The purpose here isn’t to make a forecast, but to stay open-minded about money as both a social construct and a carrier of utility value.

The prevailing view argues that the US dollar is destined to collapse, steadily declining toward worthlessness. According to this narrative, the United States will keep creating new dollars to sustain the illusion of stability, until excessive money printing ignites hyperinflation and erodes what little value the dollar has left.

This outlook draws heavily from historical episodes such as the Weimar Republic, where large-scale money creation ultimately destroyed the currency. It’s possible the dollar could follow a similar path.

But money behaves in complex ways. Because it is fundamentally a social agreement, its potential outcomes are broader than we often assume. So instead of assuming collapse, let’s imagine a case for continued dollar dominance.

Consider two hypothetical types of money. The first is a globally recognized currency backed by a basket of industrial commodities—metals like silver and copper, fuels like oil, and other tangible resources. Its value stems not from scarcity alone but from the practical utility of the assets supporting it. Since it is tied to a physical reserve, new units can only be issued if that reserve grows. It cannot be created through lending by banks.

The second type of currency expires after a set period and must be spent before it loses all value. This resembles “scrip” money. Together, these two examples illustrate money’s dual role: a store of value and a medium of exchange.

Naturally, we would save the first form for long-term security—its value rests on enduring real-world utility. The expiring currency, by contrast, would be spent quickly on goods and services.

Now consider another scenario: traveling abroad and collecting small amounts of foreign cash. Each note is valuable within its home country but useless elsewhere until exchanged. The same logic applies to precious metals. If you try to pay for a bowl of noodles with silver, the vendor must convert it into local currency, incurring transaction costs. And if taxes are owed, the government will not accept silver—only its own currency.

This highlights a frequently misunderstood aspect of fiat money. It isn’t “backed by nothing.” Its value lies in granting access to participate fully in the issuing country’s economy.

If that seems abstract, think of a work or residency permit. Without it, economic participation is limited and costly. With it, participation becomes smoother, safer, and more efficient. Currency functions similarly.

Now ask yourself: which currency would most likely be accepted almost anywhere in the world—from a remote market to a major city?

A crisp $100 US bill would probably be welcomed in more places than most alternatives. This isn’t because the paper itself has special intrinsic value. It reflects the network effect: what is already widely recognized and used carries greater practical utility than lesser-known options.

No single form of money perfectly combines store of value, ease of exchange, universal acceptance, and low friction. Searching for one flawless form is probably futile. Instead, currencies that provide:

- Access to the largest economic sphere,

- The strongest network effect and recognition, and

- Reliable price discovery with relatively stable value

That will tend to have higher utility and lower transaction costs than competing alternatives.

Demand for a currency arises from multiple sources: the desire to preserve value, the need to transact, and the appeal of participating in the broadest economic network.

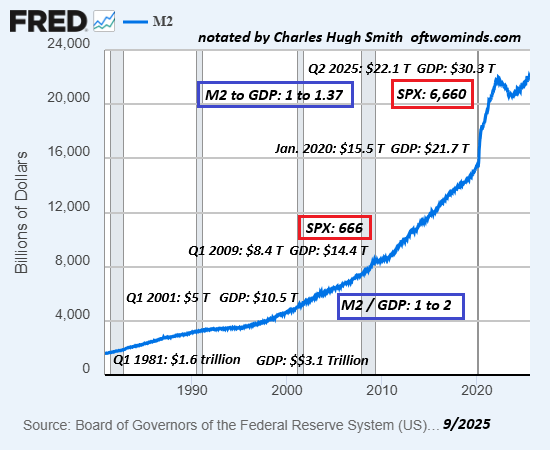

State-issued money has another distinctive trait: its supply can expand or contract. If supply grows more slowly than demand, purchasing power can rise—just as with any other commodity.

Supply is easier to measure than demand, which reflects the collective decisions of millions seeking safety, liquidity, efficiency, and opportunity.

The argument for continued US dollar dominance rests on its imperfect but still advantageous blend of features: relatively transparent pricing, low-friction transactions, powerful global network effects, and access to the world’s largest economic system.

These strengths are not merely products of short-term central bank policies. They reflect the broader framework of governance, institutions, economic depth, social trust, and cultural influence behind the issuing state.

If global uncertainty increases, demand for such a currency could outpace supply. As demand rises and network effects strengthen, a self-reinforcing cycle may emerge—supporting, rather than undermining, the dollar’s supremacy.

Money behaves in peculiar ways. We often assume we fully understand it, and even when we’re convinced a currency is about to collapse, it somehow endures—and sometimes even outperforms expectations.

The goal here isn’t to make a prediction. Rather, it’s to remain open-minded about currency as both a social construct and a vessel of utility value.

Sources: Charles

Leave a comment