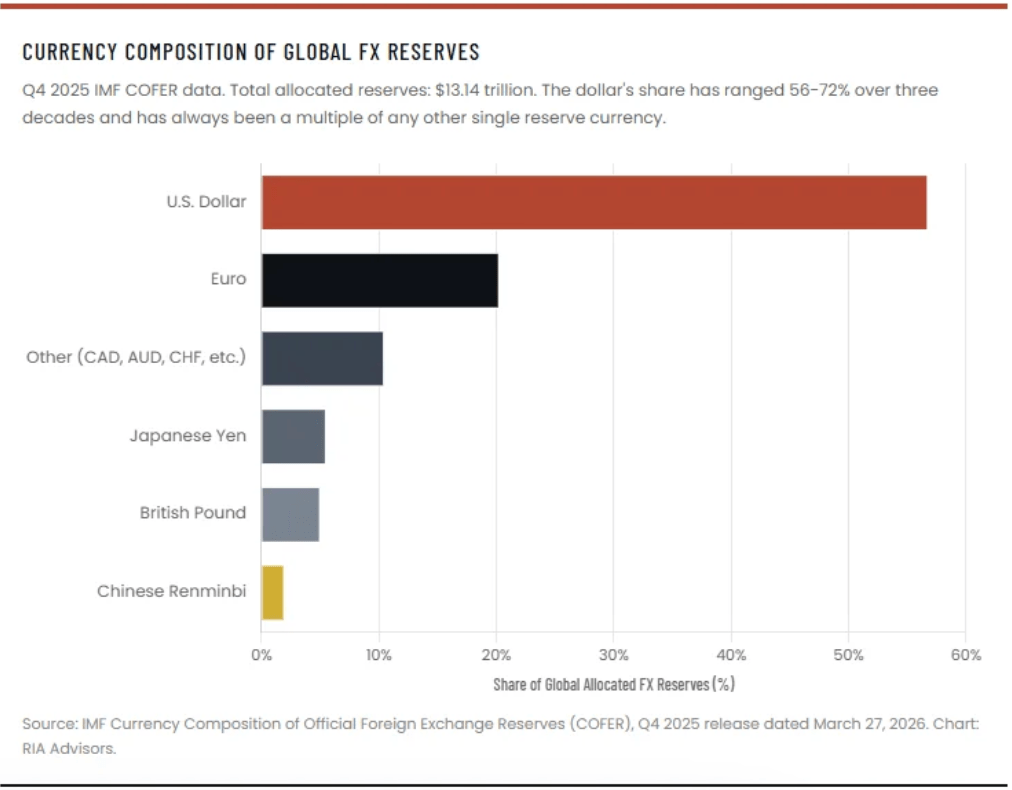

The same surveys frequently cited as evidence of de-dollarization illustrate this nuance. While many central banks expect the dollar’s share of reserves to gradually decline over the coming years, actual reserve data tells a more measured story. According to the IMF’s COFER statistics for the fourth quarter of 2025, the U.S. dollar accounted for roughly 56.8% of allocated global foreign-exchange reserves. Although lower than the levels seen decades ago, that share remained broadly stable, with much of the quarter-to-quarter movement attributable to exchange-rate fluctuations rather than aggressive reserve liquidation.

At the end of 2025, total global foreign-exchange reserves stood above $13 trillion. Within that pool, the dollar remained by far the dominant reserve currency, holding a share that exceeded the combined weight of every major competitor except the euro. The euro represented roughly one-fifth of allocated reserves, while the Japanese yen and British pound each accounted for about 5%. Despite persistent discussion of its rise, the Chinese yuan continued to represent only a small fraction of global reserve holdings.

The broader takeaway is that reserve diversification and de-dollarization are not synonymous. Central banks may seek greater exposure to gold or other currencies, but the available data still points to a global reserve system in which the dollar remains the primary benchmark, funding currency, and store of international liquidity.

Bessent’s Dollar Swap Strategy Expands Dollar Dominance

Recent discussions surrounding potential new dollar swap lines have provided another example of how U.S. policymakers are working to reinforce, rather than merely defend, the dollar’s global position.

Treasury Secretary Scott Bessent has recently floated the idea of extending dollar swap arrangements to key partners in the Persian Gulf and Asia, with the United Arab Emirates frequently mentioned as a leading candidate. Critics have interpreted the proposal as an emergency measure designed to prevent foreign holders from selling U.S. Treasuries amid geopolitical tensions in the Middle East. However, that interpretation overlooks the broader strategic objective.

Bessent’s own comments suggest a different motivation. He has emphasized that swap lines help maintain stability in dollar funding markets and reduce the risk of disorderly asset sales during periods of stress. More importantly, he has argued that expanding swap-line networks can strengthen international dollar usage and create additional dollar funding hubs across strategically important regions.

