Last week, I attended the 2026 Harvard Presidents’ Seminar with leading executives and thinkers, where Ambassador Kevin Rudd, former Australian prime minister, stood out. He warned that the post–World War II rules-based global order is likely fading, giving way to a more 19th-century style world defined by power politics and spheres of influence. Rudd, a realist rather than an alarmist, argued that a strong U.S. remains essential for global stability, while a weakened U.S. risks creating power vacuums that China and Russia are ready to exploit.

A Fracturing Global Order?

For roughly eight decades after World War II, the United States played a central role in shaping the global order—promoting open markets, free trade, democratic expansion, and the U.S. dollar as the world’s reserve currency—underpinning a period of relative stability.

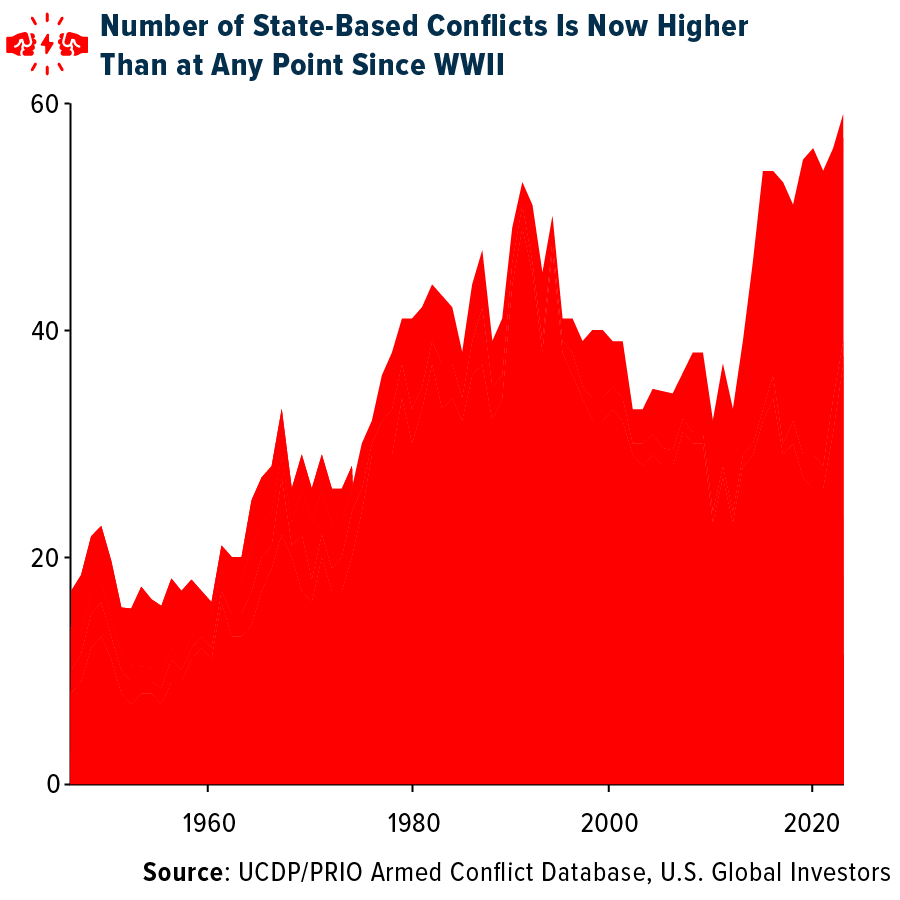

According to Rudd, that chapter may now be closing. Democratic governance is weakening worldwide, while the number of armed conflicts has climbed to its highest level since World War II.

China and Russia are making their ambitions increasingly explicit. Just last week, Xi Jinping and Vladimir Putin reaffirmed their deepening partnership, pledging mutual support across economic, military, and ideological fronts. With the New START treaty expiring this month, the final pillar of nuclear arms control between the United States and Russia has now fallen away.

Redrawing the Global Playbook

Rudd, who has written two major books on Xi Jinping, cautioned that China’s current leader is far from a pragmatist in the mold of Deng Xiaoping, whose market-oriented reforms in the 1970s set China on its path to global prominence. Instead, Xi is best understood as a Marxist-Leninist nationalist.

Under his leadership, China has moved beyond simply operating within existing global rules to actively reshaping them. The Chinese Communist Party is pursuing an all-encompassing strategy that spans nearly every sphere—military modernization, industrial leadership, energy self-sufficiency, and more. As I noted back in October, I see China’s expansive Belt and Road Initiative as a Trojan horse.

