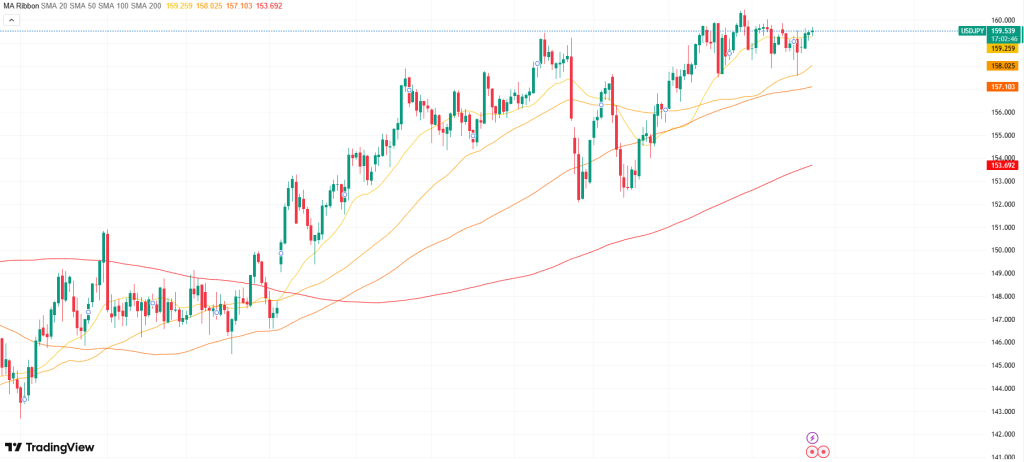

USD/JPY advances to its highest level in nearly two weeks during Thursday’s Asian session, supported by a mix of favorable factors. The Japanese Yen remains under pressure due to economic concerns linked to shipping disruptions in the Strait of Hormuz and expectations that the Bank of Japan may delay further rate hikes. At the same time, tensions between the United States and Iran over the key waterway continue to support the safe-haven US Dollar despite an extended ceasefire, providing an additional boost to the pair. Still, concerns about possible intervention limit further gains.

Technical analysis

The USD/JPY pair holds firm below the 23.6% Fibonacci retracement of the recent rally from last week’s swing low near 157.60, finding support at the 100-period EMA on the 1-hour chart. However, the Moving Average Convergence Divergence (MACD) has dipped slightly into negative territory, while the Relative Strength Index (RSI) around 48 points to neutral-to-mildly weak momentum.

Overall, momentum signals suggest that bullish strength is easing, though not enough to break the immediate intraday support near the 23.6% Fibonacci level at 159.15, which is reinforced by the 100-period EMA around 159.07. A deeper decline could bring the 38.2% retracement at 158.85 into focus, followed by additional Fibonacci support levels at 158.60, 158.36, and 158.01. If selling pressure intensifies further, the 157.57 swing low could emerge as a more significant downside support.

Fundamental Analysis

A short-term extension of the ceasefire between the United States and Iran triggers some selling pressure on the US Dollar (USD), weighing on USD/JPY. However, persistent economic concerns tied to the standoff in the Strait of Hormuz—where shipping disruptions and blockades continue despite the truce—help keep the Japanese Yen (JPY) under pressure and limit the pair’s downside.

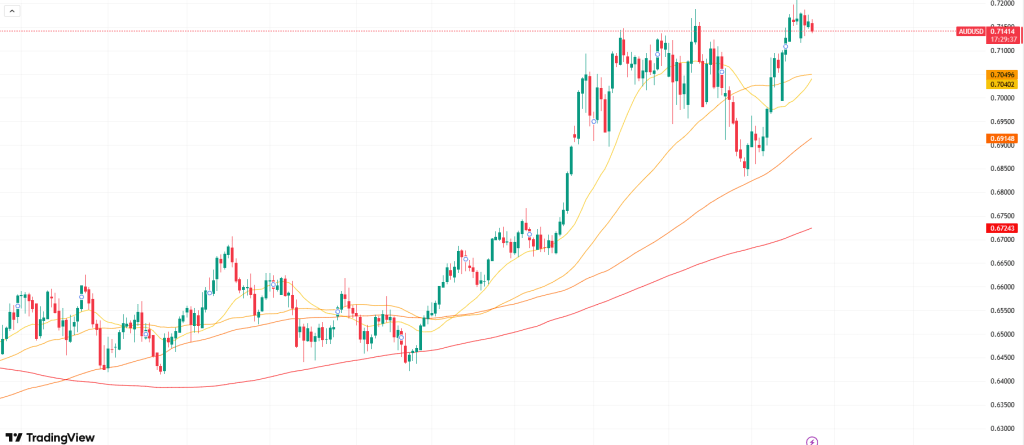

AUD/USD advances to around 0.7155 in early Asian trading on Thursday. President Trump noted there is “no set timeline” for the Iran conflict, while Australia’s preliminary PMIs returned to expansion territory in April.

The AUD/USD pair strengthens to around 0.7155 in early Thursday Asian trading, supported by improved risk sentiment after US President Donald Trump extended the Iran ceasefire. The move has eased concerns over a renewed conflict that previously drove energy prices higher, lending support to the Australian Dollar against the US Dollar. Investors now await the preliminary S&P Global PMI data due later in the day.

Trump stated that the ceasefire extension comes at Pakistan’s request as Washington looks for a unified proposal from Iran, helping calm market tensions. However, risks persist as Iran maintains control over the Strait of Hormuz and continues hostile actions in the region. Iranian parliament speaker and chief negotiator Mohammad Bagher Ghalibaf warned that reopening the key shipping route would be “impossible” amid what he described as ongoing violations of the ceasefire by the US and Israel.

Lingering geopolitical tensions in the Middle East could still support the safe-haven US Dollar and limit further upside in the pair.

On the data front, Australia’s preliminary S&P Global PMIs showed a return to expansion in April. The Manufacturing PMI rose to 51.0 from 49.8, the Services PMI improved to 50.3 from 46.3, and the Composite PMI climbed to 50.1 from 46.6, indicating a modest recovery in business activity.

WTI extends its rally for a third consecutive session, climbing to its highest level in nearly two weeks.

Persistent risks around the Strait of Hormuz offset the impact of the extended US-Iran ceasefire, lending support to oil prices.

Overall, the underlying fundamentals remain supportive of the bullish outlook, suggesting further upside potential.

WTI crude briefly surged to the $95.80–$95.85 region during the Asian session—its highest level in about a week and a half—before losing momentum and pulling back toward the lower end of the daily range. It currently trades just above $92.00, still holding modest gains of around 0.30% on the day.

Although the US-Iran ceasefire has been temporarily extended, markets remain doubtful about any lasting easing of tensions given the lack of meaningful progress in negotiations. Ongoing clashes around the Strait of Hormuz continue to raise concerns about potential supply disruptions, keeping a geopolitical risk premium embedded in oil prices and supporting a third consecutive day of gains.

Further underpinning the market, US President Donald Trump confirmed that the naval blockade of Iranian ports will remain in place. At the same time, Iran’s Tasnim news agency reported that Revolutionary Guard naval forces seized two vessels and that multiple container ships came under fire in the Strait. Coupled with an unexpected drop in US crude inventories, these developments add to the bullish tone.

That said, the latest upward spike was partly driven by unverified reports of an attack on Tehran, and the rally quickly lost steam once no concrete news followed. This calls for some caution among bullish traders, even though the broader fundamental backdrop still points to a bias for further upside in crude prices.

USD/CAD finds it difficult to build on the gains recorded over the past two days amid conflicting signals.

Tensions around Hormuz lend support to the safe-haven US dollar, while higher oil prices continue to bolster the Canadian dollar.

At the same time, differing policy outlooks between the Fed and the BoC are also limiting further upside in the pair.

USD/CAD eases slightly from a three-day high reached during Thursday’s Asian session but struggles to gain clear direction amid mixed fundamentals. While a temporary extension of the US-Iran ceasefire offers some relief, tensions surrounding the Strait of Hormuz continue to support the safe-haven US dollar. At the same time, higher crude oil prices lend strength to the Canadian dollar, limiting further upside in the pair.

US President Donald Trump announced on Tuesday an indefinite extension of the ceasefire with Iran just hours before its expiry, while reaffirming that the US Navy blockade of Iranian ports would remain in place. Iran, however, has made the lifting of the blockade a strict condition for resuming negotiations. Adding to tensions, Iran’s Revolutionary Guard reported firing on three vessels and seizing two in the Strait of Hormuz. These developments keep geopolitical risks elevated, helping the US dollar hold onto recent gains and offering support to USD/CAD.

Despite this, the dollar lacks strong bullish momentum as expectations for a hawkish Federal Reserve stance continue to fade, with markets increasingly pricing in a rate cut by year-end. In contrast, expectations are building for a possible rate hike by the Bank of Canada in April. Meanwhile, ongoing US-Iran tensions are pushing oil prices higher for a third consecutive day, benefiting the commodity-linked Canadian dollar and capping USD/CAD gains. This backdrop suggests caution, with traders likely waiting for stronger confirmation before calling a near-term bottom.

Looking ahead, attention turns to upcoming US data, including weekly jobless claims and flash PMI readings due later in the North American session. These releases could influence US dollar demand, while oil price movements and geopolitical developments remain key drivers, likely sustaining volatility and shaping trading opportunities for the pair.

GBP/USD could recover toward its two-month peak at 1.3599.

The 14-day RSI, hovering around 56, signals bullish momentum while remaining below overbought territory.

Nearby support is seen at the nine-day EMA, currently at 1.3493.

GBP/USD has edged lower for a third straight session, hovering around 1.3500 in Thursday’s Asian trading. Daily chart signals point to a possible bearish turn as the pair slips below its ascending channel.

Even so, the broader tone remains cautiously bullish. The pair is still holding just above the nine-period EMA and well above the 50-period EMA, suggesting underlying buying interest. Meanwhile, the 14-day RSI near 56 reflects healthy momentum without entering overbought territory, leaving scope for further gains on pullbacks.

If price re-enters the ascending channel, it could retest the two-month high at 1.3599 (April 17). A continued move higher may target the channel’s upper boundary near 1.3810, with a breakout potentially opening the door toward 1.3869, the highest level since September 2021.

On the downside, immediate support is seen at the nine-day EMA around 1.3493, followed by the 50-day EMA at 1.3427. A decisive break below these levels could shift momentum, exposing the March 31 low of 1.3159 and then 1.3010, the weakest level since April 2025.

Heightened geopolitical risks are weighing on gold’s short-term outlook.

Movements in oil, bond yields, and the US dollar continue to drive price action.

However, a decisive break above resistance could reignite bullish momentum.

Gold started the week under pressure, opening with a gap lower before gradually recovering toward Friday’s close. Recent developments in the Middle East have slightly shifted the near-term outlook, with risks now leaning modestly to the downside. The main concern is clear: a sharper increase in oil prices could strengthen the US dollar and lift bond yields—both factors that typically act as headwinds for gold.

