DXY bulls remain cautious, avoiding aggressive positioning as they await greater clarity on evolving geopolitical risks.

Higher oil prices are stoking inflation concerns and reinforcing expectations of additional Federal Reserve rate hikes, providing support for the US Dollar.

The favorable fundamental environment indicates that any near-term pullbacks are likely to attract fresh buying interest.

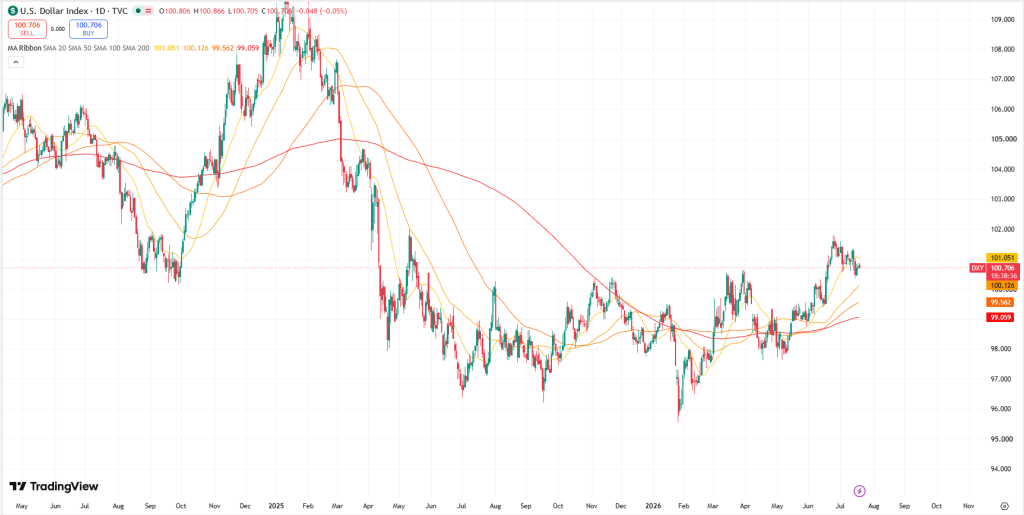

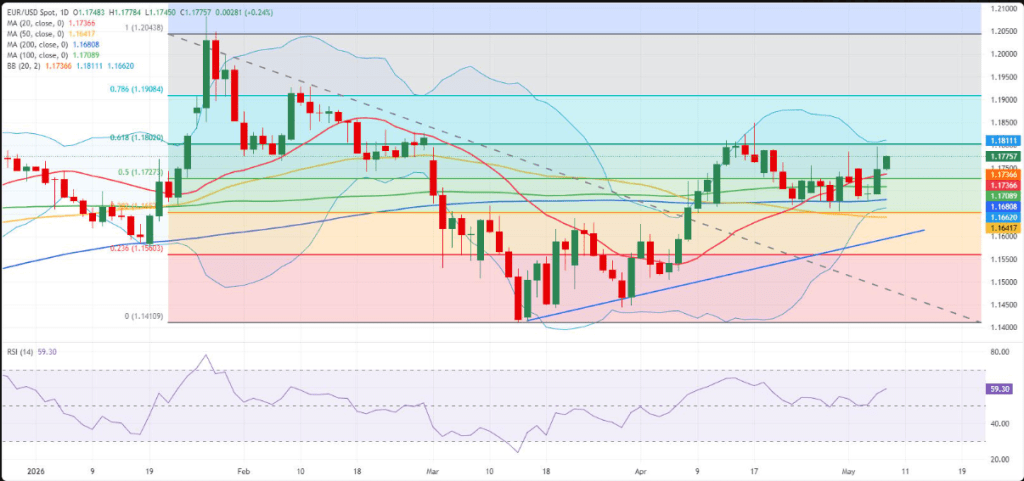

The US Dollar Index (DXY), which measures the Greenback against a basket of major currencies, is struggling to build on a modest uptick during Monday’s Asian session and is hovering near the 100.80–100.75 area, little changed on the day. Despite the subdued price action, the broader outlook remains supportive for the US Dollar as escalating US-Iran tensions and expectations of a more hawkish Federal Reserve continue to underpin sentiment.

The Middle East conflict intensified over the weekend after the United States carried out a ninth consecutive night of strikes against Iran, following reports of another American service member being killed in Iraq. President Donald Trump stated that the operation was conducted in response to recent US military casualties. Iran retaliated by launching ballistic missiles and attack drones at targets in Bahrain, Jordan, Kuwait, and Iraq, heightening fears of a wider regional conflict. The growing geopolitical uncertainty is encouraging investors to maintain a risk premium in markets, boosting demand for the US Dollar as a traditional safe-haven asset.

At the same time, crude oil prices have surged to their highest levels since June 12, driven by concerns over supply disruptions linked to the closure of the Strait of Hormuz and a US naval blockade of Iranian ports. The sharp rise in energy costs is reviving inflation worries and increasing expectations that major central banks, including the Fed, may need to keep monetary policy tighter for longer. Market pricing reflected in the CME FedWatch Tool continues to indicate the possibility of at least one Fed rate hike in 2026, reinforcing the constructive outlook for the Greenback and limiting downside risks for the DXY.

Looking ahead, the US economic calendar is relatively quiet on Monday, leaving the Dollar largely influenced by remarks from Federal Open Market Committee (FOMC) officials and developments in the Middle East. While geopolitical headlines are likely to remain a key source of volatility, the overall fundamental backdrop continues to favor the bulls, suggesting that any notable pullbacks in the DXY are likely to attract fresh buying interest.

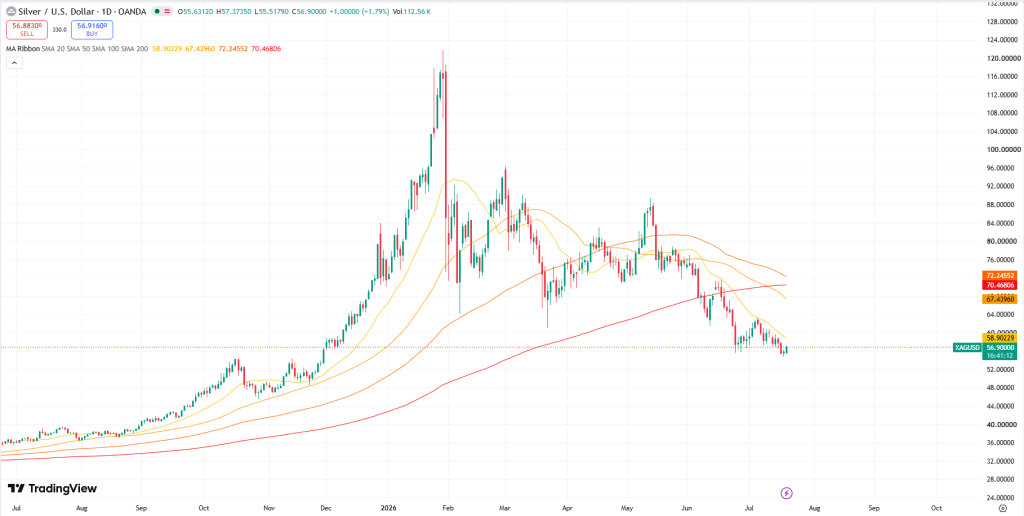

Silver remains under pressure as escalating US-Iran tensions drive oil prices higher, stoking inflation concerns and reinforcing expectations of further Fed tightening.

Overnight US military strikes on Iran led Tehran to declare the ceasefire void, raising the risk of significant disruptions to global energy supply routes.

Cleveland Fed President Beth Hammack reiterated on Friday that inflationary pressures continue to persist.

Silver prices (XAG/USD) extended their advance for a second straight session, trading near $56.80 per troy ounce during Monday’s Asian session. Despite the recent rebound, the precious metal may encounter headwinds as escalating tensions between the United States and Iran continue to push crude oil prices higher, reviving inflation concerns and strengthening expectations that the Federal Reserve could tighten monetary policy further.

The US has carried out a ninth consecutive night of strikes against Iranian-linked targets. In response, Tehran announced that the ceasefire arrangement between the two countries is effectively over, raising concerns about potential disruptions to key energy transit routes across the Middle East.

Regional tensions intensified further after Iran launched a new barrage of ballistic missiles and one-way attack drones targeting locations in Bahrain, Jordan, Kuwait, and Iraq, triggering air raid warnings across parts of the Gulf. At the same time, the US military confirmed the death of another service member, bringing the total to three casualties within two days.

The conflict has increasingly affected civilian infrastructure, with reports of damage to bridges, utility networks, and port facilities. Adding to concerns over energy security, Kuwait Petroleum Corp. stated that one of its oil installations was struck by an Iranian attack over the weekend.

Although investors largely expect the Federal Reserve to leave interest rates unchanged at its next policy meeting, market expectations for tighter monetary policy have increased. According to CME FedWatch data, traders are now pricing in a 61.4% chance of a rate hike in September, reflecting growing concerns that higher energy prices could reignite inflationary pressures.

Hammack highlights widespread inflation risks, supporting a hawkish Fed outlook

Cleveland Fed President Beth Hammack delivered a notably hawkish message, earning a 7.2/10 FXS SpeechTracker score, comfortably above the historical average of 6.6/10. Her remarks reflected growing concern that inflationary pressures remain entrenched across the economy. By stressing calls from businesses for stronger measures to contain rising prices and noting that many households continue to struggle financially despite solid economic growth and resilient consumer spending, Hammack underscored the disconnect between healthy economic activity and increasing cost-of-living challenges.

She also pointed to several sources of inflation pressure, including elevated energy costs, supply-chain constraints, rising insurance expenses, and growing demand linked to AI infrastructure and data-center investments. By identifying persistent inflation as the primary risk facing policymakers, Hammack’s comments reinforced expectations that the Federal Reserve may maintain a restrictive policy stance for longer, providing underlying support for the US Dollar.

Meanwhile, the FXS Fed Sentiment Index climbed 2.06 points to 128.64, signaling that overall Fed communication remains firmly tilted toward tightening and well above the neutral threshold of 100. Combined with Hammack’s above-average hawkish score, the increase suggests that policymakers continue to prioritize inflation control over concerns about economic growth, a backdrop that generally favors the Dollar against lower-yielding currencies.

