War, oil shocks, and market turbulence would typically create ideal conditions for gold to rally—yet prices have declined sharply. The explanation isn’t about a lack of fear, but rather the underlying mechanics of global reserve flows.

For years, the narrative was straightforward: gold and silver climbed as investors sought protection from loose monetary policy, fiscal imbalances, and a weakening dollar. Central banks—from Beijing to Riyadh—were steadily shifting away from U.S. Treasuries and into bullion, reinforcing a strong long-term bullish case for precious metals.

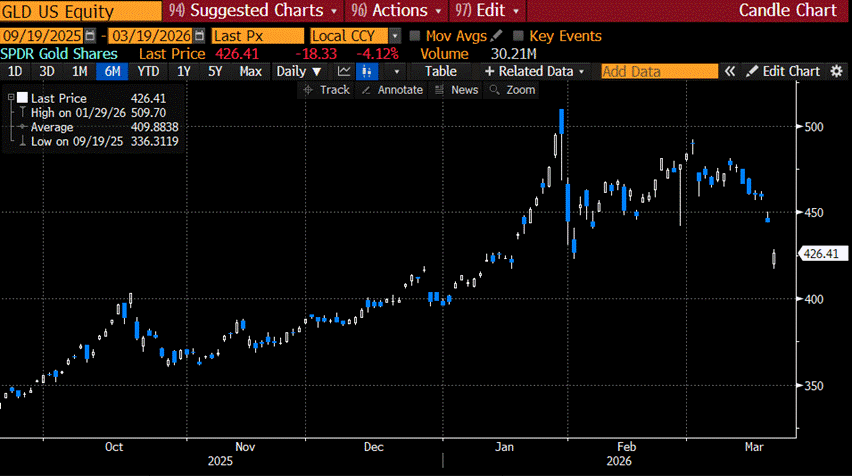

Then, within just three weeks, the trend reversed sharply. Gold dropped 14%, while silver plunged an even steeper 28%. On the surface, the timing seems counterintuitive. Global conflict is intensifying, oil markets are under stress, and volatility is rising. Although the dollar has strengthened after hitting multi-year lows, these conditions would typically support precious metals. Yet instead of rallying, they are falling sharply.

The explanation, once understood, is both surprising and illuminating: gold is no longer trading as a traditional “safe-haven” asset. Instead, it is responding to global reserve flows—and at the moment, those flows are moving in reverse.

A Decade of Currency Dilution

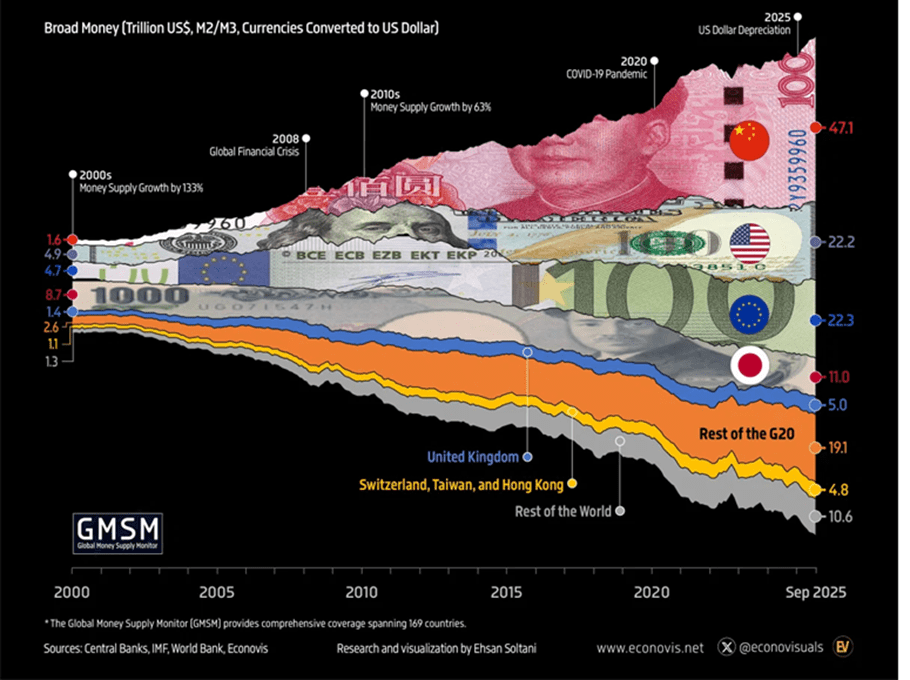

To understand gold’s long-term rise, it’s essential to recognize the two key drivers behind its bull case. The first is monetary debasement. Since the 2008 financial crisis—intensifying during the pandemic—central banks across developed economies have expanded their balance sheets on an unprecedented scale. Money supply has outpaced economic output, real interest rates have turned negative, and inflation has ultimately followed.

In such an environment, hard assets—especially gold and silver—offered something increasingly rare: a store of value that cannot be created at will. Both institutional and retail investors funneled capital into precious metals as protection against the gradual erosion of purchasing power. The logic was straightforward: if fiat currencies are being diluted, hold assets that cannot be.

