Key Highlights

Japan equities rally: Japanese stocks surged after Prime Minister Sanae Takaichi’s landslide election victory, boosting expectations of higher government spending on defense and AI. The Nikkei jumped as much as 4.2% to a record high, while the Topix rose up to 2.6%, led by gains in electronics and banking stocks.

Gold rebounds: Gold climbed above $5,000 an ounce, rising as much as 1.6% early on as dip buyers returned following a volatile week. The move was supported by Japan’s election outcome, which fueled expectations of looser fiscal policy and a weaker yen—both supportive for bullion. Gold remains about 11% below its Jan. 29 peak but is still up roughly 15% year to date.

Oil slips: Oil prices edged lower as easing Middle East tensions reduced near-term supply disruption risks. Talks between Iran and the U.S. in Oman on Tehran’s nuclear program were described by Iran as “a step forward.”

Asia markets higher: Asian equities opened higher, tracking Friday’s rebound on Wall Street. Stocks jumped in Japan and South Korea, with the Kospi—popular among AI-linked trades—surging 4%. U.S. futures were firmer after the S&P 500 closed about 2% higher on Friday amid dip-buying and improved consumer sentiment.

Algo-driven risks flagged: Goldman Sachs warned that trend-following algorithmic funds could accelerate U.S. equity selling this week. A renewed decline could trigger around $33 billion in automated sales immediately, with a break below 6,707 on the S&P 500 potentially unleashing up to $80 billion more over the next month. Thin liquidity and short-gamma positioning may keep volatility elevated.

AI fears spark selloff: Concerns over AI’s economic impact intensified after Anthropic unveiled new tools, triggering a broad selloff that erased $611 billion in market value across 164 software, financial services, and asset management stocks. Despite the selloff, fundamentals remain intact, with S&P 500 software and services earnings expected to grow 19% in 2026 and valuations becoming more attractive.

Wall Street rebound: U.S. equity futures ticked higher late Sunday after a strong rebound on Friday. Bitcoin jumped following steep losses, the Dow hit a fresh record above 50,000, and the S&P 500 reclaimed its 50-day moving average. The Nasdaq, however, remained below that key level and ended the week notably weaker.

U.S. Economic Data and Corporate Earnings Schedule

Investors are set to focus on the delayed January labor market data, alongside upcoming consumer inflation (CPI) and retail sales releases. The jobs and CPI reports were postponed due to a brief government shutdown last week, while December retail sales figures were also delayed following the 2025 shutdown.

The Federal Reserve continues to view inflation as “somewhat elevated,” with January’s CPI report, due Friday, expected to provide further clarity. As the central bank assesses risks to both inflation and employment as having eased, markets are pricing in no additional rate cuts before the June meeting. By then, Kevin Warsh—President Trump’s nominee for Fed chair—could be in office.

Despite the Fed’s year-end rate cut, futures markets still anticipate roughly two additional 25-basis-point cuts by December, a pricing stance that has remained largely unchanged since Warsh’s nomination last month.

Economic calendar:

Monday, Feb 9

Remarks from Fed officials including Governors Stephen Miran and Christopher Waller, along with Atlanta Fed President Raphael Bostic.

Tuesday, Feb 10

Key U.S. data releases include December retail sales, NFIB Small Business Optimism, the Q4 Employment Cost Index, December import prices, and November business inventories.

Cleveland Fed President Beth Hammack is also scheduled to speak.

Wednesday, Feb 11

The January U.S. employment report is due, alongside remarks from Vice Chair for Supervision Michelle Bowman.

The monthly U.S. federal budget for January will also be released.

Thursday, Feb 12

Data highlights include January existing-home sales and weekly initial jobless claims for the week ending Feb 7.

Governor Stephen Miran is scheduled to speak.

Friday, Feb 13

The January Consumer Price Index (CPI) will be released.

Earnings Calendar:

Monday, Feb. 9

Earnings are due from Apollo Global Management, Onsemi, Loews, and Principal Financial.

Tuesday, Feb. 10

A heavy earnings slate includes Coca-Cola, AstraZeneca, Gilead Sciences, BP, CVS Health, Spotify, Duke Energy, Marriott, Ferrari, Ecolab, Robinhood, Cloudflare, Ford, Honda Motor, and Barclays.

Wednesday, Feb. 11

Reports are expected from Cisco, McDonald’s, T-Mobile, AppLovin, and Shopify.

Thursday, Feb. 12

Applied Materials, Arista Networks, Unilever, Vertex Pharmaceuticals, Brookfield, Airbnb, and Coinbase Global are scheduled to report.

Friday, Feb. 13

Enbridge and Moderna round out the week.

