This week will see a series of major central bank meetings worldwide, including those of the Federal Reserve, European Central Bank, Bank of Japan, and Bank of England. With oil prices climbing sharply and inflation expectations edging higher, investors will be closely watching how policymakers assess the outlook for monetary policy and the implications of elevated energy costs.

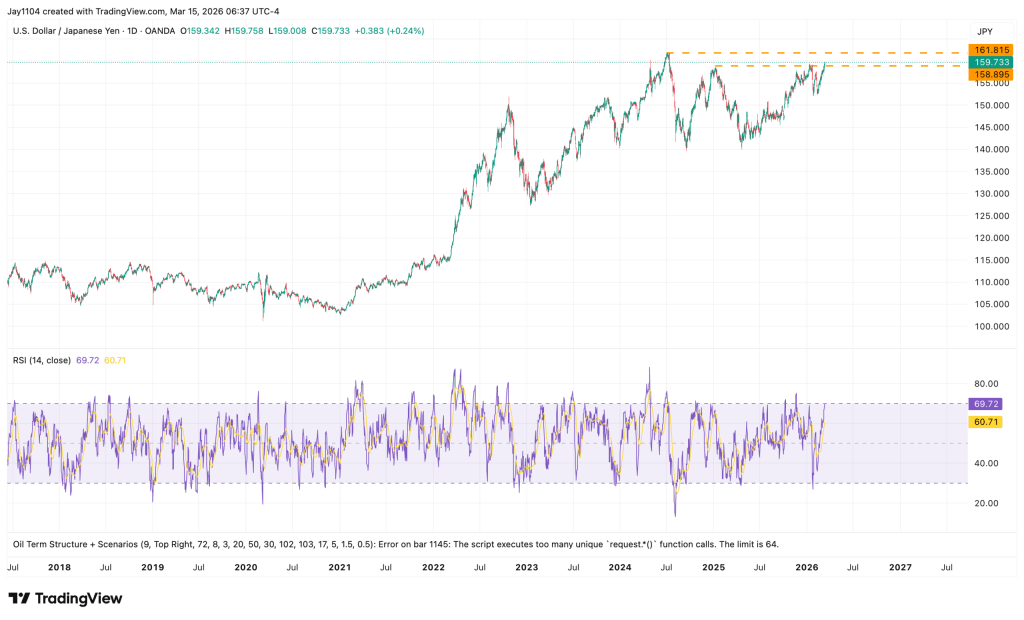

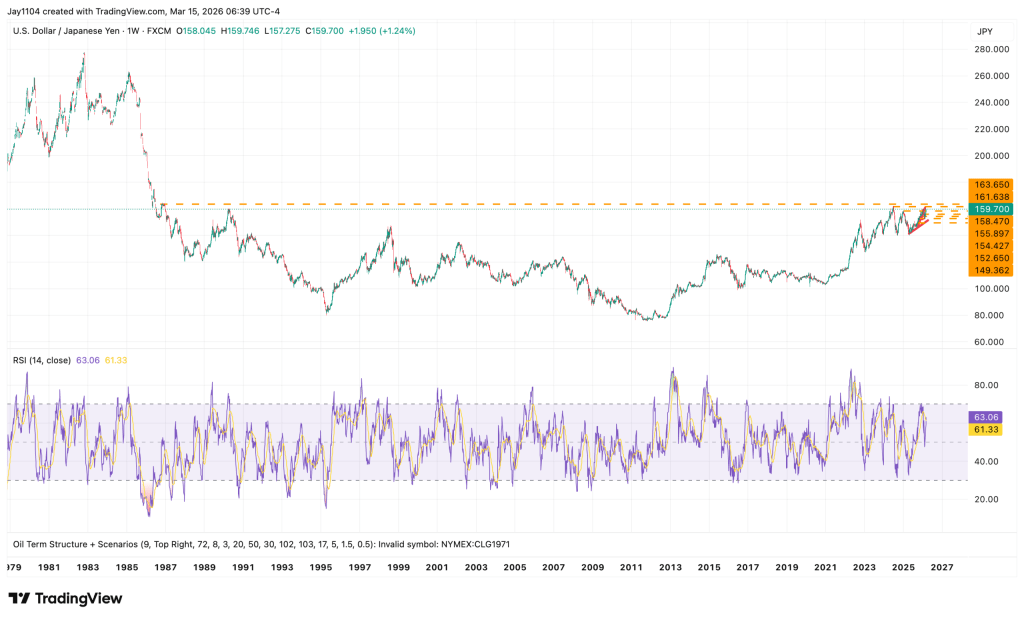

Among these institutions, the Bank of Japan faces perhaps the most delicate situation, particularly after the country’s February general election and the policy trajectory it had already been pursuing since its previous meeting. With oil trading near $100 a barrel, the BOJ must proceed cautiously as the USD/JPY exchange rate moves toward 160 — a level widely viewed as a potential tipping point for the currency.

The pair has already broken above resistance near 159, though it still remains below the highs reached in July 2024.