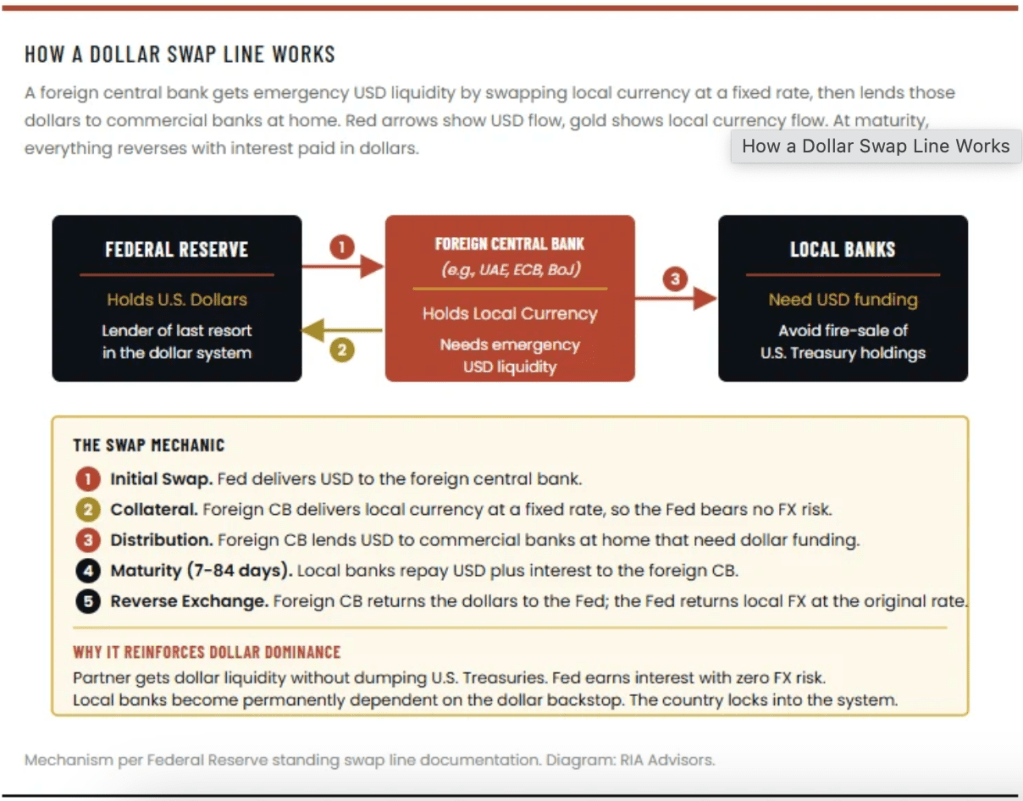

At its core, this approach is about infrastructure. Dollar swap lines are one of the most powerful tools available for extending the reach of the global dollar system. During the 2008 financial crisis, swap lines were deployed primarily as a defensive measure, providing dollar liquidity to foreign central banks and preventing disruptions in global funding markets. The emerging strategy seeks to use the same mechanism more proactively by deepening the dollar’s presence in regions where competing financial architectures have been gaining attention.

The logic is straightforward. When a central bank receives permanent or highly reliable access to dollar liquidity through a swap arrangement, its domestic financial institutions gain confidence that dollars will remain available during periods of market stress. That assurance strengthens incentives to continue conducting trade, financing, and reserve management activities in dollars rather than investing heavily in alternative systems.

From a network perspective, every new swap line effectively creates another node within the global dollar ecosystem. Countries connected to these facilities become more deeply integrated into dollar funding markets, increasing the currency’s utility and reinforcing its network effects. This dynamic helps explain why existing swap-line arrangements among the United States, the European Central Bank, Japan, United Kingdom, Canada, and Switzerland have remained central pillars of the international monetary system since the global financial crisis.

Viewed through this lens, proposed Gulf and Asian swap lines are less about preventing a collapse in Treasury demand and more about extending the geographical footprint of the dollar system. Rather than signaling weakness, they represent an effort to strengthen the institutional infrastructure that underpins the dollar’s reserve-currency status and global liquidity role.

The broader implication is that dollar dominance is sustained not only by the size of the U.S. economy or the Treasury market, but also by the network of financial relationships that make dollars readily available around the world. Swap lines are one of the clearest examples of how that network continues to expand.

More importantly, this strategy is no longer merely theoretical. Advocates argue that Treasury Secretary Scott Bessent has already demonstrated the model in practice through a swap facility extended to Argentina in 2025. The objective was straightforward: provide dollar liquidity to a strategic partner during a period of political uncertainty, stabilize financial conditions, and reinforce that country’s integration into the global dollar system. The reported repayment of the facility within a relatively short period strengthened the case that such arrangements can function as effective tools of financial diplomacy rather than permanent rescue programs.

Under this framework, swap lines serve as an incentive mechanism. They offer trusted partners access to the world’s deepest pool of liquidity and strengthen their ties to dollar-based funding markets. Proposed arrangements with Gulf states and Asian economies can therefore be viewed as efforts to expand the geographic reach of the dollar network rather than emergency measures aimed at defending Treasury demand.

At the same time, the United States retains a second source of influence: its ability to enforce financial restrictions through sanctions, regulatory oversight, and control of key financial infrastructure. In this interpretation, dollar dominance is supported by both incentives and enforcement. Countries gain significant benefits from participating in the dollar system, but they are also aware of the costs associated with operating outside it.

Recent actions targeting Iranian financial networks illustrate this point. Through sanctions programs administered by the Office of Foreign Assets Control and other agencies, the U.S. government continues to demonstrate its capacity to restrict access to international financial channels and freeze assets connected to sanctioned entities. These measures highlight the extent to which global finance remains intertwined with institutions, payment systems, and compliance frameworks linked to the dollar.

The implications extend beyond traditional banking. Cryptocurrencies and stablecoins are often portrayed as alternatives to the existing monetary order, but many of the largest digital-asset ecosystems remain dependent on regulated exchanges, custodians, issuers, and financial intermediaries. As a result, authorities can frequently exercise influence through compliance requirements and enforcement actions, limiting the extent to which these networks operate entirely outside government oversight.

From this perspective, dollar dominance is reinforced through two complementary forces. The first is attraction: deep capital markets, abundant liquidity, reserve-currency status, swap-line access, and the global demand for U.S. Treasury securities. The second is enforcement: sanctions authority, asset freezes, financial blacklists, and regulatory reach. Together, these mechanisms create powerful incentives for governments, banks, and reserve managers to remain connected to the dollar ecosystem.

This does not mean that countries are abandoning efforts to diversify reserves or reduce specific vulnerabilities. Many continue to increase gold holdings, explore alternative payment arrangements, and spread custodial risk across jurisdictions. However, diversification is not the same as disengagement. For many reserve managers, the calculation remains that participation in the dollar-centered financial system offers benefits and stability that are difficult to replicate elsewhere, even as they seek greater flexibility around the margins.

The UAE’s Exit and the De-Dollarization Debate

Supporters of the dollar-dominance thesis point to recent developments in the Gulf as evidence that financial influence often matters as much as formal reserve statistics. In their view, the reported decision by the United Arab Emirates to distance itself from the traditional OPEC framework came at a strategically significant moment, coinciding with discussions about closer financial cooperation with Washington.

