The U.S. jobs report, ISM PMI data, and another round of AI-driven tech earnings will be in the spotlight this week. Alphabet is poised to deliver robust results and upbeat guidance, making it an attractive buy. Meanwhile, Strategy heads into a difficult week as Bitcoin volatility and concerns over its BTC holdings weigh on the stock.

Wall Street stocks closed lower on Friday after President Donald Trump nominated former Federal Reserve Governor Kevin Warsh as the next Fed chair. Sharp sell-offs in gold and silver prices further unsettled markets.

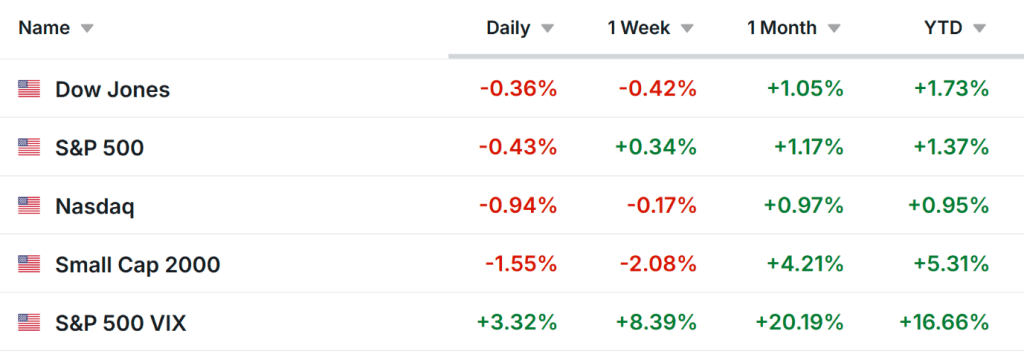

Despite Friday’s pullback, the major U.S. stock indexes ended the month higher. The Dow Jones Industrial Average and the S&P 500 posted January gains of 1.1% and 1.2%, respectively, while the Nasdaq Composite rose 1%. Small caps outperformed, with the Russell 2000 climbing more than 4% for the month.

Volatility may pick up in the days ahead as investors weigh the outlook for economic growth, inflation, interest rates, and corporate earnings.

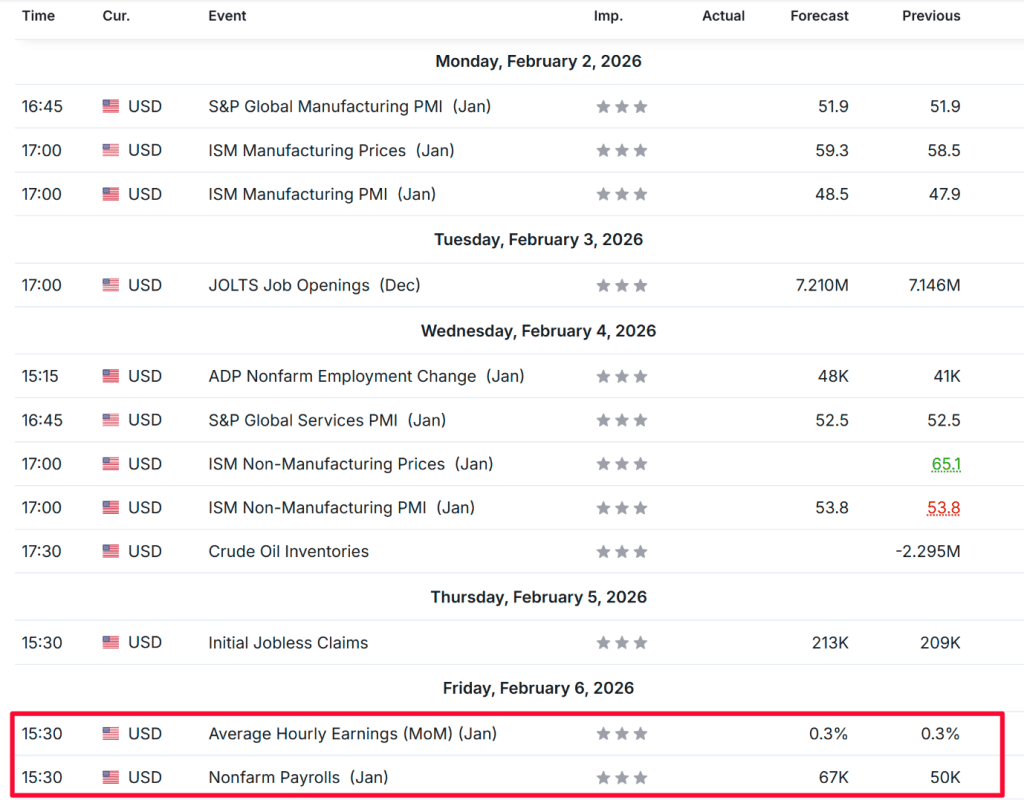

The key economic release will be Friday’s January U.S. jobs report, which is expected to show payroll growth of 67,000, with the unemployment rate unchanged at 4.4%. Ahead of that, the ISM manufacturing and services PMI readings will also be in focus.

