Middle East tensions likely to delay Fed rate cuts

The conflict in the Middle East is expected to increase price pressures, while at the same time posing risks to U.S. economic growth and employment prospects. As a result, the situation is more likely to delay potential Federal Reserve rate cuts rather than eliminate them entirely. This differs from the situation in 2022, when a combination of demand and supply shocks sharply accelerated inflation and forced the central bank to raise interest rates.

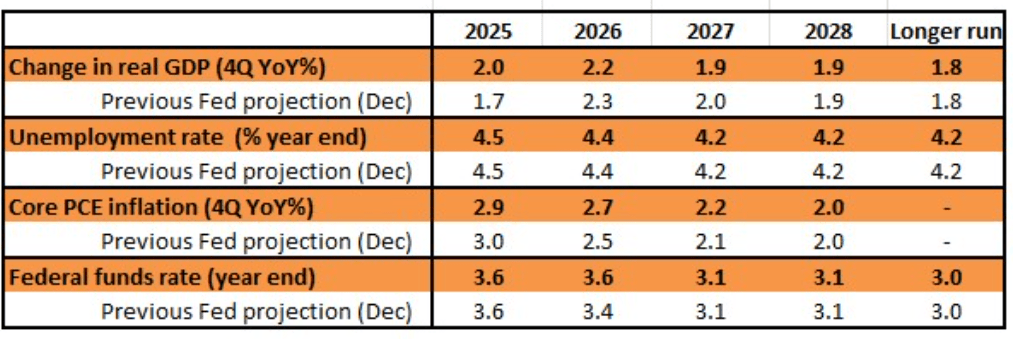

Rising inflation limits the Fed’s flexibility

Recent developments in the Middle East have significantly altered expectations for monetary policy at the Federal Reserve. Financial markets had previously anticipated two 25-basis-point rate cuts this year, but pricing has now shifted to reflect barely one cut.

Investors are also overwhelmingly expecting the Federal Open Market Committee to leave interest rates unchanged at its meeting on March 18, a view we also support.

Military activity in Iran and heightened risks to shipping through the Strait of Hormuz have driven a sharp rise in energy prices. Although the United States imports relatively little crude oil from the Persian Gulf and remains self-sufficient in natural gas, global oil pricing means domestic consumers still feel the impact.

Retail gasoline prices in the U.S. have already climbed above $3.60 per gallon, with the national average potentially approaching $4.25 per gallon in the near term. Higher fuel costs are expected to raise transportation and distribution expenses, while airline ticket prices could also increase.

If the disruption persists, price pressures may extend into other sectors such as fertilizers, food products, and plastics. As a result, inflation could rise toward 3.5% by the summer, remaining well above the Fed’s 2% target.

Growth and employment outlook uncertain

The implications for economic growth and employment remain less certain. February’s ISM business surveys suggested activity levels consistent with roughly 3% GDP growth. However, the labor market data paints a less optimistic picture.

The February employment report showed the economy lost 92,000 jobs, while the unemployment rate rose to 4.4%. This suggests the Fed may have been premature in removing its earlier assessment that “downside risks to employment rose in recent months” from the January FOMC statement.

Increasing geopolitical and economic uncertainty is unlikely to support stronger job creation and may dampen economic activity outside the U.S. energy sector.

Fed expected to signal a delay in rate cuts

Against this backdrop, attention will turn to the updated economic projections from the Federal Reserve. In its December outlook, the Fed had anticipated one interest-rate cut in 2026, followed by an additional 25-basis-point reduction in 2027.

However, the ongoing conflict and the uncertainty surrounding its duration and severity make the outlook highly unpredictable. As a result, policymakers are likely to have limited confidence in their forecasts.

At the press conference, Fed Chair Jerome Powell is expected to emphasize the difficulty of setting monetary policy amid such geopolitical and economic uncertainty.

Even so, the Fed may modestly downgrade its growth projections, raise its inflation forecasts, and ultimately push back the previously expected 2026 rate cut to 2027.

Risks still tilted toward lower interest rates

We have been projecting two interest-rate cuts in September and December, although—like financial markets—we acknowledge the possibility that these reductions could be pushed into next year. While the Federal Reserve operates under a dual mandate of maintaining price stability and promoting maximum employment, safeguarding its credibility on inflation remains crucial. Cutting rates becomes difficult to justify when inflation is already above target and appears to be moving further away from it.

In early 2022, the Fed initially argued that inflation would prove temporary because it was largely driven by supply disruptions, suggesting there was no immediate need to raise rates. However, strong job creation, rapid wage growth, pent-up consumer demand following pandemic lockdowns, and stimulus payments fueled a surge in spending. Inflation subsequently accelerated far more than expected.