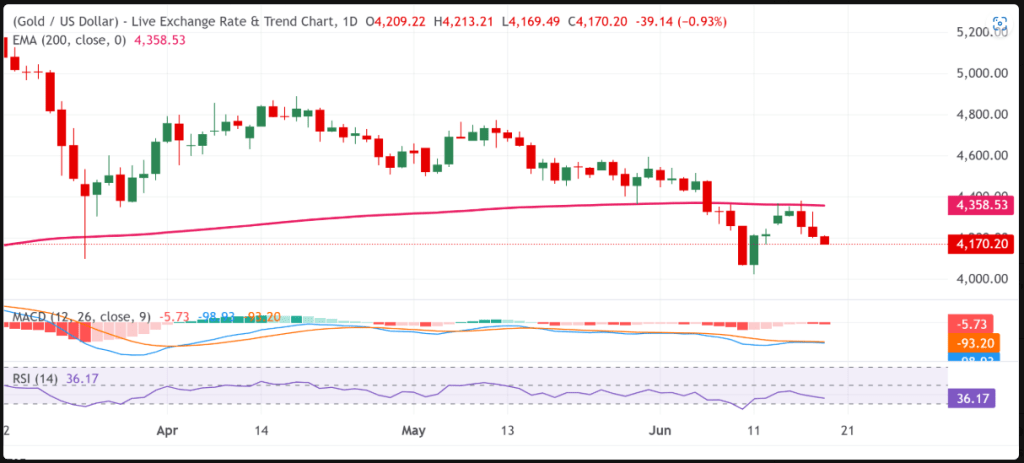

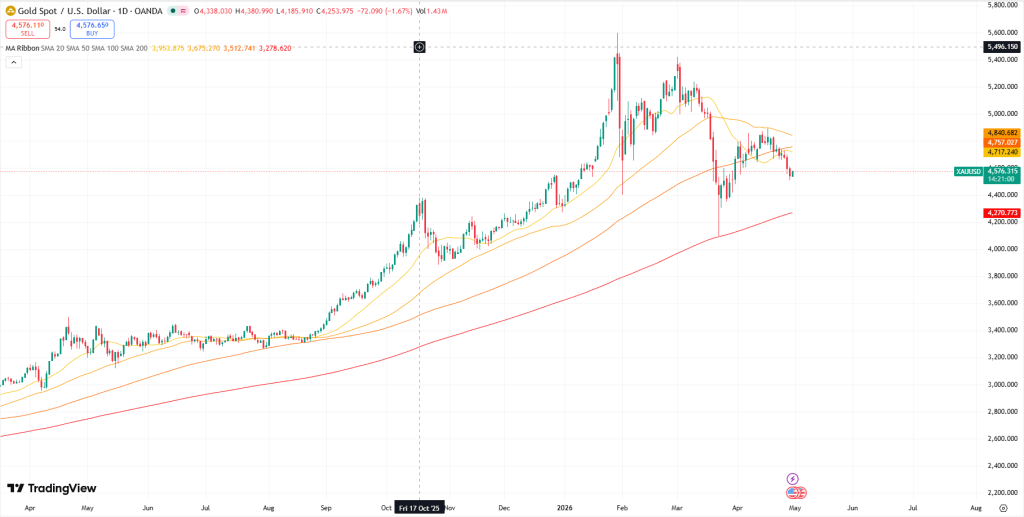

Gold’s $4,000 Test Signals Interest Rates Are Overriding Safe-Haven Demand

Gold futures dropped to $4,008.80, down $43.00 (1.06%), after opening at $4,068.90, slightly above Wednesday’s close. Spot gold weakened even further, falling to $4,010.33 by 11:03 EDT, a daily loss of $57.22. After trading near $4,041 early in the session, bullion came under steady selling pressure throughout the day.

Gold’s recent performance reflects a sharp reversal in momentum. Prices have declined 5.25% over the past month, although they remain 20.89% higher than a year ago. Since reaching $4,121.05 on July 10, the metal has steadily retreated, ending that week around $4,100 before sliding to $4,013.64 on July 13 as it tested the $4,000 level. Today’s move marks yet another return to that critical support, with the June low resting at $4,002.

The repeated tests of $4,000 suggest the market’s focus has shifted. Rather than responding primarily to geopolitical uncertainty, gold is increasingly trading in line with interest rate expectations. Rising tensions between the United States and Iran have lifted oil prices, reinforcing inflation concerns and increasing expectations that the Federal Reserve could keep monetary policy tighter for longer. Higher real yields raise the opportunity cost of holding non-yielding assets such as gold, limiting the metal’s appeal despite heightened geopolitical risks.

The broader precious metals market reflects the same trend. Silver fell to $56.90, while August Comex silver futures declined more than 3% to $57.095. Platinum slipped to $1,656.30, and palladium dropped to $1,295.75, highlighting broad-based selling across the sector as markets reassessed the outlook for inflation and interest rates.

Although softer-than-expected U.S. inflation data briefly supported gold by reducing expectations of an imminent Fed rate hike, the relief proved short-lived. As oil prices surged on renewed Middle East tensions, inflation concerns quickly resurfaced, sending gold back toward $4,000. The swift reversal from a CPI-driven rally to an oil-driven selloff illustrates the dominant theme shaping the 2026 gold market: interest rate expectations now carry more weight than traditional safe-haven demand.

War Is Hurting Gold Through Oil, Not Supporting It as a Safe Haven

The current weakness in gold reflects a market driven more by interest rate expectations than traditional safe-haven demand. The transmission mechanism is straightforward: military escalation raises concerns over crude oil supply, pushing energy prices higher. More expensive oil feeds into headline inflation, strengthening the case for the Federal Reserve to keep interest rates elevated—or tighten further. Higher real yields increase the opportunity cost of holding non-yielding assets like gold, encouraging institutional investors to reduce exposure.

Rather than acting as a catalyst for safe-haven buying, geopolitical tensions are being interpreted primarily through their impact on inflation and monetary policy.

That dynamic explains why gold has continued to decline despite intensifying conflict in the Gulf. Investors are viewing the risk surrounding the Strait of Hormuz as an interest-rate story: higher oil prices support higher bond yields and a firmer U.S. dollar, reducing gold’s appeal. The conflict itself remains significant, but the market is responding through the inflation channel instead of the traditional flight-to-safety narrative.

Oil prices continue to reinforce that view. Brent crude trades around $84.63, up 6.39% over the past month and 21.74% from a year ago, while WTI crude remains above $80 after rallying more than 11% in three sessions. Recent U.S. strikes on Iranian targets and Iran’s retaliation against American military bases across the Gulf have heightened concerns over energy supplies.

The sequence of events also helps explain the sharp swings in sentiment. A Memorandum of Understanding signed by Iran and the United States on June 17 had raised hopes for improved relations, including the easing of sanctions on Iranian oil exports and reduced disruption around the Strait of Hormuz. Those expectations unraveled on July 6, when attacks on commercial shipping prompted military retaliation, placing the agreement under severe strain.

The contrast with earlier in the year is notable. Gold rallied during the February escalation but has fallen during the July conflict because the macro backdrop has changed. Earlier, geopolitical risks boosted demand for defensive assets. Today, the same risks are reinforcing expectations of tighter monetary policy, fundamentally altering the market’s response.

A reversal remains possible but would likely require either a prolonged disruption to shipping through the Strait of Hormuz that sparks a genuine flight to safety or a deterioration in global growth severe enough to drive bond yields lower. Reports that Tehran remains open to renewed negotiations reduce the likelihood of either scenario in the near term, leaving interest rate expectations as the dominant force weighing on bullion.

Gold Has Fallen 28% From Its Record High

Gold has retreated dramatically from its January 29 record of $5,589 per ounce to approximately $4,008.80, a decline of 28.3%, or $1,580, in less than six months.

The rally earlier this year was extraordinary. Gold surged above $5,000 for the first time, briefly touched $5,595 intraday, and established multiple all-time highs before suffering a historic reversal. After peaking in late January, prices traded sideways through much of the first quarter before breaking sharply lower in March. A modest rebound in April eventually gave way to another steady decline toward the $4,000 area, with June’s low at $4,002.

Despite the correction, the longer-term picture remains relatively resilient. Gold is down roughly 7% year-to-date but still trades nearly 21% above year-ago levels and remains about $578 above its 2025 year-end close of $3,431. In that context, the decline represents a significant retracement of an exceptionally rapid rally rather than the complete breakdown of the longer-term bullish trend.

However, the technical landscape has changed. Analysts previously viewed the $4,550 region—formed by late-December highs and early-2026 support—as a major floor. That level failed during March’s selloff and now sits roughly $460 above current prices, removing an important layer of technical support.

Heavy Liquidation Intensified the Selloff

The decline was amplified by two major liquidation waves rather than a gradual reassessment of gold’s long-term value.

The first came immediately after January’s record highs, when gold plunged nearly $1,200 in just two trading sessions, marking its steepest two-day decline since 1983. The second occurred in March, when prices fell roughly 13%, producing the worst monthly decline since 2009. In both cases, rising interest-rate expectations linked to higher energy prices overshadowed gold’s traditional role as a defensive asset.

Despite the sharp correction, Wall Street remains broadly constructive. A Reuters survey of analysts projects a 2026 median gold price of $4,746.50 per ounce, the highest consensus forecast since the poll began in 2012. With gold currently near $4,009, prices remain roughly 15.6% below that consensus estimate.

Liquidity dynamics also played an important role. During periods of market stress, institutional investors often sell their most liquid holdings to meet margin calls or raise cash quickly. Gold’s liquidity makes it a frequent source of funding, creating a paradox in which a traditional safe-haven asset can come under heavy selling pressure precisely when uncertainty rises.

That behavior was evident on March 4, when the SPDR Gold Shares (GLD) experienced approximately $2.91 billion in net outflows in a single session—the largest daily withdrawal in more than a decade. Combined with profit-taking from investors who benefited from gold’s rapid rise earlier in the year, those outflows accelerated the correction. As momentum traders exited, ownership shifted toward longer-term investors whose buying tends to be steadier but less aggressive, leaving the market without the speculative demand that previously fueled the rally.

Rising Real Yields Continue to Undermine Gold

The surge in U.S. Treasury yields has become one of the primary headwinds for gold. The 10-year Treasury yield climbed to 4.60% on Thursday, approaching the two-month high of 4.62% reached on July 13, as investors increasingly positioned for another Federal Reserve rate hike.

The key driver is real yields—bond yields adjusted for inflation expectations—rather than nominal interest rates alone. As expectations for tighter monetary policy increase, real yields rise, making income-generating assets more attractive relative to gold, which offers no yield. Conversely, when markets anticipate fewer rate hikes or eventual easing, real yields typically decline, improving gold’s relative appeal.

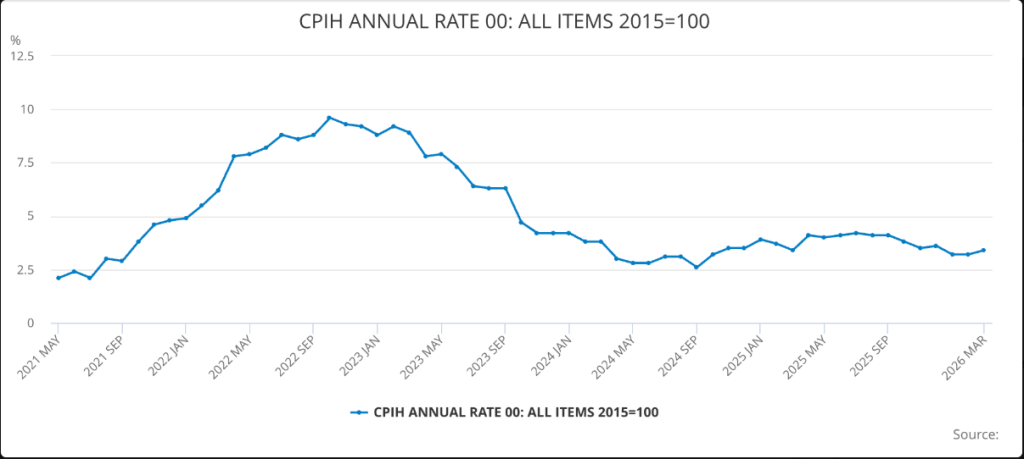

That dynamic briefly supported bullion after June’s softer inflation data. Consumer prices fell 0.4% month over month, the largest monthly decline since April 2020, while annual CPI eased to 3.5% and core inflation held at 2.6%. Producer prices also slipped 0.3%, marking their first monthly decline in nearly a year as energy costs retreated. Gold initially benefited from the weaker inflation readings.

