After a powerful rally in large-cap technology shares, investors are once again asking whether smart money is beginning to rotate.

With AI enthusiasm pushing tech valuations higher and energy names still trading at comparatively modest multiples, there are early signs that capital flows may be shifting beneath the surface. Here’s a closer look at the current landscape — and where institutional positioning may be headed.

The Case for Tech: Structural Growth Still Intact

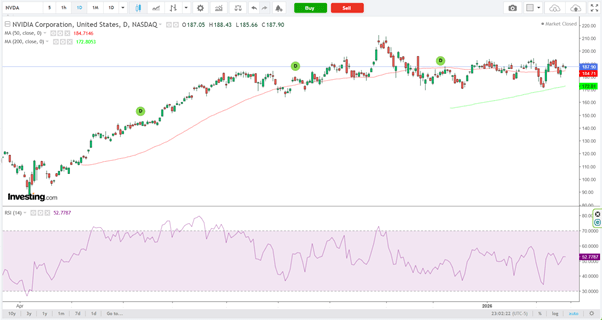

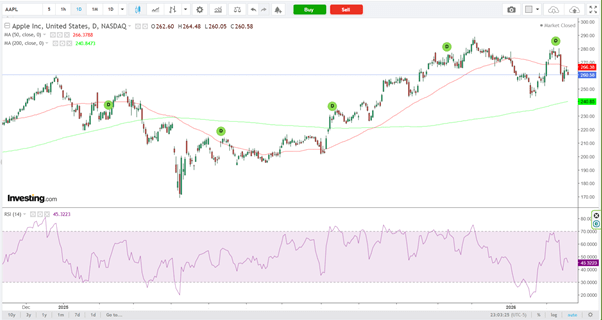

Companies such as Nvidia (NASDAQ: NVDA), Microsoft (NASDAQ: MSFT), and Apple (NASDAQ: AAPL) remain central pillars of institutional portfolios.

Technology continues to lead in earnings expansion, fueled by AI infrastructure investment, cloud migration, and ongoing software monetization.

Why capital is still favoring tech:

- Revenue growth outpacing the broader market

- High operating margins and robust free cash flow

- Sustained AI-driven capex cycles

- Strong balance sheets with significant liquidity

Mega-cap tech remains a structural core holding for institutional investors. Even during brief pullbacks, dip-buying has been persistent — a sign that long-term conviction in the sector remains strong.

That said, valuations in select segments have stretched beyond historical norms. If earnings momentum moderates, the probability of sector rotation increases, particularly as investors reassess risk-reward at elevated multiples.

The Case for Energy: Undervalued and Cash-Generative

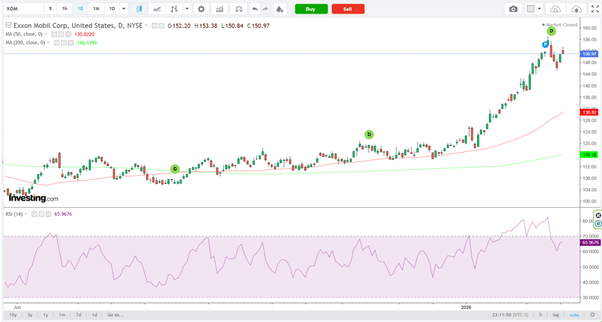

Integrated majors such as Exxon Mobil (NYSE: XOM) and Chevron (NYSE: CVX) are drawing renewed attention as investors reassess sector allocations.

Energy equities typically trade in cycles influenced by crude prices, global demand dynamics, and geopolitical developments. After extended periods of relative underperformance, the sector often becomes a magnet for value-oriented capital.

Why institutional money may rotate toward energy:

- Lower forward P/E multiples compared to technology

- Strong and visible free cash flow generation

- Dividend yields frequently above the broader market average

- Ongoing share repurchase programs

If crude prices remain stable or trend higher, integrated oil majors can produce substantial cash flows, offering a mix of income, capital return, and relative defensiveness.

In an environment where parts of the technology sector appear valuation-stretched, energy provides a compelling contrast on both multiples and yield.