So far, the rise in oil has been relatively moderate, with Brent crude up about 5% and trading near $95 per barrel. Even so, the broader environment remains fragile. The US seizure of an Iranian-flagged vessel near the Strait of Hormuz has drawn strong warnings from Tehran, including threats of retaliation and the potential for further disruption to already strained negotiations. With a two-week ceasefire set to expire on Wednesday and little tangible progress achieved, uncertainty continues to weigh on the situation. Iran has also reversed its brief reopening of the strait, accusing the US of failing to uphold its commitments while maintaining pressure on Iranian ports.

Before diving deeper into the macro drivers, let’s first take a look at gold’s chart…

Gold Technical Analysis

As the chart illustrates, gold is currently testing a key resistance zone in the $4,800–$4,850 range. This area is significant, as it combines multiple technical factors: previous support and resistance levels, the underside of a broken upward trendline, and the 61.8% Fibonacci retracement level.

Since early April, prices have repeatedly tested this resistance zone without achieving a clear breakout. However, the lack of strong selling pressure is telling. When resistance is tested multiple times without a significant pullback, it often signals underlying strength—raising the probability of an eventual upside break, though confirmation is still needed.

A daily close above $4,850 would serve as that confirmation, indicating a bullish reversal and paving the way for further upside. In that case, the next focus would be the $5,000 level, which aligns with the 78.6% Fibonacci retracement and also stands out as a key psychological milestone.

On the downside, initial support is seen near $4,750, followed by $4,600 and then $4,500. The most critical level, however, is $4,400. This zone has demonstrated its significance before—acting as support in early February and quickly being reclaimed after a brief breakdown in late March.

As long as $4,400 holds, the broader bullish structure remains intact, even if short-term conditions appear somewhat uncertain.

Can Gold Still Find Its Footing?

Despite increasingly heated rhetoric, there are still tentative signs that diplomacy hasn’t been fully abandoned. Donald Trump has struck a cautiously optimistic tone about the prospects for a deal, even while warning that military action targeting Iranian civilian infrastructure remains an option if talks break down.

On the other side, Iran continues to stand firm. The removal of restrictions around the Strait of Hormuz remains a key precondition for meaningful engagement, while officials emphasize that major sticking points—especially around nuclear issues—are still unresolved. Even so, financial markets have so far absorbed these developments without major disruption.

Behind the scenes, quieter diplomatic efforts appear to be ongoing. Asim Munir has reportedly engaged with Trump, underscoring that the Hormuz situation remains a central obstacle. There are indications that this view has been acknowledged, though it’s unclear whether it will lead to concrete progress.

If negotiations resume and produce a breakthrough, improved risk sentiment could support gold and potentially drive it toward the $5,000 level. If not, investors should be prepared for a more volatile and uneven trajectory ahead.

A Waiting Game for Now

For the time being, gold’s outlook remains finely poised. Much depends on the direction of bond yields and the US dollar—both of which are closely linked to inflation expectations and, importantly, movements in oil prices. In that context, ongoing developments in the Middle East continue to be the primary catalyst.

For now, a patient approach appears to be the most sensible course.

The conflict with Iran appears to be moving toward some kind of negotiated outcome, though the timing and specifics remain unclear. As the war drags on—and as the Iranian regime endures—the likelihood of a decisive US victory, understood as Tehran’s full capitulation, seems to diminish. This suggests a prolonged, uneven phase of de-escalation, with ongoing disruptions to the global economy likely in the meantime.

From this perspective, Iran is unlikely to win militarily. The US, on the other hand, has the capability to secure a decisive victory, but achieving unconditional surrender would almost certainly require a large-scale ground invasion—an option that appears improbable given the political costs, as seen in Afghanistan, Iraq, and Vietnam.

While the US can continue to intensify air and missile strikes, the impact of such tactics may be waning after weeks of sustained bombardment by US and Israeli forces. Expanding attacks on Iran’s infrastructure could inflict significant economic damage, but it remains uncertain whether this would compel the regime to fully concede, especially as it views the conflict as existential.

Given these dynamics, the most likely outcome is a gradual shift toward negotiations shaped by realities on the ground. The timing and structure of any agreement will depend on internal pressures—such as resource constraints and public sentiment—which create different breaking points for each side.

For the US, key concerns include maintaining its global credibility and influence in the Middle East, as well as managing economic repercussions. The closure of the Strait of Hormuz has already driven energy prices sharply higher, highlighting Iran’s ability to disrupt a critical global supply route and the limited options available to the US to fully counter such actions.

A critical vulnerability for Iran is the risk of economic exhaustion. While Tehran may be able to disrupt energy flows from the Gulf, the US has the capacity to tighten restrictions on Iran’s own oil exports—its primary source of income.

Ultimately, the situation may hinge on which side yields first.

China could emerge as a key, if understated, influence. As the largest buyer of Iranian oil—accounting for over 80% of its exports in 2025, and roughly 13–14% of China’s seaborne crude imports, according to Kpler—Beijing holds significant economic leverage. At the same time, China maintains extensive trade ties with the US, despite ongoing tariffs, giving it strong incentives to balance relations with both sides.

This dual positioning suggests China could quietly shape the path toward negotiations. One important dynamic to watch is whether Beijing uses its leverage to keep Iran engaged in talks, even as it continues to support Tehran’s capacity to withstand US pressure.

For the US, the key issue is when mounting political and economic pressures might convince President Trump that negotiation is the most viable option. Another open question is how far Washington is prepared to go in further weakening Iran’s economy. While escalation may be tempting, it comes with clear trade-offs. A renewed military push would likely keep energy exports constrained, sustaining higher inflation and dampening economic growth both domestically and globally.

In the end, neither side may achieve the outcome it seeks—only a compromise that both can ultimately accept.

The latest decline in gold and silver has taken investors by surprise again, but for reasons quite different from the late-February correction. While that earlier drop was largely the result of positioning and technical factors, the current weakness is unfolding amid escalating geopolitical tensions and tighter financial conditions. Despite these differences, both episodes underscore how sensitive precious metals are to changes in interest rates, the US dollar, and overall liquidity. Here are five key takeaways shaping the current market move:

Macro Forces Are Now in Control

Unlike the February selloff, which stemmed mainly from position unwinding, this decline is being driven by broader macro dynamics. Rising tensions between the US and Iran have pushed oil prices higher, lifting inflation expectations and prompting markets to reassess the outlook for interest rates. As yields climb and the dollar strengthens, gold faces pressure as a non-yielding, dollar-priced asset. This marks a fundamentally driven shift rather than a technical correction.

The Dollar Is Overtaking Gold’s Safe-Haven Role

Although geopolitical risks typically support gold, the US dollar has emerged as the preferred safe haven this time. Instead of flowing into gold, capital is rotating into dollar-denominated assets as financial conditions tighten. This has created an unusual scenario where risk aversion rises even as gold prices fall, with the dollar absorbing most of the defensive demand.

Real Yields Remain the Critical Channel

Real yields have played a central role in both downturns. In February, a mild adjustment in rate-cut expectations weighed on gold. Now, higher energy prices are pushing up inflation expectations while reducing the likelihood of near-term rate cuts, keeping real yields elevated. This continues to exert downward pressure on precious metals.

Silver Is Amplifying Market Moves

Silver’s steeper drop highlights its higher volatility and dual identity as both a precious and industrial metal. Previously impacted by speculative positioning, it is now also facing concerns about slowing global growth as rising energy costs threaten demand. This combination makes silver more vulnerable and prone to larger swings than gold.

Stability Hinges on Multiple Uncertain Factors

The outlook for gold and silver remains unclear. While February’s stabilization depended on positioning resetting, the current trajectory will be shaped by a more complex mix of factors: the persistence of the energy shock, the Federal Reserve’s response, and the direction of the US dollar. A de-escalation in geopolitical tensions could spark a quick rebound, but if inflation stays elevated and delays rate cuts, precious metals may continue to face headwinds in the near term.

Daily Charts for Gold and Silver

Historical performance does not guarantee future outcomes.

Trading gold and silver CFDs

Whether you’re looking to go long, short, or adjust your portfolio exposure, choosing a reliable broker is essential. Ideally, this means a platform that provides round-the-clock customer support and dedicated account assistance, ensuring smooth trade execution whenever required.

Gold prices climbed during Asian trading on Wednesday, rebounding from a one-week low after the U.S. extended its ceasefire with Iran indefinitely, though uncertainty around future peace negotiations persisted.

The precious metal had come under pressure in the previous session after Federal Reserve Chair nominee Kevin Warsh indicated he had not assured President Donald Trump of any interest rate cuts if confirmed.

Spot gold gained 0.9% to $4,763.66 per ounce, while gold futures advanced 1.3% to $4,782.21/oz as of 02:45 ET (06:45 GMT). Prices continued to trade within the $4,700–$4,900 range observed over the past two weeks.

Other precious metals also posted gains, with spot silver rising 2.4% to $78.5335/oz and spot platinum increasing 2.3% to $2,087.15/oz.

On Tuesday, Donald Trump announced an indefinite extension of the ceasefire with Iran, opening the door for further negotiations between Washington and Tehran.

Despite the extension offering some near-term relief, the outlook for future peace talks remains unclear. Expected discussions between the U.S. and Iran, which were slated for Tuesday, collapsed at the last minute.

Trump also stated that a naval blockade against Iran would stay in place, prompting backlash from Iranian officials, who described the move as an “act of war.”

Gold has faced difficulties since the conflict began, as safe-haven demand has been outweighed by concerns over the war’s potential to drive inflation.

Since the outbreak of the conflict in late February, the metal has traded more like a risk-sensitive asset, often moving in line with equities as market sentiment shifts with developments in the situation.

Warsh signals no pledge on rate cuts, hints at major Fed policy changes

Precious metals came under pressure on Tuesday as the U.S. dollar strengthened, supported by market reaction to testimony from Kevin Warsh.

Warsh stressed the importance of the Federal Reserve’s independence from political influence, while also pointing to the possibility of a significant policy overhaul at the central bank if he is confirmed as chair.

A former Fed governor, Warsh is viewed as less dovish than markets had anticipated. His nomination in late January had already sparked sharp declines in gold and other precious metals.

Although his confirmation appears likely, the timeline remains uncertain. Several Republican leaders have opposed moving forward with Warsh’s appointment until the Trump administration ends its ongoing probe into current Fed Chair Jerome Powell.

As a result, Powell is expected to remain in his role beyond the scheduled end of his term on May 15, particularly if Congress delays Warsh’s confirmation.