However, the rally proved short-lived as stronger economic data quickly shifted attention back to the Fed. Retail sales remained resilient despite lower fuel prices, while initial jobless claims fell to 208,000, a two-month low, reinforcing confidence in the labor market. Those developments strengthened expectations that the Federal Reserve could still tighten policy later this year. Interest-rate futures currently imply roughly a 44% probability of a September rate hike, down from 50% a day earlier but still keeping additional tightening firmly on the table.

A stronger U.S. dollar has added further pressure. Supported by higher Treasury yields and a resilient U.S. economy, the Dollar Index remains near 100.49. Earlier in 2026, a weaker dollar helped propel gold to its record high of $5,589, but the recent rebound in the greenback has reversed that tailwind.

History, however, offers a note of caution. Gold has often performed well after Federal Reserve rate increases, averaging gains in the month following a 25-basis-point hike during several previous tightening cycles. The decisive factor is not the hike itself but whether tighter policy ultimately slows economic growth enough to push yields lower.

A More Hawkish Federal Reserve Has Increased Uncertainty

Since taking office as Federal Reserve Chair in May 2026, Kevin Warsh has adopted a notably less predictable communication strategy. During congressional testimony in mid-July, he followed a June Federal Open Market Committee meeting that left rates unchanged but shifted the policy outlook in a more hawkish direction.

One notable feature of the June meeting was Warsh’s decision not to publish his own interest-rate projection in the Fed’s dot plot. Combined with the removal of explicit forward guidance, the move increased uncertainty around future monetary policy and made it more difficult for markets to anticipate the Fed’s reaction function.

Markets currently expect the July 28–29 FOMC meeting to end with rates unchanged, assigning roughly a 90% probability to a hold. Nevertheless, investors continue to see September as a realistic opportunity for another rate increase.

The broader policy backdrop also remains restrictive. The World Gold Council (WGC) expects at least one Federal Reserve rate hike in 2026 while anticipating additional tightening by the Bank of England, Bank of Japan, and European Central Bank. Simultaneous tightening across several major central banks reduces the currency-diversification advantages that previously supported gold.

The macroeconomic outlook remains relatively stable, with global growth projected around 2.9%, U.S. growth near 2.1%, U.S. inflation peaking around 3.9%, and global inflation averaging 4.3% during 2026. Under those conditions, elevated real yields continue to reduce the incentive to hold gold.

The primary upside risk for bullion would be a sharper-than-expected economic slowdown. According to Bank of America’s June fund manager survey, 58% of respondents expect stagflation. Should tighter monetary policy significantly weaken growth, declining yields could eventually restore support for gold.

The World Gold Council Sees Gold Near Fair Value

The World Gold Council’sMid-Year Outlook 2026, titled Point Break, values gold using a framework based on real yields, inflation expectations, the U.S. dollar, and central-bank demand. Under its baseline macroeconomic scenario, the model estimates fair value near $4,100 per ounce, with a tolerance range of roughly ±5%, implying a second-half trading band between $3,895 and $4,305.

With gold trading around $4,008.80, prices remain comfortably within that projected range. The implication is that current valuations broadly reflect consensus expectations of one additional Fed rate hike and inflation peaking near 3.9%, suggesting the market is neither significantly overvalued nor deeply undervalued.

That assessment limits both bullish and bearish arguments. It weakens expectations of a sharp collapse because the WGC’s framework identifies fundamental support near $3,895, but it also challenges forecasts of a rapid return to $5,200–6,000 unless the macroeconomic outlook changes substantially.

Future price direction will largely depend on shifts in economic growth, geopolitical developments, and the U.S. dollar. The WGC notes that while geopolitical tensions drove much of gold’s volatility during the first half of the year, currency movements could become an equally important variable in the months ahead.

Central-Bank Buying Provides Support—but Not Momentum

Central banks continue to accumulate gold despite the recent correction. The People’s Bank of China (PBoC) purchased 15 tonnes in June—its largest monthly acquisition since October 2023—marking the 20th consecutive month of reserve accumulation. China’s official gold holdings have now reached 2,346 tonnes, representing roughly 9% of its total foreign-exchange reserves.

Worldwide, central banks acquired an estimated 244 tonnes during the first quarter of 2026, with countries such as Poland also continuing to expand their holdings.

While these purchases provide an important source of structural demand, they have not prevented prices from falling. Central banks typically allocate reserves based on long-term diversification strategies rather than short-term market movements. As a result, they tend to absorb supply steadily instead of aggressively chasing prices higher.

The scale of recent buying also illustrates its limitations. China’s 15-tonne purchase represents roughly 482,000 ounces, equivalent to approximately $1.9 billion at current prices. By comparison, the SPDR Gold Shares (GLD) experienced $2.91 billion in outflows in a single trading session during March. One day of ETF liquidation outweighed an entire month of China’s purchases.

Many longer-term bullish forecasts assume central-bank buying will remain robust, with total official-sector purchases exceeding 800 tonnes in 2026. Even if that pace is achieved, however, official demand is more likely to establish a long-term price floor than trigger another powerful rally.

The broader structural arguments for gold—including reserve diversification, fiscal expansion, de-dollarization, and limited mine-supply growth—remain intact. What has weakened is private investment demand. Because marginal private buyers typically determine short-term price movements, their retreat has had a much larger impact on prices than continued sovereign accumulation.

Gold attracts fresh selling pressure on Thursday as energy-led inflation concerns revive expectations of additional Fed rate hikes.

Escalating tensions between the US and Iran underpin demand for the safe-haven US Dollar, weighing on the precious metal.

The technical outlook remains bearish, suggesting the path of least resistance is tilted toward further downside.

Gold (XAU/USD) came under renewed selling pressure during Thursday’s Asian session, retreating toward the $4,025 area near the previous day’s swing low. Although recent US inflation data pointed to easing price pressures, elevated crude oil prices continue to fuel expectations that the Federal Reserve could still raise interest rates later this year. The prospect of tighter monetary policy lends support to the US Dollar (USD) and weighs on non-yielding Gold.

Data released by the US Bureau of Labor Statistics showed that the Producer Price Index (PPI) unexpectedly fell 0.3% in June following a revised 0.6% increase in May, while annual producer inflation slowed to 5.5% from 6.0%. The report followed a sharp decline in the Consumer Price Index (CPI), reinforcing signs that inflation pressures are moderating. As a result, traders reduced expectations for an imminent Fed rate hike, sending the USD to its weakest level since June 18 and helping Gold recover on Wednesday.

However, persistent energy-driven inflation risks continue to cloud the outlook. Crude oil prices remain near one-month highs as escalating US-Iran tensions and ongoing disruptions in the Strait of Hormuz raise concerns about global energy supplies. The US launched another wave of airstrikes against Iranian military targets on Wednesday, prompting retaliatory drone and missile attacks by Iran on US-linked facilities across the region. President Donald Trump also warned that additional Iranian infrastructure could be targeted if hostilities intensify.

Meanwhile, Iran’s Islamic Revolutionary Guard Corps threatened to broaden the conflict by targeting key regional energy routes, including shipping lanes near the Bab el-Mandeb Strait through its Houthi allies in Yemen. These developments continue to support oil prices, rekindling inflation concerns and strengthening the argument for at least one 25-basis-point Fed rate hike in 2026. Consequently, USD weakness may remain limited, while the broader outlook for Gold continues to favor further downside.

Gold Daily Chart

Gold remains under bearish pressure as XAU/USD continues to trade below its 200-day Simple Moving Average (SMA) and within a well-defined descending channel. While momentum indicators show signs of stabilization, they have yet to signal a meaningful bullish reversal. The Moving Average Convergence Divergence (MACD) remains slightly positive at 9.43, while the Relative Strength Index (RSI) hovers near 40.77, suggesting weak buying interest rather than a sustained recovery.

A confirmed break and daily close below the key psychological support at $4,000 could trigger a fresh wave of selling. Such a move would bring the June year-to-date low around $3,943–$3,942 into focus. Further downside pressure could then drive Gold toward the channel’s lower boundary near $3,675.71, a major structural support level. A decisive violation of this zone would strengthen the broader bearish outlook and open the door to deeper losses.

On the upside, immediate resistance is located near $4,093.63, corresponding to the upper boundary of the descending channel. Any recovery attempt is likely to encounter renewed selling interest in this region. A sustained breakout above this barrier would improve the technical picture and pave the way for a move toward the 200-day SMA around $4,495.94, which remains the next major resistance level.

Silver remains under pressure as escalating US-Iran tensions in the Strait of Hormuz drive oil prices higher, raising concerns that the Federal Reserve may keep interest rates elevated for longer. Softer-than-expected June CPI and PPI data have helped ease near-term rate-hike concerns. Meanwhile, markets have reduced the probability of a September Fed rate increase to 44%, although the impact of recent military developments has yet to be fully reflected in asset prices.

Silver (XAG/USD) extends its decline for a second consecutive session, trading near $57.00 per troy ounce during Thursday’s Asian session. The precious metal remains under pressure as escalating tensions between the United States and Iran drive oil prices higher, raising inflation risks and reinforcing expectations that the Federal Reserve could maintain elevated interest rates for longer.

According to reports, the US Central Command (CENTCOM) launched additional operations aimed at keeping the Strait of Hormuz open, a critical route for global energy supplies. In a significant escalation, US forces reportedly targeted an oil tanker in the strategic waterway, heightening concerns over further disruptions to oil markets. Meanwhile, President Donald Trump declined to provide a timeline for potential future actions against Iranian infrastructure, adding to geopolitical uncertainty.

Despite these developments, investors are also weighing softer US inflation data. Consumer inflation eased to 3.5% year-over-year in June from 4.2% in May, coming in below the consensus forecast of 3.8%. The weaker CPI reading initially reduced expectations of an imminent Fed rate increase.

Producer inflation data reinforced the disinflationary trend. The annual PPI rate slowed to 5.5% in June from 6.0% previously, missing expectations of 6.2%, while monthly PPI fell 0.3% after a 0.6% rise in May, outperforming forecasts for a flat reading.

As a result, market expectations for a September Fed rate hike eased, with implied odds declining to roughly 44% from 50% a day earlier. However, analysts note that June inflation figures do not yet reflect the economic consequences of the renewed US-Iran conflict, leaving markets cautious about the potential inflationary effects of the latest military escalation.

The U.S. Dollar Index remains under pressure as cooling inflation signals reduce expectations of additional Fed rate hikes. However, concerns over energy-driven price pressures and rising tensions between the United States and Iran help cushion the Greenback’s downside. Market participants now await upcoming U.S. economic releases for fresh direction amid mixed fundamental signals.

The US Dollar Index (DXY), which measures the Greenback against a basket of major currencies, traded in a narrow range near 100.50 during Thursday’s Asian session, hovering close to the almost four-week low reached the previous day. While declining expectations of further Federal Reserve rate hikes continue to weigh on the dollar, concerns over energy-driven inflation and rising geopolitical tensions between the United States and Iran are helping to limit downside pressure.

