Key Takeaways from Dark Side of the Boom

- The relief rally is fundamentally an oil-and-rates story. If a US-Iran agreement holds together, inflation fears ease, bond yields retreat, and expectations for further rate hikes fade into the background.

- The dollar’s strength may prove short-lived. A credible peace deal could unwind safe-haven demand, while cheaper oil reduces pressure on the Fed, creating conditions for a rapid 3%+ decline in the dollar.

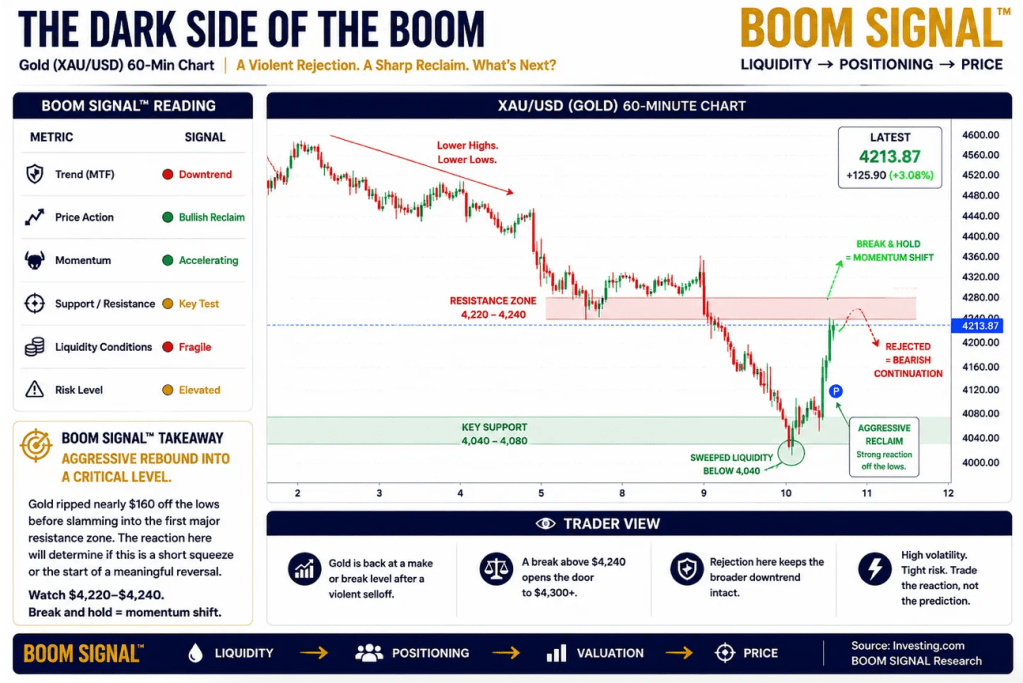

- Gold’s bull case is not broken. The metal was pressured by a stronger dollar, rising yields, and premature calls for the end of the debasement trade, but a softer backdrop for oil and interest rates could quickly put 4300+ back in play.

- SpaceX represents far more than a conventional IPO. It combines a trillion-dollar liquidity event, an AI infrastructure narrative, the power of Musk-driven market mythology, and massive benchmark-related capital flows.

- The ETF industry is already positioning SpaceX as a leveraged trading instrument. As a result, the stock could behave less like a traditional IPO and more like an entirely new volatility ecosystem.

- The larger issue is whether SpaceX paves the way for capital raises by companies like OpenAI and Anthropic, or whether markets eventually realize that even the future must obey the realities of supply and demand.

Plop Plop Fizz Fizz, Oh What a Relief It Is

The market finally got the antacid it had been searching for all week. After two sessions of geopolitical indigestion, Wall Street snapped higher as President Donald Trump signalled that the US was nearing a deal with Iran. Suddenly, traders stopped pricing missiles and started pricing relief. The S&P 500 surged 2%, oil retreated toward $86, bond yields eased, and semiconductor stocks exploded nearly 8% higher as risk appetite roared back to life. This was more than a routine rebound. It was the market aggressively repricing the idea that the war premium embedded in oil may have already peaked.

Trump’s comments acted as the catalyst. He said the US had reached a strong settlement framework with Iran, pending final documentation, and hinted that a formal agreement could arrive within days. He also suggested Vice President JD Vance may travel to Europe for a signing ceremony over the weekend. That alone was enough to flip market psychology almost instantly. Diplomacy rarely moves in a straight line, and the Middle East almost never delivers traders a clean narrative, but the core assumption shifted abruptly from escalation risk to de-escalation relief. Once that shift takes hold, investors stop obsessing over every oil tick and refocus on earnings, liquidity, margins, and the still-solid economic backdrop across the US and Europe.