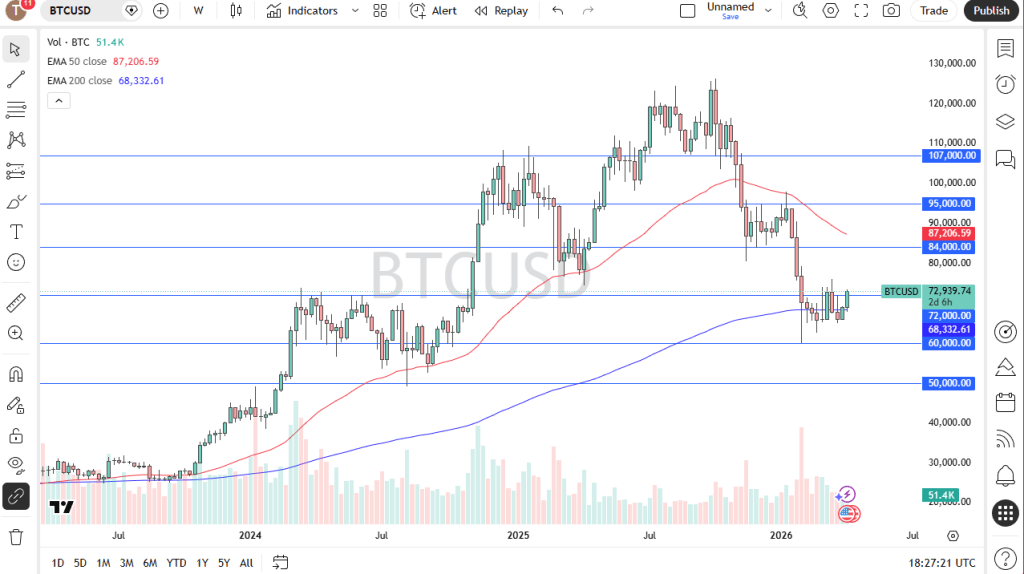

Bitcoin climbed above $78,000 on Wednesday, supported by President Donald Trump’s extension of the Iran ceasefire and stronger institutional buying, lifting overall market sentiment.

The leading cryptocurrency was last up 2.7% at $78,018.4 around 02:49 ET (06:49 GMT), after touching a 24-hour high of $78,430.4. It was also on track for a third consecutive day of gains.

Trump announces an extension of the ceasefire with Iran

U.S. President Donald Trump announced an open-ended extension of the Iran ceasefire, noting the decision was partly influenced by requests from Pakistani officials seeking additional time for peace talks in Islamabad.

The extension remains unilateral, however, leaving uncertainty over whether Tehran will formally agree.

While the ceasefire is in place, tensions persist. The U.S. continues its naval blockade of Iranian ports, and disruptions in the Strait of Hormuz have yet to fully subside.

Even so, markets viewed the move as a sign of near-term de-escalation. Oil prices declined, and the U.S. dollar weakened after recent gains.

Analysts note that Bitcoin is increasingly behaving as both a risk asset and a hedge against geopolitical tensions, attracting inflows as investors balance easing risks with ongoing uncertainty.

Strategy snapped up roughly $2.5 billion worth of Bitcoin last week, marking one of its largest purchases to date.

Strategy snapped up $2.5 billion in Bitcoin last week, reinforcing market momentum amid a fresh wave of institutional demand.

The firm, Strategy Inc (NASDAQ:MSTR), revealed it purchased 34,164 BTC in the week ending April 19 at an average price of roughly $74,395 per coin. This brings its total holdings to around 815,000 bitcoins, acquired at a cumulative cost of approximately $61.6 billion—marking one of the largest buys in its history.

To finance the acquisition, Strategy leaned heavily on capital markets, raising about $2.18 billion through the sale of high-yield preferred shares and another $366 million via common stock issuance. These preferred instruments, offering yields near 11.5%, have become a central funding mechanism, enabling the company to expand its Bitcoin position while aiming to minimize shareholder dilution.

In the broader crypto market, most altcoins also moved higher on Wednesday, though gains remained modest. Ethereum, the second-largest cryptocurrency, climbed 3.2% to $2,391.53, while XRP added 1.3% to $1.46. Solana, Cardano, and Polygon each rose around 2.5%, and Dogecoin gained 2.3% among meme tokens.

Sterling and the euro inched slightly higher on Wednesday, as markets found reassurance in Fed Chair nominee Kevin Warsh’s Senate testimony. His remarks helped ease concerns about the Federal Reserve’s independence without significantly altering expectations for interest rates.

By 03:55 ET (07:55 GMT), GBP/USD had risen 0.16% to 1.3525, moving within a daily range of 1.3498–1.3535. Meanwhile, EUR/USD climbed 0.09% to 1.1754, staying comfortably within its session band of 1.1734–1.1763.

Appearing before the Senate on Tuesday, Warsh avoided outlining specific policy moves but strongly defended the Fed’s autonomy. Analysts noted that this was enough to prevent a Treasury-driven surge in the dollar. As a result, the greenback remained largely rangebound, with the DXY struggling to break back above 99 despite steady equity performance. The S&P 500 has advanced about 3% since the beginning of the US-Iran conflict, reducing a key support factor for a stronger dollar recovery.

According to ING, the dollar’s upside remains limited by resilient equities, as European markets have not weakened enough to push EUR/USD significantly lower. The firm expects the pair to consolidate around 1.172–1.177 in the absence of meaningful diplomatic developments, with buyers likely to emerge on dips near 1.167–1.170.

For sterling, the latest UK inflation figures brought no major surprises. Higher energy prices lifted headline CPI, while core services inflation stayed broadly unchanged, reinforcing expectations that the Bank of England will keep rates on hold next week. ING continues to anticipate that the BoE will maintain its current stance through year-end, with inflation peaking around 3.5–4%—not high enough to prompt policy tightening.

Political uncertainty still weighs on the pound, as markets monitor Prime Minister Keir Starmer’s domestic position ahead of the 7 May local elections, where Labour is expected to underperform.

Meanwhile, the broader geopolitical situation remains unsettled. President Trump announced a last-minute ceasefire extension, but tensions in the Strait of Hormuz persist, with the US blockade ongoing and new reports of an incident involving a UK container ship. Going forward, both currency pairs are likely to be driven by developments related to the conflict, oil price movements, and further signals from Fed officials.

Dow Jones futures climb as sentiment improves on Iran’s plan to hold a second round of US talks ahead of the ceasefire deadline.

Wall Street ended Monday on a softer note as renewed US–Iran tensions intensified over the weekend.

Trump signaled he is unlikely to extend the truce with Tehran if no agreement is reached.

Dow Jones futures rise 0.14% to above 49,700, while S&P 500 and Nasdaq 100 futures also edge higher by 0.13% and 0.27% to around 7,160 and 26,820, respectively, during Tuesday’s European session ahead of the US market open.

US equity futures move higher as sentiment improves, driven by reports that Iran will send a delegation to Islamabad for a second round of talks with the US before the truce deadline. President Donald Trump said Vice President JD Vance is expected to travel to Pakistan to resume negotiations, “either Tuesday night or Wednesday morning,” according to Bloomberg.

In Monday’s regular session, Wall Street ended slightly lower. The Dow Jones slipped 0.01%, while the S&P 500 and Nasdaq 100 declined 0.24% and 0.26%, retreating from record highs amid renewed US–Iran tensions over the weekend. Tech stocks led the pullback, with Broadcom and Meta dropping more than 2%, and Microsoft, Nvidia, and Alphabet falling over 1%.

Trump also indicated he is unlikely to extend the truce with Tehran if no deal is reached before its expiration this week, adding that the Strait of Hormuz will remain blocked until an agreement is secured. The situation has pushed oil prices higher and increased inflation concerns, reducing expectations for near-term Federal Reserve rate cuts.

Gold comes under renewed selling pressure in the Asian session, though losses appear contained.

Persistent inflation concerns keep U.S. bond yields elevated, supporting the dollar and pressuring the metal.

However, growing expectations of Federal Reserve rate cuts may limit further dollar strength and help support the non-yielding gold.

Gold (XAU/USD) remains under pressure and trades below the $4,800 level in the early European session on Tuesday, though it stays above the one-week low touched a day earlier. Market participants remain doubtful about a potential US–Iran deal as tensions persist around the Strait of Hormuz. The US Navy’s seizure of an Iranian-flagged cargo vessel in the Gulf of Oman, followed by Iran’s renewed closure of the key shipping route, has supported crude oil prices. This, in turn, has reignited inflation concerns, boosted the US dollar, and weighed on gold.

That said, stronger gains in the dollar appear limited as expectations for further rate hikes by the Federal Reserve continue to fade. According to the CME Group’s FedWatch Tool, markets are now pricing in roughly a 45–50% chance of a rate cut by year-end, which could cap USD strength and provide underlying support for non-yielding gold. Meanwhile, traders are likely to remain cautious amid uncertainty over whether US–Iran peace talks will materialize, making it wise to wait for clear follow-through selling before expecting deeper losses in XAU/USD.

US President Donald Trump stated that American negotiators will travel to Pakistan for another round of discussions with Iran in an effort to extend a fragile ceasefire set to expire on Wednesday. However, Iranian officials remain reluctant to engage in talks under current conditions, citing the ongoing US blockade. Parliament Speaker Mohammad Bagher Ghalibaf emphasized that Iran will not negotiate under pressure, while Foreign Minister Abbas Araghchi pointed to continued US ceasefire violations as a key obstacle to diplomacy. Despite this, reports indicate that an Iranian delegation may still head to Islamabad for negotiations.

Going forward, markets will stay highly sensitive to developments in the US–Iran situation, which could drive volatility across asset classes. In addition, traders will look to testimony from Fed Chairman-designate Kevin Warsh for further direction. Given the mixed fundamental backdrop, caution remains warranted before taking strong directional positions in gold.

Gold (XAU/USD) – 4-hour timeframe chart

The bullish outlook for gold remains intact as long as price stays above the 200-period EMA and the 50% Fibonacci retracement, a zone that now acts as a confluence support after previously serving as resistance.

The metal continues to show a constructive short-term tone, holding above the 200 EMA at $4,784.25. Just below, the 50% retracement of the March decline at $4,762.13 reinforces this support area, suggesting underlying buying interest. However, momentum indicators are relatively neutral rather than strongly trending—RSI is hovering around 51, while MACD remains slightly in negative territory—indicating that although bulls are still in control structurally, upside momentum is not particularly strong at the moment.

In terms of levels, immediate support lies at the 200 EMA ($4,784.25), followed by the 50% retracement at $4,762.13. A decisive break below this zone could open the door to deeper Fibonacci support levels at $4,607.05 and $4,415.17, with the broader downside target near $4,105.01. On the upside, resistance begins at the 61.8% retracement level at $4,917.21, with further barriers at $5,138.01 (78.6%) and the cycle high around $5,419.25, where rejection could potentially limit further gains in the current bullish phase.

Oil prices dropped by more than $1 on Tuesday, giving back the previous session’s gains, as expectations grew that U.S.–Iran peace talks this week could ease tensions and allow more crude supply from the Middle East.

Brent crude fell $1.04 (1.1%) to $94.44 per barrel by 0600 GMT. U.S. West Texas Intermediate (WTI) for May declined $1.66 (1.9%) to $87.95, with the contract expiring Tuesday, while the more active June contract slipped $1.24 (1.4%) to $86.18.

This pullback followed a sharp rally on Monday, when Brent jumped 5.6% and WTI surged 6.9% after Iran closed the Strait of Hormuz again and the U.S. seized an Iranian cargo vessel as part of its blockade.

Despite ongoing risks, market sentiment is being driven by optimism that negotiations could extend the current ceasefire or even produce a broader agreement, though disruptions to supply remain a concern.