Fresh economic data released on Wednesday showed that the US Producer Price Index (PPI) fell 0.3% in June, following a revised 0.6% increase in the previous month. The weaker PPI reading came after Tuesday’s softer-than-expected Consumer Price Index (CPI) report, reinforcing expectations that inflationary pressures are easing. As a result, investors have become less concerned that the Federal Reserve will need to maintain higher interest rates for an extended period, creating a bearish backdrop for the US dollar in the near term.

Geopolitical developments, however, continue to provide some support for the Greenback. Tensions between the United States and Iran have intensified significantly this week, with both countries carrying out additional military operations. On Wednesday, US forces conducted airstrikes targeting Iranian missile and drone facilities, while Tehran responded with retaliatory attacks against US-linked military assets across the region, signaling a worsening conflict.

US President Donald Trump further heightened tensions by warning that key Iranian infrastructure, including power stations and bridges, could become targets if hostilities escalate further. In addition, a US aircraft reportedly engaged an empty oil tanker attempting to breach the naval blockade around Iranian ports. At the same time, Iran has effectively restricted access through the Strait of Hormuz and threatened to disrupt shipping in the Bab el-Mandeb Strait.

These developments raise concerns about global trade flows and energy supplies, helping to keep oil prices elevated and maintaining a geopolitical risk premium in financial markets. Furthermore, market expectations for at least one additional 25-basis-point Federal Reserve rate hike remain intact, discouraging traders from aggressively selling the dollar. Investors are now awaiting upcoming US economic data releases for clearer direction on monetary policy and the next move in the currency markets.

Gold stays under selling pressure as a firmer US Dollar and higher oil prices strengthen expectations of a hawkish Federal Reserve.

The upcoming US CPI report and the Fed Chair’s testimony are expected to provide the next key catalyst for gold prices.

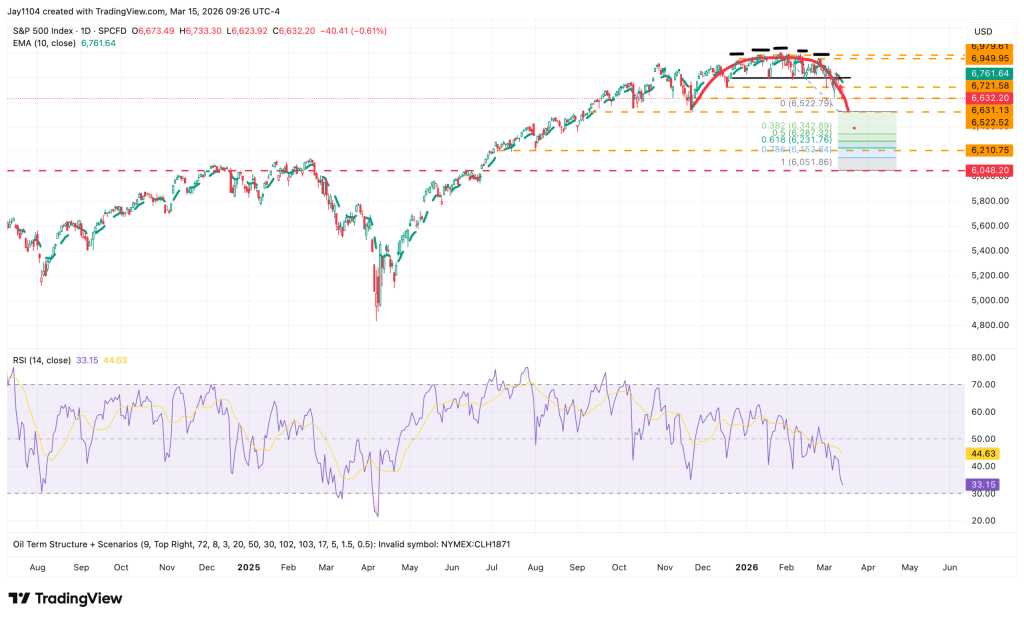

Mounting bearish momentum leaves gold vulnerable to a break below the $4,000 mark.

Gold and silver came under heavy selling pressure during the first half of Monday’s trading session. Gold extended last week’s weakness after failing to build on the modest rebound seen the previous week. The broader trend remains bearish. Although the precious metal is still marginally positive for the month, it plunged more than 11% in June, marking its fourth straight monthly decline.

As a result, downside risks continue to dominate, with gold increasingly vulnerable to a break below the key $4,000 support level in the near term.

Rising Oil Prices Keep Pressure on Gold

Renewed geopolitical tensions in the Middle East have driven crude oil prices higher at the start of the week, weighing on global equity markets. While geopolitical uncertainty would typically increase demand for safe-haven assets such as gold, the metal has increasingly moved alongside US equities in recent years, reflecting its growing sensitivity to broader market sentiment rather than its traditional defensive role.

If oil prices continue to climb, inflation concerns are likely to intensify, reinforcing expectations that the Federal Reserve will maintain a restrictive monetary policy. Such a scenario would further weaken gold’s near-term outlook.

Stronger US Dollar Adds to Headwinds

Gold is also facing pressure from a strengthening US Dollar. With the Fed emphasizing its commitment to keeping inflation under control, another surge in energy prices could strengthen expectations that US interest rates will remain elevated for longer. Even if upcoming economic data shows some moderation, persistently high energy costs would likely discourage policymakers from shifting toward a more dovish stance.

This backdrop has helped the US Dollar regain momentum, particularly against currencies such as the euro and Japanese yen, whose economies are more vulnerable to rising energy import costs.

Focus Turns to CPI and Fed Chair Testimony

As oil and natural gas prices remain elevated, markets have become less willing to dismiss the possibility of additional Fed tightening, providing further support for the Greenback while reducing gold’s appeal.

Investor attention now shifts to a busy US economic calendar. Tuesday’s Consumer Price Index (CPI) report is expected to show softer monthly headline inflation, but firm energy costs and stubborn core inflation—still around 2.8% to 2.9% year-over-year—suggest the Fed could still consider another rate increase before year-end.

Markets will also closely monitor Fed Chair Kevin Warsh’s two-day congressional testimony for fresh guidance on the policy outlook. Additional releases, including producer prices, import prices, and retail sales, could further influence market expectations.

Gold Technical Outlook

Technically, gold has repeatedly failed to reclaim the $4,100 level, remaining below both a descending trendline and the 21-day Exponential Moving Average (EMA). The metal is now approaching the critical $4,000 support zone ahead of the US CPI release.

A decisive daily close below $4,000 would likely confirm a bearish breakdown, opening the door toward $3,900, with $3,800 emerging as the next major downside target.

On the upside, initial resistance is located near $4,136, followed by $4,200 and then $4,275.

With energy prices remaining elevated and the US economy showing limited signs of slowing enough to ease inflation concerns, the broader macro backdrop continues to favor the US Dollar. Consequently, non-yielding and low-yielding assets—including gold, the Japanese yen, and the Swiss franc—remain exposed to further downside pressure.

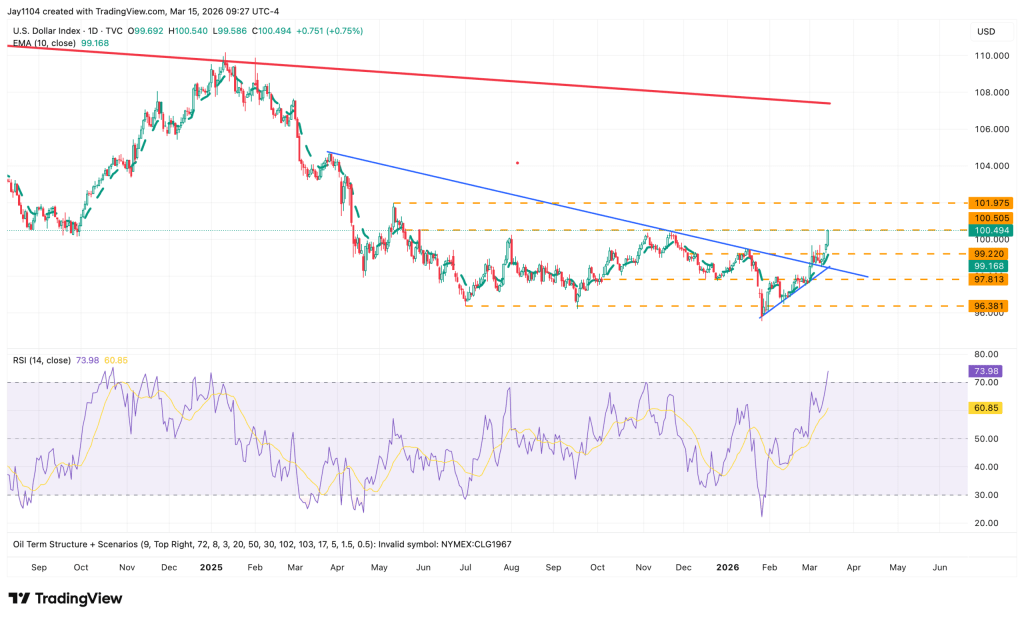

The US Dollar Index trades lower against its major counterparts as markets scale back expectations for a more hawkish Federal Reserve.

US inflation softened in June, with both headline and core CPI easing to 3.5% and 2.6% year-over-year, respectively.

Fed Chair Kevin Warsh reiterated that the central bank remains firmly committed to bringing inflation under control, emphasizing zero tolerance for persistently elevated price pressures.

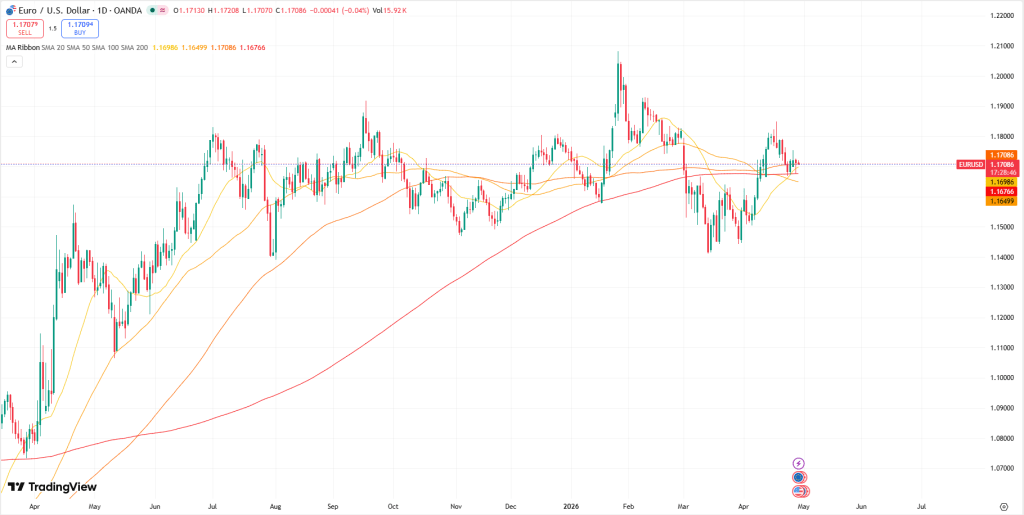

The US Dollar (USD) weakens against its major peers as investors scale back expectations for further Federal Reserve (Fed) rate hikes this year after softer-than-anticipated US inflation data for June. The US Dollar Index (DXY), which tracks the Greenback against a basket of six major currencies, is trading around 100.80, down roughly 0.12% on the day.