As a result, the central bank was forced to respond aggressively, lifting interest rates by 525 basis points between March 2022 and July 2023 in an effort to regain control over rising prices.

Currently, the U.S. labour market appears significantly weaker, with both job creation and real household disposable income showing little growth over the past six months. At the same time, consumer confidence has been weighed down by concerns over tariffs and job security, reducing the likelihood of a strong demand surge that could push inflation higher. This environment suggests that inflationary pressures may indeed prove temporary this time.

Instead, the current energy shock may ultimately dampen demand, which would help ease core inflation over time. A correction in equity markets could amplify this demand destruction further. For this reason, we continue to expect a downward bias in Federal Reserve policy rates over the next 12–18 months.

Although tax refunds this year are expected to be relatively large—averaging around $4,000 compared with $3,200 last year—a much stronger fiscal stimulus would likely be required to generate enough demand to entrench inflation. Measures such as widespread stimulus checks would probably be necessary to produce sustained price pressures that might force the Fed to raise interest rates again.

However, such a scenario could unsettle bond markets due to concerns about rising government debt and renewed inflation risks. This, in turn, could trigger fears of 1970s-style inflation dynamics, a period marked by persistent inflation and financial market volatility. For now, we view that outcome as relatively unlikely.

Should the Fed Address the Persistent Stickiness in the Effective Funds Rate?

Since the Federal Reserve resumed purchasing Treasury bills in mid-December 2025, it has accumulated about US$165 billion in T-bill holdings. Overall, the Fed’s total securities portfolio—including bills—has increased by US$130 billion, bringing the balance sheet to roughly US$6.26 trillion. At the same time, bank reserves have risen by around US$180 billion to slightly above US$3 trillion, partly supported by a moderate drawdown in the Treasury’s cash balance.

Despite this US$130 billion expansion of the balance sheet, the Fed may find it frustrating that the effective federal funds rate has not declined, even marginally. Historically, the effective rate traded roughly 8 basis points above the policy floor, but it climbed to about 14 basis points in September and October 2025—one of the factors that prompted the renewed T-bill purchase program.

The underlying issue emerged when bank reserves slipped below US$3 trillion, causing conditions in the repo market to tighten noticeably. That tightening, from a relative-value perspective, helped push the effective funds rate higher. While the broader policy narrative has been dominated by rate cuts, the real concern is the effective funds rate drifting upward within the 25-basis-point target range.

For now, the effective funds rate remains stuck at 3.64%, just 1 basis point below the interest rate on reserve balances (3.65%). Moving up to 3.65% would be difficult because eligible counterparties can choose between holding reserves or lending in the federal funds market, though the rate should not exceed that level. Whether the Fed will address this issue publicly remains uncertain, although it arguably warrants attention from reporters, given that efficient market functioning is particularly important in the current environment.

Looking more broadly at interest rates—especially the outlook for bonds—the Fed is facing signals of higher nominal yields, rising real yields, and widening inflation breakevens. This mix does little to support further rate cuts. In fact, each element points toward the logic of maintaining current policy settings. For the time being, the market is likely to see more of the same, with 10-year Treasury yields potentially moving into the 4.3%–4.5% range before real yields eventually begin to decline again.

Fed Caution Should Continue to Support the Dollar

Like the rest of the world, the United States has seen a hawkish re-pricing of short-term interest rate expectations as the Middle East energy shock reduces the likelihood of near-term monetary easing. Although the shift in US rates has been smaller than in many other regions, it has done little to weaken the dollar. At the moment, the macro impact of rising energy prices is the dominant force shaping currency markets, while traditional drivers such as rate differentials have temporarily taken a back seat.

This suggests that even a mildly hawkish Federal Open Market Committee meeting on Wednesday—where the Fed could push the projected 25-basis-point rate cut from 2026 to 2027—may not provoke a dramatic reaction in the dollar. Still, if policymakers emphasize the inflation risks posed by higher energy prices while the US labor market remains resilient, it would likely provide modest support for the currency. In fact, the market’s reassessment of the Fed’s policy path has amplified the energy shock confronting Europe, Asia, and many emerging economies, undermining earlier expectations of a gradual dollar decline this year.

As long as energy prices remain elevated—or climb further—it will be difficult for the dollar to surrender the gains it has made this month. One potential source of increased dollar supply could come from official intervention, particularly if Japan steps in to curb USD/JPY should the pair rise beyond 160. A coordinated intervention by the United States and Japan to sell dollars would be unexpected and could trigger a broader correction in the currency. However, unless energy prices retreat meaningfully, any intervention would likely serve only to limit volatility rather than reverse the dollar’s broader strength.

Sources: James Knightley

Leave a comment