Gold, silver, and mining stocks did initially move higher, but the rally was short-lived. Prices reversed intraday and then pushed lower, with the declines continuing today—benefiting all of our open trading positions. Hopefully, you followed the recommendation to short bitcoin, as previously emphasized.

The key question now is whether the corrective rebound has already run its course. In today’s analysis, the focus is on bitcoin and the equity market, as both remain closely linked to the performance of precious metals.

At this point, the odds appear evenly balanced. I’d put the chances at roughly 50/50, largely due to the factors driving the current pullback, at least over the near term.

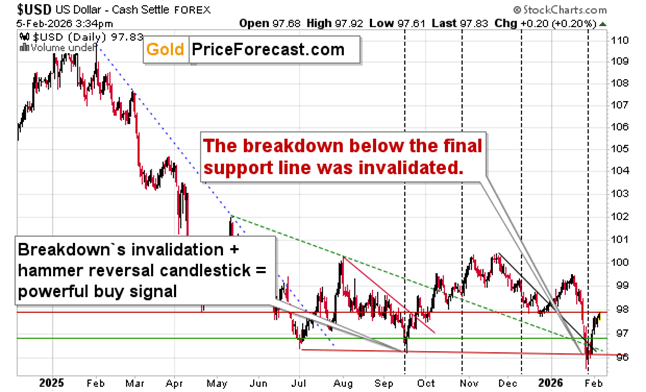

Looking Beyond the U.S. Dollar

The U.S. Dollar Index has rallied recently, and while it was one of the drivers behind last week’s decline in precious metals, it does not account for this week’s weakness, as the USDX has been relatively subdued.

So what drove the sharp selloff in silver and mining stocks? What triggered the move—aside from the fact that both markets were extremely overbought from a technical standpoint?

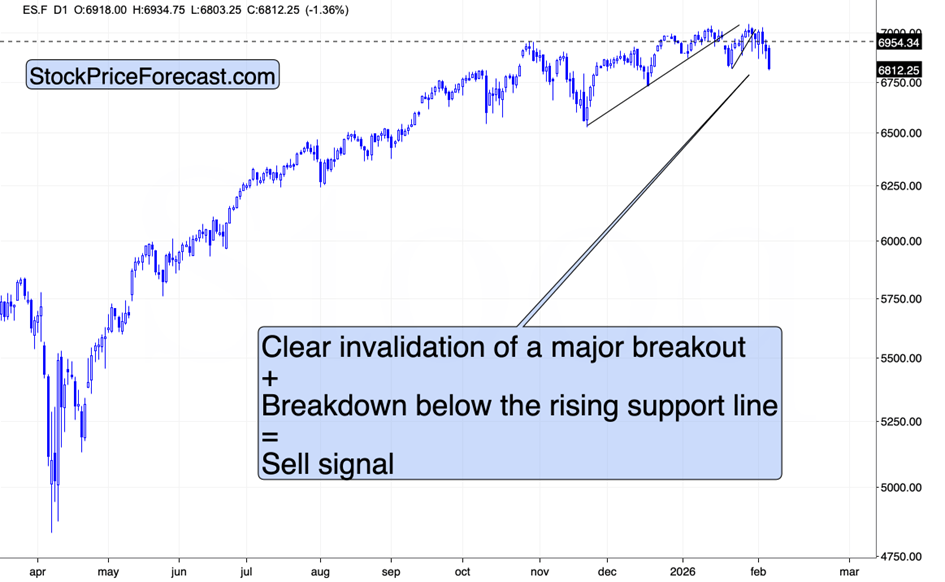

The key driver was the sharp drop in equities. While the S&P 500’s decline may not appear dramatic on the surface, it is notable given the unusually low volatility that had prevailed in recent months.

That situation is likely to shift. Some traders may even consider exposure to VIX-related instruments or call options, though shorting bitcoin arguably offers greater leverage.

Equities have moved back toward their recent lows, and silver and mining stocks followed suit. This type of synchronized behavior is typical—and closely mirrors the market dynamics observed in 2008.