Data released by the US Bureau of Labor Statistics (BLS) on Tuesday showed headline Consumer Price Index (CPI) inflation eased to 3.5% year-over-year in June from 4.2% in May, coming in below the market forecast of 3.8%. Meanwhile, core CPI, which strips out food and energy prices, rose 2.6% annually, undershooting both the 2.8% consensus estimate and May’s 2.9% reading.

Following the inflation report, market expectations for another Fed rate increase this month dropped sharply. According to the CME FedWatch Tool, the probability of a rate hike has fallen to 16.6%, down from 41.7% a day earlier.

Despite the softer inflation figures, Fed Chair Kevin Warsh maintained a firm stance on price stability during his congressional testimony on Tuesday, stressing that policymakers have “no tolerance for persistently elevated inflation.” He added that if monetary policy remains on the right path, the inflation surge seen over the past five years will eventually become a thing of the past.

Market participants now await the release of June’s US Producer Price Index (PPI), scheduled for 12:30 GMT, for additional insight into wholesale inflation trends and the Fed’s policy outlook.

Meanwhile, rising tensions between the United States and Iran could continue to support demand for the Greenback, as investors seek the safety of the world’s reserve currency amid growing geopolitical uncertainty.

Gold drifts lower as the market’s initial response to Tuesday’s softer-than-expected US inflation data loses momentum. Persistently high oil prices continue to fuel expectations of at least one additional Federal Reserve rate hike, weighing on the non-yielding metal. Meanwhile, escalating tensions between the US and Iran could boost demand for the safe-haven US Dollar, adding further downside pressure to XAU/USD.

Gold (XAU/USD) comes under renewed selling pressure after failing to sustain gains above the $4,100 level in the previous session, though it continues to hold above the key $4,000 psychological support during Wednesday’s Asian trading hours. While softer-than-expected US Consumer Price Index (CPI) data initially weighed on the US Dollar (USD), persistent concerns over energy-driven inflation continue to dominate sentiment. Escalating tensions between the US and Iran, along with the closure of the Strait of Hormuz, have kept crude oil prices elevated, reinforcing inflation fears. Meanwhile, Federal Reserve (Fed) Chair Kevin Warsh reaffirmed the central bank’s commitment to restoring price stability during his first congressional testimony, signaling that another rate hike remains possible before year-end. The hawkish tone largely offsets the impact of a weaker USD and limits demand for the non-yielding precious metal.

Data released by the US Bureau of Labor Statistics showed headline CPI fell by 0.4% in June, marking the steepest monthly decline since April 2020 and falling short of expectations for a 0.1% decrease. Core CPI, which excludes food and energy prices, was unchanged during the month, well below the expected 0.3% increase. On an annual basis, headline inflation eased to 3.5%, while core inflation slowed to 2.6%, both undershooting market forecasts. The softer inflation figures briefly dragged the USD to its weakest level in nearly four weeks as traders pared back expectations for additional Fed tightening. However, the Greenback quickly recovered after Warsh emphasized that the Fed remains firmly committed to combating inflation and highlighted the resilience of the US economy.

At the same time, crude oil prices have climbed to their highest level in nearly a month, increasing concerns that higher energy costs could reignite inflationary pressures and justify further monetary tightening. Reflecting this outlook, the CME FedWatch Tool indicates that markets continue to price in the possibility of one additional Fed rate hike, potentially in September or December. Geopolitical tensions also continue to underpin the USD’s safe-haven appeal. The US carried out another wave of airstrikes on Iranian targets, while Tehran responded by attacking US military facilities across Gulf nations. In addition, President Donald Trump warned that Washington could target Iranian bridges and power infrastructure if Tehran refuses to resume nuclear negotiations.

Overall, the prevailing fundamental backdrop remains supportive of the US Dollar and suggests that downside risks for Gold persist. Investors now await the release of the US Producer Price Index (PPI) and the second day of Fed Chair Kevin Warsh’s congressional testimony for fresh clues on the interest rate outlook. Meanwhile, any new developments in the Middle East conflict are likely to remain a key driver of market sentiment and could trigger heightened volatility across financial markets, particularly in Gold.

Technical Analysis

From a technical perspective, Gold continues to trade within a descending parallel channel and remains firmly below the 200-day Simple Moving Average (SMA), indicating that the broader trend remains tilted to the downside despite the recent recovery. The Moving Average Convergence Divergence (MACD) has crossed into positive territory and continues to improve, signaling a modest pickup in bullish momentum, while the Relative Strength Index (RSI) hovers near the neutral 40.80 mark, suggesting limited buying conviction.

The upper boundary of the descending channel, located around $4,140.69, represents the first significant resistance level. A sustained break above this barrier would be required to weaken the prevailing bearish outlook and open the door for additional gains. On the downside, immediate support is seen near the channel’s lower boundary at $3,718.03. A decisive rebound from this level would be needed to indicate that bearish momentum is fading and that sellers are beginning to lose control of the short-term trend.

Silver prices declined as escalating tensions in the Middle East drove oil prices higher, fueling inflation concerns and reinforcing expectations that the Federal Reserve will keep interest rates elevated for longer.

According to the CME FedWatch Tool, markets now assign a 51% probability to a Fed rate hike in September, compared with a 23% chance that policymakers leave rates unchanged.

Meanwhile, U.S. President Donald Trump reinstated a blockade targeting Iranian vessels and introduced a 20% transit fee on non-Iranian ships using the Strait of Hormuz under U.S. protection.

Silver prices (XAG/USD) extended their decline for a third straight session, trading near $57.60 per troy ounce during Tuesday’s Asian session. The non-yielding precious metal remained under pressure as intensifying tensions in the Middle East pushed crude oil prices higher, raising concerns that stronger energy-driven inflation could keep the Federal Reserve on a restrictive policy path for longer.

Rate expectations have turned increasingly hawkish. According to the CME FedWatch Tool, traders now see a 51% chance of a Fed rate increase in September, while the probability of policymakers leaving rates unchanged has dropped to 23%.

Geopolitical risks escalated after US President Donald Trump reinstated a naval blockade targeting Iranian vessels and ships linked to Iran passing through the Strait of Hormuz. He also announced a 20% transit fee on all other commercial cargo vessels using the strategic shipping route.

Investors are now focused on two key US events scheduled for Tuesday. The June Consumer Price Index (CPI) report is expected to show headline inflation falling 0.1% month-over-month, while core CPI is forecast to remain firm with a 0.3% monthly increase, highlighting persistent underlying price pressures.

Attention will also turn to Federal Reserve Chair Kevin Warsh, who is set to testify before Congress. Market participants will closely scrutinize his remarks for clues on whether Fed officials share the market’s increasingly hawkish outlook and are prepared to keep monetary policy tighter for longer.

Gold extends its losses, falling more than 1% toward the $4,050 level during Monday’s Asian session as escalating tensions between the United States and Iran boost demand for the safe-haven US Dollar. At the same time, concerns that higher Crude Oil prices could fuel inflation are reinforcing expectations of a Federal Reserve rate hike in 2026, strengthening the Greenback further and adding pressure on the non-yielding precious metal.

Fundamental Analysis

Gold remains under heavy selling pressure at the beginning of the week as the US Dollar strengthens, supported by a sharp rebound in Oil prices and renewed inflation concerns that reinforce expectations of a hawkish stance from the Federal Reserve.

The move follows a fresh escalation of tensions in the Middle East after the United States launched additional strikes against Iran on Sunday. In response, Iran reportedly targeted US facilities across Gulf states and reiterated the closure of the strategically important Strait of Hormuz.

Rising inflation worries have also contributed to Gold’s weakness after the Fed highlighted increasing price pressures in its semi-annual Monetary Policy Report released on Friday. The central bank noted that inflation accelerated further this spring, driven by the combined effects of tariffs, higher energy costs linked to the conflict, and continued investment in artificial intelligence infrastructure.

Market participants remain cautious ahead of Tuesday’s release of the US Consumer Price Index (CPI) report and Federal Reserve Chair Kevin Warsh’s first semi-annual testimony before Congress.

For now, traders are expected to keep a close eye on developments surrounding the US-Iran conflict and fluctuations in Oil prices for fresh market direction. From a technical perspective, the bearish outlook for Gold remains intact, with downside risks continuing to dominate the near-term picture.

Technical Analysis

On the daily timeframe, Gold (XAU/USD) is trading near $4,069, maintaining a bearish short-term bias as it remains below both the 21-day SMA at $4,128 and the 50-day SMA at $4,344. The longer-term technical outlook also continues to favor sellers, with the 200-day SMA at $4,495 and the 100-day SMA at $4,583 positioned well above current market levels. Meanwhile, the RSI near 41 suggests bearish momentum is still present, although selling pressure appears to be moderating rather than reaching oversold territory.

On the upside, the first resistance zone is located around the 21-day SMA at $4,128. A sustained move higher could then target the 50-day SMA near $4,344, followed by the 200-day SMA around $4,495 and the 100-day SMA near $4,583. With no significant moving-average support levels immediately beneath the current price, any rebound attempt remains fragile while Gold continues to trade below this cluster of resistance levels. Unless buyers can regain control above the 21-day SMA, the broader risk profile remains tilted toward further downside pressure.

The US Dollar Index (DXY) moved higher as investors sought the safety of the US dollar amid escalating geopolitical tensions in the Middle East. Tehran has rejected further negotiations, insisting that Washington first fulfill earlier commitments regarding transit security and Iranian oil exports. Meanwhile, market participants continue to anticipate one final interest-rate hike from the Federal Reserve before the end of the year, providing additional support for the greenback.

The US Dollar Index (DXY), which tracks the US Dollar against a basket of six major currencies, extended its gains for a second consecutive session, hovering around 101.10 during Monday’s Asian trading hours.

The Greenback continued to attract safe-haven flows as geopolitical tensions in the Middle East intensified. According to Bloomberg, the US Central Command (CENTCOM) carried out additional strikes on Sunday aimed at reducing Iran’s ability to threaten civilian vessels transiting the strategic waterway.

Reuters reported that US forces have struck more than 300 Iranian targets over the past three days, including approximately 140 targets on Saturday alone, while Washington and Tehran offered conflicting assessments regarding the status of maritime traffic through the strait. The latest escalation has further diminished prospects for diplomatic progress, with Tehran insisting that the US must first honor previous commitments related to shipping security and the normalization of Iranian oil exports before negotiations can move forward.

The US Dollar also found support from rising concerns that the intensifying US-Iran conflict could drive energy prices higher, fueling inflationary pressures and potentially keeping Federal Reserve policy restrictive for longer. Investors are now focused on Tuesday’s release of the US Consumer Price Index (CPI) report for fresh signals on the Fed’s policy path. Economists expect headline CPI to decline by 0.1% month-over-month in June, while core CPI is forecast to increase by 0.3%.

Market participants continue to price in one additional Federal Reserve rate hike before year-end. Attention will also turn to Fed Chair Kevin Warsh, who is scheduled to make his first official appearance before Congress on Tuesday, with traders looking for further guidance on the outlook for monetary policy.

