The U.S. dollar paused on Wednesday as softer crude oil prices helped revive some risk appetite ahead of a series of major central bank decisions.

The yen remained fragile near levels that have previously raised concerns about possible intervention by Tokyo, especially with Japanese Prime Minister Sanae Takaichi set to meet U.S. President Donald Trump in Washington. Meanwhile, the euro slipped slightly after two sessions of gains, as the European Central Bank prepared to kick off its two-day policy meeting.

Amid the ongoing Middle East crisis, now in its third week, the dollar has strengthened as the primary safe-haven currency. However, oil prices edged lower after data from the American Petroleum Institute indicated a rise in U.S. crude inventories.

According to Hirofumi Suzuki, chief FX strategist at Sumitomo Mitsui Banking Corporation, while the pause in oil’s rally hasn’t dramatically improved conditions, markets are showing signs of stabilization. He noted that USD/JPY has moved modestly in favor of yen strength.

The dollar index rose slightly by 0.06% to 99.61 following a two-day decline, while the euro dipped 0.05% to $1.1532. The yen weakened marginally to 159 per dollar, and sterling remained steady at $1.3355.

The greenback had surged to a 10-month high late last week, driven by geopolitical tensions and rising oil prices that pushed investors toward safer U.S. assets.

Highlighting the broader impact of the crisis, Trump announced he would delay a planned trip to Beijing to meet Chinese President Xi Jinping. Takaichi is expected to leave for Washington later Wednesday.

Analysts at Mizuho Securities noted that even if the conflict drags on, equities could rebound, supporting commodity-linked currencies like the Australian dollar, as well as currencies of oil-importing nations such as the yen and euro. However, they expect limited downside for USD/JPY, partly due to the Japanese government’s preference for a weaker yen.

Attention now turns to central banks, with the Federal Reserve set to announce its decision Wednesday, followed by the ECB, Bank of England, and Bank of Japan a day later. All are widely expected to hold rates steady, though markets will closely watch their outlooks on inflation and growth amid geopolitical uncertainty.

Expectations for Fed rate cuts have been trimmed to around 25 basis points this year. Meanwhile, traders are now pricing in more than one ECB rate hike in 2026—a notable shift from earlier expectations of potential cuts.

Elsewhere, the Australian dollar gained 0.1% to $0.7109, and the New Zealand dollar rose 0.05% to $0.586. In crypto markets, bitcoin slipped 0.40% to $74,257.80, while Ethereum edged up 0.22% to $2,333.60.

For investors aiming to build reliable passive income and long-term wealth, dividend stocks continue to stand out as some of the most dependable assets. Among the most consistently favored names are The Coca-Cola Company and Walmart Inc..

Both companies belong to the elite group known as Dividend Kings — firms that have increased their dividends for at least 50 consecutive years. Their proven resilience and steady growth make them particularly attractive for long-term investors. Whether constructing a retirement portfolio or seeking stable income-generating holdings, these two consumer giants remain strong candidates.

Coca-Cola and Walmart: Enduring Dividend Leaders

Coca-Cola has delivered 63 straight years of dividend increases, reinforcing its reputation as a cornerstone income stock. It currently offers a yield of around 2.65%, supported by solid price performance, with shares up more than 10% year-to-date and over 77% in the past five years.

Its strength lies beyond dividends. With a portfolio of 32 billion-dollar brands, a deeply loyal global customer base, and a localized production strategy that helps mitigate tariff pressures, Coca-Cola continues to maintain a competitive edge that investors value.

Walmart, on the other hand, has raised its dividend for 53 consecutive years and operates the world’s largest retail network, spanning over 5,000 stores in the U.S. and nearly 11,000 globally. While its dividend yield is lower at roughly 0.79%, its total return profile is exceptional — the stock has surged more than 200% over five years, far outpacing the S&P 500.

Importantly, Walmart’s growth is no longer tied solely to its physical stores. Its e-commerce division expanded 24% year-over-year in fiscal Q4 2026, while its Walmart+ subscription service continues to grow, adding a high-margin recurring revenue stream.

Both companies operate within the consumer defensive sector, meaning demand for their products remains stable regardless of economic conditions. Essentials like food, beverages, and household goods are always needed, making these businesses naturally resilient. Combined with decades of disciplined dividend growth, this stability underpins their role as long-term portfolio anchors.

Stock Snapshot: Performance and Market Outlook

As of mid-March 2026, Coca-Cola trades at $77.49 with a market capitalization of roughly $333 billion. It has a trailing P/E ratio of 25.49 and generated $3.04 in earnings per share over the past year, consistently exceeding analyst expectations. The company also boasts a strong return on equity of over 43%, alongside annual revenue nearing $48 billion and profit margins above 27%.

Analyst sentiment remains positive, with an average price target of $83.36. Notably, Barclays recently raised its target to $83 while maintaining an overweight rating.

Walmart trades around $126.07, with a market value exceeding $1 trillion. Its higher P/E ratio of 46.17 reflects the premium investors are willing to pay for its consistent growth and execution.

Over the past 12 months, Walmart generated more than $713 billion in revenue and nearly $22 billion in net income, along with strong free cash flow of $7.77 billion — supporting both dividend increases and ongoing investments.

Analysts remain optimistic. Mizuho Financial Group rates the stock as outperform, while Tigress Financial Partners recently lifted its price target to $150.

Overall, both stocks demonstrate not only dependable income potential but also strong capital appreciation. Coca-Cola has outperformed the broader market so far in 2026, while Walmart’s nearly 202% five-year gain highlights its ability to generate superior long-term returns. Investors holding these names benefit from a powerful combination of rising dividends and sustained growth that often matches or exceeds market benchmarks.

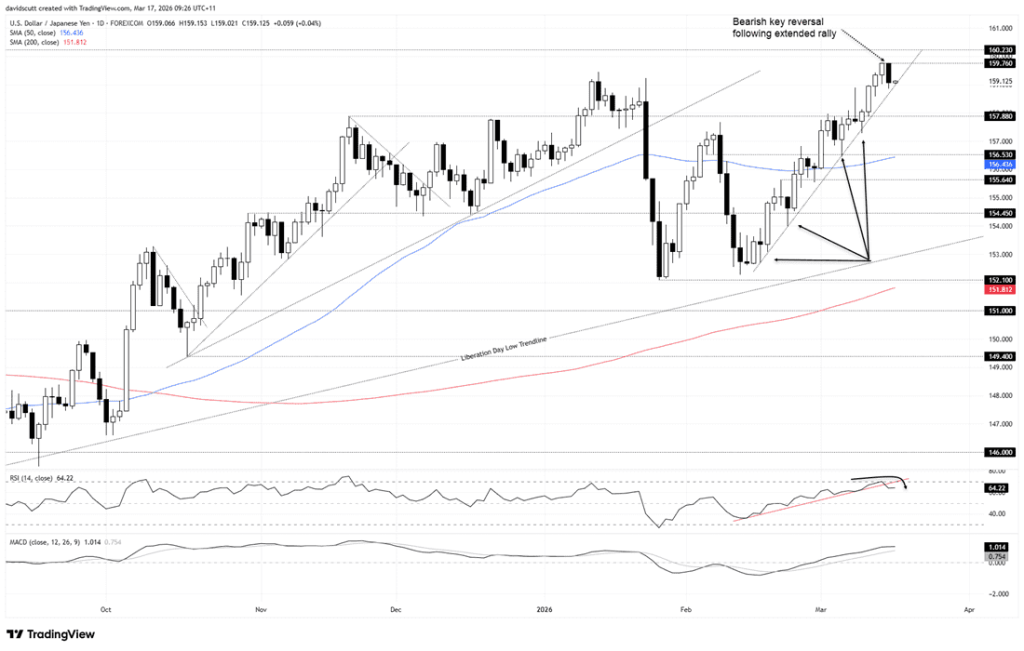

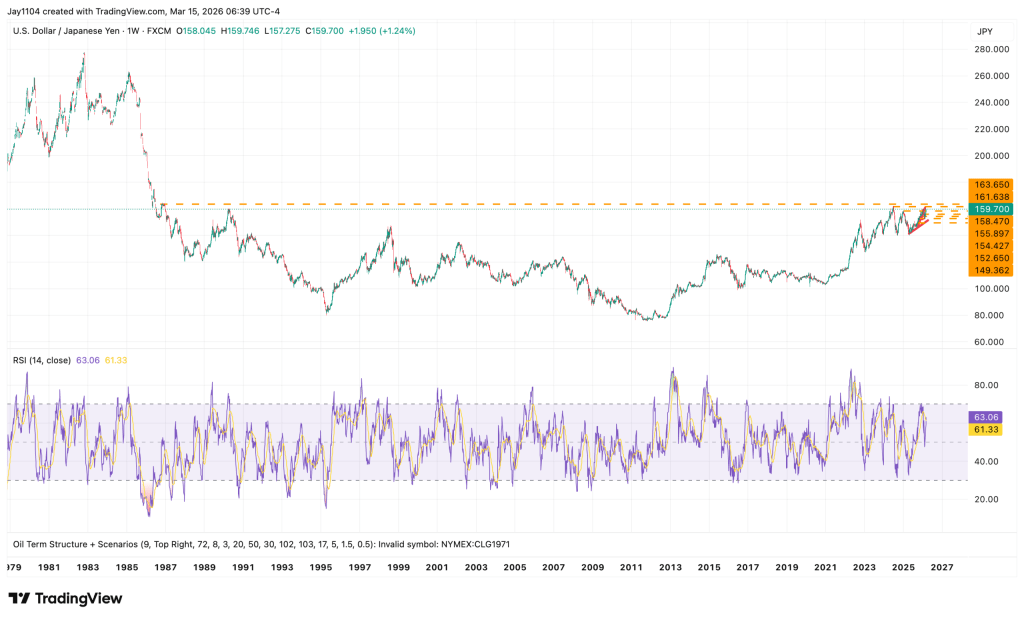

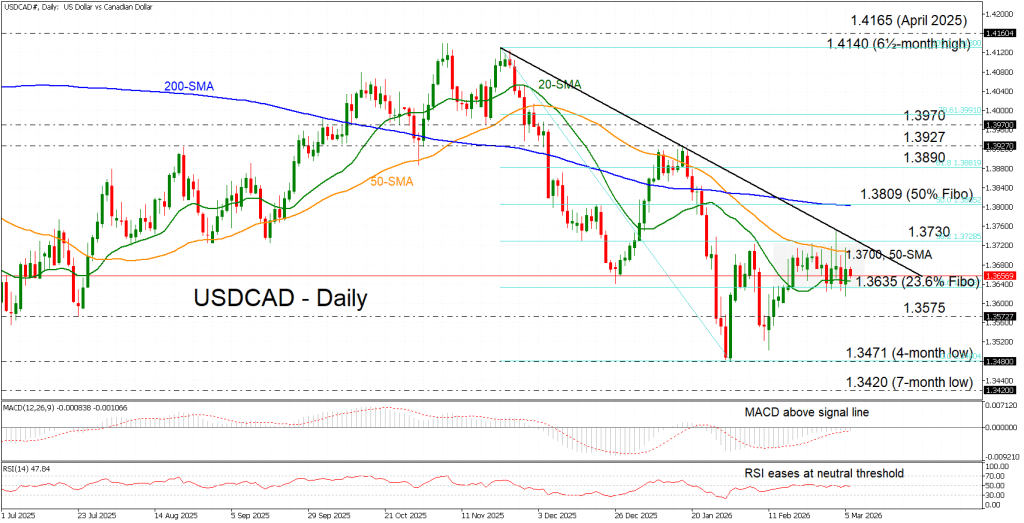

USD/JPY’s recent dip has left it caught between firm uptrend support and growing concerns about potential intervention as it approaches the 160 mark. Traders now face a key question: does this bearish signal point to a deeper correction, or is it merely a temporary pause in the broader rally?

