The U.S. Consumer Price Index (CPI) is forecast to increase by 3.3% year-on-year in March, driven sharply higher by rising energy prices. Core CPI inflation is also expected to tick up slightly to 2.7% annually. Meanwhile, the EUR/USD technical outlook remains mildly bullish in the near term.

The U.S. Bureau of Labor Statistics (BLS) is scheduled to release March Consumer Price Index (CPI) data on Friday.

The report is widely expected to show an uptick in inflation, largely driven by the surge in crude oil prices following increased tensions after a joint U.S.–Israel strike on Iran.

The monthly CPI is projected to increase by 0.9%, up from a 0.3% rise in March, while the annual rate is expected to climb to 3.3%—its highest level since May 2024—from 2.4% in February. Core CPI, which excludes food and energy, is forecast to rise 0.3% on the month and 2.7% year-on-year.

Since the outbreak of conflict in the Middle East on February 28, West Texas Intermediate (WTI) crude has surged roughly 40%, even after easing following a recent two-week ceasefire announcement between the U.S. and Iran. In March alone, WTI jumped nearly 50%, rising from around $67 per barrel to close near $100.

According to TD Securities analysts, the spike in crude prices is expected to be the main driver behind the sharp 0.9% monthly CPI increase, pushing the annual reading up by nearly one percentage point to 3.3%, marking a two-year high. They also noted that core inflation is likely to remain relatively contained at 0.27% month-on-month, though goods prices may continue to rise due to tariff pass-through, with “supercore” inflation staying firm around 0.3%.

CPI data

The next CPI report is expected to be heavily influenced by recent volatility in oil prices, meaning the March inflation print will likely show a noticeable jump in headline CPI—something that markets have already largely anticipated.

Even if annual inflation rises to around 3.3% as forecast, investors may treat it as a temporary spike rather than a lasting inflation trend, assuming oil prices retreat if geopolitical tensions ease and a durable truce in the Middle East helps stabilize supply routes such as the Strait of Hormuz.

However, uncertainty around the durability of any ceasefire—and political conditions tied to control of key shipping lanes—adds risk to the outlook. This makes it harder to assume a sustained decline in oil prices, and therefore keeps inflation expectations sensitive to geopolitical developments rather than the CPI data alone.

On the policy side, the Federal Reserve’s recent meeting minutes suggest policymakers are becoming more cautious about cutting interest rates. Many are concerned that inflation could remain stickier than expected, especially if higher energy prices begin to feed into broader price pressures.

Still, some analysts, such as those at BBH, argue that if underlying (core) inflation stays contained, the Fed may be able to “look through” the temporary oil-driven inflation spike and avoid tightening further, even amid a mixed U.S. labor market.

What impact might the US Consumer Price Index (CPI) report have on EUR/USD?

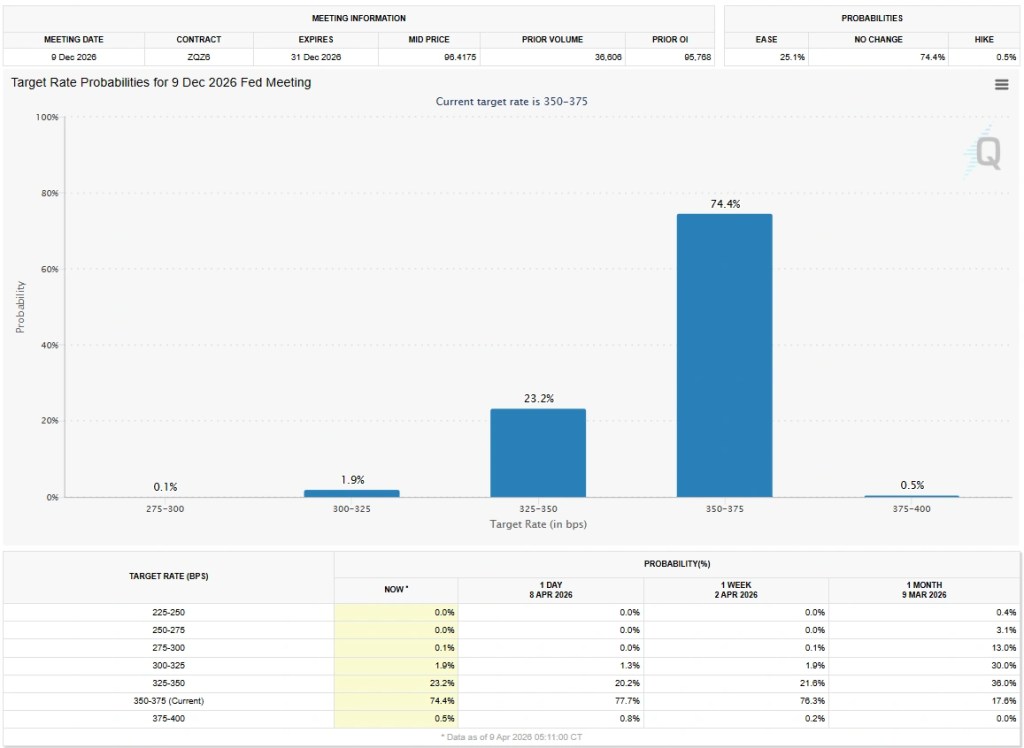

Currently, markets are pricing in about a 75% probability that the Federal Reserve will keep its policy rate unchanged at 3.5%–3.75% by the end of the year, a sharp increase from just 17% on March 9, according to the CME FedWatch Tool.

A stronger-than-expected March CPI reading may have limited impact on reshaping expectations for the Federal Reserve’s interest rate path. However, if high inflation data coincides with renewed escalation in Middle East tensions and rising concerns that shipping activity in the Strait of Hormuz will not return to normal levels soon, markets could start pricing in a higher likelihood of a Fed response to persistent inflation pressures. In that case, the US dollar could strengthen, pushing EUR/USD lower.

On the other hand, the dollar may stay under pressure—and EUR/USD could extend its recovery—if oil prices keep declining steadily, even if the CPI report comes in hot.

Overall, March inflation data alone is unlikely to trigger a major market reaction, with investors remaining more focused on the US–Iran geopolitical situation and its implications for energy prices.

From a technical perspective, Eren Sengezer, FXStreet European Session Lead Analyst, notes that EUR/USD’s short-term outlook remains tilted to the upside. The RSI on the daily chart has moved above 50 for the first time since the US–Iran conflict began, and the pair has broken above a two-month descending trendline.

Key resistance levels are seen at 1.1730 (Fibonacci 50% retracement of the February–April move), followed by 1.1800 (61.8%) and 1.1900 (78.6%). On the downside, initial support lies at 1.1650 (38.2%). If that level breaks, sellers may target 1.1560 (23.6%) and then the psychological 1.1500 level.

Leave a comment