From a technical perspective, once USD/JPY moves above its July 2024 peak, there would be no clear resistance levels ahead, potentially opening the door for further and possibly sharp depreciation of the Japanese yen.

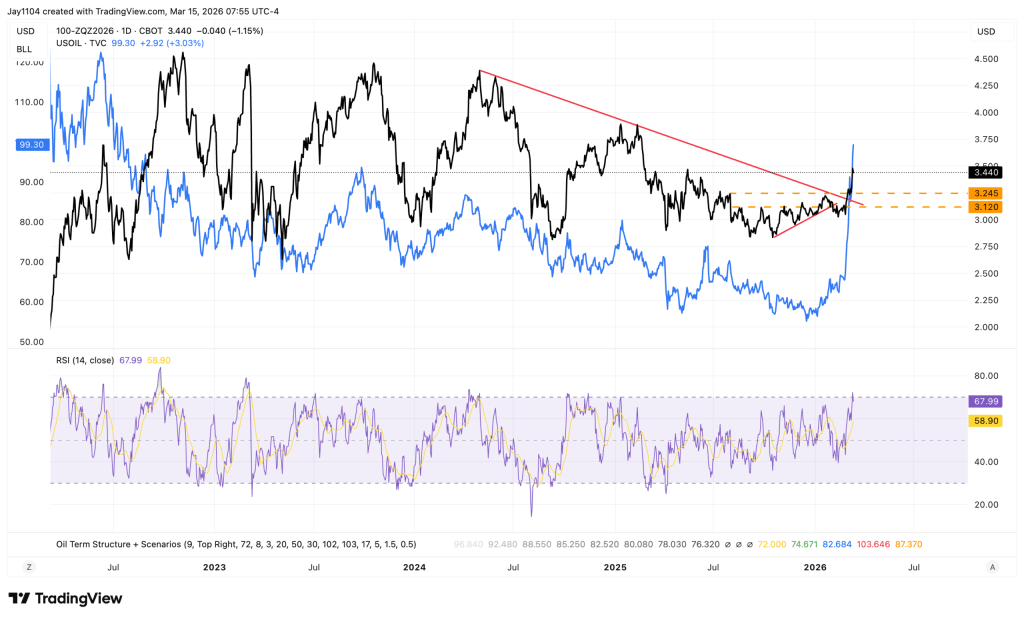

Meanwhile, the recent surge in oil prices has reshaped expectations for U.S. interest-rate cuts. Markets have gradually scaled back their projections for easing, even though the incoming Federal Reserve chair nominee has indicated a preference for looser monetary policy.

December Fed funds futures have climbed to around 3.44%, reflecting reduced expectations for rate cuts. Since 2022, market pricing for Fed easing has broadly moved in tandem with oil prices.

If oil continues to rise, it could complicate the Fed’s ability to lower rates, as higher energy costs tend to fuel inflation. Rate cuts may only become more likely if oil prices rise to a point where they begin pushing the economy toward recession.

