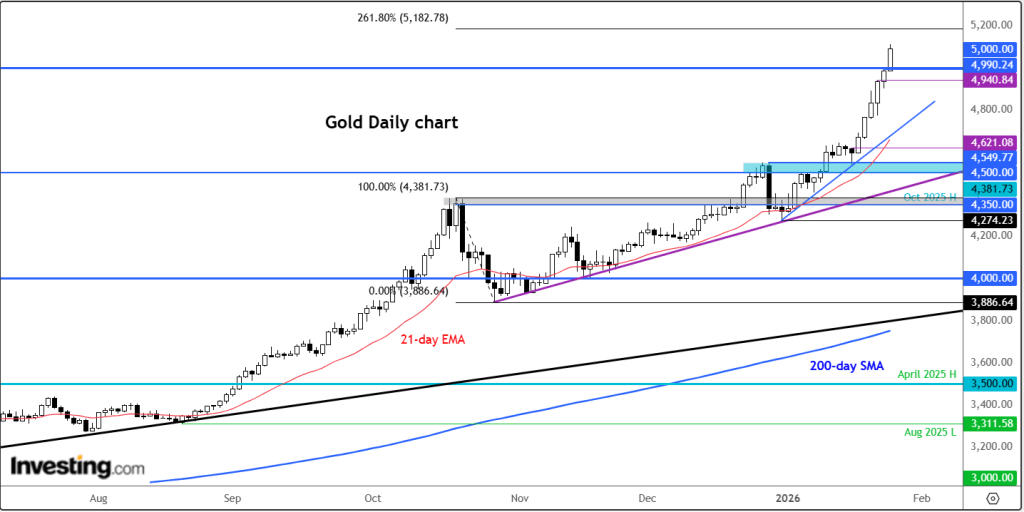

Gold prices edged higher in Asian trading on Wednesday as investors weighed mixed developments surrounding the U.S.-Israel conflict with Iran, particularly concerns about energy market disruptions and the possibility that the fighting could ease.

Traders are also awaiting U.S. consumer inflation data for February for fresh insight into the health of the world’s largest economy, although the report is unlikely to fully capture the recent surge in energy prices linked to the Iran conflict.

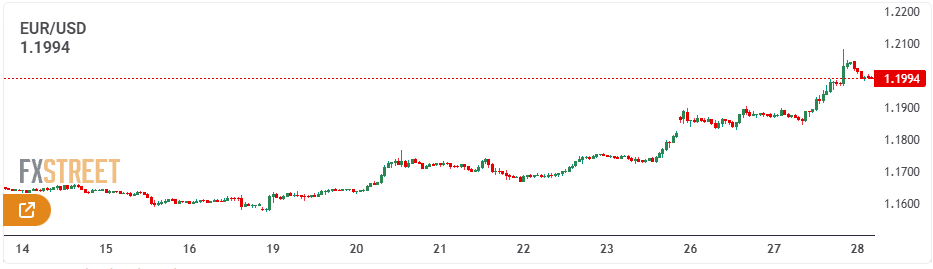

Spot gold rose 0.2% to $5,204.29 an ounce as of 01:17 ET (05:17 GMT), while gold futures slipped 0.5% to $5,213.11 per ounce.

Gold breaks above $5,200/oz as markets weigh mixed Iran signals

Gold’s gains on Wednesday pushed prices above the $5,000–$5,200 per ounce range that had contained trading over the past week, though it remained uncertain whether the breakout would hold.

The precious metal has experienced sharp volatility in recent weeks, retreating significantly after reaching a record high near $5,600 per ounce in late January.

Conflicting developments surrounding the Iran war also contributed to choppy trading this week. U.S. President Donald Trump said late Monday that the conflict was nearing an end. However, exchanges of strikes between the U.S., Israel, and Iran continued into early Wednesday, marking the twelfth straight day of fighting.

Investors remain concerned that a surge in energy-driven inflation could prompt global central banks to adopt a more hawkish policy stance—an outlook that typically weighs on gold. As a result, the metal’s gains were capped despite rising safe-haven demand.

Elsewhere in the precious metals market, price movements were relatively muted. Spot silver slipped 0.1% to $88.2245 an ounce, while spot platinum edged up 0.3% to $2,208.89 per ounce.

U.S. CPI report in focus for fresh clues on inflation

Markets are awaiting the release of U.S. consumer price index (CPI) data for February later on Wednesday, which is expected to offer clearer signals on inflation and the outlook for interest rates in the world’s largest economy.

Headline CPI is forecast to hold steady at 2.4% year-on-year, while core CPI is projected to remain unchanged at 2.5%.

Although the data is unlikely to capture the recent spike in energy prices triggered by the Iran conflict, investors will still monitor the report closely for indications on consumer spending trends and the broader health of the U.S. economy.

The CPI release follows a weaker-than-expected February payrolls report, which has fueled some concerns that economic momentum in the United States may be slowing.

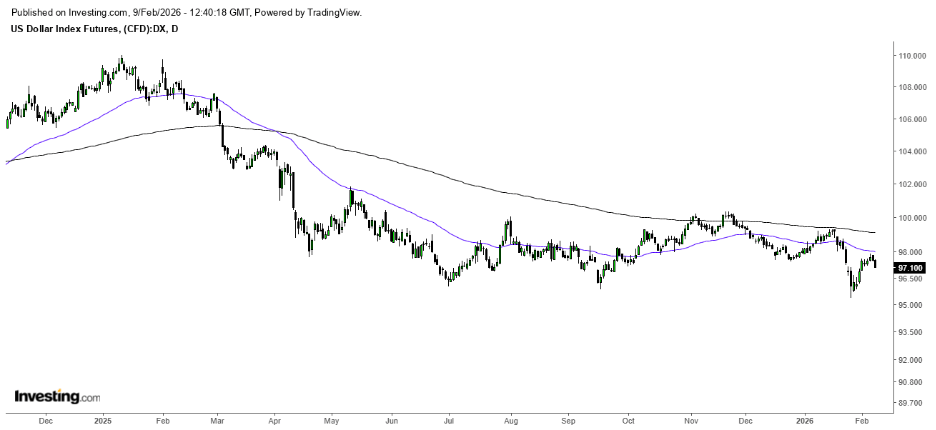

The U.S. dollar weakened on Friday after a disappointing jobs report increased expectations that the Federal Reserve could cut interest rates. Nevertheless, the currency was still on track for a strong weekly gain, supported by rising demand for safe-haven assets amid escalating tensions in the Middle East.

By 16:30 ET (21:30 GMT), the Dollar Index — which measures the dollar against six major currencies — had fallen 0.4% to 98.89. Despite the decline, it remained poised for a weekly rise of about 1.3%, its strongest performance since August 2025.

Dollar pressured by weak payroll data

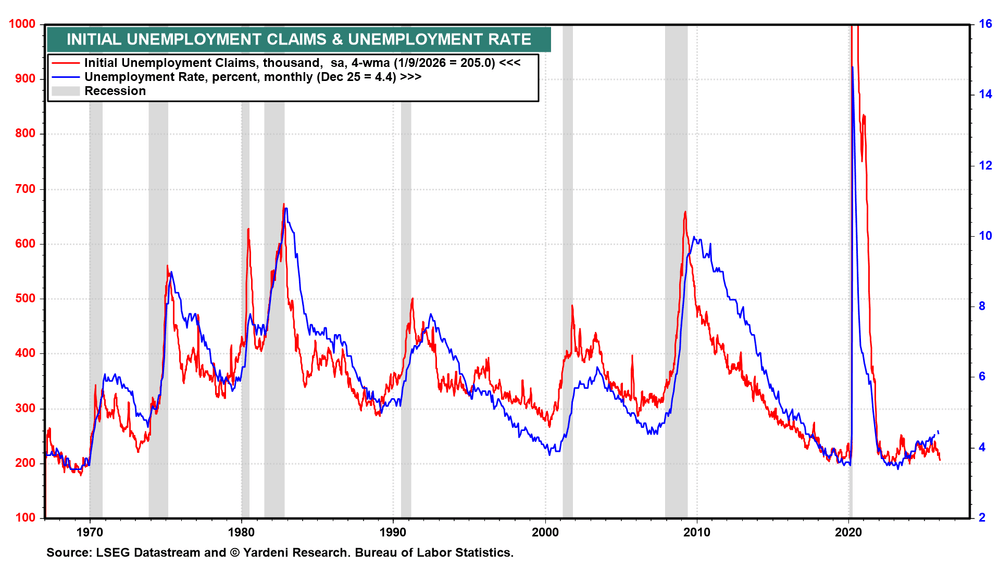

Markets focused on the February nonfarm payrolls report released Friday. The data showed the U.S. economy lost 92,000 jobs last month, far below economists’ expectations for a gain of 58,000. At the same time, the unemployment rate increased slightly to 4.4%.

The weak February figure followed a stronger January reading of 126,000 jobs, revised down from 130,000. December’s employment data was also revised lower, shifting from a gain of 48,000 to a loss of 17,000 jobs.

Following the report, traders increased their expectations that the Federal Reserve may cut interest rates. Since higher rates typically support the dollar while lower rates weaken it, the data weighed on the currency.

However, despite Friday’s pullback, the dollar benefited throughout the week from its safe-haven status as geopolitical tensions intensified in the Middle East.

U.S. Defense Secretary Pete Hegseth said Thursday that U.S. firepower directed toward Iran could increase significantly. Meanwhile, Israel announced earlier Friday that it had begun a large-scale wave of strikes targeting infrastructure in Tehran.

Iran retaliated by launching attacks against Israel and several regional countries including Gulf states, Cyprus, Turkey, and Azerbaijan, expanding the scope of the conflict.

Analysts at ING said the dollar is unlikely to resume a sustained decline unless a meaningful political breakthrough leads to a ceasefire. Until then, governments will likely continue grappling with the economic consequences of elevated energy prices. The Dollar Index is now approaching the key psychological level of 100.

According to Trade Nation senior market analyst David Morrison, the 100 level represents an important technical resistance point. The index repeatedly tested this level in November but failed to break through before eventually falling to a four-year low at the end of January.

At that time, some traders speculated the dollar’s decline could continue amid concerns it might eventually lose its role as the world’s primary reserve currency. Morrison said those predictions now appear premature, although the Dollar Index still faces several significant resistance levels.

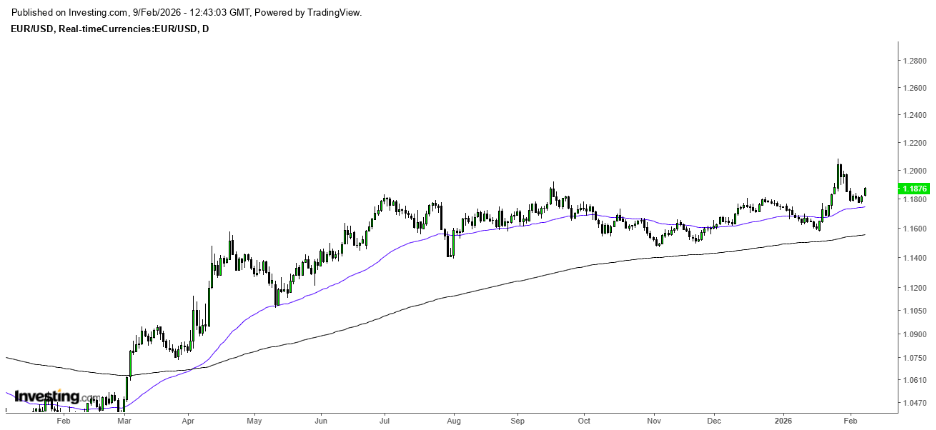

Euro heads for weekly decline

In Europe, EUR/USD was mostly unchanged at 1.1611, though the euro was on track to lose about 1.7% for the week as higher energy costs weighed on economic growth prospects in the region.

Eurozone GDP data due later in the session is expected to confirm growth of 0.3% in the final quarter of last year and annual expansion of 1.3%.

Earlier data also showed eurozone inflation in February came in higher than expected, even before the outbreak of the Iran conflict.

Despite the geopolitical developments, European Central Bank policymaker and Dutch central bank chief Olaf Sleijpen said the eurozone’s monetary policy environment remains relatively stable.

Speaking in an interview Friday, he noted that while the situation is no longer ideal, he has not significantly changed his overall assessment of the region’s economic position.

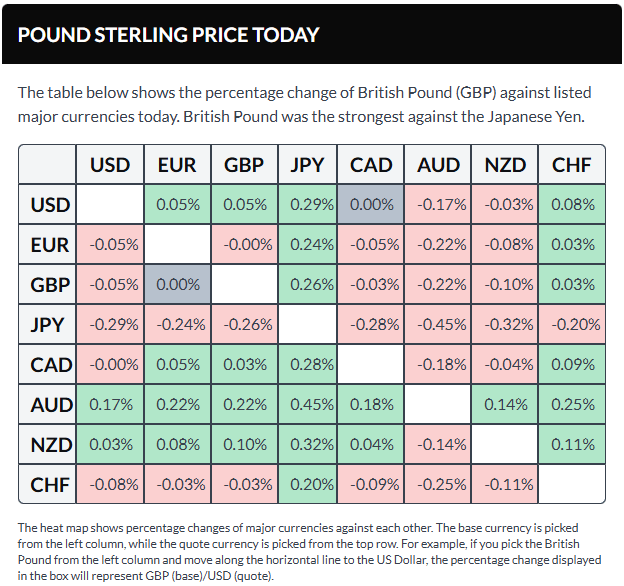

Meanwhile, GBP/USD rose 0.3% to 1.3393, although sterling was still on track for a weekly decline of around 0.8% as rising energy prices add further pressure on the U.K. economy and government.

Yen weakens amid rising oil prices

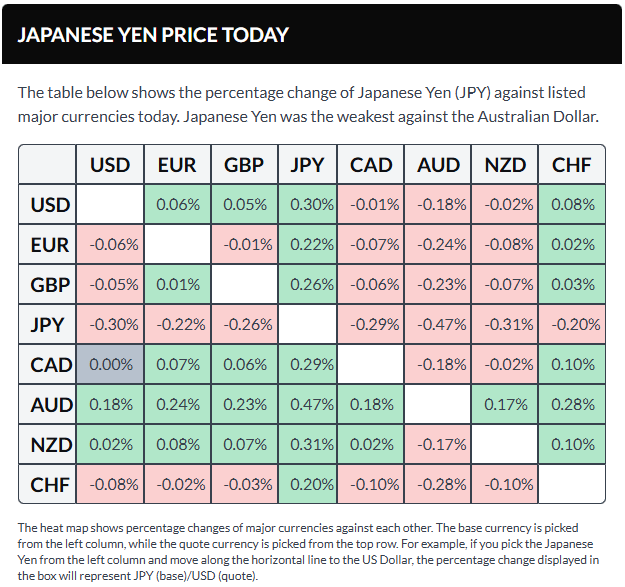

In Asia, USD/JPY increased 0.2% to 157.83 and was on track for a weekly gain of 1.1%. The Japanese yen remained under pressure as higher oil prices raise inflation risks for energy-importing economies such as Japan.

Bank of Japan Deputy Governor Ryozo Himino told parliament that the weaker yen is pushing up import costs and could influence underlying inflation.

USD/CNY rose 0.1% to 6.8965 and was also heading for weekly gains, following a week in which Chinese authorities announced their lowest economic growth target since 1991.

