The modern state increasingly rests on three foundations: debt, fiat currency, and coercive power. Concepts such as “national security” and “critical minerals” have become the latest government talking points, widely promoted and readily accepted by the public. Meanwhile, personal preparedness—once a priority during health crises—has faded from focus, even as harmful consumer habits and ultra-processed foods continue to be normalized and aggressively marketed.

Political leaders often project strength through military posturing and geopolitical confrontation while avoiding personal sacrifice, financing these actions primarily through expanding debt and currency creation. In several regions, power structures are maintained through force, information control, and repression rather than genuine legitimacy or accountability.

Across parts of the world, regimes with deeply troubling records are frequently rebranded as sources of “stability” when it suits geopolitical or economic interests, particularly in energy and resource markets. This pattern underscores a broader contradiction: governments race to announce ambitious initiatives and sweeping strategies, yet largely ignore the importance of real savings and sound money.

Against this backdrop, a growing share of the global population—particularly in Asia, along with a minority of investors in the West—has turned toward long-term wealth preservation through tangible assets such as gold and silver. For those already positioned this way, the erratic behavior and short-term thinking of governments is more a source of frustration than fear.

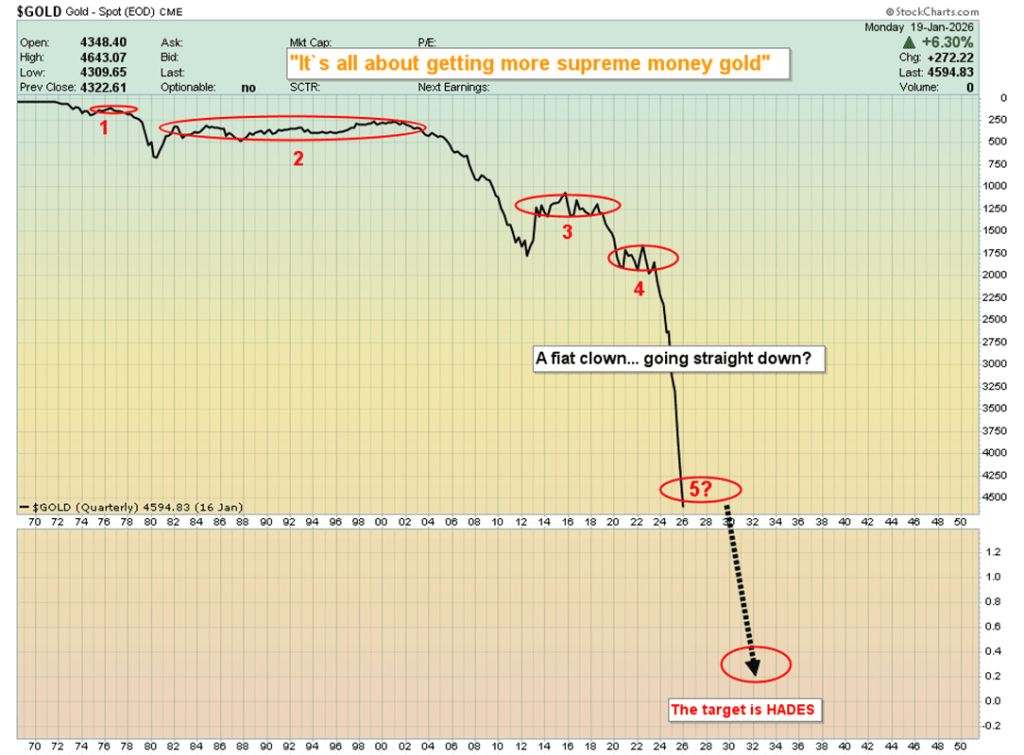

Gold is the currency of independent citizens. While the U.S. dollar is technically due for its fifth cyclical rebound against gold in the past 50 years, that does not mean it must happen immediately—and when it does…. Gold-focused savers should stay prepared to add to their gold holdings—and silver as well.

