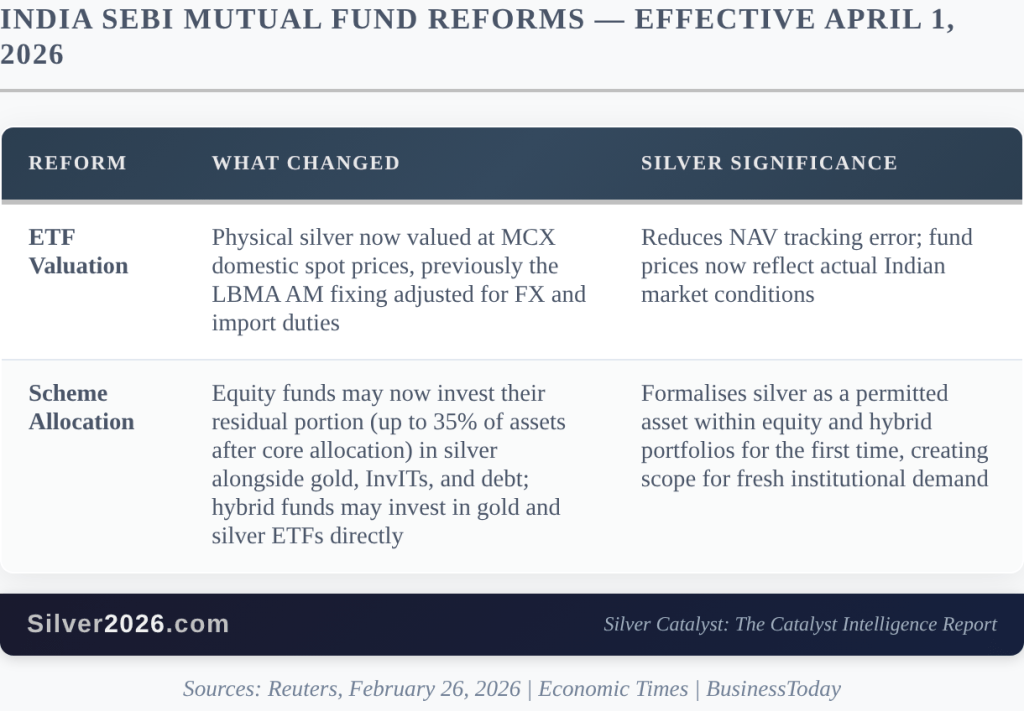

For the first time, India’s mutual fund industry is now permitted to include silver within equity and hybrid portfolio structures, marking a significant shift in asset allocation options.

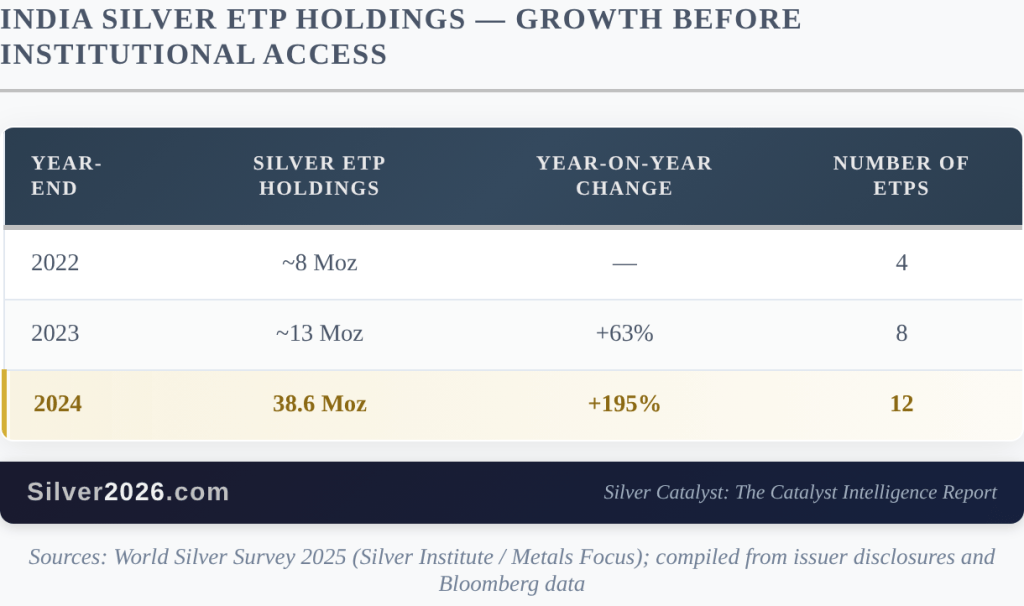

To put this into perspective, India is already the world’s most silver-intensive consumer market in bullion and investment demand. Silver imports reached a record 247.4 million ounces (Moz) in 2024, while holdings in silver ETFs surged about 195% year-on-year—from roughly 13 Moz at the end of 2023 to 38.6 Moz by the end of 2024, nearly tripling within a single year. This growth reflects a deeply rooted cultural preference for silver that is not matched in most Western markets.