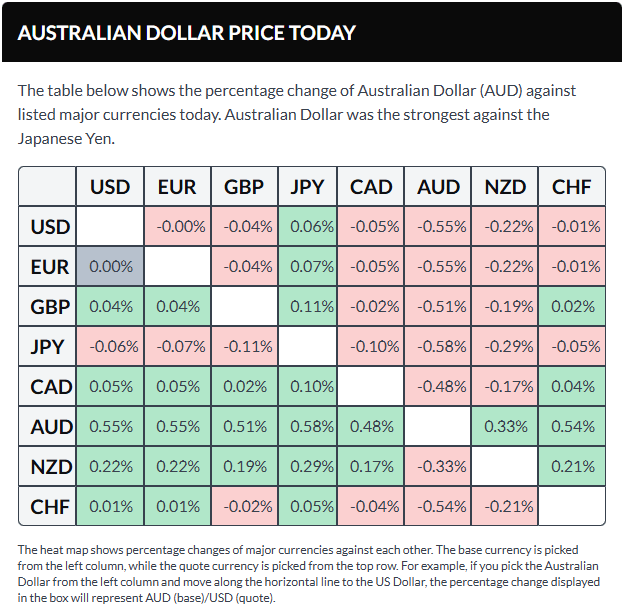

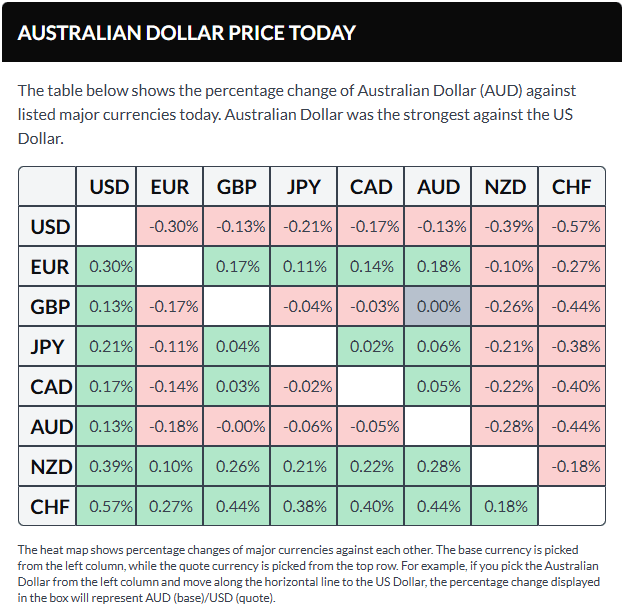

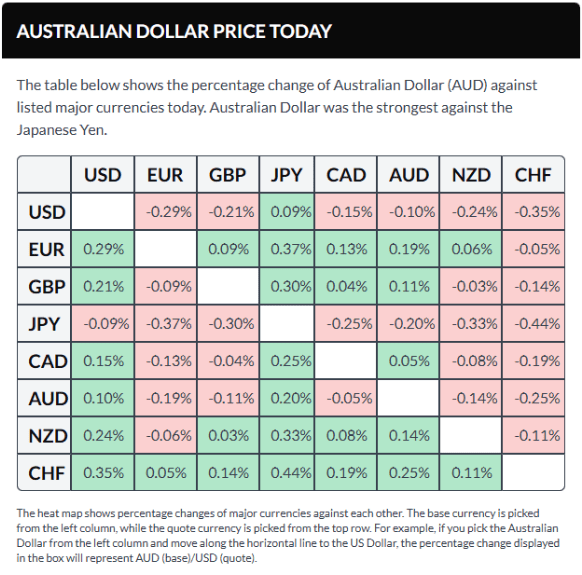

Meanwhile, AUD/USD climbed 0.3% to 0.7026, though the Australian dollar was still set for a weekly loss of about 1.3%, as risk-sensitive currencies remained under pressure.

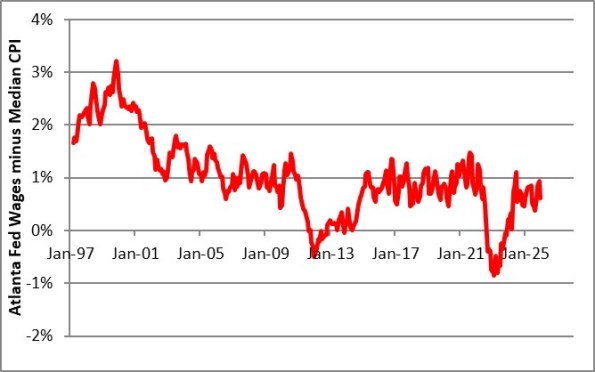

Recent U.S. growth data have pointed to notable economic resilience — but consumer sentiment tells a more cautious story.

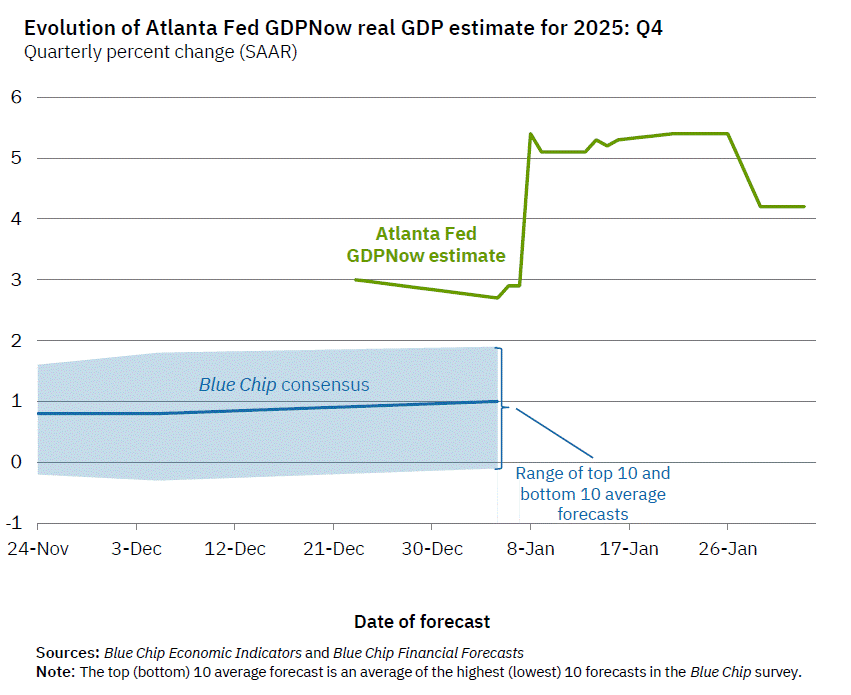

According to the Federal Reserve Bank of Atlanta, real Gross Domestic Product is projected to have expanded at an annualized pace of 4.2% in the fourth quarter of 2025. That figure exceeded expectations and represents one of the strongest quarterly performances in the past two years.

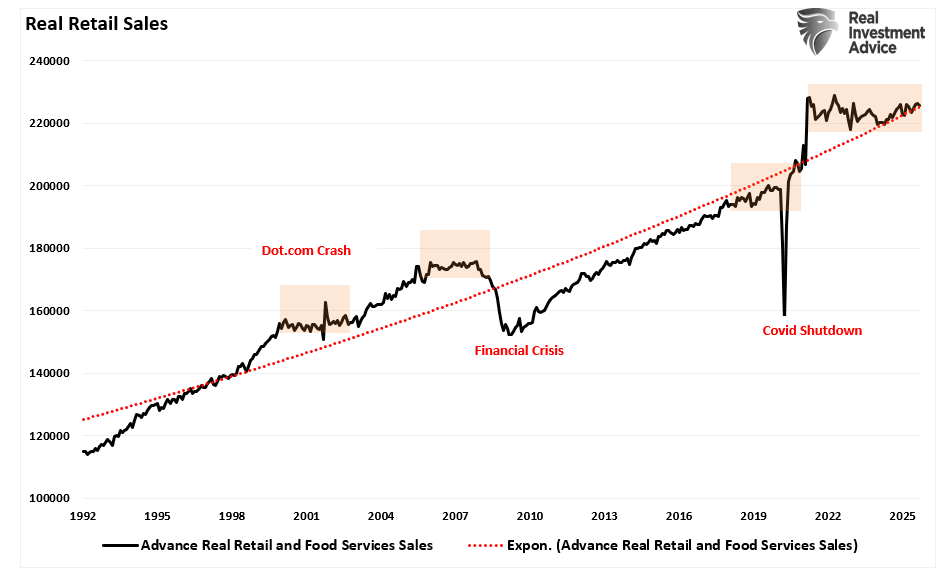

The expansion was supported by steady consumer spending, firmer exports, and higher government expenditures. Household consumption climbed 3.5%, its fastest rate of increase this year. On the surface, these numbers portray a macroeconomy that remains firmly in growth mode.

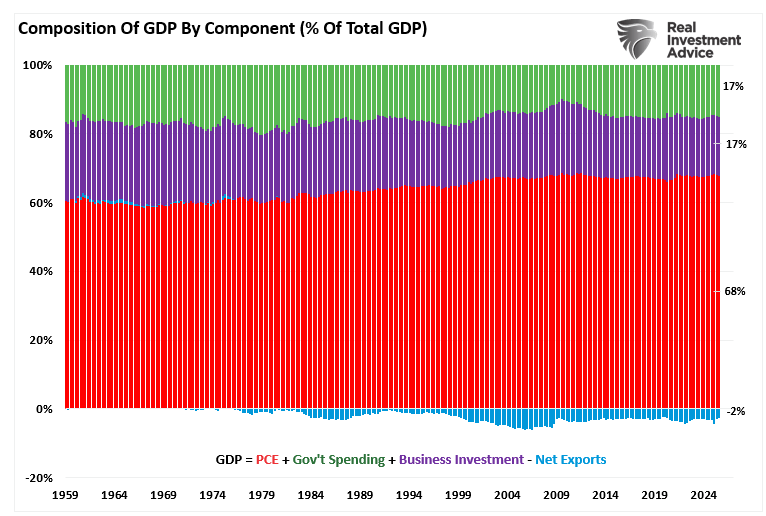

Gross Domestic Product (GDP) represents the total value of goods and services produced within the United States. Of that total, personal consumption expenditures (PCE) account for roughly 68%. Put simply, the consumer is the backbone of the U.S. economy — as household spending goes, so too goes overall economic growth.

When GDP rises, it reflects an increase in overall economic activity — stronger consumer demand that supports higher production and broader expansion. For that reason, growth rates are closely watched by policymakers, investors, and corporate leaders. Strong GDP figures are often interpreted as a signal of improving sales prospects and profit potential.

However, GDP does not tell the whole story of household financial well-being.

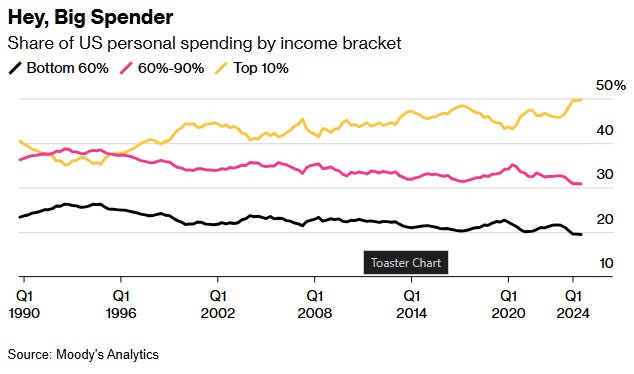

By design, economic growth data measure aggregate output. They do not reveal how income is distributed, how conditions vary across regions, or how millions of families actually experience the economy. A clear illustration is the breakdown of consumer spending by income level. At present, roughly half of all U.S. consumer spending is driven by the top 10% of earners — a share that has been increasing — while the spending contribution from the bottom 90% has been declining.

In other words, headline growth can appear solid even as the underlying breadth of participation narrows.

In short, strong headline growth can conceal areas of financial strain among households and small businesses. Expansion driven primarily by exports or government spending may not meaningfully filter through to broad segments of workers, creating a disconnect between aggregate output and lived experience.

A clear example of this distortion appeared in 2025. In the first quarter, a surge in imports aimed at front-running tariffs weighed heavily on GDP. When those trade fears subsided in the second quarter, import flows normalized, producing a sharp rebound in growth. Yet these swings in trade data had limited direct impact on most consumers. The volatility was largely statistical rather than reflective of a dramatic shift in household conditions.

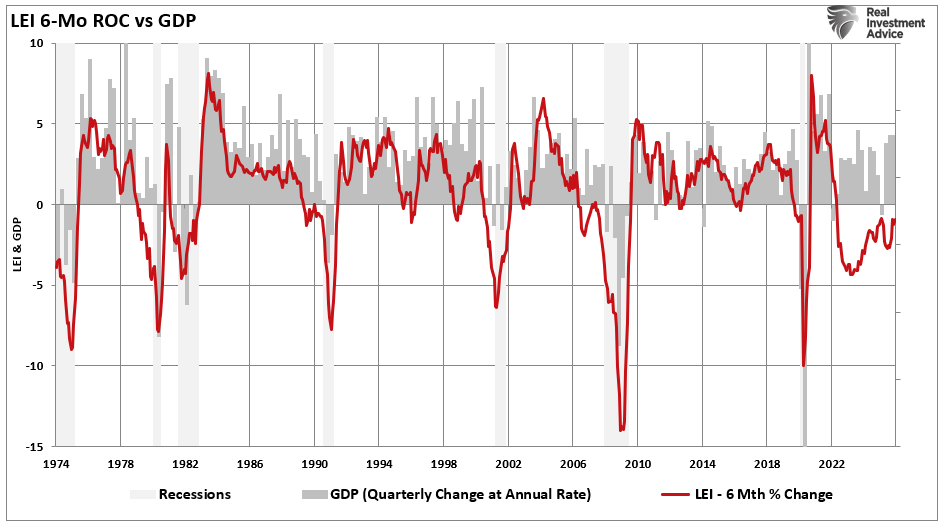

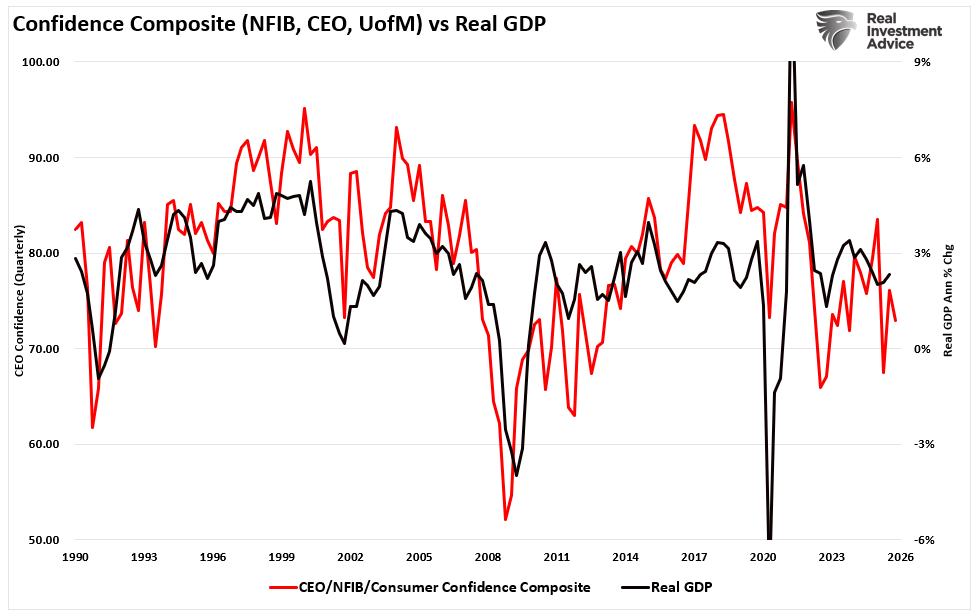

While GDP figures suggest a sturdy economic backdrop, other coincident and leading indicators tell a more cautious story. The The Conference Board Leading Economic Index (LEI), which historically leads the U.S. economy by roughly six months, has remained in contraction for an extended period. Its six-month rate of change has long been regarded as one of the more reliable signals of impending slowdowns or recessions.