For Xi’s government, economic strength and national security are inseparable, a reality most evident in its approach to energy and technology.

China’s Sweeping Energy Expansion

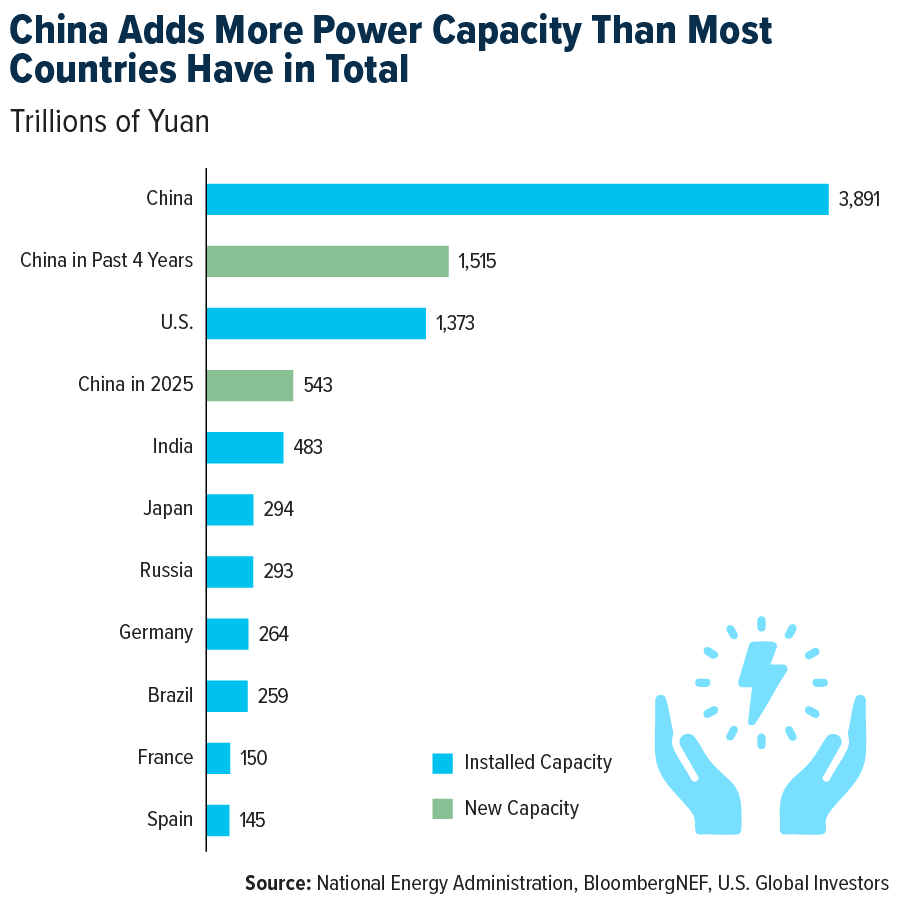

As the U.S. continues to oscillate on energy policy, China has been pressing ahead at full speed. Since 2021, it has added more power-generating capacity than the United States has built over its entire 250-year history—an astonishing feat achieved in just four years.

In 2025 alone, China brought online 543 gigawatts of new capacity across solar, wind, coal, nuclear, and gas. Looking ahead, BloombergNEF projects an additional 3.4 terawatts over the next five years—nearly six times what the U.S. is expected to add. The objective is clear: to ensure that China’s next wave of industries, including AI, robotics, and advanced manufacturing, is never constrained by energy shortages.

