The United States has built up its most significant military footprint in the Middle East since 2003, deploying two aircraft carriers and F-22 stealth fighters. Indirect negotiations in Geneva between US envoys Steve Witkoff and Jared Kushner and Iranian officials concluded Thursday without progress. The Trump administration has cautioned that Iran will face “drastic consequences” if it fails to agree to meaningful nuclear concessions.

Israel has activated bomb shelters and warned Lebanon that its infrastructure could be targeted if Hezbollah becomes involved in any US–Iran confrontation. The US State Department authorized the departure of non-essential personnel and family members from the US Embassy in Israel on February 27, following similar instructions for the embassy in Beirut issued on February 23. Meanwhile, reports suggest the US 5th Fleet in Bahrain has been scaled back to fewer than 100 essential personnel.

China has urged its citizens to leave Iran immediately. South Korea escalated its advisory to a “Level 3” red alert, instructing nationals to depart. Australia has offered voluntary departure to diplomatic dependents in the UAE, Qatar, and Jordan, citing a worsening security environment. Several European countries, including Finland, Sweden, and Serbia, have also recommended that their citizens evacuate Iran.

Commercial carriers such as KLM have begun suspending regional flights. Governments are encouraging citizens to exit while commercial routes remain available, warning that air corridors could close quickly if hostilities erupt.

Does this mean a US–Israel strike on Iran is imminent? Possibly—but diplomatic channels remain active. The State Department confirmed that Secretary of State Marco Rubio will travel to Israel early next week. Meanwhile, reports indicate that Omani Foreign Minister Badr Al Busaidi is set to meet Vice President JD Vance and other US officials in Washington in previously undisclosed talks aimed at preventing escalation.

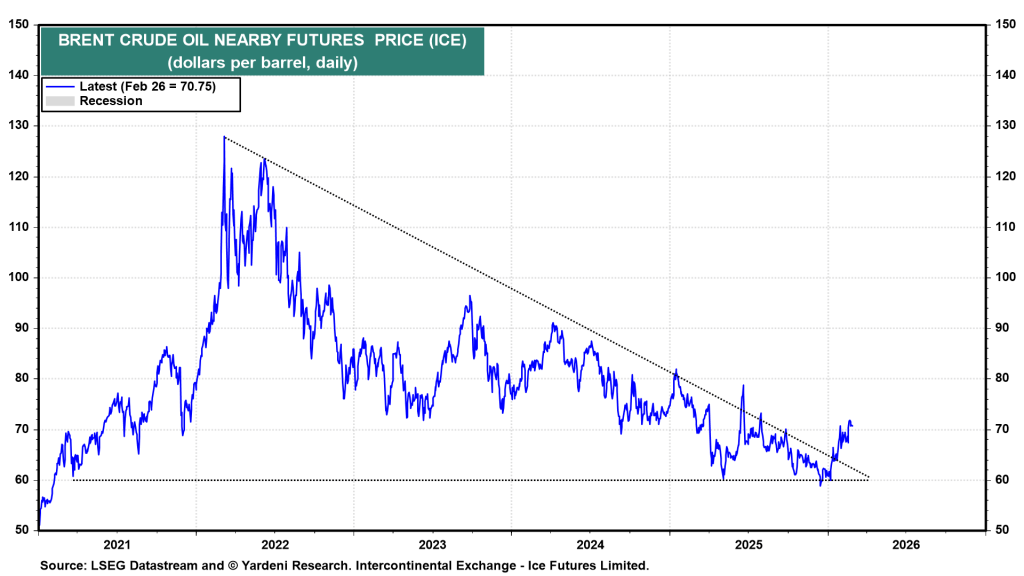

Oil markets are ending February on firm footing, with prices rising about $1 per barrel during the final trading week as tensions intensify. This week’s indirect talks in Geneva produced no tangible outcome, and Trump’s 10–15 day deadline is fast approaching. At the same time, attention to the upcoming OPEC+ summit has been muted—potentially opening the door for Saudi Arabia to surprise markets with another production increase for April.

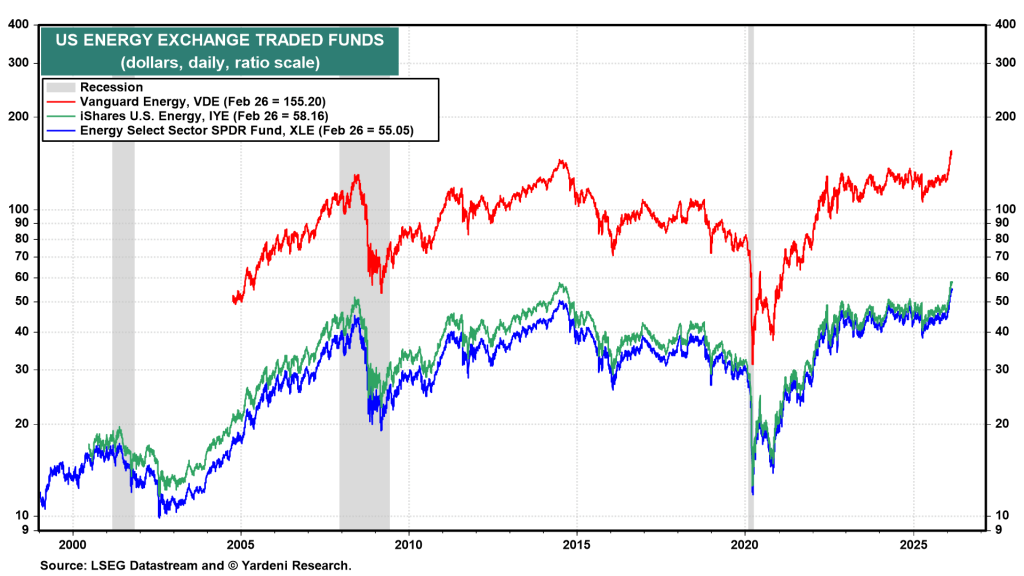

The recovery in oil prices, combined with a reshuffling of global equity allocations, has recently delivered a notable lift to US energy ETFs (see chart). However, today’s modest $1.50 rise in crude suggests markets may have already priced in the risk of a swift conflict—or remain unconvinced that one is imminent.