The argument focuses on sequence and incentives. During a period of heightened regional uncertainty and financial stress, U.S. policymakers discussed expanding dollar liquidity support to key partners. At the same time, senior UAE officials engaged with representatives from the U.S. Treasury, the International Monetary Fund, and the Federal Reserve System. Proponents of this interpretation argue that access to dollar liquidity, security cooperation, and deeper integration into U.S.-led financial networks created powerful incentives for closer alignment with the dollar-based system.

From that perspective, swap lines are not simply emergency funding mechanisms. They are strategic tools that deepen economic ties and strengthen the network effects that support the dollar’s global role. The broader claim is that countries offered reliable access to dollar liquidity have fewer incentives to build alternative financial architectures around competing currencies.

As a result, advocates argue that this episode weakens the long-running “petroyuan” narrative. Rather than seeing a major Gulf economy move toward a yuan-centered energy pricing system, they see another example of a strategically important state reinforcing its links to the dollar ecosystem.

Counterargument: Does De-Dollarization Still Matter?

The strongest de-dollarization case remains a serious one. Following the freezing of roughly $300 billion of Russian reserves in 2022, many governments concluded that reserve assets held within Western financial systems carried political and geopolitical risks. This prompted efforts to diversify reserve management practices, expand local-currency trade arrangements, accumulate gold, and explore alternatives to traditional dollar settlement networks.

Examples frequently cited include growing cooperation among BRICS members, increased bilateral trade settlement between China and Russia, and shifts in custodial arrangements for foreign-exchange reserves. These developments are real and reflect an ongoing desire among some countries to reduce exposure to potential sanctions risk.

However, supporters of the dollar-dominance view argue that these changes have largely occurred within the existing financial architecture rather than outside it. Moving Treasury holdings from direct custody in the United States to institutions such as Euroclear changes where assets are held, but not necessarily what assets are held. Likewise, increasing bilateral trade settlement in yuan or other currencies does not automatically create a viable alternative to the broader dollar-based system.

The core challenge for de-dollarization remains scale. A reserve currency must provide deep and liquid capital markets, a large supply of high-quality collateral, broad convertibility, legal protections, and global acceptance. While alternatives have made incremental gains, none have yet matched the combination of liquidity, market depth, and network effects that support the dollar.

As a result, the debate today is less about whether diversification is occurring—it clearly is—and more about whether diversification at the margins is sufficient to fundamentally reshape the global monetary system. Thus far, the evidence suggests gradual evolution rather than a rapid displacement of the dollar’s central role.

The key mistake in many de-dollarization arguments is treating diversification as if it were abandonment. Those are not the same thing. Foreign reserve managers are increasingly diversifying where they hold assets and expanding allocations to gold, but neither trend necessarily implies a departure from the dollar-centered financial system.

In practice, many central banks are pursuing two parallel objectives. First, they are reducing custodial concentration by spreading reserve assets across multiple jurisdictions and institutions. Second, they are increasing gold holdings as a hedge against geopolitical and financial uncertainty. Yet these adjustments leave the dollar largely intact as the world’s primary unit of account, dominant settlement currency, and leading reserve asset. Reserve composition may be evolving at the margins, but the underlying structure of the system remains remarkably stable.

The dollar’s influence is also expanding through channels that traditional reserve statistics often fail to capture. One of the most important developments is the rapid growth of dollar-denominated digital assets across emerging markets. In regions such as Latin America, Africa, and Southeast Asia, stablecoins have become increasingly popular as tools for savings, payments, and access to dollar exposure where local currencies face inflation or volatility.

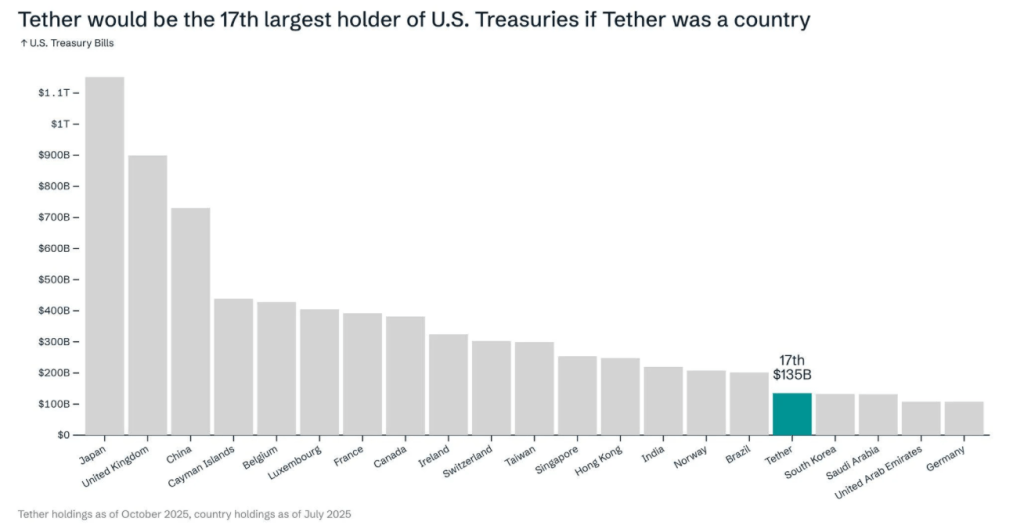

A notable example is Tether, the issuer of the USDT stablecoin. According to the company’s first-quarter 2026 attestation, it held approximately $141 billion in direct and indirect exposure to U.S. Treasury securities as of March 31, supported by total assets of roughly $191.8 billion against liabilities of $183.5 billion. The company also reported a reserve surplus exceeding $8 billion and more than $1 billion in quarterly profit.

These figures are significant because they illustrate how digital-dollar adoption can generate additional demand for U.S. government debt. Stablecoin issuers typically back their tokens with highly liquid dollar assets, including Treasury bills and other short-term government securities. As stablecoin usage grows internationally, so does the indirect demand for dollar-denominated reserves.

