- U.S. PPI inflation data and Nvidia’s earnings will take center stage in the coming week.

- Nvidia appears set to post another standout quarter.

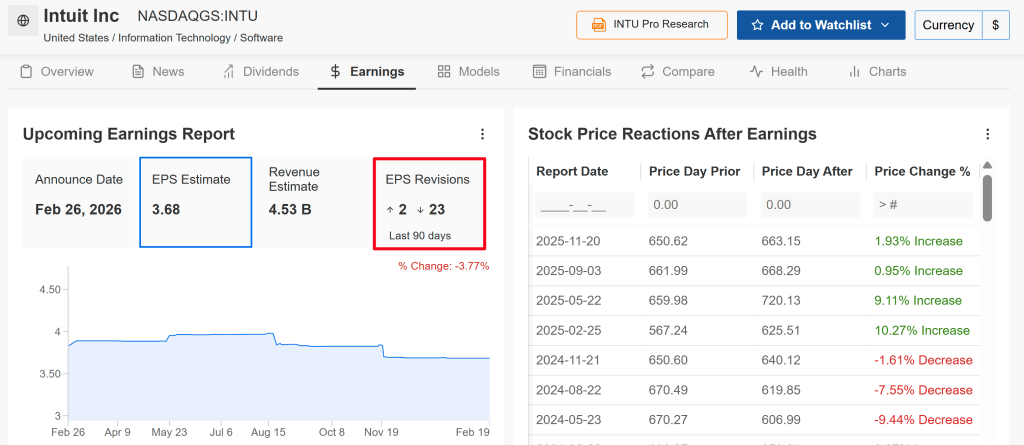

- Meanwhile, Intuit is confronting mounting fundamental and technical pressures ahead of its results.

U.S. equities closed higher on Friday after the Supreme Court invalidated President Donald Trump’s tariffs. Trump criticized the decision as a “disgrace” and said in a Truth Social post on Saturday that he would introduce a new 15% global tariff, just one day after announcing a 10% levy.

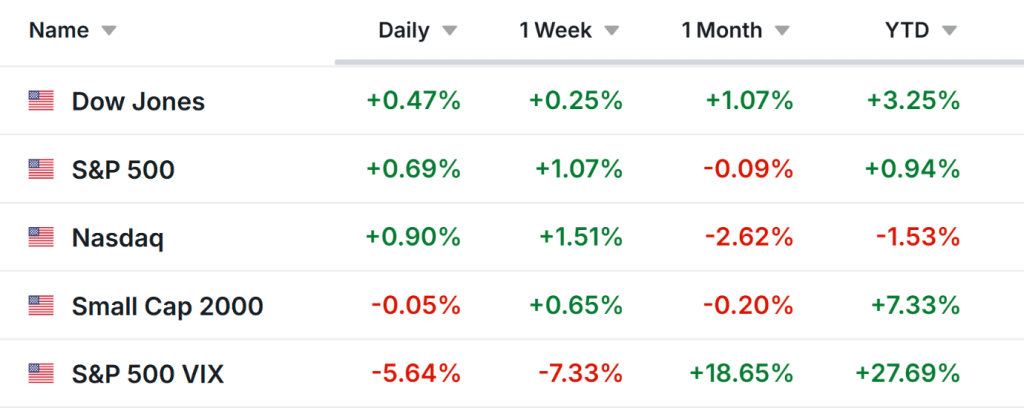

After Friday’s gains, the 30-stock Dow Jones Industrial Average finished the week up about 0.3%. The S&P 500 advanced 1.1%, while the tech-heavy Nasdaq Composite broke a five-week slide with a 1.5% surge. The small-cap Russell 2000 added nearly 0.7%.

Markets may see heightened swings in the days ahead as investors weigh prospects for growth, inflation, interest rates, and corporate earnings against a backdrop of renewed trade frictions.

