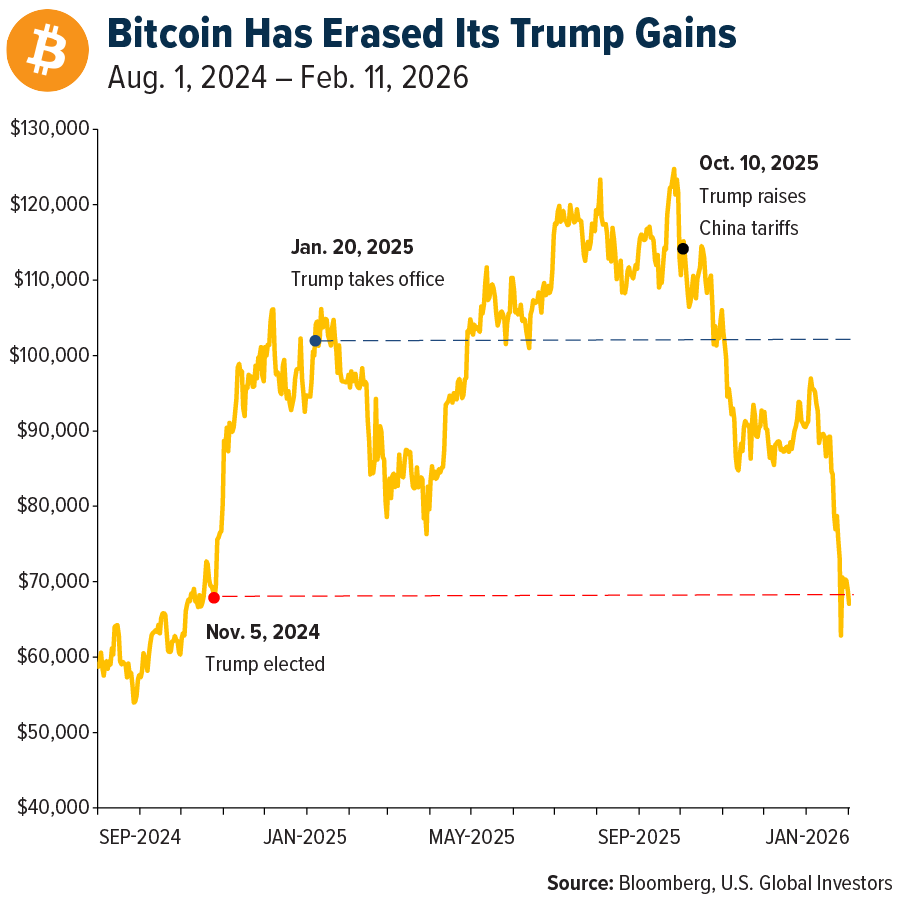

Four months ago, the digital asset market experienced what I consider its most significant liquidation event to date. On October 10, 2025, more than $19 billion in leveraged positions were erased within a matter of hours. Bitcoin tumbled from around $122,000 to $105,000, and over 1.6 million trader accounts were forced into liquidation.

The so-called “10/10” crypto crash did more than shake prices—it reshaped the psychological backdrop of crypto investing.