Viewed through this lens, digital finance may be reinforcing rather than weakening the dollar’s global position. Instead of replacing the dollar, many of the most widely used digital assets effectively extend the reach of dollar liquidity into markets that previously had limited access to traditional banking infrastructure.

The broader implication is that the future of dollar dominance may not depend solely on central-bank reserve allocations. Increasingly, it may also be shaped by private-sector demand for digital dollars, cross-border payment networks, and new forms of dollar-based financial infrastructure that continue to expand the currency’s global footprint.

The dollar’s reach is increasingly extending beyond traditional banking and central-bank reserves into the digital economy. Supporters of the dollar-dominance thesis argue that this trend is particularly visible in emerging markets, where dollar-linked stablecoins are becoming a preferred vehicle for savings, payments, and wealth preservation.

Recent growth in USDT circulation illustrates the scale of that demand. As the supply of dollar-pegged stablecoins continues to expand, issuers accumulate larger holdings of U.S. Treasury securities and other dollar-denominated assets to back those tokens. In effect, every new digital dollar created generates additional demand for the underlying dollar-based financial infrastructure.

The trend is especially pronounced across parts of Latin America, Africa, and Southeast Asia, where concerns about local currency volatility have encouraged users to hold digital dollars instead of local cash balances. Some industry reports have described this phenomenon as “digital dollarization”—a process in which individuals gain access to dollar exposure through blockchain networks rather than through traditional bank accounts.

From a monetary perspective, this is an important distinction. Many observers originally viewed cryptocurrencies as potential competitors to the dollar. Yet the fastest-growing segment of the digital asset market has often been dollar-backed stablecoins rather than non-sovereign alternatives. As a result, blockchain adoption in many regions has expanded demand for dollar-linked assets rather than displaced them.

Regulatory developments further reinforce this dynamic. The implementation of stablecoin legislation and enhanced compliance requirements has increasingly tied major issuers to the existing financial system. Requirements that reserves be backed by high-quality liquid assets—primarily short-term U.S. government securities—strengthen the connection between stablecoin growth and Treasury demand.

At the same time, regulatory oversight gives authorities greater visibility and enforcement capability within digital-dollar networks. Compliance obligations imposed on issuers, exchanges, and custodians allow regulators to block, freeze, or restrict assets associated with sanctioned entities when required by law. This means that large portions of the stablecoin ecosystem operate not outside the traditional financial system, but as an extension of it.

Viewed through this lens, digital dollars may represent one of the newest channels through which dollar dominance is being reinforced. Rather than creating a parallel monetary order, stablecoins are increasingly embedding dollar liquidity, Treasury demand, and regulatory reach into global digital payments networks.

The broader takeaway is that the future of dollar dominance may depend not only on central banks and sovereign reserves, but also on millions of individuals and businesses choosing to hold digital representations of dollars. If that trend continues, the dollar’s influence could become even more deeply integrated into everyday economic activity around the world.

What This Means for Investors

If the dollar-dominance thesis is correct, the investment implications extend across bonds, equities, gold, and digital-finance infrastructure.

First, persistent foreign demand for U.S. Treasuries suggests ongoing support for the long end of the yield curve, even amid large federal deficits. Strong international demand can help absorb increased issuance and potentially moderate upward pressure on long-term interest rates. From that perspective, duration exposure may offer more value than many deficit-focused forecasts imply.

Second, central-bank gold accumulation appears to be creating a stronger structural foundation for gold prices than existed in previous cycles. That does not necessarily make gold a substitute for fiat currencies. Rather, it reinforces gold’s role as a portfolio diversifier, inflation hedge, and geopolitical-risk buffer. Investors may benefit from maintaining strategic gold exposure, but the argument is increasingly about diversification rather than preparing for the collapse of the monetary system.

Third, the expansion of digital-dollar infrastructure is creating new investment opportunities across payments, custody, and financial technology. Companies such as CRCL, COIN, V, MA, JPM, and BK operate at the intersection of traditional finance and emerging digital-dollar networks, positioning them to benefit if stablecoin adoption continues to grow globally.

The contrarian takeaway is that many investors who positioned heavily for an imminent dollar collapse may have missed some of the strongest-performing asset classes of the past several years. U.S. equities continued to attract capital, Treasury securities remained central to global reserve portfolios, and the broader dollar-based financial system proved more resilient than many critics anticipated.

This does not mean investors should ignore risks. Fiscal deficits, rising debt-service costs, geopolitical tensions, sanctions-related fragmentation, and potential competition from future central bank digital currencies all deserve close attention. These factors could influence the dollar’s long-term trajectory and should remain part of any serious macroeconomic analysis.

However, the evidence presented by proponents of the dollar-dominance view points to a different conclusion than the popular collapse narrative. Foreign demand for Treasuries remains robust. Central banks continue to buy gold while largely operating within a dollar-priced reserve framework. Swap lines are being used to deepen dollar liquidity networks. Stablecoins and digital-dollar platforms are expanding dollar access across emerging markets.

Taken together, these trends suggest that the dollar is not disappearing from the global financial system. Rather, it is adapting to new technologies, new payment channels, and new geopolitical realities while retaining many of the advantages that have supported its dominance for decades.

For investors, the practical lesson is not necessarily to bet exclusively on the dollar, but to recognize that many of the world’s most important financial markets, reserve assets, payment networks, and digital-finance platforms remain deeply connected to the dollar ecosystem. Understanding that infrastructure may prove more valuable than betting on its imminent collapse.

US financial markets will remain closed on Monday in observance of Memorial Day, leaving investors with a shortened trading week and a relatively light economic calendar. Attention will center on Thursday’s release of the second estimate for Q1 2026 GDP, alongside April’s core PCE data — the Federal Reserve’s preferred measure of inflation.

Throughout the week, eight Federal Reserve officials are scheduled to speak. With limited new economic data available to shape expectations around the FOMC’s policy direction, investors will closely analyze their remarks for any hawkish signals. Markets are currently pricing in a 62.5% probability of a rate hike by December, up from 50% just one week earlier, though some analysts believe tightening could arrive as soon as July.

