- Gold’s recent pullback appears more like a healthy normalization than a sign of underlying weakness.

- Its outsized outperformance versus equities had become increasingly difficult to maintain.

- For investors, the key issue now is whether the correction has brought valuations back to more attractive levels.

Gold prices have recently taken many investors by surprise. After a powerful rally earlier this year, much of the optimism surrounding the metal has faded. Since the start of the year, gold has declined by roughly 5.6% — despite an environment marked by geopolitical tensions, persistent inflation concerns, and renewed demand for defensive assets.

Under normal circumstances, these conditions would strongly support higher gold prices. This time, however, the market has behaved differently. Gold has retreated while equities have regained momentum, leaving investors wondering whether the earlier rally simply became excessive.

In the short term, the answer appears to be yes.

Gold had significantly outperformed equities, reaching relative strength levels not seen in nearly two decades. When such a gap becomes too extreme, markets often respond in a familiar way: the trend reverses — rapidly, sharply, and with little warning.

The recent decline does not necessarily suggest that gold itself has become fundamentally weak. Rather, it may indicate that the metal had previously become too strong relative to other asset classes.

At first glance, the pullback seems difficult to explain. Ongoing geopolitical risks, inflation pressures, and broader uncertainty would typically favor safe-haven assets like gold. Yet markets are not driven solely by fundamentals; they also depend heavily on expectations and positioning.

And that is where the issue emerged.

Gold had become exceptionally stretched relative to the S&P 500. Investors comparing gold against U.S. equities could clearly see that the performance gap had widened to historically unusual levels — a divergence that became increasingly difficult for markets to ignore.

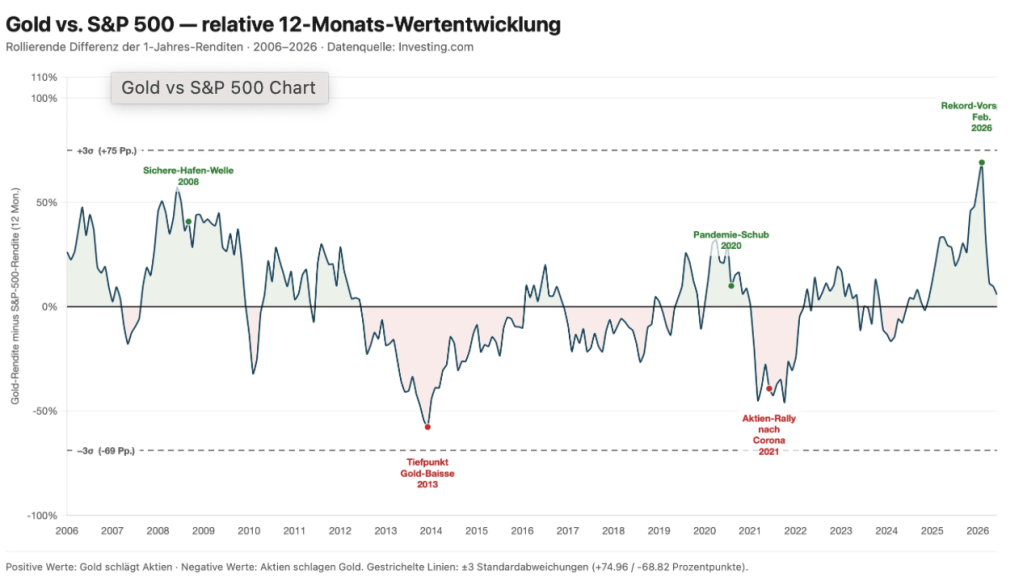

A review of the rolling one-year relative performance between gold and the S&P 500 since 2006 makes the relationship especially clear. Whenever gold sits above equities, the precious metal has outperformed over the previous twelve months. When it falls below, stocks have delivered stronger returns.

Over this period, gold outperformed the S&P 500 by an average of 3.1 percentage points across rolling 12-month windows and led equities in roughly 56% of those periods. On the surface, that appears impressive. Yet the more important detail lies beneath the averages.

The advantage was relatively modest, while the swings were extremely large.

The standard deviation of gold’s relative performance reached around 24 percentage points. In practical terms, that means gold can outperform stocks by more than 27 percentage points in a year — or underperform by roughly 21 percentage points — and both outcomes would still fall within historical norms.

This is where many investors misjudge the gold market. Gold does not steadily and consistently outperform equities. Instead, it moves in cycles. There are periods when it dramatically outshines stocks, and others when it underwhelms for years at a time.