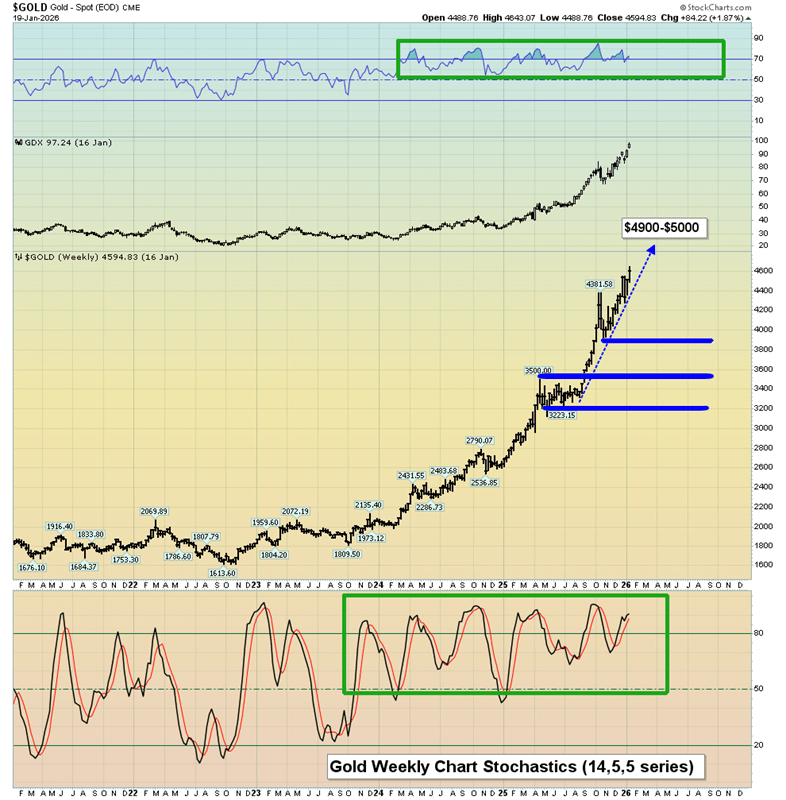

On the weekly chart, gold appears technically overbought, yet its price behavior is beginning to resemble the equity market’s powerful advance in the mid-1990s. Momentum indicators such as RSI and Stochastics are finding support near the 50 level before pushing above 70 and remaining elevated for extended periods—an indication of strong, persistent trends rather than imminent reversals.

Against a backdrop of rising debt, expanding fiat issuance, and escalating geopolitical risks, prominent gold investors such as Pierre Lassonde have projected that gold prices could approach the $20,000 level in the years ahead.

From a portfolio-management perspective, selectively taking profits—up to roughly 30% in many cases—can be prudent, not as a call on a fiat-denominated price peak, but as a way to build liquidity. That capital can then be redeployed during the next meaningful pullback, which is likely to occur at price levels well above today’s.

Psychologically, sharp corrections can be challenging, particularly for investors without available cash. Maintaining some dry powder through partial profit-taking enables investors to add to gold, silver, and mining positions when opportunities arise—this is the primary rationale for trimming exposure now.

Fundamentally, the case for gold remains exceptionally strong. Recent statements suggesting potential military actions involving NATO allies underscore the degree of geopolitical uncertainty. Even without direct conflict, such rhetoric alone could propel gold significantly higher against fiat currencies. In the event of an actual escalation, price moves of $2,000 per ounce—or more—could unfold rapidly.