Cisco is set to report fiscal Q2 results after Wednesday’s close. Consensus estimates call for adjusted EPS of $1.02, up 9% year over year, on revenue of $15.1 billion, an 8% increase. Product orders are expected to soften slightly following 13% growth last quarter, while AI-related orders may cool after reaching $1.3 billion in Q1. Investors will be watching for upside tied to Cisco’s AI-networking partnership with Nvidia and signs of a recovery in its security segment following a weak prior quarter despite the Splunk acquisition.

AstraZeneca reports Q4 results early Tuesday, with analysts forecasting flat adjusted EPS and roughly 4% sales growth. The company’s recent move from Nasdaq to the NYSE has helped propel shares sharply higher, up around 108% in February.

Robinhood is expected to post a roughly 38% decline in EPS to $0.63, even as revenue is seen rising nearly 34% to $1.36 billion on stronger options, equities, and transaction activity. Crypto revenue is projected to fall about 28% to $259 million. The company has recently faced regulatory scrutiny related to prediction markets, including halting sports-related contracts in Nevada, contributing to a sharp pullback in the stock last week.

Elsewhere, McDonald’s earnings are expected to show about 8% EPS growth—its strongest quarter since late 2023—while Coca-Cola is forecast to report modest slowing growth, despite shares gaining around 8% since breaking out in January.

By the end of the week, more than 80% of Dow Jones Industrial Average constituents will have reported earnings.

Technical Analysis:

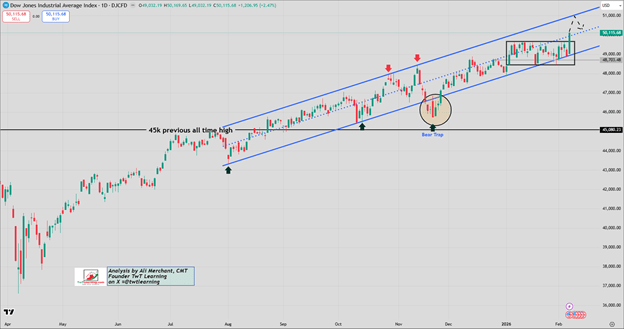

DJIA Index

The index confirmed a breakout from a bullish rectangular consolidation on Friday. As long as support at 49,970 holds, the upside target remains at 51,000.

DJIA daily candlestick chart.

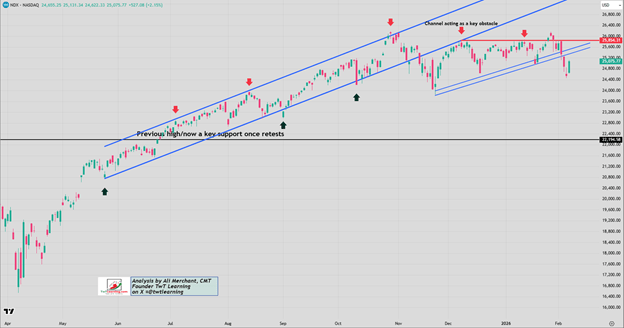

Nasdaq 100 Index

The NDX broke below the 25,200 support level last Wednesday, in line with the view that a sustained move under 25,200 would open the door toward 24,650. The index subsequently dropped to 24,455 before reclaiming 24,650. It is now rebounding toward 25,200, with further upside toward 25,370. A decisive break above 25,370 would expose resistance near 25,850.

NDX daily candlestick chart.

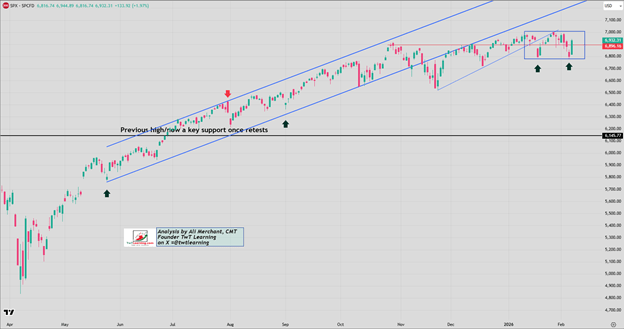

SPX Index

The SPX successfully defended the 6,790–6,780 support zone during its second pullback of the year. The index is now consolidating within a rectangular range. As long as support at 6,780 holds, the upside target remains 7,010.

SPX daily candlestick chart.

Weekly Probability Outlook for U.S. Indices

The U.S. weekly market probability map for Feb. 9–13, 2026 points to a mixed open for U.S. equity indices, followed by a stronger close and a rally developing midweek. The probability maps are based on historical seasonality trends, with sentiment readings generated through a seasonality-driven scoring model.

Sources: Ali Merchant

Leave a comment