Gold has climbed beyond $5,100, underpinned by a softer US dollar and strong, persistent structural demand. Solid technical momentum and ongoing global policy uncertainty continue to favor hard assets such as gold and silver. While the focus on potential FX intervention raises the risk of near-term profit-taking, the broader rally still shows little sign of losing steam.

Gold surged to a fresh record of $5,100 an ounce, while silver extended its rally with another 5% jump to around $110. The latest advance has been fueled by persistent US dollar weakness, signs of yen intervention, and broader unease over fiat currencies—long a structural pillar of gold’s appeal. Ongoing global policy uncertainty is also channeling capital into hard assets.

With such an extensive list of supportive factors, even the most bullish investors may question how long the rally can continue without at least a pause, especially given how stretched valuations have become. The temptation for profit-taking at these levels is clear. Yet prices continue to refuse to roll over, and that resilience is becoming the key narrative. Despite a fading geopolitical risk premium and last week’s tariff U-turn by Trump—which, in theory, should have dampened safe-haven demand—gold barely reacted and instead pushed even higher, underscoring the strength of the current trend.

US dollar remains under pressure amid easing rate expectations and declining investor confidence.

At first glance, the explanation seems simple: the US dollar has weakened, giving gold a natural boost. A softer greenback makes gold more affordable for non-US buyers, and that effect is clearly visible. However, this move goes beyond a straightforward FX translation. Gold prices have also been rising in euro and sterling terms, pointing to broader, more structural demand rather than just currency-driven gains.

That said, dollar weakness is still playing an important role. The greenback has slid amid recent geopolitical fractures, and suspected Japanese intervention in USD/JPY has added further pressure. Markets are increasingly convinced that Japanese authorities stepped in when USD/JPY pushed beyond 159. What really caught investors’ attention were reports that the Federal Reserve was “rate-checking” banks in New York around the London close. The idea that this may have been more than unilateral action by Tokyo—potentially involving coordination with Washington—is significant, as joint Japan–US intervention would send a far stronger signal than Japan acting alone.

Bullish momentum remains firmly intact, with strong follow-through buying and little sign of exhaustion despite overextended conditions.

Momentum is clearly carrying much of the move. The uptrend remains firmly intact, with trend-following behavior dominating as traders continue to buy dips rather than sell into strength. As long as that pattern persists, it is difficult to make a convincing case against further near-term gains.

From a psychological standpoint, the $5,000 threshold has now been decisively cleared. It may have seemed ambitious only a few sessions ago—much like $4,000 did not long before—but strong technical momentum, a weakening US dollar narrative, and rising anxiety in global bond markets have made these once-distant milestones appear increasingly attainable.

That said, macro fundamentals still deserve attention. Real yields, growth expectations, and inflation dynamics have not vanished, and eventually they will reassert influence. When they do, gold may find it harder to sustain these elevated levels without a renewed or deeper systemic risk backdrop.

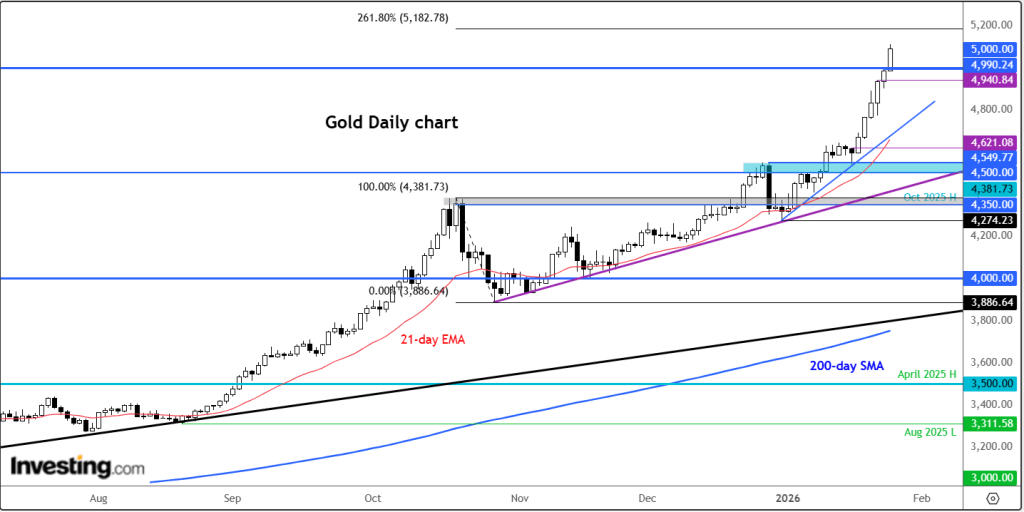

Key Levels to Monitor

For now, the bias remains to the upside. The next resistance target is near $5,182, corresponding to the 261.8% Fibonacci extension of the major October downswing, with the $5,200 psychological level just above. On the downside, multiple support zones are in focus, starting with $5,000. Other round-number levels such as $4,900 and $4,800 may also provide support, while more significant longer-term support is seen around $4,500–$4,550.

As long as the dollar stays weak, central banks continue to be net buyers of gold, and governments openly signal a willingness to intervene in FX markets, it is difficult to identify a catalyst that would meaningfully reverse gold’s advance at this stage, aside from bouts of profit-taking.

Sources: Fawad Razaqzada

Leave a comment