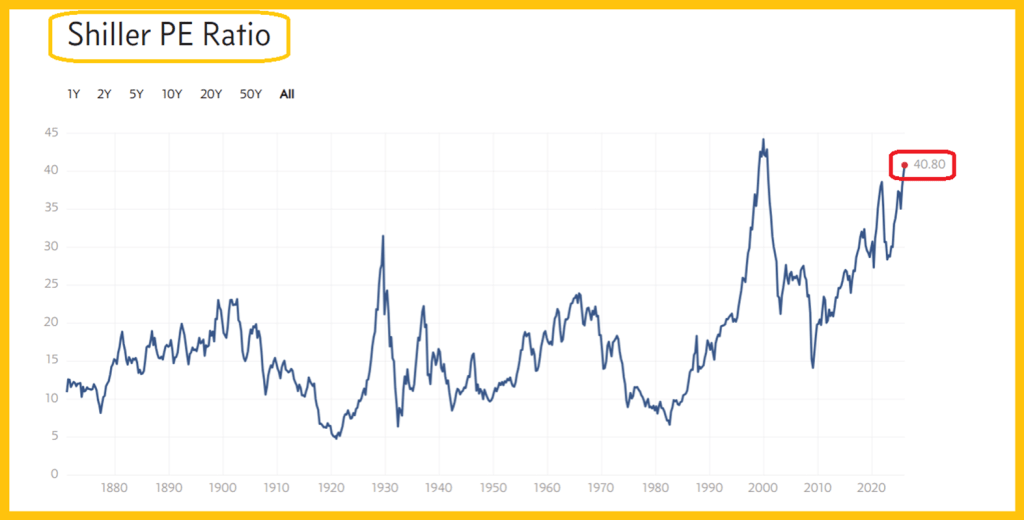

The Shiller (CAPE) ratio—an inflation-adjusted price-to-earnings measure for the S&P 500—highlights the extreme valuation levels currently embedded in U.S equities.

If U.S. policymakers continue to pressure European allies through aggressive tariff measures while openly discussing military options, the resulting backlash could be severe. At some point, a tipping point may be reached, prompting European governments and institutions to rapidly reduce exposure to U.S. government bonds and U.S. equities.

Such a scenario would carry profound risks. Asset freezes or retaliatory measures could follow, severely disrupting global financial markets. Under those conditions, gold could experience explosive upside moves, potentially rising by thousands of fiat-denominated dollars in very short order. At the same time, forced selling from Europe could trigger a rapid collapse in U.S. equity markets, with a speed and scale rivaling—or even exceeding—historic market crashes.

The broader takeaway is that gold increasingly functions as a form of sovereign money for billions of individuals, particularly across Asia, who already view it as a long-term store of value. As pressures build on systems dominated by fiat currency, debt expansion, and coercive policy tools, the resilience of those systems may be tested. Should confidence fracture, the adjustment—especially in the U.S.—could be both abrupt and far-reaching.

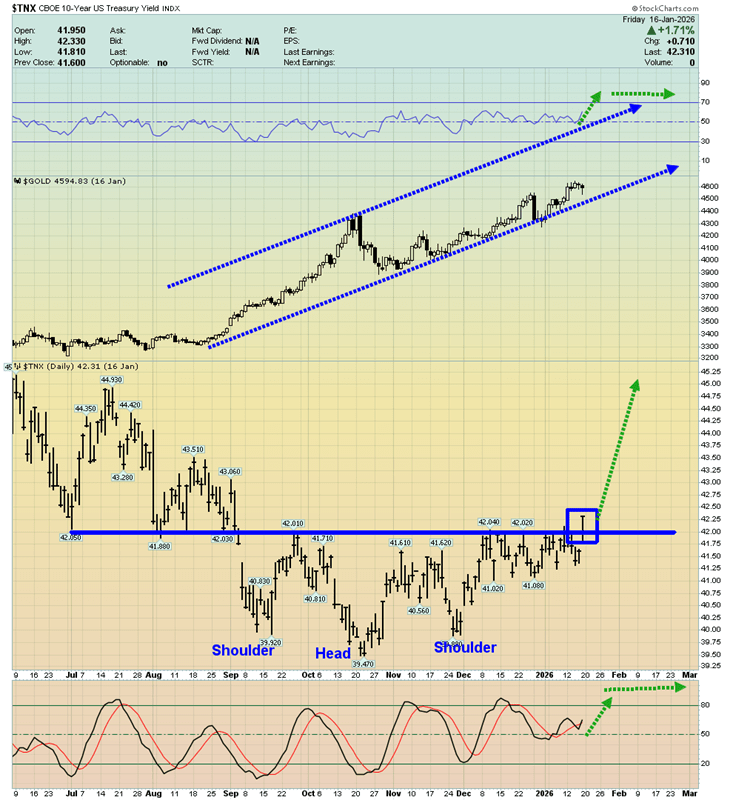

Turning to the 10-year Treasury yield chart, the recent upside breakout carries profound implications for both the U.S. government and gold. For years, the notion of unlimited quantitative easing was promoted as a sustainable solution, but that framework was always unrealistic. Instead, it appears to be giving way to a regime of persistently higher interest rates—and, in parallel, steadily rising fiat-denominated gold prices.