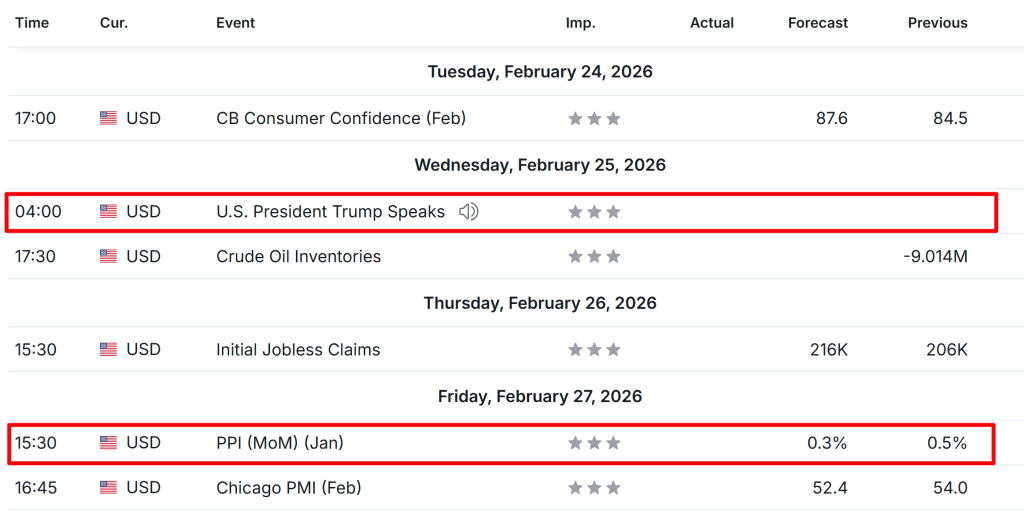

With a relatively light economic calendar, attention will center on Friday’s January U.S. producer price index report. As of Sunday morning, traders are pricing in slightly better than even odds that the Federal Reserve will lower rates by its June meeting.

On the earnings front, Nvidia’s (NASDAQ: NVDA) report will headline the week as the season winds down. Beyond Nvidia, investors will be tracking several major tech names, particularly software companies facing pressure from concerns that AI could disrupt their core businesses, including Salesforce (NYSE: CRM), Intuit (NASDAQ: INTU), Snowflake (NYSE: SNOW), Zscaler (NASDAQ: ZS), and Zoom Video Communications (NASDAQ: ZM).

AI infrastructure providers Dell Technologies (NYSE: DELL) and CoreWeave (NASDAQ: CRWV) are also set to post results. Outside the tech space, prominent retailers such as Home Depot (NYSE: HD), Lowe’s Companies (NYSE: LOW), and TJX Companies (NYSE: TJX) are scheduled to report.

At the same time, markets will be parsing President Trump’s State of the Union address on Tuesday and monitoring any developments involving the U.S. and Iran.

No matter which way markets move, below I outline one stock that could attract buying interest and another that may face renewed downside pressure. Keep in mind, this outlook covers only the week ahead—Monday, February 23 through Friday, February 27.

Stock to Buy: Nvidia

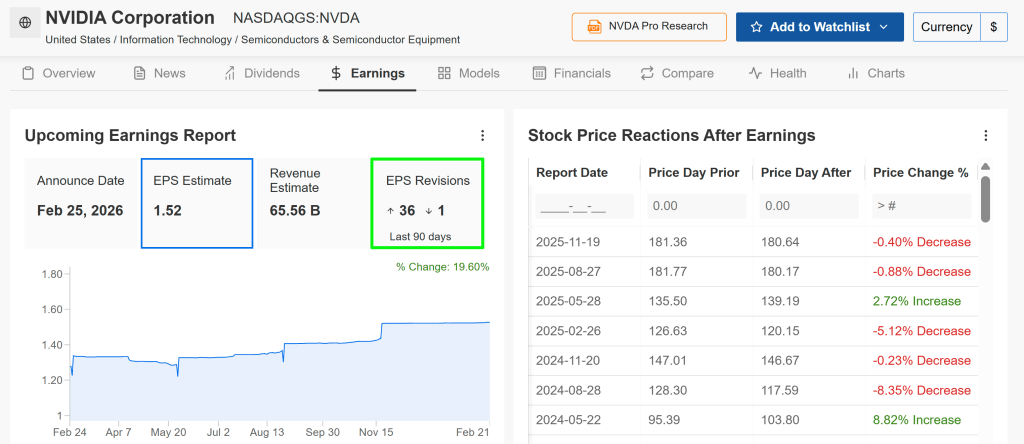

Nvidia heads into its earnings report with analysts anticipating another “beat-and-raise” performance, fueled by robust demand for AI infrastructure. Fourth-quarter results are scheduled for release after Wednesday’s market close at 4:20 p.m. ET, followed by a 5:00 p.m. ET conference call with CEO Jensen Huang.

According to an InvestingPro survey, profit forecasts have been lifted 36 times in recent weeks, compared with just one downward revision—highlighting growing optimism around Nvidia’s earnings outlook. In the options market, traders are pricing in a potential move of roughly ±6% in NVDA shares following the announcement.

Wall Street expects the AI powerhouse to deliver earnings of $1.52 per share, up 71% from a year earlier. Revenue is forecast to climb 67% to $65.6 billion, underscoring the company’s ongoing strength in the AI chip space.

Citi recently suggested that January-quarter revenue could exceed $67 billion, with projections pointing to even stronger results in the April quarter.

Another solid showing in data-center sales, along with widening margins and healthy free cash flow, would bolster the view that Nvidia remains firmly in the midst—not at the tail end—of an AI supercycle.

