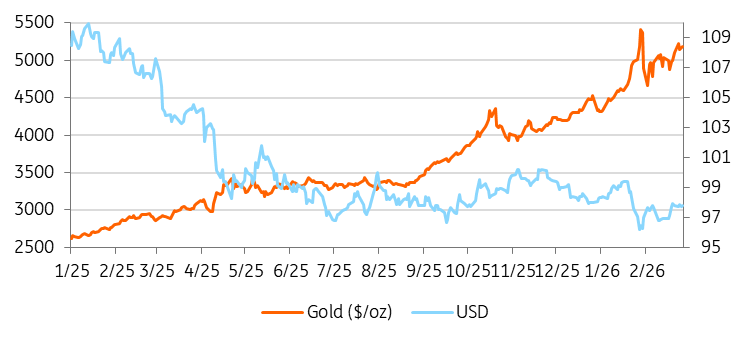

Although gold has paused following January’s sharp advance and the pullback that followed, we don’t think the broader uptrend has ended.

In this article:

- Central banks continue accumulating gold

- Geopolitical risks are resurfacing

- Potential Fed rate cuts could provide additional support

- ETF demand is picking up again

- The rise of digital currencies and shifting reserve strategies

While momentum may cool in the near term, the fundamental forces supporting gold remain solid — and in some areas, are even gaining strength.

Gold’s Structural Backdrop Holds Firm Despite January’s Pullback

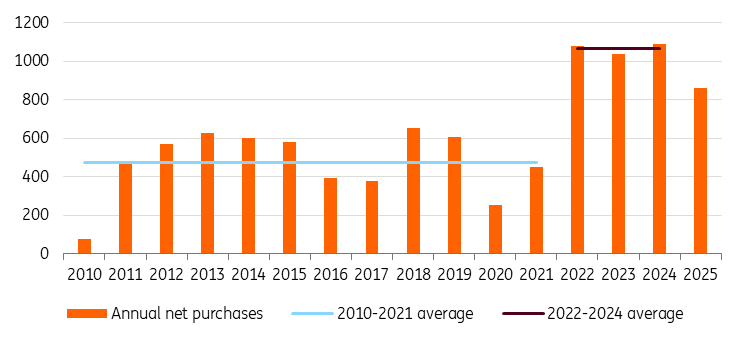

Central Banks Continue to Accumulate

Official sector demand remains the cornerstone of the gold market. Since Russia’s invasion of Ukraine in 2022, central banks—especially in emerging economies—have stepped up efforts to diversify reserves amid sanctions risks, rising geopolitical fragmentation, and a push to reduce dependence on the United States dollar. Importantly, this buying trend has been consistent and largely insensitive to price swings.

Poland, the largest reported gold buyer last year, has indicated it will continue adding to its holdings, aiming to raise its total gold reserves to about 700 tonnes from roughly 550 tonnes. Rather than targeting a fixed 30% share of reserves, authorities are focusing on increasing the absolute level of holdings—highlighting that reserve accumulation is a strategic priority rather than a short-term tactical move.

Meanwhile, China’s central bank extended its gold-buying streak to a fifteenth consecutive month in January.

With geopolitical fragmentation still in place, a significant pullback in central bank demand appears unlikely. This enduring structural support continues to provide a firm foundation for gold prices, even at elevated levels.

Central Bank Demand Stays Strong

Geopolitics Returns to Center Stage

Geopolitical tensions have once again become a key macro driver. From renewed strains in the Middle East to escalating trade frictions and tariff threats, investors are facing a more fragile and unpredictable global landscape. Policy uncertainty—particularly around trade—has added volatility across asset classes. In this environment, demand for safe-haven assets remains well supported, with gold’s role as a hedge against geopolitical and policy shocks back in sharp focus.

Potential Fed Easing as a Tailwind

A shift in the US monetary policy outlook could provide additional support for gold. Although the Federal Reserve remains cautious, risks are gradually tilting toward policy easing as economic growth moderates and inflation continues to cool.

Our US economist expects rate cuts to begin in the second quarter, with policy becoming progressively less restrictive thereafter. Even a modest easing cycle would likely benefit gold by pushing real yields lower and reducing the opportunity cost of holding non-yielding assets.

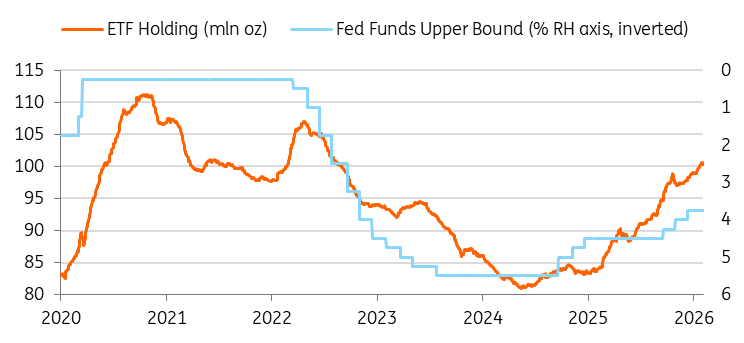

Renewed Interest in ETFs

ETF positioning remains well below its 2020 peak, suggesting room for additional inflows. Following a period of consolidation, gold ETFs are once again drawing investor interest. While central bank purchases continue to anchor the market, ETF flows have the potential to magnify price movements.

If expectations for rate cuts strengthen or geopolitical risks intensify, a fresh wave of ETF inflows could drive another leg higher in gold prices. Historically, ETF holdings tend to rise alongside prices and closely track expectations for US monetary policy—reinforcing the case for stronger inflows as the Fed pivots toward a more accommodative stance.

ETF Flows Track Changes in Fed Policy

Digital Dollars and the Evolution of Reserves

Reserve diversification is no longer limited to central banks. The rapid expansion of US dollar–backed stablecoins has introduced a new class of institutional reserve buyers.

Stablecoin issuers—most notably Tether—have emerged as meaningful purchasers of reserve assets, including US Treasuries and, increasingly, gold.

Tether alone acquired more than 70 tonnes of gold last year, ranking second only to Poland among disclosed buyers, and now holds roughly 140 tonnes across its reserves and gold-backed token. If gold continues to play a role in stablecoin reserve allocation, the sector’s growth could become an additional structural source of demand—one that behaves more like central bank accumulation than retail investment flows.

Although still smaller in overall scale, this emerging channel adds another layer of long-term support to the market.

Momentum May Cool, but the Bullish Case Endures

The advance in gold prices is unlikely to follow a straight line. At record levels, physical demand tends to become more price-sensitive, making consolidation phases or short-term pullbacks increasingly likely.

That said, the core drivers behind the rally—central bank diversification, ongoing geopolitical fragmentation, the prospect of policy easing, and renewed ETF inflows—remain firmly in place. For now, the broader macro backdrop continues to favour gold.

Sources: Ewa Manthey

Leave a comment