For years, a dependable macro strategy was to buy dips when economic data weakened. Softer labor figures implied a more accommodative Fed, leading to lower discount rates and, in turn, higher equity valuations. That chain is now being tested.

The key issue this Wednesday isn’t whether the data are weak—they clearly are. The real question is whether markets can continue to interpret soft data as a trigger for policy easing when inflation signals remain stubborn.

A Familiar Macro Play—and Why It May Be Breaking Down

For much of the past three years, equity markets leaned on a simple framework: weaker growth would trigger easier monetary policy, and that easing would offset the damage from slowing activity. Soft payrolls boosted expectations of rate cuts, often lifting stocks. Weak manufacturing data pushed bond yields lower, compressing discount rates and supporting higher valuations—especially in growth equities. The pattern became almost automatic.

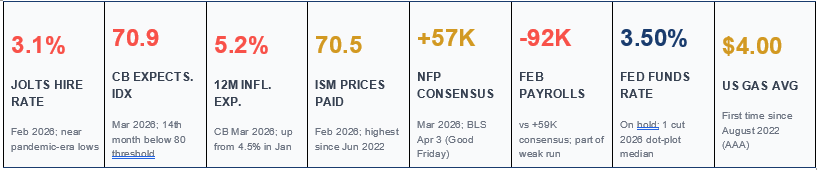

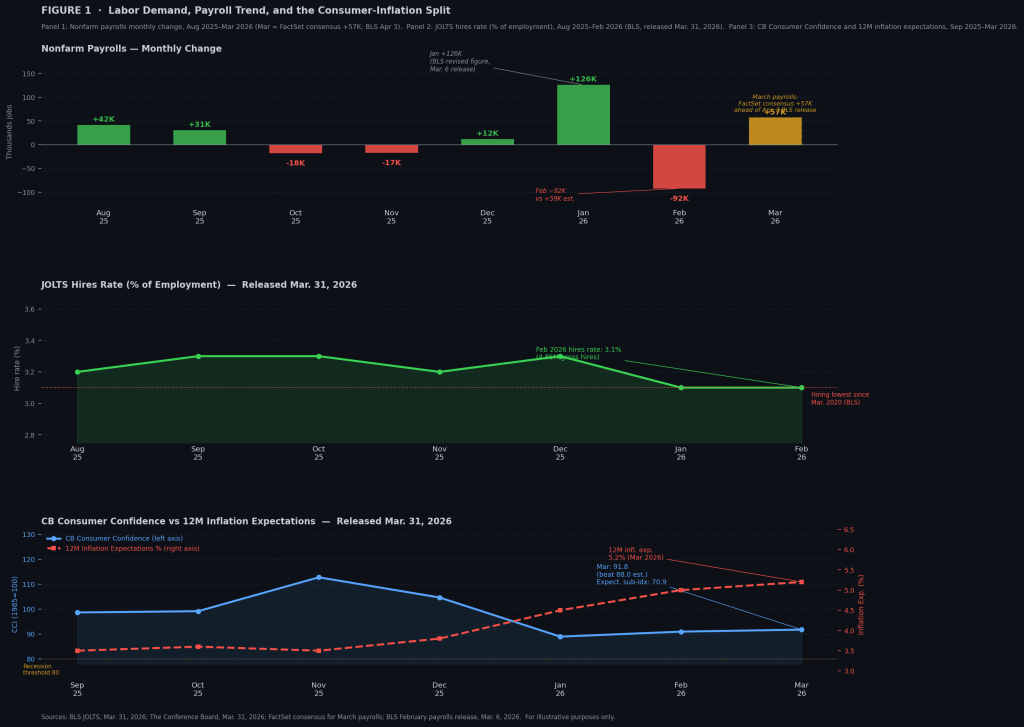

But that playbook only works when slowing growth comes with easing inflation. A disinflationary slowdown gives the Fed room to cut rates. When growth weakens while inflation pressures stay firm, that flexibility disappears. Easing policy into persistent price pressure risks unanchoring inflation expectations, which could later require more aggressive tightening. Today’s data point to exactly that mismatch: labor conditions are deteriorating, while inflation-sensitive indicators remain elevated. The JOLTS hires rate for February dropped to 3.1%, near pandemic-era lows, with hiring at its weakest since March 2020. Meanwhile, the Conference Board’s 12-month consumer inflation expectations rose to 5.2% in March, up from 4.5% in January. In other words, hiring is slowing sharply even as households expect higher inflation ahead.

Jerome Powell addressed this dilemma directly in remarks at Harvard on Monday. He highlighted the downside risks to the labor market, which argue for lower rates, alongside upside risks to inflation, which argue against easing. The Fed can afford to sit with that tension and wait for clearer trends—but markets typically cannot; they adjust immediately to incoming data. If Wednesday’s ISM Prices Paid index stays elevated following February’s 70.5 reading—the highest since mid-2022—it would reinforce what the mixed signals already suggest: this is not the kind of slowdown the old “buy-the-dip” reflex was designed for.

What the Hiring Data Is Already Signaling

The labor market’s weakening is showing up more clearly in the JOLTS hires rate than in headline payroll numbers. This metric tracks gross hiring as a share of total employment, and at 3.1% in February, it has dropped to levels last seen during the pandemic slowdown. While layoffs remain relatively low—and initial jobless claims around 213,000 suggest companies aren’t aggressively cutting staff—the real shift is in reduced hiring activity. The labor market is losing momentum on both sides: workers are less willing to quit, and employers are less willing to hire. Both trends point to softening demand.

