The Australian Dollar softened even as China’s RatingDog Manufacturing PMI edged up to 50.3 in January from 50.1. Meanwhile, Australia’s TD-MI Inflation climbed 3.6% year over year, though the monthly increase eased to 0.2%, its slowest pace since August. The US Dollar could gain further support after Donald Trump nominated Kevin Warsh as Fed Chair, a move seen as signaling a more cautious stance on monetary easing.

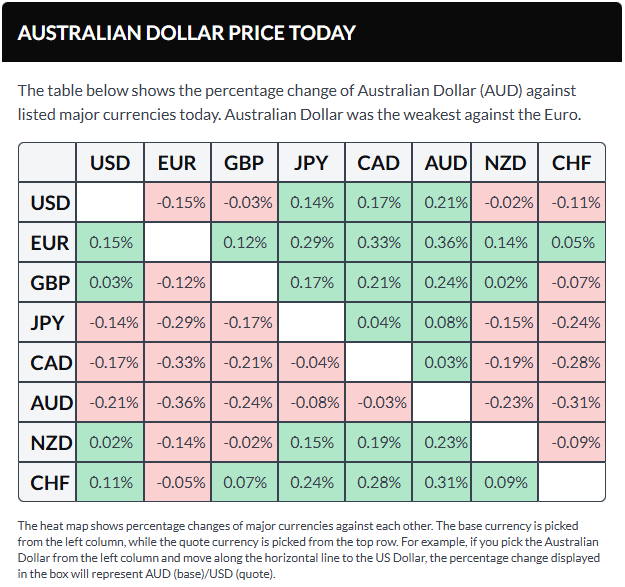

The Australian Dollar weakened against the US Dollar on Monday, extending losses after falling more than 1% in the prior session. The AUD/USD pair stayed under pressure despite China’s RatingDog Manufacturing PMI ticking up to 50.3 in January from 50.1 in December, in line with market expectations. While the reading signaled a modest expansion in factory activity, it marked the strongest growth since October.

Meanwhile, Australia’s TD-MI Inflation Gauge rose to 3.6% year over year in January from 3.5% previously. On a monthly basis, inflation increased by 0.2%, easing sharply from December’s two-year high of 1% and registering its slowest pace since August.

ANZ Job Advertisements surged 4.4% month over month in December 2025, rebounding from a revised 0.8% decline and marking the first increase since July. The rise was also the strongest monthly gain since February 2022, pointing to renewed hiring momentum toward the end of the year.

The data come ahead of the Reserve Bank of Australia’s policy meeting on Tuesday, following the central bank’s decision to keep the cash rate unchanged at 3.6% for a third consecutive meeting in December. Policymakers are widely expected to maintain a cautious stance, as underlying inflation remains above target and labor market conditions stay relatively tight, supporting a restrictive and data-dependent policy approach.

Meanwhile, Australia’s Consumer Price Index increased 3.8% year over year in December, up from 3.4% previously. With headline inflation still exceeding the RBA’s 2–3% target range, recent PMI and employment indicators strengthen the argument for a tighter monetary policy bias.

US Dollar edges lower ahead of ISM Manufacturing PMI

The US Dollar Index (DXY), which tracks the Greenback against six major currencies, is edging lower after posting gains of more than 1% in the previous session, trading near 97.10 at the time of writing. Market attention is turning to the release of the US ISM Manufacturing PMI for January later in the day.

Despite the modest pullback, the US Dollar had recently drawn support following President Donald Trump’s nomination of Kevin Warsh as the next Federal Reserve Chair, a move markets viewed as signaling a more disciplined and cautious approach to monetary easing. The Greenback also benefited from improved risk sentiment after the US Senate reached an agreement to advance a government funding package, averting a potential shutdown, according to Politico.

US producer-side inflation data further underpinned the Dollar, reinforcing the Federal Reserve’s restrictive policy stance. Headline PPI remained unchanged at 3.0% year over year in December, exceeding expectations for a slowdown to 2.7%. Core PPI, which excludes food and energy, accelerated to 3.3% YoY from 3.0%, defying forecasts for a decline to 2.9% and highlighting persistent upstream price pressures.

Federal Reserve officials echoed a cautious tone on easing. St. Louis Fed President Alberto Musalem said additional rate cuts are not justified at present, describing the current 3.50%–3.75% policy rate range as broadly neutral. Atlanta Fed President Raphael Bostic also urged patience, arguing that monetary policy should remain modestly restrictive.

In Australia, inflation and trade data pointed to continued price pressures. The RBA’s Trimmed Mean inflation rose 0.2% month over month and 3.3% year over year, while the monthly CPI jumped 1.0% in December from zero previously, exceeding forecasts of 0.7%. Export prices increased 3.2% quarter over quarter in Q4 2025, rebounding from a 0.9% decline in Q3 and marking the strongest gain in a year, while import prices climbed 0.9%, beating expectations for a fall and reversing a prior decline.

Following the data, markets now price in more than a 70% probability of a 25-basis-point rate hike by the Reserve Bank of Australia from the current 3.6% cash rate, up from around 60% previously. Rates are fully priced at 3.85% by May and near 4.10% by September.

Australian Dollar slides toward key confluence support near 0.6900

The AUD/USD pair is trading near 0.6940 on Monday. Analysis of the daily chart shows the pair continuing to move higher within an ascending channel, pointing to a sustained bullish bias. The 14-day Relative Strength Index has eased from the 70 level to around 67, suggesting a cooling in bullish momentum rather than a trend reversal.

On the upside, AUD/USD could recover toward 0.7093, its highest level since February 2023, reached on January 29. A sustained break above this level would open the door for a test of the channel’s upper boundary near 0.7190. On the downside, initial support is seen at a confluence zone around the nine-day Exponential Moving Average at 0.6927, which aligns closely with the lower boundary of the ascending channel near 0.6920.

AUD/USD: Daily Chart

Sources: Investing

Leave a comment