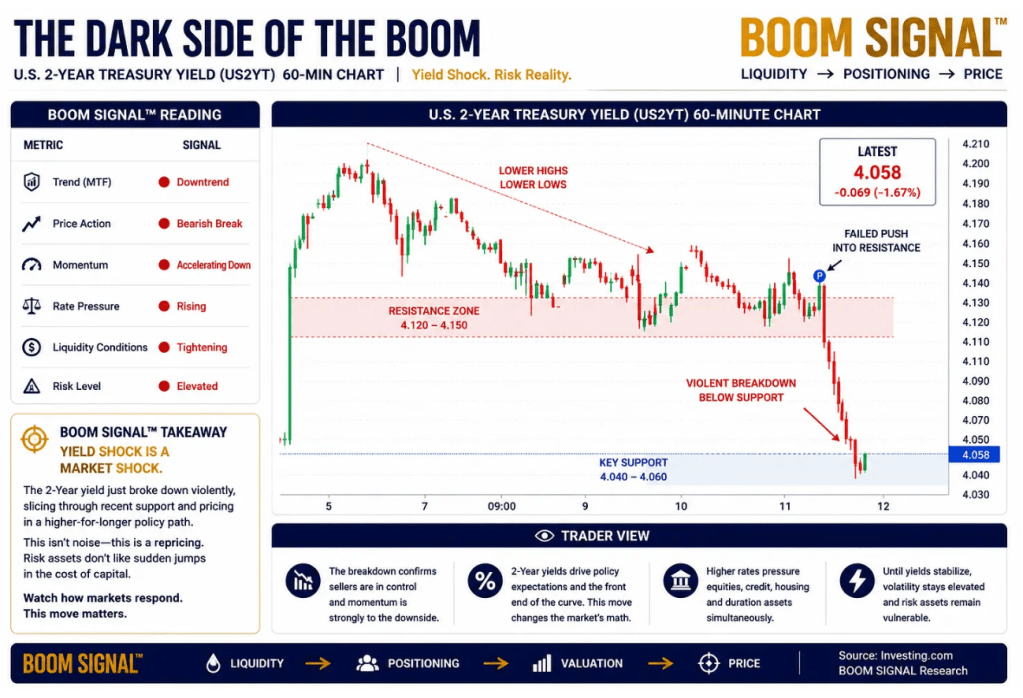

The biggest asymmetry now sits in rates. Only recently, traders had effectively abandoned the idea of rate cuts altogether, and that repricing hit markets hard. It pressured equities, strengthened the dollar, and ultimately crushed gold as social media prematurely declared the debasement trade dead. But much of that move flowed directly through the oil channel. Higher crude became the inflation ghost haunting the Fed’s outlook. Once oil retreats, that ghost loses power. If this peace framework holds together, even imperfectly, the probability of further rate hikes falls sharply. Markets do not need a dramatic dovish pivot from the Fed to sustain a rally. They simply need the war premium to stop feeding the inflation narrative.

My core view has never been that rate cuts are suddenly locked in. The real thesis is that the conflict ends sooner than markets were pricing, and that shifts the entire macro backdrop. Dollar strength still looks temporary to me. As the war premium fades, safe-haven demand for the dollar should unwind, oil prices should cool, and the Fed conversation can return to underlying inflation trends, which remain far more contained than the panic narrative suggests.

Put those dynamics together, and the dollar could fall 3% or more in relatively short order if a peace agreement comes together cleanly. That same environment would likely put gold back in control, with $4300+ firmly back on the table.

The setup is fairly straightforward. Remove the oil shock and the fear of renewed rate hikes, and the dollar loses a major source of support while gold regains the macro oxygen it needs to rally again.

Then, just as the macro backdrop finally starts to breathe again, SpaceX explodes across the equity landscape with what is being framed as the largest IPO in history. Space Exploration Technologies Corp sold 555.6 million shares at $135 apiece, raising $75 billion — more than double the $29.4 billion raised by Saudi Aramco in 2019. At that price, the company commands a market capitalization of roughly $1.77 trillion, or close to $1.8 trillion fully diluted when including employee stock options and restricted stock units. That instantly places SpaceX among the largest public companies on earth, values it above Tesla, and pushes Elon Musk to the edge of becoming the world’s first trillionaire.

But this is not merely an IPO. It is a liquidity event fused with a new space race, powered by an artificial intelligence narrative, and marketed to a retail crowd desperate for a ticket into the future. Musk’s retail following is not a sideshow to this deal — it is the combustion engine underneath it. Retail orders reportedly topped $100 billion, vastly exceeding the 20% allocation initially reserved for individual investors. Friends have been chasing me for access to the deal as if I were some Wall Street syndicate insider. I keep reminding them I am just a tiny minnow hiding out in Hua Hin, Thailand. Yet the frenzy makes perfect sense. Investors are not simply buying shares. They are buying proximity to the next mythology trade.

Naturally, there is another side to the rocket launch. Critics see SpaceX as a hopes-and-dreams IPO, driven more by Musk’s aura, AI hype, and collective imagination than by the financial reality of a company that still has not posted a profit. That criticism matters, but perhaps not immediately. In today’s market, hope is not a side note. Hope itself has become a factor model. Investors want exposure to the future, and in a tape constantly swinging between greed and fear, that alone can generate its own gravitational pull.