Pullback brings USD/JPY toward key support around 159

Intervention fears resurface near the 160 threshold

Attention shifts to the RBA decision and upcoming JGB auction

Reversal Highlights Tension Within the Uptrend

USD/JPY fell sharply on Monday, though the drivers behind the move were not particularly compelling.

The decline coincided with a sudden pullback in the US dollar and a drop in Treasury yields, despite a lack of meaningful new macro developments. At the same time, crude oil prices reversed earlier gains even as no additional countries committed to joining the United States in protecting tanker routes through the Strait of Hormuz. Given how energy supply concerns have recently underpinned the dollar, this suggests the move was more about positioning adjustments than a shift in the broader macro outlook.

For USD/JPY, the timing stands out. Japan’s finance minister, Satsuki Katayama, signaled readiness to take “decisive action” to curb excessive currency volatility as the pair neared 160. Considering Japan’s track record of intervening or conducting rate checks around this level, such remarks likely prompted traders to scale back long positions, accelerating the pullback.

A single bearish reversal candle is rarely enough to shift the narrative—especially when it appears without a clear fundamental catalyst. Without follow-through selling, Monday’s move in USD/JPY is more likely to be seen as a pause rather than confirmation of a broader trend reversal.

Technically, the pair is at a crossroads.

USD/JPY is now testing uptrend support drawn from the January lows, while hovering just above the 159.00 zone—a level that previously acted as strong resistance before being broken last week.

At the same time, momentum is starting to fade. The RSI (14) has broken its upward trajectory, and the MACD is flattening and drifting back toward its signal line after a prolonged climb. When this kind of momentum deterioration shows up at key support, it typically forces a decisive move.

So the setup boils down to two scenarios:

A continuation of selling that breaks trend support, opening the door for a deeper pullback toward 157.88

Or a defense of the uptrend, despite rising risks of Japanese intervention as price nears the psychologically important 160 level

Recent price action has largely been driven by sentiment around energy supply disruptions. The United States benefits from relative energy independence, while Japan—heavily reliant on imports—tends to see its currency weaken when oil prices surge. However, Monday’s reversal in crude oil hints that this geopolitical tailwind for the dollar may be fading.

Macro catalysts could now take the lead.

The upcoming policy decision from the Reserve Bank of Australia (RBA) may influence broader G10 currency flows. Markets are pricing only about a 62% chance of a 25bps hike, but if delivered, it would reinforce the divergence between a potentially easing Federal Reserve and other central banks that may still tighten—potentially pressuring the US dollar.

On the flip side, if the RBA holds rates steady, it could signal broader caution among central banks, which may end up supporting the dollar instead.

Bond markets also matter here.

20-year government bond auctions in both Japan and the US could offer additional clues. Demand for Japanese government bonds is particularly important—weak demand may reignite yen weakness, while strong bidding could stabilize sentiment and lend support to the currency.

In short, USD/JPY is no longer just a technical story. It’s sitting at the intersection of fading momentum, intervention risk, and shifting macro drivers—making the next move especially pivotal.

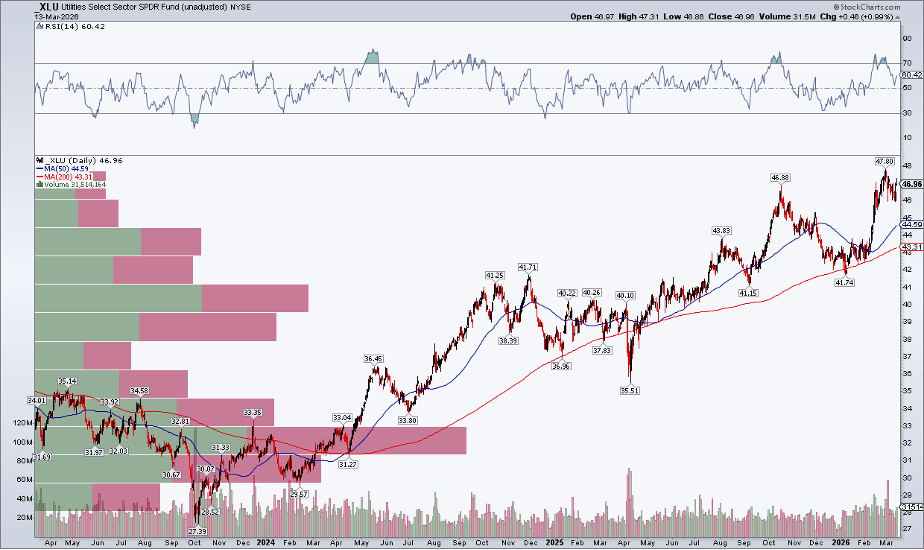

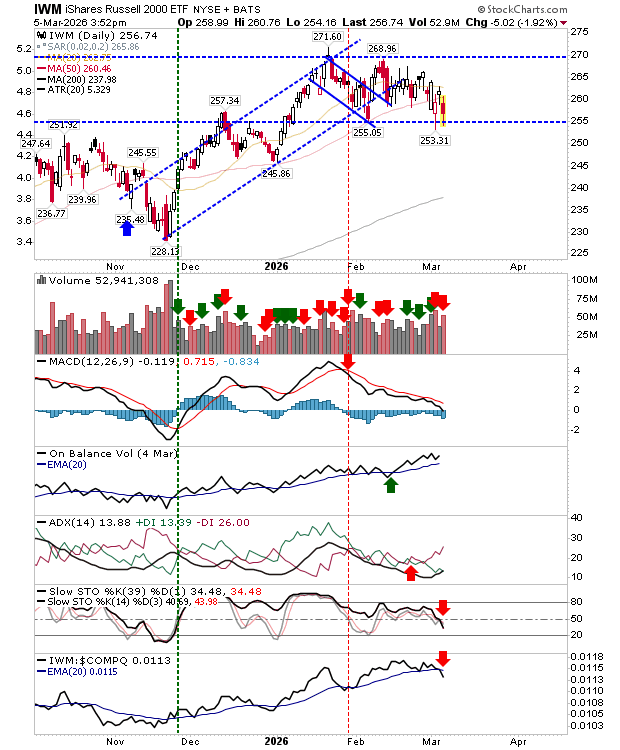

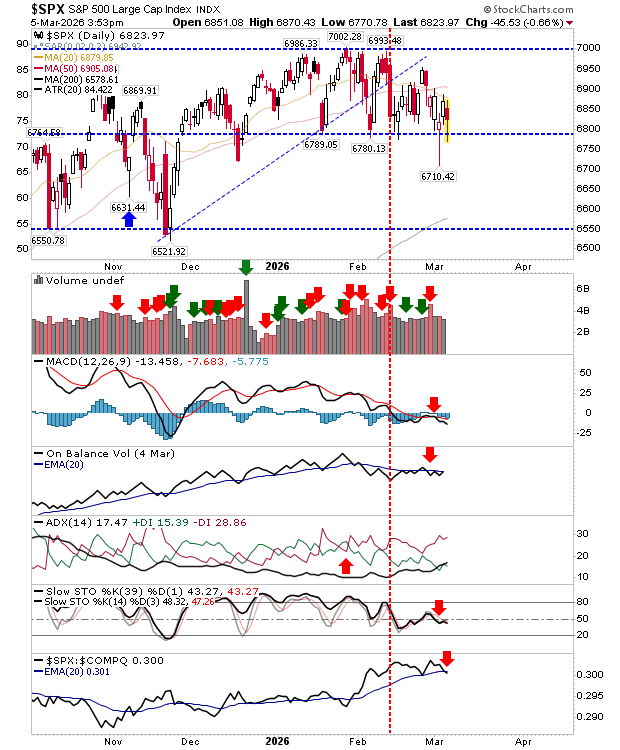

Utilities are outperforming the S&P 500, signaling growing investor demand for defensive positioning.

Consumer Staples and Health Care present mixed signals as traders evaluate potential rotation into risk-off sectors.

Tracking both absolute and relative sector strength can offer insight into broader market risk.

It’s March Madness on Wall Street: the VIX remains in the mid-20s, WTI crude oil has climbed back to $100, and bearish momentum continues to build. With “defense wins championships” in mind, traders may be weighing whether bracing for further downside is the prudent strategy.

In that context, sector analysis deserves a spot in your playbook. Within the 11 S&P 500 sectors, Utilities, Consumer Staples, Health Care, and Real Estate are typically viewed as less cyclical, lower-growth, defensive areas. Together, they account for about 18.5% of the index (under 10% excluding Health Care). From a portfolio standpoint, shifting heavily into these sectors represents a meaningful active bet. If sentiment flips and bulls regain control, a sharp rebound could quickly punish defensive positioning.

Even so, opportunities may lie beyond the high-growth “headline” sectors. Let’s take a closer look.

Utilities Gaining Momentum

Starting with Utilities (XLU), it’s useful to assess both absolute and relative price action. The sector ETF remains firmly in an uptrend.

As shown in the chart, a pattern of higher highs and higher lows has persisted since September 2023. The upward-sloping 200-day moving average indicates that bulls still dominate the primary trend. Meanwhile, the RSI momentum indicator has frequently reached overbought territory—often a sign of strength rather than weakness. In short, XLU continues to show strong upside momentum.

XLU remains in a strong uptrend and is trading near record highs.

