Bank of Japan (BoJ) Governor Kazuo Ueda is speaking at a press conference, outlining the rationale for keeping the benchmark interest rate unchanged at 0.75% at the January policy meeting.

Key takeaways from the BoJ press conference

Japan’s economy is showing a moderate recovery and is expected to continue growing at a steady pace.

The government’s economic stimulus package has improved the overall outlook.

Underlying inflation is projected to rise gradually and move closer to the 2% target.

Board members Takata and Tamura suggested revisions to the outlook report.

The BoJ will continue to raise interest rates if economic and price projections are realized.

Lending rates tied to the BoJ’s policy rate are already trending higher.

Financial conditions remain accommodative despite the December rate hike.

Foreign exchange movements are influenced by multiple factors.

The governor refrained from commenting on specific yen levels but emphasized close monitoring of FX developments.

Government bond yields are increasing at a rapid pace.

The BoJ stands ready to conduct bond-buying operations flexibly in exceptional circumstances.

Measures may be taken to support stable yield formation when necessary.

Currency movements, particularly the yen, may be having a stronger impact on prices.

Greater attention will be paid to foreign exchange trends going forward.

The rise in long-term yields is partly influenced by end-of-fiscal-year factors.

Price developments in April will be an important consideration when assessing the timing of future rate hikes.

The section below was published at 3:35 GMT on January 23 to cover the Bank of Japan’s monetary policy announcement and the initial market reaction.

The Bank of Japan (BoJ) board voted to keep the short-term policy rate unchanged at 0.75% at the conclusion of its two-day monetary policy meeting on Friday, a move that was widely expected.

As a result, borrowing costs remain at their highest level in roughly three decades.

Key takeaways from the BoJ’s policy statement

Japan’s economy is expected to continue a moderate recovery.

Consumer inflation is likely to pick up gradually.

The virtuous cycle in which wage growth and inflation reinforce each other is expected to be sustained.

The output gap is projected to improve over time and expand at a moderate pace.

Medium- to long-term inflation expectations are seen rising gradually.

No major imbalances are observed in Japan’s financial activity.

The overall financial system remains stable.

Firms’ moves to pass higher wages on to selling prices could strengthen more than previously anticipated.

The recent increase in food prices, including rice, mainly reflects temporary supply-side factors.

Significant uncertainty surrounds the global economic outlook, particularly due to trade policies that could push up import prices through supply-side channels.

Trade measures announced so far may weigh on global economic growth.

Regarding the US economy, close attention is needed on how tariffs could affect employment and income via weaker corporate profits.

High uncertainty persists around China’s economic outlook, especially the future pace of growth.

A sharp rise in import prices could further reinforce households’ cautious stance on spending.

Current trade policies could lead to a shift in the long-term trend of globalisation.

The Board raised its median real GDP growth forecast for fiscal 2025 to +0.9% from +0.7% in October.

The fiscal 2026 median growth forecast was revised up to +1.0% from +0.7%.

The fiscal 2027 median growth forecast was lowered to +0.8% from +1.0%.

BoJ’s Quarterly Outlook Report: Key Highlights

The Board kept its median core consumer price index forecast for fiscal 2025 unchanged at +2.7%, the same as in October.

The median real GDP growth forecast for fiscal 2025 was revised up to +0.9% from +0.7% in October.

Real interest rates remain at significantly low levels.

Risks to the economic outlook are assessed as roughly balanced.

The impact of foreign exchange volatility on prices has become more pronounced than in the past, as firms are more willing to raise prices and wages.

Core consumer inflation is expected to slow to below 2% during the first half of this year.

Companies’ efforts to pass higher wages on to selling prices could strengthen more than anticipated.

Japan’s economy is projected to continue a moderate recovery.

Market reaction following the BoJ policy announcements

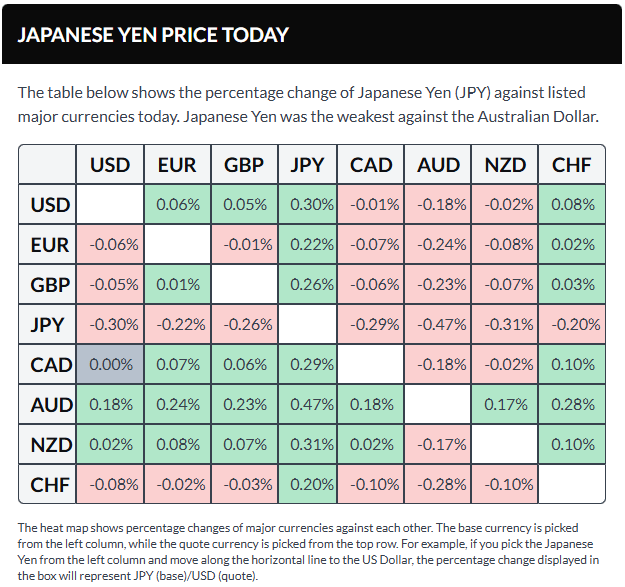

USD/JPY climbed further toward 158.60 in an immediate reaction to the Bank of Japan’s (BoJ) decision to keep interest rates unchanged, rising 0.11% on the day.