Notably, however, despite the prolonged weakness in the LEI, the broader economy has not formally entered recession — underscoring the growing divergence between traditional warning signals and realized economic outcomes.

At first glance, headline growth data suggest the economy remains on firm footing. Output is expanding, spending is holding up, and aggregate indicators point to continued resilience.

But a closer examination reveals a more nuanced picture. Beneath the surface, several crosscurrents — from uneven income distribution and trade-related distortions to persistent weakness in leading indicators — point to a mixed underlying environment.

That divergence helps explain why economic sentiment can feel far weaker than the headline numbers imply. Strong aggregate growth does not automatically translate into broad-based confidence, particularly if gains are concentrated or forward-looking indicators continue to flash caution.

The Gap Between Rising Stocks and Weak Consumer Sentiment

Historically, it makes sense that stock markets and economic data would trend in the same direction over the long run. Corporate earnings ultimately derive from economic activity, and sustained growth in output and income should support higher equity valuations over time.

As discussed in “Return Expectations Are Too High,” long-term market returns are anchored to the growth of the underlying economy, productivity gains, and profit expansion — not simply short-term momentum or sentiment-driven rallies.

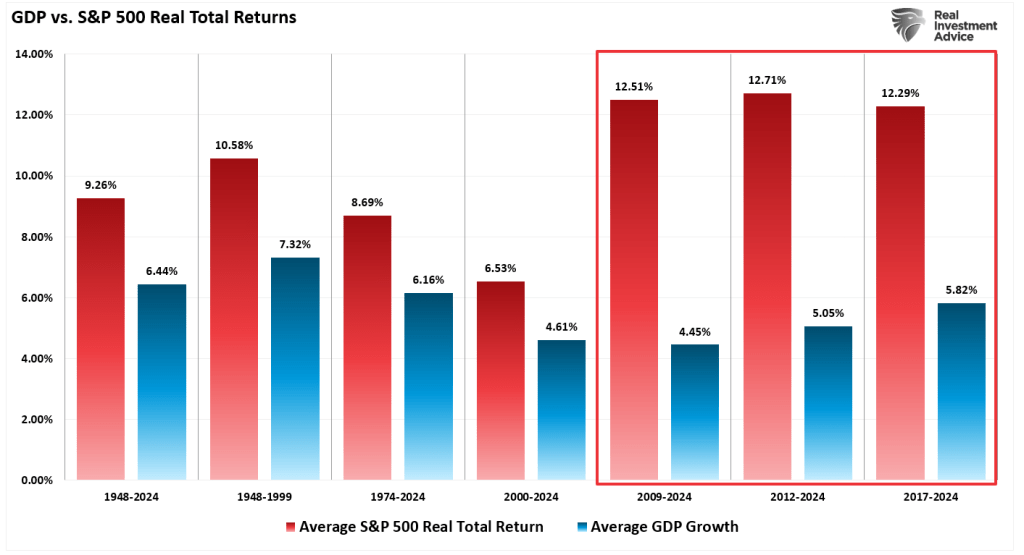

“The chart illustrates average annual inflation-adjusted total returns (including dividends) dating back to 1948, using total-return data compiled by Aswath Damodaran at the NYU Stern School of Business. From 1948 through 2024, the stock market delivered an average real return of 9.26%.

However, in the years following the 2008 financial crisis, inflation-adjusted total returns increased by nearly three percentage points across the last three measured periods.

Here’s the challenge: real (inflation-adjusted) equity returns are relatively straightforward to conceptualize. Over time, they reflect economic growth (GDP) plus dividend income, minus inflation. That relationship broadly held from 1948 to 2000.

Since 2008, though, the math has diverged. Nominal GDP growth has averaged roughly 5%, and dividend yields have hovered near 2%. Yet actual market returns have significantly exceeded what that underlying economic engine would normally justify in terms of sustainable earnings expansion.”

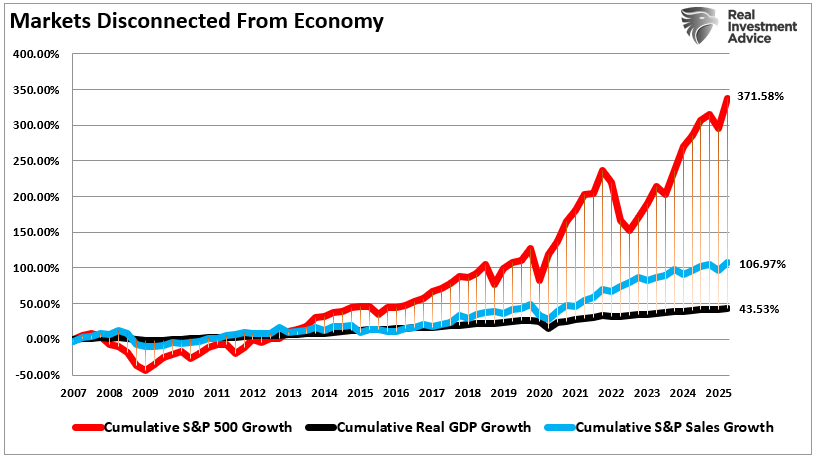

That 15-year divergence is not particularly surprising. As discussed in “Pavlov Rings the Bell,” markets have repeatedly been cushioned from deeper corrections by aggressive fiscal and monetary intervention.

Over the past decade and a half, major drawdowns were often met with policy stimulus — whether through deficit spending or actions by the Federal Reserve. Each episode of support was followed by market recovery, reinforcing a powerful feedback loop: intervention became associated with rising asset prices.

In effect, investors were conditioned to expect rescue during periods of stress — to buy every dip under the assumption that policymakers would step in. That conditioning ties directly to the concept of “moral hazard.”

Moral hazard (noun, economics): A reduced incentive to guard against risk when one is shielded from its consequences — as with insurance protection.

Following the Global Financial Crisis, near-zero interest rates and repeated rounds of quantitative easing strengthened the belief that a policy backstop would reappear whenever volatility increased. Over time, that expectation hardened into a reflexive behavior: assume support, assume recovery, assume higher prices.

Those sustained supports — in both the real economy and financial markets — helped drive a wedge between underlying economic fundamentals and realized financial returns. In other words, policy intervention became a key force behind the growing disconnect between economic reality and asset-price performance.

At present, GDP growth has continued to surprise to the upside, and several macro indicators reflect ongoing resilience. At the same time, major equity benchmarks such as the S&P 500 have climbed to record levels. That advance has been fueled less by current consumer sentiment and more by expectations of future earnings growth.

The challenge, however, is that equity valuations appear increasingly disconnected from underlying revenue growth. Markets are pricing in optimism about future expansion, even as broad-based income and demand trends remain uneven.

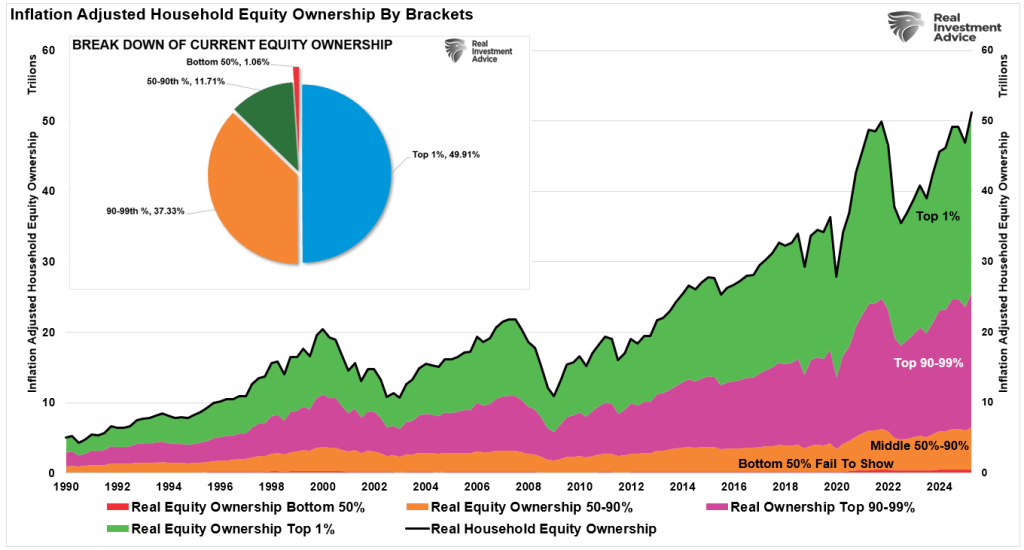

There is also a structural limitation embedded in the “wealth effect.” Rising stock prices can support consumption by boosting household net worth. Yet equity ownership in the United States is highly concentrated. Roughly 87% of equities are owned by the top 10% of households. As a result, the transmission from higher stock prices to broader economic activity is narrower than headline gains might suggest.

That concentration is reflected in spending patterns as well. The top 40% of income earners now account for approximately 80% of total consumption. Consequently, while financial asset values have surged, the macroeconomic lift from those gains is disproportionately tied to higher-income households — leaving sentiment among the broader population more subdued than market performance alone would imply.

That divergence goes a long way toward explaining the disconnect between subdued consumer sentiment and robust headline economic data.

When growth and market gains are concentrated among higher-income households — and asset-price appreciation primarily benefits those with significant equity exposure — aggregate statistics can remain strong even as large segments of the population feel financial strain.

In other words, the macro numbers reflect the strength of those driving the bulk of spending and asset ownership, while sentiment surveys capture the broader lived experience. The result is an economy that looks resilient on paper but feels far less secure to many households.

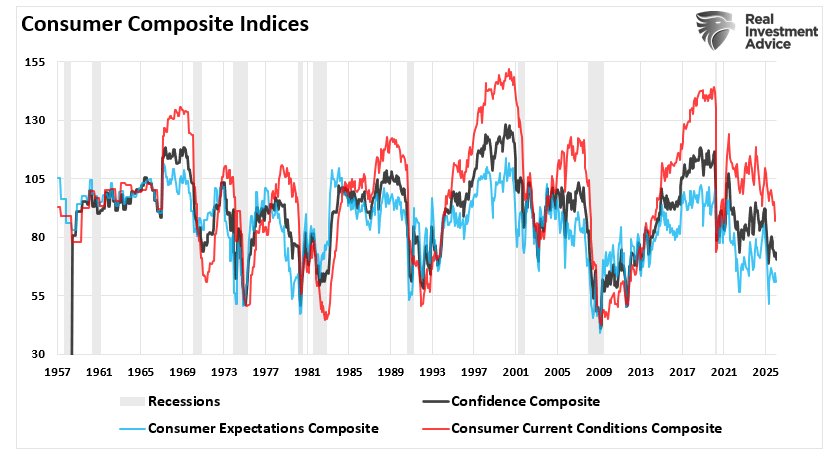

Consumer Confidence Surveys Remain Soft Even as Economic Data Stays Strong

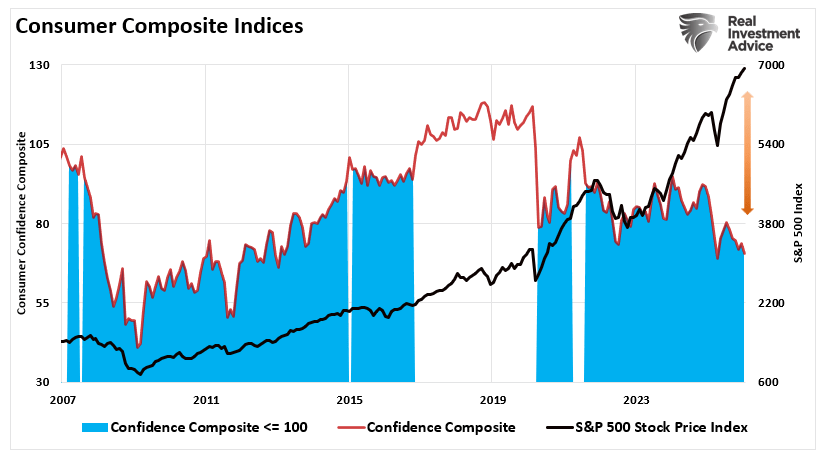

In clear contrast to upbeat macroeconomic indicators and strong equity market gains, consumer sentiment readings have deteriorated significantly. Both the Conference Board Consumer Confidence Index and the University of Michigan Surveys have fallen steeply over the past two years, even as stock prices have climbed. Historically, consumer sentiment tends to move in tandem with rising markets, which is intuitive. The chart below presents a composite measure combining these two leading sentiment indicators.

In both surveys, readings on current conditions and future outlook remain notably subdued, with the expectations component dropping to levels that have historically been linked to recession warnings.

The downturn in sentiment points to rising concerns over employment prospects, business conditions, and future income. Respondents frequently highlighted worries about inflation, elevated prices, food and energy expenses, the affordability of health insurance, and broader geopolitical and political uncertainty. Yet despite this widespread unease, GDP has continued to grow.

Importantly, the gap between soft sentiment data and hard economic figures is not unprecedented. Analysts have often observed that consumer attitudes tend to lag underlying economic performance, and sentiment could improve if expansion persists. In the near term, surveys typically capture prevailing fears and uncertainty, which can weigh on confidence even when actual spending remains relatively solid. Although nominal figures indicate that consumer spending is holding up, much of that resilience reflects paying higher prices for the same—or even fewer—goods, rather than an increase in real consumption, which helps explain the sustained weakness in sentiment readings.

Importantly, if consumer sentiment influences spending—and consumption accounts for roughly 68% of the economy—then that spending ultimately represents demand for businesses of all sizes. In a genuinely strong growth environment, we would expect improving demand to be mirrored by rising confidence across households. Yet, as the composite index illustrates, sentiment levels remain subdued. The historical relationship between confidence measures and the future trajectory of economic activity underscores why this divergence warrants attention.

Soft sentiment readings do not necessarily signal an imminent downturn. However, they do reflect a guarded mindset among both consumers and business owners. That caution can translate into more restrained spending across key components of GDP. If confidence remains depressed, a moderation in economic activity would be a reasonable outcome.

Why the Divergence Matters and What It May Signal Ahead

The gap between solid economic data, rising equity markets, and subdued consumer confidence carries meaningful implications. On the surface, macro indicators point to continued expansion, reinforcing higher stock prices and optimistic earnings forecasts. Yet beneath that strength, households and many business owners report lingering insecurity and pessimism about the future.

This disconnect prompts several key questions:

Can growth remain durable if confidence stays depressed?

Will corporate earnings hold up if consumers begin to retrench?

Could persistent pessimism eventually shape real-world behavior, leading to slower spending and softer growth?

History offers cautionary precedents where negative sentiment foreshadowed downturns—not because the hard data was inaccurate, but because sentiment ultimately influenced economic decisions.

The divergence also highlights distributional dynamics. Aggregate growth figures often mask disparities in income and wealth. Higher-income households account for roughly half of total consumption, while lower-income groups may not fully share in the benefits of expansion. That imbalance helps explain weaker sentiment readings. It also leaves markets vulnerable to any shock that prompts affluent consumers to scale back spending—particularly in an environment where the gap between economic “haves” and “have-nots” remains wide.

Investment Implications

For investors, this mixed backdrop argues for disciplined risk management. Markets may continue advancing on elevated earnings expectations, but those expectations can shift quickly as economic conditions evolve.

Scrutinize valuations. Rising indices do not preclude overpricing. Favor firms with strong balance sheets, reliable cash flows, and pricing power.

Diversify thoughtfully. Sector performance can diverge sharply. Defensive areas such as utilities, consumer staples, and healthcare often prove more resilient during sentiment-driven slowdowns.

Track leading indicators. Watch employment trends, consumer credit conditions, and forward-looking economic indices. Weak confidence can precede softer activity.