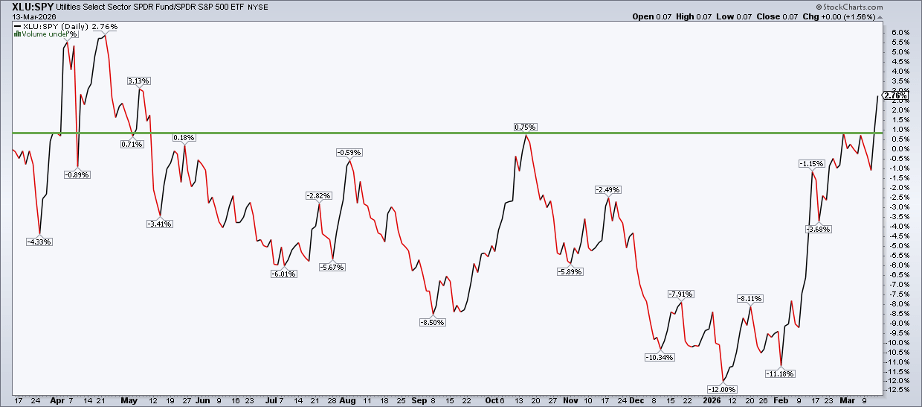

But how does it compare to the S&P 500 ETF (SPY)?

To check, enter “XLU:SPY” in the SharpCharts symbol box (or “_XLU:_SPY” for a price-only view). As of last Friday, the ratio hit its highest level since May 2025, breaking above key resistance.

In short, relative strength is shifting toward Utilities, which implies a more bearish tilt for the broader S&P 500.

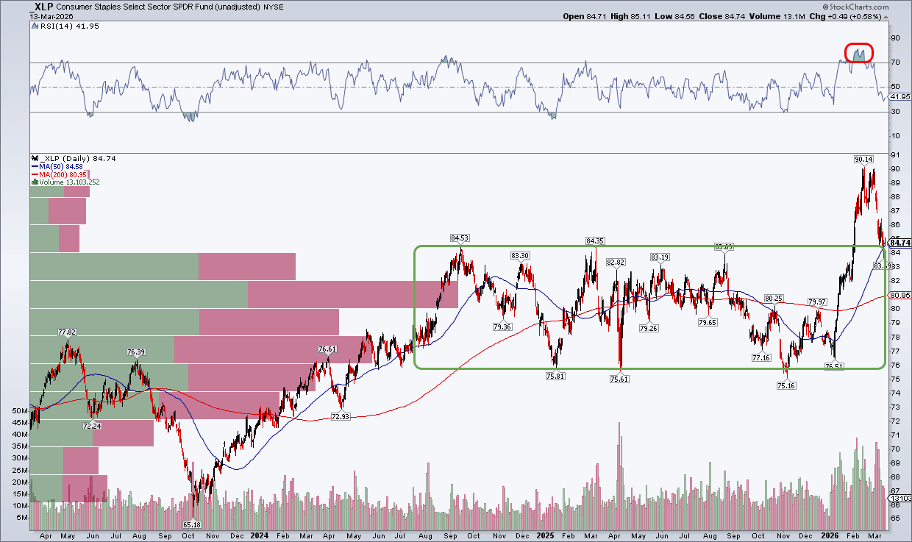

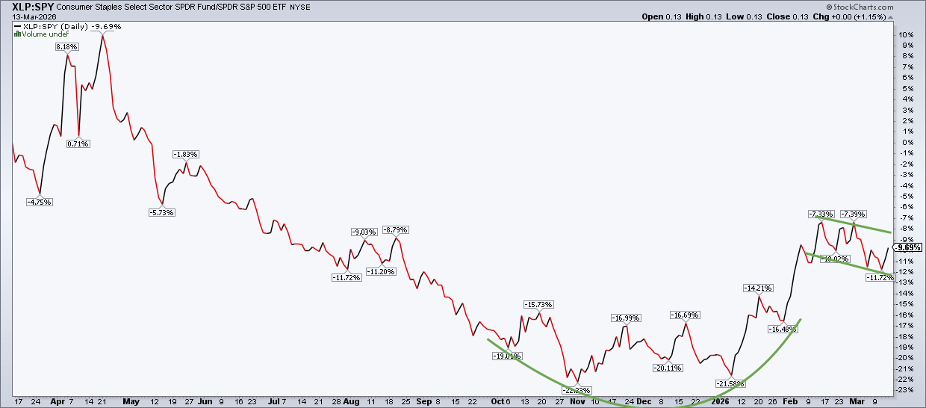

Staples Near a Crucial Support Zone

Looking at Consumer Staples (XLP), the price trend is less decisive. The ETF is edging closer to correction territory, pulling back toward key support around $84 and its 50-day moving average. Given the strong volume-by-price concentration in the mid-$80s, there’s an expectation buyers may step in at this level. The coming weeks will be pivotal.

Similarly, the XLP:SPY ratio is not as well-defined as XLU:SPY. It formed a rounded bottom around the start of the year and has since moved into a consolidation phase—potentially a bull flag.

From a technical perspective, consolidations typically break in the direction of the broader trend—which is upward here. That suggests XLP could maintain support near $84 and resume outperforming the S&P 500 in the weeks and months ahead.

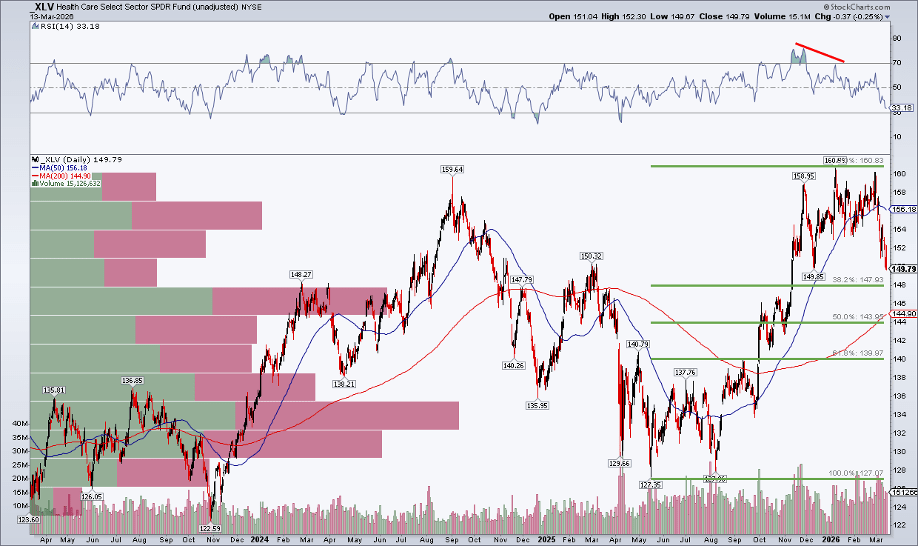

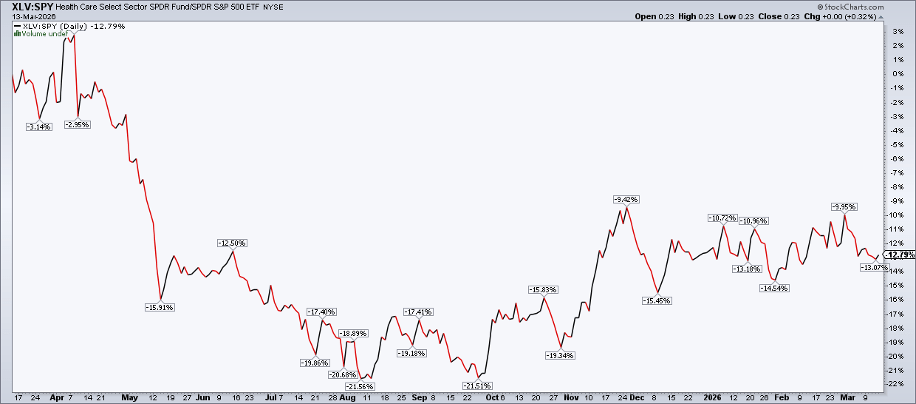

Health Care Still on the Sidelines

Turning to Health Care (XLV), the chart shows a clear bearish double top, with sellers stepping in twice around the $160 level—first in Q3 2024 and again more recently over an extended period.

The sector, which includes defensive pharmaceutical firms, somewhat cyclical medical device makers, and higher-risk biotech names, has seen its RSI drop to its weakest level since just after Liberation Day. Meanwhile, the rising 200-day moving average sits only a few percentage points below the current price. In addition, after breaking below an upward trendline, the next key level to watch is the 38.2% Fibonacci retracement near $148.

Overall, XLV looks better left on the sidelines for now.

XLV:SPY lacks a compelling setup. The sector found a bottom last August, showed some strength in November, but has largely moved sideways since December.

Much like how Walmart and Costco lead the Staples space, Health Care performance is heavily driven by Eli Lilly, Johnson & Johnson, and UnitedHealth Group.

Don’t Overcomplicate the Defensive Trade

At a high level, it’s easy to get lost comparing relative strength across defensive, cyclical, and growth sectors. But the reality is simple: risk-off areas like Utilities, Staples, and Health Care can rally—and have done so multiple times during this bull market. In fact, companies such as Walmart, Costco, and Eli Lilly often behave more like growth stocks than traditional defensive names.

The takeaway: sector analysis—including relative strength—is just one tool within a broader top-down and intermarket framework.

When Defensive Strength Signals Trouble

So when does outperformance in defensive sectors shift from a caution sign to a real warning? If Utilities, Staples, Health Care (and possibly Real Estate) start showing relative strength while declining in absolute terms, it’s usually a sign the S&P 500 is under pressure.

There have been early hints of this dynamic alongside the index’s bearish rounded top, but so far it’s been inconsistent rather than decisive. While it’s not ideal for defensive sectors to lead, such phases can persist longer than expected.

Bottom Line

While attention is centered on Energy and Technology—with $100 oil and NVIDIA grabbing headlines—along with Financials facing stress from private credit concerns, traders shouldn’t ignore the defensive sectors. Monitoring both absolute and relative trends in these areas can provide clarity and help filter out noise during volatile market conditions.

Oil jumps more than 2% as markets assess supply threats from the Iran conflict.

Oil prices rebounded over 2% early Tuesday, recovering part of the previous session’s losses as supply concerns intensified amid major disruptions in the Strait of Hormuz.

Brent crude climbed to around $102.69 a barrel, while WTI rose to about $95.92. The gains follow a sharp selloff in the prior session, when prices dropped after some tankers managed to pass through the key shipping route.

The Strait of Hormuz—responsible for roughly 20% of global oil and LNG trade—has been largely disrupted by the ongoing US-Israel conflict with Iran, now in its third week, heightening fears of supply shortages, rising energy costs, and persistent inflation.

Tensions remain elevated as several US allies declined calls to deploy naval escorts for tankers, while risks of further attacks on shipping continue to threaten stability in the region. Iran has also sought the release of seized Indian tankers as part of efforts to secure safe passage through the Gulf.

The disruption has already forced the UAE to cut oil output by more than half, tightening global supply. In response to rising energy costs, the International Energy Agency is considering additional releases from strategic reserves beyond the 400 million barrels already planned.

Meanwhile, major banks have raised their oil price forecasts, reflecting the risk of prolonged supply disruptions. Scenarios range from a quick resolution that pushes prices back toward $70 to an extended conflict that could drive Brent toward $85 or higher.