ING analysts noted that while prices spiked after the Strait of Hormuz closure, trading patterns still reflect confidence in diplomatic progress, warning that markets may be underestimating the scale of supply disruptions.

Iran is considering joining peace talks in Pakistan, according to a senior official, as Islamabad works to mediate and end the U.S. blockade. However, the blockade continues to complicate Tehran’s participation, especially with the current two-week ceasefire nearing its expiry.

Citi analysts expect a memorandum of understanding or a ceasefire extension this week, potentially leading to a wider deal, but caution that prolonged disruptions remain possible if negotiations fail.

Uncertainty persists, as Iranian officials emphasized no final decision has been made. Foreign Minister Abbas Araqchi cited ongoing U.S. ceasefire violations as a barrier, while Parliament Speaker Mohammad Baqer Qalibaf reiterated that Iran will not negotiate under pressure.

Meanwhile, shipping through the Strait of Hormuz—responsible for roughly 20% of global oil flows—remained constrained. Citi estimates that if disruptions last another month, losses could reach 1.3 billion barrels, pushing prices toward $110 per barrel in Q2 2026.

Kuwait has declared force majeure on oil exports due to the blockade, while higher prices have already reduced global demand by about 3%, according to Societe Generale. The bank warned that risks skew toward greater losses the longer supply disruptions persist, with full normalization unlikely before late 2026.

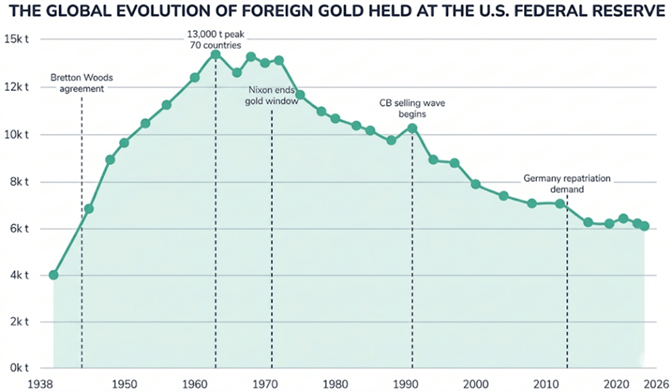

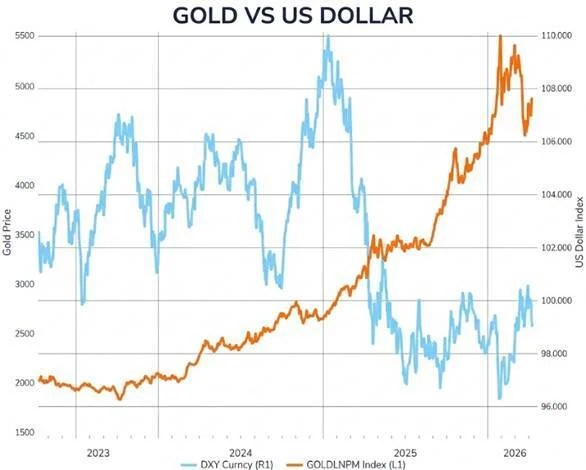

One by one, quietly and without public notice, central banks around the world are repatriating their gold reserves. From New Delhi to Belgrade, Frankfurt to Paris, institutions are arriving at similar conclusions independently. The trust that once supported the postwar reserve architecture is beginning to show visible cracks.

Introduction

The last time France withdrew its gold from American custody was in 1965. Under Charles de Gaulle, who viewed the Bretton Woods system as granting the United States an “exorbitant privilege,” France dispatched a warship to New York to exchange dollars for gold—directly challenging US monetary supremacy.

Six years later, President Richard Nixon ended the dollar’s convertibility into gold, effectively dismantling the Bretton Woods gold standard. Six decades on, France has again quietly reduced its gold holdings stored at the New York Federal Reserve. This time, instead of geopolitical confrontation, the move is executed through discreet financial transfers, driven by a €12.8 billion arbitrage opportunity.

Despite the change in method, the underlying motivation appears familiar: persistent skepticism toward dollar-centric financial systems and a renewed emphasis on monetary sovereignty. While history does not repeat exactly, developments in gold markets often echo earlier patterns with notable precision.

The Silent Return

For much of the postwar period, the physical location of gold reserves was rarely questioned. Many central banks—particularly in Europe and the developing world—kept their gold in custodial vaults such as the Federal Reserve Bank of New York and the Bank of England, assuming these locations were neutral, liquid, and politically secure. That long-standing assumption is now weakening.

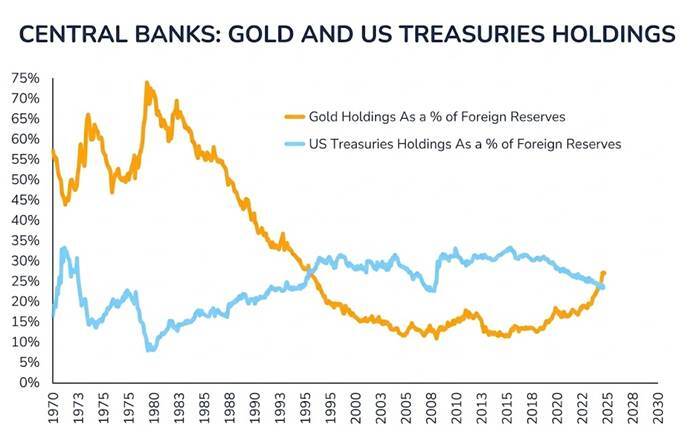

Recent data supports this shift. The World Gold Council’s Central Bank Gold Reserves Survey 2025, based on responses from 73 institutions, shows that 59% of central banks now store at least part of their gold domestically, up from 41% in 2024 and 50% in 2020. Since 1972, approximately 6,900 tonnes of gold have been repatriated to national vaults.

This marks an 18-percentage-point increase in just five years, with most of the change occurring in the past year alone. The same survey also found that 95% of central banks expect global gold reserves to rise further over the next 12 months, indicating a broadly shared expectation of continued accumulation among monetary authorities.

The driver behind this shift is increasingly evident. The 2022 freezing of around $300 billion in Russian foreign currency reserves sent a powerful message: assets held abroad may not remain fully under the owner’s control in times of geopolitical stress. An updated 2025 Invesco survey of central banks shows that the share storing gold domestically has increased by 18 percentage points since that episode—suggesting a striking alignment between the event and changing reserve behavior.

Gold has traditionally been regarded as the ultimate safe-haven asset, but recent developments revealed a less discussed vulnerability: what was once framed as market risk has increasingly become jurisdictional and counterparty risk. In other words, even physical reserves held in trusted foreign vaults depend on political continuity and legal access—risks that were previously underappreciated.

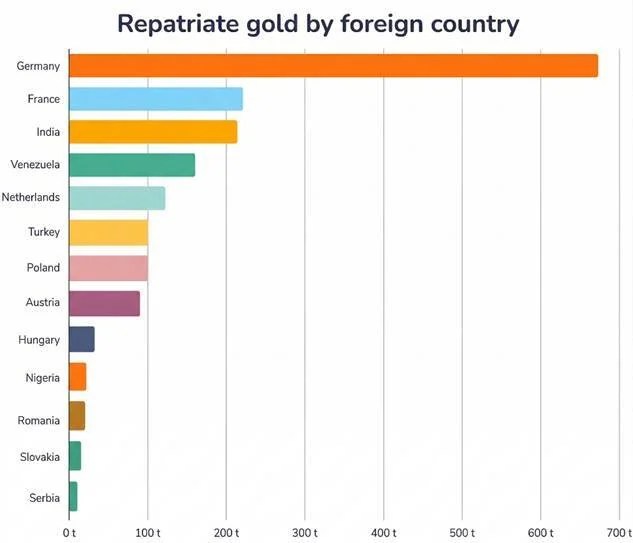

The reaction has been broad-based and measured in substantial volumes. Bloomberg reports that India has repatriated roughly 280 tonnes of gold over the past four years, including a notable transfer from the Bank of England in 2024. In July 2025, it was also reported that Serbia brought back its entire gold holdings—worth about $6 billion—into domestic storage, deliberately avoiding reliance on established international custodial centers.

Other countries, including Poland, Turkey, and Nigeria, have followed similar paths. While much of this movement has been led by emerging markets, the trend is gradually extending into parts of Western Europe as well, pointing to a broader structural rethinking of where ultimate financial security resides.

The pace of accumulation further strengthens this trend. According to World Gold Council data, central banks purchased more than 1,000 tonnes of gold annually in 2022, 2023, and 2024—an unprecedented sustained buying cycle in modern history. Although this pace eased to 863 tonnes in 2025, it still remained exceptionally high by historical standards.

By early 2026, total gold held by central banks worldwide was estimated at around $4 trillion, overtaking, for the first time, the roughly $3.9 trillion in US Treasury securities held by the same institutions. According to the World Gold Council and Visual Capitalist, this shift reflects a meaningful rebalancing of global reserve preferences, with potential long-term implications for the international monetary system.

France’s Banque de France offers a particularly illustrative case. Between July 2025 and January 2026, it carried out a discreet program involving 129 tonnes of gold stored at the New York Federal Reserve—about 5% of its total 2,437-tonne holdings—executed through 26 separate transactions. However, this was not a straightforward physical repatriation.

Instead of transporting older bars across the Atlantic, the central bank sold legacy-format gold in New York and replaced it with modern London Good Delivery bars held in Paris. The result was effectively a swap in form rather than a logistical relocation.

As reported by La Tribune, the financial outcome was striking: a combined €12.8 billion gain—€11 billion in 2025 and €1.8 billion in 2026—achieved without physically moving the metal. While often described in the press as repatriation, the operation was more accurately a form of quality arbitrage that incidentally increased domestic holdings.

The End of the American Vault Illusion

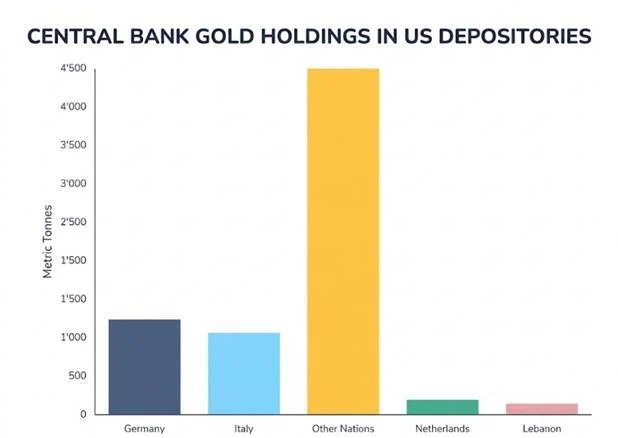

Germany’s case underscores the strategic significance of this shift more clearly than France’s quieter financial maneuvers. The Bundesbank continues to hold 1,236 tonnes of gold at the Federal Reserve Bank of New York—around 36.6% of its total 3,378-tonne reserves—and this remains the largest single foreign gold position stored at the NY Fed.

Between 2013 and 2017, Germany conducted the largest gold repatriation operation in modern history, withdrawing 674 tonnes from both New York and Paris. This process was framed at the time as a technical modernization of reserve management rather than a strategic pivot.