A busy earnings calendar is also on tap, featuring reports from several major companies. These include “Magnificent Seven” members Alphabet and Amazon (NASDAQ: AMZN), along with AI-focused leaders Palantir Technologies (NASDAQ: PLTR) and Advanced Micro Devices (NASDAQ: AMD). Other high-profile reporters include Eli Lilly, Novo Nordisk, Pfizer, PepsiCo, Walt Disney, PayPal, Uber, Reddit, Roblox, Snap, Qualcomm, and Super Micro Computer.

Meanwhile, the federal government entered another shutdown on Saturday, though it is expected to be resolved by Monday.

No matter how markets move, I outline below one stock that could attract buying interest and another that may face renewed downside pressure. Keep in mind that this outlook applies only to the week ahead, from Monday, February 2, through Friday, February 6.

Buy Call: Alphabet

Alphabet goes into its quarterly earnings release with expectations for an upside surprise on both profit and revenue, driven by two key growth engines: a rebound in advertising and rising AI-driven contributions across Search, YouTube, and Google Cloud.

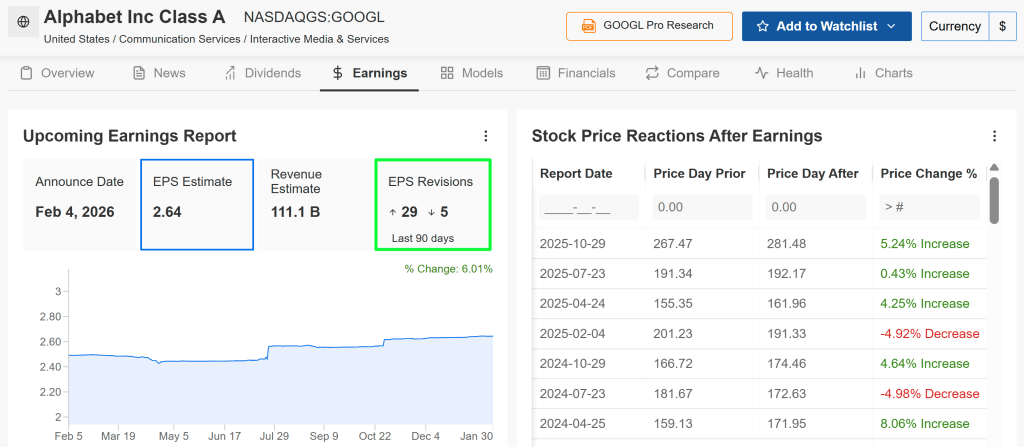

The company is set to report fourth-quarter results after the market closes on Wednesday at 4:00 p.m. ET. Options markets are pricing in a potential move of about ±6.4%, with positioning tilted to the upside as roughly 80% of whisper estimates point to a beat.

Earnings forecasts have been raised 29 times in recent weeks, compared with just five downward revisions, underscoring increasing confidence in Alphabet’s earnings outlook.

Wall Street expects Alphabet to deliver earnings of $2.64 per share, up 21.8% from a year earlier, while revenue is projected to rise 15.7% year over year to $111.1 billion. Cloud remains a standout performer, with Google Cloud Platform revenue forecast to grow more than 37% annually, driven by robust demand for AI infrastructure and enterprise offerings.

A meaningful earnings beat, paired with upbeat forward guidance, could propel the stock to fresh record highs as the search giant continues to unlock monetization from its expanding suite of AI initiatives and builds on accelerating cloud momentum.

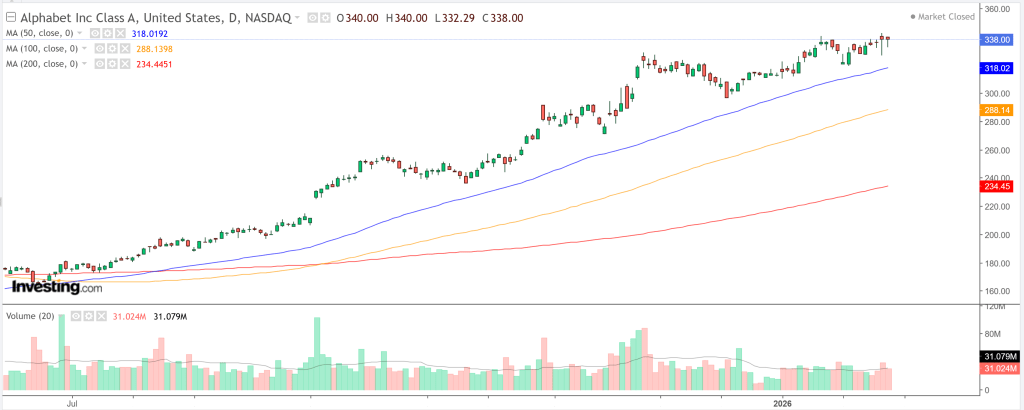

GOOGL shares are trading near their 52-week high of $342.29 and remain above the 50-day moving average at $317.97. The stock is up about 8% year to date and has gained 66.3% over the past 12 months. From a technical perspective, the shares have held up well, consolidating above key support near $325 and setting up for a potential breakout above $350 if earnings exceed expectations.