Security sources report that drones and rockets were launched at the US embassy in Baghdad.

Several rockets and at least five drones targeted the US embassy in Baghdad early Tuesday, in what Iraqi security sources described as the most severe attack since the US–Israel conflict with Iran began.

Witnesses saw multiple drones heading toward the compound, with air defenses intercepting some, while at least one hit inside the embassy, sparking fire and smoke. Blasts were also reported across the city.

The strike reflects escalating retaliation by Iran-backed militias against US interests in Iraq following the war that started on February 28.

In response, Iraqi forces have increased security across Baghdad, shutting down the fortified Green Zone that houses key government buildings and diplomatic missions.

The US Dollar Index holds onto Monday’s pullback around the 100.00 mark as attention turns to the Fed’s policy decision.

Iran has permitted multiple countries to move their energy tankers through the Strait of Hormuz.

The Fed is widely anticipated to leave interest rates unchanged on Wednesday.

The US Dollar (USD) is holding onto Monday’s corrective move, which was triggered by a sharp pullback in oil prices that helped ease concerns about unanchored consumer inflation.

At the time of writing, the US Dollar Index (DXY), which measures the Greenback against a basket of six major currencies, is edging slightly higher near 99.90.

The index retreated notably from Friday’s more-than-nine-month high of 100.54 as oil prices dropped after Iran permitted several countries to transport oil and Liquefied Petroleum Gas (LPG) shipments through the Strait of Hormuz, potentially reducing worries over energy supply disruptions.

In recent weeks, the USD has rallied strongly, supported by its safe-haven appeal amid escalating tensions involving Iran, the United States, and Israel. Additionally, elevated oil prices have dampened expectations for near-term interest rate cuts by the Federal Reserve (Fed).

Data from the CME FedWatch tool suggests that markets are largely convinced the Fed will keep rates unchanged until at least the September meeting, with the probability of a rate cut at that time standing at around 50%.

Looking ahead, investors will closely watch Wednesday’s Fed policy decision for further guidance. Attention will also be on the FOMC’s Economic Projections report, which will provide updated forecasts for interest rates, inflation, and economic growth.

WTI

WTI prices advance to around $94.20 during early Tuesday trading in Asia.

Rising geopolitical tensions in the Middle East continue to support crude prices.

The IEA is considering releasing additional oil reserves to mitigate the economic fallout from the US–Israel conflict with Iran.

West Texas Intermediate (WTI), the US crude benchmark, is hovering near $94.20 during early Tuesday trading in Asia, supported by ongoing tensions surrounding Iran, with no clear signs of de-escalation. Market participants are also awaiting the American Petroleum Institute (API) report due later in the day.

On Tuesday, the Israeli military reported detecting missiles launched from Iran toward Israeli territory, urging residents in impacted areas to seek shelter immediately. Meanwhile, the United Arab Emirates (UAE) announced a temporary full closure of its airspace as a precautionary step, with its defense ministry confirming responses to incoming missile and drone threats from Iran.

Fears of retaliatory Iranian strikes targeting ships, infrastructure, and key transit ports for oil shipments have raised concerns that the conflict could evolve into a prolonged regional war. Such risks may continue to provide near-term support for WTI prices.

However, on the supply side, the International Energy Agency (IEA) is considering releasing additional oil reserves into the global market to ease upward pressure on prices. The agency indicated a potential release of up to 400 million barrels, which, if coordinated among member countries, could temporarily boost supply and help limit sharp price spikes.

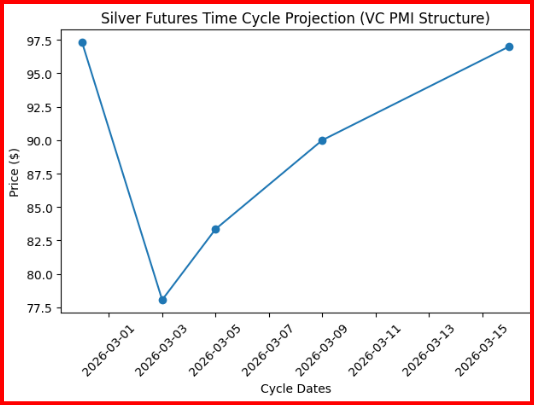

Silver (XAG/USD)

Silver declines as traders adjust positions ahead of Wednesday’s Federal Reserve policy decision.

Higher oil prices, driven by escalating tensions in the Middle East, are fueling inflation concerns and dampening expectations for near-term Fed rate cuts.

At the same time, geopolitical risks involving the United States, Iran, and Israel are helping to cap deeper losses by maintaining demand for safe-haven assets like silver.

Silver (XAG/USD) is trading near $80.50 on Tuesday, down about 0.60% on the day. The metal remains under pressure as fading expectations for near-term US rate cuts—amid rising inflation concerns tied to Middle East tensions—continue to weigh on sentiment.

Markets broadly expect the Federal Reserve to keep its benchmark rate unchanged within the 3.50%–3.75% range at Wednesday’s meeting, according to the CME FedWatch tool. If confirmed, this would mark a second straight pause following the prior easing cycle. Prolonged higher rates tend to pressure non-yielding assets like Silver, as they raise the opportunity cost of holding them.

Escalating geopolitical tensions in the Middle East have driven Oil prices higher, fueling fears of persistent inflation. Rising gasoline costs in the US are adding strain on households and may keep inflation expectations elevated, reinforcing the case for the Fed to maintain restrictive policy for longer.

Geopolitical developments continue to influence the precious metals market. Recent US strikes on Iran’s key export hub on Kharg Island have intensified concerns over global energy supply disruptions. While Washington has indicated the conflict could be resolved within weeks and is exploring an international effort to secure shipping routes through the Strait of Hormuz, uncertainty remains high.

This fragile geopolitical backdrop may help limit further downside in Silver. As a safe-haven asset, it tends to attract demand during periods of heightened risk, which could cushion losses even as higher interest rate expectations dampen overall investor appetite.

Sources: Ghiles Guezout, Lallalit Srijandorn and Sagar Dua

Gold draws safe-haven demand as tensions in the Middle East escalate further.

Inflation concerns dampen expectations of Fed rate cuts, supporting the USD and limiting the metal’s upside.

Traders remain cautious, avoiding aggressive positions ahead of this week’s major central bank events.

Gold (XAU/USD) ticks modestly higher in Tuesday’s Asian session but struggles to build momentum, hovering near a three-week low reached the day before. Ongoing tensions in the Middle East continue to provide some support, as the conflict shows little sign of easing. Israel has expanded its ground operations in southern Lebanon—an area where Hezbollah maintains a strong presence—keeping geopolitical risks elevated and sustaining demand for the safe-haven metal.

Now in its third week, the conflict has seen Iran target civilian infrastructure across six Gulf nations, including airports, ports, oil facilities, and commercial centers, using missiles and drones. Disruptions in the Strait of Hormuz—a critical route for about one-fifth of global oil supply—have also kept crude prices elevated. This adds to inflation concerns, potentially pushing the Federal Reserve to maintain higher interest rates for longer or even consider further tightening, which in turn limits upside for non-yielding assets like gold.

At the same time, rising geopolitical tensions have revived demand for the US Dollar following a pullback from its highest level since May 2025, further capping gains in XAU/USD. However, USD bulls remain cautious ahead of the outcome of the Federal Open Market Committee (FOMC) meeting on Wednesday. Policy decisions from other major central banks, including the ECB, BoJ, and BoE, are also expected later in the week and could drive fresh volatility in gold prices.

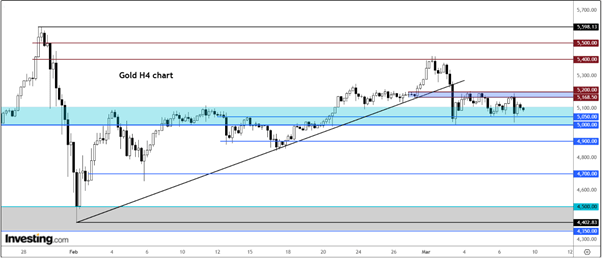

Gold (XAU/USD) on the 4-hour timeframe chart

Gold appears at risk, with a break below the 200-period SMA and the 38.2% Fibonacci level still in effect

Gold’s recent drop below the 200-period Simple Moving Average (SMA) on the 4-hour chart, along with sustained trading beneath the 38.2% Fibonacci retracement of the February–March rally, continues to favor bearish momentum in XAU/USD. The Moving Average Convergence Divergence (MACD, 12, 26, 9) remains in negative territory, with the MACD line below its signal line and a bearish histogram, pointing to ongoing downside pressure. Meanwhile, the Relative Strength Index (RSI) sits around 41, tilting toward the weaker side of neutral and suggesting sellers are still in control.

On the upside, initial resistance is seen near the 38.2% Fibonacci level around $5,040, followed by the 200-period SMA close to $5,063. A decisive move above this zone would help reduce bearish pressure and potentially pave the way toward the 23.6% retracement near $5,186. On the downside, immediate support lies at the key psychological level of $5,000, with further support around the recent lows between $4,995 and $4,985. A break below this area could open the door to a deeper pullback toward the 50.0% retracement at $4,921.41. A sustained move back above the 200-period SMA would weaken the bearish outlook, while continued rejection below $5,040 keeps the focus on further declines.

U.S. Strategy I: Roaring 2020s vs. Stagflating 1970s Redux

In last Tuesday’s QuickTakes, reacting to the latest Middle East conflict, we noted that although markets were already due for a pullback because of excessive bullish sentiment, the escalation increased the likelihood of a deeper correction. We suggested the market could fall around 10% from its peak, potentially reaching 15% if Iran’s Islamic Revolutionary Guard Corps (IRGC) succeeded in sustaining a blockade of the Strait of Hormuz using drones and fast boats.

Since then, much of Iran’s conventional naval capability has reportedly been destroyed. However, as long as the IRGC retains drone capabilities, the strategic waterway could remain effectively constrained. Donald Trump has authorized the United States Navy to escort vessels through the Strait, though the operation may take time to deploy and may not fully eliminate the threat of Iranian drone attacks.

Media reports over the weekend underscored those risks. According to the New York Post, an Iranian suicide drone struck a commercial oil tanker in the Strait, setting it ablaze while U.S. naval protection efforts for shipping lanes could still be weeks away.

Limits of Air Power

Military historians have long debated whether air power alone can decisively win wars. Most conclude it rarely achieves lasting victory by itself. While air strikes can destroy infrastructure, supply chains, and concentrated forces, they cannot control territory, conduct searches, or administer local governance. Nor can they fully eliminate dispersed threats such as drones.

Over the weekend, President Trump declined to rule out deploying ground forces, though he dismissed the idea of using Kurdish fighters as proxies for an invasion of Tehran, saying the conflict was already “complicated enough.” He indicated ground operations would only occur if the adversary were sufficiently weakened.