For context, the New York Federal Reserve currently stores roughly 6,331 tonnes of foreign sovereign gold. Germany alone accounts for nearly one-fifth of all foreign-held gold in its vaults in lower Manhattan, highlighting how concentrated global trust once was in a single custodial hub.

From 2013 to 2021, Germany repatriated about 300 tonnes from New York and 283 tonnes from Paris, completing what was widely regarded as a normalization of storage practices. The remaining 1,236 tonnes were, at the time, still considered securely and appropriately held abroad.

What has changed since then is not necessarily the security of the vault itself, but the perception of what “secure custody” means in a more fragmented geopolitical environment.

This ruling is increasingly subject to political debate. In January 2026, former senior Bundesbank official Emanuel Mönch warned that, amid heightened geopolitical uncertainty, concentrating large volumes of gold in the United States poses risks. He argued that the Bundesbank should consider further repatriation as a way to enhance strategic autonomy. His position echoes a widening political consensus in Germany, spanning parties from the AfD to figures within the Greens and FDP.

Despite this, the Bundesbank has not changed its official policy. It continues to regard New York as a safe and dependable storage hub, and no additional repatriation initiative is currently planned. Nevertheless, the divergence between institutional continuity and mounting political pressure is becoming more pronounced.

At a deeper level, the issue is structural. For many years, the rationale for keeping gold in New York rested on three foundations: liquidity, given the ability to quickly trade or mobilize gold in the world’s largest market; network advantages, driven by the scale and efficiency of the LBMA and New York Federal Reserve gold markets; and political confidence, based on the assumption that US custody would not be used as a geopolitical lever.

Each of these pillars has since been weakened to some extent. The 2022 sanctions episode demonstrated that the US and its allies are willing to deploy financial infrastructure as an instrument of geopolitical pressure. A more transactional approach in US foreign policy has further reinforced such concerns. At the same time, improvements in European gold markets and LBMA access have reduced the liquidity advantages of storing reserves in New York, making domestic storage increasingly viable without significant market disadvantage.

The Overlooked Gold Catalyst Markets Still Haven’t Factored In

Investment banks are largely aligned on a continued rise in gold prices, though their forecasts differ, reflecting varying views on how quickly central bank behavior is shifting.

Goldman Sachs has lifted its 2026–2027 outlook to $4,000–$5,400, pointing to sustained demand from emerging-market central banks. J.P. Morgan Private Bank is even more bullish, projecting $6,000–$6,300, attributing the upside to accelerating diversification away from the US dollar. UBS takes a more moderate stance at around $4,200, but similarly highlights a global trend of reducing dollar exposure.

Taken together, the wide forecast range of roughly $3,100 to $6,300 is less a sign of disagreement about direction and more about uncertainty over timing—particularly the speed of gold repatriation and reserve reallocation. The common thread across all projections is a shared conviction in a longer-term bullish trend, driven by evolving central bank strategies. Early 2026 pricing behavior already appears to be reinforcing this growing institutional confidence in gold.

Gold repatriation does not change the total global supply; it simply reallocates where and how gold is held and accessed. For example, when the Banque de France substituted New York-held ingots with London Good Delivery bars in Paris, global central bank reserves remained unchanged, with only a shift in classification and location. The London Bullion Market Association (LBMA), which clears roughly $30 billion in gold transactions daily, operates on the assumption that institutional gold is readily accessible regardless of storage location.

As the pool of immediately available gold tightens, borrowing costs tend to increase, price spreads widen, and physical gold can trade at a premium to paper claims. This reflects a scarcity of deliverable metal that is not captured in conventional supply-flow data and is often underrepresented in market models—highlighting that distribution can matter as much as total stock.

If Germany were to pursue a similar repatriation of its 1,236 tonnes held at the New York Fed, the effects on the physical market would be more pronounced. Such a move would require sourcing, refining to current delivery standards, and physically transporting the gold, generating real demand pressure within the LBMA system, even though global central bank holdings would remain unchanged.

This scenario is not currently priced in by markets. While the German repatriation debate remains largely political and the Bundesbank has given no indication of imminent action, the underlying drivers that prompted France’s earlier decision—bar standard considerations, proximity to European counterparties, and a geopolitical preference for domestic custody—are similarly relevant to Germany.

Understanding the De-Dollarisation Trend

Gold repatriation is frequently framed as a symbolic geopolitical gesture, but its implications are more tangible. When central banks repatriate gold, they also reduce their dependence on the dollar-based financial system, including its clearing mechanisms, custodial arrangements, and settlement infrastructure. Each tonne of gold brought back reduces exposure to dollar-linked channels and potential sanctions risk.

This shift is already becoming measurable. By early 2026, the value of gold held by central banks exceeded their holdings of US Treasuries—approximately $4 trillion compared with $3.9 trillion. This signals a gradual but persistent move away from the US dollar’s role as the dominant reserve asset. Unlike traditional currency diversification, this transition is difficult to capture fully in official statistics, yet it is ongoing, accelerating, and still not fully reflected in market pricing.

Historically, gold prices have tended to decline when the US dollar strengthens and real interest rates rise. However, this relationship has weakened since 2022, as central banks have emerged as significant buyers driven more by geopolitical considerations than by traditional market indicators such as yields or currency movements. This introduces a form of demand that is relatively insensitive to price.

Consequently, conventional gold valuation models are becoming less reliable and often understate price levels. This shift also helps explain why institutions such as Goldman Sachs, J.P. Morgan, and UBS are projecting significantly higher gold prices than would have been considered plausible prior to 2022. In effect, the pricing dynamics of gold have evolved, while many existing models have yet to fully adjust.

Conclusion

The structural argument for gold repatriation is compelling, but it is not without inconsistencies. Recent conflicts in the Middle East have added further complexity, at times pressuring both gold and the US dollar simultaneously and disrupting traditional market correlations. Central banks also do not act as a single coordinated group—some are accumulating gold, others are repatriating it, while some are still selling under financial or policy constraints.

Although data from the World Gold Council, analyst price targets, and observable repatriation flows support the broader trend, the pace is uneven and motivations vary significantly across institutions. Gold continues to function as a form of monetary insurance, but its behavior and underlying drivers are more nuanced and less linear than the prevailing narrative often implies.

Markets are increasingly betting that the conflict with Iran has come to an end. Yet even if that assumption holds, the economic repercussions are likely to persist for months—if not years.

While global attention tends to center on the immediate spectacle of war—airstrikes, blockades, and sanctions—the most disruptive consequences often emerge more slowly. In the Persian Gulf, the true impact is delayed, carried across the world through disrupted shipping routes and declining exports of oil, natural gas, and key agricultural inputs. Because of these lags, the global economy is only beginning to absorb the shock from reduced supply.

As Comfort Ero of the International Crisis Group observes, wars expose the fragile systems that quietly sustain everyday life. Strategic chokepoints like the Strait of Hormuz—normally overlooked—suddenly become critical when they falter.

Oil shipments from the Gulf typically take between 30 and 45 days to reach major markets. That delay means supply disruptions don’t show up immediately. Instead, countries draw down existing inventories while incoming supply gradually shrinks. By the time shortages become visible, the disruption has already been building for weeks.

Recent data underscores this dynamic. OPEC output plunged by 27% in March, signaling the first wave of global supply strain. Even under a sustained ceasefire, a rapid recovery appears unlikely. Industry leaders estimate it could take months for production in the region to return to normal levels.

At the same time, the easing of military tensions may create a false sense of stability. Beneath the surface, the economic damage continues to accumulate. Supply chain pressures are only now intensifying. Companies are beginning to feel the strain—illustrated by manufacturers halting orders due to shortages tied to disruptions in the energy supply chain.

The agricultural sector offers another clear example. With planting season nearing its end, rising fertilizer and fuel costs are forcing farmers to make difficult choices: cut back production or absorb significant financial losses. Many are already reporting deteriorating financial conditions.

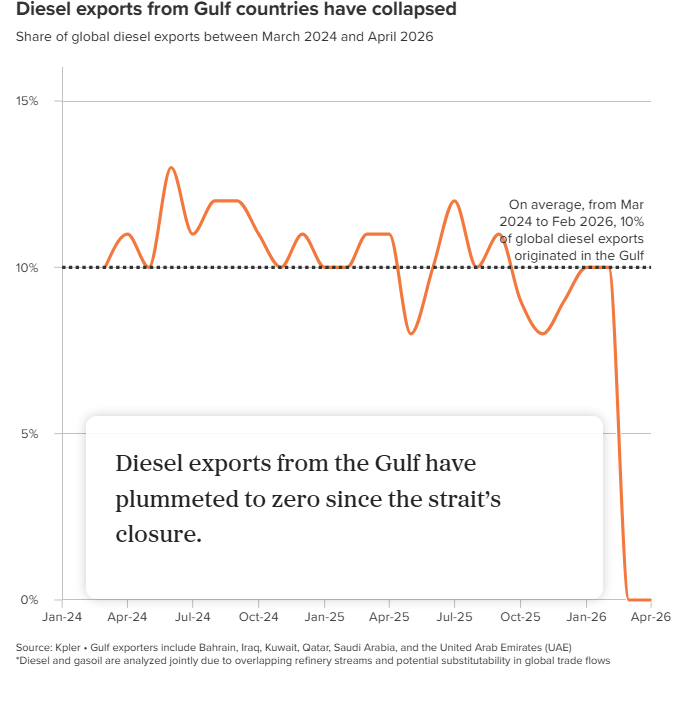

Although limited shipping activity has resumed through the Strait of Hormuz, it remains uncertain how quickly normal export levels can be restored. Even if the passage reopens soon, the broader damage—to infrastructure, refining capacity, and logistics networks—will take far longer to repair, ensuring that the war’s economic aftershocks continue well into the future.

Oil isn’t the only export under threat. The Persian Gulf also supplies large volumes of natural gas liquids, ammonia, urea, and other petrochemical inputs that are vital to global fertilizer production. Prolonged disruptions to these flows could ripple through agricultural supply chains worldwide.

Even a short delay in shipments can trigger cascading effects—tightening fertilizer supplies, reducing crop yields, and driving up food prices months down the line.

In this sense, the war’s impact on oil and fertilizer inputs resembles a slow-building shockwave. For now, the global economy is cushioned by existing inventories and shipments made before the conflict. But as those buffers wear thin, declining exports from the Gulf are likely to place increasing strain on energy markets, food production, and overall economic stability.

The most significant consequences are not in the past—they are only starting to surface.