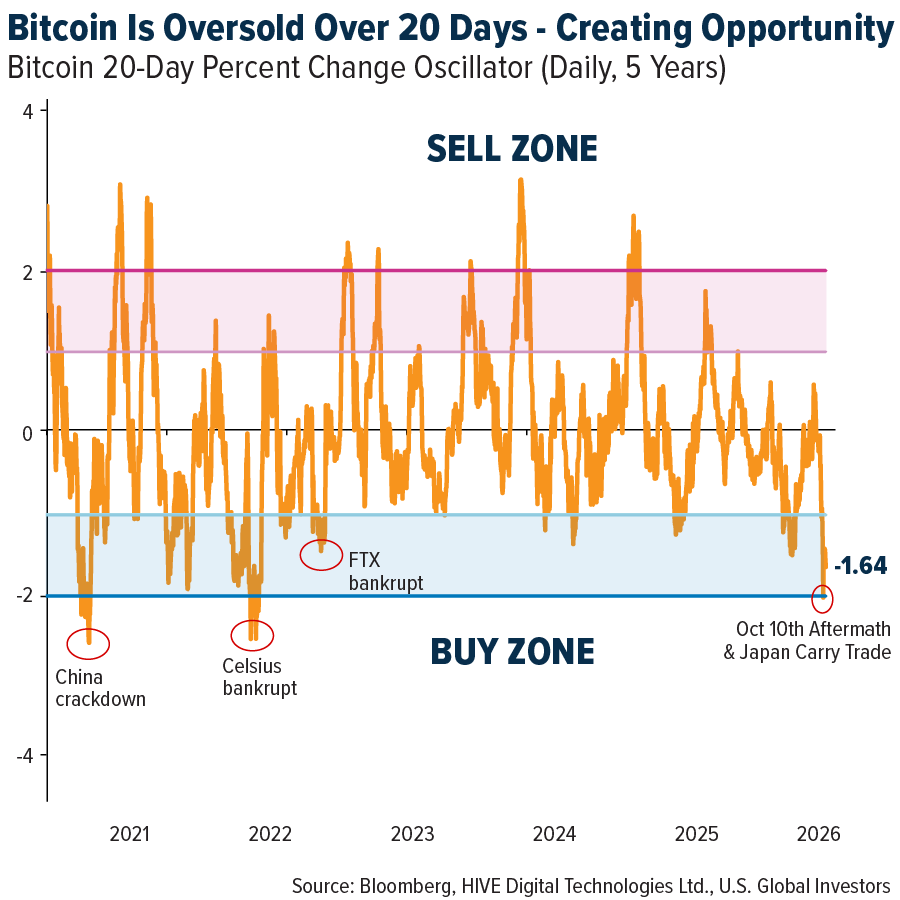

As I mentioned on PreMarket Prep last week, from a technical perspective Bitcoin is currently trading about two standard deviations below its 20-day average—a condition that has appeared only three times in the past five years. Historically, such stretched readings have tended to precede short-term rebounds over the following 20 trading sessions.

The unwinding of the Japanese carry trade—estimated at roughly $500 billion—likely added to the weakness seen in January and again this month. Still, I believe much of that pressure has now run its course.

With Bitcoin still trading below $70,000—about 45% off its all-time high—some investors may be asking whether the events of October 10 are the reason the downturn has lingered.

The short answer is yes. But the deeper explanation is more complex—and, in my view, more relevant for portfolio positioning going forward.

What Really Happened

To put it in context, the 10/10 crash surpassed the FTX collapse in absolute dollar losses. It effectively overshadowed the failure of what had been the world’s second-largest crypto exchange. Binance alone reportedly drew $188 million from its insurance fund to cover bad debt, while several other trading platforms faced comparable strains.

As for the catalyst, many point to President Donald Trump’s announcement of a 100% tariff on Chinese imports, layered on top of an existing 30% levy.

That geopolitical jolt rattled global markets. But in crypto—where leverage is deeply embedded in the system—it transformed what might have been a routine correction into a cascading liquidation event.

The crash laid bare deep structural flaws in how exchanges were managing risk, with one platform in particular drawing scrutiny.

The Binance Factor

Star Xu, founder and CEO of OKX, recently posted a detailed breakdown on X outlining his view of how the 10/10 meltdown unfolded.

According to Xu, Binance rolled out an aggressive user acquisition push offering 12% APY on USDe, a synthetic dollar built on Ethereum. At the same time, the exchange permitted USDe to be posted as collateral under the same terms as established stablecoins such as Tether (USDT) and USD Coin (USDC).

Xu argues this created a distorted incentive structure. Users were enticed to swap USDT and USDC for USDe in pursuit of higher yields, often without fully appreciating the added risk profile.

A leverage loop soon followed. Traders converted USDT into USDe, pledged USDe as collateral to borrow more USDT, then recycled the borrowed funds back into USDe—repeating the process. Xu claims this dynamic drove advertised yields as high as 24%, 36%, and even above 70%.

When volatility surged, USDe quickly lost its peg, unleashing cascading liquidations. The market entered a classic doom loop: forced selling triggered margin calls, which in turn sparked further forced selling.

For its part, Binance has denied responsibility. Speaking at a crypto conference last week, co-CEO Richard Teng attributed the turmoil entirely to President Donald Trump’s tariff announcement. Still, allowing heavily leveraged positions in a market where stop-losses can be gamed and safeguards are thin creates systemic fragility. In such an environment, even a minor shock can ignite a chain reaction.

The Psychological Fallout

October 10 erased more than leveraged trades—it shattered investor confidence. The event coincided with Bitcoin peaking near $126,000 and sparked a wave of fear that continues to weigh on sentiment.

In the weeks that followed, ETFs saw meaningful outflows. Retail traders—many of whom had piled into futures and margin positions as Bitcoin hit record highs—were hit hardest. More than 1.6 million accounts were liquidated, a large share belonging to smaller participants.

This month’s follow-on decline, which marked Bitcoin’s largest realized loss on record as prices slid from $70,000 to $60,000, was described by one analyst as a “textbook capitulation.” The drop was swift, volume-heavy, and flushed out holders with the weakest conviction.