Domestic Economic Backdrop

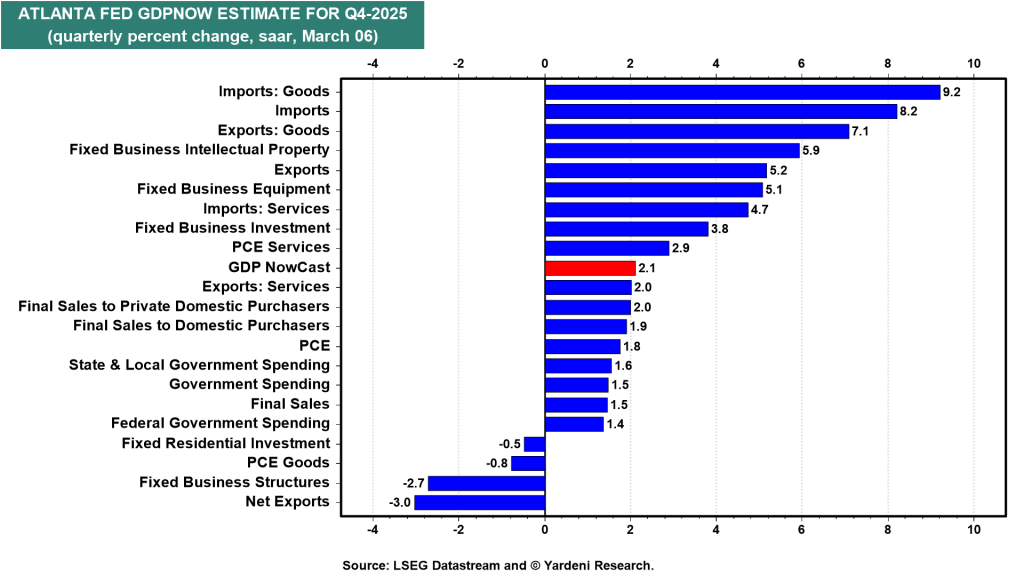

At home, economic data has also softened. February’s U.S. employment report came in much weaker than expected, while January retail sales disappointed. As a result, the Federal Reserve Bank of Atlanta’s GDPNow model lowered its estimate for Q1 real GDP growth to 2.1% (annualized), down from 3.0%.

This leaves both the U.S. economy and equity markets caught between geopolitical shocks and slowing domestic momentum. The Federal Reserve faces a similar dilemma: if higher oil prices persist, its dual mandate could be squeezed between rising inflation and weakening employment.

Implications for the Economic and Market Outlook

Rapidly Changing Conditions

Given the speed of developments, scenario probabilities are being adjusted. The base case remains the “Roaring 2020s” with a 60% probability. However, the “Meltup” scenario has been cut from 20% to 5%, while the “Meltdown” scenario—now including the risk of 1970s-style stagflation—has been raised from 20% to 35%.

Looking beyond this year to the rest of the decade, the outlook narrows to two primary possibilities:

Roaring 2020s: 85% probability

Stagflating 1970s Redux: 15% probability

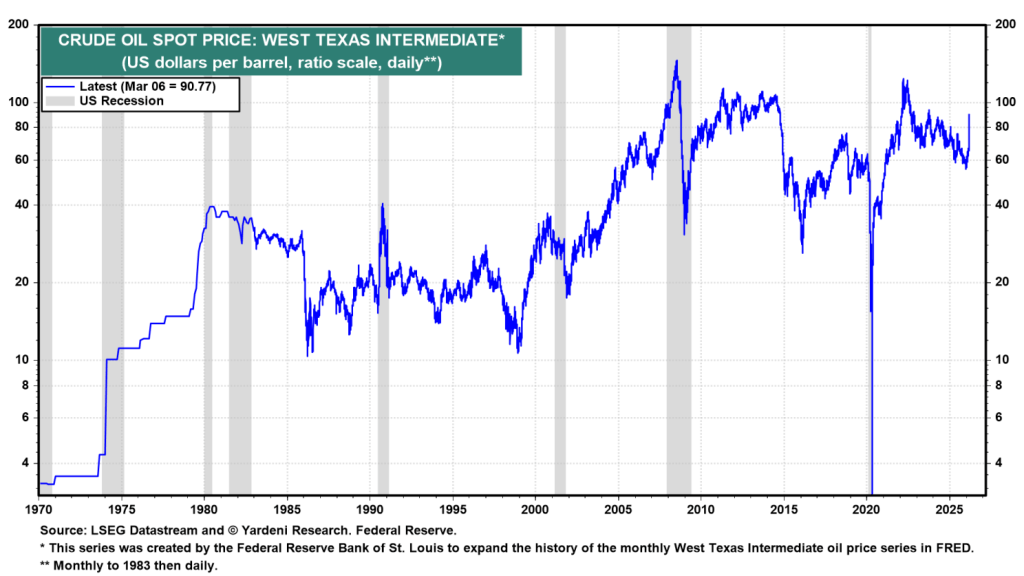

Oil Prices and Market Risk

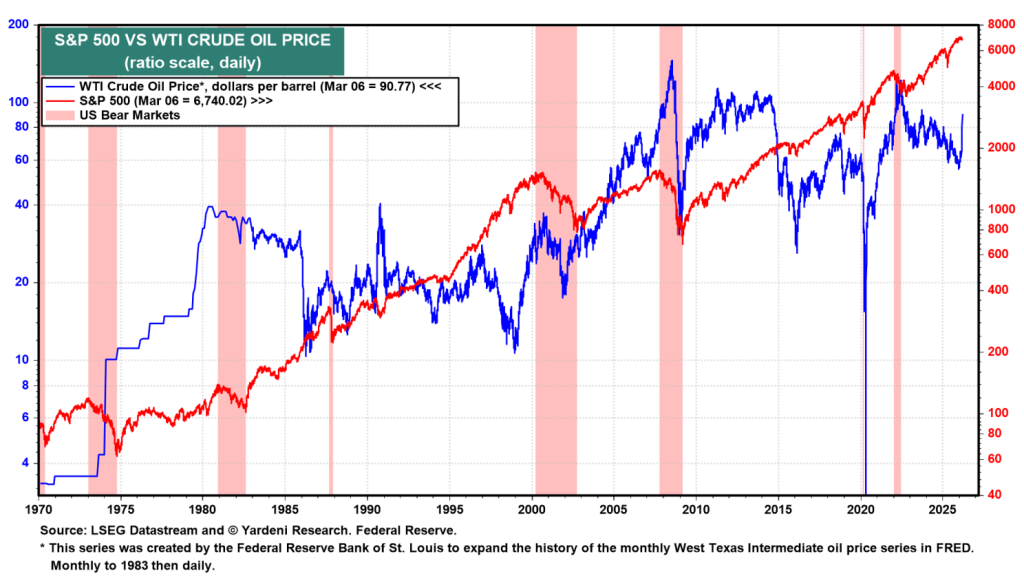

Historically, sharp oil price spikes have often coincided with recessions and bear markets. One recent exception was the 2022 surge following Russia’s invasion of Ukraine, which produced a bear market but not a recession—highlighting the resilience of the U.S. economy.

A similar pattern could play out today. While the economy may absorb higher energy costs, the current oil shock still increases the likelihood of a 10%–15% correction in equities, even if a full bear market ultimately proves avoidable under current conditions.

War Likely to Continue for Several More Weeks

Our relatively optimistic scenario assumes the conflict will persist for a few more weeks, while the U.S. economy and corporate earnings remain resilient, as they have during previous shocks.

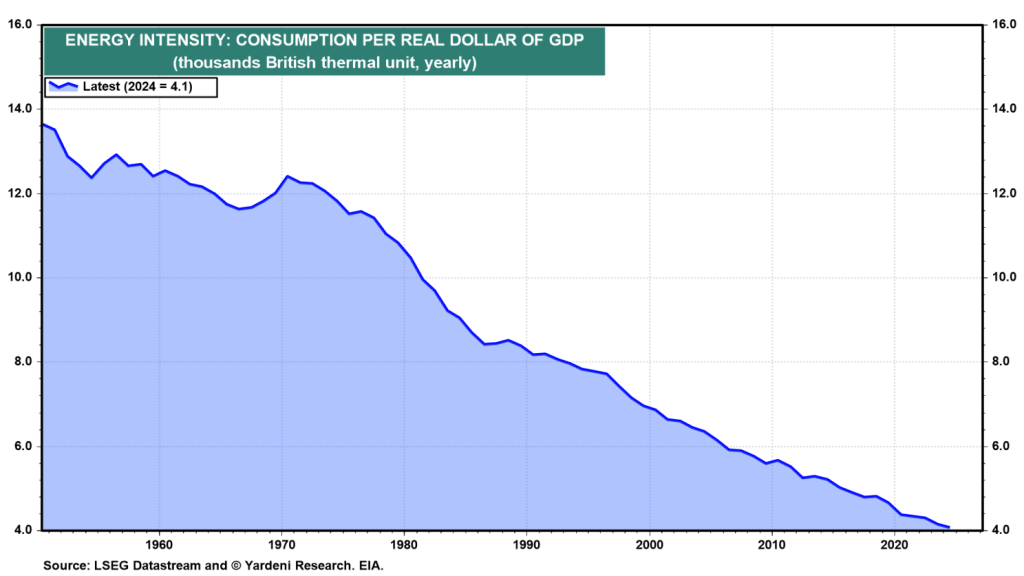

One reason for this resilience is the sharp decline in the economy’s energy intensity—measured as total energy consumption per unit of real GDP. In the United States, energy intensity has fallen dramatically over the past several decades, dropping about 70% between 1950 and 2024 and roughly 62% since 1979.

This structural shift means the U.S. economy is far less sensitive to oil-price shocks than in earlier decades, particularly compared with the 1970s oil crisis period when energy costs had a much larger impact on growth and inflation.

The United States economy has gradually shifted from heavy reliance on energy-intensive manufacturing toward a more service-oriented structure, which has helped reduce overall energy consumption relative to economic output.

Additional factors behind the decline in energy intensity include the introduction of Corporate Average Fuel Economy (CAFE) standards and ongoing technological improvements in internal combustion engines, both of which have improved fuel efficiency across the transportation sector.

At the same time, the expansion of the digital economy—including data centers, cloud computing, and artificial intelligence—has been driving stronger electricity demand. Even so, the growing use of natural gas and renewable energy sources in power generation, as well as their increasing adoption in industrial processes that previously relied on oil, should continue to moderate the economy’s direct dependence on crude oil.

