The US Federal Reserve experienced an eventful week. On Monday, it contacted New York–based banks to assess their USD/JPY exposure, sparking speculation that Washington could be coordinating with Japan to address the Japanese Yen’s weakness. This development prompted a sharp sell-off in the US Dollar early in the week.

The Fed’s midweek policy meeting resulted in no change to the federal funds rate, which was kept within the 3.50%–3.75% range, in line with expectations. During his press conference, Chair Jerome Powell avoided questions related to politics, his tenure, and the subpoena. However, he pointed to improving economic momentum and reduced risks to both inflation and the labor market.

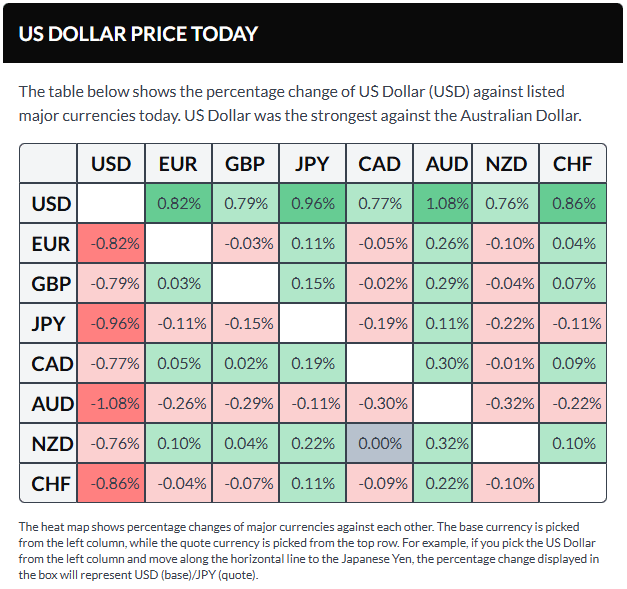

The US Dollar Index (DXY) has since rebounded toward the 96.90 level, recovering most of its weekly losses after President Donald Trump nominated former Fed Governor Kevin Warsh as the next Fed Chair on Friday. The nomination now awaits Senate approval. Looking ahead, the US is set to release several key data points next week, including the ISM Manufacturing PMI for January, MBA mortgage applications, Challenger job cuts, and weekly initial jobless claims.

EUR/USD is hovering around the 1.1880 area after the US Dollar rebounded and recovered nearly all of its weekly losses. In the coming week, Hamburg Commercial Bank (HCOB) will release Manufacturing, Services, and Composite PMIs for both Germany and the Eurozone. Additional Eurozone data include the ECB Bank Lending Survey and December Producer Price Index (PPI), while Germany will publish December Factory Orders and Industrial Production figures.

GBP/USD is trading near 1.3600 ahead of the Bank of England’s monetary policy announcement on Thursday. Governor Andrew Bailey’s subsequent press conference is expected to shed further light on the central bank’s outlook for interest rates. UK data releases include the final January S&P Global PMIs and the Halifax House Price Index.

USD/JPY is holding close to the 154.50 level, paring earlier gains after Tokyo CPI data indicated easing inflation in January. Headline inflation slowed to 1.5% year-over-year from 2% in December, while core measures eased to 2%, undershooting forecasts. The softer inflation profile reduces pressure on the Bank of Japan to tighten policy.

USD/CAD is trading around 1.3580, with the Canadian Dollar maintaining a slight edge against the greenback despite data showing economic stagnation in November. Monthly GDP was flat following a 0.3% contraction in the prior month and fell short of expectations for modest growth. Upcoming Canadian releases include January S&P Global PMIs and the Ivey PMI.

Gold is trading near the $4,880 area after surrendering all weekly gains. Prices retreated from a record high of $5,598 as profit-taking emerged and the US Dollar strengthened sharply.

Looking ahead: Emerging views on the economic outlook

Scheduled central bank speakers for the week:

Monday, February 2:

– Bank of England’s Breeden

– Federal Reserve’s Bostic

Tuesday, February 3:

– Federal Reserve’s Barkin

Wednesday, February 4:

– Federal Reserve’s Cook

Thursday, February 5:

– Bank of England Governor Andrew Bailey

– Federal Reserve’s Bostic

– Bank of Canada Governor Tiff Macklem

Friday, February 6:

– European Central Bank’s Cipollone

– European Central Bank’s Kocher

– Bank of England’s Pill

– Federal Reserve’s Jefferson

Central bank meetings and upcoming data set to influence monetary policy decisions

Key economic data and policy events for the week:

Monday, February 2:

– Germany’s December Retail Sales

– US ISM Manufacturing PMI

Tuesday, February 3:

– Reserve Bank of Australia monetary policy decision

– US December JOLTS job openings

Wednesday, February 4:

– Eurozone January Harmonized Index of Consumer Prices (HICP)

– US January ADP employment report

Thursday, February 5:

– Australia’s December trade balance

– Eurozone December retail sales

– Bank of England monetary policy decision

– European Central Bank monetary policy decision

Friday, February 6:

– Canada’s January employment change

– US January nonfarm payrolls

– US February Michigan consumer sentiment

Sources: Fxstreet

Leave a comment