The sharp rise in oil prices following escalating tensions between the United States and Iran has reignited talk of stagflation. That concern is largely misplaced. What markets may actually be reacting to is not a repeat of the 1970s, but the early stages of a broader shift in capital allocation — away from financial assets and toward tangible ones.

The Stagflation Comparison Falls Apart

Whenever oil prices surge, fears of stagflation quickly emerge. The pattern appeared in 2022 and is resurfacing again. The instinct makes sense: higher energy costs can push inflation upward while weighing on economic growth. However, drawing a direct parallel with the stagflation period of the 1970s and early 1980s oversimplifies the situation.

Classic stagflation requires a persistent combination of three conditions: entrenched inflation far above target levels, stagnating or shrinking economic activity, and limited policy tools capable of correcting the imbalance without worsening the problem. In the United States during 1973 and again in 1979, all of these factors were present. Today’s environment looks very different.

Inflation is the first major distinction. During the 1970s, U.S. consumer prices averaged above 7% for much of the decade and surged beyond 13% at the end of the period. Inflation was embedded in wages, expectations, and policy frameworks. By contrast, today’s inflation has already declined significantly from its 2022 highs. While still above the ultra-low levels seen after 2008, it remains far more controlled. Importantly, central banks now possess the credibility that was missing during the Federal Reserve leadership of Arthur Burns. Inflation expectations remain relatively stable — a crucial difference.

Economic growth tells a similar story. Real GDP continues to expand at a respectable pace, and while the labor market is gradually cooling, it is far from collapsing. Corporate profits have generally remained resilient, apart from sectors particularly sensitive to higher interest rates. Consumer spending — supported by continued employment — has not stalled. In this context, an oil price spike represents a headwind rather than an automatic trigger for recession.

Supply conditions also differ dramatically from those of the 1970s. The earlier oil crises were driven by coordinated OPEC embargoes that deliberately restricted supply to Western economies. At the time, alternatives were limited and domestic production could not compensate. Today, the United States is the world’s largest oil producer thanks to the shale revolution. A disruption involving Iran can lift prices, but it does not recreate the systemic vulnerability that defined the 1973 crisis.

The reality is straightforward: energy prices may push inflation slightly higher and shave some growth at the margins. But an isolated oil shock does not produce stagflation unless the broader economic structure is already broken — and that is not the case today.

What the Oil Spike Actually Signals

Rather than focusing on stagflation, investors should consider what oil’s move may be revealing about broader market dynamics.

Historical patterns following geopolitical shocks offer a useful guide. In the first three months after such events, oil tends to be the strongest performer among major assets, rising roughly 18% on average. Gold typically advances about 6%, while equities post modest gains of around 4%, often reflecting relief that the situation did not escalate further.

Six months later, however, the picture often changes. Gold generally continues to climb, with average gains near 19%. Equity markets lose momentum, and oil frequently gives back much of its initial spike as supply responses and fading fear premiums bring prices back down.

The tactical takeaway is clear: oil tends to perform best during the initial shock phase, while gold benefits from the longer period of uncertainty that follows. The geopolitical risk premium embedded in oil prices is often temporary, but in gold it can evolve into a more lasting repricing tied to concerns about currencies, fiscal sustainability, and the reliability of financial assets.

