Key Highlights:

- S&P 500 futures edge lower as investors prepare for a packed week of corporate earnings and major central bank meetings.

- The U.S. payrolls report looms as a critical test for market direction following the Fed’s pause in rate cuts.

- Japan’s Nikkei records a rare gain, supported by polls pointing to a likely LDP majority victory.

- Gold and silver extend sharp losses after Friday’s volatility, adding to broader market unease.

- The dollar stabilizes while the yen stays weak; Asian equities mostly track Wall Street futures lower.

- Roughly 25% of S&P 500 companies report earnings this week, including Alphabet, Amazon, and Eli Lilly.

- The dollar jumped after reports that President Trump nominated Kevin Warsh as Fed chair, while CFTC data show asset managers increased bearish dollar positions by $8.3 billion in the week to Jan. 27.

- Copper falls further, extending last week’s steep declines as metals traders brace for continued volatility; U.S. natural gas futures slump, reversing Friday’s spike on milder weather forecasts.

- Bitcoin slips below $76,000 in thin weekend trading, down about 40% from its 2025 peak, with demand fading amid thinning liquidity and subdued investor sentiment.

Dow Jones, S&P 500, and Nasdaq futures fell on Sunday night. The U.S. federal government entered another shutdown on Saturday, although it is widely expected to be resolved quickly.

A busy week of earnings lies ahead, led by Alphabet (NASDAQ: GOOGL), Amazon (NASDAQ: AMZN), Eli Lilly (NYSE: LLY), Palantir (NASDAQ: PLTR), Advanced Micro Devices (NASDAQ: AMD), and Disney (NYSE: DIS), with Disney set to report early on Monday.

Key U.S. Economic Data and Earnings Ahead

Wall Street will also be closely focused on the U.S. monthly jobs report due on February 6, after the Federal Reserve signaled some stabilization in the labor market by pausing its rate-cutting cycle last week.

Following the decision to hold interest rates steady, Fed officials will be watching hiring trends closely, balancing persistent inflation risks against signs of cooling job growth. Some policymakers continue to argue that additional rate cuts may be needed to support employment. Investors will also keep an eye on February consumer sentiment, consumer credit figures, and PMI data for both manufacturing and services.

Economic calendar:

- Mon, Feb 2: ISM manufacturing PMI (Jan); Atlanta Fed President Raphael Bostic speaks.

- Tue, Feb 3: Job openings (Dec).

- Wed, Feb 4: ADP employment (Jan); remarks from Fed Governor Lisa Cook; ISM services PMI (Jan) in focus.

- Thu, Feb 5: Initial jobless claims (week ending Jan 31).

- Fri, Feb 6: U.S. employment report (Jan); preliminary consumer sentiment (Feb) and consumer credit data also due.

Earnings calendar:

- Mon, Feb 2: Palantir (PLTR), Disney (DIS), Mizuho Financial (MFG)

- Tue, Feb 3: AMD (AMD), Merck (MRK), Amgen (AMGN), Pfizer (PFE), PepsiCo (PEP)

- Wed, Feb 4: Alphabet (GOOG, GOOGL), Eli Lilly (LLY), AbbVie (ABBV), Novartis (NVS), Novo Nordisk (NVO), Uber (UBER), Qualcomm (QCOM)

- Thu, Feb 5: Amazon (AMZN), Philip Morris (PM), Shell (SHEL), ConocoPhillips (COP), Bristol-Myers Squibb (BMY)

- Fri, Feb 6: Toyota Motor (TM)

Amazon (AMZN) shares jumped after the company reported strong third-quarter results, posting adjusted EPS of $1.95, up 36% year over year, on revenue of $180.2 billion, a 13% increase. AWS revenue rose 20% to $33 billion, while advertising sales climbed 24% to $17.7 billion. According to The Wall Street Journal, Amazon is in discussions to invest as much as $50 billion in OpenAI, having already committed $8 billion to Anthropic, for which AWS serves as the primary cloud and AI-training partner using its Trainium and Inferentia chips. Looking ahead, FactSet forecasts Amazon’s fourth-quarter EPS at $1.96, up 6%, with revenue expected to rise 13% to $211.4 billion.

FactSet estimates that Advanced Micro Devices (AMD) will report fourth-quarter EPS of $1.32 on revenue of $9.65 billion, while analysts forecast EPS of $1.23 and revenue of $9.38 billion for the following quarter. Some analysts expect AMD to exceed fourth-quarter expectations when it reports on February 3.

Analysts also anticipate that Alphabet (GOOGL) will report quarterly EPS of $2.58, representing 20% year-over-year growth, on revenue of $94.7 billion, up 16%. Consensus EPS estimates for the quarter have been trimmed by 0.4% over the past 30 days.

Technical Analysis:

DJIA Index

The Dow Jones Industrial Average is currently trading in a rectangular consolidation pattern, with prices compressing between 49,700 and 48,450. A decisive breakout above or breakdown below this range is likely to set the direction of the next major trend.

DJIA Daily Candlestick Chart

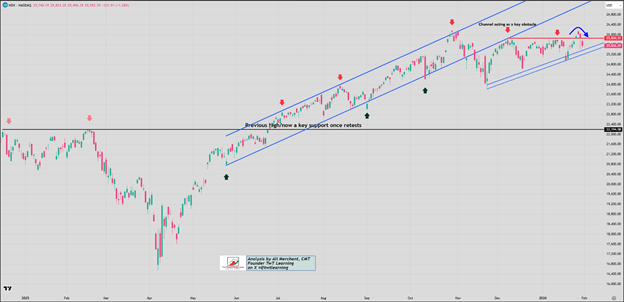

Nasdaq 100 Index

The Nasdaq 100 (NDX) failed to sustain gains above 25,860 last week and remains range-bound between 25,860 and 25,200, with stronger support near 24,650. A clear break below 25,200 would increase the risk of a decline toward 24,650. Conversely, if 25,200 continues to hold on repeated tests, the index is likely to remain choppy within the 25,860–25,200 range.

NDX Daily Candlestick Chart

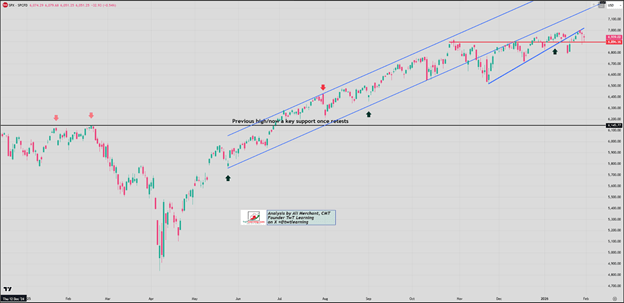

SPX Index

The S&P 500 (SPX) has been hovering around the 6,900–6,890 zone for several weeks, with 7,000 acting as a key psychological resistance for bulls. For now, price action is expected to remain range-bound between 7,000 and 6,880. A decisive break below 6,880 would likely open the door to a deeper pullback toward 6,830.

SPX Daily Candlestick Chart

Weekly US Indices Probability Map:

Sources: Ali Merchant

Leave a comment