This shift reflects a deeper issue: confidence in governments and their currencies is eroding. As debt burdens expand and monetary credibility weakens, markets are beginning to price in a structural change rather than a temporary cycle. In that environment, higher yields and higher gold prices are not contradictions but complementary signals of systemic stress.

The loss of trust in fiat-based systems is no longer a distant risk; it is an active force shaping global markets—and one that is likely to persist.

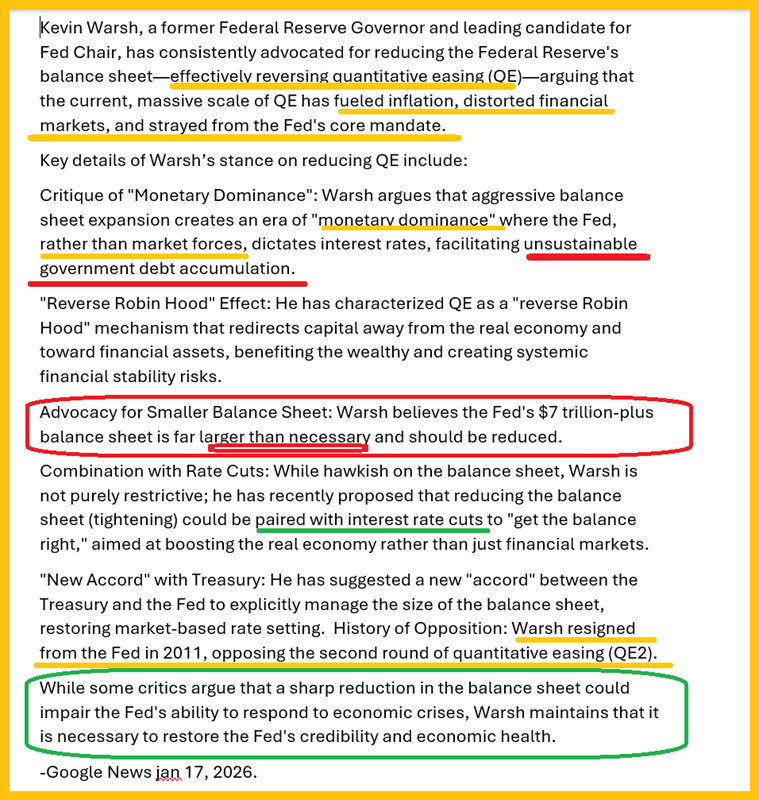

While a new Federal Reserve chair has yet to be appointed, the leading candidate, Kevin, is known to favor aggressive quantitative tightening and has openly described equity markets as severely overvalued. To restore credibility in the U.S. government, its bond market, and the dollar, a substantial and sustained QT program would likely be required.