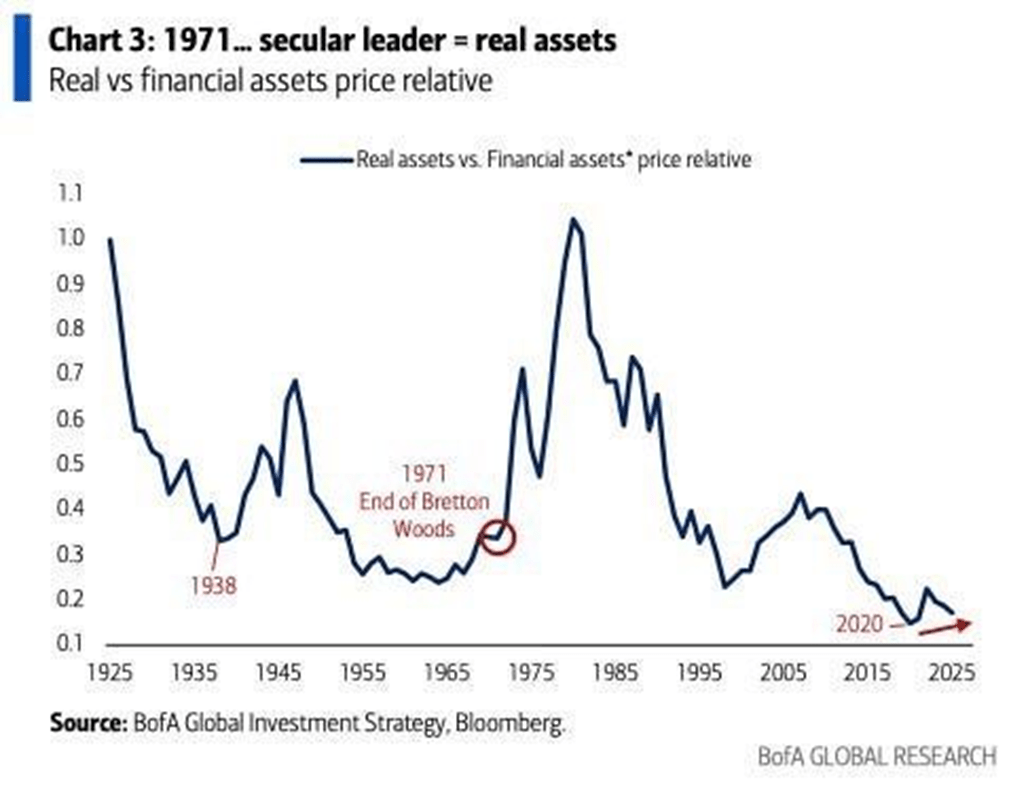

The Bigger Shift: Real Assets Regaining Importance

Looking at the broader market landscape, the oil rally may represent just one element of a larger transition.

During 2024 and 2025, equity markets were dominated by a single theme: artificial intelligence. Capital poured into a small group of large technology companies investing heavily in AI infrastructure. The narrative was simple — if AI would reshape the economy, investors should own the companies leading that transformation.

By 2026, leadership appears to be shifting. The strongest performers are increasingly the firms supplying the physical foundations of the AI economy: semiconductor manufacturers, materials producers, energy providers, and industrial supply chains. Meanwhile, some of the technology platforms themselves face rising costs and pressure on their traditional software revenue models.

This development suggests something deeper than a normal sector rotation.

For decades, capital markets favored companies that consumed resources while undervaluing those that produced them. Asset-light businesses commanded premium valuations, while industries tied to the physical economy — mining, energy, utilities, and heavy industry — were often neglected and underfunded.

Yet the real economy never disappeared. In fact, its importance is now becoming more apparent.

The expansion of artificial intelligence requires enormous amounts of electricity to power data centers. Electrification of transportation and manufacturing depends on vast quantities of copper and other metals. Efforts to rebuild domestic manufacturing and strengthen supply chains demand steel, critical minerals, and engineering capacity that has been underdeveloped for years. Energy security has also become a top political priority, encouraging renewed investment in domestic production infrastructure.

All of these forces point toward the same conclusion: the materials and energy systems that underpin the global economy are increasingly scarce relative to rising demand.

When markets begin to recognize a prolonged supply gap in strategically important commodities, the resulting repricing can be powerful and long-lasting. Recent strength in assets such as copper, gold, uranium, and energy infrastructure may be early evidence of that process.

Investment Implications

Viewing the current environment through the lens of stagflation frames it as a temporary economic problem. That interpretation misses the larger opportunity.

The macroeconomic risks are likely overstated: inflation is not deeply entrenched, the economy continues to expand, and the conditions that produced 1970s-style stagflation are absent. Investors who position primarily for economic collapse may find themselves overly defensive.

At the same time, the stagflation narrative understates the structural shift taking place. If markets are beginning to rotate from financial assets toward real ones — from digital platforms to the physical infrastructure supporting them — then the investment strategy should focus less on protection and more on positioning.

In simple terms, the beneficiaries are likely to be the builders rather than the spenders: companies involved in energy production, materials, infrastructure, and industrial supply chains, along with scarce hard assets.

History shows that when these types of market rotations begin, they often last longer and move further than most investors expect. Commodity sectors have experienced more than a decade of underinvestment, while the forces driving demand — artificial intelligence power needs, electrification, and reindustrialization — are structural trends rather than short-term cycles.

This moment may not replicate the 1970s. But it could mark the beginning of a similarly significant shift: a period in which the physical economy returns to the center of global capital markets, rewarding investors who recognize the change early.

Sources: Charles-Henry Monchau

Leave a comment