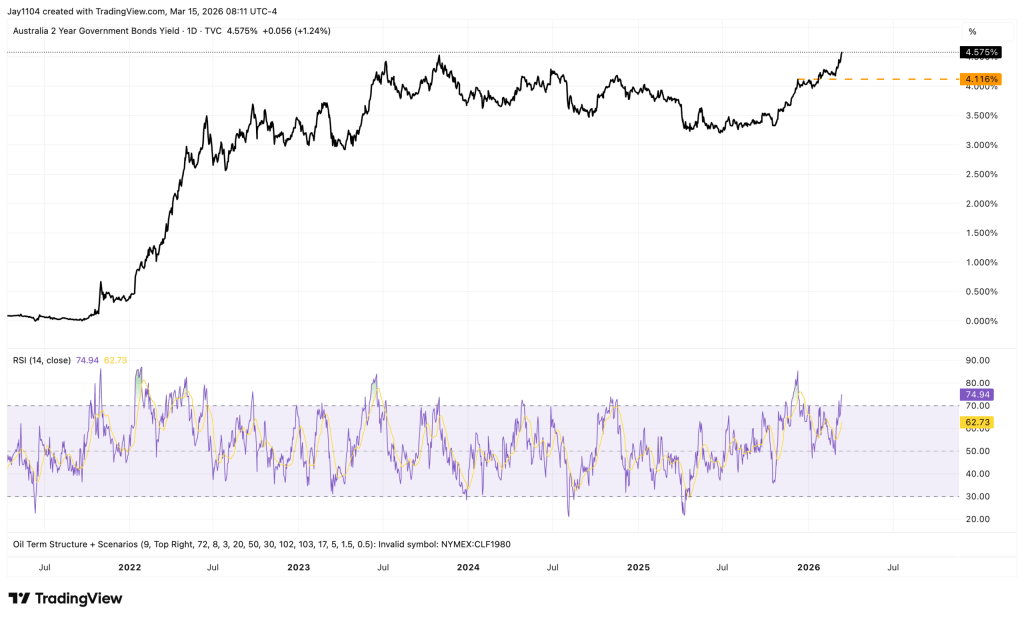

Rising rates are not limited to the U.S., as Australia’s 2-year bond yield has now moved above its October 2023 peak.

Rising global oil prices are likely to tighten liquidity and financial conditions worldwide. Tighter financial conditions typically place pressure on economic activity and risk markets. As long as oil prices remain elevated — or continue to climb — they are likely to further tighten global financial conditions and weigh on risk assets.

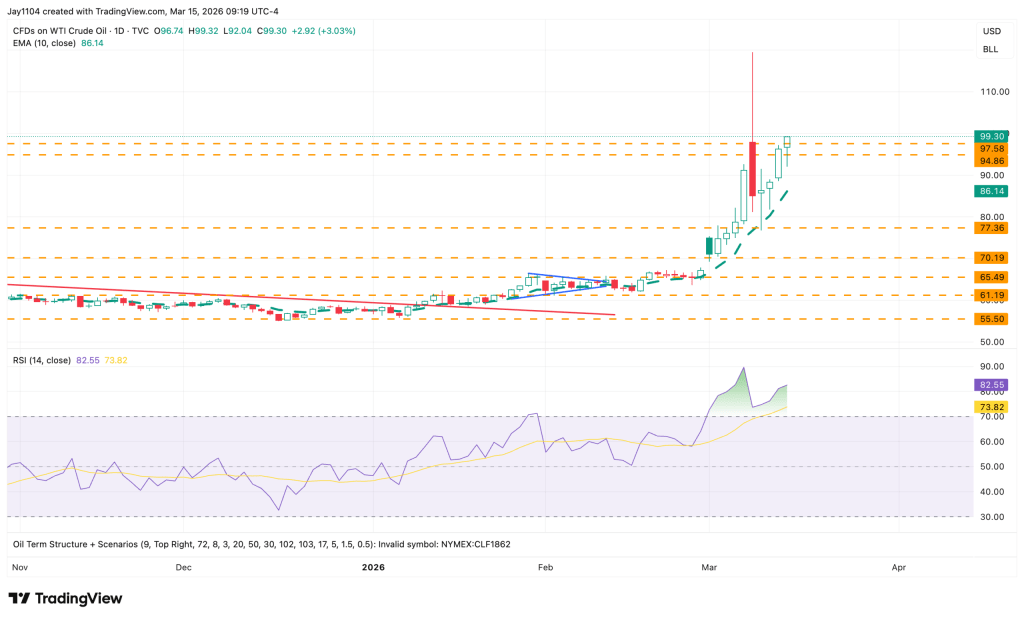

For investors trying to gauge the outlook for risk assets, the direction of oil prices has become increasingly important. However, predicting oil’s near-term path remains challenging. Weekend oil CFDs were trading about 3% higher and above $100 per barrel.