Maintain liquidity. Holding cash provides flexibility amid volatility created by divergence.

Consider hedging strategies. Exposure to bonds or volatility-linked instruments may help cushion downside risks.

Emphasize quality. Companies with durable competitive advantages are typically better positioned to navigate uncertainty.

The split between hard data, market performance, and consumer mood represents a meaningful economic signal. While there are persuasive arguments that markets can continue climbing and that pullbacks should be bought, prudence requires acknowledging alternative outcomes.

To borrow a well-known observation from Bob Farrell:

Historically, when “all experts agree,” discipline and preparation for the unexpected have often proven wise.

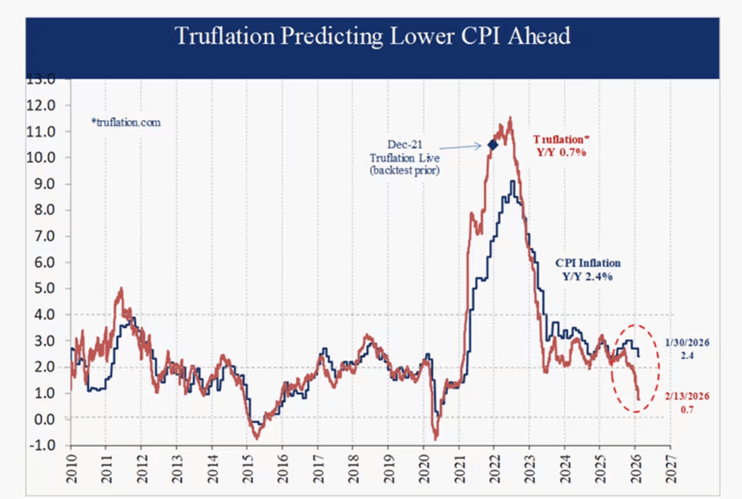

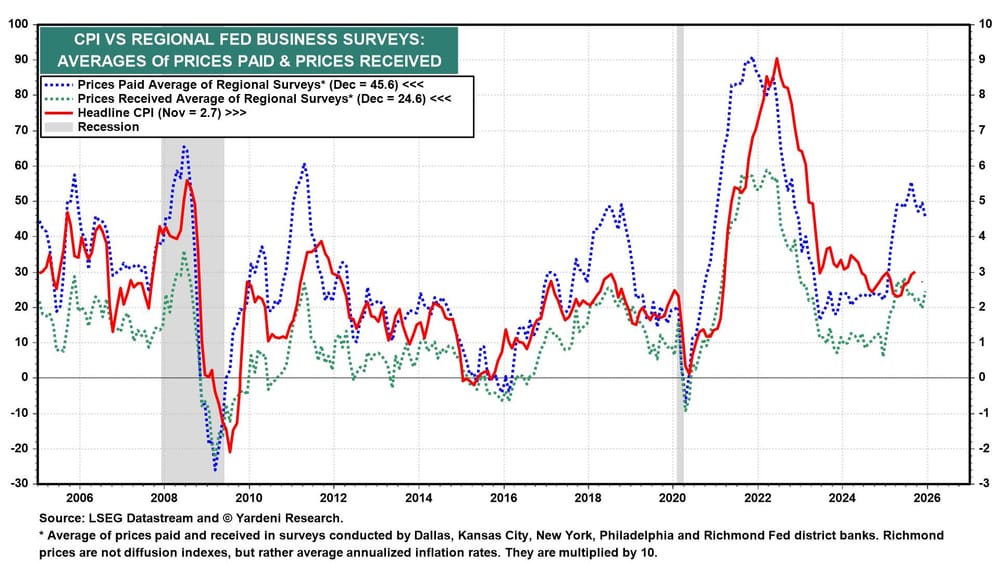

Inflation measurement sits at the core of modern macroeconomics. Interest-rate policy, asset valuations, fiscal planning, and central-bank credibility all hinge on how price pressures evolve. Yet the benchmark most policymakers rely on — the Consumer Price Index (CPI) — is a monthly government report designed for a far less digitized and fast-moving economy.

Increasingly, market participants are supplementing that traditional gauge with real-time alternatives. Among them, Truflation has emerged as the most widely cited live inflation index. Built from millions of observed prices and updated continuously, it offers a near real-time snapshot of price dynamics. In early 2026, its signal diverges meaningfully from official CPI data.

Methodology and Structural Differences

Truflation was launched in December 2021 amid frustration over the lag in official inflation reporting. While CPI is released monthly and relies heavily on surveys, sampling, and statistical smoothing, Truflation applies a bottom-up, digitally native methodology.

The index aggregates data from more than 30 million items across 30+ licensed providers — including online retailers, housing platforms, and consumer-data firms. Prices update daily and are secured through decentralized oracle infrastructure on the Chainlink network, increasing transparency and reducing the risk of retrospective revisions.

Like CPI, Truflation tracks twelve broad consumption categories. However, its category weights are recalibrated annually using observed spending patterns rather than fixed survey-based assumptions. This allows the index to adjust more quickly to shifts in consumer behavior and pricing trends.

Historically, that responsiveness has mattered. Empirical comparisons suggest Truflation has often led CPI turning points by roughly 40 to 75 days, flagging inflection points in inflation momentum well before they appear in official releases.

Institutional Validation

Skepticism toward alternative measures is natural. Still, Truflation has begun clearing some of the credibility hurdles required for broader institutional adoption.

Throughout 2024 and 2025, its short-term forecasting accuracy was notable. In many instances, its readings anticipated CPI outcomes within approximately ±0.1 percentage points. That degree of precision has encouraged growing usage among macro hedge funds and systematic trading strategies.

Institutional validation advanced further in early 2026 when Truflation was integrated into the Bloomberg L.P. terminal ecosystem — a quiet but meaningful step that elevated it from a crypto-native experiment into a recognized macro data input.

Transparency also strengthens its appeal. Daily updates, publicly documented methodology, and auditability offer advantages in markets that reprice continuously, where a 30-day lag can materially affect positioning.

The 2026 Divergence

By mid-February 2026, the spread between Truflation and official CPI readings had widened to one of the largest gaps since the index was created:

Official CPI (January 2026): 2.4% year-over-year

Truflation (Feb 1–18, 2026): ~0.7%

Core CPI: ~2.5%

Truflation core proxy: ~1.3%

Such a divergence presents a challenge: either real-time data are signaling a rapid disinflationary shift not yet captured by government statistics, or the high-frequency approach is temporarily underestimating sticky components embedded in CPI.

If historical lead times hold, markets may need to reassess the inflation trajectory sooner rather than later.

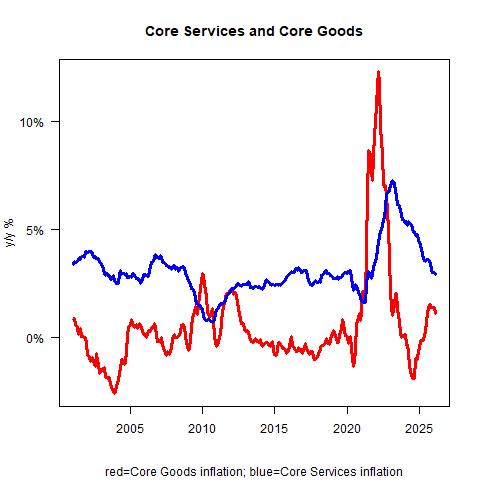

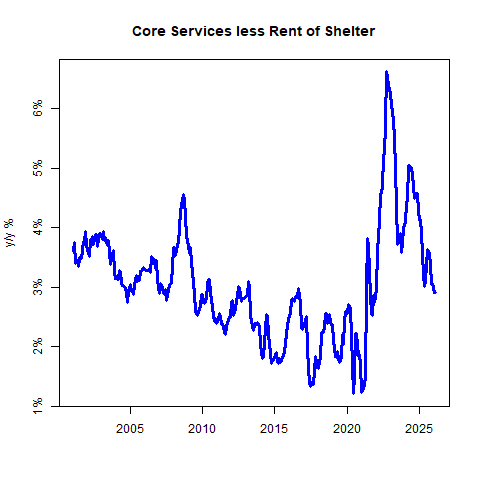

The widening gap between the two measures points to fundamentally different interpretations of current inflation momentum. The central source of divergence is housing.

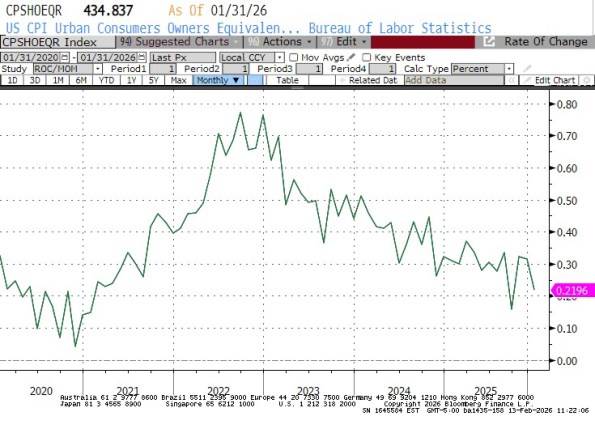

Truflation incorporates real-time asking rents pulled from active market platforms, capturing the recent cooling in rental prices as it happens. By contrast, official CPI relies heavily on “Owner’s Equivalent Rent,” a survey-based estimate that typically lags actual rental-market conditions by six to twelve months.

In effect, the two gauges are measuring different time horizons. Truflation reflects present housing dynamics, while CPI still embeds rental trends from prior quarters.

The macro implications are significant. If the real-time signal is more accurate, the U.S. economy could be moving closer to disinflation — or even deflationary — conditions, historically associated with rising recession risk. Meanwhile, official data continue to portray a controlled soft landing, with inflation appearing comfortably near target.

Explaining the Reluctance

Despite its growing track record, many economists remain hesitant to incorporate Truflation into formal macro frameworks. The resistance tends to rest on three main arguments.

1. Institutional inertia. CPI has decades of embedded usage. Forecasting models, policy rules, asset-allocation frameworks, and academic research are all synchronized to its monthly release cycle. Integrating a daily inflation measure would require reworking not only projections, but established institutional workflows.

2. Volatility bias. Because Truflation updates continuously, it can display sharp short-term swings. A rapid daily decline may be dismissed as noise, even when it reflects genuine pricing shifts. By comparison, CPI’s smoothed profile feels more stable — even if that stability comes at the expense of timeliness.

3. Composition differences. Truflation assigns slightly less weight to housing than CPI. Critics argue this could understate inflation during periods of accelerating rents. Yet the reverse also holds true: when rental markets cool quickly, CPI may overstate underlying price pressure — which appears to be the present dynamic.

Ultimately, the hesitation is less about data availability and more about comfort. A measure that moves faster and smooths less inevitably challenges established interpretive habits.

Conclusion: Why the Signal Matters

If Truflation’s current reading is directionally correct, monetary-policy expectations could be misaligned with underlying inflation trends. The Federal Reserve may have greater scope to ease than prevailing consensus assumes, even as headline data suggest economic resilience.

This does not mean Truflation should replace CPI as the official benchmark. But when divergences persist and widen, dismissing the alternative becomes increasingly difficult.

More broadly, the debate underscores a structural issue: inflation cannot be treated solely as a once-a-month statistic in an economy where prices adjust continuously. Measurement tools must evolve alongside market speed.

Truflation’s importance does not rest on perfection. Its value lies in timeliness, transparency, and the growing challenge of ignoring what it is signaling.

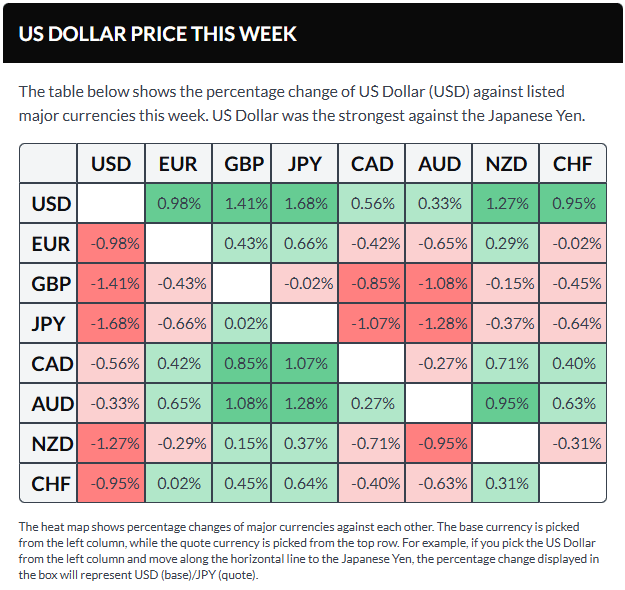

Most Asian currencies slipped on Friday as investors weighed a mixed interest rate outlook across the region. The Australian dollar was on track for a solid monthly gain, while the Japanese yen remained under pressure.

The Chinese yuan declined after Beijing lowered a key reserve requirement to make dollar purchases cheaper domestically, though the currency continued to hover near three-year highs.

Meanwhile, the dollar index and dollar index futures edged down about 0.1% in Asian trading. Despite the dip, the greenback was up 0.7% for February, supported by safe-haven demand and lingering uncertainty over the direction of interest rates.

Japanese yen subdued after weak Tokyo CPI, February decline in focus

The Japanese yen saw the USD/JPY pair slip 0.2% on Friday and was on track to gain 0.7% for February.

Pressure on the yen intensified as uncertainty grew over the timing of the Bank of Japan’s next interest rate hike. Those doubts deepened following softer-than-expected consumer price index data from Tokyo for February.

The reading—often viewed as a leading indicator for nationwide inflation—showed core CPI falling below the BOJ’s 2% annual target for the first time in nearly four years, potentially complicating the central bank’s plans for further rate increases.

The yen had weakened earlier in February amid concerns about the fiscal implications of Prime Minister Sanae Takaichi’s proposed stimulus measures and tax cuts. However, she appeared to gain momentum for advancing her fiscal agenda after her ruling coalition secured a supermajority in Japan’s lower house of parliament.

Chinese Yuan slips after PBOC lowers FX risk reserve ratio

The Chinese yuan’s USD/CNY pair rose 0.2% on Friday after the People’s Bank of China removed a key foreign exchange risk reserve requirement for certain forward contracts—a step that makes dollar purchases cheaper domestically.

The move follows a strong rally in the yuan against the dollar in recent months, partly fueled by exporters offloading the greenback amid a robust trade surplus with the United States.

However, rapid appreciation of the yuan can weigh on Chinese exporters by shrinking returns on overseas sales. Friday’s decision suggests the central bank may be aiming to curb further strength in the currency.

The yuan had approached a three-year high on Thursday before pulling back.

Australian dollar set for February gains on hawkish RBA outlook

The Australian dollar’s AUD/USD pair climbed 0.25% on Friday, ranking among Asia’s top performers for the month.

The Aussie was on track to advance 2.3% in February, largely supported by a more hawkish stance from the Reserve Bank of Australia. The central bank raised interest rates by 25 basis points earlier in the month and signaled it would tighten further if inflation fails to ease.

Stronger-than-expected January CPI data released this week reinforced expectations that the RBA could deliver additional rate hikes.

Elsewhere in the region, most Asian currencies edged lower on Friday. The South Korean won’s USD/KRW pair ticked up slightly but remained down 1.3% for February.

The Indian rupee’s USD/INR pair steadied after climbing back above the 91-per-dollar mark, though it was still 0.8% weaker this month, despite gaining support from a U.S.–India trade agreement.

Meanwhile, the Singapore dollar’s USD/SGD pair was little changed on the day and down 0.7% for February.