“Gold evolved from a traditional safe haven into a preferred reserve asset—a structural shift that changed both the profile of buyers and their motivations.”

The second pillar supporting gold’s rise was de-dollarization. The 2022 move by Washington and Brussels to freeze Russia’s foreign reserves sent a clear signal to surplus nations worldwide: dollar-based assets, including Treasuries, carry political risk. Gold, by contrast, does not.

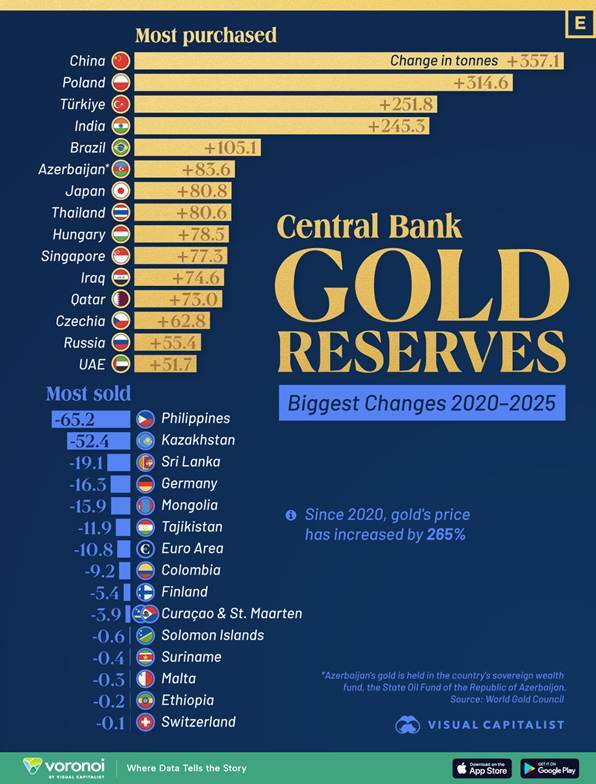

The reaction was both rapid and unprecedented. Central banks—particularly across the Global South and the Gulf—accelerated gold purchases to levels not seen in decades. Countries such as Saudi Arabia, the UAE, Kuwait, and China emerged as major buyers. This was not speculative demand, but a strategic shift in sovereign asset allocation—reducing reliance on the dollar and increasing exposure to an asset with no counterparty risk.

The Hormuz Shock

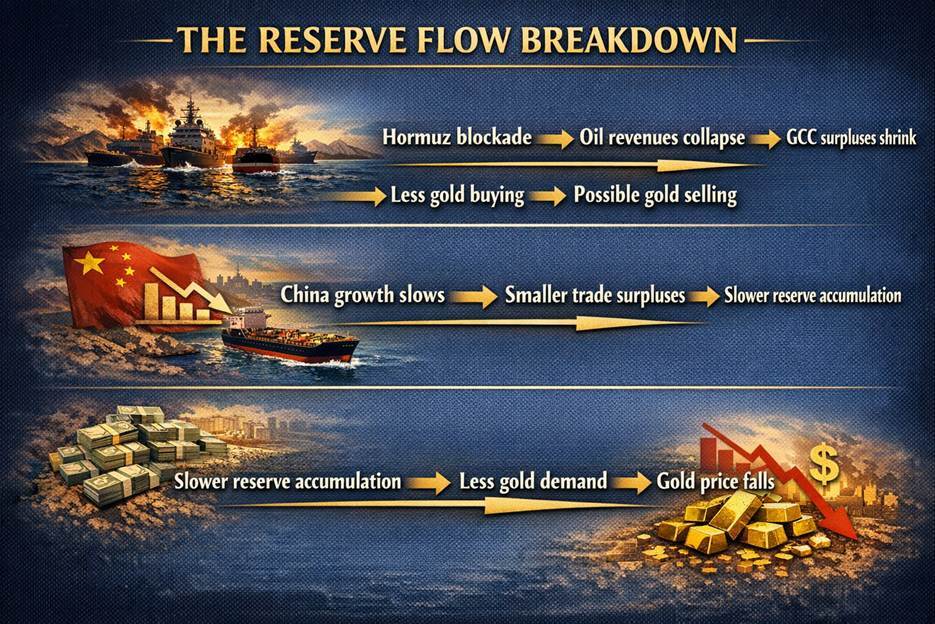

The conflict with Iran—particularly the blockade of the Strait of Hormuz—has rapidly disrupted this dynamic. As a critical artery of the global oil market, roughly 20% of the world’s petroleum flows through the strait each day. When that passage is constrained, the impact goes beyond higher oil prices—it directly squeezes the revenue streams of the very countries that had been the most consistent marginal buyers of gold.

Saudi Arabia, the UAE, and Kuwait manage their sovereign wealth and reserves largely through petrodollar surpluses. When oil revenues fall sharply—as they do when a critical shipping route is disrupted—those surpluses shrink or vanish. The consequence is clear: the marginal buyer of gold steps back, or in some cases becomes a forced seller, liquidating assets to meet domestic fiscal needs.