Trade Setup:

- Entry: $338–$340 (ahead of earnings)

- Target: $350–$355 (approximately 5% upside)

- Stop-Loss: $330 (around 2.4% downside risk)

Sell Call: Strategy

Strategy heads into its earnings release under markedly different conditions. The Michael Saylor–led company, which has transformed itself into the world’s largest corporate holder of Bitcoin, is facing mounting pressure as cryptocurrency markets turn volatile.

The firm holds roughly 712,647 Bitcoin, accumulated at an average cost of about $76,037 per coin, representing more than $54 billion at recent market prices. Over the weekend, however, Bitcoin fell below Strategy’s average purchase price for the first time since October 2023, pushing the company’s holdings into an unrealized loss position and heightening investor concerns.

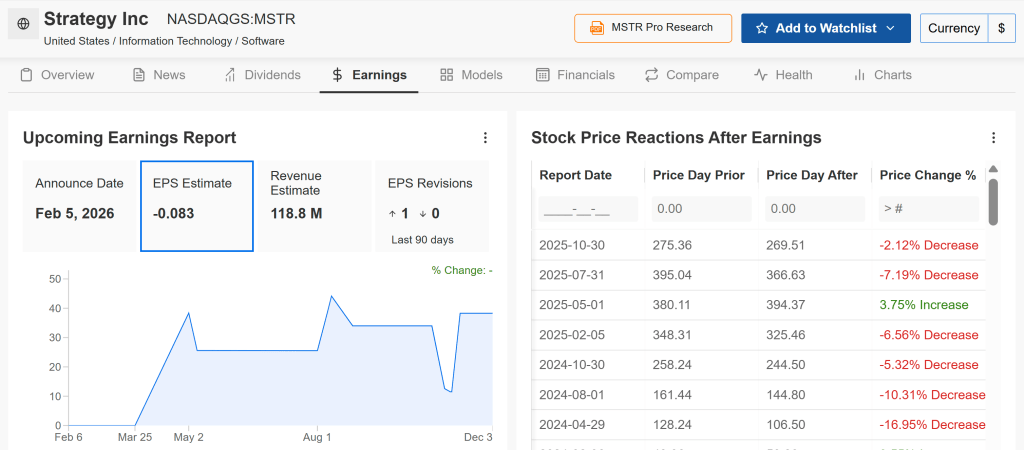

Strategy is scheduled to report its fourth-quarter earnings after the market closes on Thursday at 4:20 p.m. ET.

Wall Street is forecasting a loss of $0.08 per share on revenue of $118.8 million, though investors’ attention will center less on the core figures and more on the company’s Bitcoin treasury and any related impairment charges.

In the third quarter of 2025, the company booked a massive $17.44 billion in unrealized losses tied to cryptocurrency price declines, and the prospect of similar write-downs could pressure fourth-quarter results as well.

Even with the stock trading at an estimated 0.7x the value of its Bitcoin holdings, Strategy’s elevated beta of 3.4 magnifies downside exposure in a risk-off market environment.

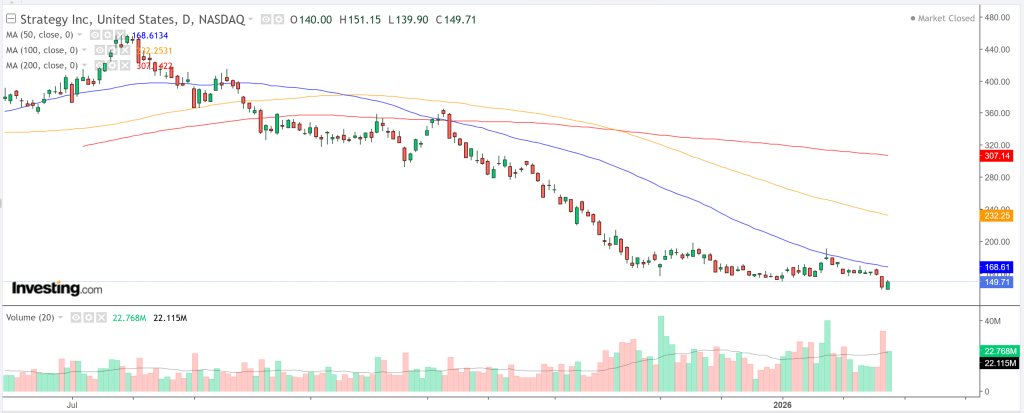

MSTR shares have plunged 55.3% over the past year and are currently trading around $149.71, just above their 52-week low of $139.36. From a technical standpoint, the stock has fallen below both its 50-day and 200-day moving averages, while momentum indicators point to oversold conditions without signaling a decisive reversal.

Elevated short interest and negative sentiment leave the shares vulnerable to additional downside, particularly if the earnings report points to slower Bitcoin accumulation or greater dilution from further capital-raising efforts.

Trade Setup:

- Entry: $149.71

- Target: $130 (approximately 12.7% downside potential)

- Stop-Loss: $155 (around 4% upside risk)

Sources: Jesse Cohen

Leave a comment