And this is where the situation turns especially grim

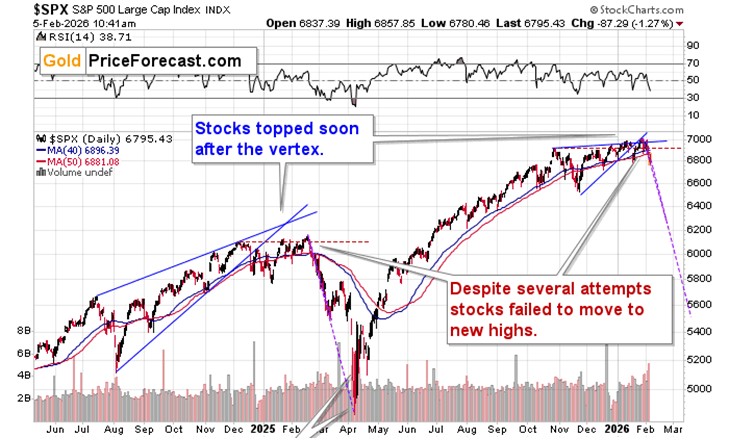

The stock market is now in a position similar to where it stood last year. After multiple attempts, it failed to hold a breakout above the prior year’s highs, effectively invalidating that move. The market also peaked shortly after reaching the vertex formed by earlier support and resistance lines.

If this pattern plays out again, the S&P 500 could fall toward the 6,300 area in the near term, stage a corrective rebound, and then slide further toward roughly 5,500.

Could it really drop that far?

Yes.

And in fact, a move to 5,500 may not mark the end of the market’s broader decline.

The AI Bubble Is Bursting

If the AI bubble does burst—and the sharp selloff in bitcoin suggests that risk appetite may already be cracking—the broader stock market could face a severe downturn. Much of the market’s prior strength was driven by aggressive buying in tech and AI-related names in the first place.