The plumbing beneath the market matters just as much as the narrative. Regulatory adjustments could accelerate SpaceX’s inclusion into benchmark indices like the Nasdaq 100, forcing passive funds and institutions that missed the IPO to become buyers in the open market. That is the moment where the story evolves from corporate finance into pure market structure. SpaceX is not simply going public — it is being embedded directly into the machinery of modern finance: index flows, ETFs, institutional benchmarking, retail speculation, and algorithmic liquidity. Once that machine starts spinning, valuation becomes only one variable. Flow becomes the dominant force.

SpaceX may also represent the opening shot in what becomes a massive AI-driven public equity supply cycle. Companies like Anthropic and OpenAI are reportedly preparing for eventual public listings that could seek valuations north of $1 trillion. Their trajectories may now hinge partly on how the SpaceX trade performs. Venture capital firms will treat it as a signal for fundraising appetite. Wall Street will interpret it as a test of liquidity capacity. If SpaceX trades well, the floodgates open wider. If it struggles, the entire AI issuance window suddenly feels colder. Add Alphabet’s massive equity raise and the possibility that other mega-cap technology firms follow, and the question becomes unavoidable: does the market truly have enough demand to absorb the future, or will Wall Street rediscover that even dreams obey the laws of supply and demand?

What makes the SpaceX story even more extraordinary is the speed of its transformation. Less than a year ago, the valuation already looked enormous. Then the xAI acquisition in February pushed the combined private valuation toward $1.25 trillion, lifting the implied standalone SpaceX value to roughly $1 trillion. That came after an insider share sale in December valued the company near $800 billion, nearly double the level seen in mid-2025. In barely six months, the narrative evolved from rockets and Starlink into something much larger: an aspiring AI infrastructure titan. Agreements to provide computing infrastructure to companies like Anthropic and Google, reportedly worth up to $2.17 billion per month, are now expected to become some of its largest revenue streams. That is the real pivot. SpaceX is no longer marketed purely as Mars exploration or satellite broadband. It is now being sold as a foundational power grid for artificial intelligence.

And Wall Street, never one to leave speculative enthusiasm unmonetized, is already transforming SpaceX into a leveraged retail casino. The $15 trillion ETF industry is not waiting around to see how the stock behaves before packaging it into high-octane trading products. Nearly a dozen SpaceX-linked ETFs are expected to launch shortly after the debut, with firms such as ProShares, Leverage Shares, Defiance ETFs, GraniteShares, REX Shares, Direxion, and Tradr ETFs racing to market. Many of these products are designed to deliver double the daily long or inverse performance of the stock, giving traders instant leverage tied to the most anticipated listing in years.

This is the point where the rocket gets bolted directly onto the casino floor. More than 20 ETF filings tied to SpaceX have reportedly already appeared this year, ranging from leveraged strategies to inverse products and options overlays. Exchanges may delay launches briefly, but the larger point remains unchanged: the product machine is already sitting on the runway with engines fully ignited. Since many of the products are structurally similar, the competition becomes all about distribution, marketing power, and speed to market. In ETF land, being first to the shelf often matters more than being best to the shelf. Sometimes a few minutes is enough to determine who captures the first tidal wave of inflows.

The comparison to spot Bitcoin ETFs is unavoidable, except this time the package combines a giant IPO with embedded leverage and Musk mythology. When spot Bitcoin ETFs launched in early 2024, a cluster of nearly identical products hit the market simultaneously before one dominant issuer eventually captured the bulk of assets. SpaceX could become a similar battlefield, only this time the cocktail includes AI hype, rockets, meme energy, retail leverage, and one of the most recognizable entrepreneurs in the world. The hype gauge is not flashing caution anymore. It is completely maxed out.

This is the new Wall Street assembly line: file the ETF before the company even trades. Package the dream before the first candle prints. Sell the upside, the downside, the volatility, the options, the access, and the fear of missing out. ETF filings tied to Anthropic and OpenAI are reportedly already waiting in the wings despite those companies not yet being public. If they eventually list, this process may become the default template for every mega-cap AI IPO going forward. The IPO itself is no longer the final destination. It is merely the starting gun for a financial product arms race.

So the tape now has two engines firing simultaneously. The first is macro relief: falling oil weakens the inflation narrative, lowers yields, softens the dollar, and potentially revives gold. The second is speculative supply: SpaceX arrives as the largest IPO ever and instantly becomes the centerpiece for passive inflows, retail obsession, and leveraged ETF speculation. One side of the market is saying, “Plop Plop Fizz Fizz, what a relief it is.” The other side is screaming, “Strap in, because the rocket has not even started trading yet and Wall Street is already selling tickets to the afterburner show.”

Leave a comment