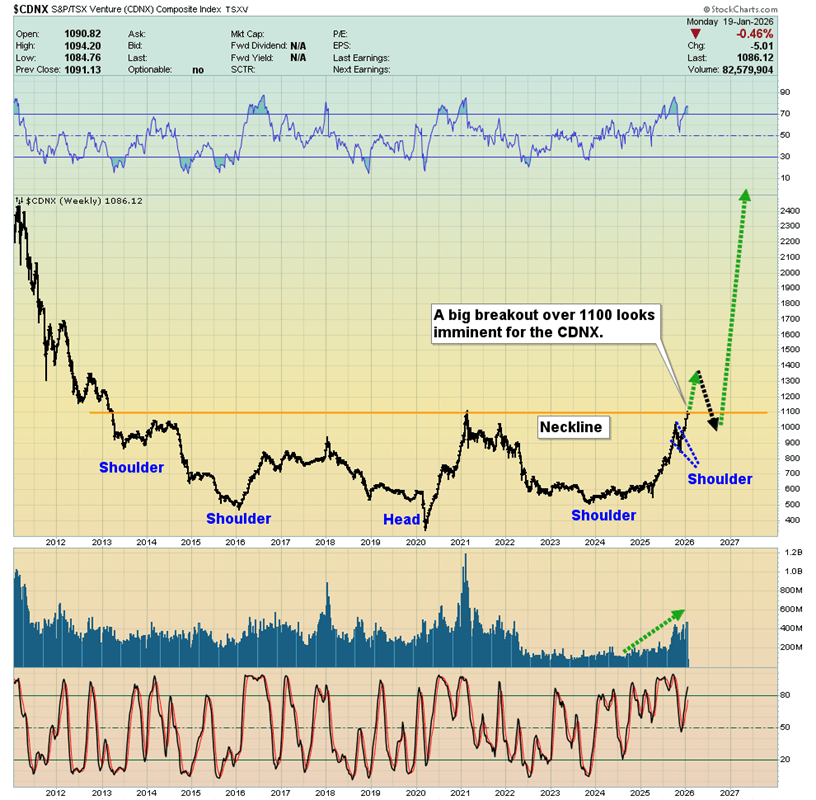

What I continue to regard as one of the most significant base formations in market history is the inverse head-and-shoulders pattern on the CDNX. I have long argued that a breakout from this structure would likely coincide with a major move higher in long-term interest rates, and recent developments suggest that this scenario is unfolding decisively.

My long-term objective for the CDNX stands at 10,000, and well before that level is reached, many junior resource stocks could deliver outsized returns—potentially achieving multi-hundred- or even thousand-fold gains.

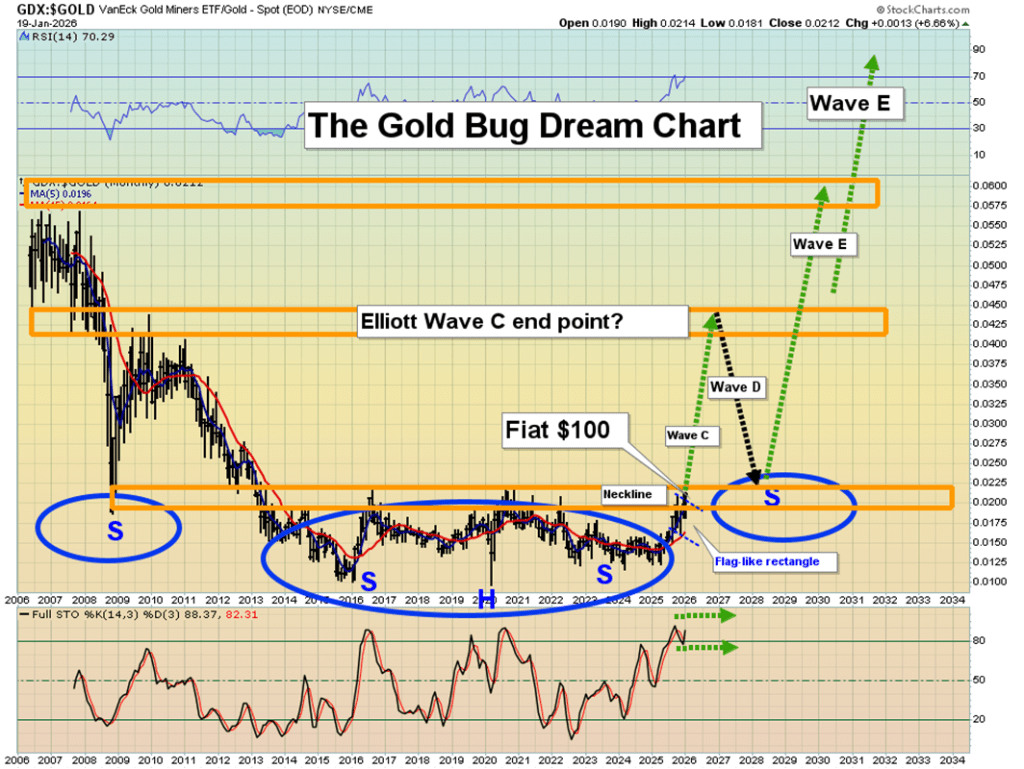

Another chart I encourage investors to monitor closely is the GDX-to-gold ratio. Of particular note is the 14,3,3 Stochastics oscillator at the bottom of the chart. As the upside breakout gains traction and the rally develops, this momentum indicator could remain in overbought territory not merely for months or years, but potentially for an extended secular period.

The broader takeaway is clear: Markets appear to be entering a new phase—one defined by a sustained gold bull cycle. In this environment, informed and disciplined investors stand to benefit the most, as capital increasingly shifts toward real assets and away from fiat-based complacency.

Sources: Stewart Thomson

Leave a comment