From a technical perspective, the trend remains upward for now, as long as oil continues to hold above its 10-day exponential moving average.

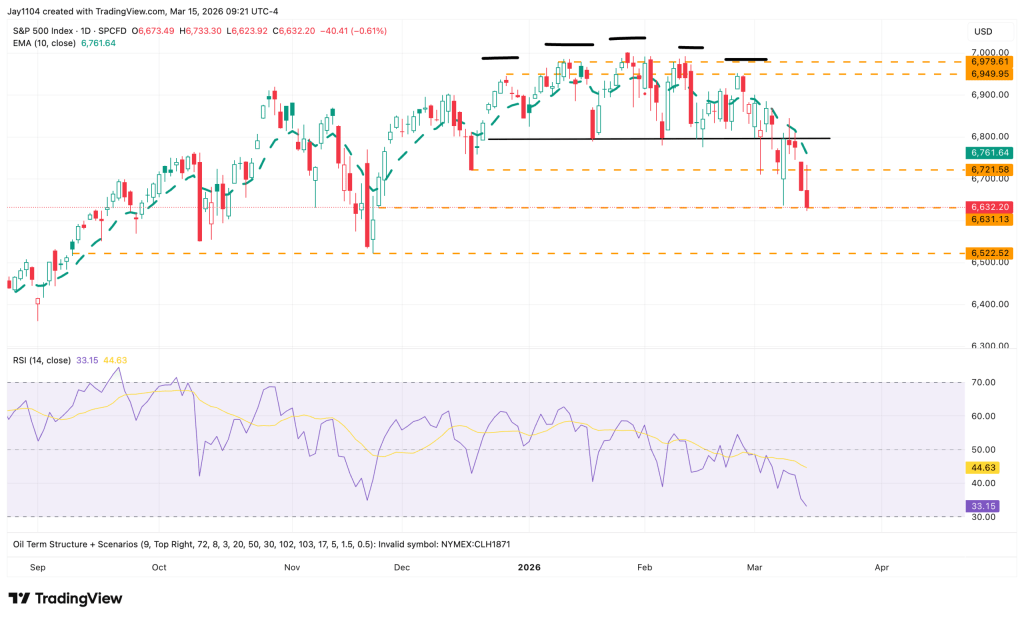

The situation is similar for the S&P 500—as long as the index stays below its 10-day exponential moving average, the short-term trend is likely to remain downward.

