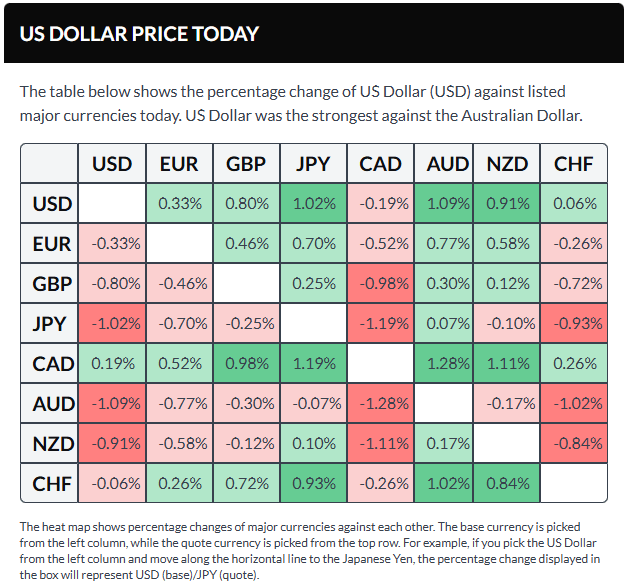

The US dollar weakened over the week, with the US Dollar Index (DXY) falling back below the 100 mark to around 99.60 by Friday, after a midweek boost following the Federal Reserve’s decision to keep interest rates unchanged at 3.50%–3.75%. Meanwhile, the conflict in Iran has entered its third week, and the Strait of Hormuz remains effectively shut, keeping oil prices elevated. Reports of the Pentagon sending thousands more Marines to the region point to a prolonged standoff. At the same time, Fed Chair Jerome Powell warned that inflationary pressures may still build further.

EUR/USD is hovering around the 1.1550 level after hitting new lows for 2026 earlier in the week, despite the European Central Bank’s hawkish stance, with markets now assigning an 85% chance of a rate hike this year.

GBP/USD is trading near 1.3330 after the Bank of England kept rates unchanged on Thursday but hinted that further tightening could be necessary if energy-led inflation continues.

USD/JPY is holding close to 159.30, with the yen gaining support as the Bank of Japan signaled a return to policy normalization.

AUD/USD is sitting around 0.7010 following a second straight rate hike from the Reserve Bank of Australia, though broader risk-off sentiment is still weighing on the currency.

West Texas Intermediate (WTI) crude is near $98 per barrel, close to weekly highs, after Israeli Prime Minister Benjamin Netanyahu indicated efforts to reopen the Strait of Hormuz.

Gold dropped sharply to $4,583 amid a heavy selloff driven by rising Treasury yields and forced liquidations of leveraged positions, overwhelming any safe-haven demand linked to the conflict.

Upcoming economic outlook: Key voices to watch

Monday, March 23:

- ECB’s Escrivá

- ECB’s Cipollone

- ECB’s Lane.

Tuesday, March 24:

- RBNZ’s Breman

- ECB’s Kocher

- ECB’s Sleijpen

- ECB’s Cipollone

- ECB’s Nagel

- ECB’s Lane

- Fed’s Barr

Wednesday, March 25:

- ECB’s President Lagarde

- ECB’s Lane

- BoE’s Greene

- Fed’s Miran

Thursday, March 26:

- ECB’s De Guindos

- BoE’s Breeden

- BoE’s Greene

- BoE’s Taylor

- Fed’s Cook

- Fed’s Miran

- Fed’s Jefferson

- Fed’s Logan

- Fed’s Barr

Friday, March 27:

- Fed’s Daly

- Fed’s Paulson

- ECB’s Schnabel

Saturday, March 28:

- ECB’s Cipollone

These scheduled speeches and appearances from central bank officials across the European Central Bank, Federal Reserve, Bank of England, and Reserve Bank of New Zealand will be closely watched for signals on inflation, interest rates, and policy direction amid ongoing global uncertainty.

Key economic data and central bank signals shaping policy outlook

Monday, March 23:

- Eurozone March Consumer Confidence (Preliminary)

- Australia March S&P Global PMIs (Preliminary)

- Japan February Consumer Price Index

Tuesday, March 24:

- Eurozone March HCOB PMIs (Preliminary)

- UK March S&P Global PMIs (Preliminary)

- US ADP Employment Change

- US Q4 Nonfarm Productivity & Unit Labor Costs

- US March S&P Global PMIs (Preliminary)

- Bank of Japan Monetary Policy Meeting Minutes

Wednesday, March 25:

- Australia February Consumer Price Index

- United Kingdom Inflation Data (CPI, PPI, RPI)

- Switzerland March ZEW Expectations Survey

- Germany March IFO Business Climate

- Swiss National Bank Quarterly Bulletin (Q1)

Thursday, March 26:

- Germany April GfK Consumer Confidence

- Eurozone Q4 Gross Domestic Product

- Deutsche Bundesbank Monthly Report

- US Initial Jobless Claims

- New Zealand March ANZ–Roy Morgan Consumer Confidence

Friday, March 27:

- UK March Consumer Confidence

- UK February Retail Sales

- Eurozone March Harmonized Index of Consumer Prices (Preliminary)

- US March Michigan Consumer Sentiment & Inflation Expectations

This packed calendar of releases across major economies—alongside guidance from institutions like the European Central Bank, Federal Reserve, and Bank of England—will play a crucial role in shaping expectations for interest rates, inflation trends, and overall monetary policy direction in the near term.

Sources: Agustin Wazne

Leave a comment