Gold’s record-setting bull market has resumed its charge—but under a new set of drivers. Aggressive buying from China has increasingly taken over from gold’s traditional engines of demand, namely U.S.-based gold ETFs and futures traders. With American participation fading, gold’s ability to hold lofty levels now rests heavily on sustained Chinese demand. This shift has helped gold remain elevated, postponing the corrective phase typically required to rebalance overheated markets.

Between late July and mid-October 2025, gold surged an extraordinary 32.9% in just 2.7 months. During that stretch, the metal logged 24 record closes—roughly three-sevenths of all trading days—while its strongest gains were spread relatively evenly across the calendar. At the time, U.S. investors were aggressively piling into gold, providing powerful upside momentum.

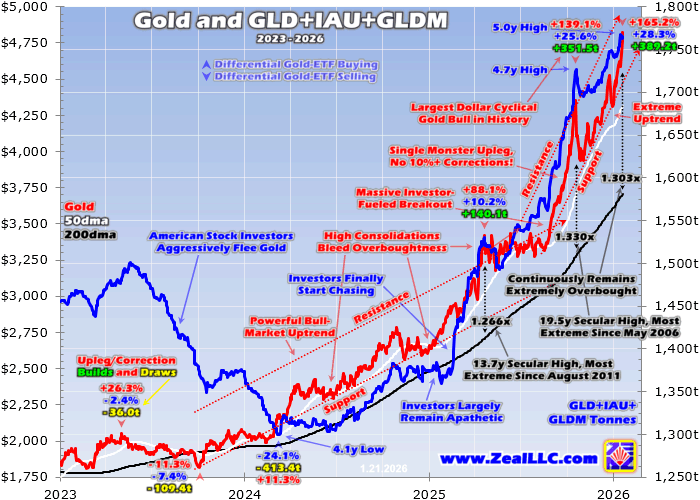

That enthusiasm was clearly reflected in holdings of the world’s largest gold ETFs—SPDR Gold Shares (GLD), iShares Gold Trust (IAU), and SPDR Gold MiniShares (GLDM). According to the World Gold Council’s Q3’25 data, these three vehicles together accounted for more than three-sevenths of all gold held by global ETFs. During the rally, their combined bullion holdings jumped 10.9%, or 169.4 metric tons, helping propel gold to around $4,350 by mid-October and pushing technical conditions to extreme levels.

At its peak, gold was trading 33% above its 200-day moving average—ranking among the most overbought readings since 1981. The bull market had delivered gains of 139.1% over 24.5 months without a single correction exceeding 10%, making it the largest cyclical gold bull ever in U.S. dollar terms since the gold standard was abandoned in 1971. Historically, such excesses have almost always been followed by sharp pullbacks.

A correction initially appeared to be unfolding, with gold dropping 9.5% into early November—its steepest decline of the cycle and close to formal correction territory. Then the pattern abruptly changed.

Since mid-October, gold has climbed another 10.9% over roughly three months, yet this time without meaningful participation from U.S. investors. ETF holdings at GLD, IAU, and GLDM rose just 2.2% (37.8 tons), less than one-quarter of the prior buildup—and all of that increase occurred only in the past month. Those holdings didn’t even recover their mid-October peak until mid-December, shortly before gold began printing fresh record highs.

Gold’s ability to avoid a deeper correction despite some of the most extreme overbought conditions in decades raised questions. Normally, such excesses demand a reset in sentiment and positioning. Since U.S. investors were not driving the rebound, another source of demand had to be absorbing supply.

Clues emerged in the timing of gold’s strongest advances. Since mid-October, nearly all of gold’s gains have occurred on Mondays—a striking anomaly given that Mondays have historically been gold’s weakest trading day. Major upside moves were logged on November 10, November 24, December 22, January 5, January 12, and again this week following a Monday market holiday. Collectively, these few sessions accounted for the vast majority of gold’s rally since October.

Closer inspection revealed that most of these gains occurred overnight during Asian trading hours—well before European or U.S. markets opened. In other words, Chinese traders were responsible for driving price action when the rest of the world was largely inactive. These sessions effectively became “China Mondays,” periods when Chinese market flows dominated global pricing due to minimal competing liquidity.

Because China is uniquely active during the late Sunday-to-early Monday window, its influence on gold prices during that time is disproportionate. On other weekdays, extended trading hours in Western markets dilute that impact. The clustering of gains during these windows strongly suggests that China has become the primary marginal buyer supporting gold at record levels.

Until U.S. investors re-engage meaningfully, gold’s resilience at these heights will depend largely on whether Chinese demand remains strong enough to keep the rally alive.

China’s influence on Sunday-night trading is further magnified by the weekend effect. Weekends represent the longest stretch when traders are unable to react to new, market-moving developments. As a result, many participants square positions and shut down algorithmic trading systems ahead of the weekend. Meanwhile, algorithms that remain active into early Monday often have a backlog of news to process, which can intensify price moves during thin overnight liquidity. This dynamic can significantly amplify China-driven buying in gold.