Another key uncertainty remains President Donald Trump’s recently announced “likely negotiated” peace agreement. On Saturday, Trump stated that the arrangement would reopen the Strait of Hormuz. Iran’s foreign ministry noted that the proposed framework currently consists of a memorandum of understanding as an initial step, with broader negotiations expected within the next 30 to 60 days. However, substantial differences between the two sides still persist.

Meanwhile, global bond yields retreated from recent highs but continued to trade at elevated levels. The yield on the US 10-year Treasury declined to 4.56% after peaking at 4.69%, while the UK 10-year gilt yield eased to 4.90% from 5.19%.

GDP

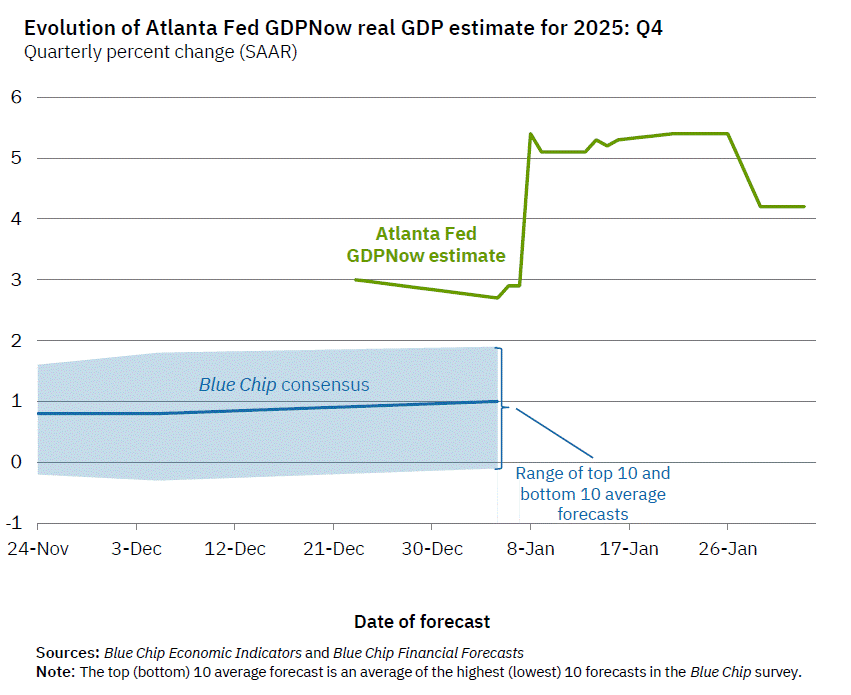

Thursday’s second estimate of Q1 2026 GDP is expected to remain close to the preliminary 2.0% growth reading. Meanwhile, the Atlanta Fed’s GDPNow model is already projecting Q2 growth at 4.3%, supported largely by a sharp increase in business equipment investment.

Core PCED

April’s core PCED — the Federal Reserve’s preferred measure of inflation — will also be released on Thursday. The index rose 3.2% year-over-year in March, accelerating from 3.0% in February, while headline inflation reached 3.5%. With both the latest CPI and PPI figures coming in stronger than expected, markets are increasingly concerned about another upside inflation surprise, which could reinforce expectations for an additional Fed rate hike.

Consumer Confidence

The May Consumer Confidence Index, due Tuesday, is expected to edge higher from April’s reading of 92.8. Market attention will mainly center on the survey’s labor market components, which are anticipated to show modest improvement.

Unemployment

Initial jobless claims, scheduled for release on Thursday, previously came in at 209,000, while the four-week moving average stood at 202,500. Continuing claims were reported at 1.782 million, with the corresponding four-week average at 1.778 million. Overall, the data continues to point toward gradual improvement in labor market conditions.

Regional Business Surveys

This week’s regional Federal Reserve manufacturing surveys will include the Dallas Fed survey on Tuesday and the Richmond Fed survey on Wednesday. Both the national ISM Manufacturing PMI and the average readings from the five regional Fed surveys have shown improvement in recent months, signaling that the manufacturing recovery is becoming increasingly broad-based.

The regional prices-paid average has risen again to 54.9, while the Producer Price Index (PPI) for final demand is already increasing at an annual rate of 6.0%, highlighting persistent inflationary pressures across the production pipeline.

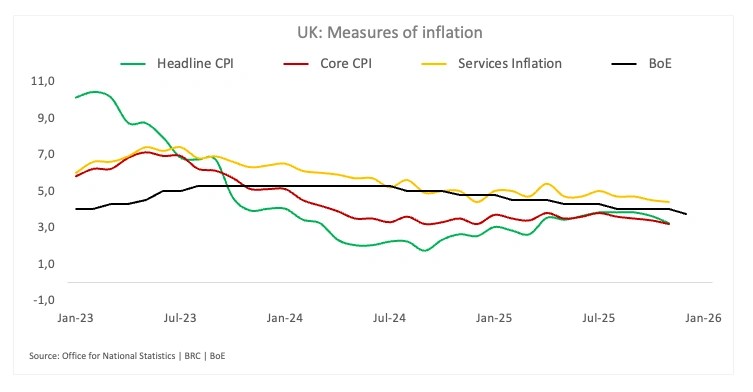

UK annual headline inflation is expected to soften in April even as monthly inflation edges higher.

The upcoming UK CPI report could give the BoE additional room to leave interest rates unchanged in June.

Pressure on the Pound Sterling remains to the downside, while an inflation figure above forecasts may add to the currency’s weakness.

The Office for National Statistics is set to release the UK Consumer Price Index (CPI) data for March at 06:00 GMT.

As inflation remains a key focus for central banks, investors will closely examine April’s CPI figures for clues on the next policy move by the Bank of England. Any significant divergence from market expectations could trigger short-term volatility in the British Pound (GBP).

What to expect from the upcoming UK inflation report

UK annual inflation is projected to ease to 3% in April from 3.3% in March, although monthly CPI growth is expected to accelerate slightly to 0.9% from the previous 0.7% reading.

The reduction in Ofgem’s energy price cap ahead of the Iran conflict appears to have helped limit the impact of higher energy costs, while fading Easter-related price effects have also contributed to moderating inflation pressures.