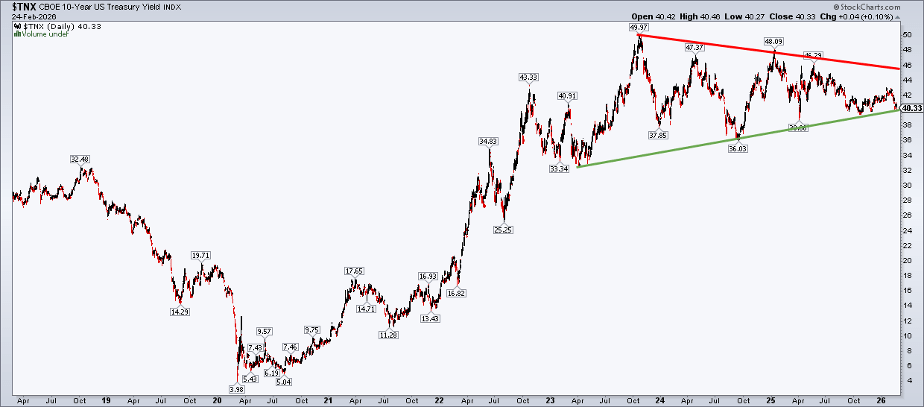

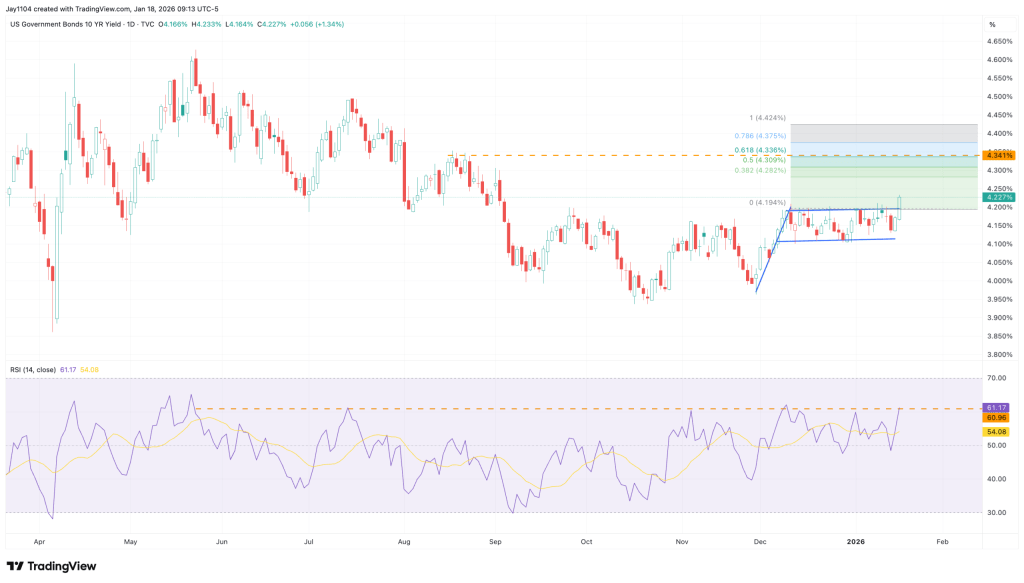

The benchmark 10-year Treasury yield is testing critical support, with downside pressure beginning to build.

Equities and bond yields are sliding in tandem — an unusual combination that may reflect deteriorating macro-risk conditions.

A strengthening US dollar alongside declining yields could point to a broader defensive rotation across markets.

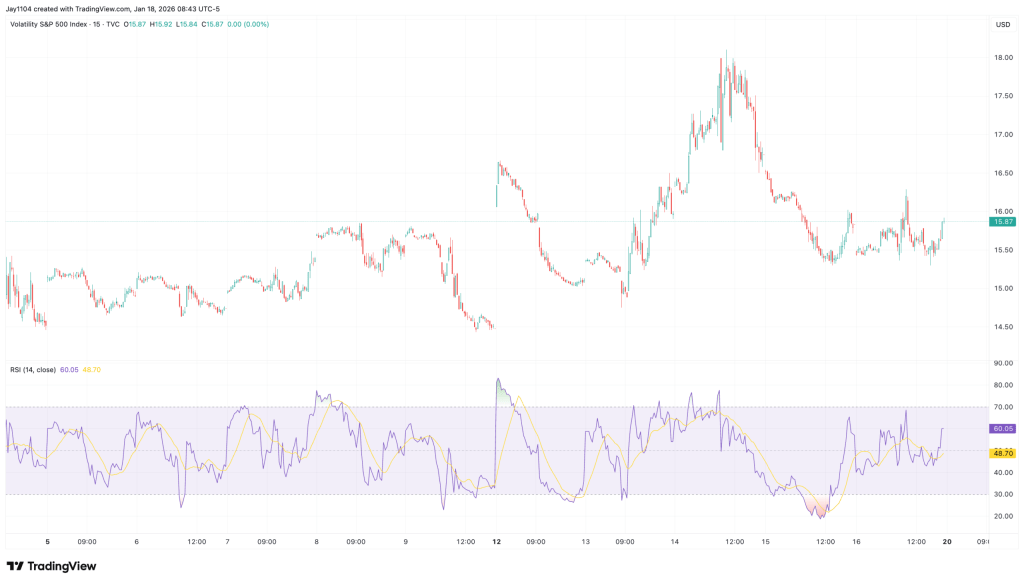

Last week, attention was drawn to the danger zone in the CBOE Volatility Index. Historically, when Wall Street’s “fear gauge” climbs into the mid-20s, equity markets have tended to experience heightened turbulence.

Now, focus shifts to the benchmark 10-year US Treasury yield. Recently, declining yields have supported the S&P 500 — particularly small- and mid-cap shares — since the so-called Liberation Day and the development of the expansive One Big Beautiful Bill Act (OBBBA). Additional fiscal stimulus or tax relief may still be forthcoming, as suggested by Donald Trump during Tuesday night’s State of the Union address.

Importantly, the surge in yields last April and May was not confined to the United States. Global bond markets reached multi-decade highs, pulling US Treasuries higher in tandem. Despite narratives around “selling America,” the primary US bond bear market unfolded between August 2020 and October 2023, when the 10-year yield climbed sharply from 0.504% to 4.997%. The past two and a half years have largely represented a consolidation phase rather than a fresh structural breakout.

The key question now: is that consolidation nearing resolution — and if so, in which direction?

10-Year Treasury Yield: A historic tightening pattern after the major bond bear market. Chart courtesy of StockCharts.com.

Treasuries Under the Spotlight

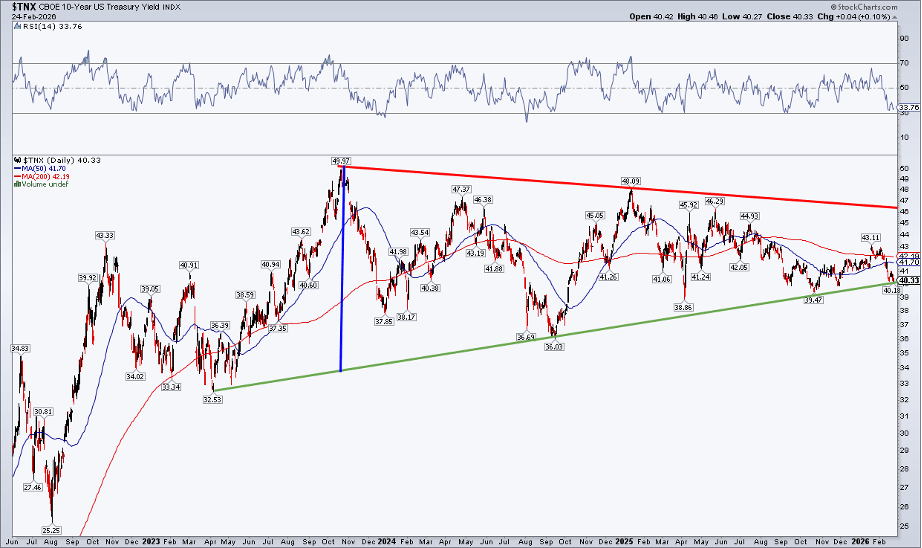

The chart below suggests that the 10-year Treasury yield could be slipping beneath a critical support level. A brief upside breakout in January quickly reversed as sellers stepped in, and now the benchmark rate is hovering near the 3% mark. It’s worth reminding traders that diagonal trendlines can be unreliable, while horizontal support and resistance levels tend to carry more weight. Additionally, log-scale charts are generally better suited for evaluating wide swings in price or yield.

With those caveats noted, what is the chart signaling? Trading below both the 50-day and 200-day moving averages, the primary trend favors Treasury price bulls (and lower yields). Meanwhile, the RSI has eased back toward the 30 level after failing to reach 70 during the fourth-quarter rate advance. The green upward-sloping support line is now pivotal — a decisive break beneath it, along with a drop below the late-2025 low of 3.947%, could push the 10-year yield down into the low 3% range.

10-Year Treasury Yield: Multi-Year Consolidation With Key Support at Risk (Log Scale). Chart courtesy of StockCharts.com.

In isolation, increasing exposure to Treasuries would be logical if yields break down and bond prices attract strong demand. But stepping back with an intermarket perspective, the bigger question becomes: what would that move signal for the broader financial markets?

A Potential Shift in the Stock–Bond Dynamic?

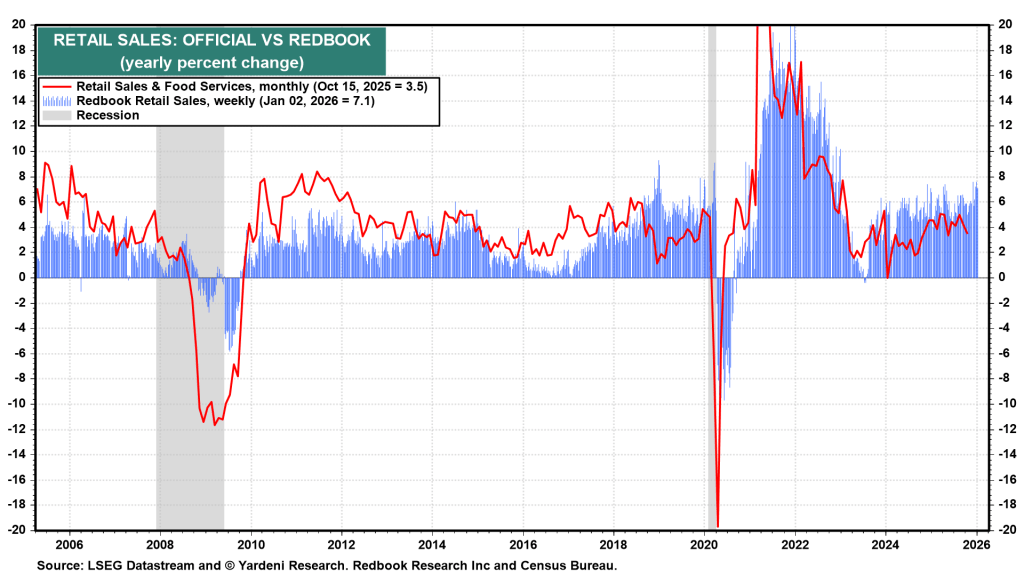

For stocks, a move toward 3–4% intermediate-term rates would likely coincide with softer economic conditions — perhaps a weak jobs report, sharply cooling CPI or PCE inflation, a downturn in sentiment indicators such as the ISM Manufacturing survey, or another disappointing Retail Sales release.

That said, with the fourth-quarter earnings season mostly wrapped up — including NVIDIA’s (NASDAQ: NVDA) results released Wednesday — it would probably take truly bleak off-season earnings updates or a wave of negative preannouncements to significantly rattle equities.

Another potential driver of a renewed bond bull market could be the ever-intensifying AI theme. In a “sell first, ask questions later” climate, fresh cautionary analyses or existential-impact discussions around artificial intelligence could further unsettle investors and sustain demand for safe-haven assets.

When Trading Ranges Start to Break Down

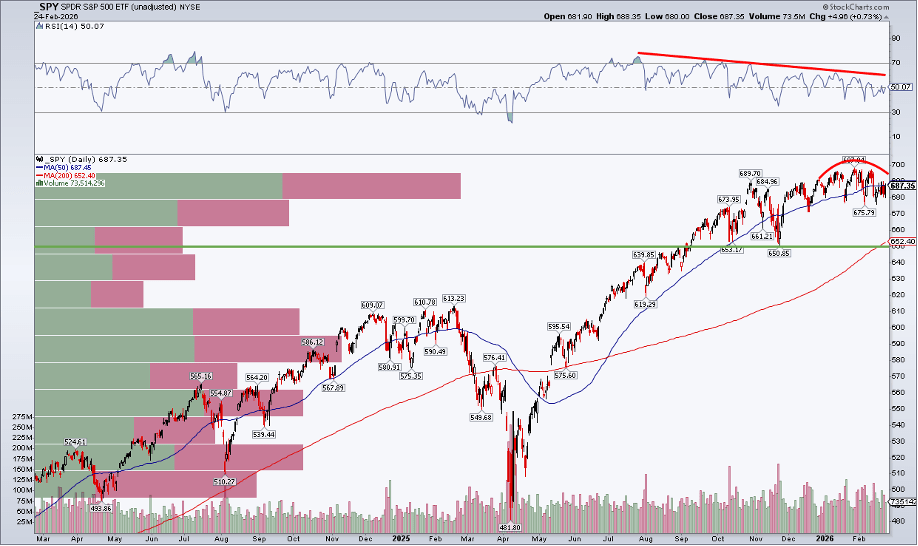

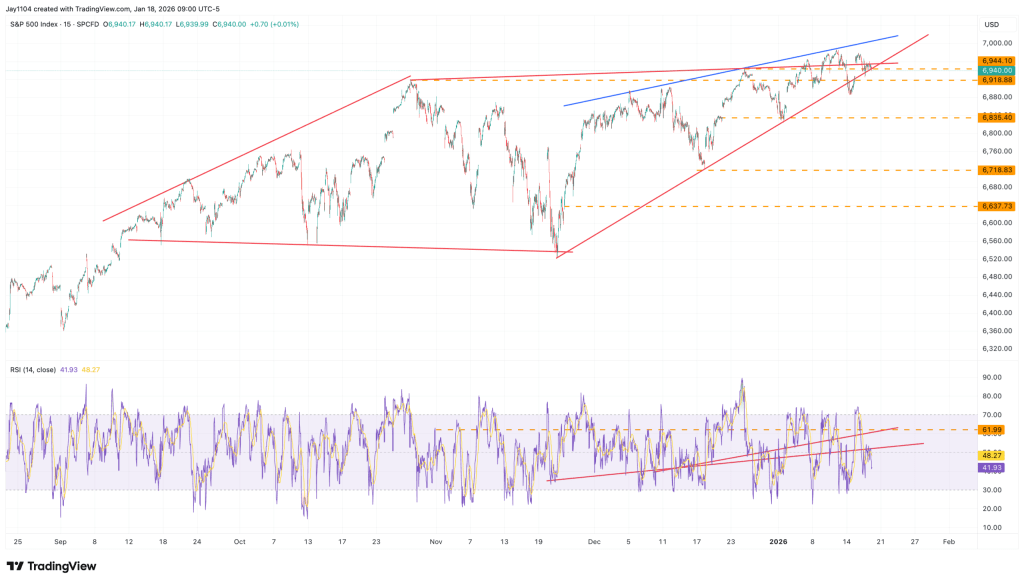

Regardless of the underlying catalyst, it’s evident that stocks and bonds are no longer moving in sync the way they did last spring and summer. The S&P 500 — like the 10-year Treasury yield — has been edging lower in recent weeks. We’re now nearly a month past the SPDR S&P 500 ETF Trust (SPY) intraday record of $697.84. Although much attention has focused on the tight trading range since late November, one could argue that a rounded-top formation is beginning to take shape.