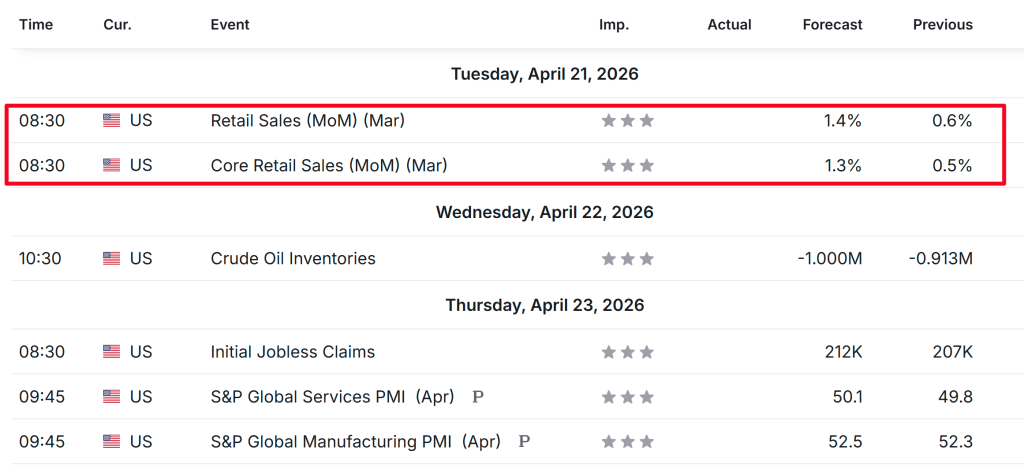

Geopolitical tensions involving Iran, fresh U.S. retail sales figures, and a surge in Q1 earnings reports are set to drive market sentiment in the coming week.

Tesla stands out as a potential buy, supported by improving turnaround momentum and closely watched forward guidance that could reshape investor expectations.

In contrast, Intel appears vulnerable after a strong recent rally, with downside risks emerging from stretched valuations and potential profit-taking.

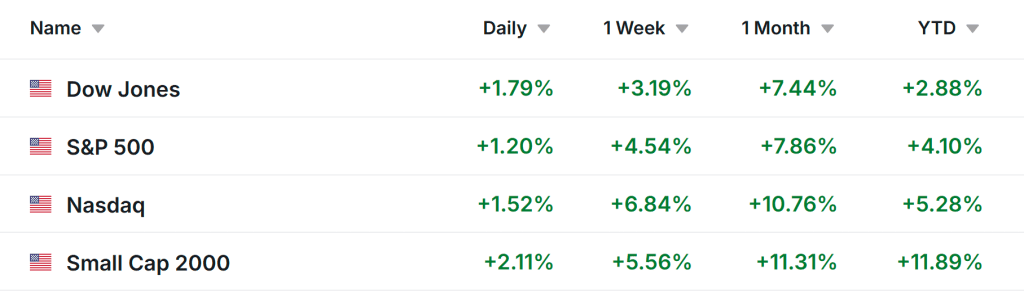

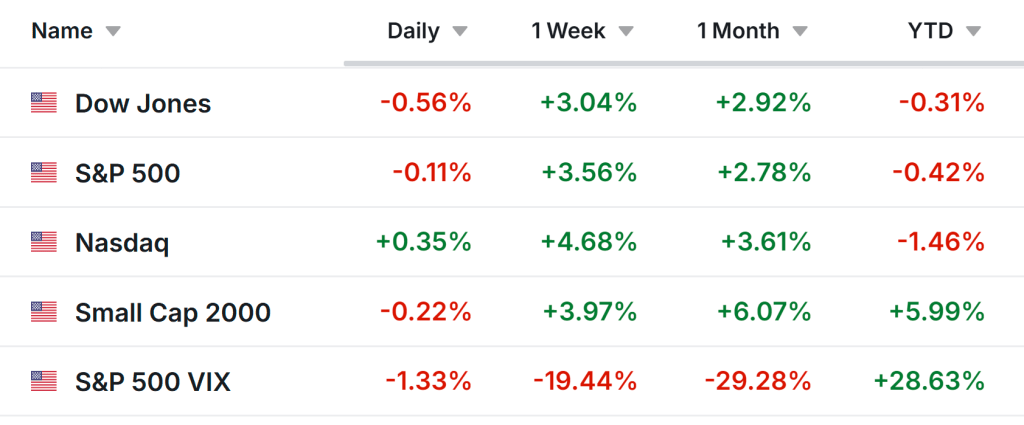

U.S. equities surged on Friday after investors welcomed Iran’s move to reopen the Strait of Hormuz. The S&P 500 and Nasdaq Composite each notched their third consecutive record close, while the blue-chip Dow Jones Industrial Average posted its strongest finish since late February.

For the week, the S&P 500 climbed 4.5%, the Dow Jones Industrial Average advanced 3.2%, the tech-heavy Nasdaq Composite surged 6.8%, and the small-cap Russell 2000 gained 5.6%.

Looking ahead, market focus will once again center on developments in the Middle East and movements in oil prices, after Iran stated on Saturday that the Strait of Hormuz is now “under strict control” by its forces—marking a sharp shift from Friday’s stance.

Potential direct talks between the U.S. and Iran may take place in Pakistan on Monday, although Tehran indicated that no official date has been confirmed. Meanwhile, the current two-week ceasefire is set to expire on Wednesday.

On the economic front, attention will also turn to U.S. data releases, including retail sales, initial jobless claims, and consumer sentiment, in what is expected to be a relatively quiet week for macroeconomic indicators.

The Senate Banking Committee is set to hold a confirmation hearing on Tuesday for Kevin Warsh regarding his nomination as Federal Reserve chair.

At the same time, earnings season is moving into full swing, with several major companies scheduled to report results in the week ahead, including Tesla, Intel, IBM, Boeing, GE Aerospace, UnitedHealth, AT&T, American Express, and United Airlines.

Regardless of how the broader market unfolds, the focus below highlights one stock that appears poised to attract buying interest and another that could face renewed downside pressure. Note that this outlook is strictly short-term, covering the trading week from Monday, April 20 through Friday, April 24.

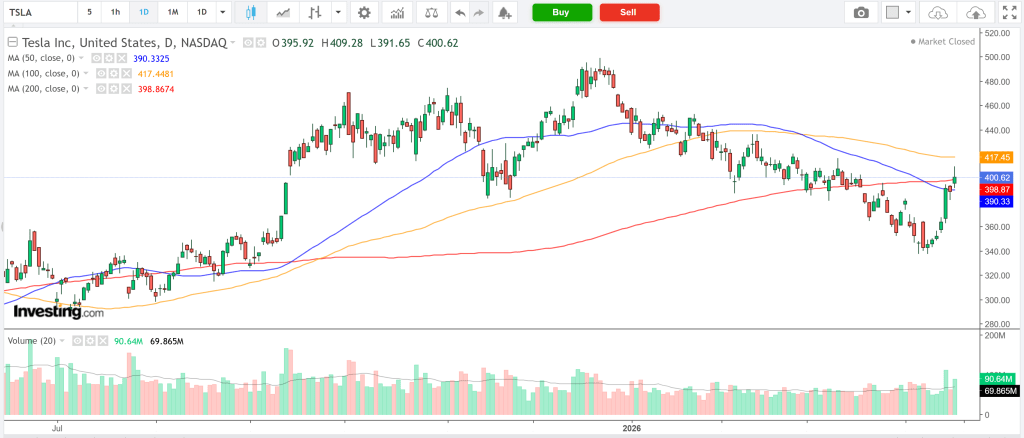

Stock to watch for buying: Tesla

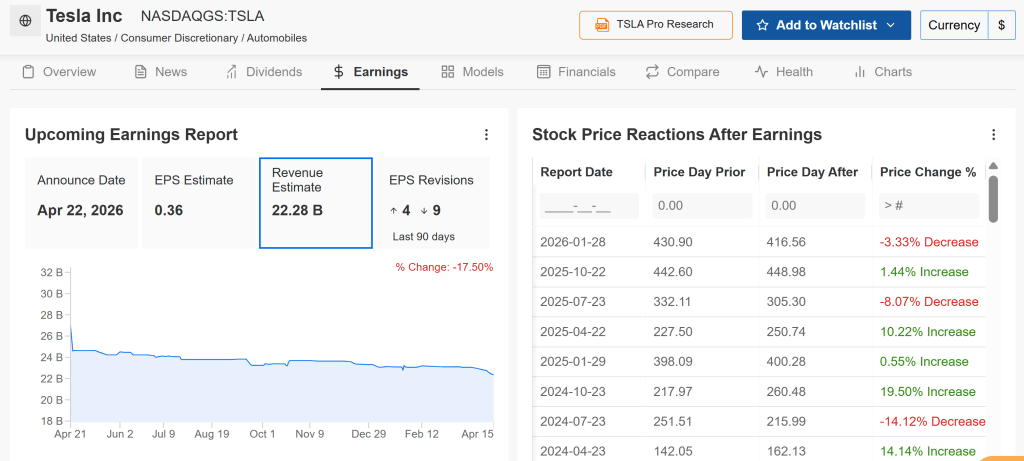

Tesla heads into its Q1 2026 earnings with strong momentum. After breaking a prolonged losing streak, the stock posted its best weekly gain since last May and is now trading close to the $400 level ahead of the announcement.

Options markets are pricing in a move of around 6% following the earnings release—significant, though not unusual for Tesla. If results meet or exceed expectations, accompanied by positive forward guidance and convincing updates on long-term autonomy and product development, the stock could see an even larger upside move as investor sentiment shifts.

Wall Street forecasts adjusted earnings of $0.36 per share, marking an approximate 33% year-over-year increase from a weaker Q1 2025. Revenue is expected to rise 15% to $22.28 billion.

However, the spotlight will be on guidance and strategic commentary from CEO Elon Musk. Investors will closely watch developments in key areas such as the robotaxi initiative, Cybercab production plans, and the rollout timeline for Full Self-Driving technology.

Markets are also paying attention to any updates related to a potential SpaceX IPO and how it might connect to Tesla’s broader ecosystem. Positive signals on this front could further boost bullish sentiment.

As Tesla continues to be valued more as an AI and robotics company rather than purely an EV manufacturer, strong earnings or encouraging autonomy-related updates could drive additional upside.

Trade Setup:

Entry: ~$401

Target: $436 (+8.7%)

Stop-loss: $387 (-3.5%)

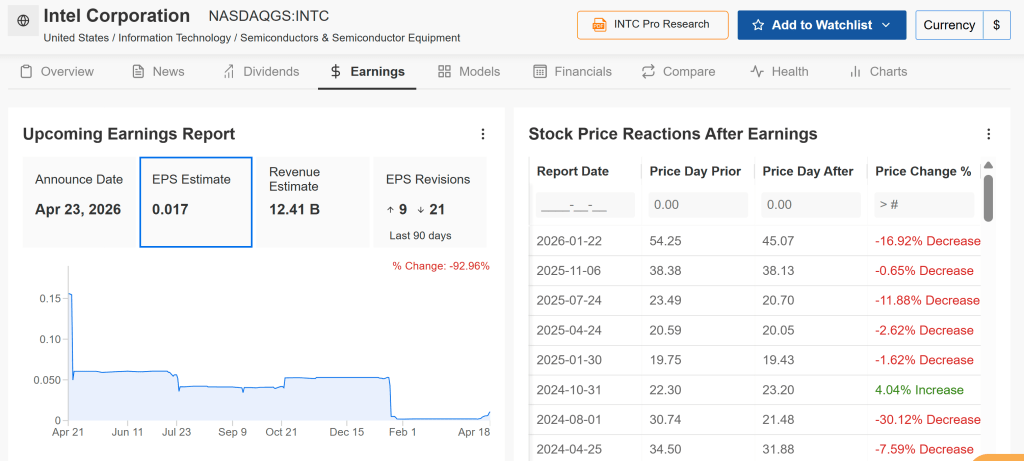

Stock to consider selling: Intel

Intel is heading into a more difficult earnings setup, making it a potential sell or avoid candidate this week. The company is scheduled to report Q1 results on Thursday at 4:00 PM ET, with options markets implying a sizable post-earnings move of around ±9%.

