Zurich Insurance Group AG (SIX: ZURN) and Beazley PLC (LON: BEZG) have agreed in principle on the main financial terms of a potential all-cash offer, valuing the UK-based insurer at around £8 billion. Under the proposed transaction, Beazley shareholders would receive up to 1,335 pence per share, consisting of 1,310 pence in cash plus allowable dividends of up to 25 pence for the year ending December 31, 2025.

The indicative offer implies a premium of almost 60% to Beazley’s closing price of 820 pence on January 16, the final trading day before the offer period commenced, and represents a 34.6% uplift to the company’s record high of 973 pence reached on June 6, 2025.

Beazley’s board said it would be “minded to recommend” the proposal to shareholders should a firm offer be made on the outlined financial terms, subject to agreement on remaining conditions and the execution of definitive documentation.

The proposed deal would bring together two complementary operations, forming a leading global specialty insurance group with roughly $15 billion in gross written premiums, supported by Beazley’s strong position at Lloyd’s of London.

Zurich is required to announce a firm intention to proceed with an offer by February 16, or confirm that it does not plan to make a bid. The Swiss insurer currently owns a 1.479% stake in Beazley, equivalent to 8,866,051 ordinary shares.

Morgan Stanley published a new analysis of Japan’s tire industry, reaffirming Overweight (OW) ratings on two major companies with solid growth prospects despite differing market pressures. The report highlights firms well positioned to benefit from opportunities in North America while navigating sector-specific challenges.

1. Toyo Tire — Morgan Stanley reiterates its Overweight rating on Toyo, pointing to growing confidence in the company’s growth strategy and shareholder return outlook ahead of its Medium-Term Plan announcement on March 4. Analysts see additional upside as investors continue to factor in stronger demand for WLTR (Wide Light Truck Radial) tires in North America, where Toyo holds a well-established market position.

2. Bridgestone — Bridgestone also retains an Overweight rating, supported by initiatives to reinvigorate the Firestone brand in the North American market. Morgan Stanley highlights encouraging expectations from the company’s restructuring efforts, while cautioning that soft OE (Original Equipment) demand for TBR (Truck and Bus Radial) tires in North and South America presents a downside risk. Nonetheless, replacement demand in these regions remains resilient.

Bitcoin hovered just above 15-month lows on Wednesday after a sharp sell-off drove the world’s largest cryptocurrency down toward the $73,000 level amid a wave of liquidations and heightened risk aversion. The token was last trading 2.8% lower at $76,509.1 as of 01:56 ET (06:56 GMT), having earlier touched $73,004.3—its weakest level since November 2024.

Following the weekend’s slump, Bitcoin fell nearly 12% last week, building on a roughly 10% decline in the prior week. The latest drop marks its lowest point since Donald Trump’s U.S. election victory, wiping out gains that had previously been supported by optimism around potential regulatory easing for the cryptocurrency sector.

Bitcoin sinks to a 15-month low as mass liquidations accelerate

The downturn was accompanied by widespread liquidations of leveraged long positions. According to data from crypto analytics firm CoinGlass, nearly $740 million in bullish bets were erased over the past 24 hours, as falling prices triggered margin calls and forced traders to close positions.

Bitcoin’s latest weakness represents a sharp reversal from the strong rally seen late last year, when prices surged in the wake of Donald Trump’s election victory. At that time, investors poured into cryptocurrencies on expectations that a new U.S. administration would adopt a more supportive regulatory approach to digital assets. Additional tailwinds came from Federal Reserve rate cuts starting in December 2024, which helped fuel demand for higher-risk assets.

Gold and other traditional safe-haven assets rebounded on Wednesday as geopolitical tensions between the United States and Iran intensified.

At the same time, cryptocurrency markets remain under pressure amid uncertainty surrounding U.S. monetary policy following President Trump’s nomination of former Federal Reserve Governor Kevin Warsh as the next Fed chair. Warsh is widely regarded as a policy hawk, raising concerns over tighter liquidity conditions.

Most altcoins remained under pressure on Thursday, posting steeper losses than Bitcoin. Ethereum, the world’s second-largest cryptocurrency, slipped 2.3% to $2,268.92, while XRP, ranked third, edged 1.1% lower to $1.59.

Solana dropped 6%, while Cardano also moved lower and Polygon declined 3.5%. Among meme tokens, Dogecoin was marginally weaker, down 0.2%.

The mainstream narrative claims that a new Fed chair will safeguard the central bank’s independence from U.S. government influence—and that this alone justifies a $1,200/oz drop in gold and a $50 collapse in silver.

Put simply, that narrative is complete nonsense.

Fiat currency is best thought of as meme—or even junk—money, and despite its obvious flaws, it can still enjoy periodic rallies against what many see as the ultimate form of money: gold. These countertrend moves typically emerge during bouts of speculative excess, much like the frothy conditions that have dominated markets over the past couple of months.

From a fundamental standpoint, the gold bull market remains fully intact. Billions of gold-focused savers across China and India—along with a smaller group of informed Western investors—do not rely on central banks for validation. Their priority is building long-term wealth in gold, not accumulating ever more fiat currency and debt.

In the context of this broader bull cycle, it makes little difference who occupies the Fed chair. What matters is whether gold is attractively priced. When it is, prudent savers see it as an opportunity to accumulate more, regardless of short-term fiat-driven narratives.

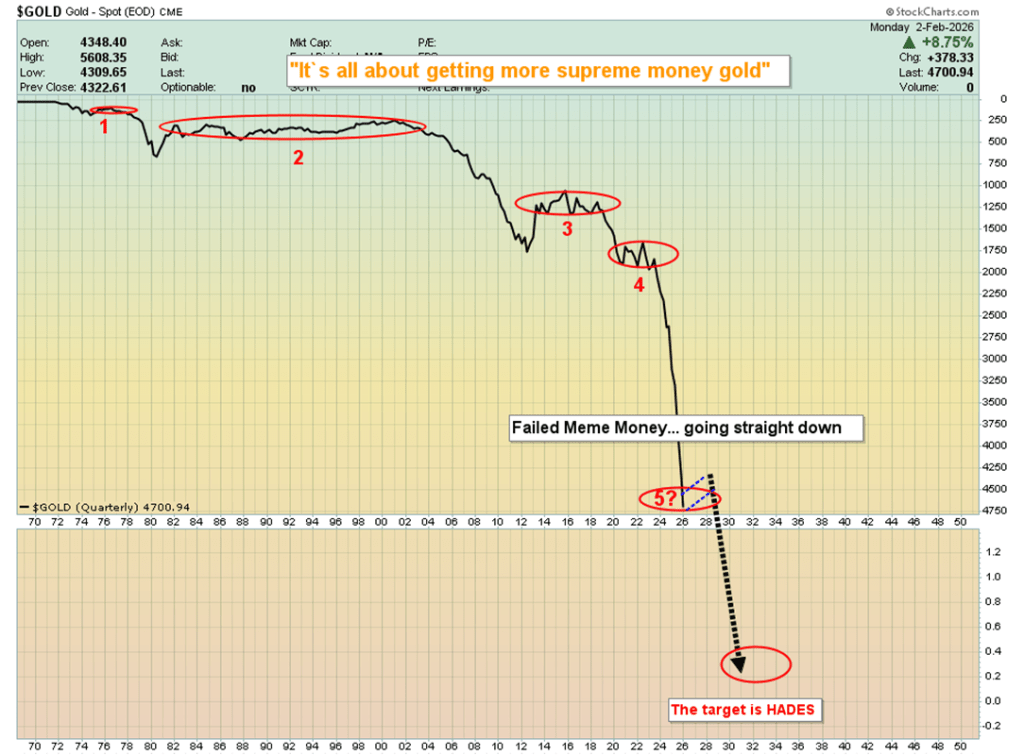

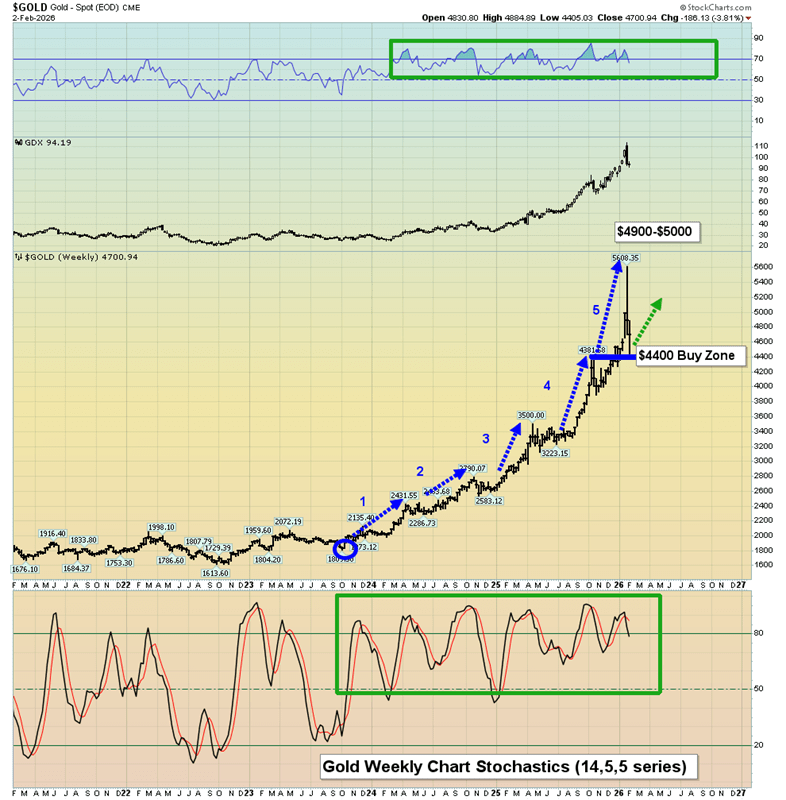

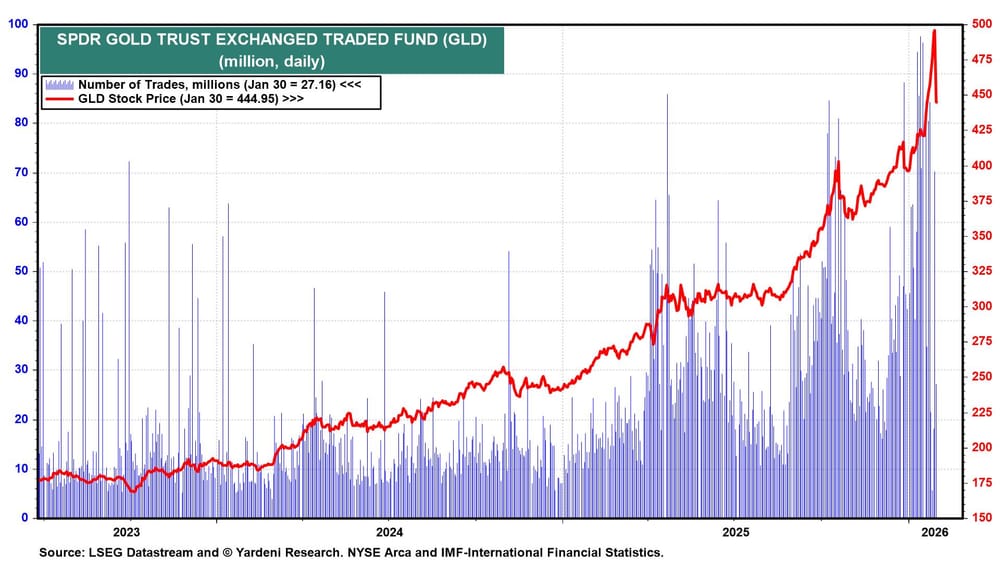

The long-awaited “exciting buy zone” has finally come into play. Gold investors were encouraged to prepare for a meaningful dip into the $4,400 area, and that discounted opportunity has now materialized.

Sustainable wealth building is not about predicting prices, but about preparing for unexpected moves. This pullback unfolded over just a few days, leaving unprepared investors confused and still focused on guessing what happens next.

The key development now is that the $5,600 region has emerged as a major accumulation zone on any future pullback. Gold investors should already be positioning themselves to take advantage of that opportunity if and when it presents itself.

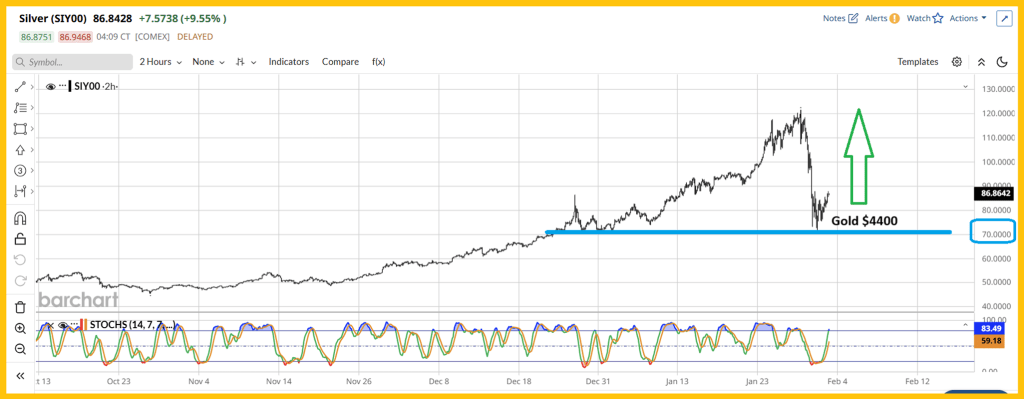

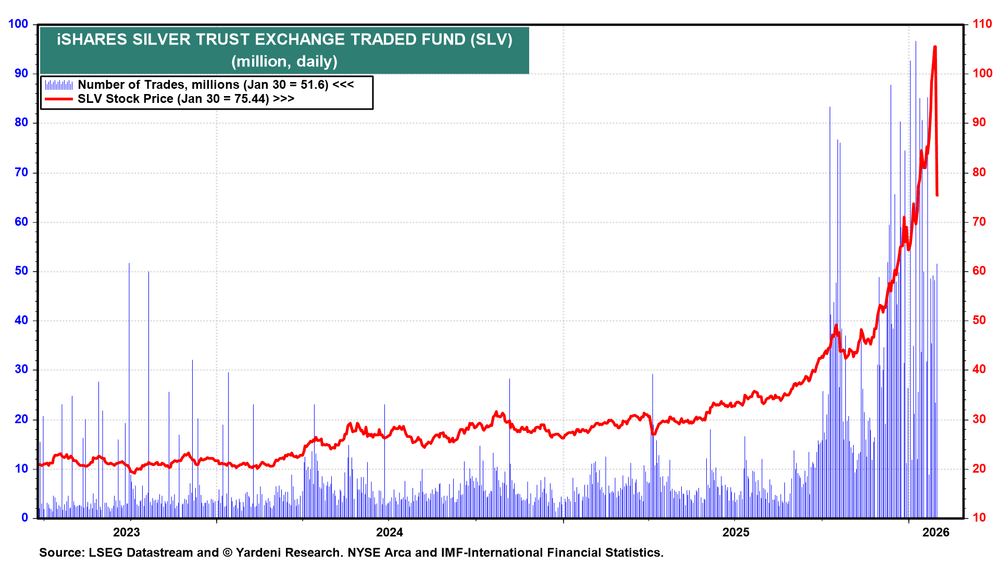

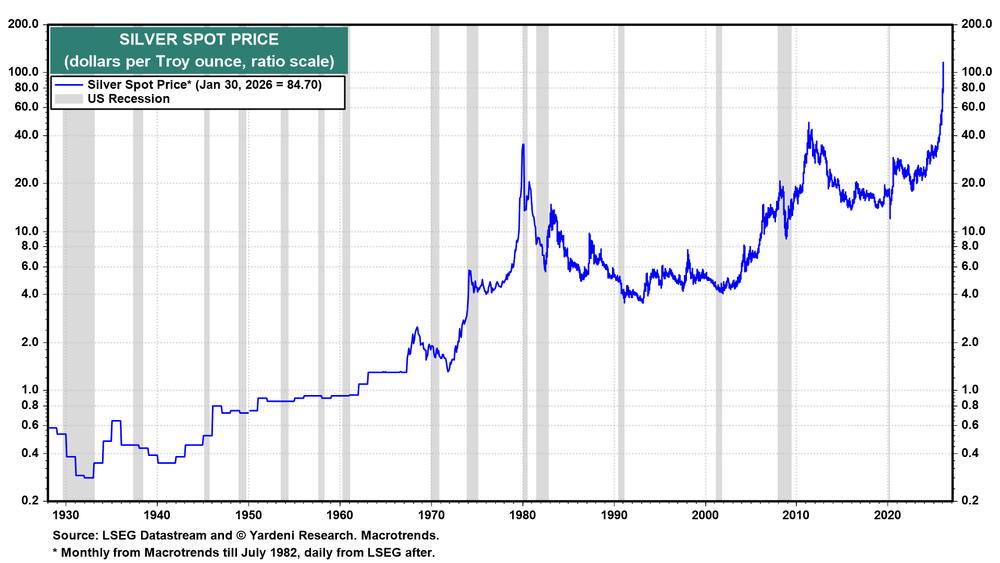

As for silver, the recent price sell-off was “super-sized,” driven by large and heavily leveraged bets against fiat currencies. That decline ultimately found support at the $70 buy zone, aligning perfectly with gold’s move into the $4,400 area.

