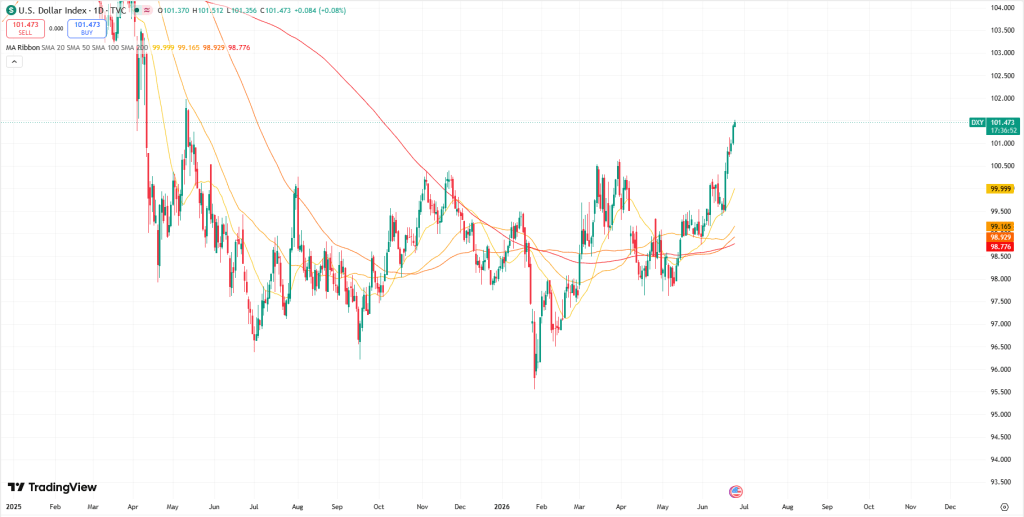

The US Dollar Index (DXY) advanced to a fresh 13-month high of 101.45 on Wednesday, supported by strong domestic economic data and a complex geopolitical backdrop that continued to underpin demand for the Greenback. Further boosting sentiment, the US S&P Global Composite PMI rose to 52.2, surpassing May’s 51.5 reading and indicating that business activity in the United States remained on a solid expansionary path.

The US Dollar Index (DXY), which tracks the US Dollar’s performance against a basket of six major currencies, remained firmly supported for a third straight session, trading near a fresh 13-month high of 101.45 during Wednesday’s Asian trading hours.

The Greenback continued to draw strength from a combination of solid US economic fundamentals and an evolving geopolitical environment. Market participants weighed conflicting developments surrounding a potential diplomatic opening between the United States and Iran. While Donald Trump claimed that Tehran had fully agreed to allow nuclear inspections, Iranian Foreign Minister Abbas Araghchi cautioned that meaningful nuclear negotiations have yet to commence.

Geopolitical tensions remained elevated after Iran’s lead negotiator emphasized that the strategic Strait of Hormuz would not return to its pre-conflict status and would remain under Iranian control. At the same time, diplomatic efforts elsewhere appeared constructive, with Washington hosting a new round of discussions between Israel and Lebanon aimed at securing a ceasefire involving the Iran-backed Hezbollah.

On the economic front, upbeat US data reinforced the narrative of American economic resilience. The preliminary June S&P Global Composite PMI rose to 52.2, exceeding May’s 51.5 reading and signaling continued expansion in overall business activity.

The manufacturing sector remained particularly strong, with the output index climbing to 55.7 from 55.1, outperforming expectations of 54.8. Meanwhile, the Services PMI improved to 51.3 from 50.7, slightly above the market forecast of 51.0, highlighting persistent strength in service-sector demand. Investors now turn their attention to the May Personal Consumption Expenditures (PCE) Price Index, due on Thursday, for further clues on inflation trends.

According to the CME FedWatch Tool, expectations for a more hawkish stance from the Federal Reserve have strengthened considerably. Markets are currently pricing in an 86.1% probability of a rate hike in December, up sharply from 61% prior to last week’s FOMC meeting.

Leave a comment