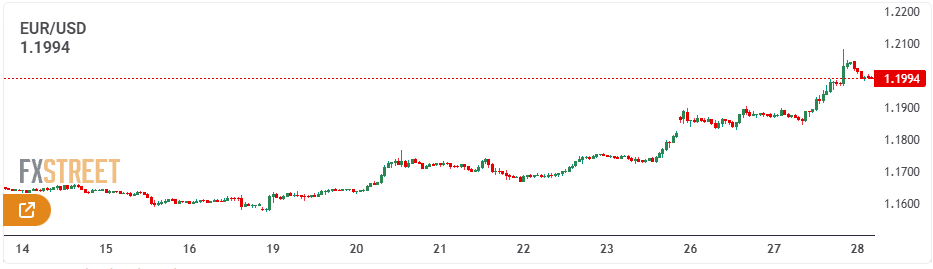

EUR/USD extended Monday’s positive momentum, pushing closer to the key 1.2000 level and reaching highs not seen since June 2021. The latest advance reflects continued selling pressure on the U.S. dollar, supported by a constructive risk backdrop and renewed investor focus on potential tariff-related risks stemming from the White House.

Macro & Fundamental Overview

EUR/USD’s bullish momentum remains firmly intact, closely mirroring persistent selling pressure on the U.S. dollar, which continues to be weighed down by concerns over trade policy, questions surrounding the Federal Reserve’s independence, and renewed shutdown risks.

The pair extended its advance for a fourth straight session on Tuesday, edging closer to the pivotal 1.2000 level for the first time since June 2021.

The latest leg higher reflects a further deterioration in the dollar’s outlook amid revived trade tensions and geopolitical uncertainty, all ahead of the Federal Reserve’s interest rate decision due on Wednesday.

Meanwhile, sentiment surrounding U.S.–European Union trade relations has improved after President Donald Trump softened his rhetoric last week regarding potential tariffs tied to the Greenland dispute. Markets have interpreted this shift positively, boosting risk appetite and lending support to the euro alongside other risk-sensitive currencies.

By contrast, the U.S. dollar continues to underperform. The Dollar Index (DXY) remains under heavy pressure, extending its decline toward the 96.00 area — levels last seen in late February 2022.

The FED: Rates on hold, politics in focus

The Federal Reserve delivered its widely anticipated December rate cut, but the key signal came from its messaging rather than the policy action itself. A divided vote and Chair Jerome Powell’s measured language suggested that additional easing is far from assured.

The Fed begins its two-day policy meeting today, with markets largely expecting rates to remain unchanged when the decision is released on Wednesday.

However, monetary policy may not be the primary focus this time. Market attention has increasingly turned to questions surrounding the Fed’s independence after reports earlier this month of a Justice Department investigation involving Chair Powell.

Compounding the uncertainty, President Trump has indicated that an announcement on his nominee for the next Fed Chair could be imminent, keeping scrutiny on the central bank well beyond the outcome of this week’s meeting.

ECB urges patience, not complacency

The European Central Bank left interest rates unchanged at its December 18 meeting, adopting a more measured and patient tone that has pushed expectations for near-term rate cuts further into the future. Modest upward revisions to growth and inflation projections helped underpin this approach.

Minutes from the meeting, released last week, showed policymakers saw little immediate need to adjust policy. With inflation hovering near target, the ECB has room to remain patient, while still retaining flexibility should risks materialize.

Governing Council members emphasized that patience does not equate to complacency. Monetary policy is viewed as appropriately calibrated for now, but not on autopilot. Markets appear to have absorbed this message, currently pricing in just over 4 basis points of easing over the coming year.

Positioning remains constructive, but confidence has softened

Speculative positioning remains tilted toward the euro, although bullish conviction appears to be easing.

CFTC data for the week ended January 20 show non-commercial net long positions declining to a seven-week low of around 111.7K contracts. At the same time, institutional participants also reduced short positions, which now stand near 155.6K contracts.

Meanwhile, open interest slipped to approximately 881K contracts, breaking a three-week streak of increases and suggesting that market participation may be thinning alongside fading confidence.

Key Events Ahead

Near term: The FOMC meeting is set to keep attention firmly on the U.S. dollar, while flash inflation data from Germany and preliminary GDP readings for the euro area will dominate the regional data calendar later in the week.

Risk: A more hawkish-than-expected outcome from the Fed could quickly tilt momentum back in favor of the dollar. In addition, a clear break below the 200-day simple moving average would increase the risk of a deeper medium-term correction.

EUR/USD Technical Outlook

EUR/USD continues to exhibit a firm bullish bias, trading at levels last seen in mid-2021 while gradually shifting focus toward the key 1.2000 psychological handle.

On the downside, initial support is located at the 2026 low of 1.1576 (January 19), reinforced by the closely watched 200-day simple moving average. A more pronounced correction could open the door to the November 2025 trough at 1.1468, followed by the August base at 1.1391.

Momentum indicators remain broadly supportive of further gains, although elevated conditions may challenge the immediate upside. The Relative Strength Index is hovering near 75, pointing to overbought territory, while an Average Directional Index reading above 26 confirms the presence of a well-established trend.

Bottom Line

For the time being, EUR/USD continues to be influenced primarily by U.S.-centric developments rather than euro area dynamics.

Absent clearer signals from the Federal Reserve on the extent of potential policy easing, or a more compelling cyclical recovery in the eurozone, any additional upside is likely to unfold in a steady, incremental manner rather than marking the beginning of a decisive breakout.

Sources: Fxstreet

Leave a comment