A glance at the RSI momentum oscillator reinforces this view. Momentum has been trending lower since July. Much like a ball tossed into the air slows before changing direction, RSI often decelerates ahead of a price reversal. The unfolding narrative could be this: bond yields break down first — and equities eventually follow.

SPY: Emerging Rounded-Top Pattern, RSI Deteriorating, 200-Day Moving Average Around $650. Chart courtesy of StockCharts.com.

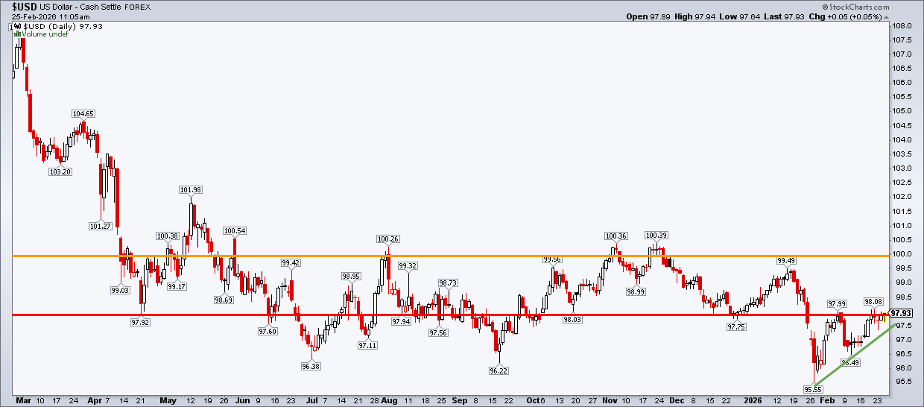

Don’t Overlook the Dollar

Largely flying under the radar is the US Dollar Index (USD). The greenback carved out a low near 95.55 around the same time U.S. large-cap equities peaked. Since then, the 98 level has surfaced as a potential breakout zone.

A setup featuring falling Treasury yields, declining stocks, and a strengthening dollar would reflect a classic risk-off macro environment. Based on a measured-move projection, the USD could target the 100 area — just shy of the zone where the dollar encountered resistance from May through November 2025.

US Dollar Index: Short-Term Ascending Triangle Pattern Points Toward 100. Chart courtesy of StockCharts.com.

The Bottom Line

Is this a doomsday forecast? Not at all. Market corrections are a normal part of the cycle. On average, the S&P 500 experiences an intra-year drawdown of about 14.2%, yet it has still finished higher in 35 of the past 46 years.

Rather than sounding alarms, this is simply a cross-asset check-in as we head into a month that has historically delivered heightened volatility. I tend to think of March as October’s little brother — price swings can become exaggerated. And with the CBOE Volatility Index still hovering around 20, disciplined risk management deserves to remain front and center.

The U.S. dollar recovered on Tuesday after the prior session’s slide, supported by upbeat economic data, while investors stayed cautious amid fresh volatility tied to President Donald Trump’s tariff policies.

At 15:24 ET (20:24 GMT), the Dollar Index—measuring the greenback against six major currencies—rose 0.2% to 97.86, after falling as much as 0.5% a day earlier.

Strong data underpin dollar

Encouraging economic releases lent the dollar some backing. ADP reported a gain of 12.8K in private payrolls last week, exceeding the previous reading. In addition, the Conference Board’s consumer confidence index for February surprised to the upside at 91.2.

According to José Torres, senior economist at Interactive Brokers, the stronger-than-expected figures nudged both the dollar and yields modestly higher, with a bear-flattening move led by shorter-dated maturities that are more sensitive to monetary policy.

He noted that firmer labor data are pushing rates up, as improving employment conditions weaken the case made by dovish Federal Reserve members for interest rate cuts based on softening job trends.

Trade tensions cloud outlook

Despite the rebound, uncertainty surrounds the U.S. currency as Trump’s revised tariff plans take shape following a Supreme Court ruling that his use of a 1977 emergency law to impose tariffs overstepped his authority.

In response, Trump said he would lift a temporary import tariff from 10% to 15% on goods from all countries. The move has cast doubt on the reliability of trade agreements reached prior to the ruling. Reflecting this uncertainty, the European Parliament delayed a vote on the European Union’s trade pact with the United States due to the new import tax.

Trade concerns have resurfaced at a time when questions are also emerging over the durability of heavy investment in artificial intelligence and the resilience of the U.S. economy after last week’s weak growth data.

Euro steady; Yen under pressure

In Europe, EUR/USD slipped 0.1% to 1.1779, with the euro largely steady after ECB President Christine Lagarde reiterated in Washington that the European Central Bank’s rate policy remains in a “good place,” while emphasizing the need for flexibility.

GBP/USD edged up 0.1% to 1.3501 ahead of parliamentary testimony from four Bank of England rate-setters, which may shape expectations before the March policy meeting.

In Asia, USD/JPY jumped 1% to 155.76 as expectations for near-term tightening by the Bank of Japan softened. The yen was also pressured by a Nikkei report suggesting U.S. authorities led recent rate-check efforts aimed at supporting Japan’s currency.

USD/CNY fell 0.4% to 6.8830 after the People’s Bank of China kept its one-year and five-year loan prime rates unchanged, signaling Beijing’s preference for calibrated support while balancing growth and financial stability. Chinese markets reopened Tuesday following the Lunar New Year holiday.

Elsewhere, AUD/USD rose 0.1% to 0.7060, while NZD/USD advanced 0.2% to 0.5967.

Thursday’s headline from the United States Department of Commerce showed the U.S. trade deficit widening sharply to $70.3 billion in December and reaching $901.5 billion for full-year 2025. December imports jumped 3.6% to $357.6 billion, while exports fell 1.7% to $287.3 billion. Economists had projected a $55.8 billion gap, making the release a significant downside surprise that prompted many to cut fourth-quarter GDP forecasts. Following the data, the Federal Reserve Bank of Atlanta lowered its Q4 GDP estimate to 3% from 3.6%.

The Commerce Department’s preliminary report showed the economy expanded at just a 1.4% annualized pace in Q4, well below the 2.8% consensus estimate. Federal government spending dropped 16.6% during the quarter — largely due to the shutdown — subtracting roughly one percentage point from growth. The wider trade deficit further weighed on output. For all of 2025, GDP rose 2.2%. Treasury yields drifted lower after the report, increasing expectations that the Federal Reserve may move toward another rate cut.

One potential obstacle to near-term easing is inflation. The Personal Consumption Expenditures (PCE) index rose 0.4% in December and 2.9% year-over-year. Core PCE, excluding food and energy, also climbed 0.4% on the month and 3% annually. On a positive note, consumer spending advanced 0.4% in December, offering some support for future growth momentum.

In financial markets, private credit came under scrutiny after Blue Owl Capital permanently restricted redemptions from one of its retail vehicles, Blue Owl Capital Corp II. The move triggered declines in alternative asset managers including Ares Management, Apollo Global Management, KKR, Blackstone, and TPG. Adding to concerns, BlackRock recently marked down portions of its private credit portfolio. Former PIMCO CEO Mohamed El-Erian publicly questioned whether this could signal a broader stress point for the sector.

In a separate development, The Wall Street Journal reported that President Donald Trump ordered the release of government files related to UFOs and unidentified aerial phenomena following heightened public interest. The directive reportedly came after comments by former President Barack Obama referencing extraterrestrial topics. Christopher Mellon, who previously helped publicize the “Tic Tac” military footage, suggested the move could have far-reaching implications.

Taken together, the combination of a widening trade deficit, softer GDP growth, persistent inflation, and emerging private credit strains presents a complex macro backdrop — one that leaves markets balancing expectations of further rate cuts against lingering structural risks.

When President Donald Trump returned to the White House in January 2025, he reaffirmed tariffs as the core instrument of his economic strategy — a blend of leverage, protectionism, and industrial revival. That strategy is now facing meaningful strain.

The recent ruling by the Supreme Court of the United States that Trump exceeded his authority in imposing sweeping global tariffs without congressional approval represents more than a procedural setback. It challenges the legal scaffolding underpinning a trade agenda that has shaped U.S. economic and foreign policy over the past year.

Markets have taken note — but without panic.

The contrast is notable. A defining pillar of presidential economic policy has been curtailed, yet equity markets remain resilient. Volatility has surfaced intermittently, but capital has not fled risk assets. Understanding this requires separating political drama from financial mechanics.

In theory, tariffs were meant to rebalance trade and accelerate reshoring. In practice, they largely operated as a cost-transfer mechanism. Importers absorbed part of the burden; consumers absorbed another portion through higher goods prices. Manufacturers dependent on global inputs faced margin compression. Retailers recalibrated pricing strategies. Supply chains, already strained in prior years, became more complex.

Economic data reflect this friction. Growth momentum has slowed from last year’s pace. Manufacturing surveys show uneven demand. Trade-sensitive capital expenditure has cooled. Meanwhile, inflation remains sticky — particularly in services — and goods categories exposed to import costs have seen renewed firmness. The anticipated mix of rapid expansion and stable prices has not materialized.

Markets, however, trade forward expectations — earnings trajectories and liquidity conditions — rather than political symbolism.

Large-cap U.S. equities continue to attract global capital, particularly in AI and advanced technology. Investment in semiconductors, cloud infrastructure, and computing capacity remains strong despite macro uncertainty. Earnings concentration in these sectors offsets weakness in more cyclical areas.

Investors see deceleration, not collapse. Corporate balance sheets remain broadly healthy. Employment is moderating but not deteriorating sharply. Financial conditions are tighter than in prior cycles, yet not restrictive enough to signal systemic stress.

Against this backdrop, a potential scaling back of tariffs introduces nuance rather than shock.

If trade barriers are diluted or subject to firmer congressional oversight, input costs could ease over time. That may gradually relieve goods-based inflation pressures. Supply chain planning could improve. Corporate forecasting may gain clarity — and clarity reduces risk premiums.

Bond markets reflect this balance. Treasury yields have fluctuated as investors weigh persistent inflation against moderating growth. Should tariff-driven price pressures fade, longer-term yields may stabilize. However, fiscal deficits and wage resilience continue to exert upward pressure. The tension remains unresolved.

Currency markets face competing forces. Reduced trade escalation could temper safe-haven demand for the dollar. Yet relative U.S. growth and yield differentials still offer structural support. Conviction remains limited.

Emerging markets are unlikely to move uniformly. Economies closely tied to U.S. demand may feel slower export momentum if domestic growth softens. Commodity exporters could benefit if inflation expectations anchor raw material prices at elevated levels. Capital allocation is becoming more selective.

None of this implies smooth conditions ahead.

Political backlash to the court’s decision could generate renewed volatility. Legislative countermeasures remain possible. Trade partners will recalibrate strategy in response to shifting U.S. authority.

Markets tend to resist escalation but adapt to adjustment.

Trump’s tariff strategy was presented as transformative. The measurable economic payoff has been less decisive. Growth has moderated, inflation has persisted, and structural trade imbalances remain largely intact.

Investors are pragmatic. A policy losing legal footing does not automatically trigger liquidation. If the outcome is reduced uncertainty and steadier price dynamics, equities can continue advancing even as political narratives fragment.

Cautious optimism defines the current tone.

Risk appetite remains conditional. A renewed acceleration in inflation would alter expectations quickly. A material deterioration in employment would challenge confidence. Fiscal expansion without corresponding growth would intensify long-term sustainability concerns.Markets are not celebrating policy unraveling — they are recalibrating probabilities.

The assessment is sober: an economy that is softer but not broken; inflation that is persistent but not runaway; profitability concentrated but durable in structurally advantaged sectors.Trade authority may now face clearer constitutional limits. Structural investment in innovation continues.

Capital ultimately flows toward earnings visibility and long-duration growth themes. Tariffs have dominated headlines. Technology and AI dominate capital expenditure.

Investors are adjusting exposure and preparing for volatility — but not retreating.The tariff agenda is under pressure. Financial markets, for now, are looking past it.

The U.S. dollar edged lower on Friday as investors digested the impact of the Supreme Court’s decision to invalidate President Donald Trump’s broad tariff measures. Despite the pullback, the greenback remained on track for its strongest weekly advance since November, supported by a more hawkish tone from the Federal Reserve and ongoing geopolitical tensions between the U.S. and Iran.

As of 17:31 ET (22:31 GMT), the Dollar Index slipped 0.2% to 97.72, though it was still poised to post a weekly gain of around 1%, its best showing in nearly three months.

The Supreme Court ruled 6–3 that Trump lacked authority under the International Emergency Economic Powers Act (IEEPA) to implement sweeping reciprocal tariffs. The president criticized the decision as “deeply disappointing” and indicated that tariffs would remain in effect through alternative legal channels, alongside a new 10% global levy.

According to Jeff Buchbinder of LPL Financial, removing the tariff overhang eliminates a drag on economic growth that had been expected to lift costs and pressure corporate margins. With that risk easing, growth may stabilize and inflation expectations embedded in bond markets could cool more quickly, potentially prompting a modest reassessment of Fed rate-cut expectations and weighing slightly on the dollar.

Even so, the dollar had attracted demand earlier in the week, underpinned by resilient U.S. economic data, hawkish Fed meeting minutes, and heightened Middle East tensions.

Friday’s data, however, delivered mixed signals. Core PCE — the Fed’s preferred inflation measure — rose 0.4% month-over-month and 3.0% year-over-year in December 2025, marking the highest annual reading since November 2023 and remaining well above the 2% target. Meanwhile, preliminary fourth-quarter GDP growth came in at 1.4%, falling short of the 2.8% consensus forecast.

In Europe, EUR/USD ticked up 0.1% to 1.1781, though the euro was still headed for a 0.7% weekly decline amid uncertainty surrounding ECB President Christine Lagarde’s tenure and softer German producer price data. Analysts at ING noted that while sentiment indicators such as the ZEW survey disappointed, the eurozone composite PMI is expected to stay above the 50 threshold, limiting downside pressure on the euro.

GBP/USD rose 0.1% to 1.3474, but sterling hovered near a one-month low and was set for a weekly loss of about 1.3%. Strong January retail sales — up 1.8% month-over-month and 4.5% year-over-year — failed to provide sustained support. ING analysts said markets are pricing in a Bank of England rate cut in March, with another possible move in June, while political risks continue to weigh on the pound.

In Asia, USD/JPY held steady at 155.06 after data showed Japan’s inflation slowed to 1.5% in January, slipping below the Bank of Japan’s target for the first time in nearly four years. Core inflation excluding fresh food and fuel also moderated, reinforcing uncertainty over the timing of the next rate hike. Separate data showed Japanese factory activity expanded at its fastest pace in over four years in February.

USD/CNY was unchanged at 6.9087, with Chinese markets closed. Meanwhile, AUD/USD climbed 0.5% to 0.70892, although the Australian dollar trimmed some gains after unemployment held at 4.1% in January, signaling a still-tight but gradually cooling labor market.

Here’s what you need to know for Friday, February 20:

The US Dollar Index (DXY) maintains its upward momentum, hovering near 98.00 after reaching a near one-month high on Thursday. The economic agenda for Friday features preliminary February Purchasing Managers’ Index (PMI) data from Germany, the Eurozone, the UK and the US. The spotlight, however, will be on the first estimate of fourth-quarter Gross Domestic Product (GDP) growth and the December Personal Consumption Expenditures (PCE) Price Index, both to be released by the US Bureau of Economic Analysis.