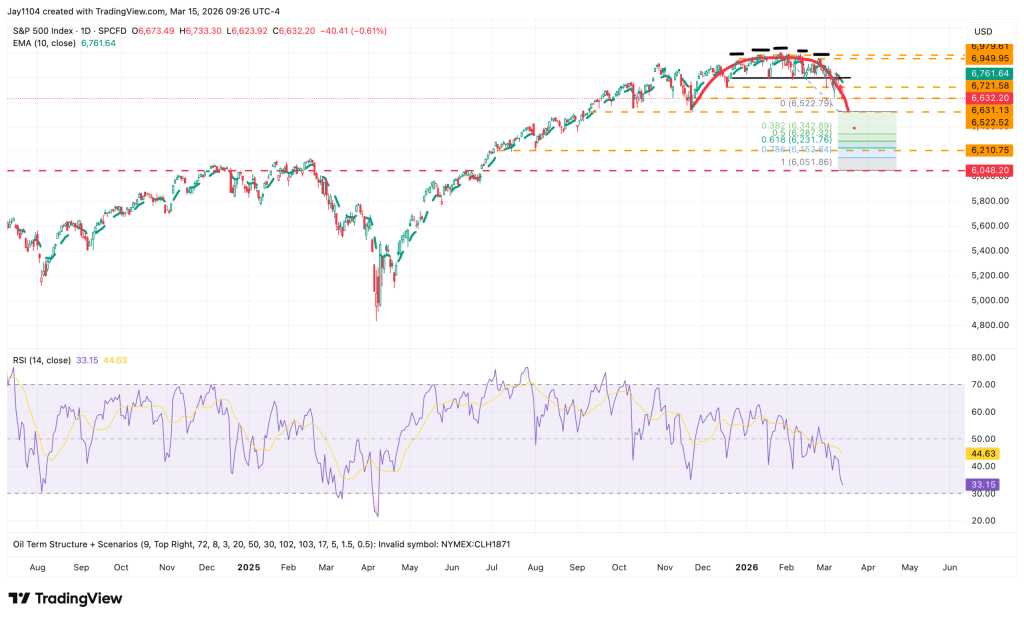

The distribution pattern in the S&P 500 appears relatively clear, with a key pivot level near 6,525, which coincides with the index’s November lows.

More significantly, measuring the decline from the recent high to this pivot level and projecting that move 100% lower points to a potential downside target near 6,050. Such a move would also fill the price gap from June 24 and allow the index to retest the breakout level from the pre-tariff highs, an area that could act as technical support.