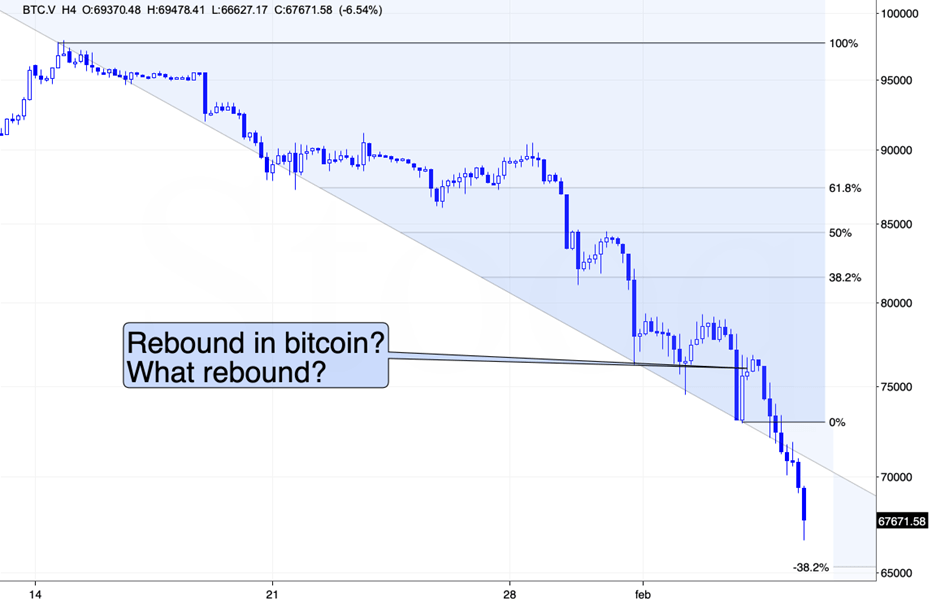

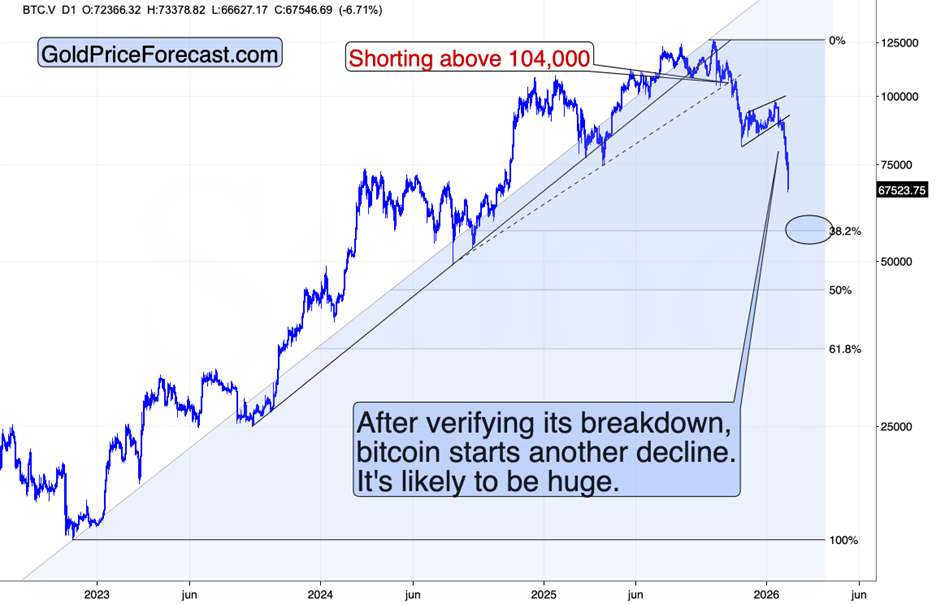

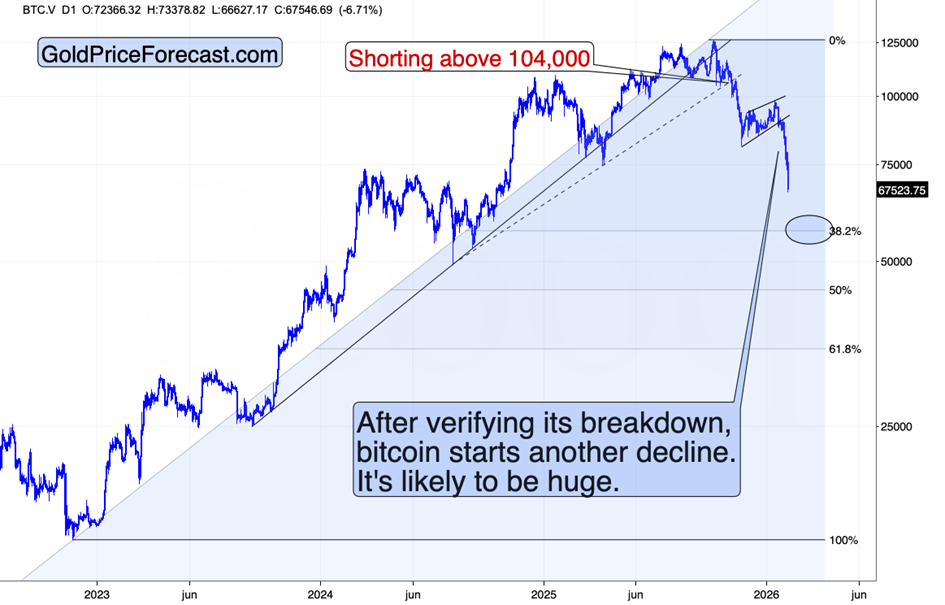

On the topic of bitcoin, here’s what I noted in yesterday’s Gold Trading Alert when discussing its recent “rebound”:

And while we’re on the subject of rebound magnitude, this is bitcoin’s rebound that barely qualifies as one. While prices did tick higher briefly, the move is almost imperceptible when viewed against the scale of the prior decline, visible only on very short-term charts.

This further underscores bitcoin’s underlying weakness and reinforces the case that gains on our short positions were likely to expand in the near term.

And that is precisely what unfolded.

The encouraging takeaway is that bitcoin still appears to have further downside ahead, suggesting our profits are likely to continue growing. The next meaningful support sits just below $60,000, though a brief drop toward the $50,000 level—a key round number and prior low—remains possible.

Such a move could, but does not necessarily have to, spark a rebound similar to the consolidation seen in 2024. If that scenario unfolds, it would likely form the right shoulder of a head-and-shoulders pattern, which could ultimately point to a much deeper decline toward the $30,000–$35,000 range.

So what does all of this mean for the precious metals market?

It suggests that a 2008-style crisis could indeed unfold again in the coming months.

This is a critical point. Although there is limited data to confirm it conclusively, silver and mining stocks have so far shown a strong correlation with the broader equity market’s performance.

Sources: Przemyslaw Radomski

Leave a comment