Gold remains the undisputed leader of the precious metals complex. If silver investors and mining-stock enthusiasts take their cues from gold bullion, they position themselves to build substantial and durable wealth. The most likely near-term path for silver is a broad trading range between $70 and $120, followed by a powerful upside breakout that could propel prices toward the next target zone of $170–$200.

Over the longer term, silver has the potential to trade well above $1,000, largely because governments worldwide—both in the East and the West—continue to cling to fiat currencies and debt rather than returning to sound money anchored in gold.

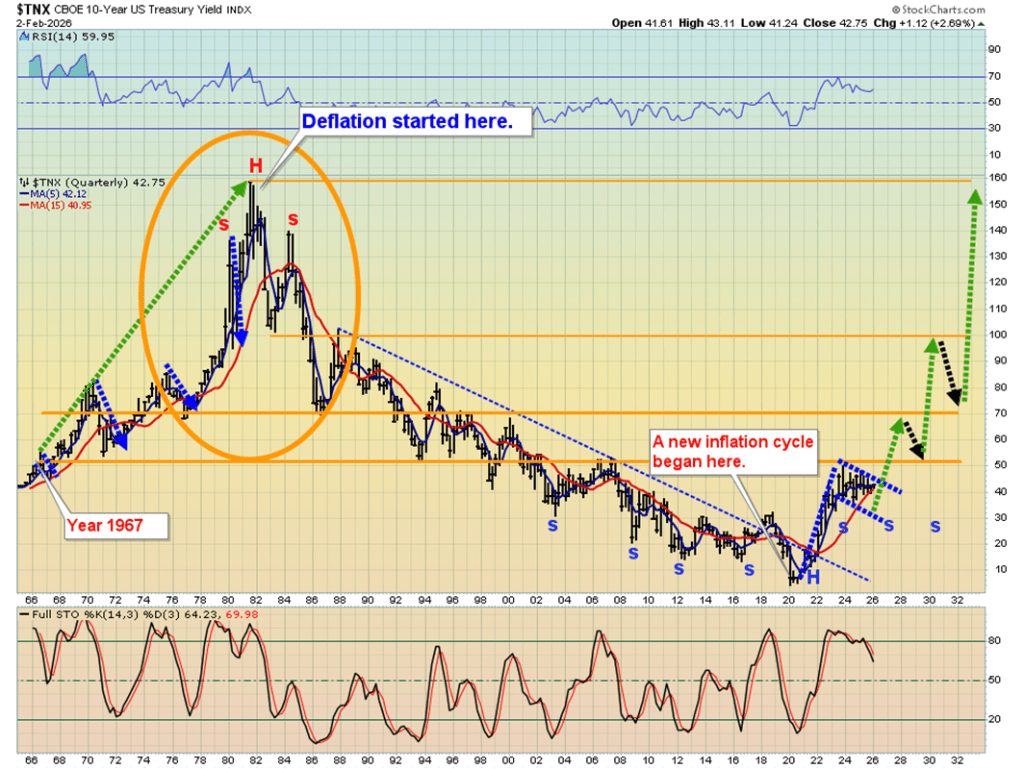

A new 40-year inflation cycle began in 2020 and is unlikely to end until U.S. interest rates reach record highs. Unlike the cycle’s conclusion in 1980, however, elevated rates this time are unlikely to curb inflation, as it is being driven by ongoing government policies rather than purely monetary conditions.

Another perspective on U.S. rates: the incoming Fed chair is more likely to lean toward fiscal restraint on a debt-addicted U.S. government than to dispense easy-money policies of QE and rate cuts. Such a stance would have implications for long-term sovereign yields worldwide, and global money managers are likely to continue shifting capital into gold as a strategic response.

As interest rates continue their relentless climb in the years ahead, governments will inevitably confront their “Queen Gold maker.” They will be forced to begin replacing fragile fiat currencies with gold—or face effective financial ruin.

As for robots, they will simply become another cost burden for citizens already trapped in stagflation. As automation expands rapidly and robot populations eventually outnumber humans, workers will be left competing for a shrinking pool of jobs. Confronted with government-driven stagflation and lacking the protection of gold savings, many will endure severe financial stress—conditions that would be further worsened by a stock market crash.

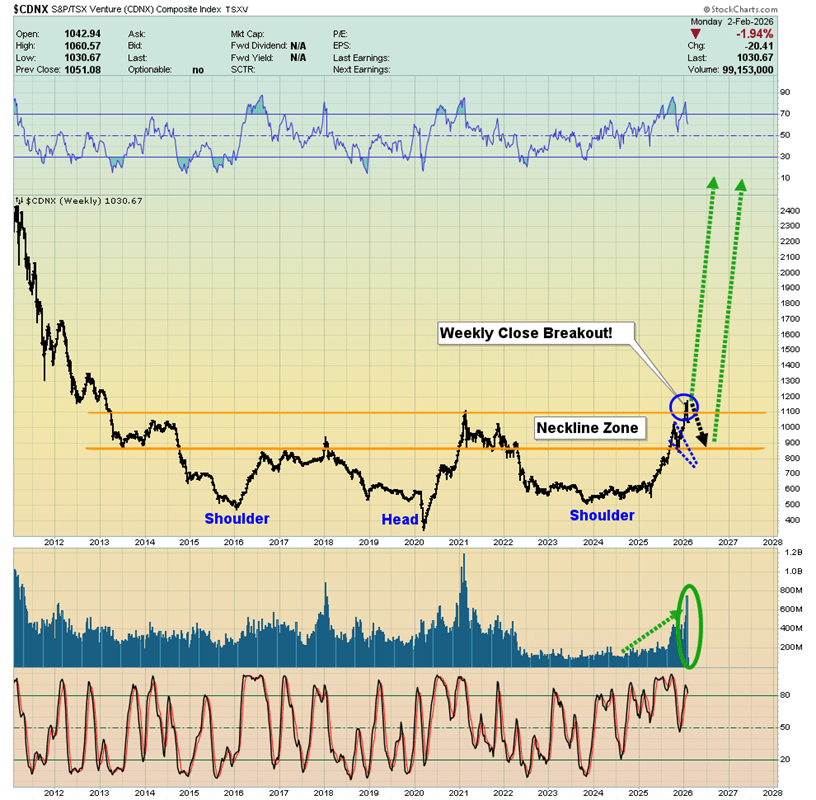

As for the miners, they too presented exceptional buying opportunities when gold dipped to $4,400. The CDNX is now starting to emerge from a decade-long base, with price action that closely resembles gold’s breakout above $2,000. The initial rally may appear deceptive, but it is genuine—because this type of breakout unfolds as a process rather than a single, short-lived move. Notably, trading volumes across CDNX-listed stocks have surged, reinforcing the strength of the move.

While pockets of speculative excess briefly appeared in gold and silver bullion, such froth has been absent in the mining sector. Several silver explorers nearing production are projecting all-in sustaining costs well below $20, while gold explorers with large-scale projects are reporting AISC figures under $2,000. The conclusion is clear: junior gold and silver miners may represent the most undervalued segment in market history.

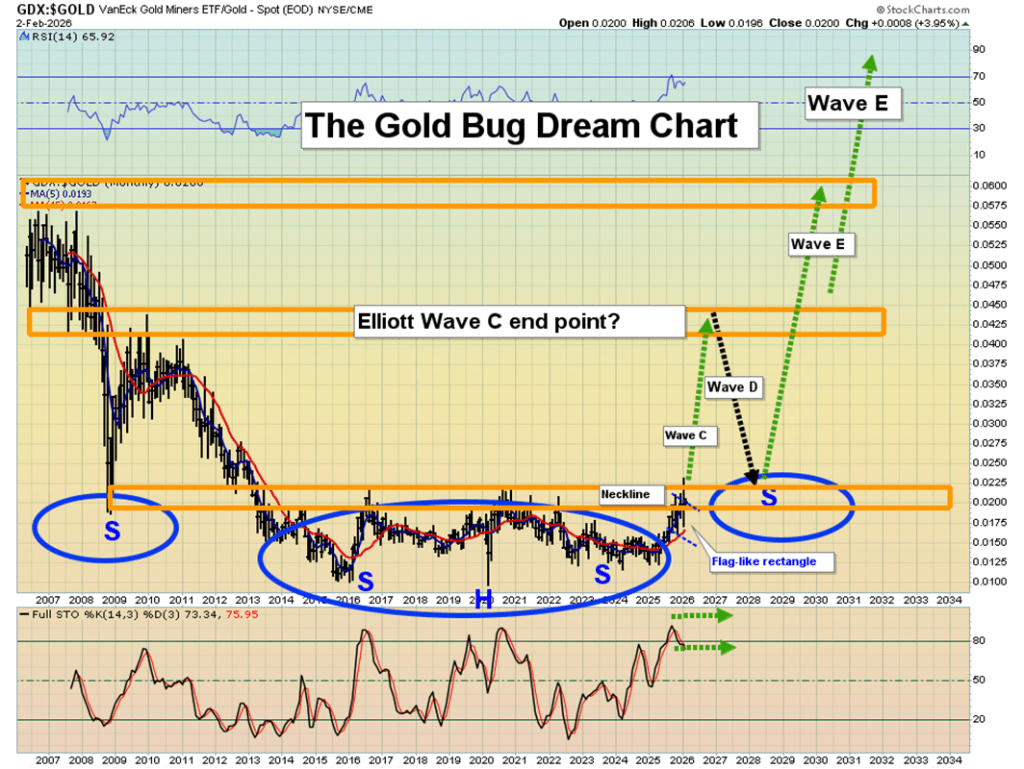

And what about the senior miners? The GDX versus gold chart is striking. Since the 2015 low—when the head of a massive inverse head-and-shoulders pattern began to form—I’ve been guiding investors through this setup. That structure points not merely to years, but potentially decades of strong performance for gold equities. In alignment with the CDNX-to-fiat picture, the breakout process is now underway.

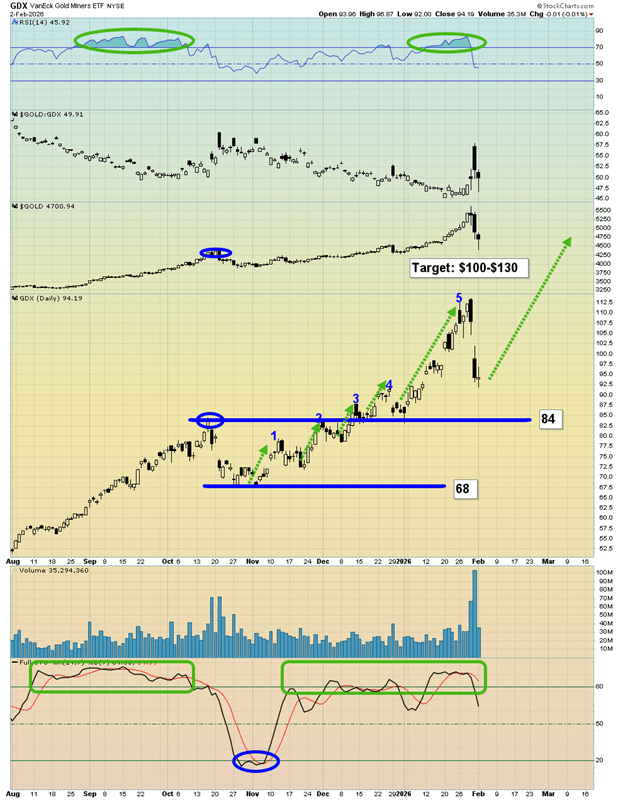

The GDX daily chart delivers a real “wow factor.” The latest five-wave advance was remarkable—and signs suggest a new leg higher may already be unfolding. Notably, GDX’s recent pullback held well above its October highs, even as gold retraced back to that level. That kind of relative strength is a powerful signal that further upside is likely.

Even if gold consolidates between $5,600 and $4,400, and silver oscillates between $120 and $70, GDX and many of its underlying stocks could still push on to new highs. With 2026 marking the Chinese Year of the Fire Horse—symbolizing bold action and the fight for freedom—the question arises: are gold and silver equities poised for their own moment of liberation, breaking out to extraordinary new levels? The evidence suggests they are.

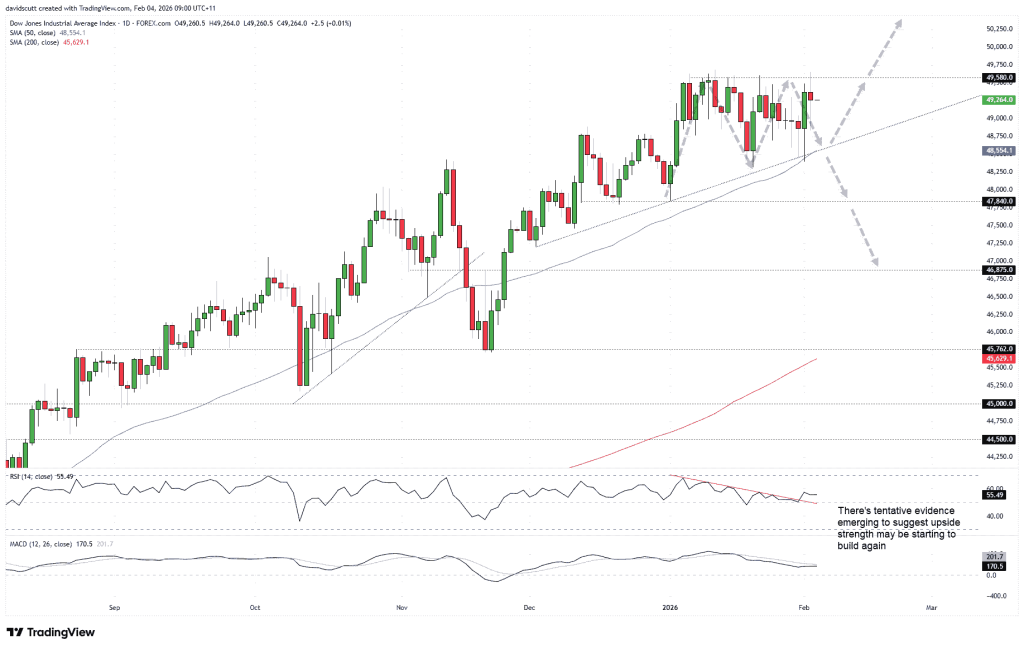

The Dow Jones continues to trade within an increasingly narrow range, as buyers find support along the December trendline while sellers cap advances near 49,580. The longer this compression persists, the higher the likelihood of a decisive and volatile breakout once the range is resolved.

Triangle pattern continues to tighten as pressure mounts.

49,580 stands as the critical upside barrier.

The breakout will determine direction, not strength.

Something has to give in the Dow Jones contract as price action continues to compress within an ascending triangle. Buyers remain active along the trendline support drawn from early December, while sellers continue to defend the 49,580 area. The market is effectively locked in a stalemate, and the longer this coiling persists, the greater the likelihood of a sharp, potentially explosive move once the pattern finally resolves.

Traditionally, this setup favors a bullish resolution, opening the door to fresh record highs, with a push beyond 51,000 possible given the placement of the triangle. A decisive break and close above 49,580 would allow long positions to be established above the level, with stops placed just below for risk management. While the 50,000 mark will naturally attract close attention due to its psychological importance, I would prefer to see a clear topping formation before reassessing whether to trim, exit, or maintain positions.

That said, technical conventions do not always play out—particularly against a backdrop of elevated valuations—so traders should remain mindful of the potential for a downside break from the pattern.