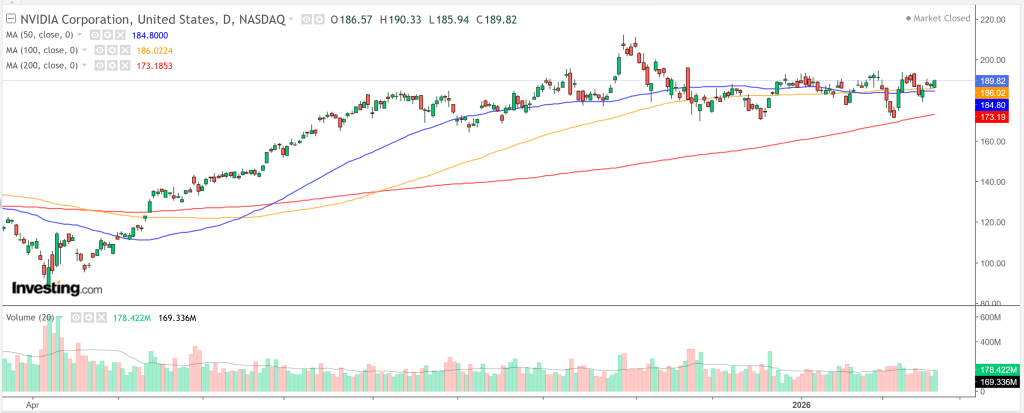

NVDA shares ended Friday at $189.82, consolidating after a strong advance but still positioned to move higher on favorable catalysts. Across multiple timeframes—from intraday charts to the monthly view—technical indicators and moving averages continue to signal a “strong buy.”

A beat-and-raise report could ignite another leg up, particularly if management emphasizes longer-term visibility into 2026–2027 growth driven by next-generation architectures such as Rubin.

Trade Setup:

- Entry: Near current levels (around $190)

- Target: $210 (approximately 10% upside)

- Stop-Loss: $184 (roughly 3.5% downside risk)

Stock to Sell: Intuit

Intuit—the parent company of TurboTax, QuickBooks, Credit Karma, and Mailchimp—heads into earnings week facing mounting pressure. Concerns have escalated in early 2026 that generative AI tools could weaken its competitive moat across tax prep, accounting, and financial software by enabling free or lower-cost alternatives, custom AI agents, or in-house solutions for small businesses and consumers.

This anxiety has fueled broader “SaaSpocalypse” sentiment, with the software sector shedding trillions in market value. INTU shares have been particularly hard hit in recent months, sliding sharply alongside peers such as Salesforce.

Analyst sentiment has also turned more cautious ahead of the report, with 23 of the last 25 estimate revisions moving lower—signaling growing skepticism around near-term performance.

Wall Street expects Intuit to post earnings of $3.68 per share, up roughly 11% year over year, on revenue of about $4.5 billion. The bigger concern, however, centers less on the headline numbers and more on the narrative surrounding AI-driven disruption.

Although Intuit has made significant investments in artificial intelligence, investors seem to view these efforts as largely defensive—designed to protect its existing franchises rather than meaningfully expand them or counter broader competitive threats. TD Cowen recently cut its price target, pointing to doubts about the strength of Intuit’s AI strategy and intensifying competition.

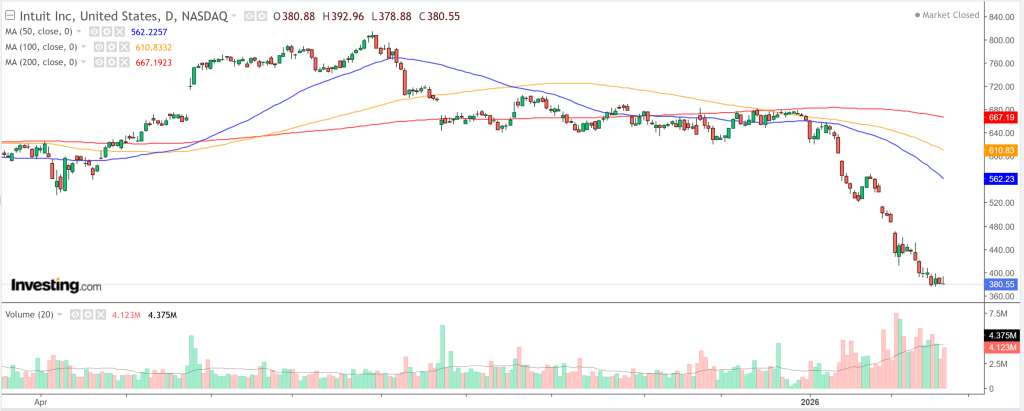

Any remarks about rising competitive pressures, decelerating growth in key segments, or conservative forward guidance could amplify downside risks—particularly in a stock that may be technically oversold but remains vulnerable in a sentiment-driven market.

Shares of Intuit have fallen 42.5% over the past three months and are now hovering just above their 52-week low of $375.40. Technical signals remain decisively negative: across timeframes—from hourly charts to the monthly view—both moving averages and momentum indicators continue to flash “strong sell.”

With management’s outlook likely to face intense scrutiny, any earnings miss or cautious commentary reflecting a more competitive, AI-driven environment could deepen the selloff.

Trade Setup:

- Entry: Near current levels (around $381)

- Target: $355 (approximately 7% downside)

- Stop-Loss: $400 (about 5% risk)

Sources: Jesse Cohen

Leave a comment