The quit rate has stayed at or below 2.0% for eight straight months through February, with total quits falling to 2.97 million—the lowest since August 2020. When workers stop leaving jobs, it reflects declining confidence in finding better opportunities. This kind of stagnation tends to push unemployment higher धीरे through attrition rather than layoffs, making the deterioration less visible in monthly payroll reports. February’s payroll decline of 92,000 followed a series of inconsistent and often weak readings, including multiple recent negative months. Even January’s gain was driven by narrow sector strength rather than broad-based hiring. For March, the FactSet consensus sits at +57,000, but much of that expected increase may simply reflect the return of workers temporarily excluded in February due to a healthcare strike—hardly a sign of genuine improvement.

The ADP private payroll report, scheduled for release Wednesday morning, will offer an early look at March hiring trends. While ADP emphasizes that its data is independent and not a forecast of official figures, its February reading of +63,000 diverged significantly from the government’s count. At this point, the exact number matters less than the direction: whether hiring picked up meaningfully in March, or whether the slowdown seen in JOLTS extended into the new data.

Technical Snapshot

JOLTS – February 2026 (released Mar 31)

Job openings declined to 6.9 million from 7.2 million in January. Hiring totaled 4.85 million, with the hires rate at 3.1%—near pandemic-era lows and the weakest since March 2020. Quits fell to 2.97 million, marking an eighth straight month at or below 2.0%.

Conference Board Consumer Confidence – March 2026

The headline index came in at 91.8, above the 88.0 consensus. The Present Situation component rose 4.6 points to 123.3, while Expectations slipped 1.7 points to 70.9—its 14th consecutive month below the 80 threshold often associated with recession risk. One-year inflation expectations climbed to 5.2%, up from 4.5% in January.

ISM Manufacturing PMI – February (latest actual)

The headline PMI registered 52.4. The Prices Paid component surged to 70.5, the highest since June 2022. The March reading is due Wednesday, April 1 at 10:00 AM ET, marking the first release since the late-February escalation.

ADP Private Payrolls – March (Apr 1, 8:15 AM ET)

Still pending. February showed a gain of 63,000, though this diverged sharply from the BLS estimate (roughly -50,000 in private payrolls). ADP emphasizes that its figures are independent and not a direct forecast of official data.

Nonfarm Payrolls – March (Apr 3, 8:30 AM ET)

Consensus stands at +57,000, according to FactSet. U.S. equity markets (NYSE, Nasdaq) will be closed for Good Friday, with SIFMA recommending a full bond market closure. The next regular equity session is Monday, April 6.

10-Year U.S. Treasury Yield

Currently at 4.41%, hovering near an eight-month high and up 44 basis points from 3.97% before the late-February escalation.

U.S. National Average Gasoline Price (AAA, Mar 31)

$4.00 per gallon, reaching that level for the first time since August 2022.

How the Data Panels Frame the Argument

The three panels together lay out the core evidence. The first highlights a choppy payroll trend with several negative prints, and even if March meets expectations, hiring remains subdued. The second shows that the drop in the hires rate is not just monthly noise but a structural shift—hovering near pandemic-era lows while separations stay relatively stable, meaning the weakness is concentrated in reduced hiring. The third panel captures the real tension: consumer confidence from the The Conference Board came in stronger than expected at 91.8, yet the Expectations index sits at 70.9, below the recession signal threshold for 14 straight months. At the same time, 12-month inflation expectations climbed to 5.2%. Households are both pessimistic about growth and anticipating higher inflation—a mix that limits the Fed’s flexibility. Cutting rates risks reinforcing inflation expectations, while holding steady risks deepening the slowdown.

ISM Prices Paid: The Deciding Variable

While early attention will likely focus on the ADP payroll release, the more critical variable is the inflation signal from ISM. The Prices Paid index surged to 70.5 in February, its highest since mid-2022, reflecting rising input costs across commodities and tariffs. March will be the first reading to fully capture conditions after the late-February conflict, including the energy shock.

With oil prices elevated and gasoline back above $4 per gallon, this release becomes the first real test of how deeply cost pressures are feeding into the production chain. If Prices Paid remains high—or climbs further—while hiring data weakens, it creates the exact setup that challenges the old market playbook. Soft labor data alone would typically support expectations of easing, but persistent cost pressures make that response less likely without accepting inflation risk.

That divergence matters. The traditional “bad data is good news” logic only works when both growth and inflation move in the same direction. If hiring weakens while inflation signals stay firm, that relationship breaks down.

A Shift in Market Interpretation?

The issue isn’t that one week of data changes the macro outlook—it’s that the framework markets use to interpret data may no longer hold. The familiar reflex—weak data leads to rate-cut expectations, which lifts equities—was built in an environment where the Fed had room to ease because inflation was falling alongside growth. When those two forces diverge, that reflex starts to fail.

Jerome Powell emphasized this balance in recent remarks, noting that policy operates with long and variable lags and that the Fed does not respond mechanically to every short-term shock. That approach preserves institutional credibility. Markets, however, operate differently—they price probabilities in real time. The risk isn’t simply weak data; it’s weak data paired with stubborn inflation, which removes the usual policy backstop.

What Comes Next: CPI as the Decisive Test

The next major checkpoint is the March CPI release on April 10. February’s data largely preceded the late-February shock, while March will begin to reflect its impact—especially through energy prices. If CPI confirms what current indicators suggest—a cooling labor market alongside rising inflation expectations—it would strengthen the case that the old interpretation mechanism is no longer reliable.

Wednesday’s data won’t settle the question. But it will be the first structured test of whether markets can still treat weak data as bullish in an environment where inflation refuses to cooperate.

Sources: Khasay Hashimov

Leave a comment