Wall Street expects adjusted earnings per share of roughly $0.02, representing a steep 87% decline compared to the same period last year. Revenue is projected to slip 2% to about $12.4 billion, pressured by ongoing softness in the PC market and continued losses in its foundry segment.

Looking forward, Intel is likely to guide revenue in the $11.7–$12.7 billion range. Despite its widely discussed turnaround strategy, tangible progress remains limited. The foundry business continues to burn cash while facing intense competition from TSMC and Samsung. Meanwhile, its GPU and AI accelerator products have yet to gain meaningful traction in the market.

Although INTC shares have surged about 85% year-to-date in 2026, this strong rally leaves the stock exposed to profit-taking, especially if earnings or guidance disappoint.

From a technical perspective, the RSI stands at an elevated 79.05, signaling overbought conditions. Additionally, declining volume during recent price increases suggests weakening buying momentum as the stock nears resistance in the $70.33–$72.33 range (upper Bollinger Band).

Given the likelihood of underwhelming results and cautious guidance, Intel may present a classic “sell-the-news” scenario. Investors could consider trimming positions ahead of the earnings release.

Silver remained under pressure as rising oil prices—driven by renewed tensions in the Strait of Hormuz—intensified inflation concerns. Meanwhile, Iran accused the U.S. of violating the ceasefire after firing on a commercial vessel and warned of imminent retaliation, while also reversing plans to reopen the strait after Washington refused to lift its blockade on Iranian ports.

Silver (XAG/USD) trimmed losses to trade near $80.50 per ounce in Asian hours, but remained under pressure as a surge in oil prices—driven by renewed Strait of Hormuz tensions—heightened inflation risks and expectations of further rate hikes.

The situation escalated after Iran accused the U.S. of breaching a ceasefire by attacking a commercial vessel, while Washington confirmed seizing an Iranian ship. Tehran also отказed to resume negotiations, reversed its brief plan to reopen the strait after the U.S. maintained its port blockade, and warned of retaliation as geopolitical tensions intensified.

Oil

WTI crude climbed to around $86.70 in early Asian trading, supported by the renewed closure of the Strait of Hormuz, which heightened supply concerns, while Iran warned of imminent retaliation following a U.S. naval seizure.

WTI crude traded near $86.70 in early Asian hours on Monday, supported by escalating U.S.–Iran tensions in the Strait of Hormuz that raised fears of supply disruptions. Iran accused the U.S. of breaching a ceasefire after attacking a commercial vessel and warned of retaliation, while also rejecting new peace talks despite Washington’s push for further negotiations.

Meanwhile, traders are awaiting Tuesday’s API inventory report, with a larger draw likely to support prices and a build potentially weighing on the market.

Bitcoin, the largest cryptocurrency by market value, fell 2.02% to trade at 75,064.2 as of 5:46 ET (10:46 GMT), declining after Iran shut the Strait of Hormuz, which triggered a broader risk-off mood across global markets.

Often described as “digital gold,” the asset has struggled to retain its safe-haven status amid the uncertainty, contributing to a wider crypto sell-off as investors move to reevaluate their portfolio exposure.

Geopolitical pressures and institutional flows

Bitcoin’s recent drop is closely tied to escalating tensions in the Middle East. With the renewed closure of the Strait of Hormuz and rising concerns about a broader regional conflict, global markets have turned cautious, prompting investors to shift capital away from riskier, more volatile assets.

Even so, institutional activity tells a more layered story. Bitcoin ETFs have recently attracted $663.91 million in inflows, lifting total net assets in the segment beyond the $100 billion mark.

At the same time, Ether ETFs recorded $127.49 million in inflows, extending their streak to seven consecutive days and pointing to steady growth in institutional demand.

Wider fund participation also remains visible, as XRP saw $13.74 million in inflows while Solana drew $13.04 million, highlighting continued interest across a range of crypto ETF products.

Industry developments deepen the downturn

Beyond the immediate geopolitical shock, underlying structural challenges within the digital asset space have further weighed on investor sentiment.

Recent reports indicate continued regulatory uncertainty surrounding decentralized finance (DeFi) protocols, dampening enthusiasm across ecosystems like Ethereum and Solana. This lack of clarity has created a feedback loop of caution, indirectly pressuring Bitcoin as investors adopt a more defensive, wait-and-see approach.

The cautious mood is reinforced by thin market conditions. Data shows a noticeable decline in stablecoin liquidity across major centralized exchanges, reducing depth in order books. In such an environment, price swings tend to be more pronounced, leaving Bitcoin increasingly exposed to sharp drops and forced liquidations during periods of heightened stress.

Adding to the pressure, persistent inflation concerns and evolving interest rate expectations continue to weigh on risk assets. With yields on safer instruments remaining relatively high, the opportunity cost of holding non-yielding assets like Bitcoin increases, discouraging the kind of aggressive accumulation that previously supported its upward momentum.

Crypto prices today: altcoins decline after Strait closure

Altcoins also moved lower following Iran’s announcement, mirroring the broader market downturn triggered by renewed geopolitical tensions.

Ethereum, the second-largest cryptocurrency, dropped 2.89% to $2,307.42, while XRP, ranked third, fell 2.12% to $1.4198.

Meanwhile, Solana and Cardano recorded steeper losses of 3.40% and 3.54%, respectively.

Among meme coins, Dogecoin slid 3.40%, reflecting widespread weakness across the altcoin segment.

The U.S. dollar climbed to a one-week high against major currencies on Monday, as renewed tensions between the U.S. and Iran and fading hopes for a Middle East peace agreement pushed investors toward safe-haven assets.

Washington said it had seized an Iranian cargo vessel attempting to breach its blockade, while Tehran vowed retaliation, raising fears that hostilities could flare up again. Iran also announced it would not join a second round of talks the U.S. had aimed to begin before a two-week ceasefire expires on Tuesday.

According to Charu Chanana, chief investment strategist at Saxo, the weekend escalation has brought geopolitical risk back into focus just as markets had begun to price in a potential peace dividend. She added that rising oil prices are not only an energy concern but also have broader implications for economic growth and interest rates.

The euro slipped 0.14% to $1.1746, while the British pound dropped 0.29% to $1.3479. The Australian dollar, often seen as a risk-sensitive currency, declined 0.3% to $0.7145 in early trading.

The U.S. dollar index, which tracks the currency against six major peers, stood at 98.38, near a one-week high and recovering some recent losses. Despite this rebound, the index remains down 1.5% for April, as improving risk sentiment earlier in the month had weighed on the dollar. In contrast, it surged 2.3% in March amid strong safe-haven demand following the outbreak of war.

Barclays analysts noted that investor sentiment still favors the dollar, suggesting there may be room for further downside if Middle East tensions ease. They added that any short-term market volatility could present opportunities to rebuild short dollar positions, though uncertainty remains high.

Now in its eighth week, the conflict has triggered one of the most severe disruptions to global energy supply, driving oil prices sharply higher due to the effective closure of the Strait of Hormuz, a key route for roughly 20% of global oil shipments.

The U.S. has continued its blockade of Iranian ports, while Iran has alternated between lifting and reimposing restrictions on shipping through the strategic waterway. This uncertainty pushed oil prices higher on Monday, with Brent crude rising 7% to $96.8 per barrel and U.S. West Texas Intermediate gaining over 8% to $90.74.

Nick Twidale, chief market strategist at ATFX Global in Sydney, said the Strait of Hormuz remains the central concern, and hopes for renewed negotiations before the ceasefire ends now appear unlikely. He expects risk assets to face further downward pressure in the near term.

Elsewhere, the New Zealand dollar edged down slightly to $0.5876, while the Japanese yen weakened to 159.06 per dollar, approaching the key 160 level that could prompt intervention by authorities.

Attention is also turning to the Bank of Japan’s upcoming meeting later this month. Governor Kazuo Ueda has avoided firmly signaling an April rate hike due to uncertainty from the conflict but hinted at a more hawkish stance following last week’s IMF meetings, leaving open the possibility of policy tightening by June.

In cryptocurrency markets, bitcoin fell 0.56% to $74,229.65, while ether declined 0.2% to $2,276.04.

Gold continues to trade in a narrow range below the $4,800 mark early Friday, failing for a third straight day to hold above that level. Market participants remain cautious as they await clearer direction from upcoming US–Iran peace talks, while the metal still looks set for a fourth consecutive weekly gain.

Fundamental Overview

With the two-week US–Iran ceasefire set to expire on April 22, uncertainty around both the timing and outcome of the next round of negotiations continues to unsettle investors, keeping Gold prices fluctuating within a familiar range.

Upside momentum in Gold remains limited, pressured by the recent rebound in Oil prices amid ongoing concerns about supply disruptions tied to the US naval blockade of the Strait of Hormuz. Higher Oil prices have revived inflation fears, reinforcing expectations that major central banks—including the US Federal Reserve (Fed)—may maintain a tighter monetary policy stance.

Late Thursday, the US Central Command (CENTCOM) stated that the USS Abraham Lincoln is operating in the Arabian Sea as part of a large-scale enforcement of the blockade on Iranian ports, involving more than a dozen ships, over 100 aircraft, and around 10,000 personnel, with no reported violations so far.

Meanwhile, a modest rebound in the US Dollar from near six-week lows is adding further pressure on USD-denominated Gold.

That said, downside risks for the precious metal appear limited. A newly announced 10-day ceasefire between Israel and Lebanon has lifted hopes for a near-term de-escalation in the Middle East, reducing safe-haven demand for the US Dollar and offering some support to Gold.

Heading into the weekend, Gold remains directionless and highly sensitive to developments on the Middle East front. Thin end-of-week flows could also amplify price swings, especially amid lingering uncertainty over US–Iran negotiations and the durability of the Israel–Lebanon truce.

From a technical perspective, the daily chart setup adds another layer of intrigue, keeping traders focused on both geopolitical headlines and key chart signals for the next move.

