Before the attack began on Feb. 28, lingering inflation concerns had already made the Federal Reserve cautious about continuing the interest rate cuts introduced last year. While several indicators of price pressure had eased compared with earlier highs, policymakers were reluctant to declare victory over inflation, which had peaked at 9.0% year over year in the Consumer Price Index in June 2022.

Since then, inflation has fallen sharply and stabilized around the mid-2% range, slightly above the Fed’s 2% target. However, the cautious optimism that accompanied this disinflation may quickly fade because of the war.

The main concern is that surging energy prices could reignite inflation and force the central bank to keep monetary policy tighter for longer. With oil, gasoline, and natural gas prices rising sharply, it remains unclear how persistent the shock will be—or how the Fed should respond. This uncertainty creates a policy gray area that may take time to resolve. The longer the conflict lasts, the more uncertain the outlook for monetary policy becomes.

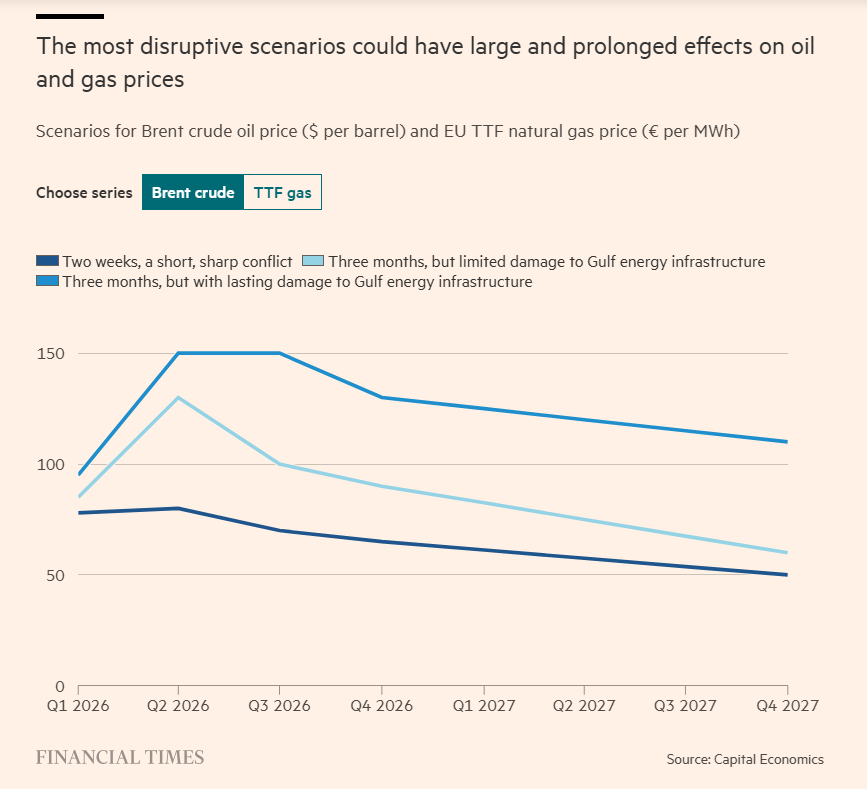

Two key questions dominate the discussion: When will the war end, and what economic consequences will follow? For now, the answers remain highly speculative. Much of the analysis focuses on the recovery of oil exports through the Strait of Hormuz, which remains largely closed due to the conflict and normally handles about one-fifth of the world’s seaborne oil exports.

The basic calculation is straightforward: the longer shipments remain disrupted, the greater the hit to global supply, which could sustain upward pressure on energy prices. According to estimates from Capital Economics, cited by the Financial Times, prolonged export disruptions would likely extend the period of elevated oil prices and complicate the inflation outlook.

The challenge for the Federal Reserve is determining which scenario is most likely and calibrating monetary policy accordingly. With no clear end to the war in sight, the near-term outlook for energy prices—and their implications for inflation and economic growth—remains highly uncertain.

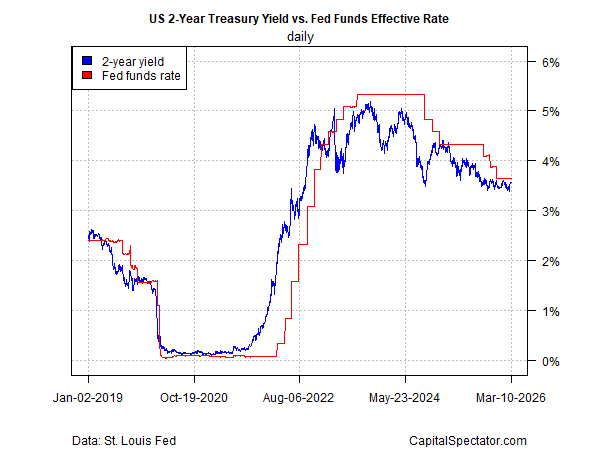

Financial markets are also struggling to assess the range of possible outcomes and are largely adopting a wait-and-see stance. One signal of this caution can be seen in the U.S. 2‑Year Treasury Yield, which is widely viewed as a proxy for expectations about Fed policy. In recent days, the yield has hovered close to the Effective Federal Funds Rate, suggesting investors broadly expect the central bank to keep interest rates steady in the near term.

Fed funds futures point to a similar outlook, indicating that markets expect the Federal Reserve to keep interest rates unchanged over the next three policy meetings. Current pricing suggests the first potential rate cut could come in July or September, although those expectations remain tentative given the high level of uncertainty surrounding the war’s impact on growth and inflation.

“The Fed always has a problem in deciding how to respond to a supply shock,” said Alan Detmeister, a former Fed economist now at UBS. “On the one hand, the inflationary effects argue for raising interest rates. On the other, weaker output and rising unemployment point toward lowering rates. It’s not clear-cut, which often leads the Fed to wait and see which side of its dual mandate—inflation or employment—requires the most support.”

Ultimately, even if a ceasefire eventually stabilizes the region, the economic aftershocks could persist. As a result, the Fed’s policy outlook is likely to remain uncertain for some time, with policymakers needing clearer signals on how the conflict will shape inflation and economic growth.

Sources: James Picerno

Leave a comment