China introduces an additional layer of pressure. As the world’s largest oil importer, it is now facing a meaningful terms-of-trade shock. Slower economic growth translates into reduced trade surpluses, which in turn limits reserve accumulation. With fewer reserves being built, demand weakens for gold—the preferred alternative reserve asset.

Why Silver Is Falling More Sharply

Silver’s decline has been nearly twice as severe as gold’s, reflecting its dual role. Unlike gold, which is primarily a monetary asset, silver is heavily tied to industrial demand—electronics, solar panels, electric vehicles, and semiconductors account for roughly half of its usage.

When global growth expectations deteriorate quickly, industrial demand contracts just as rapidly. As a result, silver is hit on two fronts: declining reserve demand and weakening industrial consumption. The same slowdown that compresses Gulf surpluses also dampens manufacturing activity, amplifying the downside.

The Paradox of Geopolitical Precious Metals

The common belief that gold thrives during geopolitical turmoil is not incorrect—but it is incomplete. Gold performs best in crises where capital seeks safety and liquidity flows toward hard assets. The current Iran-related shock, however, is different: it disrupts the underlying flow of global capital that has been supporting gold’s long-term rally.

This is the core paradox. Gold is not responding to headlines—it is reacting to balance sheets, particularly the weakening financial positions of sovereign buyers that have driven demand in recent years. Fear is abundant, but in this case, it is not the primary driver of price action.

“In the short term, gold follows liquidity and reserve flows—not headlines or fear. The long-term bull case remains intact, but the marginal buyer has stepped away.”

Momentum, Retail, and the Unwind

Prior to the conflict, precious metals had increasingly taken on the characteristics of momentum trades. Although the underlying drivers—monetary debasement, de-dollarization, and central bank demand—remained intact, they also drew in a more speculative wave of capital. Retail investors, propelled by sustained price gains, social media influence, ETF inflows, and commission-free trading, rapidly piled into gold and silver.

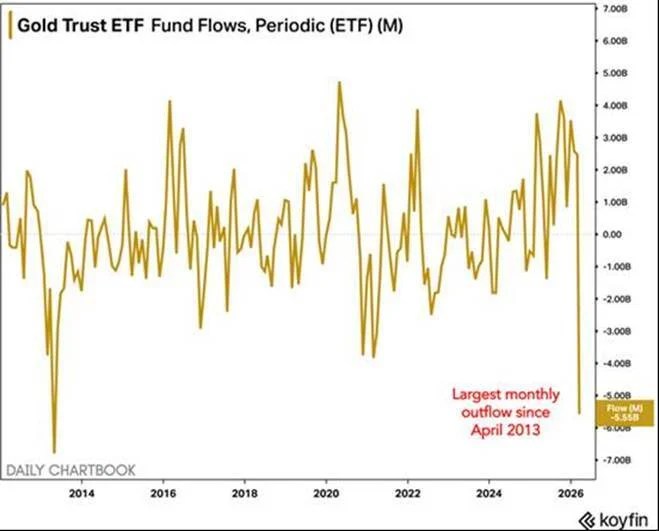

Gold ETFs experienced some of their strongest inflows in the months leading up to the conflict, while silver—more affordable and volatile—became a favorite among momentum-driven traders seeking outsized returns.

This backdrop helps explain the severity of the current selloff. When prices are supported not only by fundamentals but also by a momentum premium, reversals tend to be abrupt. As that premium unwinds, selling pressure intensifies. Notably, the Gold Trust ETF has just posted its largest monthly outflow since April 2013, highlighting how quickly market sentiment can reverse.

The same investors who drove prices higher often operate with tight stop-losses, leverage, and short investment horizons. As the trend reversed, this momentum-driven crowd unwound positions just as quickly as it had built them, magnifying the decline far beyond what fundamentals alone would justify. The Hormuz shock may have sparked the selloff, but the real accelerant was the excess speculation that had built up during the rally.

Outlook: The Structural Case Remains—For Now

Nothing in the current environment fundamentally undermines the long-term case for gold. Monetary debasement persists, and de-dollarization remains a gradual, multi-decade shift rather than a short-term trade. Central banks are unlikely to abandon gold accumulation strategies due to temporary revenue pressures. As conditions stabilize—oil flows normalize, China regains momentum, and GCC surpluses recover—the structural demand for gold is likely to return.

However, markets do not operate on long-term narratives in the near term. They respond to immediate flows—who is buying and who is selling right now. At present, the key marginal buyers are facing financial constraints. More than any geopolitical storyline, this explains gold’s decline in an environment that would typically support higher prices.

For investors, the takeaway is both humbling and instructive: understanding an asset’s long-term drivers does not guarantee insight into its short-term movements. Gold may remain a form of sound money, but like all assets, it is still influenced by shifts in global liquidity—and at the moment, that liquidity is receding.

Sources: Charles-Henry Monchau

Leave a comment