For now, the December uptrend is tracking closely alongside the 50-day moving average, creating a key zone where both long and short opportunities could emerge, depending on price behavior, should another pullback unfold.

A successful test and rebound from support could offer opportunities to establish long positions, targeting a retest of resistance near 49,580. Conversely, a decisive break and close below this zone would flip the bias, opening the door for short positions with stops placed above the trendline for protection. On the downside, 47,840 emerges as the first notable objective, aligning with multiple rebound points seen in December. Below that, 47,200—where the current uptrend originated—comes into focus, followed by the 46,875 area, which saw considerable two-way price action in the final quarter of 2025.

Adding some support to the bullish case, the 14-period RSI has broken its downward trend and is holding above the 50 level, indicating that downside momentum has stalled for now. The MACD echoes this view, turning back toward its signal line from below while remaining in positive territory. Overall, the signals suggest a neutral near-term bias, though with a slight edge still favoring the bulls.

The United Nations is considering a global tax framework that would tie oil and gas industry profits to climate compensation, though deep divisions among member states leave the outcome uncertain. Attempts to hold major energy producers financially accountable for climate change are not new. However, as the costs of the energy transition mount and legal efforts deliver mixed results, taxation is increasingly being viewed as an alternative policy instrument.

The United Nations is currently weighing the creation of a new international tax cooperation framework that could, among other objectives, channel funds from the oil and gas industry toward climate-related compensation. While the proposal reflects a familiar ambition to hold the industry financially accountable for climate change, its prospects remain uncertain.

The initiative falls under the Framework Convention on International Tax Cooperation, which is being negotiated at UN headquarters in New York. The broader goal is to strengthen global tax collection mechanisms and increase taxation on the world’s wealthiest entities and individuals. Sustainability features prominently in the discussions, with many countries—particularly those experiencing frequent climate-related disasters—supporting efforts to make major oil producers contribute financially. At the same time, resistance remains strong among other member states that oppose assigning climate liability to the energy sector or implementing a global wealth tax.

Recent proposals have suggested linking oil and gas profits directly to climate compensation payments. However, critics argue that these ideas lack sufficient clarity and enforcement power, limiting their viability. Supporters note that such measures could have generated as much as $1 trillion in additional revenue since the 2015 Paris Agreement, highlighting the scale of the opportunity lost if no agreement is reached.

Any move to formally tax Big Oil for its alleged role in man-made climate change would almost certainly provoke a strong response from the industry, likely through legal challenges. This would build on an already extensive record of climate-related litigation, where activist groups have achieved mixed results.

In the United States, California launched a lawsuit against major oil companies in 2024, accusing them of downplaying the climate risks associated with fossil fuels. The case targets companies including Exxon Mobil, Chevron, BP, and ConocoPhillips. State Attorney General Rob Bonta later strengthened the case by adding a provision aimed at forcing companies to surrender profits derived from alleged wrongful conduct. However, the lawsuit’s progress remains unclear, and California officials have recently softened their rhetoric toward oil companies in an effort to keep refineries operating and prevent fuel price spikes.

Maine has pursued a similar legal path, filing a “climate deception” lawsuit against several oil majors and the American Petroleum Institute. A federal judge allowed the case to proceed last year, with plaintiffs alleging that the defendants concealed information about the environmental and economic consequences of fossil fuel use.

This wave of so-called climate lawfare has become a favored strategy among activists seeking to penalize the fossil fuel industry. Yet given the uncertain outcomes of court cases, taxation is increasingly viewed as a more reliable alternative. The energy transition has proven far more expensive than initially anticipated, and governments are searching for sustainable funding sources.

Big Oil remains an obvious target due to its substantial profits from essential energy commodities that are widely blamed for climate change. Whether the UN negotiations ultimately result in a binding global tax remains to be seen. Even if they do, governments hoping for swift revenue may need patience—because the oil and gas industry is unlikely to accept such measures without a prolonged fight.

Solana remains below the $100 level on Wednesday after shedding more than 6% in the previous session.

Weakening retail sentiment alongside subdued institutional interest points to a growing bearish bias.

From a technical perspective, rising selling pressure suggests further downside toward the $85 region.

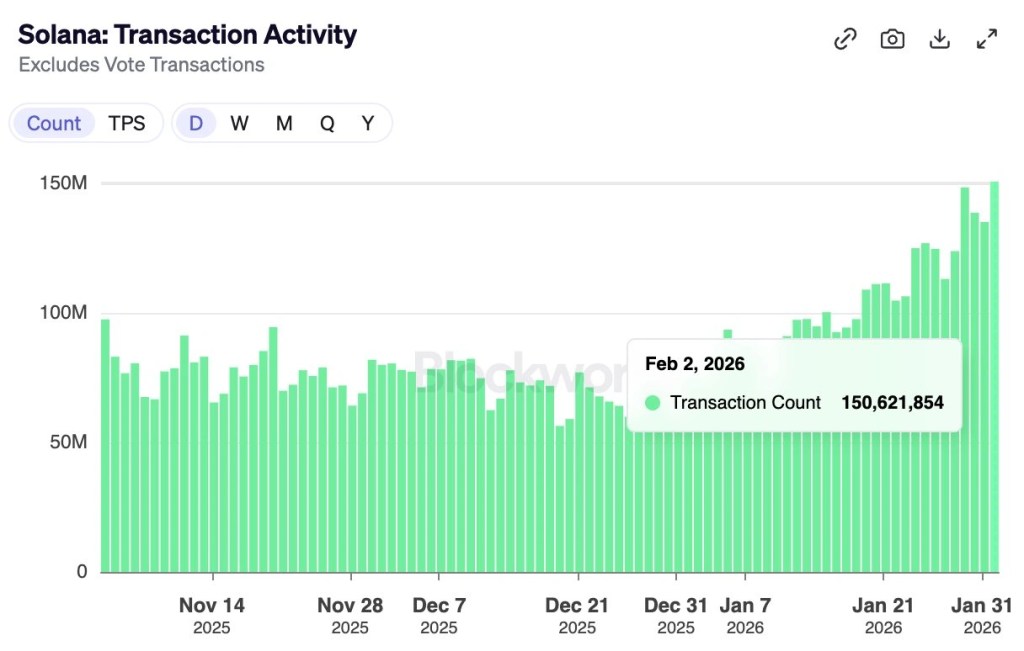

Solana (SOL) remains below the $100 mark at press time on Wednesday, following a decline of more than 6% in the prior session amid broader weakness across the cryptocurrency market. Both institutional and retail interest in Solana continue to fade, even as on-chain metrics recorded a record 150 million daily transactions on Tuesday. From a technical standpoint, strengthening bearish momentum points to the risk of a further slide toward the $85 level.

Solana continues to see robust on-chain user activity, with daily transaction volume reaching a record high on Tuesday. According to Blockworks data, the network processed over 150 million transactions during the day, averaging approximately 1,743 transactions per second.

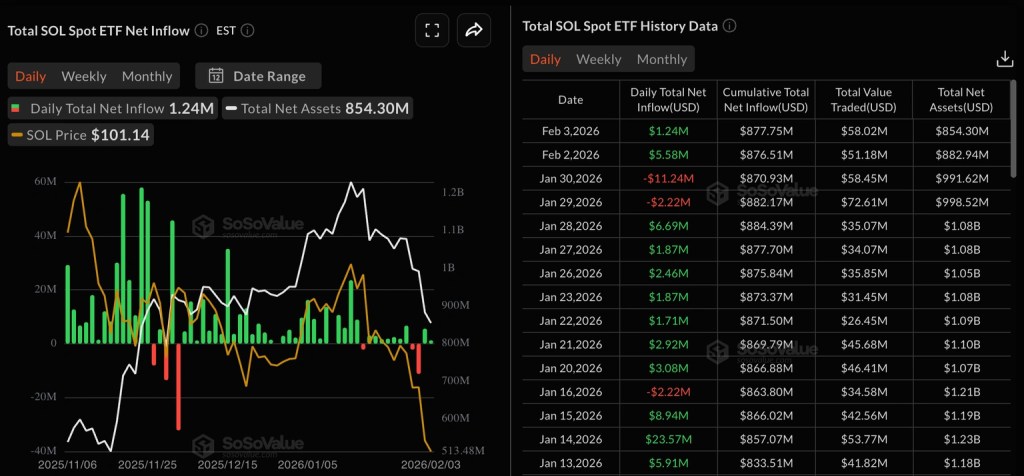

Despite resilient on-chain activity, institutional inflows have stayed muted over the past three weeks, averaging no more than $9 million per day since January and including three sessions of net outflows. Data from Sosovalue shows that U.S. Solana-focused exchange-traded funds (ETFs) posted inflows of $1.24 million on Tuesday, following a $5.58 million inflow recorded on Monday.

Meanwhile, signals from the derivatives market point to a bearish tilt in Solana sentiment, accompanied by capital outflows. CoinGlass data shows that SOL open interest fell by 1.24% over the past 24 hours to $6.37 billion, suggesting capital exited the market through position closures or reduced leverage.

Liquidation data further highlights the bearish bias, with long liquidations totaling $22.31 million during the period—more than five times the $4.39 million in short liquidations.

In addition, Solana’s OI-weighted funding rate has slipped to -0.0238%, underscoring increasingly negative sentiment as traders holding or initiating short positions are willing to pay a premium to maintain them.

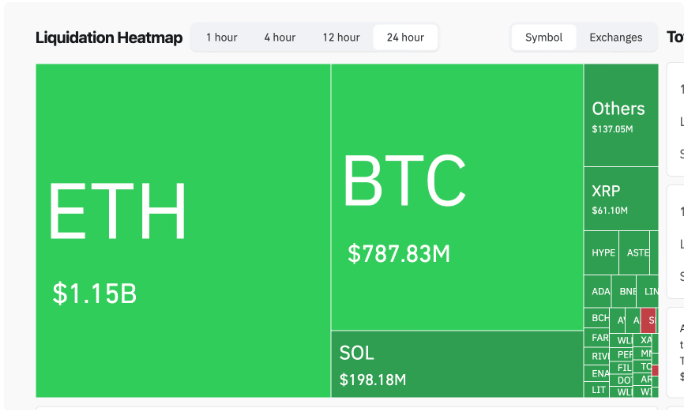

The waning bullish appetite for Solana mirrors the broader market downturn, which has seen total liquidations of around $735 million over the past 24 hours, including approximately $529 million from long positions.

Moreover, the broader cryptocurrency market remains under pressure, with the Fear and Greed Index falling to 14 on Wednesday—pointing to extreme risk-averse sentiment among investors. Without a meaningful improvement in market mood, Solana may face additional downside.

Technical Outlook: Is Solana headed toward $85?

Solana continues to trade below its 50-, 100-, and 200-day Exponential Moving Averages at $127, $139, and $153, respectively, keeping the broader trend firmly under pressure. The shorter-term EMAs remain positioned beneath the longer-term averages, forming a bearish alignment that has capped recent rebound attempts.

A sustained move below the $95 level would leave the S1 Pivot Point at $85 as the next downside target.

Momentum indicators remain decisively negative, with the MACD and signal line both trending lower and extending further into bearish territory on the daily chart. Meanwhile, the Relative Strength Index stands at 28 and is consolidating within oversold territory, a setup that could still allow for additional downside despite stretched conditions.

On the upside, a recovery back above the $100 level could shift focus toward the 50-day EMA near $127 as the initial upside objective.

The Japanese yen stays under pressure as fiscal worries and political uncertainty outweigh stronger-than-expected data.

Concerns over possible intervention and the BoJ’s increasingly hawkish stance may deter traders from adding new bearish yen positions.

Rising expectations of further Fed easing weigh on the U.S. dollar and could limit upside in USD/JPY.

The Japanese yen (JPY) continues its downward trajectory against the U.S. dollar for a fourth consecutive session on Wednesday, sliding to a near two-week low during Asian trading. Persistent concerns over Japan’s fiscal position—linked to Prime Minister Sanae Takaichi’s expansionary spending agenda—remain a key drag on the currency. In addition, heightened political uncertainty ahead of the February 8 snap election further weakens sentiment toward the yen, driving USD/JPY above the 156.00 level.

At the same time, markets remain cautious amid the risk of coordinated Japan–U.S. intervention aimed at curbing excessive yen weakness. Expectations of gradual policy normalization by the Bank of Japan may also discourage traders from adding aggressive bearish positions. Meanwhile, expectations that the Federal Reserve will deliver two additional rate cuts limit U.S. dollar demand, potentially capping further upside in USD/JPY ahead of later U.S. economic data releases.

Yen sellers stay in charge as fiscal strains and political uncertainty persist.

Japan’s services sector gathered momentum at the start of 2026, with business activity expanding for a tenth straight month and at the fastest pace in nearly a year. The Jibun Bank Services PMI rose to 53.7 from 51.6 in December, coming in slightly above market expectations of 53.4. The figures point to a more sustained recovery in the services industry, which represents about 70% of Japan’s GDP.

Despite the encouraging data, market reaction was subdued as concerns over Japan’s fiscal outlook continued to weigh on sentiment. Investor unease has been amplified by Prime Minister Sanae Takaichi’s expansionary fiscal agenda, including aggressive spending plans and proposed tax cuts. As part of her campaign ahead of the February 8 snap lower house election, Takaichi has pledged to suspend the 8% consumption tax on food for two years, bringing renewed focus to Japan’s already stretched public finances and keeping the yen under pressure on Wednesday.

Meanwhile, a recent and unusual rate check by the New York Federal Reserve was interpreted as the clearest indication so far of coordination between Japanese and U.S. authorities to curb excessive yen weakness. This lowers the bar for potential intervention and could help limit further JPY losses, particularly alongside expectations of a more hawkish Bank of Japan.

The Summary of Opinions from the BoJ’s January meeting, released Monday, revealed that policymakers discussed rising inflationary pressures stemming from a weaker yen. Board members also agreed that additional rate hikes would be appropriate over time, a stance that could provide underlying support for the JPY.

On the other side, the U.S. dollar has struggled to extend last week’s rebound from a four-year low, despite support from the nomination of Kevin Warsh as the next Federal Reserve chair. Even the approval of a government funding package to end a partial shutdown failed to generate meaningful upside for the greenback.

Looking ahead, traders are awaiting the U.S. ADP employment report and the ISM Services PMI. In addition, remarks from influential FOMC members could shape near-term USD demand amid expectations for two more Fed rate cuts in 2026, with implications for the USD/JPY pair.

USD/JPY must clear the 156.50 confluence zone to reinforce bullish momentum.

Wednesday’s push above the 156.00 handle builds on the overnight breakout through the 50% retracement of the 159.13–152.06 decline, tilting the near-term bias in favor of USD/JPY bulls. The 14-period Relative Strength Index stands at 66.9, remaining below overbought territory and pointing to a solid, albeit increasingly mature, upswing.

That said, the MACD histogram, while still in positive territory, is narrowing—an early sign of waning bullish momentum. The MACD line remains above the Signal line, with both oscillating close to the zero level, underscoring a more cautious and transitional setup.

As a result, further upside is likely to face notable resistance around the 156.51 confluence, which combines the 100-period Simple Moving Average on the 4-hour chart and the 61.8% Fibonacci retracement. A sustained move above this zone would be required to reassert a constructive short-term outlook.

A decisive break could pave the way toward the 78.6% retracement at 157.62. Conversely, an inability to clear this hurdle would leave the rebound exposed to renewed downside pressure. Moreover, USD/JPY continues to trade below a downward-sloping 100-period SMA, suggesting that upside attempts may remain constrained for now.

U.S. President Donald Trump has signed legislation bringing the government shutdown to an end, an outcome that markets largely took in stride given how routine such episodes have become.

However, UBS Chief Economist Paul Donovan noted that Democrats have coalesced in opposition to confirming former Federal Reserve Governor Kevin Warsh as the next Fed chair until the administration’s legal challenge involving the Fed is resolved. This impasse raises the possibility that Chair Jerome Powell could remain in office beyond May.

Resolution of the government shutdown influences market conditions.

Government dysfunction in the U.S. has become so routine that financial markets largely ignored it.

Democrats have indicated they will block the confirmation of former Federal Reserve Governor Warsh as the next Fed chair unless the administration halts its legal actions against the Federal Reserve.

While this outcome was widely anticipated, it increases the likelihood that Chair Powell could remain as FOMC chair—though not as Chair of the Board of Governors—beyond May.