Before delving further into China’s growing dominance in the gold market, it’s useful to look at how dramatically conditions shifted around gold’s mid-October peak. In the months leading up to that high, heavy share buying in GLD, IAU, and GLDM was the primary force behind gold’s explosive rally. Since then, demand from U.S. equity investors has been largely muted. Even so, gold has managed to surge back into extreme overbought territory—an outcome that underscores how unusual and China-dependent this phase of the rally has become.

China’s dominance during Sunday-night trading is reinforced by the structure of weekends themselves. Weekends are the longest periods when traders cannot respond to new, market-moving information. As a result, many participants flatten positions and shut down algorithmic systems before markets reopen. Meanwhile, algorithms that remain active into early Monday often need to process a backlog of news, which can magnify price movements in thin overnight liquidity. This dynamic amplifies China-driven gold buying when global participation is minimal.

Before exploring China’s growing grip on gold prices further, it helps to contrast the months before and after gold’s mid-October peak. In the run-up to that high, aggressive share buying in GLD, IAU, and GLDM was the dominant force behind gold’s explosive advance. Since then, U.S. stock investor demand has been largely muted—yet gold has still surged back into extreme overbought territory, underscoring how unusual and externally driven this rally has become.

While American equity investors were slow to chase this China-led surge until recently, U.S. gold-futures speculators jumped in aggressively. Futures positioning is reported weekly, and in late November—just after gold’s second “China Monday” surge—total speculative long positions stood at 307,000 contracts. Over the following seven weeks, that figure ballooned. By the January 13 Commitments of Traders report, total spec longs had risen to 362,400 contracts—an increase equivalent to roughly 172 metric tons of gold. That dwarfed the roughly 52-ton increase in GLD, IAU, and GLDM holdings over the same period, meaning futures traders significantly amplified China-driven momentum.

However, futures-driven buying power is limited and quickly exhausted. Gold futures allow extreme leverage—often 20x to 25x—which dramatically restricts the pool of participants willing to assume such risk. Assessing speculative positioning within its historical range provides insight into whether traders are more likely to add exposure or begin selling.

As of mid-January, speculative long positions were already 58% into their bull-market range, while shorts were just 6% in. The most bullish setup occurs when longs are near the bottom of their range and shorts are near the top, leaving ample room for buying. The current configuration is far closer to the opposite—suggesting diminishing upside fuel from U.S. speculators.

That leaves gold’s ability to continue defying a necessary corrective phase largely dependent on China. Unfortunately, reliable, consistent data on Chinese gold markets is scarce, especially in English. Even if such data were available, it would require extensive historical analysis to establish meaningful relationships with price behavior.

Still, anecdotal evidence is abundant. Major financial publications regularly report frenzied gold buying in China. Silver’s recent parabolic surge—largely driven by Chinese demand—appears to have spilled over into gold, fueling enthusiasm both domestically and globally. Without transparent data, Western analysts are left guessing how long this demand can persist.

Cultural factors may offer some clues. In Western markets, gold had long been dismissed as outdated, resulting in minimal portfolio allocations for years. In contrast, gold has always held deep cultural significance in China. Chinese investors therefore began this cycle with far greater enthusiasm, potentially making them more willing to buy aggressively and stay invested longer.

Capital controls also play a role. Chinese investors have limited avenues to diversify wealth outside the domestic financial system, while gold and silver offer a rare escape from policy risk. Additionally, Chinese culture places a stronger emphasis on wealth accumulation and status—traits that can fuel speculative behavior.

These dynamics make China uniquely susceptible to a speculative gold mania. Evidence increasingly suggests one is underway, reinforced by the repeated “China Monday” surges. Yet Chinese markets remain opaque. Financial transparency is limited, economic data series have been quietly discontinued when trends turn unfavorable, and even official gold reserve figures from the People’s Bank of China are widely viewed with skepticism.

For example, China reported identical gold reserves for more than six years before suddenly announcing a 57% jump in a single month—an implausible scenario. Many analysts believe China has accumulated far more gold than officially disclosed for years. If official reserve data lacks credibility, confidence in broader market transparency is equally questionable.

That uncertainty is unsettling. History shows that speculative manias eventually end in sharp, symmetrical collapses once buying power is exhausted. Whether China’s gold frenzy lasts months—or reverses abruptly—is unknowable.

What is clear is that gold’s recent breakout has been almost entirely driven during Chinese trading hours. Since December 19, gold has climbed roughly $487, yet nearly all of those gains occurred on just four “China Mondays.” This concentration of upside is highly abnormal and inherently risky.

Chinese markets have repeatedly demonstrated how quickly sentiment can flip once fear takes hold. Any government action—such as curbing speculative activity—could trigger rapid selling. Without strong participation from U.S. investors or futures traders to absorb that supply, gold could fall sharply.

In short, Chinese trading has seized control of the gold market. After peaking at extreme overbought levels in mid-October, gold required a corrective reset. That process was prematurely halted by surging Chinese demand. With U.S. participation limited and futures buying power fading, gold’s current position is precarious. If Chinese enthusiasm wanes or policy shifts intervene, a forced and potentially violent rebalancing could follow.

Sources: Adam Hamilton

Leave a comment