Clean Energy Emerges as the Next Growth Engine

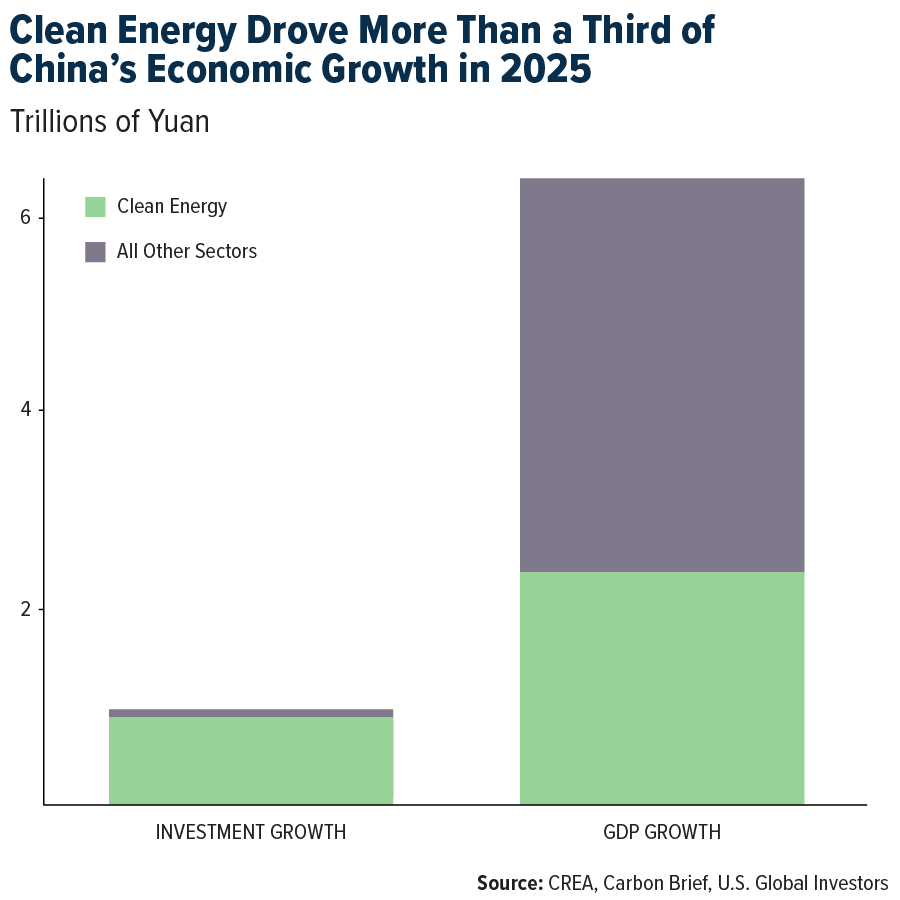

As I’ve noted before, both Elon Musk and NVIDIA CEO Jensen Huang have warned that China’s enormous power surplus could give it a decisive edge in AI computing—and the data backs that up.

In 2025, clean energy accounted for more than a third of China’s GDP growth and over 90% of new investment. Industries such as solar, electric vehicles, and battery technology generated more than $2.1 trillion in economic output, roughly on par with the GDP of Canada or Brazil. Viewed on its own, China’s clean energy sector would rank as the world’s eighth-largest economy.

Meanwhile, in Washington, progress remains stalled by politics.

By contrast, the United States has struggled to execute large-scale energy buildouts amid political gridlock and partisan divides. While China plans decades ahead, U.S. policymakers too often remain focused on the next election cycle.

According to a recent report from the Information Technology and Innovation Foundation (ITIF), China is on course to overtake the U.S. across a wide range of what it terms “national power industries.” These span military sectors such as guided missiles and tanks, dual-use industries like electronic displays and semiconductors, and enabling industries including automobiles and heavy construction equipment.

That said, the U.S. continues to commit heavily to defense spending. Congress recently approved an $839 billion defense bill—$8 billion more than requested by the Pentagon—with funding directed toward key systems such as the F-35, the B-21 bomber, and the Sentinel intercontinental ballistic missile program. More than $13 billion is also allocated to space and missile defense under President Trump’s Golden Dome initiative.

What This Means for Investors

Equity markets may already be signaling the start of a new investment cycle. In January, leadership shifted toward small-cap, domestically oriented stocks. While the S&P 500 hit new highs with a gain of about 1.4%, the Russell 2000 jumped 5.4%, markedly outperforming large caps. Small caps also logged a 15-day streak of outperformance versus the S&P—the longest since May 1996.

This strength does not appear to be a one-off. Since the beginning of Trump’s second term, the Russell 2000 has edged ahead of the S&P 500, rising roughly 17% versus 15% as of Friday, February 6. Some small-cap companies, though not all, tend to be less exposed to tariffs and could benefit over time in a less globalized world.

That said, careful stock selection is critical. Around 40% of Russell 2000 constituents are currently unprofitable.

Finally, with precious metals retreating from recent highs, investors may want to consider buying the dip. A 10% allocation to gold—split evenly between physical bullion and high-quality mining stocks—can help diversify portfolios, with regular rebalancing remaining essential.

Sources: Frank Holmes

Leave a comment