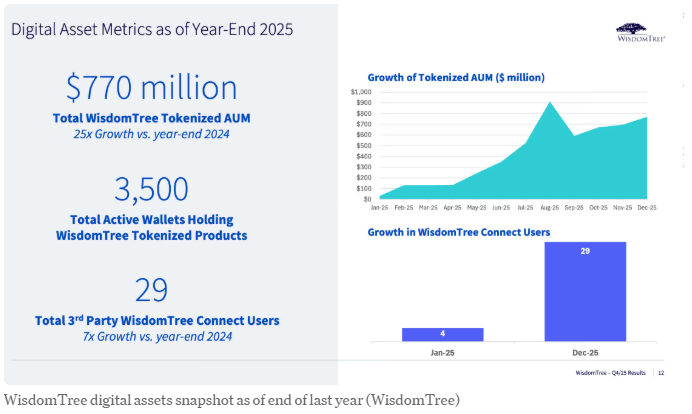

WisdomTree CEO Jonathan Steinberg said the firm’s push into tokenization is approaching profitability, underscoring a shift in which crypto has evolved from a small-scale experiment into a core pillar of the company’s strategy.

The asset manager has rapidly expanded its digital-asset business, growing tokenized assets under management from roughly $30 million to about $750 million, while extending its offerings across additional blockchains, including Solana.

Steinberg described crypto as a foundation for modernizing financial infrastructure, pointing to initiatives such as tokenized investment products, the WisdomTree Connect platform, and a deliberate focus on compliance-oriented tokenization technology as central to the firm’s long-term growth plans.

New York — WisdomTree’s crypto business has moved beyond the experimental phase and is now central to the firm’s long-term strategy, with profitability coming into view, CEO Jonathan Steinberg said during a fireside chat at the Ondo Summit in New York on Tuesday.

“We want to continue to scale,” Steinberg said, noting that the firm’s digital-asset business expanded from roughly $30 million to about $750 million in assets last year. While WisdomTree does not yet generate profits from its crypto operations, Steinberg said the company is now “within line of sight of taking this to a profitable business.”

The $150 billion asset manager has been investing heavily in blockchain infrastructure, rolling out tokenized investment products and expanding to additional blockchains, including Solana. Steinberg emphasized that the push reflects long-term conviction rather than short-term experimentation. “It’s still early days, but it’s not an experiment now,” he said. “We have conviction, and we believe that eventually everything will move on-chain.”

WisdomTree’s growing commitment to digital assets was also highlighted in its latest earnings presentation, which showed total tokenized assets under management rising to $770 million—an increase of roughly 25 times from 2024 levels.

WisdomTree has emerged as an early and aggressive leader among traditional asset managers in the digital-asset space, rolling out a range of tokenized funds and recently broadening distribution through WisdomTree Connect, a platform that allows these assets to move seamlessly across self-custodied wallets and institutional systems.

The firm has also made a strategic push into blockchain infrastructure, most notably through its acquisition of Securrency, a compliance-focused tokenization company that was later sold to the DTCC. Steinberg said the deal laid the groundwork for “compliance-aware tokens” and programmable finance, forming the backbone of WisdomTree’s long-term, interoperable digital-asset strategy.

For Steinberg, crypto represents far more than a new product line—it signals a transformation of the financial system itself. “This is bigger than asset management; it’s really about financial services,” he said. He noted that many financial institutions are built on layers of legacy infrastructure accumulated over centuries, underscoring the need for modernization.

The steep sell-off in cryptocurrencies eased on Tuesday after the U.S. House narrowly approved a funding package, sending the legislation to President Donald Trump’s desk and effectively ending the partial government shutdown.

The House passed the bill by a slim 217–214 margin, clearing the way for the government to reopen once the president signs it. While lawmakers will continue negotiations over funding for the Department of Homeland Security in the coming days, most major federal agencies will remain funded.

The development helped pause a panic-driven rout in crypto markets earlier in the session. Bitcoin briefly slid to around $72,800—its lowest level since before Trump’s election victory in November 2024—before stabilizing. At roughly $74,800, bitcoin was still down about 4.5% over the past 24 hours.

Ether traded near $2,181, down 7% on the day and roughly 26% over the past week. Other major tokens, including XRP and Solana, recorded similar losses.

U.S. equities also rebounded from their intraday lows but remained sharply lower overall, with the Nasdaq down around 2% and the S&P 500 lower by about 1.3%.

WTI crude prices edged higher to around $63.75 during Wednesday’s Asian trading session.

The move came after the U.S. military said it shot down an Iranian drone that “aggressively approached” a U.S. aircraft carrier, heightening geopolitical tensions.

Oil prices were also supported by data showing U.S. crude inventories recorded their largest decline since August 2023.

West Texas Intermediate (WTI), the U.S. crude oil benchmark, was trading near $63.75 during Asian hours on Wednesday, edging higher amid rising concerns over escalating tensions between the United States and Iran. Market participants are also positioning ahead of the release of the U.S. Energy Information Administration’s (EIA) crude oil inventory report later in the day.

According to CNBC, the U.S. military shot down an Iranian drone on Tuesday that had “aggressively” approached the USS Abraham Lincoln aircraft carrier in the Arabian Sea. The incident comes at a time of heightened Middle East tensions, as U.S. President Donald Trump weighs potential military action against Iran.

Iran has also insisted that talks with the United States this week be held in Oman rather than Turkey, and that negotiations be limited to bilateral discussions focused solely on nuclear issues, further complicating an already fragile diplomatic process. Any escalation in tensions between Washington and Tehran—OPEC’s fourth-largest crude producer—could provide near-term support to WTI prices.

Meanwhile, the American Petroleum Institute’s (API) weekly report showed that U.S. crude inventories fell by 11.1 million barrels in the week ended January 30, sharply deeper than the 250,000-barrel decline seen the previous week and well below market expectations for a 700,000-barrel build. The sizeable drawdown in stockpiles could lend additional support to oil prices.

On the downside, renewed demand for the U.S. dollar may cap gains in dollar-denominated commodities. U.S. President Donald Trump’s nomination of Governor Kevin Warsh as the next Federal Reserve chair has led traders to expect a slower pace of interest rate cuts and a greater emphasis on reducing the Fed’s balance sheet under his leadership.

Silver prices climbed to around $87.60 during Wednesday’s Asian trading session.

However, shifting expectations surrounding the next Federal Reserve chair could limit further upside in the metal.

Demand for safe-haven assets strengthened after reports that the United States shot down an Iranian drone that was approaching an aircraft carrier.

Silver prices (XAG/USD) climbed to around $87.60 during Asian trading on Wednesday, rebounding after a historic correction last week as dip-buying activity returned to the market.

On Friday, U.S. President Donald Trump nominated Kevin Warsh to replace Jerome Powell as the next Chair of the Federal Reserve, with Warsh expected to assume the role when Powell’s term ends in May. Expectations that Trump’s nominee may favor keeping interest rates elevated to combat inflation have supported the U.S. dollar, potentially weighing on dollar-denominated commodities such as silver.

Precious metals have also faced pressure from margin hikes by the CME Group. Over the weekend, the exchange raised margin requirements for gold and silver, forcing many leveraged traders to liquidate positions to meet higher costs.

On the other hand, safe-haven demand has been underpinned by rising geopolitical risks and economic uncertainty. Reuters reported on Tuesday that the U.S. military shot down an Iranian drone that “aggressively” approached the Abraham Lincoln aircraft carrier in the Arabian Sea.

Separately, Iran requested that this week’s negotiations with the United States be held in Oman rather than Turkey and limited to bilateral discussions focused solely on nuclear issues. President Trump warned that with U.S. warships moving toward Iran, “bad things” could occur if an agreement is not reached.

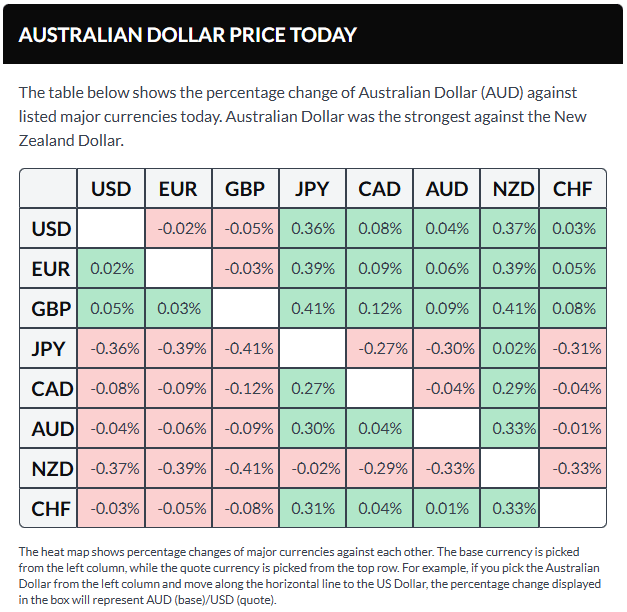

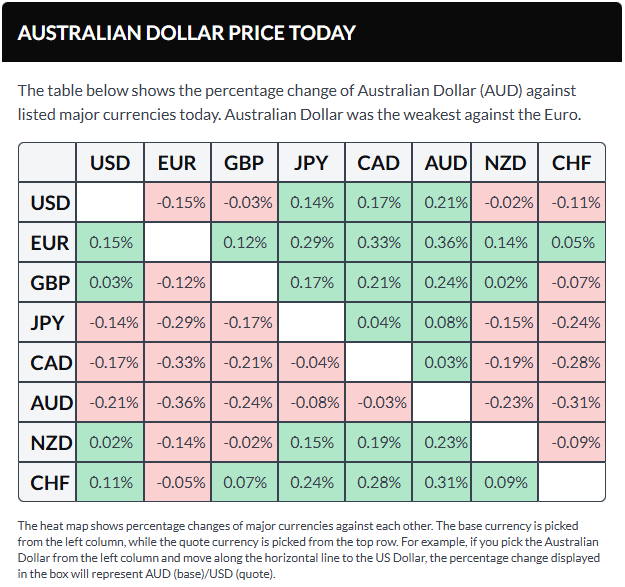

The Australian dollar strengthened after the Composite PMI surged to 55.7 in January, marking the fastest pace of expansion in nearly four years.

The Aussie also benefited as markets priced in an 80% probability of an interest rate hike in May, along with around 40 basis points of additional policy tightening.

Meanwhile, the U.S. dollar remained subdued for a second straight session.

The Australian dollar strengthened against the U.S. dollar on Wednesday, extending gains of more than 1% from the previous session. The AUD/USD pair held firm after China’s Services Purchasing Managers’ Index (PMI) rose to 52.3 in January from 52.0 in December, beating market expectations of 51.8. As China is Australia’s largest trading partner, improvements in Chinese economic activity tend to support the Aussie.

The AUD also drew support from upbeat domestic PMI data. Seasonally adjusted figures from S&P Global showed Australia’s Composite PMI climbed to 55.7 in January from 51.0 in December, marking the strongest expansion in 45 months. The Services PMI jumped to 56.3 from 51.1, its highest reading since February 2022, exceeding the flash estimate of 56.0 and remaining well above the 50.0 threshold. This extended the run of expansion in services activity to two years.

The Reserve Bank of Australia raised its Official Cash Rate by 25 basis points to 3.85% on Tuesday, pointing to stronger-than-expected economic growth and persistently elevated inflation. As the tightening cycle gathers momentum, markets have increased the odds of another rate hike in May to around 80% and are now pricing in roughly 40 basis points of additional tightening through the rest of the year.

Speaking at the post-meeting press conference, RBA Governor Michele Bullock said inflationary pressures remain uncomfortably high, warning that a return to the target range will take longer than previously expected and is no longer acceptable. She emphasized that the board will remain data-dependent and avoid providing forward guidance.

U.S. dollar little changed after recent losses

The U.S. Dollar Index (DXY), which tracks the greenback against six major currencies, remained subdued for a second straight session, trading near 97.40 at the time of writing.

Data released on Monday showed an unexpected rebound in U.S. manufacturing activity, underscoring economic resilience. The ISM Manufacturing PMI rose to 52.6 in January from 47.9 in December, comfortably beating expectations of 48.5.

Markets have also been assessing President Donald Trump’s nomination of Kevin Warsh as the next Federal Reserve chair, a move widely interpreted as signaling a more disciplined and cautious approach to monetary easing. The dollar found some support earlier as risk sentiment improved after the U.S. Senate reached an agreement to advance a government funding package, averting a shutdown, according to Politico.

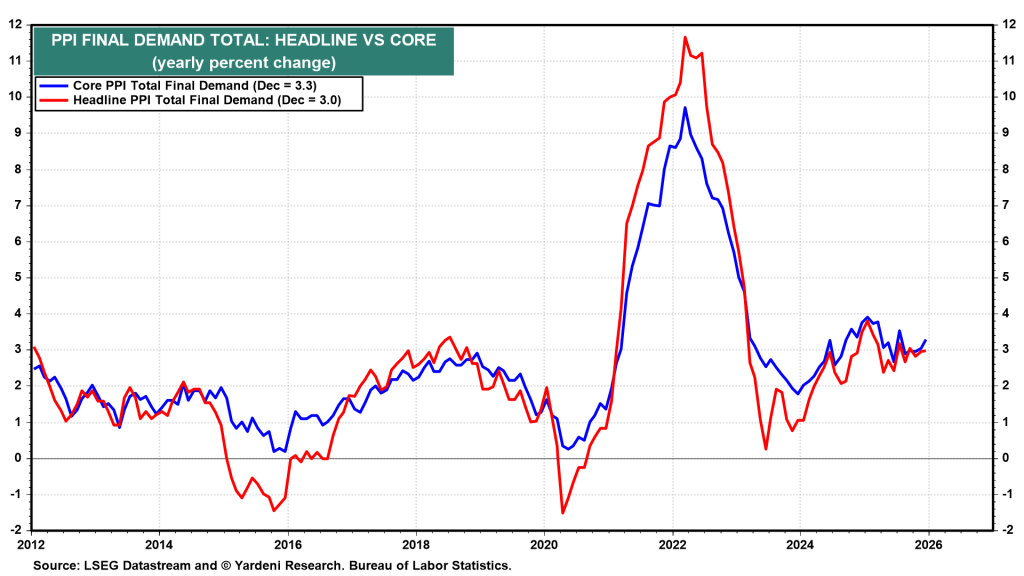

Producer-side inflation in the U.S. remained firm, reinforcing the Fed’s policy stance. Headline PPI held steady at 3.0% year-over-year in December, unchanged from November and above expectations for a slowdown to 2.7%. Core PPI, which excludes food and energy, accelerated to 3.3% from 3.0%, defying forecasts for a decline to 2.9% and highlighting persistent upstream price pressures.

Fed officials struck a cautious tone. St. Louis Fed President Alberto Musalem said additional rate cuts are not warranted at this stage, describing the current 3.50%–3.75% policy rate range as broadly neutral. Atlanta Fed President Raphael Bostic echoed this view, urging patience and arguing that policy should remain modestly restrictive.

In Australia, inflation data showed mixed signals. The RBA’s trimmed mean inflation rose 0.2% month-over-month and 3.3% year-over-year, while the monthly CPI jumped 1.0% in December, exceeding forecasts of 0.7%. Export prices climbed 3.2% quarter-on-quarter in Q4 2025—the first increase in three quarters and the strongest gain in a year—while import prices rose 0.9%, beating expectations for a decline.

China’s RatingDog Manufacturing PMI edged up to 50.3 in January from 50.1 in December, in line with expectations and marking the fastest pace of factory expansion since October.

Additional Australian indicators pointed to easing inflation momentum and improving labor demand. The TD-MI Inflation Gauge rose 3.6% year-over-year in January, while monthly inflation increased just 0.2%, the weakest pace since August. Meanwhile, ANZ Job Advertisements surged 4.4% month-over-month in December, posting the strongest increase since February 2022 and signaling renewed momentum in hiring toward year-end.

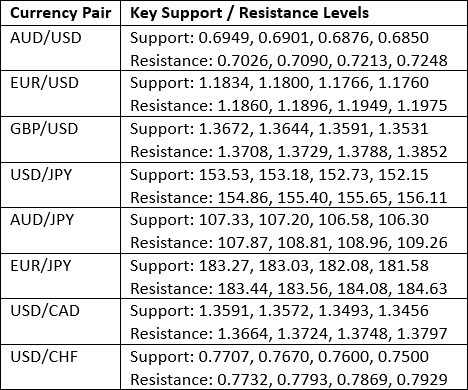

Australian dollar rebounds toward three-year highs near 0.7100

The AUD/USD pair was trading near 0.7030 on Wednesday. Analysis of the daily chart shows the pair remains within an ascending channel, pointing to a sustained bullish bias. The 14-day Relative Strength Index (RSI) stands at 73.30, signaling strong upward momentum, though conditions appear increasingly stretched.