The US Dollar Index remains under pressure after the FOMC Minutes failed to deliver a more hawkish signal. Still, expectations for a Fed rate hike later this year and renewed tensions between the US and Iran are helping to limit downside momentum.

The US Dollar Index (DXY), which measures the Greenback against a basket of major currencies, remains under mild selling pressure for a second consecutive day. However, the decline has been limited, with the index trading within Wednesday’s range during Thursday’s Asian session and hovering just below the 101.00 level, down roughly 0.1% on the day.

Demand for the US Dollar has softened following the release of the latest FOMC Minutes, which failed to deliver a significantly more hawkish policy signal. The minutes from the June 16–17 meeting showed policymakers remained divided on the future path of interest rates, with many officials suggesting the federal funds rate could finish the year at or slightly below its current level.

Despite this, Federal Reserve officials continued to highlight persistent upside inflation risks, indicating that additional policy tightening may still be necessary to bring inflation back toward the 2% target. Markets continue to price in approximately a 70% probability of a 25-basis-point rate increase in September. At the same time, renewed geopolitical tensions between the US and Iran have provided support for the Greenback by reinforcing safe-haven demand and fueling expectations of higher inflation.

The latest escalation in the Middle East followed fresh US military strikes against Iran in response to attacks on commercial shipping in the Strait of Hormuz. Tehran retaliated with ongoing attacks targeting US military facilities and assets in Bahrain and Kuwait. Further adding to uncertainty, US President Donald Trump stated on Wednesday that the memorandum of understanding intended to ease regional tensions had effectively collapsed. Against this backdrop, traders are reluctant to initiate aggressive bearish positions on the Dollar ahead of the release of US Weekly Jobless Claims data, which could offer fresh direction for the market.

Gold remains under pressure as buyers stay cautious despite a weaker US Dollar. Escalating US-Iran tensions, persistent inflation concerns, and expectations of further Fed tightening continue to support the greenback, while the technical outlook suggests bullion could face additional downside.

Gold (XAU/USD) extends its decline for a fourth consecutive session on Thursday, hovering near the one-week low around $4,020 reached the previous day. Renewed conflict between the United States and Iran has reignited inflation concerns and strengthened expectations that the Federal Reserve could resume tightening policy in 2026, weighing on the non-yielding precious metal during Asian trading. However, a softer US Dollar, pressured by the absence of a strongly hawkish signal in the latest FOMC Minutes, is helping to cushion gold’s losses.

The minutes from the Federal Reserve’s June 16–17 meeting, released Wednesday, showed policymakers remain divided on the future path of interest rates. Several officials suggested that the federal funds rate could end the year at or slightly below its current level. Combined with last week’s weaker-than-expected US Nonfarm Payrolls report, the minutes did little to significantly shift market expectations. Nonetheless, Fed officials emphasized that inflation risks remain skewed to the upside and acknowledged that further policy tightening may be necessary to bring inflation back toward the 2% target.

Market participants continue to assign roughly a 70% probability to a Fed rate hike in September. That outlook, together with escalating tensions in the Middle East, is preventing a deeper decline in the US Dollar. The latest developments saw US forces launch additional strikes against Iran following attacks on commercial vessels in the Strait of Hormuz. Tehran responded with continued strikes on US military assets in Bahrain and Kuwait, while President Donald Trump declared on Wednesday that the ceasefire with Iran had effectively ended.

Against this backdrop, the broader fundamental picture remains supportive of the US Dollar and suggests that any rebound in gold could face selling pressure. Investors are now awaiting US Weekly Initial Jobless Claims data and remarks from key Federal Reserve officials for fresh policy clues. Even so, market attention is likely to remain focused on developments in the Middle East, which could continue to drive volatility across global markets and create significant trading opportunities in gold.

Gold Daily Chart

Gold may continue to struggle in attracting significant buying interest as the technical outlook remains tilted to the downside.

From a chart perspective, XAU/USD retains a bearish near-term structure, trading below its 200-day Simple Moving Average (SMA) and remaining confined within a descending channel. Although the Moving Average Convergence Divergence (MACD) indicator has crossed into positive territory and the Relative Strength Index (RSI) has improved to 40.26 from previously oversold levels, momentum remains relatively weak. As a result, any recovery attempt could encounter stiff resistance near the upper boundary of the channel around $4,247.94.

For sentiment to improve meaningfully, gold would need to break decisively above the channel resistance, with the next major hurdle located at the 200-day SMA near $4,492.08. On the downside, immediate support is seen at the lower edge of the descending channel around $3,811.93. A move toward that area could attract renewed buying interest from longer-term bulls seeking to preserve the broader upward trend if the current corrective phase deepens further.

Silver is poised for a strong rebound amid a softer Fed outlook, easing inflation concerns, and weaker oil prices.

Silver gains momentum as signs of a slowing US labor market prompt investors to reassess the path of interest rates.

According to the CME FedWatch tool, the probability of a September rate hike fell to 52% from 66% following the latest data release.

Silver prices extended gains for a fourth straight session on Friday, with XAG/USD trading near $62.60 per troy ounce during Asian trading hours. A softer inflation outlook, weaker oil prices, and a less aggressive Federal Reserve are providing strong support for the non-yielding metal’s recovery.

Silver is attracting renewed buying interest as signs of a slowing US labor market prompt investors to sharply reassess the outlook for interest rates. The shift in sentiment followed Thursday’s June Nonfarm Payrolls (NFP) report, which showed the US economy added only 57,000 jobs, well below expectations of 110,000. Although the unemployment rate unexpectedly edged down to 4.2% from 4.3% in May, the weak hiring figures reinforced concerns about broader economic cooling.

In response, traders pared back expectations for tighter monetary policy. Data from the CME FedWatch tool showed the probability of a September rate hike falling to 52%, compared with 66% before the jobs report.

Additional support came from recent comments by Federal Reserve Chair Kevin Warsh at the ECB Sintra Conference, where he reiterated the Fed’s commitment to its 2% inflation target while noting that inflation pressures and expectations have eased in recent weeks.

Silver is also benefiting from declining energy prices, which are helping reduce inflationary pressures. Crude oil prices have weakened as shipping activity through the Strait of Hormuz continues to normalize following progress in US-Iran diplomatic negotiations in Doha. The easing geopolitical tensions have reduced the risk premium that had previously supported energy markets.

U.S. benchmark crude oil prices dropped below $70 per barrel on Wednesday, hitting their lowest point since the conflict with Iran erupted on Feb. 28. The decline is expected to reduce pressure on headline inflation in the months ahead. However, the key issue now is whether the bond market will also adjust by pricing in lower inflation expectations, as uncertainty surrounding the Federal Reserve’s interest-rate path remains unresolved.

Oil prices were pressured by a preliminary agreement aimed at ending the conflict with Iran, while shipping activity through the Strait of Hormuz has started to recover gradually. Even so, energy transport volumes are still significantly below levels seen before the war. “What shippers are looking for is consistency over days and weeks,” said Matthew Wright, a freight analyst at Kpler, a firm specializing in global shipping analysis.

The oil market is currently reflecting expectations of continued progress toward stability and a gradual recovery in global energy exports over the coming weeks and months. “Traders are pricing in a return to normality,” said Francis Osborne, head of oil analysis at Argus Media, a firm that monitors global oil prices. “They are not taking into account the risks further down the road, which still remain very real.”

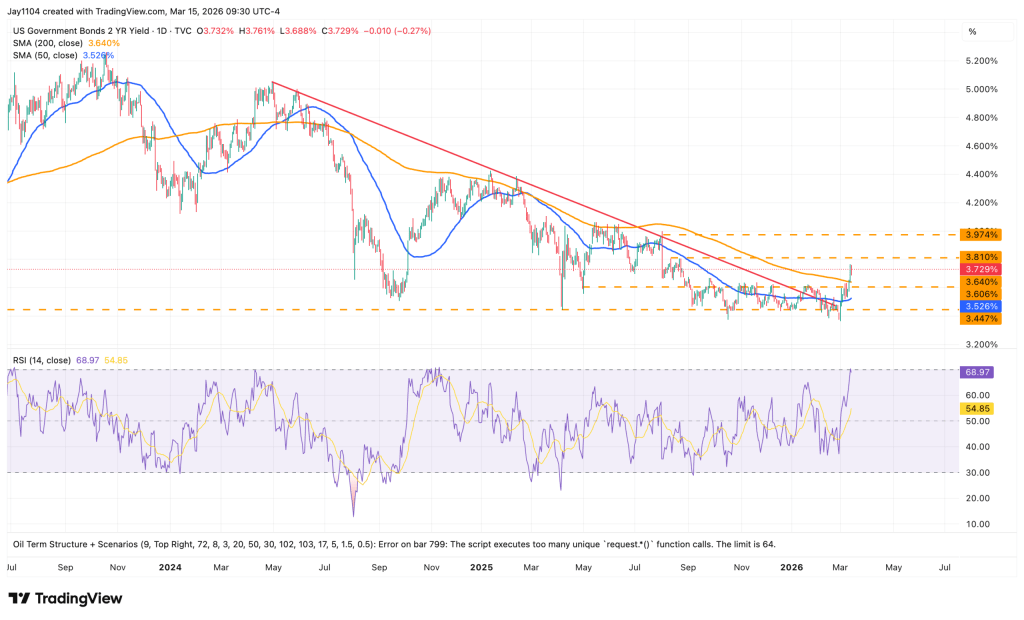

Despite ongoing uncertainty surrounding the Middle East, U.S. Treasury yields have started to retreat, though the decline has been uneven across maturities. The 30-year Treasury yield — typically the most sensitive to inflation expectations — dropped sharply yesterday to 4.84%, its lowest level in several months. Meanwhile, the benchmark 10-year yield also moved lower, reversing much of the increase seen over the past month.

One key exception is the policy-sensitive 2-year Treasury yield. Although it edged lower yesterday, it remained near 4.16%, close to the recent high reached only days earlier. This suggests that investors are not yet fully convinced that inflation pressures have disappeared or that further Federal Reserve rate hikes are off the table.

Torsten Slok argues that lower oil prices could ultimately become inflationary, writing:

“The narrative in markets is changing from ‘lower oil prices mean lower inflation’ to ‘lower oil prices mean more demand in an already overheating economy, which means higher inflation.’ Driven by the strong April CPI, hot May non-farm payrolls, and a hawkish Fed, the market narrative now suggests that the reopening of the Strait of Hormuz will further overheat the economy, forcing the Fed to raise interest rates soon.”

Whether Slok’s view proves correct will take time to assess, as geopolitical tensions and broader macroeconomic uncertainty continue to cloud the outlook. In the near term, however, inflation pressures are still expected to ease somewhat.

The Federal Reserve Bank of Cleveland’s inflation nowcast points to a modest slowdown in year-over-year CPI after several months of elevated readings. Meanwhile, Core CPI — which has remained relatively stable throughout the conflict, rising only slightly — is projected to increase 2.9% in the latest monthly update compared with a year earlier.