Why I’m Still Constructive

Despite persistent volatility, I remain long-term bullish because the underlying fundamentals remain intact.

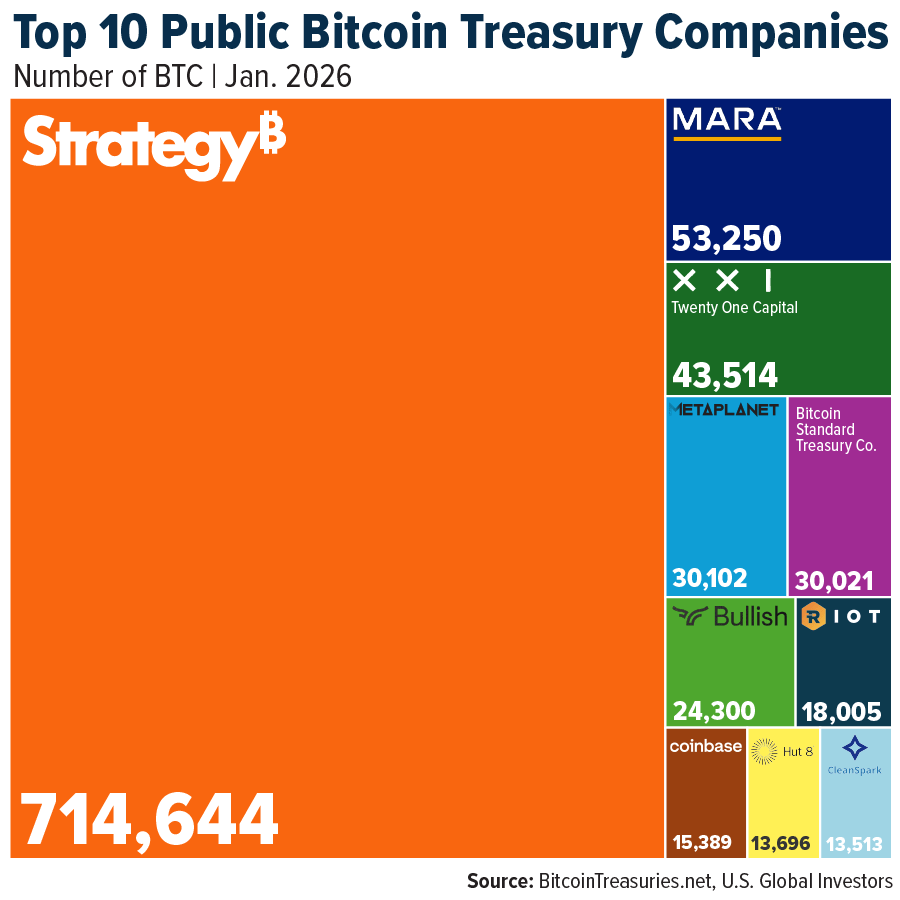

Institutional participation continues to expand. Corporate Bitcoin treasuries—often referred to as Digital Asset Treasury (DAT) firms—now collectively control more than 1.1 million BTC, about 5.7% of total supply, valued near $90 billion. MicroStrategy (now operating as Strategy) alone holds roughly 3.5% of Bitcoin’s circulating supply.

Notably, institutions added around 43,000 BTC in January, even amid adverse price conditions—suggesting that long-term capital remains engaged despite the market’s recent turbulence.

The U.S. Strategic Bitcoin Reserve now reportedly holds more than 325,000 BTC—about 1.6% of total supply—making it the largest sovereign holder globally. At the same time, other nation-states are building positions, much as they do with gold, and major corporations continue to add to their allocations.

The Bottom Line

I’ve long described Bitcoin as “digital gold,” but I don’t believe it has fully evolved into a true safe-haven asset. For now, institutions largely categorize it as a risk-on asset rather than risk-off. That suggests it is still carving out its place within diversified portfolios.

Was October 10 the root cause of Bitcoin’s prolonged weakness? In my view, yes. The event delivered a structural shock that obliterated leveraged positions and forced a sweeping—if painful—deleveraging across the digital asset ecosystem.

Did aggressive marketing and flawed incentive structures at certain platforms worsen the fallout? Again, I would argue yes. Encouraging investors to treat what was effectively a tokenized hedge strategy as if it were a stablecoin—while layering on substantial leverage—inevitably magnified systemic risk.

As severe as the collapse was, it may ultimately prove constructive. Excess leverage often needs to be purged before a sustainable advance can resume. My sense is that we are nearing the final phase of that cleansing process.

Sources: Frank Holmes

Leave a comment