AUD/USD recently rebounded toward 0.7094, its highest level since February 2023, reached on January 29. A decisive break above this resistance could open the way for a move toward the upper boundary of the ascending channel around 0.7210. On the downside, initial support is seen at the nine-day Exponential Moving Average (EMA) near 0.6964, which coincides with the channel’s lower boundary. A deeper pullback could bring the 50-day EMA at 0.6759 into focus.

Asian equity markets were mixed on Wednesday, with South Korean stocks climbing to a record high, though broader gains were limited as a rally in technology shares lost momentum following a weaker close on Wall Street.

U.S. markets finished lower overnight, led by declines in the technology sector as concerns resurfaced over potential disruption stemming from the rapid pace of advancements in artificial intelligence.

The Nasdaq underperformed broader market indexes, as investors adopted a cautious stance ahead of key earnings reports from major U.S. technology companies.

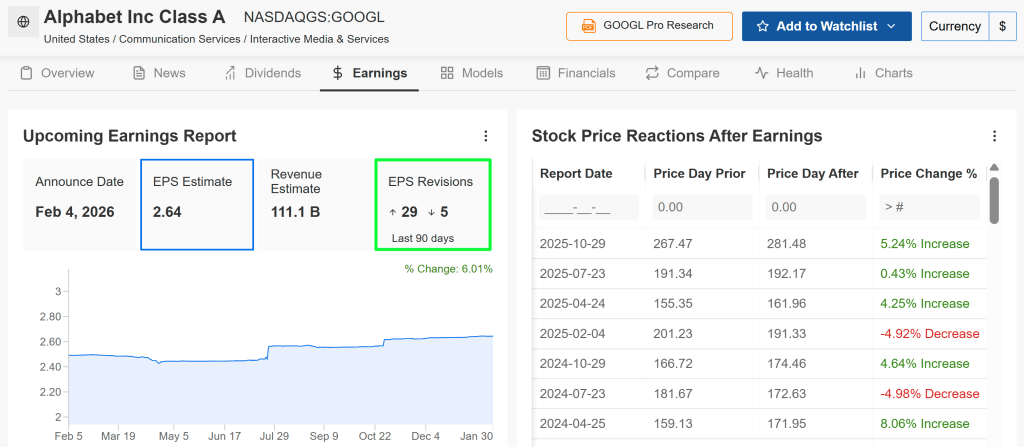

Alphabet (NASDAQ: GOOGL) is set to release its results later on Wednesday, followed by Amazon (NASDAQ: AMZN) on Thursday, with both reports expected to serve as important gauges of demand for advertising, cloud services, and AI-related spending.

Asian stocks mixed as South Korea’s KOSPI hits record high

Asian markets were coming off a strong previous session, when equities rallied broadly across the region.

South Korea’s KOSPI climbed nearly 1% on Wednesday to a record high of 5,361.85 points, after surging almost 7% the day before on strong gains in heavyweight chipmakers and technology stocks.

Japan’s Nikkei 225 slipped 0.7% following a roughly 4% advance in the prior session.

Sentiment toward artificial intelligence remained volatile, as overnight declines in U.S. technology shares weighed on regional peers and triggered some profit-taking after recent sharp rallies.

Elsewhere in the region, China’s Shanghai Composite edged up 0.1%, while the blue-chip CSI 300 slipped 0.2%. Hong Kong’s Hang Seng fell 0.5%.

Australia’s S&P/ASX 200 added 0.5%, Singapore’s Straits Times Index was flat, and futures for India’s Nifty 50 ticked higher. The Nifty surged nearly 3% on Tuesday after the U.S. signed a trade agreement with India that sharply reduced tariffs.

Fed overhaul concerns persist as China services PMI comes into focus

Investors also remained cautious over President Donald Trump’s nomination of former Federal Reserve governor Kevin Warsh as the next Fed chair.

Warsh is widely regarded as having a hawkish policy stance, fueling concerns that U.S. interest rates may stay higher for longer.

In China, a private-sector survey released on Wednesday showed that the services sector expanded in January at its fastest pace in three months.

While the data provided some reassurance about underlying demand in the world’s second-largest economy, investor sentiment remained restrained amid ongoing concerns about uneven growth and subdued consumer confidence.

Bitcoin fell sharply on Tuesday, giving up all gains made since President Donald Trump’s election victory, as selling pressure remained intense following heavy liquidations over the weekend. Ongoing uncertainty surrounding U.S. monetary policy further weighed on sentiment.

The world’s largest cryptocurrency was last down 4.2% at $74,699.9 by 15:12 ET (20:12 GMT), marking its lowest level since early November 2024. Prices touched an intraday low of $73,004.3, leaving Bitcoin down roughly 59% from its record high and firmly entrenched in bear market territory.

Menno Martens, a crypto specialist and product manager at VanEck, said the market is simply entering another familiar phase of the cycle.

“There’s no question that this is a bear market,” Martens told Investing.com, noting that the current downturn differs from previous ones due to growing geopolitical and macroeconomic influences, particularly developments in the United States.

He explained that the path of this cycle does not mirror past bull and bear markets exactly, largely because of these new external factors. However, Martens emphasized that the broader outlook remains unchanged, adding that VanEck continues to maintain a long-term perspective despite the current bearish conditions.

Bitcoin weighed down by heavy liquidations and Trump’s Fed pick

The sharp sell-off in cryptocurrencies over the weekend was fueled by widespread liquidations of leveraged positions, underscoring the heavy speculative buildup that had accumulated during last year’s rally. Data from derivatives tracking firms showed that crypto positions worth several billion dollars were wiped out in a short span, with long trades accounting for most of the forced closures.

Thin market liquidity further amplified volatility, allowing relatively modest price moves to trigger cascading liquidations.

Investor sentiment has also been dampened by broader macroeconomic uncertainty. Markets are weighing the implications of Kevin Warsh’s nomination as the next chair of the U.S. Federal Reserve, prompting a reassessment of the outlook for interest rates.

Warsh is broadly perceived as leaning toward a more hawkish policy stance, stoking concerns that tighter financial conditions could persist for longer.

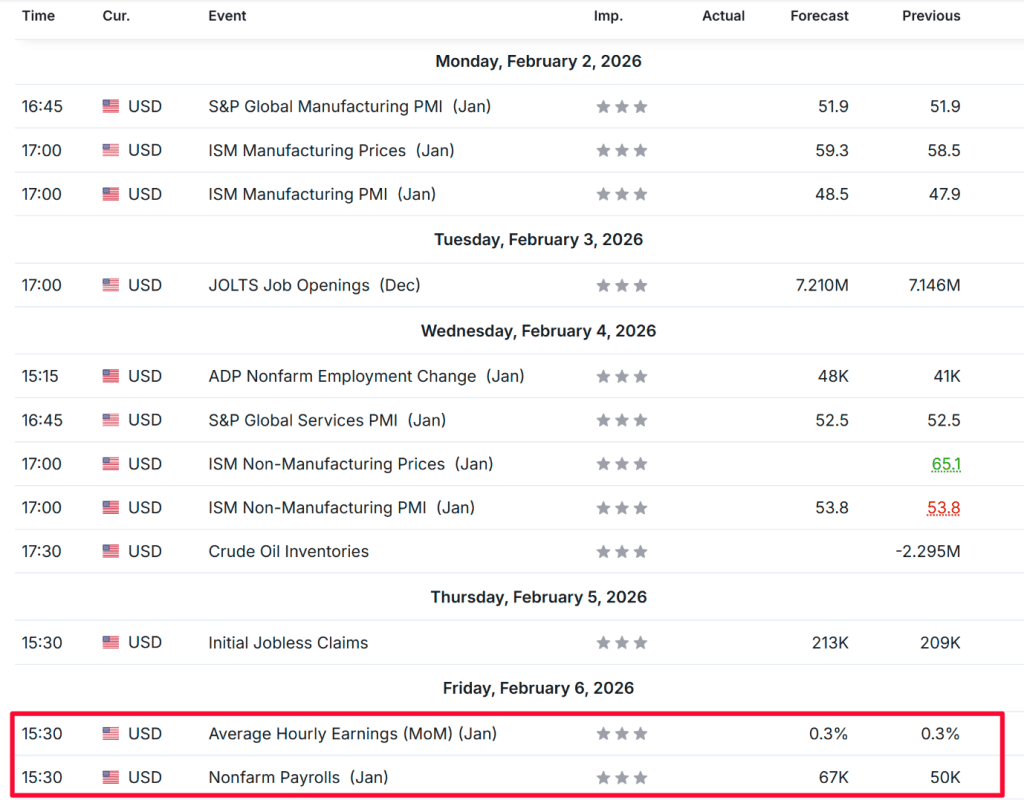

Separately, the release of January’s closely watched U.S. employment report—originally scheduled for Friday—has been delayed due to a partial government shutdown, according to the Bureau of Labor Statistics.

White House crypto meeting ends without agreement on stablecoin yields

The cryptocurrency industry and major U.S. banks remain divided over how to regulate stablecoin yields following a White House meeting, underscoring ongoing hurdles to advancing long-delayed crypto legislation, according to media reports.

Executives from crypto companies, representatives from large banks, and government officials gathered in Washington to discuss market-structure rules, but made little headway on the key question of whether stablecoin issuers should be permitted to offer yield-like returns.

Banks have warned that yield-bearing stablecoins could accelerate deposit outflows and threaten financial stability, while crypto firms argue that such features are essential for innovation, growth, and maintaining competitiveness.

Crypto prices today: altcoins rebound as Polygon surges 10%

Most altcoins also moved lower on Tuesday.

Ethereum, the world’s second-largest cryptocurrency, fell 4.9% to $2,242.43, while third-ranked XRP declined 3.6% to $1.58.

Solana dropped 4.1%, and Cardano eased 1.8%.

Among meme tokens, Dogecoin slipped 2.1%, while the $TRUMP token fell 1.4%.

Gold prices climbed back above key technical levels during Asian trading on Wednesday, as renewed signs of tension between the United States and Iran fueled safe-haven demand for the precious metal.

Bullion extended its rebound from Tuesday after sharply recovering from recent losses, with dip-buying activity also remaining strong following last week’s more than $1,000 price sell-off.

Spot gold gained 2% to $5,048.37 per ounce by 21:00 ET (02:00 GMT), while April gold futures advanced 2.8% to $5,017.19 per ounce.

Other precious metals also moved higher on Wednesday, building on the rebound seen in the previous session. Spot silver gained 0.5% to $85.5245 per ounce, while spot platinum climbed 1.7% to $2,256.04 per ounce.

Iran concerns return ahead of upcoming nuclear talks

Renewed concerns over escalating tensions between the United States and Iran were a key catalyst for safe-haven demand, particularly after overnight reports that U.S. forces shot down an Iranian drone over the Arabian Sea.

In a separate development, Iranian gunboats were reported to have approached a U.S.-linked oil tanker in the Strait of Hormuz.

These incidents partially offset earlier statements from both Tehran and Washington indicating that talks would be held this Friday. News of the planned negotiations had previously eased market anxiety and weighed on safe-haven demand for gold.

Gold’s recent pullback was largely driven by expectations that U.S. President Donald Trump’s nominee for Federal Reserve chair, Kevin Warsh, may adopt a less dovish stance than markets had anticipated. This fueled a sharp rally in the U.S. dollar, pressuring precious metals, while gold also faced profit-taking after surging to a record high near $5,600 per ounce last week.

Despite the recent decline, gold remains up nearly 15% so far in 2026.

ANZ analysts noted that the core fundamentals underpinning gold’s strength—safe-haven demand, robust physical buying, and ongoing central bank purchases—remain firmly intact.

Oil prices climbed sharply during Asian trading on Wednesday, driven by reports of escalating tensions between the United States and Iran, which heightened fears of possible supply disruptions in the Middle East.

Crude prices also found support from industry figures showing an unexpected and substantial drawdown in U.S. oil inventories last week, as severe cold weather across the country curtailed production.

April Brent futures advanced 1.2% to $68.15 per barrel, while U.S. West Texas Intermediate crude rose 1.4% to $63.69 per barrel as of 21:01 ET (02:01 GMT).

Overnight reports indicated that U.S. forces shot down an Iranian drone that was approaching a U.S. aircraft carrier in the Arabian Sea.

In a separate incident, several Iranian gunboats were observed nearing a U.S.-flagged oil tanker in the Strait of Hormuz.

These developments came just ahead of planned talks between Washington and Tehran later this week. However, Iranian officials have reportedly insisted that the negotiations—scheduled for Friday—be limited to bilateral discussions focused solely on nuclear issues, raising uncertainty over whether the talks will proceed at all.

U.S. President Donald Trump has warned of further military action if Iran fails to comply with U.S. demands to rein in its nuclear program, while Tehran has vowed strong retaliation against any U.S. aggression.

Any escalation of military activity in the Middle East could potentially disrupt regional oil supplies, a risk that has helped support crude prices in recent trading sessions.

U.S. oil inventories fall sharply amid production disruptions, API data shows

Oil prices also found support from industry figures showing a large and unexpected drawdown in U.S. crude inventories.

Data from the American Petroleum Institute indicated that U.S. stockpiles fell by 11.1 million barrels in the week ended January 30, sharply contrasting with expectations for a 0.7 million-barrel build.

API figures often signal a similar outcome in the official inventory report due later in the day.

The sizeable drawdown was driven by severe cold weather across the United States, which disrupted oil production nationwide and hampered exports from the Gulf Coast.

Supply disruptions in the U.S. have also contributed to stronger oil prices in recent weeks.

European stocks inched higher on Tuesday, supported by a solid overnight close on Wall Street, as the recent sell-off in precious metals appeared to be short-lived.

By 03:05 ET (08:05 GMT), Germany’s DAX was up 0.8%, France’s CAC 40 added 0.4%, and the U.K.’s FTSE 100 edged 0.1% higher.

Global markets—including European equities—have steadied after several days of heightened volatility, marked in particular by sharp declines in gold and silver prices late last week and over the weekend.

Precious metals rebounded on Monday, restoring some investor confidence and helping lift the blue-chip Dow Jones Industrial Average by more than 500 points, or around 1%, on Wall Street.

Market sentiment also improved after U.S. President Donald Trump announced late Monday that the United States had reached a trade agreement with India, cutting tariffs on Indian goods to 18% from 50%.

The deal followed months of negotiations during which punitive tariffs had climbed as high as 50% and was widely viewed as a step toward normalizing trade relations.

Publicis draws investor attention.

Back in Europe, focus has returned to the quarterly earnings season, with a large number of major companies across the region scheduled to report results this week.

Publicis Groupe is in focus on Tuesday after a series of strong client wins helped the French advertising group deliver underlying fourth-quarter revenue ahead of expectations. The company generated €2.03 billion in free cash flow before working capital movements in 2025, up 10.6% from the previous year, and proposed a fully cash dividend of €3.75 per share, representing a 4.2% increase.

Elsewhere in France, asset manager Amundi posted a 6% rise in adjusted pretax income for 2025 to €1.86 billion, supported by record net inflows of €88 billion as it rolled out a new strategic plan aimed at driving growth through 2028.

In the Netherlands, Akzo Nobel reported a solid improvement in fourth-quarter margins compared with a year earlier, as the paints manufacturer contends with subdued demand while pursuing a potential merger with U.S. rival Axalta Coating Systems.

Attention is also on U.S. earnings later Tuesday, with results due from companies such as PayPal, Pfizer, and Marathon Petroleum, ahead of Advanced Micro Devices’ earnings after the close. Sentiment toward AI-related stocks remains fragile following poorly received results from Microsoft last week.

French consumer prices decline.

Data released earlier in the session indicated that inflation pressures remain subdued in France, the eurozone’s second-largest economy.

French consumer prices declined 0.3% month on month in January, while annual inflation stood at just 0.3%, undershooting expectations of 0.6%.

Attention now turns to the European Central Bank’s policy meeting later this week, where policymakers are widely expected to leave interest rates unchanged at 2% for a fifth consecutive meeting.