Gold vs. Stocks: Where Investors Often Miscalculate

Many investors treat gold as a permanent hedge against every form of uncertainty. Economic crisis? Buy gold. Inflation? Buy gold. Geopolitical risk? Buy gold. But markets rarely work in such a straightforward way.

Gold tends to perform best when confidence in risk assets weakens. During the 2008–2009 financial crisis, for example, the metal benefited as investors sought safety while equity markets struggled.

The environment between 2013 and 2019 looked very different. During those years, equities significantly outperformed while gold delivered relatively disappointing returns for an extended period.

This highlights an important point: gold is not a guaranteed return enhancer. It is a cyclical asset. And that cyclical nature is exactly what gives it value within a diversified portfolio.

Gold’s greatest strength is not necessarily its ability to beat stocks over time, but rather the fact that it often behaves differently from them. Since 2006, the correlation between monthly gold returns and the S&P 500 has been only around 0.07, suggesting that the two asset classes move largely independently.

Gold’s Extreme Lead Became a Warning Sign

The divergence became particularly pronounced around the turn of 2025/26, when gold’s outperformance relative to the S&P 500 surged to roughly 69 percentage points — the largest gap seen in about two decades.

That level no longer represented a normal market move. It reflected an extreme.

Gold was approaching the upper three-sigma threshold near 75 percentage points, implying that the metal had become historically overstretched relative to equities. It was no longer simply expensive or overheated; it had entered territory where caution became increasingly necessary.

The correction that followed was therefore not entirely surprising.

Since its peak, gold has fallen by roughly 23%, while the S&P 500 gained around 6% over the same period. Much of gold’s extraordinary lead disappeared rapidly — a classic example of mean reversion in financial markets.

For investors, the lesson is important. Once an asset has rallied excessively, a compelling long-term narrative alone is no longer enough to sustain prices indefinitely. At some stage, optimism becomes overly priced in, and markets begin to rotate toward relatively more attractive opportunities elsewhere.

Gold Is Moving Back Toward Historical Norms

At present, gold’s 12-month outperformance versus the S&P 500 has narrowed to roughly 6 percentage points, much closer to the long-term average of 3.1 percentage points.

Very little remains of the extreme divergence seen earlier in the year. The previous overextension has already been substantially corrected — and far more quickly than many investors anticipated.

That is what makes the current environment particularly interesting. Investors focusing only on the recent decline may conclude that gold has suddenly turned weak. In reality, the market may simply be witnessing a normalization after an unusually powerful rally.

Gold’s Long-Term Case Remains Intact

Despite the recent correction, gold’s long-term performance remains stronger than many assume. Since 2006, gold prices have risen by approximately 616%, compared with roughly 470% for the S&P 500 on a price-only basis.

However, this comparison requires context. Dividends are excluded from the S&P 500 figure, and over nearly two decades dividend reinvestment makes a substantial difference.

On a total-return basis, including dividends, equities still hold a slight advantage. That is why it would be misleading to declare gold the definitive long-term winner.

Stocks possess structural advantages that gold lacks. Companies generate earnings, expand operations, reinvest capital, buy back shares, and distribute dividends. Gold does none of these things. Its value is driven primarily by scarcity, investor confidence, and supply-demand dynamics.

That is also why gold should not be viewed as a replacement for equities, but rather as a complement to them within a broader portfolio strategy.

Why Gold Still Deserves Attention

In the near term, gold could continue losing relative ground to equities after its exceptional outperformance. Over the next six to twelve months, there are reasonable arguments that stocks may continue to narrow the gap further.

Yet the long-term structural backdrop for gold remains supportive.

One major factor is central bank demand. Around the world, central banks continue diversifying reserves away from U.S. Treasury assets, with gold playing a central role in that process. Unlike sovereign debt, gold is politically neutral, finite in supply, and globally recognized as a store of value.

Importantly, this is not a short-term trend. Reserve allocation shifts typically unfold over many years, creating a persistent structural source of demand for the precious metal.

Geopolitical uncertainty, inflation concerns, and broader questions surrounding long-term currency stability also continue to support gold’s strategic relevance within portfolios.

Still, valuation matters.

Investors buying after an extended rally often need considerable patience. Those evaluating gold after a meaningful correction may once again find a more balanced risk-reward setup. That is precisely why the current phase in the gold market deserves closer attention.

Leave a comment