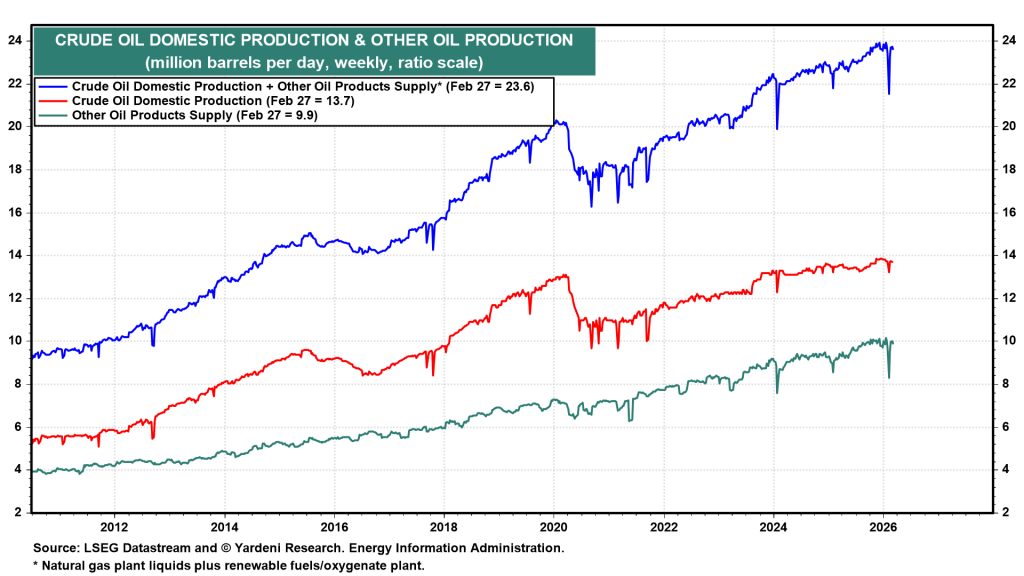

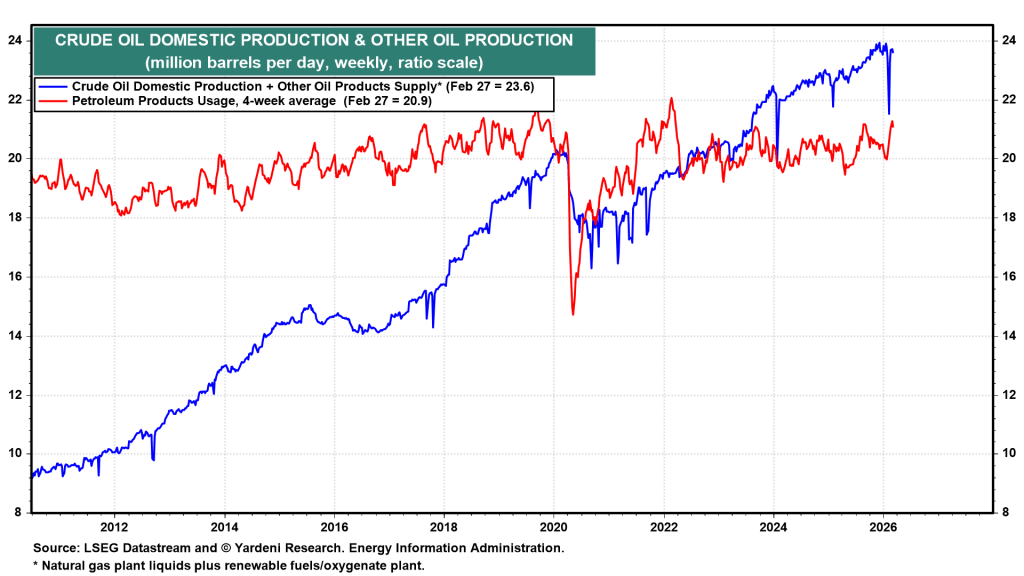

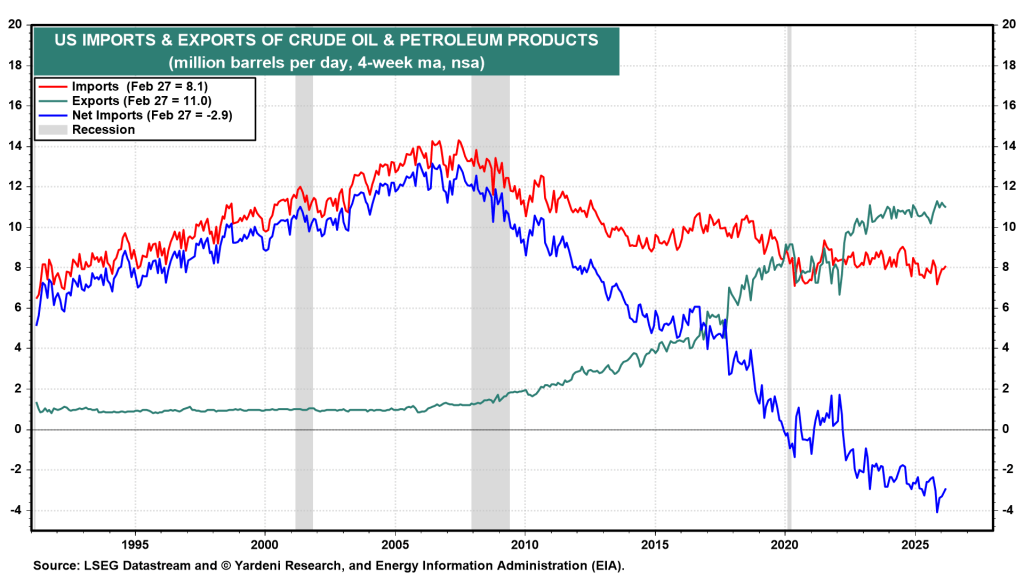

Oil production

U.S. oil production, which includes natural gas plant liquids and renewable fuels/oxygenates, has reached a record level of 24 million barrels per day (mbd), significantly exceeding domestic consumption of 21 mbd (Fig. 7 and Fig. 8). As a result, the United States has become a net exporter of roughly 3.0 mbd (Fig. 9). This represents a dramatic shift compared with 2007, when the country was a net importer of approximately 12 mbd.

A potential return of 1970s-style stagflation

A bear market cannot be ruled out if investors begin to expect a repeat of the stagflationary conditions seen in the 1970s. At that time, the global economy was hit by two major oil shocks. In October 1973, Arab members of Organization of the Petroleum Exporting Countries (OPEC) imposed an oil embargo on the United States and other countries that supported Israel during the Yom Kippur War.

Oil prices surged dramatically, rising about fourfold from roughly $3 to nearly $12 per barrel within only a few months. This led to stagflation—an unusual and painful economic condition characterized by slow economic growth, high unemployment, and accelerating inflation (Fig. 10). The crisis resulted in long queues at gasoline stations, fuel rationing, and a heightened awareness of the United States’ dependence on foreign energy supplies.

The second oil crisis occurred after the Iranian Revolution, which significantly disrupted global oil supplies. As a result, oil prices surged, rising to more than twice their previous level. This shock further weakened an already fragile economy and deepened the stagflationary pressures. Together, the two oil crises contributed to two recessions during the 1970s.

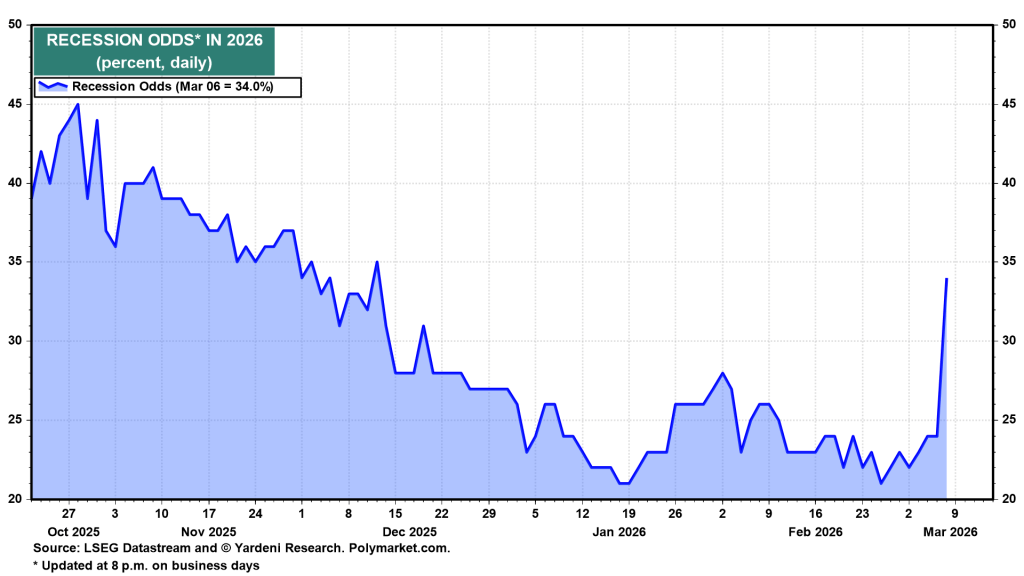

According to Polymarket, the probability of a recession this year rose to a three-month high of 34% on Friday, up from 21% on Wednesday, February 25, just before the conflict began (Fig. 11).

U.S. Strategy II: A Direct Confrontation with the IRGC

When the conflict began on Saturday, February 28, the initial assumption was that it would end quickly. However, by the following Tuesday, that view changed, prompting further analysis in that day’s QuickTakes. A key concern is that by eliminating the leadership of the Iranian regime in the opening hour of the war, the United States and Israel effectively unleashed the regime’s most powerful force—the Islamic Revolutionary Guard Corps (IRGC). Often described as a “state within a state,” the IRGC is believed to control 20–40% of Iran’s economy, including large construction companies, telecommunications networks, and oil engineering firms. This financial base allows it to sustain operations even under severe sanctions.

In April 2019, the United States officially designated the IRGC as a Foreign Terrorist Organization—the first time Washington had applied such a label to a branch of another government. Because of their decentralized structure and access to weapons such as suicide drones, the group would be difficult to eliminate through air power alone.

Donald Trump first publicly demanded Iran’s “unconditional surrender” on Friday, March 6. The following day, he clarified that the phrase meant a situation where Iran could no longer continue fighting. On Sunday morning, he also warned that any new Supreme Leader selected by Iran’s Assembly of Experts “would not last long” without his approval, implying a U.S. veto over the succession process following the death of Ali Khamenei.

Without a central leader, Iran lacks a figure capable of formally accepting unconditional surrender. For example, on Saturday, Iranian President Masoud Pezeshkian issued a public apology for Iran’s “fire-at-will” attacks on neighboring countries. Yet only hours later, the IRGC launched another wave of strikes, highlighting a severe breakdown in command and control after Khamenei’s death on February 28. Even without the regime’s top leader, the IRGC’s decentralized design allows regional commanders to operate independently, already carrying out retaliatory drone and missile attacks against U.S. assets and allies in the Gulf.