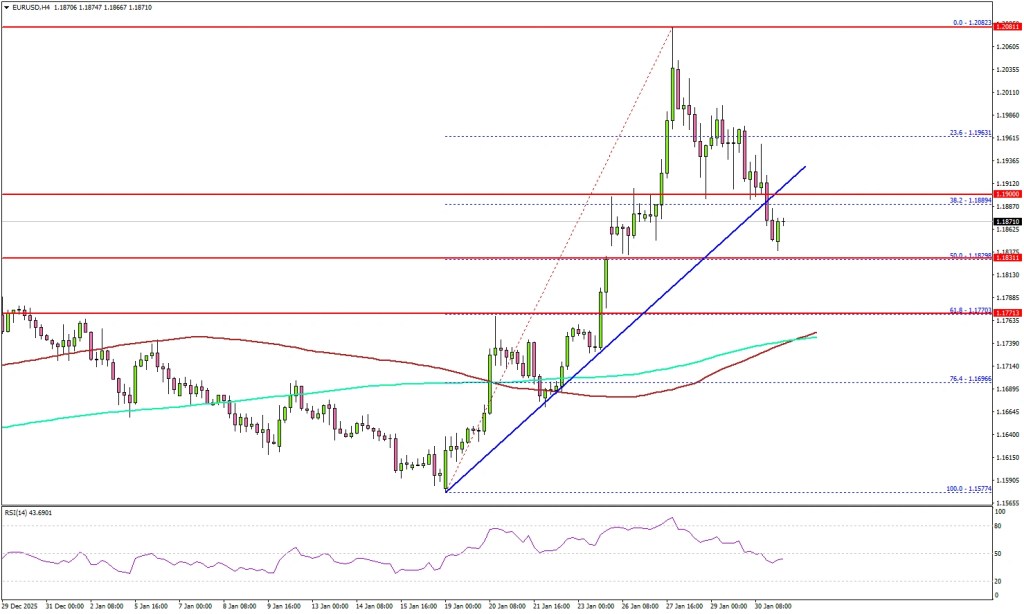

ECB President Christine Lagarde may also be pressed on the implications of a stronger euro for inflation, after the single currency briefly climbed above $1.20 last week, marking its highest level since 2021. It has since retreated but remains more than 2% higher over the past two weeks.

Crude prices continue to edge lower

Oil prices edged lower on Tuesday, extending losses for a second straight session, as easing tensions between the United States and Iran reduced the geopolitical risk premium in crude markets.

Brent futures slipped 0.4% to $65.96 a barrel, while U.S. West Texas Intermediate crude fell 0.4% to $61.90.

Both benchmarks dropped more than 4% in the previous session after President Donald Trump said Iran was “seriously talking” with Washington, signaling a potential de-escalation with the OPEC member.

Further pressure came from reports that Iran and the U.S. are set to resume nuclear talks on Friday in Turkey, according to Reuters.

Oil prices were also weighed down by a firmer U.S. dollar, with the dollar index hovering near a more-than-one-week high, dampening demand from holders of other currencies.

Silver has climbed above $87.00 after rebounding from one-month lows below $72.00. Precious metals are rising on Tuesday as overall market sentiment improves, though XAG/USD bulls may face resistance in the $88.00–$90.00 zone.

Silver (XAG/USD) is posting modest gains on Tuesday, trading around $87.05 at the time of writing. The white metal has stabilized after plunging more than 30% over the previous two sessions, which pushed prices to one-month lows just below the $72.00 level.

In a departure from their typical behavior, precious metals are rebounding alongside an improvement in broader market sentiment. Optimism stemming from a trade agreement between the United States and India, along with reports of forthcoming nuclear talks with Iran, has lifted investor confidence and increased appetite for risk assets.

Technical analysis: XAG/USD faces immediate resistance at $88.00.

XAG/USD has recovered part of its recent losses, though technical indicators continue to signal a bearish bias. The Moving Average Convergence Divergence (MACD) remains below both the signal line and the zero level, even as the negative histogram narrows toward zero. Meanwhile, the Relative Strength Index (RSI) is ticking higher, suggesting a gradual easing of downside pressure, but it remains below the critical 50 threshold.

On the upside, the pair is expected to encounter resistance near Monday’s highs around the $88.00 mark. A sustained break above this level could shift attention toward the psychological $100.00 handle, followed by intraday resistance near $104.00.

On the downside, immediate support is located at the monthly low of $71.37. A break below this level would expose the early-December highs and mid-December lows clustered around the $60.00 area.

UK grocery inflation slowed to 4.0% in the four weeks ending January 25, marking its lowest level since April last year, according to figures released Tuesday by market researcher Worldpanel by Numerator.

The reading eased from the 4.3% inflation rate reported in Worldpanel’s previous update, offering modest relief to households grappling with elevated food prices.

The data also serves as an early signal of price pressures ahead of the UK’s official inflation release scheduled for February 18.

Despite the moderation in inflation, Worldpanel noted that UK grocery sales increased 3.8% year on year in value terms over the four-week period. Adjusted for inflation, however, this translates into a decline in volumes, indicating that consumers are buying less even as overall spending rises.

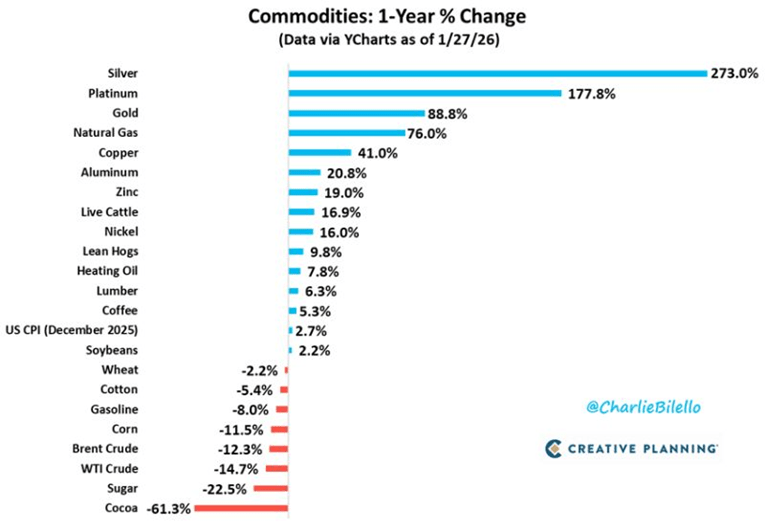

Although gold, silver, and platinum were the top-performing commodities over the past year, they came under pressure late last week.

Metals suffer a sharp pullback after hitting record highs.

Silver and gold suffered a sharp sell-off early Friday, dragging mining stocks and related ETFs lower. After an exceptional run in 2025, both metals have begun to give back part of their gains. Silver slid roughly 15%, falling back below the $100 level, while gold dropped about 7% and struggled to hold above $5,000. Weakness spread across the sector, with platinum and palladium also declining by around 14% and 12%, respectively.

Mining equities and ETFs came under heavy pressure. Producers such as Fresnillo, along with silver miners Endeavour and First Majestic, posted double-digit losses in pre-market trading. Silver-focused ETFs were hit even harder, with some falling as much as 25%.

Following last year’s explosive rally—when silver surged 150% and gold gained 65%—the market appears to be undergoing a correction. Overcrowded positioning, uncertainty surrounding the Federal Reserve’s policy outlook, and shifts in geopolitics and the U.S. dollar have all fueled the sell-off.

The move underscores that even traditional safe-haven assets are vulnerable to sharp volatility. When positioning becomes one-sided, even fundamentally strong markets can reverse quickly. Investors are now reassessing exposure, with some stepping in to buy the dip while others remain on the sidelines.

Top-Performing Commodities Over the Past Year

The three best performers are silver (+273%), platinum (+178%), and gold (+89%). These mark the strongest year-over-year gains for the metals since 1979–1980.

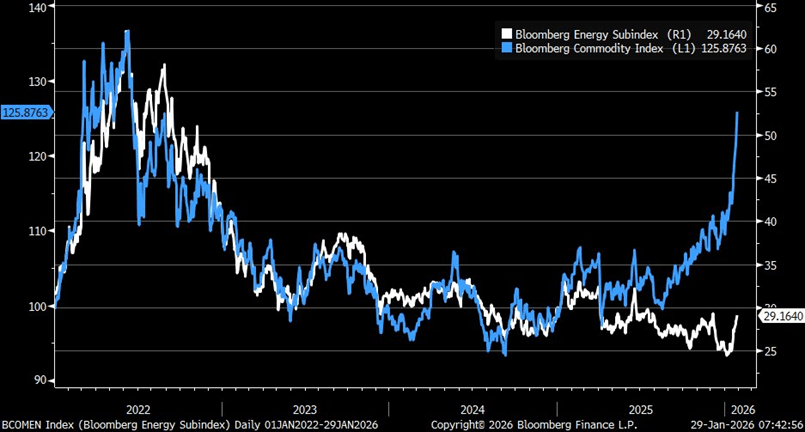

Can oil keep pace with the broader commodities rally?

The Bloomberg Commodity Index has surged, but the gains are not being driven by energy. Instead, strength is coming from other commodities, highlighting an unusual source of the rally.

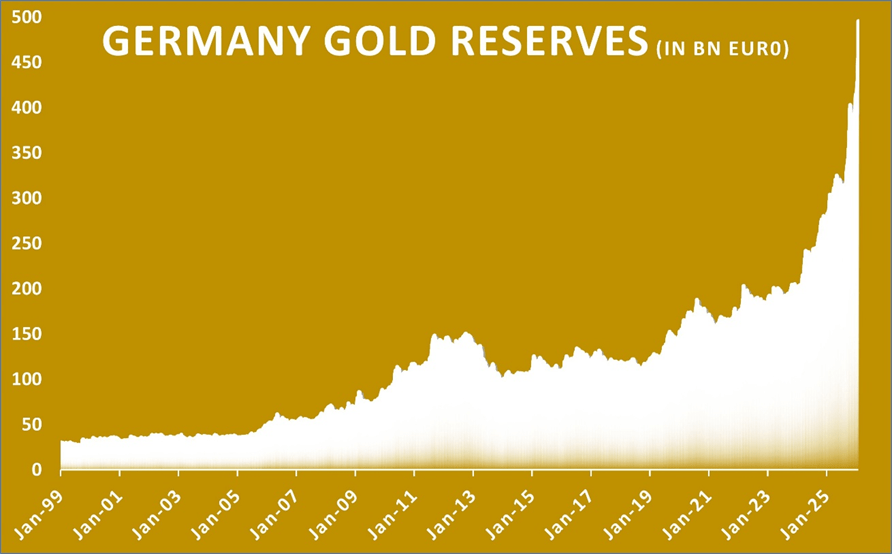

Germany’s gold reserves are valued at nearly €500 billion.

Germany’s gold reserves are now valued at €496 billion. The Bundesbank holds 3,352 tonnes in total, with more than 1,200 tonnes stored in New York and the rest kept in Frankfurt and London.

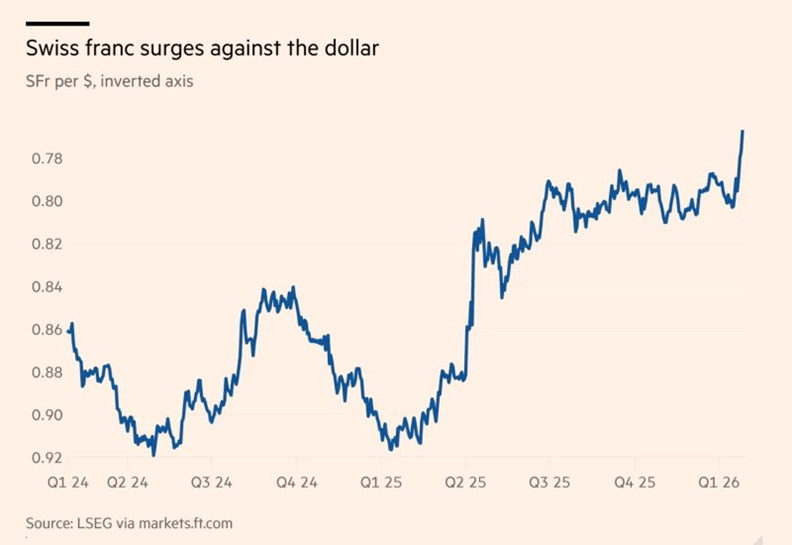

The Swiss franc strengthens against the U.S. dollar.

While market attention remains focused on the U.S. dollar and the yen, the Swiss franc has quietly climbed to its strongest level in more than a decade.

Here’s why the move matters globally:

The “safe-haven” appeal

Investors are gravitating toward stability. With gold pushing above $5,000 an ounce and political uncertainty weighing on major economies, the Swiss franc has reasserted itself as a preferred refuge. The currency is up about 3% so far this year, building on a strong 14% gain last year.

The Swiss National Bank’s policy challenge

Such strength is a double-edged sword. While it helps keep inflation exceptionally low—currently around 0.1%—it also increases pressure on Switzerland’s export-driven economy. This leaves the Swiss National Bank facing a difficult decision:

Cut interest rates? With rates already at 0%, a return to negative territory would be a step policymakers are reluctant to take.

Here is a refined paraphrase that flows naturally from the previous section:

Intervene? Direct action in currency markets risks accusations of manipulation and could spark diplomatic frictions.

The global backdrop

When the world’s primary reserve currency—the U.S. dollar—shows signs of instability, capital doesn’t disappear; it reallocates. Increasingly, those flows are moving toward perceived safe havens, with the Swiss franc emerging as a key beneficiary.

In an era of heightened market volatility, genuine stability has become one of the rarest—and most valuable—assets.

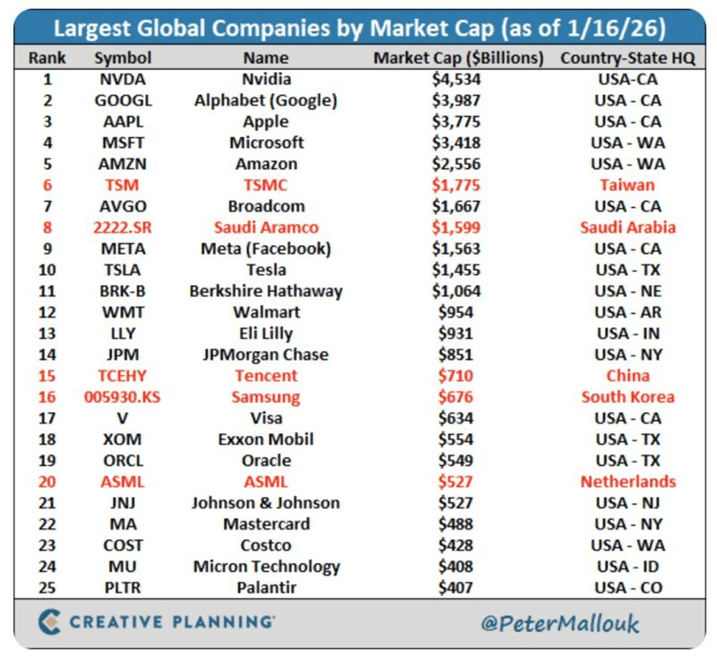

U.S. companies account for 20 of the world’s 25 largest market capitalizations.

The remaining five companies are based outside the U.S., with one each from Europe, China, Taiwan, South Korea, and Saudi Arabia.

Within the United States, California dominates with six of the world’s largest companies by market value. Texas and Washington follow with three each, while New York is home to two. Nebraska, Arkansas, Indiana, New Jersey, Idaho, and Colorado each host one of the top global firms.

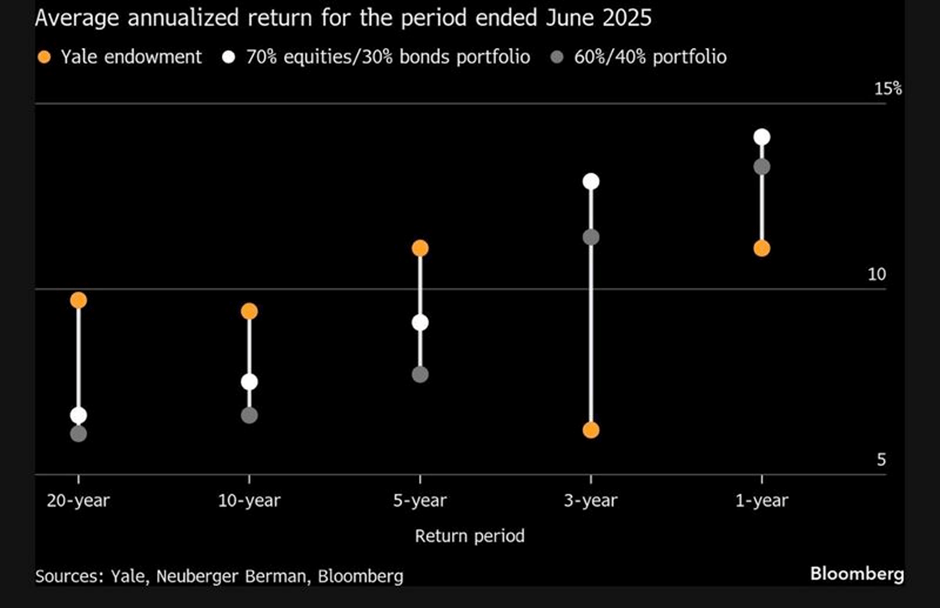

The endowment model faces mounting challenges.