The US Dollar outperformed major peers on Thursday amid a risk-off market tone fueled by rising tensions between the US and Iran. According to BBC, US President Donald Trump warned that Iran must strike a deal or face serious consequences. Iran, in communication with UN Secretary-General Antonio Guterres, stated it does not seek conflict but would not tolerate military aggression. Iranian officials also reportedly cautioned that any US military move over the nuclear issue would be met with a decisive response. Early Friday, US stock index futures were modestly higher.

The US economy is expected to have expanded at an annualized pace of 3% in Q4, following a 4.4% increase in the prior quarter. Meanwhile, the core PCE Price Index — the Federal Reserve’s preferred inflation gauge — is forecast to rise 2.9% year-over-year in December, up slightly from 2.8% in November.

EUR/USD, which closed lower on Thursday, remains under pressure early Friday, trading near 1.1750. PMI figures from Germany and the Eurozone are anticipated to continue signaling expansion in private-sector activity for February.

GBP/USD extended its decline for a fourth straight session on Thursday and trades below 1.3450, marking its weakest level since late January. Data from the UK’s Office for National Statistics showed that Retail Sales climbed 1.8% month-over-month in January, significantly beating the 0.2% consensus estimate.

USD/JPY continues its weekly advance and holds comfortably above 155.00 in early Friday trading. Japan’s Prime Minister Sanae Takaichi stated that necessary expenditures would largely be financed through the initial budget, adding that efforts would be made to gradually reduce the debt-to-GDP ratio and restore fiscal discipline. Japan’s National Consumer Price Index rose 1.5% in January, down from 2.1% in December.

Gold benefited from safe-haven demand on Thursday but struggled to build momentum amid broad USD strength. XAU/USD edges higher during the European session on Friday, trading above $5,000.

In Australia, flash data from S&P Global showed the Composite PMI easing to 52 in February from 55.7 in January. AUD/USD largely brushed off the release and was last seen slightly lower on the day near 0.7050.

Most Asian equities declined on Friday as mounting uncertainty over the U.S. interest-rate outlook and escalating tensions surrounding Iran dampened appetite for risk assets.

South Korea stood out as a bright spot, with the KOSPI surging to fresh record highs on sustained optimism in domestic markets following a recent tech-led rally.

Regional bourses tracked overnight losses on Wall Street, where a wave of risk-off sentiment pressured stocks. S&P 500 Futures edged up 0.16% by 22:37 ET (03:37 GMT), as investors awaited key inflation and growth data due later in the session. Chinese markets remained shut for the Lunar New Year holiday.

Japan slides despite mixed data; Hong Kong retreats after break

In Japan, the Nikkei 225 and TOPIX were the region’s weakest performers, falling 1.4% and 1.2%, respectively.

Shares came under pressure following mixed economic releases. Data showed Japan’s headline consumer price index slowed to its lowest level in nearly four years in January, while core inflation also eased but remained above the Bank of Japan’s 2% annual target.

Meanwhile, purchasing managers’ index figures indicated factory activity expanded to a four-year high in February, supported by firm overseas demand.

Hong Kong’s Hang Seng Index fell 0.6% as trading resumed after a three-day holiday, with local technology stocks mirroring earlier global declines.

Among the laggards were Alibaba Group and Baidu Inc, which tumbled between 4% and 6% after being briefly named on a U.S. government list of firms allegedly linked to the Chinese military. BYD Co, also cited in the list, slipped 1.6%.

Elsewhere, markets were subdued. Australia’s S&P/ASX 200 dipped 0.2%, Singapore’s Straits Times Index edged up 0.1%, and India’s Nifty 50 was little changed, with local tech shares remaining cautious despite reports of new artificial intelligence ventures.

Risk sentiment remained fragile after U.S. President Donald Trump gave Iran a 10–15 day deadline to reach a nuclear agreement or face potential U.S. action, with multiple reports suggesting further strikes were under consideration.

South Korea outperforms as KOSPI hits record

South Korea’s KOSPI bucked the regional trend, climbing more than 1.6% to a record 5,768.61 points and marking its second straight session at an all-time high.

While Thursday’s gains were driven by technology stocks, Friday’s advance was led by strong performances in brokerage, defense, and insurance names.

Local media reported a surge in buying by retail investors, even as foreign investors continued to pare holdings.

Separately, South Korea’s top court on Thursday sentenced former President Yoon Suk-Yeol to life imprisonment over charges linked to an attempted insurrection in late 2024.

Inflation came in cooler than anticipated in January, though markets still largely expect the Federal Reserve to hold its benchmark rate steady until June. However, the bond market appears ready to test that timeline, increasingly factoring in the possibility of a rate cut arriving sooner.

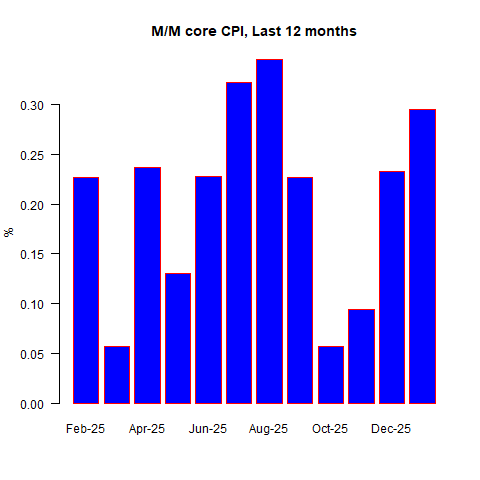

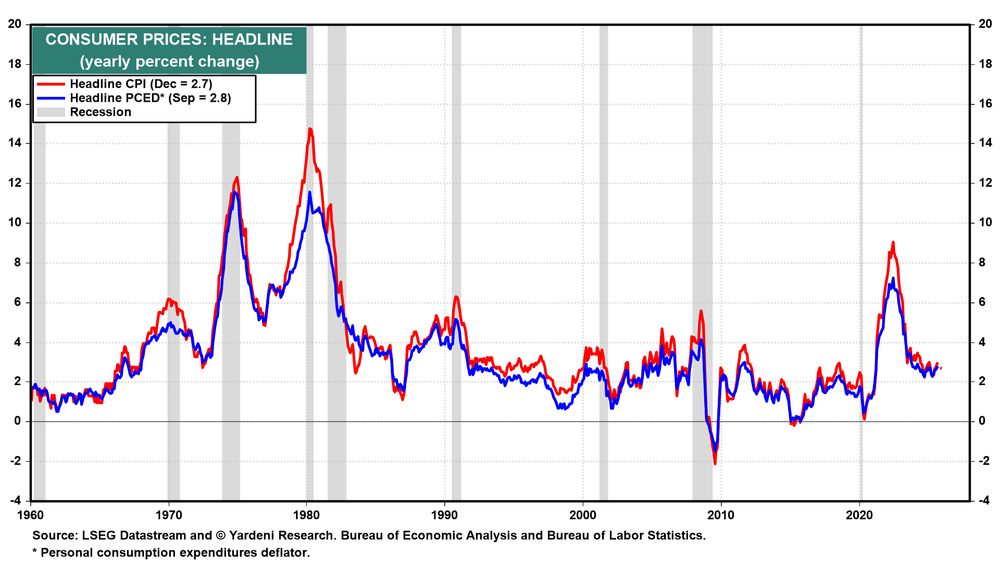

According to government data released Friday, the Consumer Price Index (CPI) rose 2.4% year over year in January, down from 2.7% in December and marking the lowest reading in eight months. Core CPI—which excludes volatile food and energy prices and is considered a clearer gauge of underlying inflation—also eased to 2.5% annually, its slowest pace since 2021.

While the slowdown in headline inflation is a welcome development, a deeper dive into the data suggests it may be premature to relax concerns about where prices are headed next. Persistent increases in tariff-sensitive goods remain one pressure point. Food prices are another, climbing 2.9% year over year—elevated by historical standards.

Energy costs rose even more sharply, and both homeowners’ and renters’ insurance premiums continued to increase. Moreover, inflation is still running above the Federal Reserve’s 2% target, reinforcing the likelihood that policymakers will proceed carefully.

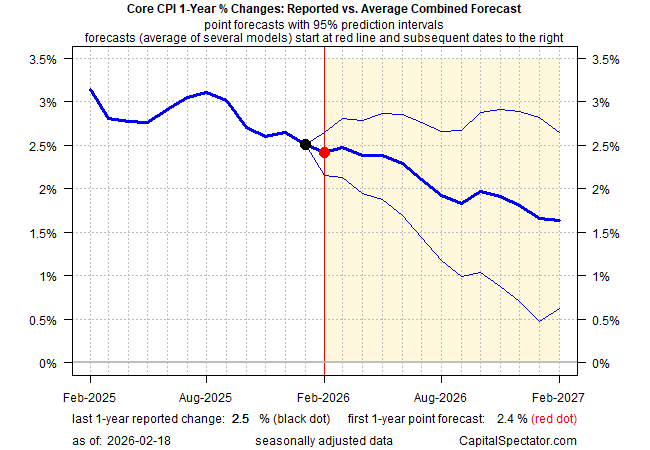

Although it’s too soon to claim inflation has been fully tamed, the broader trend of moderating price growth strengthens the argument that the worst may be behind us. The Capital Spectator’s ensemble forecast has long projected continued disinflation in core CPI, a view that has so far aligned reasonably well with actual data. The model still anticipates further easing, with core CPI’s 12-month rate expected to edge down to around 2.4% in the upcoming February report.

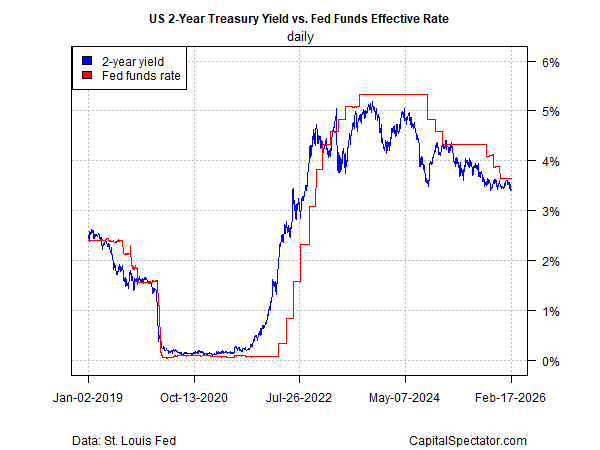

Fed funds futures continue to indicate that the first rate cut won’t arrive until the June meeting. In contrast, the Treasury market appears to be probing the possibility of an earlier move. The policy-sensitive 2-year Treasury yield has fallen to about 3.45%—near its lowest level since 2022—and now sits below the Federal Reserve’s current target range of 3.50% to 3.75%, signaling that bond investors may be anticipating a faster shift in policy.

In short, Treasury market sentiment is tilting toward the idea that a rate cut could come sooner than previously anticipated. Other market-based indicators are reinforcing that view by assigning higher odds to continued disinflation.

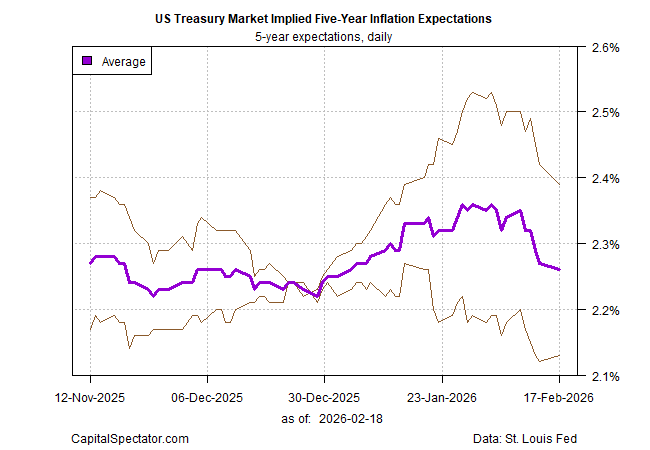

The average of two Treasury-derived inflation gauges now projects five-year inflation in the low 2% range—the mildest reading in a month and not far from the Federal Reserve’s 2% objective. The surge in inflation expectations seen in January has since unwound, signaling that investors have grown less worried about upside inflation risks in recent weeks.

Markets are not infallible, but it would likely require a meaningful upside surprise in the economic data—pointing to renewed inflationary pressure—to overturn the prevailing disinflation narrative. For now, investors show little appetite for betting on a reflationary turn.

USD/JPY is consolidating Wednesday’s strong advance, hovering near the 155.00 mark early Thursday. The bullish bias remains intact as concerns over Japan’s fiscal outlook and a generally positive market sentiment continue to weigh on the safe-haven Japanese Yen.

At the same time, the latest FOMC Minutes revealed divisions among Fed officials regarding the need and timing of additional rate cuts amid lingering inflation risks. This uncertainty lends support to the US Dollar, providing an added tailwind for the pair.

USD/JPY Technical Overview

The US Dollar (USD) is trading with a mild bullish bias against the Japanese Yen (JPY) this week, hovering near the top of the 153.00 range. However, the pair remains confined within its weekly boundaries, as resistance around 154.00 continues to cap upside attempts ahead of the release of the minutes from the US Federal Reserve’s latest meeting.

Fundamental Overview

The Federal Reserve kept its benchmark rate unchanged at 3.5%–3.75% and signaled that policy is likely to remain steady in the near term. The meeting minutes are expected to underscore divisions within the committee—differences that are drawing added attention after last week’s softer U.S. inflation data and disappointing jobs report.

On Tuesday, Chicago Fed President Aistan Goolsbee pointed to those internal splits, noting that if inflation continues to ease, the central bank could lower rates multiple times this year.

In Japan, weak fourth-quarter GDP data released Monday have renewed worries about the country’s economic prospects, reinforcing Prime Minister Sanae Takaichi’s push for substantial fiscal stimulus and tax cuts.

Meanwhile, the International Monetary Fund cautioned that reducing the consumption tax could strain public finances and urged the Bank of Japan to tighten monetary policy further to keep inflation in check. As a result, the yen’s recent bullish momentum has faded somewhat, offering relief to the previously pressured U.S. dollar.

GBP/USD is struggling to stage a meaningful rebound after dropping to a four-week low in Thursday’s Asian session, with the pair hovering just below the 1.3500 psychological level and appearing vulnerable to further losses. It is currently consolidating declines recorded over the past three days within a tight range near weekly lows.

The British pound remains under pressure amid growing expectations that the Bank of England will deliver a rate cut at its March meeting. Those bets were reinforced by weaker UK employment data and a slowdown in consumer inflation to its lowest level in nearly a year. Combined with a firm US dollar, this keeps the near-term bias tilted to the downside for GBP/USD.

Meanwhile, minutes from the Federal Reserve’s January meeting revealed divisions among policymakers regarding the timing and need for additional rate cuts, given persistent inflation concerns. While some officials signaled that easing could be appropriate if inflation continues to cool, others warned that premature cuts might jeopardize the Fed’s 2% target. The relatively less dovish tone has helped underpin the US dollar.

Geopolitical tensions also remain in focus, with reports suggesting the US military could be ready to strike Iran as soon as this weekend. Such risks have supported safe-haven demand for the greenback, allowing it to hold onto recent gains and reinforcing the case for an extension of the pair’s weekly downtrend. Any attempted recovery in GBP/USD may therefore attract fresh selling interest.

Traders now turn to Thursday’s US data releases, including weekly initial jobless claims, the Philadelphia Fed Manufacturing Index, and pending home sales. Speeches from key FOMC members are also due later in the North American session, though attention will ultimately center on Friday’s US Personal Consumption Expenditures (PCE) Price Index for clearer policy direction.