One objective of the ongoing air campaign is to weaken the IRGC’s ability to suppress domestic opposition. By striking the Basij—the IRGC’s paramilitary force used for internal control—the United States hopes to open the door for a possible uprising inside Iran. However, from the perspective of financial markets, the war will not truly end until commercial ships can move through the Strait of Hormuz without the threat of IRGC attacks. Once that happens, the stock market’s bullish trend could resume.

U.S. Economy: Domestic Impact

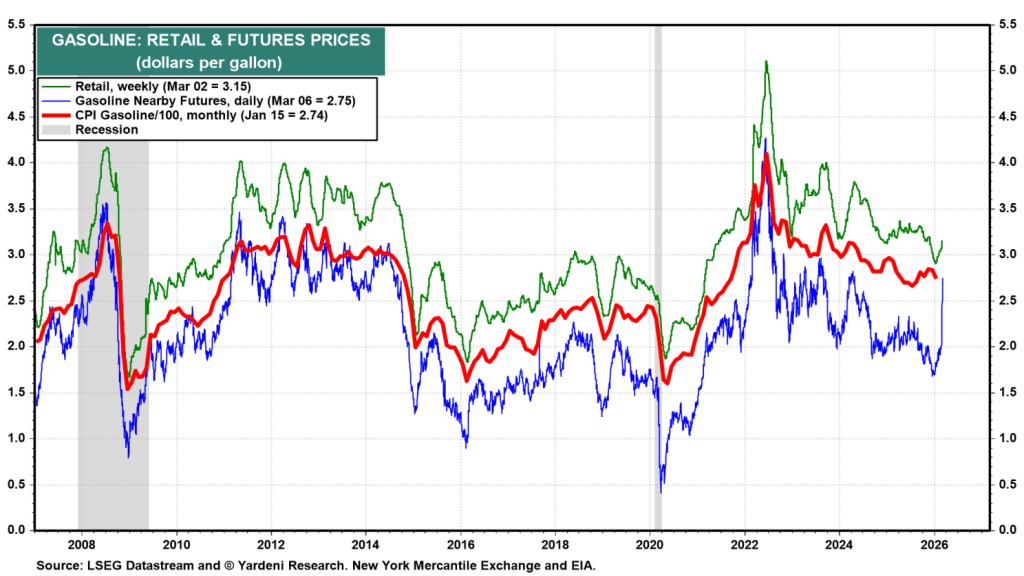

Within the United States, economic data from January and February were collected before the war and present a mixed picture. Data from March will likely reveal the first economic effects of the conflict, including rising inflation and a weakening labor market. One immediate sign of inflationary pressure is the sharp increase in gasoline prices, driven by the surge in crude oil prices (Fig. 12).

Food prices may not increase right away, but fertilizer shortages could push them higher in the months ahead. Roughly 25%–33% of the global nitrogen fertilizer trade—particularly urea and anhydrous ammonia—moves through the Strait of Hormuz. On March 2, an Iranian drone attack struck the Ras Laffan Industrial City in Qatar, the world’s largest export hub for liquefied natural gas. Since natural gas is the main feedstock used to produce nitrogen fertilizers, disruptions there could have significant downstream effects. Meanwhile, Saudi Arabia, Oman, and the United Arab Emirates—all among the world’s top ten exporters of urea—are facing logistical and production challenges because of the ongoing air conflict.

If the blockade remains in place into early April, farmers might be forced to shift away from nitrogen-intensive corn-based fertilizer systems toward soybean alternatives or simply reduce fertilizer usage. Lower fertilizer application typically results in reduced crop yields, which could lead to a secondary food price shock toward the end of 2026.

This conflict represents another major test of the resilience of the U.S. economy since the beginning of the decade. It also challenges the so-called “Roaring 2020s” outlook. Despite the new risks, that optimistic scenario remains the base case with a 60% probability. However, the likelihood of a 1970s-style stagflation scenario has been raised to 35%, while the probability of a market melt-up has been reduced to 5% for the rest of 2026.

Recent economic data suggest that the labor market weakened in February and retail sales were soft in January. On the positive side, productivity growth has been particularly strong in recent quarters. If that trend continues, higher productivity could help mitigate some of the stagflationary pressures created by the war.

Employment

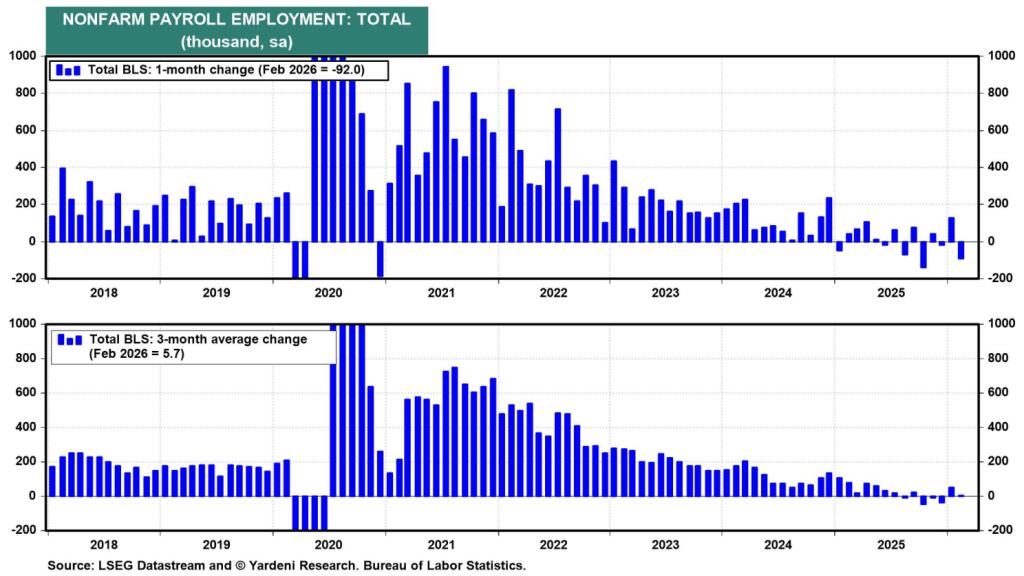

The January employment report came in significantly stronger than expected, whereas the February report was much weaker than forecasts. Severe weather conditions and a labor strike negatively affected February’s figures. As a result, nonfarm payrolls declined by 92,000 last month.

In addition, the January payroll figure was slightly revised downward by 4,000 to 126,000, while December’s data was adjusted from a previously reported gain of 48,000 to a decline of 17,000 (Fig. 13). Meanwhile, the unemployment rate increased marginally, rising to 4.4% in February from 4.3% in January.

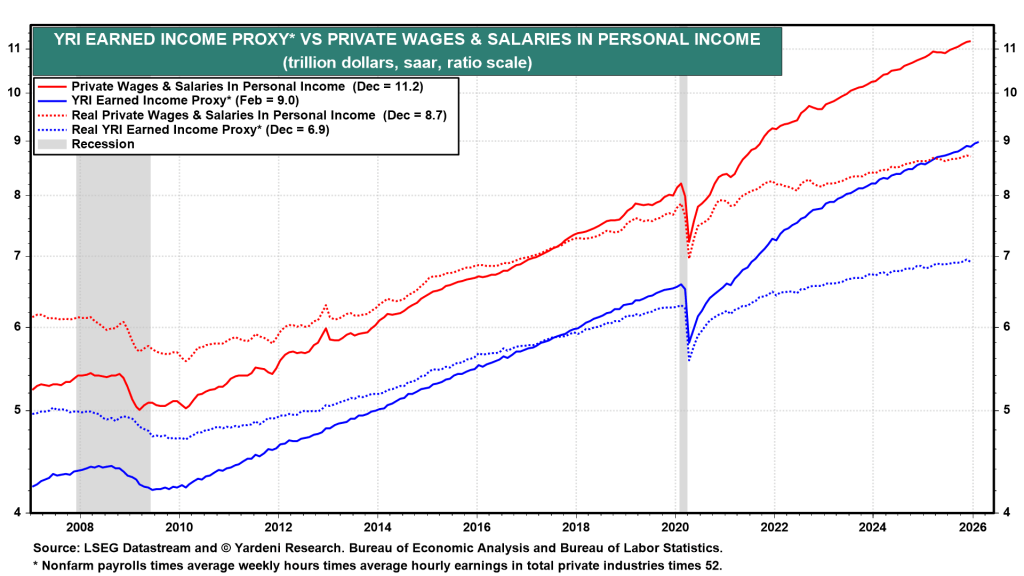

The positive development is that average hourly earnings increased by 0.4% month over month in February, while the average workweek remained unchanged. Consequently, our Earned Income Proxy, which estimates wages and salaries within personal income, rose by 0.3% in February, reaching a new record high (Fig. 14).

The Federal Reserve is facing a policy dilemma: a softening labor market, which would normally justify cutting the federal funds rate, versus rising energy and fertilizer costs linked to the Iran conflict, which could push inflation higher and argue for keeping rates unchanged or even tightening policy.

This clash of signals complicates the Fed’s next move. Weak employment data suggests the economy may need monetary support, while higher oil and commodity prices risk reigniting inflation, forcing policymakers to remain cautious about easing.

Retail Sales

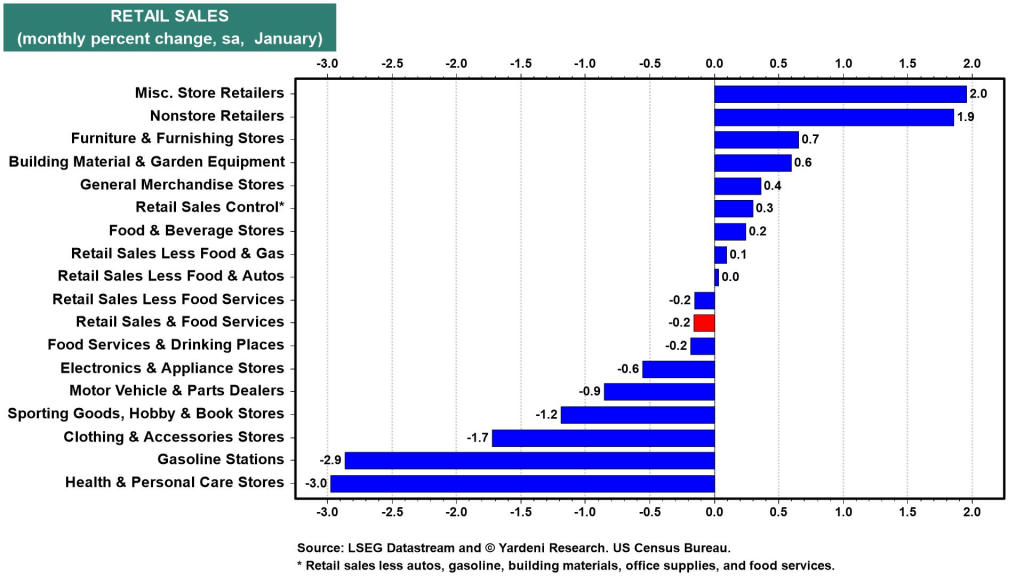

In January, retail sales declined by 0.2% month over month, while December’s figures, previously reported as showing moderate growth, were revised downward to no change compared with the previous month.