For years, the endowment model—heavily tilted toward private assets—was held up as the gold standard for long-term investment success. Its track record was so compelling that institutions across the globe rushed to replicate it.

But every “secret sauce” loses its edge once it becomes common knowledge. As capital flooded into the same private markets, the once-distinct advantage began to erode.

Today, the space is increasingly crowded, and the classic endowment model is showing signs of strain. At the same time, more traditional portfolios with greater exposure to public markets are quietly regaining relevance.

The drivers are clear: too much money is chasing a limited pool of private opportunities, alpha in private equity is harder to extract, and liquid, public-market portfolios are proving more resilient than many expected.

This raises a critical question: is the era of private-heavy allocations coming to an end, or merely pausing? It may be time to revisit the “Yale model,” with a sharper focus on less congested private strategies and new sources of return—especially if the strong 60/40 performance of the past one and three years turns out to be more cyclical than enduring.

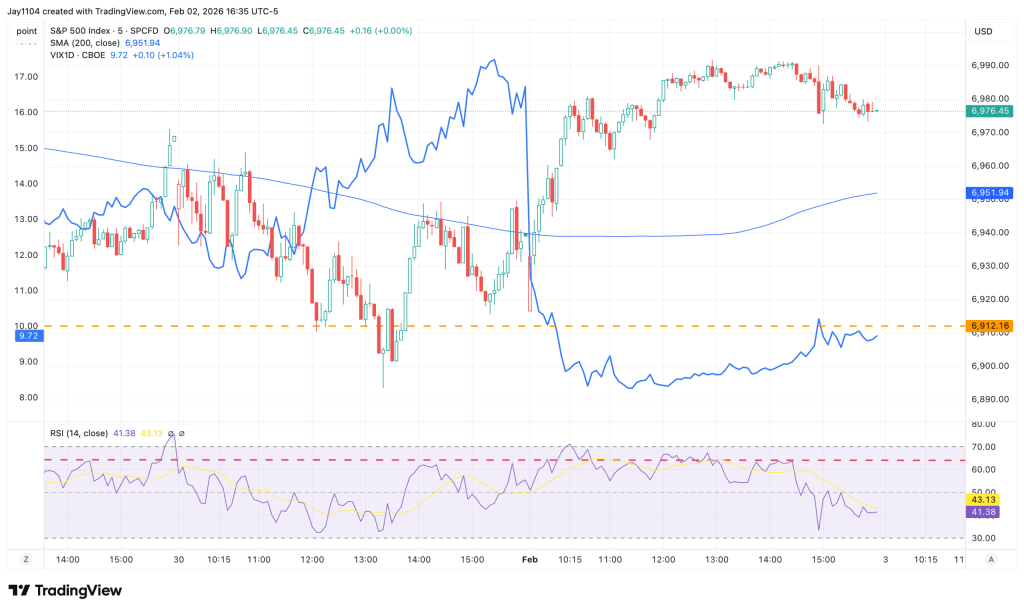

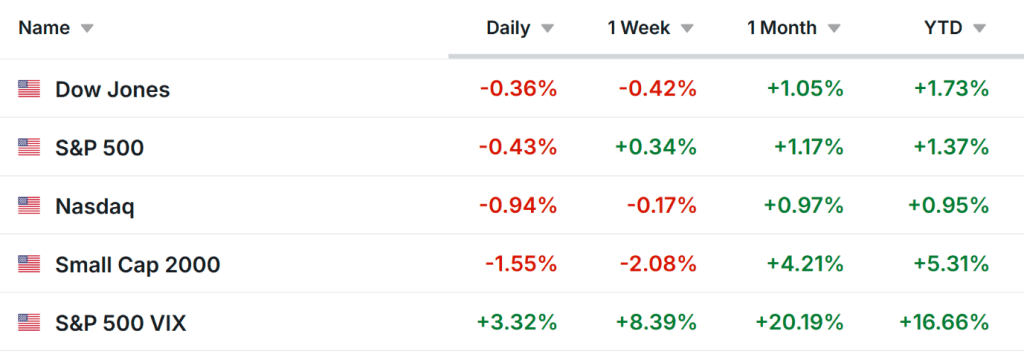

The S&P 500 closed the session up just over 50 basis points, in what felt like a familiar Monday pattern following Friday’s sharp drop in the 1-day VIX from 16.4 to 9.5. While the repetition can feel tiresome, the signal is clear: with volatility effectively reset, the index is once again at risk of stalling.

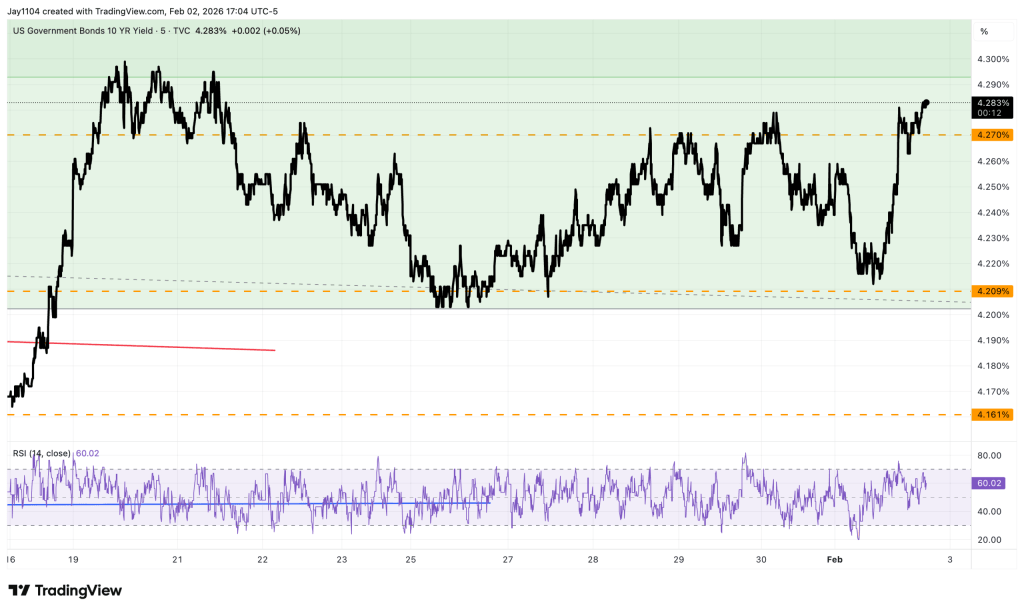

In other developments, the quarterly refunding announcement came in stronger than anticipated based on prior guidance, with the second quarter standing out as the key surprise. The Treasury now expects to issue $109 billion, assuming a Treasury General Account balance of $900 billion. The increase in the TGA target from $850 billion was unsurprising given the scale of U.S. debt and is a point that has been repeatedly highlighted.

Treasury yields were higher for much of the session following the stronger-than-expected ISM manufacturing data and extended those gains after the Treasury’s 3:00 p.m. ET announcement. Further clarity on the composition of the issuance is expected Wednesday morning.

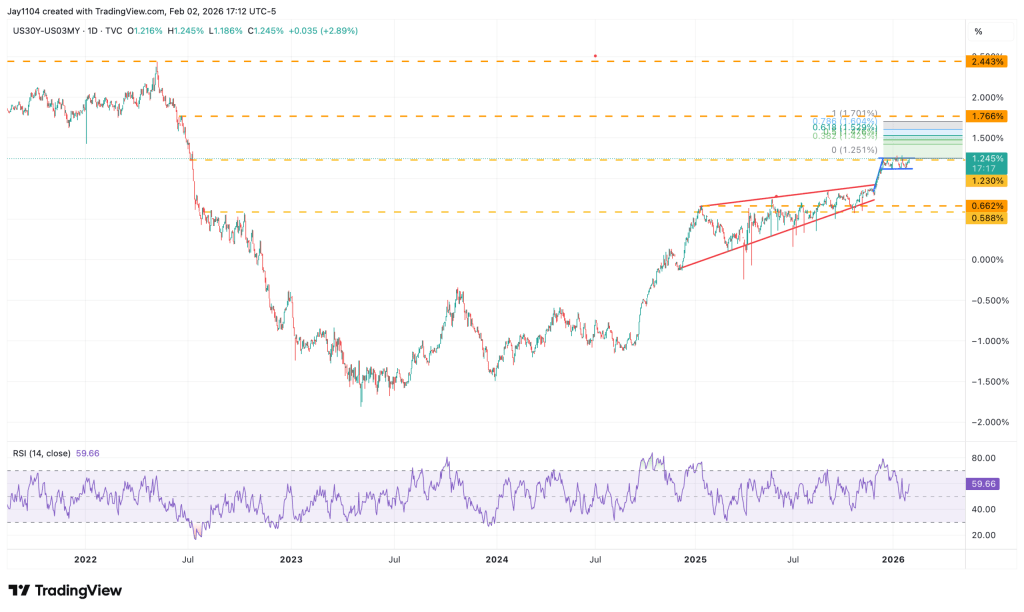

The 30-year minus 3-month spread has returned to the upper boundary of its bull-flag formation. A decisive break above the 1.25% level could trigger further upside momentum, with scope for a move toward the 1.7%–1.75% range.

Absent a meaningful downside shock, the yield curve is likely to continue steepening, driven primarily by higher long-end yields.

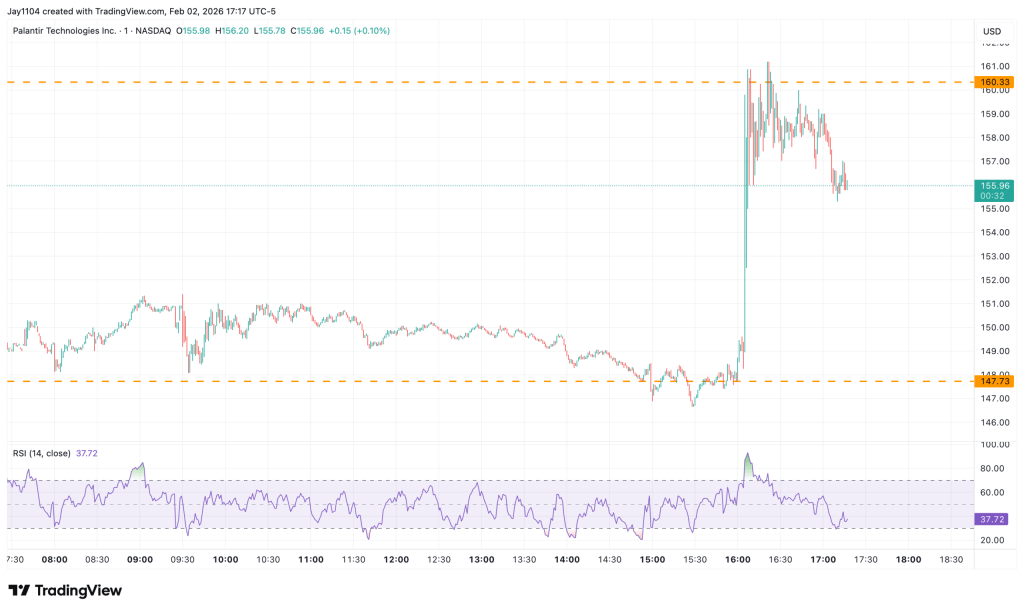

As highlighted yesterday, Palantir’s (NASDAQ: PLTR) key resistance level from an options-positioning perspective sits near $160, which is where the stock stalled in after-hours trading. If shares fail to break decisively above that level, a reversal of recent gains and a sharp pullback during today’s session would not be unexpected.

The U.S. dollar weakened broadly in January, defying its usual seasonal strength — what lies ahead in February?

Key Takeaways From February Forex Seasonality

The U.S. dollar weakened broadly in January, defying its typical seasonal strength. While USD/JPY has historically underperformed in February, the relevance of seasonal averages may be diminished amid anticipated political developments on both sides of the Pacific. Meanwhile, tonight’s RBA meeting could be pivotal in determining whether AUD/USD retreats from three-year highs and aligns with its traditionally weak February seasonality.

The start of a new month provides an opportunity to revisit the seasonal patterns that have shaped the forex market over more than five decades, following the dismantling of the Bretton Woods system in 1971 and the emergence of the modern foreign exchange regime.

As always, these seasonal tendencies reflect historical averages, and individual months or years can deviate from long-term norms. As such, seasonality should be used alongside other forms of analysis when building a robust, long-term trading strategy, as past performance is not necessarily indicative of future results.

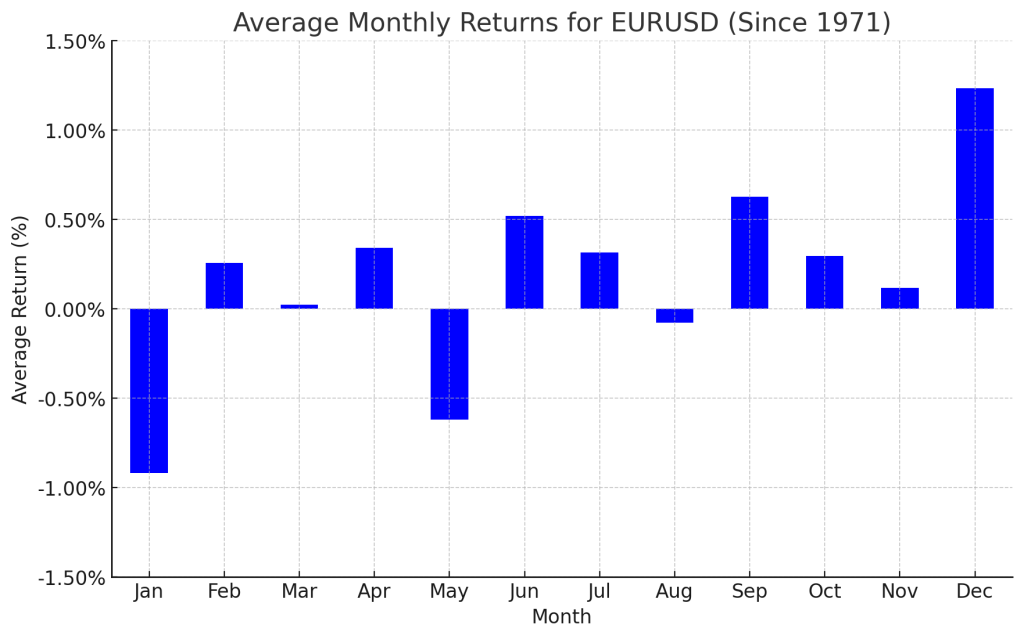

Euro Forex Seasonality – EUR/USD Chart

Historically, February has tended to be mildly bullish for EUR/USD, with the world’s most heavily traded currency pair posting an average gain of around 0.3% over the past 50-plus years. In January, EUR/USD defied its typical seasonal pattern, pushing higher to briefly touch a 4.5-year high near 1.21 before retreating to finish the month lower. For a U.S. dollar that has historically underperformed against the euro, the prospect of another government shutdown—potentially delaying key economic releases such as the NFP report—offers an encouraging backdrop.