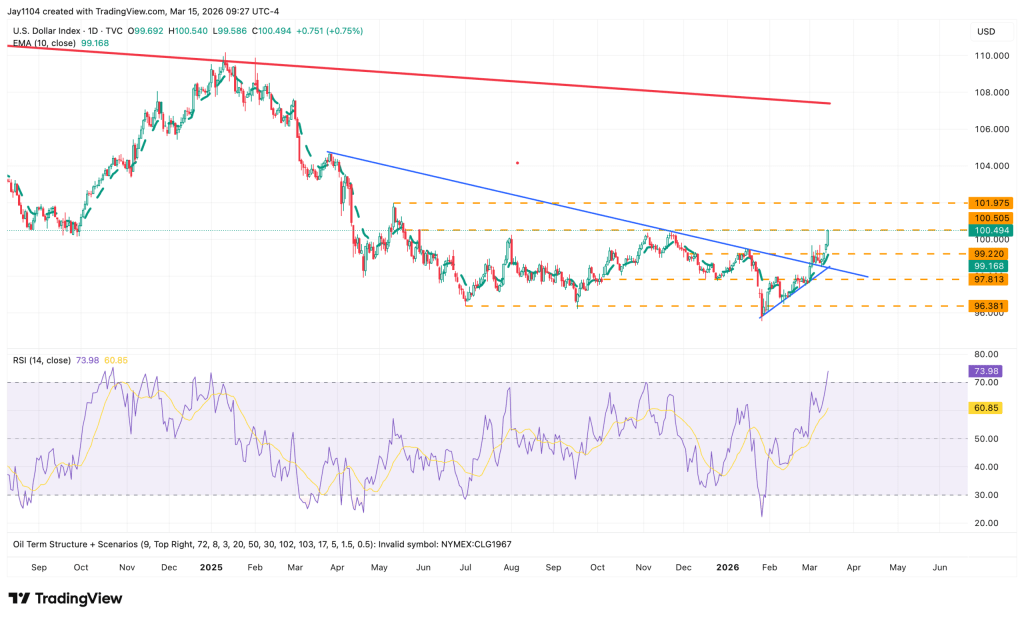

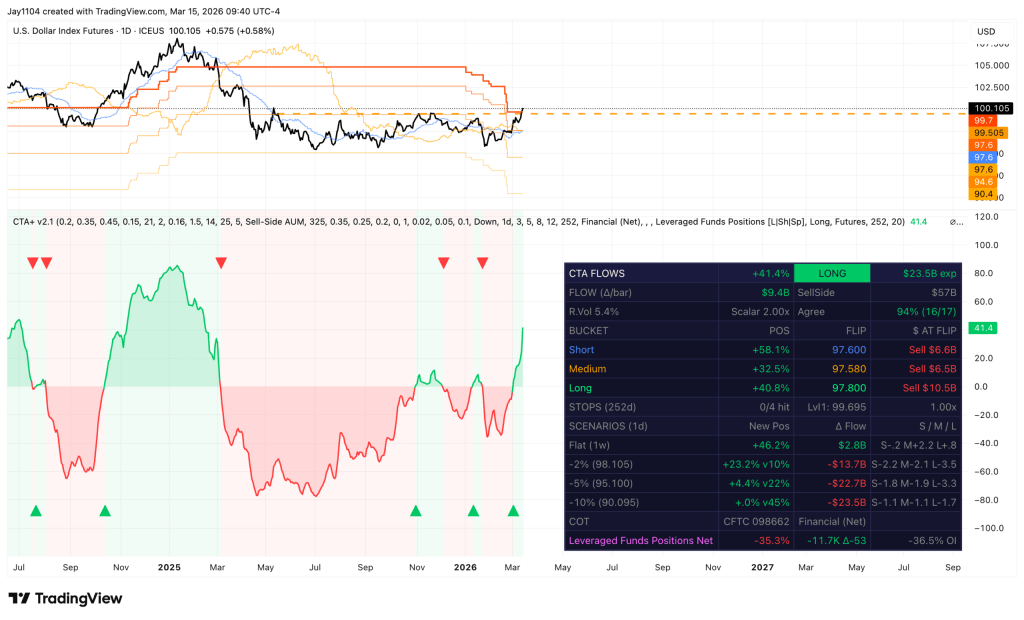

Such a scenario would likely require oil prices to stay elevated while interest rates and the U.S. dollar continue to strengthen. The U.S. Dollar Index could also extend its gains; a decisive break above 100.50 may open the door for a move toward 102.

With momentum indicators turning positive, it appears likely that CTAs and leveraged funds may start adding long dollar positions while reducing their existing shorts.

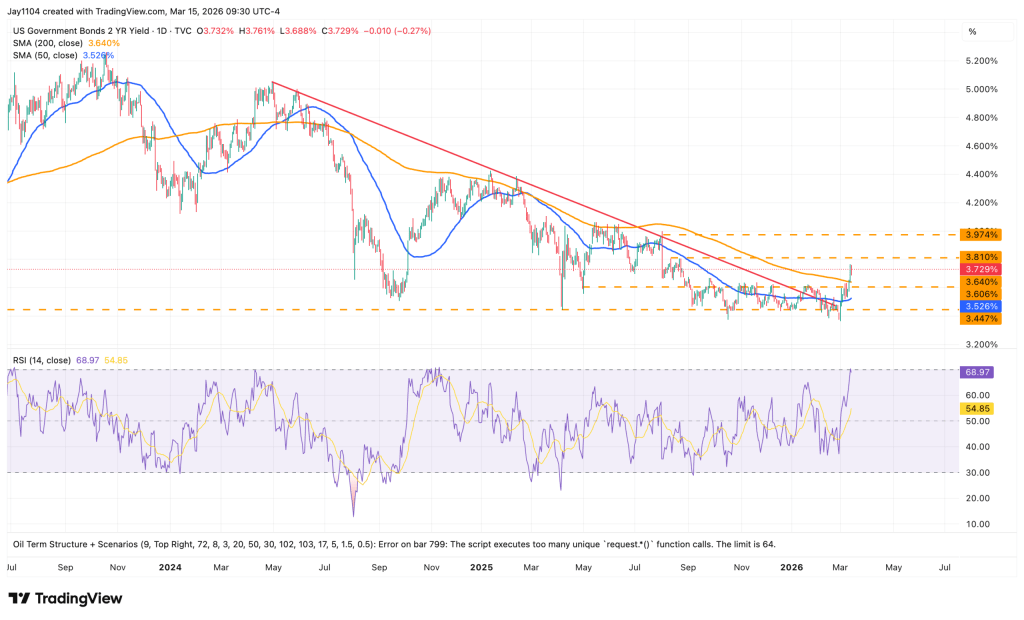

Meanwhile, the U.S. 2‑Year Treasury Yield may have room to extend higher, with the next resistance level seen near 3.80%, followed by a potential move toward 3.97%.