Core CPI, which excludes volatile items such as energy, food, alcohol, and tobacco, is projected to slow to 2.6% YoY in April — the weakest pace since July 2021 — reinforcing expectations for softer overall inflation.

Alongside the CPI report, the Office for National Statistics will also release April’s Producer Price Index (PPI) data. PPI Input inflation is forecast to cool sharply to 1% from 4.4% in March, while PPI Output inflation is expected to edge up slightly to 1% YoY from 0.9%.

If confirmed, easing inflation pressures could reduce the urgency for the Bank of England to raise interest rates, particularly as UK unemployment continues to rise following Tuesday’s labor market data. However, the relief may prove temporary. Ofgem is scheduled to revise the energy price cap in July, likely leading to higher household energy bills and renewed upward pressure on headline inflation. The BoE currently expects inflation to peak around 4% later this year.

Analysts at TD Securities noted that while the latest inflation figures may offer short-term reassurance, the full impact of higher energy costs is expected to emerge in the third quarter, with potential second-round inflation effects later in the year.

How could the UK CPI report impact GBP/USD?

Inflation remains a central factor in BoE policymaking and therefore has a major influence on the British Pound. Still, Sterling has been weighed down in May by mounting political uncertainty following the Labour Party’s poor performance in local elections, creating additional pressure on the currency.

In this context, a softer-than-expected inflation reading could offer some support to the Pound by giving the BoE more flexibility to monitor domestic conditions and assess the economic fallout from tensions in the Middle East before adjusting interest rates. BoE Deputy Governor Sarah Breeden warned on Monday that political uncertainty is affecting the business climate and cautioned policymakers against acting too aggressively on rates.

On the other hand, a stronger-than-expected inflation print could place the BoE in a more difficult position and potentially deepen bearish sentiment toward the Pound.

From a technical standpoint, Guillermo Alcala believes the British Pound remains under pressure following last week’s decline. He noted that although Monday’s bullish engulfing pattern on the daily chart helped reduce some downside momentum, the near-term outlook for GBP remains bearish. According to Alcalá, buyers still require stronger momentum to reclaim the former support zone near 1.3450 and shift attention toward the mid-May highs around 1.3530–1.3540.

On the downside, he highlighted Monday’s low near 1.3305 as an important support level. A decisive break below that area could pave the way for further losses toward the late-March and early-April highs around 1.3175.

Gold prices traded sideways during Thursday’s Asian session as investors remained cautious ahead of the Trump–Xi summit in Beijing. US President Donald Trump arrived in China for talks with Xi Jinping, with trade tensions and the Iran conflict expected to dominate discussions. Meanwhile, US producer inflation surged at its fastest yearly pace in four years, lending support to the US Dollar.

Gold prices remained largely unchanged during Thursday’s Asian session as investors stayed cautious ahead of the summit between US President Donald Trump and Chinese President Xi Jinping in Beijing. Market attention is also turning to the upcoming US April Retail Sales data due later in the day.

According to Bloomberg, Trump arrived in Beijing on Wednesday for the first state visit to China by a US president in nine years. The meeting comes as Washington and Beijing attempt to stabilize relations amid ongoing geopolitical tensions linked to the Iran conflict.

The US and China are reportedly exploring a framework that would allow both countries to reduce tariffs on approximately $30 billion worth of goods without compromising national security concerns.

Meanwhile, US producer inflation rose at its fastest annual pace in four years, strengthening expectations that the Federal Reserve will keep interest rates elevated to contain persistent inflation pressures.

Data from the US Bureau of Labor Statistics released on Wednesday showed that the Producer Price Index (PPI) climbed 6.0% year-over-year in April, up from 4.3% in March and above market forecasts of 4.9%. On a monthly basis, PPI increased 1.4% after a 0.7% gain in March, significantly exceeding expectations of 0.5%.

Wholesale inflation reached its highest level since December 2022, largely driven by surging oil prices amid Middle East tensions. The stronger inflation data reinforced expectations that the Federal Reserve will maintain higher interest rates for longer, which could pressure Gold prices. Although Gold is often viewed as a safe-haven asset during geopolitical uncertainty, higher interest rates reduce its appeal because the metal does not offer yield.