Despite this strong demand base, India’s large institutional capital pools previously had no scalable or direct route to allocate to silver ETFs through standard equity and hybrid fund structures.

As of April 1, 2026, that constraint has been lifted.

What SEBI Has Changed and Why It Is Important

India’s Securities and Exchange Board of India has officially introduced two linked reforms today, reshaping the way mutual funds in India are able to invest in silver.

The valuation change is largely technical but still important: funds benchmarked to the London price previously traded at a persistent divergence from actual silver prices in Mumbai. That spread acted as a structural barrier to institutional participation. Its removal effectively eliminates an arbitrage that had made silver ETF exposure in India less precise for fund managers.

The allocation change, however, is the more consequential structural shift.

India’s mutual fund industry manages around ₹82 trillion (about $950 billion) in assets under management as of February 2026. Equity and hybrid schemes form the largest segment. Before this reform, these schemes were not permitted to allocate to silver at all. The new framework changes that, though access is limited to the residual allocation bucket—assets left after meeting core equity or hybrid mandates—capped at 35% and shared among gold, InvITs, and debt instruments as competing options.

To put the scale in perspective:

- A 0.1% allocation from equity and hybrid AUM into silver ETFs would translate to roughly $950 million in new demand, or about 13 Moz at current prices.

- A 0.5% allocation would imply around $4.75 billion, or approximately 65 Moz.

- A 1.0% allocation would equate to about $9.5 billion, or roughly 130 Moz.

These figures represent potential scale rather than immediate inflows; actual deployment will depend on how quickly fund managers adopt the new flexibility and is expected to unfold gradually. Moreover, this is a simplified upper-bound illustration, as silver must compete within the residual bucket alongside other asset classes such as gold, InvITs, and debt. Analysts cited by the Economic Times suggest most equity schemes are unlikely to fully utilize the 35% cap and will instead treat precious metals as a tactical, not structural, allocation.

Even so, when set against a sixth consecutive structural silver deficit projected at around 67 Moz by Metals Focus and the Silver Institute, even conservative participation levels could be material relative to the underlying supply shortfall.

The growth trend that was already in motion

What makes this reform significant is the existing momentum it builds upon. Even before institutional access was expanded, Indian retail investors were already fueling strong growth in silver ETPs:

That nearly threefold increase between 2023 and 2024—and almost fivefold growth over two years—was driven entirely by retail investors and fund categories that already had permission to hold silver. The institutional equity and hybrid segment contributed nothing to that expansion.

The SEBI reform today layers institutional access onto a base that was already accelerating at a 63% annual growth rate before 2024, before surging 195% in 2024 alone. The key question is no longer whether institutional capital will eventually flow into silver through this channel, but how quickly fund managers begin acting on a mandate that did not exist until now.

Why Institutional Flows Behave Differently

Retail silver demand in India is inherently cyclical and seasonal. Wedding seasons drive jewelry and silverware purchases, while festivals spur buying of coins and bars. This demand is substantial—reflected in 247.4 Moz of imports in 2024—but it fluctuates strongly with the calendar.

Institutional allocations operate on a different mechanism. Once a fund’s mandate includes silver ETFs, exposure is expressed as a portfolio weight and rebalanced systematically over time. It does not switch off after festivals, weaken during sentiment downturns, or disappear in corrections. The first clear signal of adoption will likely appear in AMFI monthly flow data, which tracks how mutual funds are reallocating across asset classes, showing whether managers are actively implementing the new framework or taking a cautious, wait-and-see approach.

The structural significance, therefore, is not immediate multi-billion-dollar inflows. It is the creation of a permanent allocation channel in a market that already combines the world’s largest physical silver demand base with a rapidly expanding institutional asset management system.

The SEBI reform is one component. The broader story is the convergence of multiple catalysts within a very short time window.

Sources: Golden Meadow

Leave a comment