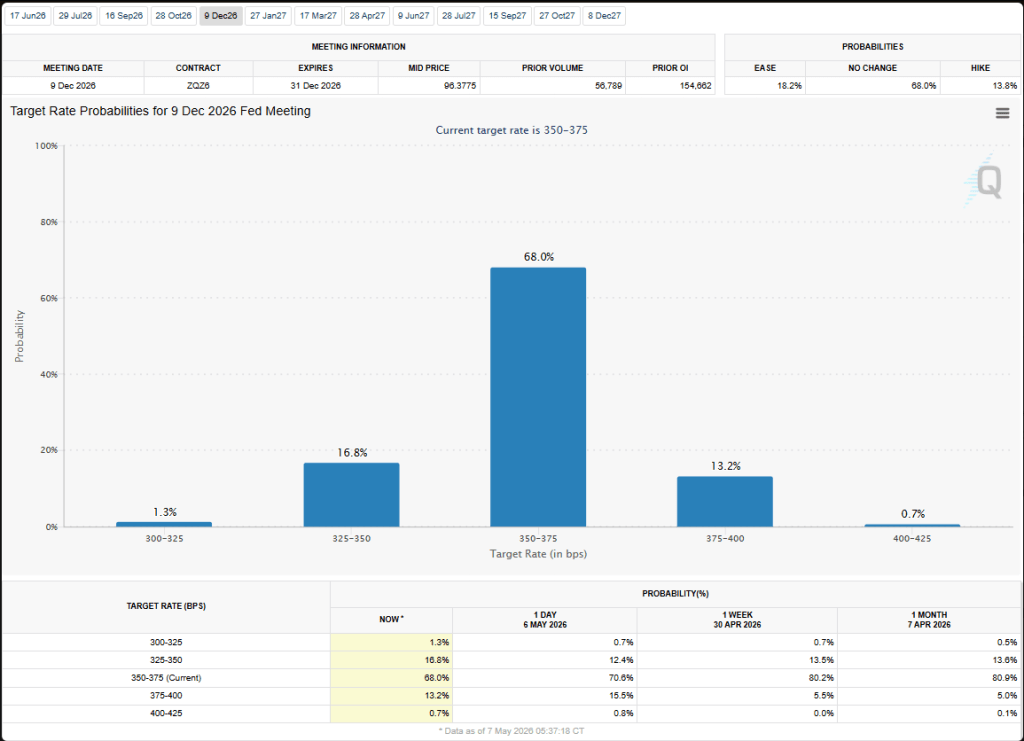

Fed funds futures markets are now assigning higher odds of near-term tightening, pricing in a 34% probability of a 25-basis-point rate hike at the next FOMC meeting on July 29, with expectations rising to around 67% in favor of further tightening by September.

Morningstar expects any near-term inflation persistence to gradually fade over time. The firm notes: “We expect inflation to fall in the coming years. Receding energy prices will be reflected in a negative impulse to inflation in 2027. The tariff impact should also cease going forward. Moreover, wage growth has slowed considerably, which should help push services inflation back to normal. Housing inflation also continues to trend down.”

Still, while the longer-term outlook points toward easing inflationary pressure, that horizon remains distant. In the immediate term, markets are taking comfort in signs of cooling prices, though uncertainty around the Federal Reserve’s policy path suggests that current stability may not last.

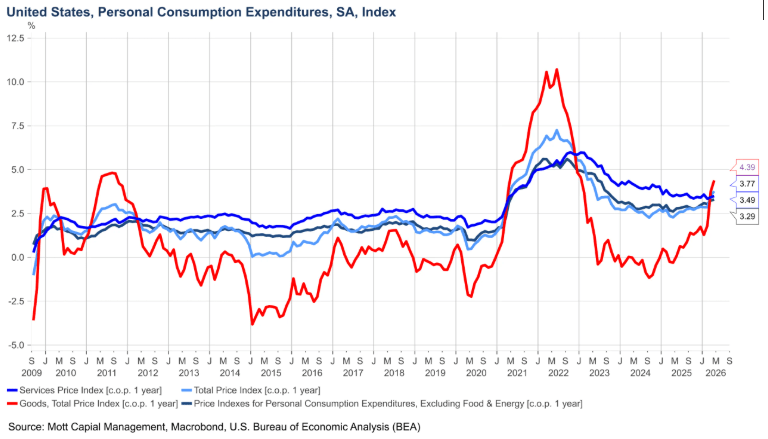

The United States Dollar Index remains supported as expectations for a Federal Reserve rate hike continue to build. Markets are now pricing in a 63.4% chance of a rate increase in September, according to the CME Group FedWatch tool. Meanwhile, US PCE inflation accelerated to 4.1% in May amid oil supply concerns linked to tensions in the Middle East, reinforcing expectations that the Fed could keep tightening policy.

The US Dollar Index (DXY), which tracks the performance of the US Dollar (USD) against a basket of six major currencies, recovers some of its previous session losses and trades near 101.50 during Friday’s Asian session. Investors now await the release of the Michigan Consumer Sentiment Index later in the day for fresh market direction.

The Greenback remains supported by increasing expectations that the Federal Reserve (Fed) could raise interest rates again. According to the CME FedWatch tool, markets are currently pricing in a 63.4% chance of a rate hike at the Fed’s September 15–16 meeting.

The hawkish outlook follows stronger inflation data, with the headline Personal Consumption Expenditures (PCE) Price Index rising to 4.1% year-over-year in May from 3.3% previously. The jump marks the first time in three years that headline PCE inflation has moved above the 4.0% threshold, largely driven by higher energy prices linked to tensions in the Middle East, keeping the possibility of additional Fed tightening alive.

Meanwhile, the core PCE Price Index, the Fed’s preferred measure of underlying inflation, climbed to 3.4% annually from 3.3% in April, marking the strongest core inflation reading since October 2023.

BMO Chief US Economist Scott Anderson stated that elevated PCE inflation is likely to keep the Fed cautious, with further rate hikes remaining a possibility. He added that persistent service-sector inflation may not ease quickly even if energy prices decline, suggesting continued policy debates between Fed hawks and doves.

The Australian Dollar remains under pressure versus the US Dollar as expectations for further Federal Reserve rate hikes stay firm.

Investors are now focusing on the US PCE Inflation data for fresh signals regarding the Fed’s future monetary policy direction.

Meanwhile, Australia’s labor market showed resilience, with employers adding 40.3K new jobs in May, surpassing market forecasts of 25K.

The AUD/USD pair edges slightly lower to around 0.6890 during Thursday’s European session as the Australian Dollar remains under mild pressure against the US Dollar. The Greenback continues to stay supported by expectations that the Federal Reserve’s next policy move could be another rate hike.

The US Dollar Index (DXY), which measures the USD against six major currencies, trades near 101.55 at the time of writing, remaining close to Wednesday’s more-than-one-year peak of 101.80.

Data from the CME FedWatch Tool shows markets are pricing in nearly an 82% probability of at least one Fed rate increase this year.

Traders are now turning their attention to the US Personal Consumption Expenditures (PCE) Price Index for May, scheduled for release at 12:30 GMT, as the report could provide fresh insight into the Fed’s future interest-rate path.

Meanwhile, Australia’s May labor market figures exceeded expectations. The Australian Bureau of Statistics reported that employers added 40.3K jobs during the month, well above forecasts of 25K. This follows April’s revised decline of 40.7K jobs, compared with the previously reported 18.6K drop. The unemployment rate also eased to 4.4% from 4.5%, matching market expectations.

Technical Analysis

AUD/USD trades near 0.6890 and continues to show a bearish short-term outlook, with the pair remaining below the 20-day Exponential Moving Average (EMA) at 0.7025. Price action has continued to drift away from the key trend indicator, while the Relative Strength Index (RSI) stands at 26.6 in oversold territory, suggesting that bearish momentum remains strong even though the recent decline may be overstretched.

On the upside, the first major resistance is seen around the 20-day EMA near 0.7025. A recovery above this level would help reduce immediate downside pressure.

On the downside, key support is located at the March 30 low of 0.6833. A break beneath this area could open the door for a deeper decline toward the January 7 high near 0.6766.

United States Dollar Index remains close to 13-month highs

The United States Dollar Index stays near a 13-month peak around 101.13, supported by hawkish expectations surrounding the Federal Reserve policy outlook. Meanwhile, US Vice President JD Vance stated that negotiations have achieved “great progress,” despite lingering tensions behind the scenes.

The United States Dollar Index (DXY), which tracks the US Dollar against six major currencies, traded steadily near the 101.00 mark during Tuesday’s Asian session after posting modest gains in the previous session.

The index continues to hover close to its 13-month high of 101.13, reached on June 19, as markets maintain a hawkish view on the Federal Reserve policy outlook. The Fed kept interest rates unchanged at 3.50%–3.75% during its June meeting.

Still, updated economic forecasts and remarks from Kevin Warsh, who chaired his first Fed meeting, were viewed as more hawkish than expected. Following the announcement, futures markets fully priced in a 25-basis-point rate hike for September, while also assigning a small probability to a potential increase as early as next month.

Despite the Dollar’s resilience, easing geopolitical tensions may limit further upside. Ongoing peace discussions between the US and Iran have improved market sentiment and reduced inflation concerns. According to CNBC, US Vice President JD Vance said negotiations had made “great progress,” although some tensions remain unresolved.

On Monday, Vance also stated that Iran had agreed to allow inspectors from the International Atomic Energy Agency back into the country. Iranian Foreign Minister Abbas Araghchi echoed the positive tone, noting that the Switzerland talks had produced “major progress.”

Gold holds steady near $4,200 as US–Iran peace progress offset by Fed hawkish stance

Gold prices remain flat near $4,190 during early Asian trading on Tuesday. Progress in US–Iran peace negotiations may pressure the precious metal, while expectations of a Fed rate hike later this year grow after the new Fed Chair struck a hawkish tone.

Gold prices remained steady near $4,190 during Tuesday’s early Asian session as traders monitored ongoing developments surrounding the US–Iran peace negotiations.

US Vice President JD Vance said talks between Washington and Tehran had made “great progress,” despite recent tensions. He noted that negotiations in Bürgenstock were continuing and that Iran had agreed to allow inspectors from the International Atomic Energy Agency back into the country.

However, discussions became strained after Iran announced the closure of the Strait of Hormuz in response to Israeli strikes on Lebanon, arguing the attacks violated the ceasefire agreement.

According to Saxo Bank analyst Ole Hansen, energy prices remain a major short-term driver for precious metals. He added that the uneven progress in US–Iran talks could pressure oil prices while supporting demand for gold.

Meanwhile, expectations for tighter US monetary policy also weighed on bullion. Markets increasingly anticipate a Federal Reserve rate hike later this year after new Fed Chair Kevin Warsh adopted a hawkish stance on inflation during his first policy meeting. Higher interest rates tend to reduce gold’s appeal since the metal does not offer yields.

Traders are now pricing in nearly an 89% probability of a Fed rate hike in December, up sharply from 61% before last week’s FOMC meeting, according to the CME FedWatch Tool.

The peace dividend is real, but the bigger story for oil may be the delayed release of Gulf crude into an Asian market that is already better supplied than it was just a few months ago.

Falling oil prices provide support for bonds and a select group of equity leaders, but they do not automatically eliminate the inflation risks that have recently pushed the Fed toward a more hawkish stance.

The 24–48 hour rule after a central-bank surprise remains relevant: betting against the Fed too quickly can be costly, particularly when the US dollar is gaining momentum.

The more compelling opportunity may emerge after the initial dollar rally fades, when gold and major currencies reveal whether weaker energy prices are starting to undermine the Fed’s inflation narrative.