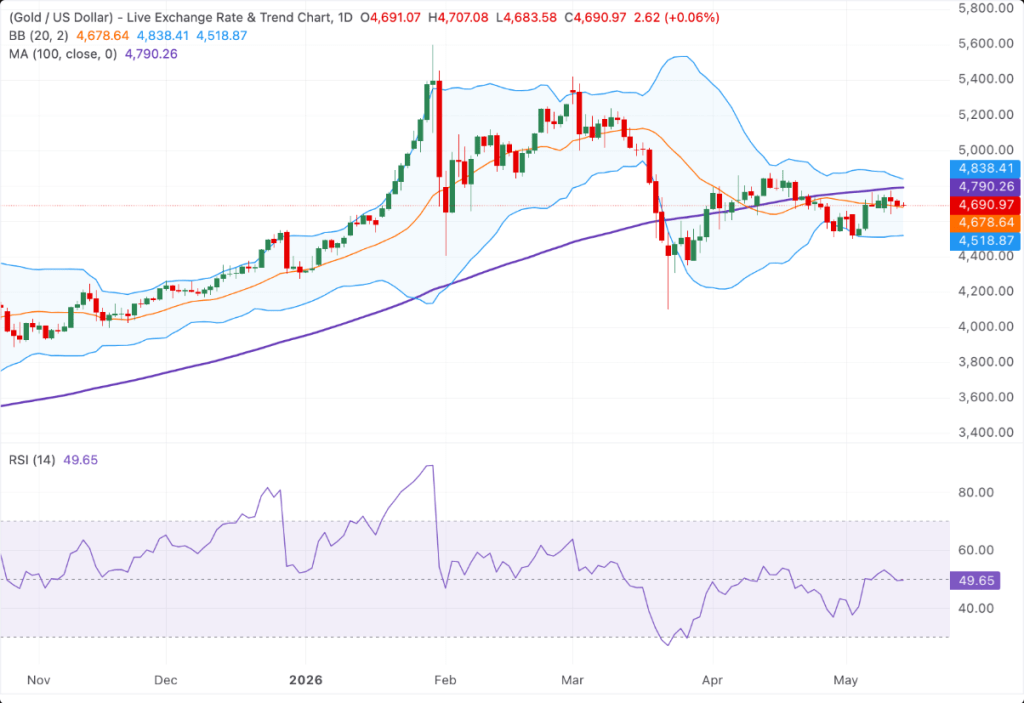

Gold Daily Chart

Technical Analysis

On the daily chart, XAU/USD is trading near $4,690 and continues to show a slightly bearish tone while remaining below the 100-day simple moving average (SMA). The metal is hovering just above the Bollinger Band midpoint, indicating short-term support within the current trading range. Meanwhile, the Relative Strength Index (RSI) stands at 49.65, reflecting neutral momentum and signaling consolidation rather than a strong directional move.

To the upside, the first resistance level is located near the 100-day SMA around $4,790. Additional gains could face resistance near the upper Bollinger Band at roughly $4,838 if bullish momentum strengthens further. On the downside, initial support is found around the Bollinger midpoint near $4,680, followed by a stronger support area close to the lower Bollinger Band around $4,518, where any deeper correction may begin to stabilize.

Gold advocates often argue that an expanding supply of dollars automatically weakens the currency: more money in circulation means each dollar buys less, prices rise, and gold serves as the ultimate hedge against this erosion of purchasing power. From this perspective, growth in the money supply is treated as inherently inflationary.

However, this view is overly simplistic for two main reasons. First, it strips away important context around how and why money supply expands. Second, it ignores a crucial driver of inflation that is just as important as supply itself: the velocity of money.

A recent commentary by Michael Oliver of Momentum Structural Analysis prompted a closer look at this debate. He points out that M2 has increased by roughly 45% since 2020, implying a steady erosion in the real value of cash “year by bloody year,” while reinforcing gold’s role as a preferred alternative store of value. While this is a persuasive narrative, the link between money supply expansion and inflation is not as direct or mechanical as often implied, and requires a more nuanced interpretation of M2 dynamics.

It is also worth noting that Oliver’s bullish stance on gold is not based solely on M2 growth. He also cites several additional factors, including the long-term debasement of fiat currencies by central banks, supportive technical structures, declining confidence in central bank credibility, geopolitical tensions increasing safe-haven demand, and persistent fiscal deficits that necessitate continued monetary accommodation.

Context Matters

Simply pointing to M2 growth in isolation is not meaningful without proper context. To clarify this point, we can refer back to a recent Commentary.

If inflation is the key reason for buying or selling gold, then what truly matters is how money supply growth compares to economic growth. On that basis, the picture changes significantly. During 2020 and 2021, M2 expanded far more rapidly than the real economy. However, in the years since, money supply growth has slowed considerably. Over the broader six-year period referenced by Oliver, GDP growth has actually modestly outpaced M2 expansion.

Assuming, for simplicity, that monetary velocity remains stable (a topic we address separately below), the implication is clear: M2 growth was strongly inflationary during 2020–2021, but in the current environment it is, at best, neutral—and may even be disinflationary or deflationary.

The intuition is straightforward. If an economy produces 10% more goods and services, but the money supply only expands by 5%, there is relatively more supply of goods than purchasing power. That imbalance forces either price reductions or rising unsold inventories. In both cases, the pressure on prices is downward rather than upward.

In that sense, if gold is being held primarily as a hedge against inflation, then relying on M2 growth alone may have been a reasonable argument during the pandemic-era monetary surge. But under current conditions, that same rationale is far less convincing without additional supporting factors.

Monetary Velocity Also Matters

Consider a simple thought experiment.

What if the government secretly printed an enormous amount of money, locked it away in a vault, and permanently lost the key? Would that sudden increase in the money supply drive prices of goods and services higher?

The answer is no—it would have virtually no impact.

Now imagine a different scenario: rumors of that hidden stockpile begin to circulate. Even though the money still isn’t being spent, expectations shift. People start to anticipate future spending, and that change in behavior alone could begin to influence prices.

The distinction here is important. Inflation is not determined solely by how much money exists “on paper.” It also depends on how actively that money is used—how quickly it circulates through the economy. This is what economists refer to as monetary velocity.

In other words, price levels are shaped not just by the supply of money, but by the willingness and ability of households, businesses, and institutions to spend it. When velocity is high, money changes hands quickly and exerts more upward pressure on prices. When velocity is low, even a large money supply may have limited inflationary impact.

This is why analyzing inflation through M2 alone can be misleading: without considering velocity, the picture is incomplete.

What Is Monetary Velocity

According to the Federal Reserve Bank of St. Louis, the velocity of money refers to the rate at which a single unit of currency is used to purchase domestically produced goods and services over a given period of time. In simpler terms, it measures how often each dollar is spent within the economy.

Put differently, it reflects how many times one dollar changes hands to facilitate transactions during a specific timeframe. When monetary velocity rises, it indicates that more economic transactions are taking place between individuals and businesses, signaling a more active flow of spending.

Velocity is therefore influenced by both economic activity and the money supply. A shrinking money supply does not necessarily imply lower prices if economic activity is strong and money is circulating rapidly—velocity can rise and still exert upward pressure on prices. Conversely, even if the money supply expands significantly, inflation may remain muted if that money is not actively being spent, meaning demand for goods and services stays weak and price pressures remain limited.

In short, monetary velocity helps explain why the relationship between money supply and inflation is not mechanical: it is the interaction between how much money exists and how quickly it is used that ultimately matters for price dynamics.

What Impacts Velocity?

Monetary velocity doesn’t move randomly—it reflects how people, businesses, and financial systems behave. A range of economic and psychological factors can either accelerate or slow the rate at which money changes hands.