The section below was published at 23:00 GMT on January 22 as a preview of the Bank of Japan’s interest rate decision.

- The Bank of Japan is widely expected to leave interest rates unchanged at 0.75% on Friday.

- The central bank is likely to wait and assess the effects of December’s rate hike before considering further tightening.

- February’s general elections introduce an additional layer of uncertainty to the BoJ’s monetary policy outlook.

The Bank of Japan (BoJ) is widely expected to keep its benchmark interest rate unchanged at 0.75% following the conclusion of its two-day monetary policy meeting next Friday.

The Japanese central bank raised interest rates to their highest level in three decades in December and is now likely to keep policy unchanged on Friday to better evaluate the economic impact of earlier hikes.

BoJ Governor Kazuo Ueda is expected to reaffirm the bank’s commitment to continued policy normalisation. As a result, investors will closely scrutinise his press conference for clues on the timing and extent of the next phase of the tightening cycle.

What to anticipate from the Bank of Japan’s interest rate decision?

The Bank of Japan is broadly expected to leave interest rates unchanged in January while signaling the possibility of further tightening if economic conditions unfold as projected.

In December, the BoJ raised rates by 25 basis points to 0.75%, and the meeting minutes showed that some policymakers favor additional tightening, noting that real interest rates remain sharply negative once inflation is taken into account.

Markets, however, have ruled out consecutive rate hikes, especially following Prime Minister Sanae Takaichi’s surprise call for snap elections and her proposal to suspend food and beverage taxes for two years to ease the burden on households amid rising inflation.

While the implications of these political developments for monetary policy remain uncertain, the BoJ has emphasized a cautious, gradual normalization of policy, aiming to withdraw stimulus without undermining economic growth. As a result, the central bank is likely to wait for greater political clarity and for the effects of past rate increases to become clearer before moving again.

Meanwhile, the yen has weakened steadily amid speculation surrounding the snap election. This raises the question of whether the currency’s depreciation will push the BoJ to adopt a firmer stance on monetary tightening.

How might the Bank of Japan’s monetary policy decision influence the USD/JPY exchange rate?

Markets have fully priced in a Bank of Japan rate pause on Friday, but the central bank will need to clearly signal further monetary tightening to curb the Yen’s ongoing weakness.

Yen sellers have eased off in recent days, helped by broad US Dollar softness linked to the EU–US trade dispute following President Donald Trump’s threats over Greenland. Even so, USD/JPY is still up roughly 0.7% year to date and remains close to last week’s 18-month peak around 159.50.

Investors are also concerned that Prime Minister Takaichi could secure stronger parliamentary backing after the elections, allowing her to push ahead with expansionary fiscal policies such as higher spending and tax cuts. This has heightened worries about Japan’s already stretched public finances, driving the Yen lower and pushing long-term government bond yields to record highs amid fears of a potential fiscal crisis.

Meanwhile, recent remarks from BoJ Governor Ueda have reinforced the bank’s cautious tightening stance, suggesting Japan is transitioning toward a more sustainable inflation environment where wages and prices rise together. For the Yen’s recent, still-fragile rebound to continue, markets will need clearer evidence that interest rate hikes are on the horizon.

USD/JPY 4-Hour Chart

From a technical standpoint, FXStreet analyst Guillermo Alcalá views USD/JPY as undergoing a bearish correction, with an important support zone just above 157.40. He notes that while the pair has pulled back from recent highs, Yen buyers would need to push it below the 157.40–157.60 support area to invalidate the short-term bullish structure and open the door to a move toward the early-January lows near 156.20.

A cautious or non-committal message from the BoJ would likely disappoint markets and weaken the Yen. In that scenario, Alcalá expects USD/JPY to climb to new long-term highs. He points out that technical signals are improving, with the 4-hour RSI rebounding from the 50 level, indicating strengthening bullish momentum. At the time of writing, the pair is challenging resistance around 158.70 (the January 16 high), which stands as the final hurdle before the 18-month peak close to 159.50.

Sources: Fxstreet

Leave a comment