Saudi Arabia could still opt to raise output, but much of that additional supply would need to transit the Strait of Hormuz, a critical chokepoint that Iran has repeatedly threatened to shut down.

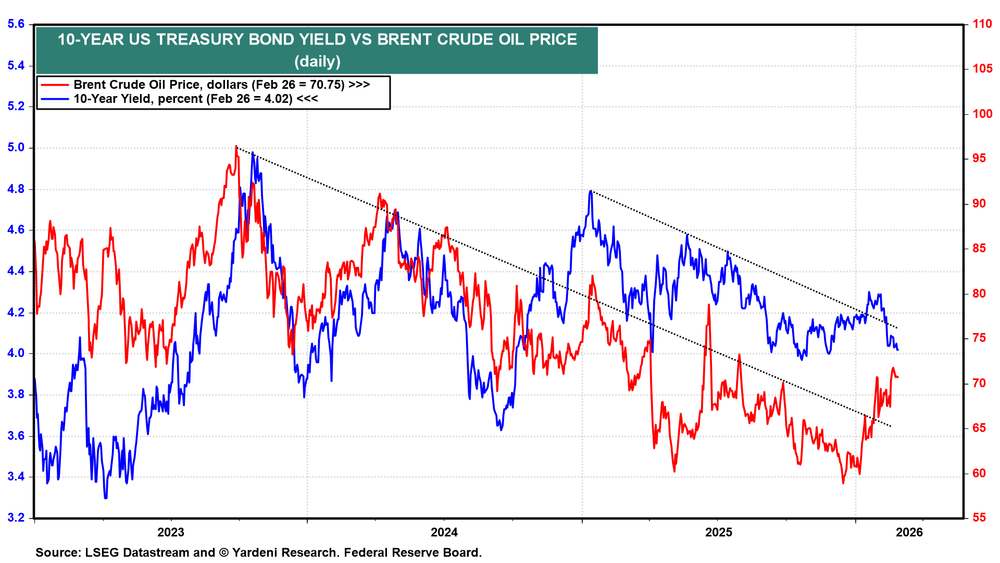

Between 2023 and 2025, the 10-year US Treasury yield moved largely in tandem with the price of Brent crude (see chart), reflecting a strong correlation between energy prices and long-term interest rates.

In recent weeks, however, that relationship has diverged. While oil prices have climbed, the 10-year yield has declined. This shift suggests that investors may be rotating into bonds as a safe haven, anticipating that a renewed conflict in the Middle East could trigger broader geopolitical instability and economic uncertainty.

It was notable that the 10-year yield slipped below 4.00% today, even after a stronger-than-expected PPI inflation print.

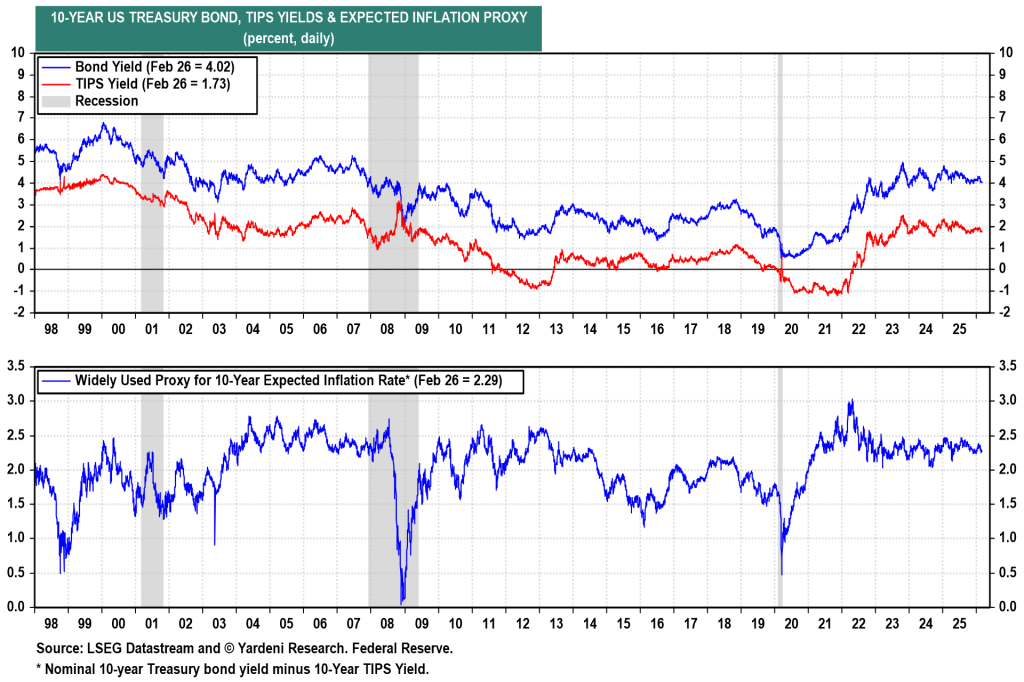

More broadly, both nominal and real 10-year yields have traded within a relatively narrow range since 2023 (see chart). In our view, that sideways pattern is likely to persist through the remainder of the year.

Sources: Ed Yardeni

Leave a comment