As option-related market support fades, investors could face greater volatility just as the peace trade, the oil-overhang trade, and the Fed trade begin pulling markets in different directions.

The Fed’s Hard Edge

Wall Street delivered the kind of rebound that appears straightforward at first glance but becomes far more complex beneath the surface. Equities advanced, bonds recovered, oil prices retreated, and semiconductor stocks surged back toward record highs after the interim US-Iran agreement offered markets their clearest signal yet that the Strait of Hormuz could reopen. An inflation risk that had dominated macro discussions suddenly looked less like an imminent shock and more like a pressure point beginning to ease.

That shift matters. Lower crude prices have given parts of the equity market much-needed breathing room following the Fed’s latest message. They have also offered support to longer-duration assets after policymakers signaled they are prepared to respond forcefully should inflation pressures re-emerge. While cheaper energy does not solve every macro challenge, it removes one of the most visible drivers of inflation expectations.

The market is correctly focusing on oil. Reopening Hormuz does more than restore disrupted supply—it unlocks a significant backlog of Gulf crude destined for Asia. More than 60 million barrels reportedly remain stored on tankers in the region, waiting for transport routes to normalize. Once confidence returns and those cargoes begin moving, Asian buyers may face not only additional supply but a delayed surge of barrels entering a market that has already adapted by securing alternative shipments from West Africa, the Americas, and other exporters.

As a result, the oil market may be transitioning rapidly from a scarcity narrative to an oversupply narrative. The immediate concern was whether crude could leave the Gulf. The next challenge is how quickly delayed cargoes arrive in a market that is already relatively well stocked. This dynamic suggests the decline in oil prices may have further room to run, as the reopening of Hormuz removes both the geopolitical risk premium and exposes the inventory buildup created during the disruption.

That is why developments in the Dubai crude market are attracting attention. The shift of Dubai prompt time spreads into contango is more than a technical detail—it may be an early sign that the last remnants of the geopolitical premium are fading. Contango indicates that immediate barrels are becoming less valuable relative to future supply, suggesting traders are beginning to worry less about securing cargoes and more about finding storage for them. This subtle change in market structure often signals a transition from supply anxiety toward concerns about excess inventory.

For Asian refiners, the market is entering a new phase. The original shock came from the loss of Gulf crude supplies. The next challenge may be the opposite: a surge of delayed Gulf barrels arriving simultaneously into a region that has already secured alternative supplies. For months, oil traders focused on the closure of the gate; now they must assess the growing traffic jam waiting on the other side, particularly around Singapore’s storage and trading hub.

Meanwhile, equity markets have reverted to a familiar script. The Nasdaq is outperforming, semiconductor stocks are leading the advance, and renewed optimism surrounding domestic chip production has added fresh momentum to the broader AI and capital-expenditure story. Retail stocks remain resilient, energy shares have softened alongside crude prices, and investors are once again embracing growth-oriented sectors as concerns over energy-driven inflation begin to fade.

However, the post-Fed recovery remains narrow beneath the surface. While technology and semiconductors have resumed leadership, broader market participation remains limited. Cross-asset signals from currencies, rates, and volatility markets suggest caution rather than a full-fledged risk-on environment. The generals may be charging ahead, but the rest of the market has yet to follow, making the rally appear selective rather than comprehensive.

That distinction is important because the Fed did more than leave rates unchanged—it reshaped the market’s expectations. The latest dot plot revealed that nine policymakers now support additional rate hikes this year, strengthening the US dollar and forcing investors to consider a scenario in which the Fed’s next move could be another hike rather than an extended pause. Even if further tightening is not the base case, its inclusion in the discussion changes the complexion of every risk asset rally.

Lower oil prices help ease inflation concerns, but a stronger dollar can still tighten financial conditions. Gold finds itself caught between these opposing forces. While the metal has stabilized above $4,200 as the initial shock from the Fed fades, currency markets continue to favor the dollar. The message remains clear: traders are still responding to the Fed’s tougher stance, and gold remains constrained by expectations of higher real rates and a Dollar Index trading back above the psychologically important 100 level.

For gold investors, the peace dividend and the Fed’s hawkish turn are working against one another. Falling energy prices reduce inflation pressure and should support a less restrictive policy outlook. Yet the Fed’s latest communication suggests policymakers remain concerned enough about inflation to maintain a cautious stance. This tension now sits at the center of the market debate. If Hormuz fully normalizes, Gulf exports recover, and oil prices continue to soften, the Fed’s current inflation concerns may begin to look increasingly outdated. The key question is whether declining energy costs can cool inflation expectations quickly enough to make recent hawkish repricing appear excessive, especially if consumer demand weakens later in the year.

This is the central fault line for markets. Investors are not debating whether lower oil is positive—it clearly is. The debate is whether it merely softens the Fed’s inflation challenge or fundamentally shifts the policy outlook back toward patience.

Another factor entering the equation is June options expiration, which is removing a subtle but important source of market stability. Recent gains have benefited from heavy call-option positioning, a dynamic that suppressed volatility and encouraged frequent intraday reversals. Dealer hedging acted as an invisible cushion beneath the market, but much of that support is now fading just as investors attempt to determine whether cheaper oil can offset a more hawkish Fed.

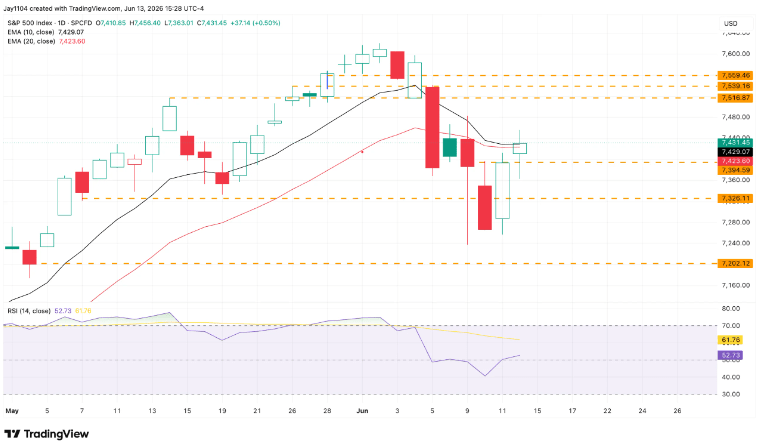

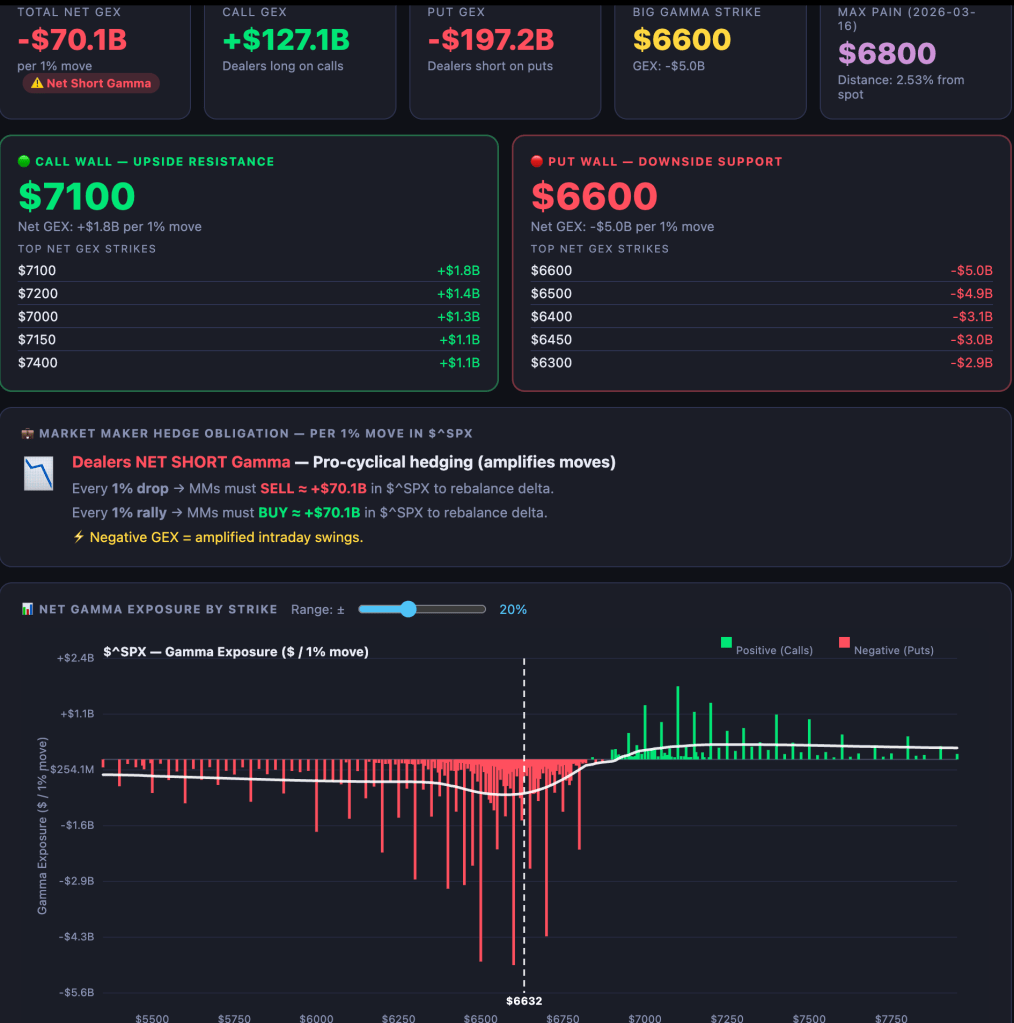

The S&P 500’s position below 7,500 is particularly important from a positioning perspective. Above major option strike concentrations, dealer hedging tends to dampen volatility by encouraging purchases during declines and sales during rallies. Below 7,500, that stabilizing effect begins to weaken.

With negative gamma extending toward 7,350, dealer hedging can start amplifying market moves instead of smoothing them. In that environment, declines may trigger additional selling from dealers seeking to maintain hedges, potentially accelerating downside momentum. This does not imply a market crash; rather, it suggests a greater sensitivity to directional flows and reduced resilience during periods of selling pressure.

The June expiration itself is not necessarily bearish. The removal of substantial call exposure may simply represent a cooling of speculative enthusiasm without damaging the broader trend. Nevertheless, once that call-heavy structure disappears, equities lose part of the mechanical support that has helped keep volatility subdued. Combined with a hawkish Fed and mixed cross-asset signals, the margin for error becomes increasingly narrow.

In practical terms, traders should expect a market with fewer shock absorbers. The derivatives landscape is becoming less supportive at the same time that the macro backdrop grows more complex. Oil is falling and the Strait of Hormuz is reopening—both constructive developments. Yet the Fed remains focused on inflation risks, and the dollar continues to reflect that reality. The key question is whether the peace dividend can cool inflation quickly enough to soften the Fed’s tougher stance.

For now, equities are voting yes. Technology leadership has returned, bonds have stabilized, and lower oil prices are removing one of the market’s most visible inflation threats. Yet this is not the classic Goldilocks environment. Investors are attempting to balance the benefits of cheaper energy against a central bank that appears increasingly willing to tighten policy if inflation resurges. As Hormuz reopens, one support mechanism is returning to markets while another—options-related protection—is quietly fading away.