XAU/USD Technical Overview

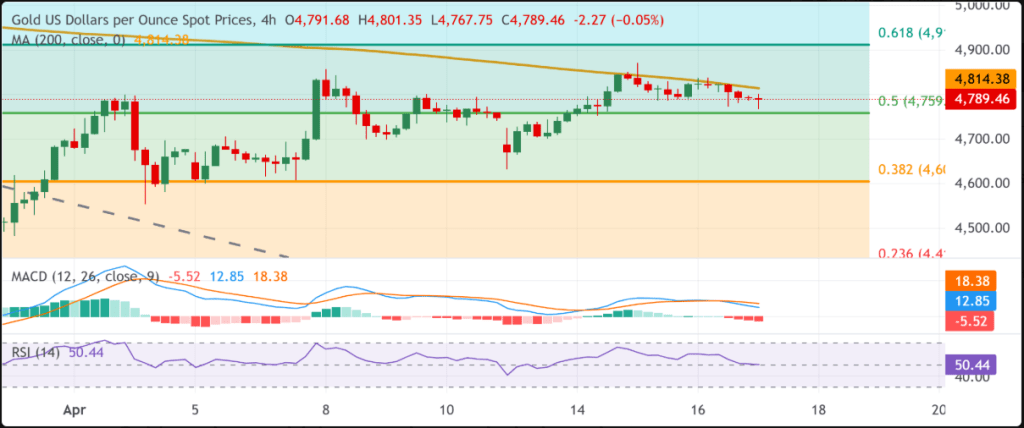

On the daily chart, XAU/USD is trading around $4,789.50, with price action confined between key support levels and overhead resistance. The metal remains supported above the 21-day and 100-day SMAs, near $4,646 and $4,715 respectively, but continues to struggle below the 50-day SMA at $4,897 and a descending trendline resistance around $4,792. The Relative Strength Index (14), hovering near 51, points to neutral momentum with a slight bullish tilt, indicating consolidation rather than a clear breakout as price lingers just beneath trend resistance.

At the same time, bearish signals persist in the background. A Bear Cross between the 21-day and 100-day SMAs confirmed on April 13, along with a similar crossover seen on March 25, continues to weigh on bullish prospects.

Looking higher, immediate resistance is seen at the descending trendline near $4,792. A decisive daily close above this level could pave the way toward the 50-day SMA at $4,897 as the next upside target. On the downside, initial support lies at the 100-day SMA around $4,715, followed by a broader ascending trendline zone in the mid-$4,500s, which reinforces demand ahead of the 21-day SMA near $4,646. Only a sustained break below these support layers would expose the longer-term 200-day SMA near $4,215.

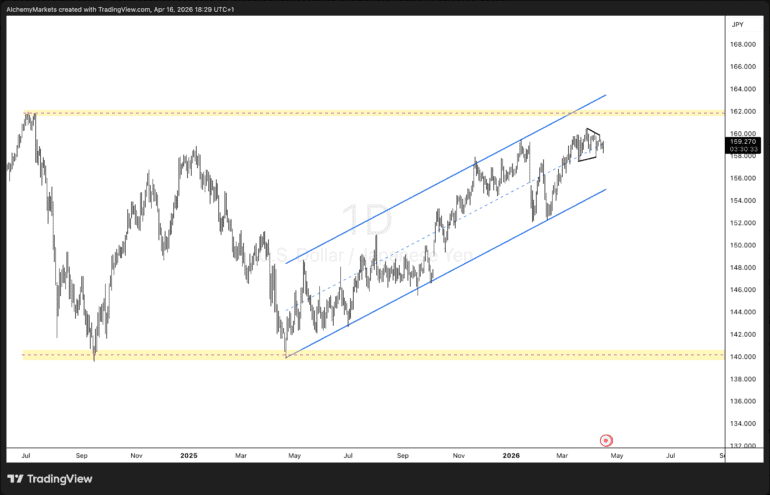

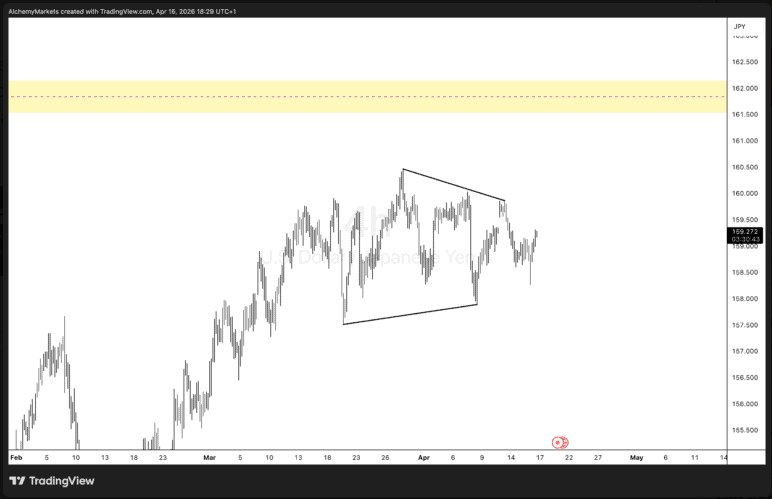

USD/JPY remains confined within a well-defined ascending channel on the higher timeframe, preserving a strong bullish structure. The pair continues to post higher highs and higher lows, indicating that buyers are still firmly in control.

Attention now shifts to the 162.00 level, a key resistance zone that has previously limited upward moves. As price approaches this area once again, the setup points toward a possible breakout.

On the lower timeframe, price action is forming a tight triangle pattern, reflecting short-term consolidation and indecision. Such formations often precede a surge in volatility.

Given the prevailing uptrend, the bias favors an upside break. A decisive move above the triangle resistance could spark fresh momentum, paving the way toward the 162.00 barrier.

Key takeaway:

USD/JPY is consolidating within a triangle while maintaining a broader uptrend. A breakout to the upside would likely target 162.00, while in the meantime, price may remain compressed—but not indefinitely.

Easing tensions in the Middle East have weakened the dollar.

Meanwhile, the Bank of England is guiding rate expectations, keeping the prospect of two hikes intact.

Over the past two weeks, the US dollar has slid to its weakest level since early March, erasing nearly all the gains recorded at the onset of the Middle East conflict. With talks involving Iran expected to resume soon, and Donald Trump maintaining that the war will end shortly without the need for a ceasefire extension, geopolitical support for the greenback has faded. Alongside record highs in US equity indices, this shift has helped sustain the EUR/USD rally, as macroeconomic factors regain prominence.

At the same time, investor focus has turned toward corporate earnings and Congressional discussions over Kevin Warsh’s potential appointment as Fed Chair. Despite Trump’s assurances, a leadership change at the Fed could coincide with rising inflation driven by higher oil prices, potentially necessitating tighter monetary policy. The key question remains whether Warsh would align with the president’s stance or uphold the Fed’s independence.

Some investors are drawing comparisons to the 1970s, when an oil-driven inflation shock prompted a Fed Chair aligned with the White House to loosen policy. That decision fueled even higher inflation and entrenched expectations, leading to a sharp decline in the US dollar. Only after a change in leadership and aggressive rate hikes—despite a recession—did the dollar begin a sustained recovery from mid-1980 onward.

Potential currency interventions may also weigh on the dollar. Japan’s Finance Minister, Satsuko Katayama, has long advocated selling USD/JPY, and her rhetoric has intensified following talks with Scott Bessent. This hints that the US may be open to coordinated action in the FX market, reminiscent of the 1985 interventions that triggered a prolonged decline in the dollar.

Meanwhile, other European currencies are advancing alongside the euro. The British pound has climbed back to pre-war levels, supported in part by the Bank of England’s hawkish tone. Megan Green has backed market expectations of two rate hikes in 2026, while Andrew Bailey suggested earlier projections of four hikes were excessive.

The US Dollar Index trades sideways near 98.25 during Friday’s Asian session.

Donald Trump signals optimism over a potential peace agreement with Iran.

Meanwhile, markets anticipate that interest rates will remain unchanged throughout the year.

The US Dollar Index (DXY), which tracks the US Dollar against a basket of six major currencies, is hovering around 98.25 during Friday’s Asian session. The index remains largely unchanged as uncertainty persists over the Israel–Lebanon ceasefire. Investors are also looking ahead to potential US–Iran talks this weekend for clearer direction.

A 10-day ceasefire between Lebanon and Israel came into force on Thursday, but tensions in the region remain elevated, supporting demand for safe-haven assets like the US Dollar. On Friday, the Lebanese army accused Israel of breaching the truce, citing sporadic shelling in several southern villages.

At the same time, optimism surrounding a US–Iran ceasefire could limit further gains in the Dollar. A temporary two-week agreement is currently in place and is set to expire next week. US President Donald Trump indicated that the next round of discussions between Washington and Tehran could happen over the weekend.

According to Sim Moh Siong, FX strategist at OCBC, markets are currently consolidating after pricing in earlier optimism about a ceasefire extension. He noted that a new catalyst will be needed to drive clearer directional moves, as the Dollar’s trajectory is no longer one-sided.

Meanwhile, traders are closely monitoring how Federal Reserve officials will respond to inflation risks stemming from the conflict. Fed funds futures suggest that markets still expect the central bank to keep interest rates unchanged this year, Reuters reported.

Gold stays under pressure but lacks strong follow-through selling amid mixed signals. The US dollar finds support from ongoing Hormuz-related risks, acting as a headwind for the metal. However, optimism over Iran diplomacy and easing expectations for Fed rate hikes help cap the dollar, providing some support to bullion.

Gold (XAU/USD) trims its earlier losses from the Asian session, rebounding from the $4,768–$4,767 area—a three-day low—but struggles to build momentum and stays below the $4,800 level amid mixed signals. While diplomatic efforts to resolve the Middle East conflict are intensifying, lingering tensions between the US and Iran, particularly due to the ongoing US naval blockade of Iranian ports, continue to support the US Dollar’s safe-haven appeal and weigh on the metal.

At the same time, a 10-day ceasefire between Israel and Lebanon has raised hopes for a broader US-Iran agreement. US President Donald Trump struck an upbeat tone, suggesting Iran is close to a deal, and reports indicate both sides have agreed in principle to resume talks, though details remain undecided. These developments support a more positive market mood, which, alongside reduced expectations of further Federal Reserve rate hikes, limits the USD’s rebound from recent lows and helps cushion Gold’s downside.

Earlier in the week, US Producer Price Index (PPI) data eased concerns about inflation stemming from rising energy costs linked to the conflict. Additionally, expectations of easing geopolitical tensions have kept Crude Oil prices subdued, softening hawkish Fed expectations. Markets are now pricing in about a 30% chance of a Fed rate cut by year-end, restraining USD strength and providing support for non-yielding assets like Gold. As such, traders may prefer to wait for stronger selling pressure before anticipating a deeper pullback from the recent one-month high.

Looking ahead, the absence of key US economic data on Friday leaves the USD influenced by speeches from FOMC members. However, attention will remain focused on potential US-Iran talks over the weekend, with headlines likely to drive volatility and create trading opportunities in Gold. Despite recent fluctuations, XAU/USD is still on track for modest gains for a third consecutive week.

Gold H4 chart

From a technical standpoint, the failure to break above the 200-period SMA on the 4-hour chart overnight signals a note of caution for bullish traders. Although prices pulled back afterward, the decline found support ahead of the 50% retracement of the March drop, suggesting that traders may prefer to wait for a decisive move below the $4,765 support area before anticipating deeper losses.

Momentum indicators offer a mixed picture. The RSI is hovering around the neutral 50 level, while the MACD remains below the zero line in negative territory, indicating that sellers still hold a near-term edge. For sentiment to improve, price would need to reclaim the 200-period SMA near $4,814, followed by a stronger resistance at the 61.8% Fibonacci retracement around $4,912. A sustained breakout above these levels could shift the outlook more positively and pave the way toward $5,130 and $5,409.