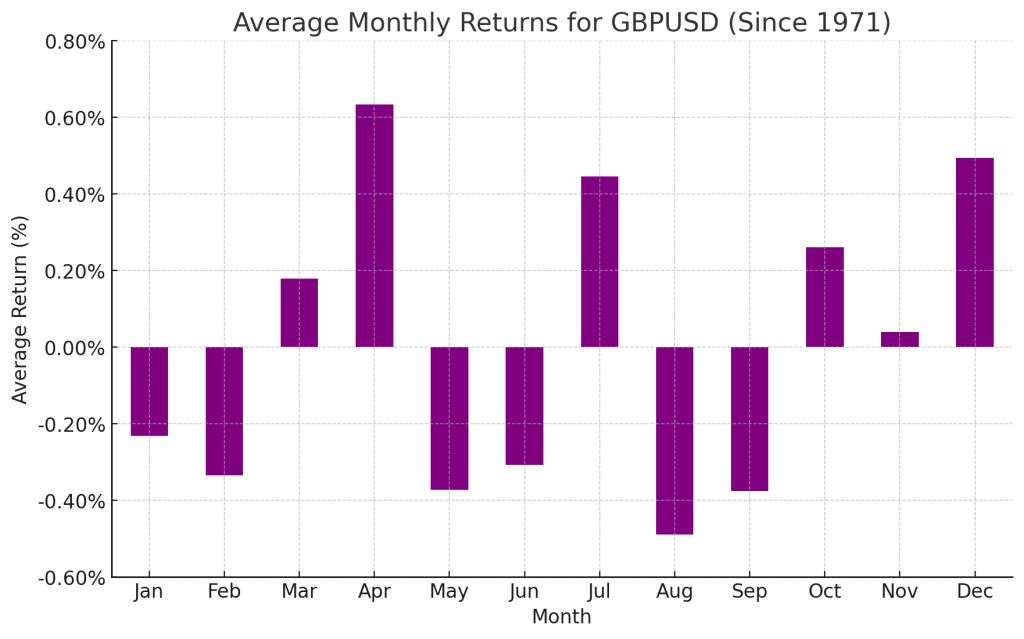

British Pound Forex Seasonality – GBP/USD Chart

As shown in the chart above, GBP/USD has historically tended to decline in February, posting average returns of roughly -0.3% since 1971. Similar to the euro, sterling has advanced for three consecutive months and briefly surged to multi-year highs in January before retreating to finish back within last year’s trading range. While no changes to interest rates are anticipated, this week’s BOE and ECB meetings remain key event risks for European currencies.

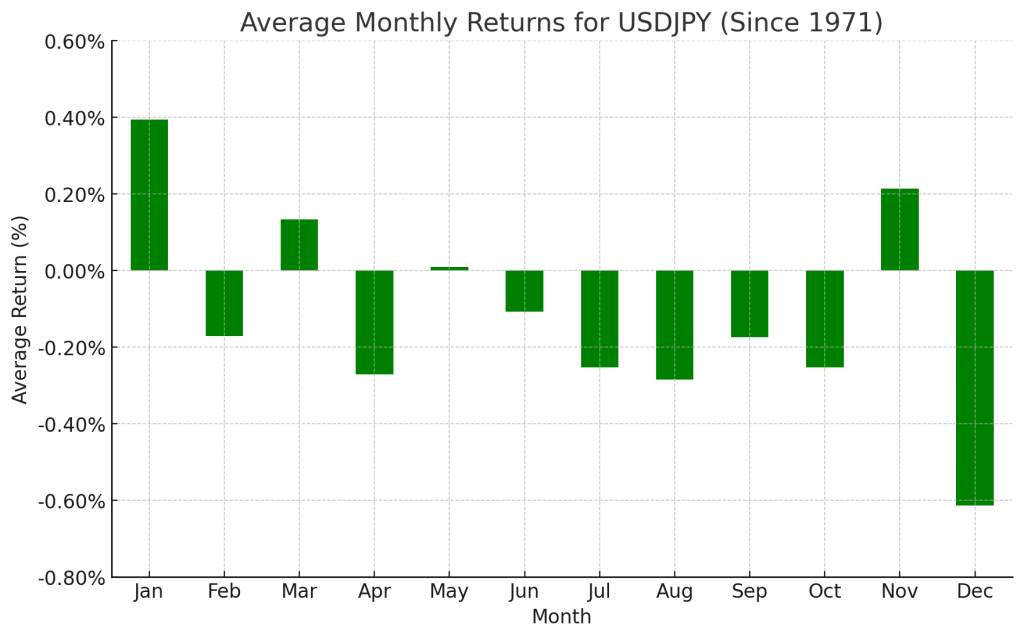

Japanese Yen Forex Seasonality – USD/JPY Chart

February has historically been a mildly bearish month for USD/JPY, with the pair posting average declines of around 0.2% since the Bretton Woods era. The year began with a volatile but ultimately weaker January for USD/JPY, running counter to its usual seasonal pattern amid broad-based U.S. dollar softness. With idiosyncratic political factors exerting an outsized influence on markets on both sides of the Pacific, traders may want to be cautious about placing too much weight on USD/JPY’s seasonal history at present.

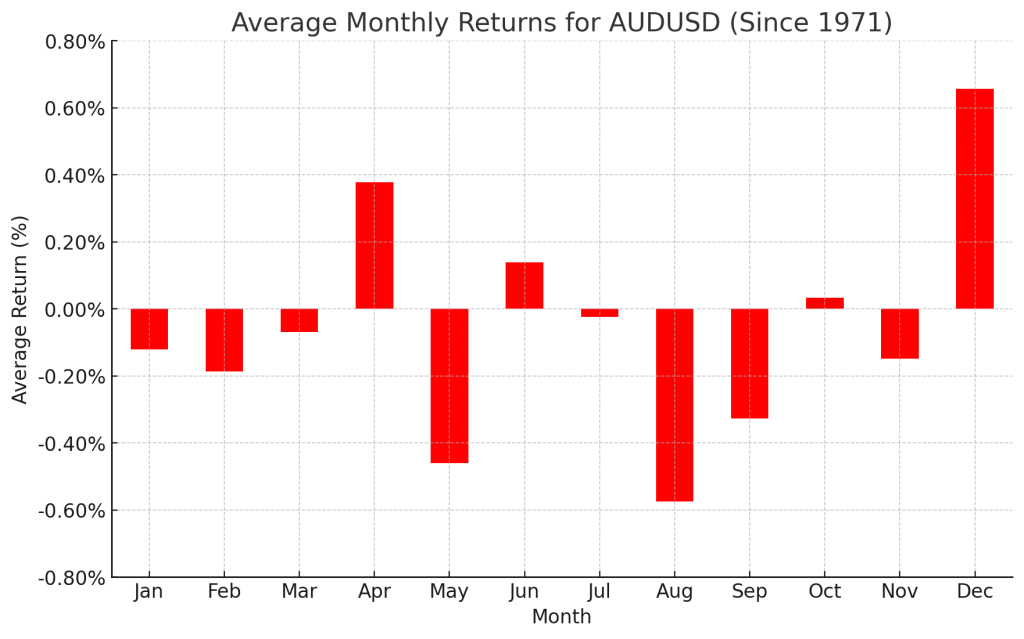

Australian Dollar Forex Seasonality – AUD/USD Chart

Shifting focus to Australia, AUD/USD has historically posted modest declines in February, averaging losses of around 0.2% since 1971. In January, the Australian dollar rallied sharply, breaking out of a three-year range on the back of strong domestic employment and inflation data. While the RBA is widely expected to deliver a rate hike shortly after publication, the central bank’s forward guidance for the remainder of the year may prove more influential for the currency than the rate decision itself.

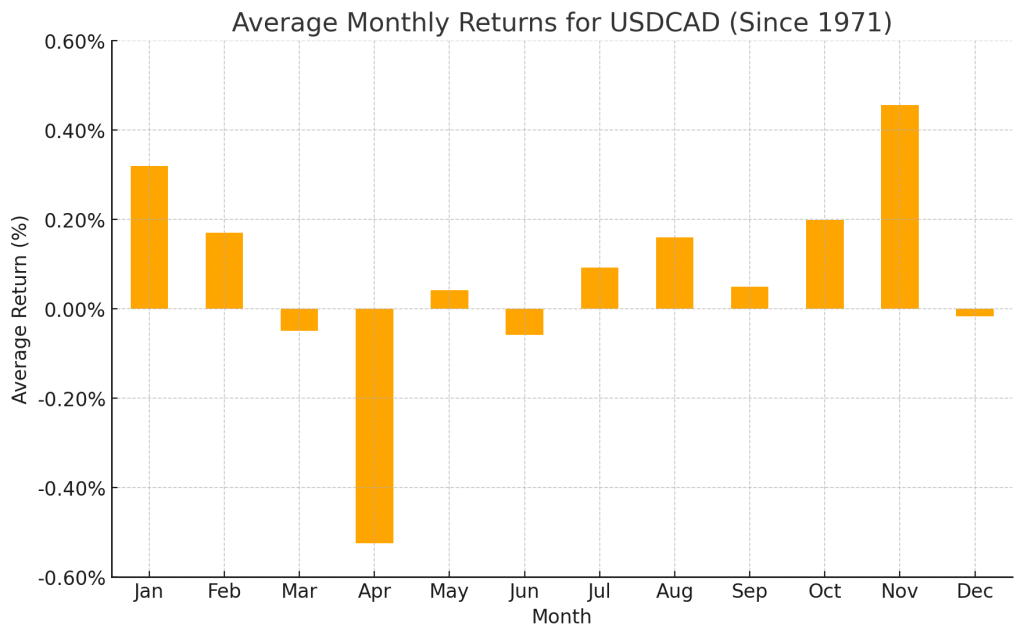

Canadian Dollar Forex Seasonality – USD/CAD Chart

Finally, February has historically been a mildly supportive month for USD/CAD, delivering an average gain of around 0.2%. At the time of writing, the pair is holding above support near its 15-month low in the mid-1.3500s after briefly dipping below that level last month. However, USD/CAD remains below its key medium- and long-term moving averages clustered around the 1.3800 area, marking that zone as a critical hurdle if bulls are to regain control after a difficult three-week stretch.

As always, we close by emphasizing that seasonal patterns are not definitive—even when they appear to be tracking well. This analysis should be paired with a thorough review of current fundamental and technical conditions across the major currency pairs.

Stablecoin issuer Tether said its newly launched MiningOS is a modular, self-hosted software stack designed to support mining operations ranging from small home rigs to large, multi-site industrial facilities.

What to know:

Tether has introduced MiningOS, an open-source, modular operating system for Bitcoin mining designed to streamline infrastructure management and lessen reliance on proprietary vendor software.

The self-hosted platform uses a peer-to-peer architecture, allowing miners to manage operations without centralized services and scale seamlessly from home rigs to multi-site industrial facilities.

Released under the Apache 2.0 license and built on Holepunch peer-to-peer protocols, MiningOS is hardware-agnostic and positions Tether alongside other advocates of open-source mining solutions, including Jack Dorsey’s Block.

Tether has unveiled an open-source operating system for Bitcoin mining, positioning it as a tool to simplify infrastructure management while cutting dependence on closed, vendor-controlled software. On Monday, the stablecoin issuer announced the launch of MiningOS (MOS), a modular and scalable mining platform built to serve everyone from individual hobbyists to large institutional operators.

The software aims to eliminate the “black box” nature of many existing mining setups, where hardware and monitoring systems are tightly locked into proprietary ecosystems. According to Tether, MiningOS prioritizes transparency, openness, and collaboration, and is designed with no vendor lock-in.

MOS operates on a self-hosted architecture and uses an integrated peer-to-peer network to communicate with connected devices, enabling miners to manage operations without centralized services. Operators can tailor settings via a companion interface based on their scale and production needs. Tether CEO Paolo Ardoino described MOS as a “complete operational platform” capable of scaling from a single home rig to industrial-grade mining sites spread across multiple locations.

Tether first outlined plans for an open-source mining operating system in June last year, saying new miners should be able to compete without relying on costly third-party software and management providers. The launch puts Tether alongside other crypto companies advocating open-source mining infrastructure, including Jack Dorsey’s Block.

MiningOS is released under the Apache 2.0 license and is built on Holepunch peer-to-peer protocols, a design choice intended to keep the software stack independent of external third-party dependencies.

Bernstein notes that the ongoing pullback in the crypto market may be short-lived, with Bitcoin potentially starting a recovery in the first half of the year.

The firm’s analysts point to rising institutional inflows and shifting US policy dynamics as factors that could underpin what they describe as Bitcoin’s “most consequential cycle.”

Other market participants anticipate capital rotation away from “overcrowded” precious metals and into Bitcoin.

Bitcoin may find a price floor near its previous cycle peak in the $60,000 area before staging a potential recovery in the first half of the year, according to analysts at Bernstein.

Led by Gautam Chhugani, the analysts noted that the recent pullback in crypto prices follows a period of strong outperformance by gold relative to Bitcoin over the past year. They added that Bitcoin’s market capitalization compared to that of gold is nearing a two-year low, as central banks have significantly increased their gold purchases over the past year.

Bernstein added that the recent market softness may represent a short-lived correction rather than the start of a prolonged bearish cycle, driven by several underlying factors.

New catalysts help Bitcoin remain resilient despite price weakness

The firm argued that robust institutional inflows into Bitcoin ETFs — which now hold roughly $165 billion in assets — alongside growing allocations from corporate treasuries, have helped the market move beyond the traditional boom-and-bust cycle.

Bernstein also pointed to the lack of miner-led capitulation, a feature commonly seen in past market downturns. Instead, miners have increasingly diversified their revenue by expanding into AI-focused data center operations, reducing their reliance on Bitcoin price fluctuations.

US policy developments were cited as another potential upside catalyst. Bernstein highlighted the creation of a Strategic Bitcoin Reserve funded by seized government BTC holdings, while potential changes in Federal Reserve leadership under nominee Kevin Warsh could further enhance Bitcoin’s standing. The analysts suggested that broader political alignment with the crypto sector could pave the way for Bitcoin to be viewed as a sovereign or reserve-like asset.

“We do not expect a passive response from the U.S. government if digital asset markets continue to decline,” the analysts wrote.

The latest assessment follows Bernstein’s projection last month that Bitcoin had bottomed near $80,000. At the time of publication, the world’s largest cryptocurrency was trading around $78,000, up 1.8% over the past few hours.

Hyperliquid rises 8% above its 200-day EMA on Tuesday, extending Monday’s nearly 9% advance.

The project unveiled plans to support outcome trading through the HIP-4 proposal.

Retail participation picks up as HYPE futures Open Interest posts double-digit gains to around $1.85 billion.

Hyperliquid (HYPE) continued its recovery on Tuesday, rising 8% at the time of writing, fueled by optimism surrounding the HIP-4 proposal aimed at introducing outcome trading, including prediction markets and bounded options contracts. Growing retail engagement with the decentralized exchange and its native token is reflected in a more than 25% jump in HYPE futures Open Interest, signaling strong capital inflows. From a technical perspective, HYPE maintains a bullish bias, with strengthening buying pressure and improving trend momentum.

Hyperliquid rekindles retail interest with prediction market plans

Hyperliquid unveiled the HIP-4 proposal on Monday during early US trading, outlining plans to introduce prediction markets and fixed-range options contracts in an effort to compete with established platforms such as Polymarket and Kalshi. Retail participation in prediction markets has surged amid heightened volatility across global financial markets and geopolitical developments.

The latest initiative marks an expansion of the Hyperliquid exchange beyond commodity trading, which was introduced under the HIP-3 proposal, and underscores the platform’s ongoing development aimed at better meeting trader demand.

CoinGlass data shows that HYPE futures Open Interest (OI) jumped 27% over the last 24 hours to $1.84 billion, indicating significant inflows. Typically, such a large capital inflow in futures markets during an uptrend indicates an upside bias among traders.

A massive wipeout of short sellers over the last 24 hours, evidenced by short liquidations of $31.69 million outpacing long liquidations of $1.58 million, corroborates the upside bias in HYPE futures. Additionally, the funding rate of 0.0046% signals a bullish interest among traders.

Technical outlook on Hyperliquid: Can HYPE reach the $50 level?

Hyperliquid rebounded from the 100-day Exponential Moving Average (EMA) at $30.61, posting gains of around 24% so far this week. At the time of writing on Tuesday, HYPE is up 14% on the day and has reclaimed the 200-day EMA at $32.89. The next upside hurdles are seen at $35.51 — aligned with the August 2 low — and the R1 Pivot Point at $37.07.

The broader technical structure reinforces a strong recovery bias, with longer-term EMAs trending higher above shorter-term averages on the daily chart. A sustained close above $37.07 could pave the way toward the R2 Pivot Point at $43.15, followed by a key resistance zone near the $50.00 psychological mark.

Momentum indicators also favor further upside. The Moving Average Convergence Divergence (MACD) continues to strengthen, with histogram bars expanding above the zero line, signaling accelerating bullish momentum. Meanwhile, the Relative Strength Index (RSI) stands at 71, entering overbought territory and reflecting strong buying pressure.