Factors typically associated with higher velocity

These conditions encourage spending, investing, and faster circulation of money:

Lower interest rates — reduce the incentive to hold cash, encouraging spending and investment instead

Strong consumer and business confidence — optimism about the future leads to higher spending activity

Rising inflation expectations — if people expect prices to increase, they tend to spend sooner rather than later

Easy credit conditions — abundant lending increases effective purchasing power and transaction volume

Technological innovation — new products, services, and platforms create additional channels for spending

Income and wage growth — higher earnings support more frequent and larger transactions

Economic expansion — growing output naturally leads to more economic exchanges per unit of money

Factors typically associated with lower velocity

These conditions encourage saving, caution, or reduced spending:

Recessions or economic uncertainty — fear leads households and firms to defer spending

Expectations of falling prices (deflation) — consumers delay purchases in anticipation of cheaper goods later

Debt reduction (deleveraging) — paying down loans removes credit-driven money from active circulation

Aging populations — older demographics generally spend less and save more

Financial or banking stress — tighter credit conditions reduce lending and the “multiplier” effect of money

The key takeaway

Velocity is ultimately a behavioral and structural variable. It reflects confidence, incentives, credit conditions, and demographics—not just monetary policy or money supply figures. This is why two economies with similar M2 growth can experience very different inflation outcomes depending on how actively money is being used.

M2 and Core CPI

With a clearer understanding of monetary velocity, we can re-examine the common claim among gold advocates that M2 growth and inflation move closely together.

To test this more rigorously, a regression analysis is conducted using quarterly data on M2 and monetary velocity against Core CPI since 2010.

In this context, Core CPI is used instead of headline CPI because it excludes volatile food and energy components. These categories are often influenced by short-term shocks such as geopolitical events or weather conditions, which can obscure underlying inflation trends. By focusing on Core CPI, the analysis aims to capture a more stable and statistically meaningful relationship.

The first step of the analysis examines how M2 alone relates to Core CPI, allowing us to quantify the direct association between money supply growth and underlying inflation over time.

The results suggest that M2 growth, in isolation, has a very weak and statistically insignificant relationship with Core CPI. The R-squared value of 5.13% implies that changes in M2 explain only a small fraction of the variation in Core CPI over the sample period. In practical terms, most inflation dynamics are driven by other factors outside the money supply variable alone.

The negative t-statistic (-1.771) further indicates that the estimated relationship is not only weak but also inversely signed in this model specification—meaning that, within this dataset, higher M2 growth is associated with slightly lower Core CPI. However, this relationship is not statistically robust and should not be interpreted as causal.

Using the regression equation to forecast Core CPI from M2 alone therefore produces unreliable results. As expected from the low explanatory power of the model, the output has little predictive value and is effectively not useful for practical forecasting.

Overall, the takeaway is that M2 by itself is a poor standalone indicator of inflation dynamics, reinforcing the importance of incorporating additional variables—such as velocity, credit conditions, and broader economic activity—when analyzing price pressures.

M2, Velocity, and CPI

Next, we extend the analysis by incorporating monetary velocity into the multiple regression framework alongside M2.

The R-squared value indicates that the relationship becomes substantially stronger when both M2 and monetary velocity are included in the model, with the combined variables explaining more than half of the variation in Core CPI.

In addition, the F-statistic’s near-zero p-value suggests that the overall model is highly statistically significant, meaning there is a very low probability that these results are due to chance.

Finally, when the model’s implied Core CPI is plotted against actual Core CPI, the comparison shows that the combination of money supply and velocity tracks inflation much more closely than M2 alone. This supports the view that inflation dynamics are better understood as a function of both liquidity (M2) and its rate of circulation (velocity), rather than money supply in isolation.

Summary

There are valid reasons to buy and hold gold, but for short-term traders, it is important to understand the narratives that often drive gold price action.

The idea that rising money supply alone explains inflation—and therefore supports higher gold prices—can be misleading. As discussed, this relationship needs to be placed in proper context relative to economic growth. Equally important is not just the quantity of money in circulation, but the rate at which it circulates through the economy, or monetary velocity.

Many widely accepted macro narratives appear intuitive at first glance, but lose explanatory power once examined more closely. It is in these gaps between narrative and reality that investors can better understand the true drivers of asset prices—and reduce the risk of being caught offside when simplified stories fail to hold up in practice.

USD/GBP has remained under pressure since early April, driven mainly by uncertainty among central banks over how the conflict in Iran could affect inflation and energy prices. On Thursday, April 30, a fresh batch of economic data reinforced the cautious stance adopted by both the Federal Reserve (Fed) and the Bank of England (BoE).

Over the past month, the pair has fallen 2.8%, with ongoing tensions in the Middle East continuing to fuel market volatility.

While recent inflation data from both the United States and the United Kingdom drew attention, markets remained focused on the broader energy risks linked to the closure of the Strait of Hormuz, which has become a key factor behind the cautious outlook.

Energy driving USD/GBP

For currency traders, USD/GBP has increasingly behaved like a proxy for crude oil rather than reacting primarily to interest rate differentials, though energy market disruptions have also directly influenced monetary policy expectations on both sides of the Atlantic.

Over the past week, the pair has maintained a notably strong correlation with Brent crude, ranging between 0.96 and 0.97. In practical terms, this suggests that USD/GBP tends to rise alongside oil prices and fall when crude declines. Since correlations closer to 1 indicate an almost perfect relationship, the current pattern highlights the extent to which oil prices are steering movements in the pair.

Recent volatility in crude — which briefly surged nearly 7% to a four-year high of $126 per barrel — was largely triggered by reports that the US military was preparing to brief President Donald Trump on potential new actions involving Iran.

“We saw oil prices climb on fears over supply disruptions, making energy one of the few sectors to post gains,” Wealthify said in its monthly market summary. “Equity markets declined broadly, with losses across the US, Europe, the UK, and Asia, leaving investors with limited regional shelter.”

“The Federal Reserve kept rates unchanged in March, but rising oil prices and inflation concerns cast uncertainty over future rate cuts, pressuring bond prices lower. In the UK, mounting inflationary pressures alongside a softer labour market strengthened expectations that the Bank of England may keep rates elevated for longer, with the possibility of another hike later this year.”