Technically, the outlook has strengthened as the yield has moved above its 200-day moving average, while the 50-day moving average is beginning to trend upward. In addition, the yield recently broke above a multi-year downtrend line that had been in place since April 2024, reinforcing the case for further upside momentum.

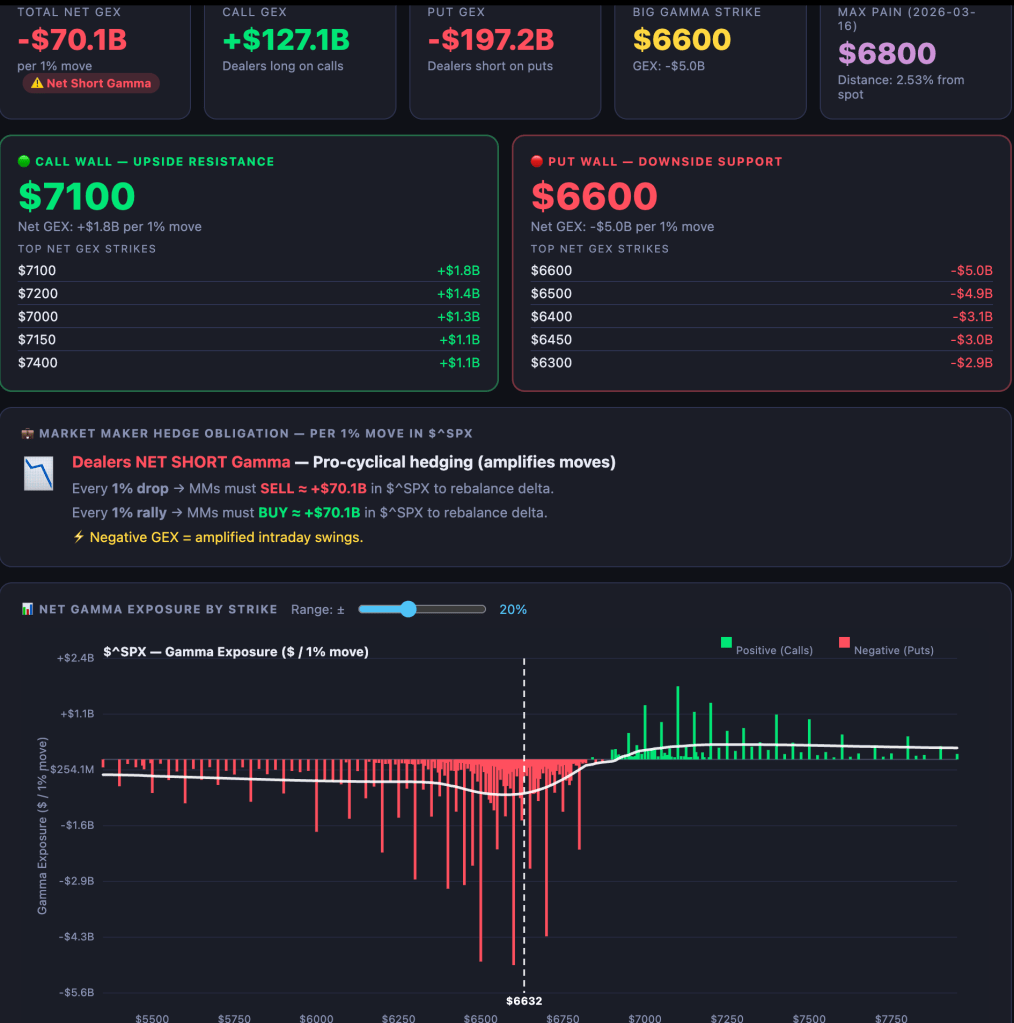

We’ll have to watch how the week develops. With options expiration (OPEX) taking place, market volatility could remain elevated. This is particularly true for the S&P 500, where put options currently dominate positioning, increasing the potential for sharp and erratic intraday price swings.

Sources: Michael Kramer

Leave a comment