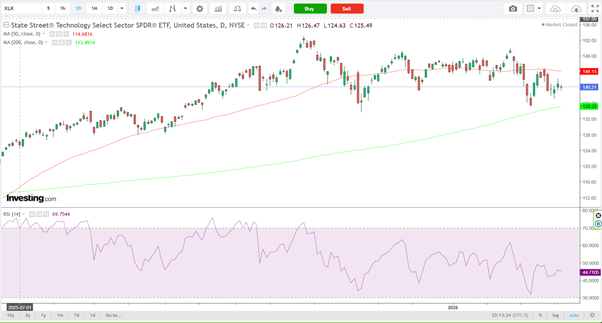

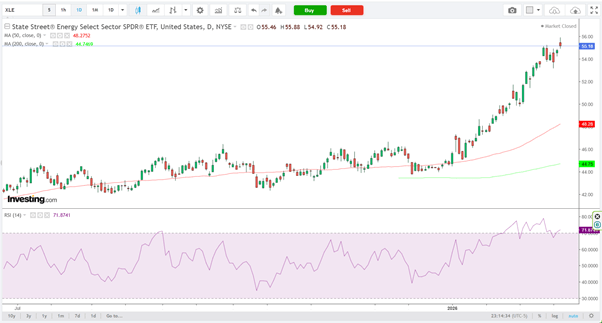

Sector ETF Signals: Tracking Institutional Flows

Sector ETFs can offer valuable insight into how institutional capital is rotating beneath the surface. Two key vehicles to monitor are the Technology Select Sector SPDR Fund (NYSE: XLK) and the Energy Select Sector SPDR Fund (NYSE: XLE).

ETF performance and fund flow data often act as real-time indicators of positioning shifts:

- If XLK continues to outperform, it suggests growth leadership remains firmly in place.

- If XLE begins to show sustained relative strength versus XLK, it may signal that rotation into energy is gaining traction.

Historically, sector leadership transitions tend to coincide with:

- Shifts in interest rate expectations

- Narrowing earnings growth differentials

- Sharp moves in commodity prices

Monitoring the relative strength ratio between XLE and XLK can provide early confirmation of whether capital is merely rebalancing tactically — or whether a broader structural rotation is unfolding.

Macro Forces Driving Sector Rotation

1. Interest Rates

Elevated yields tend to weigh more heavily on high-multiple technology stocks, as future cash flows are discounted at higher rates. In contrast, energy companies—often valued on nearer-term cash generation—can prove more resilient. If bond yields move higher, defensive value sectors may attract incremental capital at the expense of growth.

2. Commodity Prices

Oil prices remain a primary earnings driver for energy producers. A sustained rally in crude can rapidly alter sector performance dynamics, drawing capital into integrated majors and upstream names as profit expectations improve.

3. Earnings Revisions

Institutional allocation models closely track forward earnings revisions. If analyst upgrades begin to slow in technology while turning more constructive for energy, portfolio rebalancing flows may follow.

4. Risk Appetite

Technology typically outperforms in strong risk-on environments characterized by abundant liquidity and growth optimism. Energy, by contrast, can gain relative strength during inflationary phases or periods of geopolitical tension, when commodity exposure and cash yield become more attractive.

What Institutional Capital Is Likely Doing Now

Rather than making an outright “either/or” shift, institutional investors typically adjust exposure more subtly. That can mean trimming extended technology positions, selectively adding energy holdings, or rotating within sectors—such as moving from mega-cap AI leaders into second-tier beneficiaries of the theme.

The real driver is relative earnings momentum, not headlines.

Which Sector Offers More Upside?

Tech Upside Scenario

- Continued acceleration in AI-related spending

- Consistent earnings beats from mega-cap leaders

- Declining bond yields that support higher valuation multiples

Energy Upside Scenario

- Oil prices establish a sustained uptrend

- Inflation concerns re-emerge

- Technology valuations compress

In the near term, technology remains the structural growth narrative, supported by AI infrastructure, cloud expansion, and software monetization. However, energy presents potential asymmetric upside if commodity dynamics shift in its favor.

Sector rotation is rarely abrupt. More often, it unfolds gradually through portfolio rebalancing rather than wholesale liquidation.

While tech continues to dominate leadership, energy’s relative valuation discount and strong cash generation could attract incremental capital if macro conditions evolve.

Key indicators to monitor:

- Relative strength between the Energy Select Sector SPDR Fund and the Technology Select Sector SPDR Fund

- Forward earnings revisions

- Oil price trends

- Bond yield movements

The critical question is not whether rotation will occur — but whether it is already quietly underway beneath the surface.

Sources: Tafara Tsoka

Leave a comment