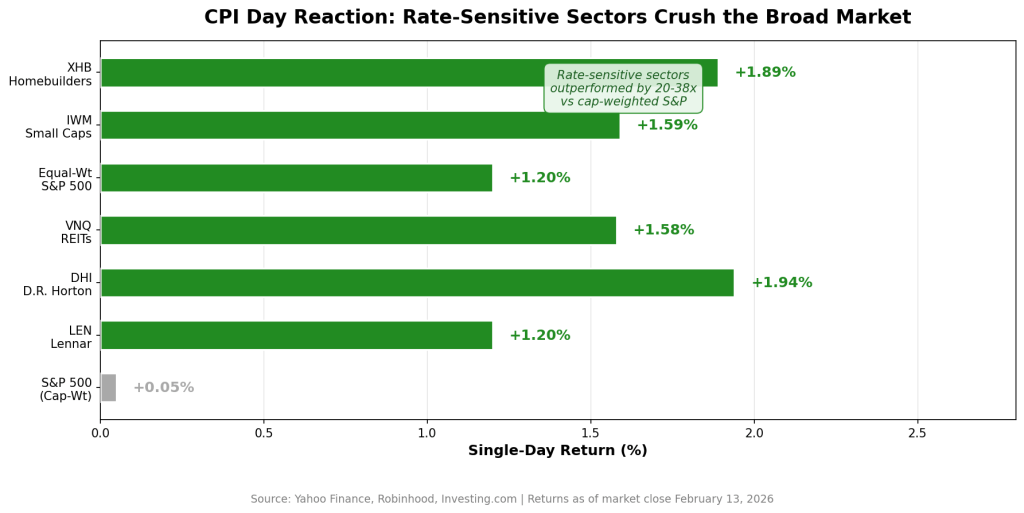

The inflation print investors had been bracing for came in cooler than expected.

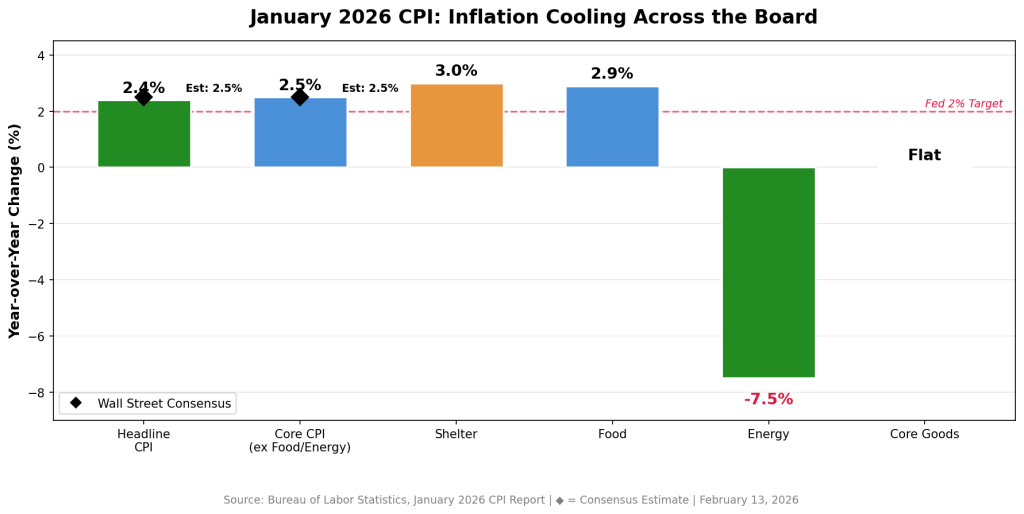

Friday’s January CPI showed headline inflation at 2.4%—below the 2.5% consensus forecast and the lowest annual reading since May 2025. Core CPI, which excludes food and energy, eased to 2.5%, marking its softest level since April 2021. On a monthly basis, prices rose just 0.2%, the smallest increase since July.

Markets reacted swiftly. Homebuilder stocks rallied sharply, small caps climbed 1.2%, and the 10-year Treasury yield slid to its lowest point since early December.

My takeaway: the market may have just received the confirmation it was waiting for. And the most compelling opportunities from here likely aren’t the mega-cap tech leaders that have dominated performance, but rather rate-sensitive sectors that were punished under the “higher for longer” narrative and are now repricing for a potentially different 2026 backdrop.

What the CPI Report Really Signals

Shelter—by far the largest CPI component and the category that has stubbornly kept headline inflation elevated—rose only 0.2% in January, bringing the annual rate down to 3%. That’s a notable slowdown and perhaps the clearest indication yet that the housing inflation lag is beginning to unwind.

Energy prices declined 1.5%, with gasoline tumbling 3.2% during the month. Food inflation held at 2.9% year over year—still somewhat elevated, but not alarming. Importantly, core goods prices were flat, helping to counter concerns that renewed tariffs would reignite goods inflation.

“Headline CPI inflation was a touch softer than expected in January, delivering a welcome surprise to the downside at the beginning of the year,” said Bernard Yaros, lead economist at Oxford Economics. He added that tariff-related price pressures “are largely behind us.”

Lindsay Rosner of Goldman Sachs Asset Management was even more direct: “Trust the groundhog. The Fed’s path to normalization cuts appears clearer now.”

The timing is critical. A stronger-than-expected January jobs report—130,000 payrolls versus forecasts of 55,000—had pushed expectations for rate cuts further out, likely into the summer. This softer CPI reading shifts that outlook. Economists surveyed by Bloomberg now anticipate as much as 100 basis points of easing this year, with the first cut potentially arriving in June—or even March if disinflation continues.

Why Rate-Sensitive Stocks Stand Out

One key dynamic investors often overlook is that by the time the Federal Reserve actually begins cutting rates, much of the upside in rate-sensitive sectors has already played out. Markets tend to price in policy shifts well in advance.

Friday’s CPI data appeared to give institutional investors the confidence to begin reallocating toward sectors poised to benefit from lower yields. The equal-weight version of the S&P 500 and the Russell 2000 both climbed 1.2%, notably outperforming the traditional cap-weighted S&P 500, which was little changed.

That divergence is often viewed as a textbook signal of sector rotation—away from mega-cap dominance and toward more rate-sensitive, economically cyclical areas of the market.

Capital is rotating down the market-cap ladder and into economically sensitive groups. Three segments stand out most clearly: homebuilders, REITs, and small caps.

How to Position

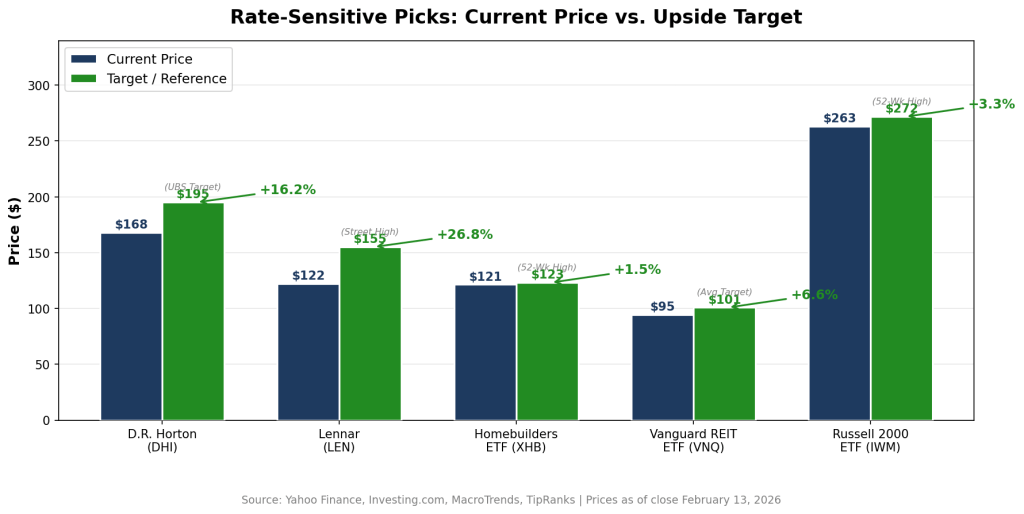

D.R. Horton (DHI)

Closing Friday at $167.78, DHI is arguably the purest expression of the housing-affordability theme. The largest U.S. homebuilder by volume posted solid fiscal Q1 results in January, with revenue of $6.89 billion (ahead of $6.59 billion estimates) and EPS of $2.03 (vs. $1.93 expected).

At roughly 15.3x trailing earnings, the stock trades at a notable discount to the broader market. Beyond the rate backdrop, there’s also a policy angle: the Trump administration’s reported “Trump Homes” initiative has involved direct engagement with builders around affordability measures—potentially creating a dual tailwind of lower mortgage rates and regulatory support.

The median analyst price target is $170, with UBS as high as $195—suggesting upside potential of roughly 16%.

Lennar (LEN)

Trading at $122.28, Lennar offers a slightly different profile as the second-largest U.S. builder. Its “land-light” model—optioning land instead of holding it outright—reduces balance-sheet risk and positions it well for a rate-cutting cycle.

The stock has rebounded about 40% from its April 2025 lows but remains below its 2024 peak. With fiscal Q1 earnings due in late March, improving mortgage application trends could serve as a near-term catalyst if rates continue to ease.

SPDR S&P Homebuilders ETF (XHB)

At $121.36, XHB is up nearly 18% year-to-date and recently marked a fresh 52-week high of $123.13. As an equal-weighted ETF, it offers diversified exposure across the housing ecosystem—not just large builders, but also building products manufacturers, home improvement retailers, and construction suppliers.

For investors who prefer sector exposure over single-stock risk, XHB provides a balanced approach.

Vanguard Real Estate ETF (VNQ)

Trading near $94.59—close to its 52-week high—VNQ provides broad exposure to the REIT space, one of the most rate-sensitive areas of the market. The ETF holds over 150 REITs across healthcare, industrial, data center, and retail subsectors.

Its largest holdings include Welltower, Prologis, and American Tower.

With an average analyst target near $100.81, implied upside sits around 8%, in addition to a dividend yield of roughly 3.6%. After significant underperformance during the rate-hiking cycle, REITs are positioned to benefit mechanically as yields decline.

iShares Russell 2000 ETF (IWM)

At approximately $263, IWM tracks small-cap equities—arguably the most interest-rate-sensitive segment of the equity market. Smaller firms tend to carry more floating-rate debt and are disproportionately affected by elevated borrowing costs. That dynamic can reverse sharply when policy eases.

IWM surged 1.6% on Friday’s CPI release alone. With its 52-week high of $271.60 within reach, sustained rate declines could drive a prolonged catch-up rally in small caps.

The Big Picture

If inflation continues to moderate and rate-cut expectations firm, the leadership baton may continue shifting away from mega-cap growth and toward housing, real estate, and smaller domestically oriented companies. Markets typically front-run the policy cycle—and this rotation suggests that repositioning may already be underway.

The Bear Case (and Why It May Be Overstated)

There are valid reasons for caution. Fox Business pointed out that January’s CPI could carry a downward bias tied to last fall’s government shutdown. During that period, the Bureau of Labor Statistics missed portions of October data collection and relied on a “carry-forward” methodology that may influence inflation readings into spring 2026. In short, the 2.4% headline figure could be somewhat understated.

There’s also the Federal Reserve itself. Policymakers are not signaling urgency. Oxford Economics continues to project cuts in June and December rather than March. Meanwhile, although the labor market is cooling—annual benchmark revisions show 2025 job growth was the weakest since 2003 outside recessionary periods—it is far from collapsing. Jerome Powell has consistently emphasized the need for a sustained disinflation trend, not a single favorable report.

The Counterargument

Even if the Fed waits until June, markets won’t. Yields have already declined meaningfully. Mortgage rates are edging lower. And sectors that trade on rate expectations—rather than the actual fed funds rate—are beginning to reprice now. By the time the first official cut arrives, much of the move in rate-sensitive equities could already be behind us.

What to Watch

Three near-term catalysts will likely shape the next phase:

Fed Minutes (Feb. 18): The release of the latest policy meeting minutes could shift expectations quickly. Any dovish commentary on inflation progress or labor-market softness may pull forward rate-cut pricing.

Walmart Q4 Earnings (Feb. 19): As the largest U.S. retailer—now with a market cap above $1 trillion and up 13% year-to-date—Walmart’s guidance will offer real-time insight into consumer spending trends. If easing inflation is translating into stronger purchasing power, that reinforces the soft-landing narrative.

PCE Price Index (Later This Month): The Fed’s preferred inflation gauge will be pivotal. Confirmation of CPI’s cooling trend would likely solidify expectations for a June cut and intensify debate around a possible March move—potentially fueling the next leg higher in rate-sensitive stocks.

Bottom Line

The inflation backdrop has shifted in a way that favors investors. The opportunity isn’t complex—but it does require stepping away from the mega-cap tech trade that has dominated for the past two years and leaning into sectors positioned to benefit most from falling yields.

Here’s what you need to know for Monday, February 16:

Major currency pairs begin the week trading within established ranges, as investors remain cautious ahead of several key events and important macroeconomic releases scheduled for later in the week. In Europe, December Industrial Production figures are due on Monday. Meanwhile, US stock and bond markets are closed for the Presidents Day holiday.

The US Dollar Index ended last week on a softer note, as below-forecast inflation data prevented the greenback from gaining momentum before the weekend. According to the US Bureau of Labor Statistics, annual Consumer Price Index (CPI) inflation slowed to 2.4% in January from 2.7% in December, undershooting expectations of 2.5%. Early Monday, the USD Index is moving sideways around the 97.00 mark during European trading hours.

Early Monday, CBS News reported—citing two sources—that US President Donald Trump told Israeli Prime Minister Benjamin Netanyahu he would back Israeli strikes targeting Iran’s ballistic missile program. So far, markets have shown little reaction, with West Texas Intermediate crude trading largely flat near $62.80 per barrel.

EUR/USD remains in consolidation mode, hovering just above 1.1850 after ending last week slightly higher. European Central Bank policymaker Joachim Nagel is expected to speak later in the day.

In Asia, Japan’s data showed that fourth-quarter Gross Domestic Product (GDP) expanded at an annualized rate of 0.2%, rebounding from a 2.6% contraction in the prior quarter but missing the 1.6% growth forecast. After dropping nearly 3% last week, USD/JPY is recovering modestly, up 0.4% on the day to trade near 153.30.

AUD/USD trades in a tight range below 0.7100 in European hours. The Reserve Bank of Australia will release minutes from its February meeting early Tuesday, when it raised the policy rate by 25 basis points to 3.85%.

Gold surged on Friday and closed the week higher, though XAU/USD is struggling to maintain upward momentum and is trading below the $5,000 level on Monday morning in Europe.

The UK’s Office for National Statistics is set to publish employment data on Tuesday. GBP/USD remains subdued, edging slightly below 1.3650.

Finally, Statistics Canada will release January CPI data on Tuesday. USD/CAD trades steadily around 1.3600 in European hours after posting modest losses last week.

The US Dollar (USD) posted notable weekly losses, briefly rebounding after stronger-than-expected US jobs data showed 130K new positions added in January and the Unemployment Rate dipping to 4.3% from 4.4%. However, softer January CPI figures pressured the currency.

The US Dollar Index (DXY) slipped to around 96.80 from 97.15 highs as weak inflation data boosted expectations of a Federal Reserve rate cut later this year. Attention now turns to Friday’s release of the December Personal Consumption Expenditures (PCE) report, the Fed’s preferred inflation measure.

EUR/USD hovers around 1.1880, erasing earlier losses after Eurozone flash Q4 GDP came in at 1.4% YoY, above the 1.3% forecast. Focus next week includes the Eurogroup Meeting and December Industrial Production on Monday, followed by the EcoFin Meeting and February Eurozone and German ZEW Surveys on Tuesday.

AUD/USD trades near 0.7080, close to a three-year peak, supported by the hawkish stance of the Reserve Bank of Australia. Upcoming data include NAB Business Confidence and the Wage Price Index on Wednesday, then Australian jobs figures and the February flash S&P Global Composite PMI on Thursday.