Among sectors, nonstore retailers experienced a 1.9% monthly increase, whereas motor vehicle and parts dealers recorded a 0.9% decline (Fig. 15). Sales at gasoline stations also dropped 2.9%.

One positive sign was a 0.3% month-over-month rise in core retail sales, which excludes several more volatile categories.

The rollout of last year’s One Big Beautiful Bill Act is expected to support consumer spending in the weeks ahead. A “February rebound” in retail activity is likely as record-high tax refunds—about 20% larger on average than last year—begin reaching households’ bank accounts.

Productivity

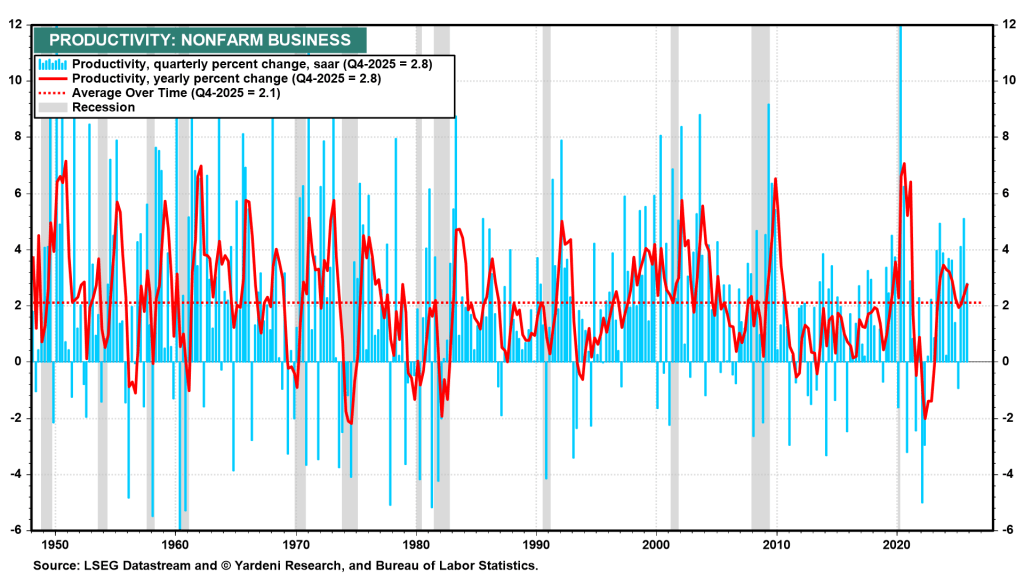

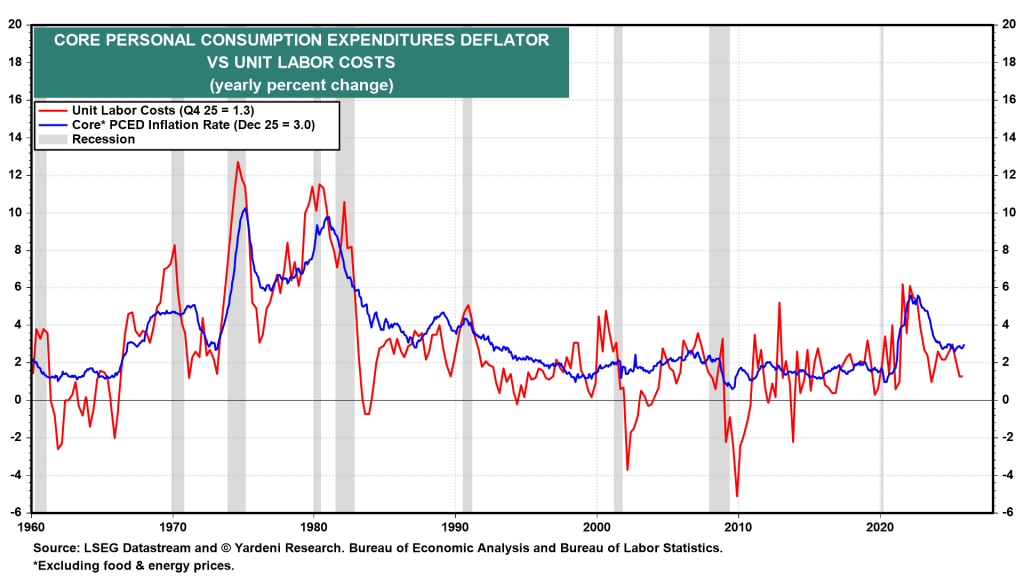

Labor productivity—defined as output per hour worked—increased at an annualized rate of 2.8% in Q4 2025. This marks the third consecutive quarter in which productivity growth has surpassed the long-term average of 2.1%, a benchmark calculated from data beginning in the late 1940s (Fig. 16).

At the same time, unit labor costs rose by only 1.3% year over year in Q4 2025, which helped contain inflationary pressures in the economy (Fig. 17).

GDPNow

As noted earlier, the newest economic data prompted the Federal Reserve Bank of Atlanta’s GDPNow model to lower its forecast for first-quarter 2026 economic growth from 3.0% to 2.1% (Fig. 18).

This week will see a series of major central bank meetings worldwide, including those of the Federal Reserve, European Central Bank, Bank of Japan, and Bank of England. With oil prices climbing sharply and inflation expectations edging higher, investors will be closely watching how policymakers assess the outlook for monetary policy and the implications of elevated energy costs.

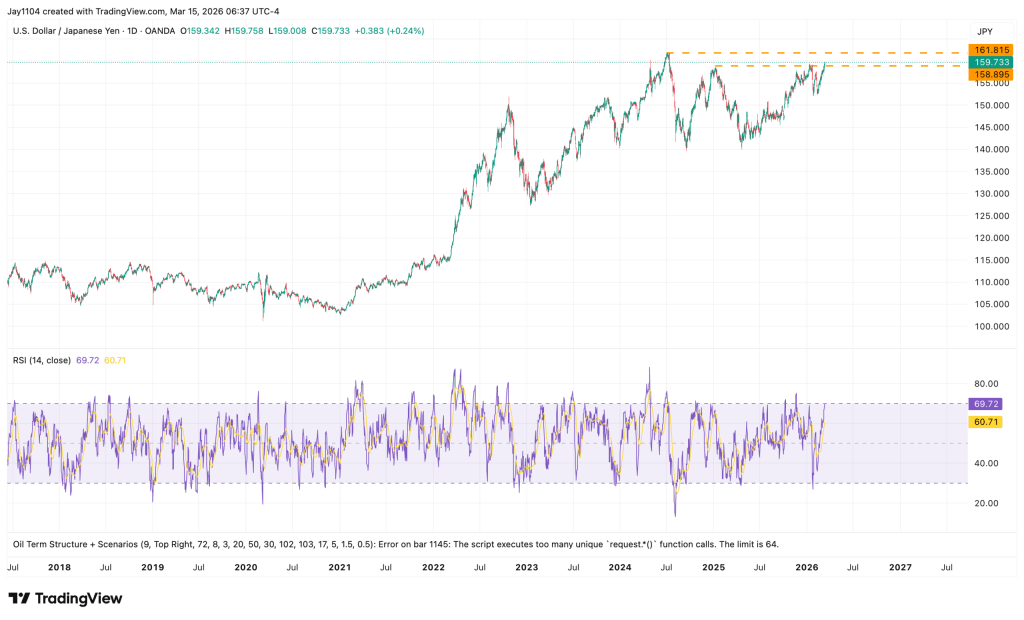

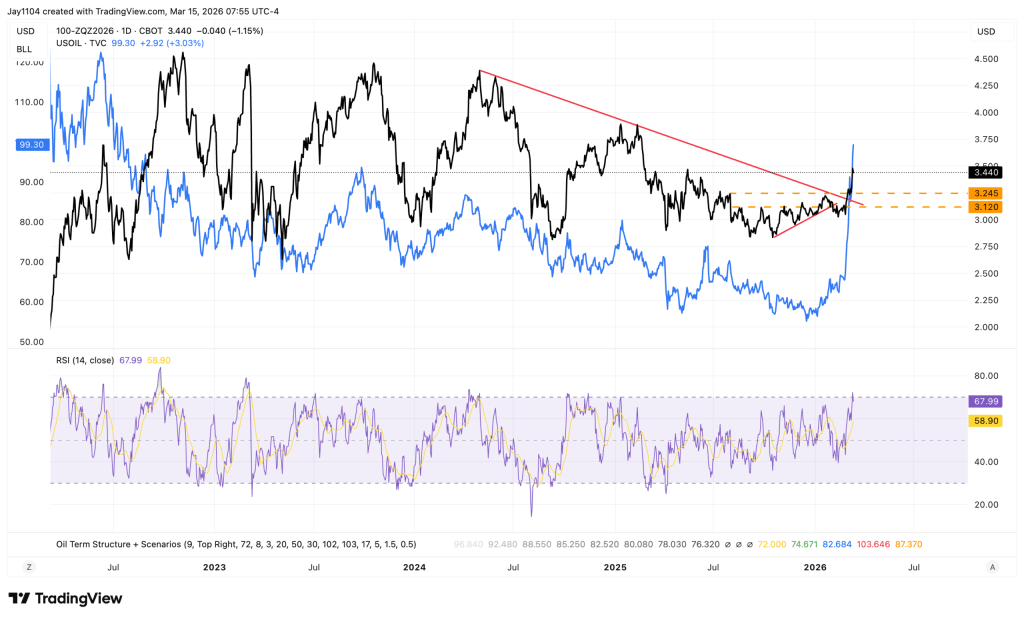

Among these institutions, the Bank of Japan faces perhaps the most delicate situation, particularly after the country’s February general election and the policy trajectory it had already been pursuing since its previous meeting. With oil trading near $100 a barrel, the BOJ must proceed cautiously as the USD/JPY exchange rate moves toward 160 — a level widely viewed as a potential tipping point for the currency.

The pair has already broken above resistance near 159, though it still remains below the highs reached in July 2024.

From a technical perspective, once USD/JPY moves above its July 2024 peak, there would be no clear resistance levels ahead, potentially opening the door for further and possibly sharp depreciation of the Japanese yen.

Meanwhile, the recent surge in oil prices has reshaped expectations for U.S. interest-rate cuts. Markets have gradually scaled back their projections for easing, even though the incoming Federal Reserve chair nominee has indicated a preference for looser monetary policy.

December Fed funds futures have climbed to around 3.44%, reflecting reduced expectations for rate cuts. Since 2022, market pricing for Fed easing has broadly moved in tandem with oil prices.

If oil continues to rise, it could complicate the Fed’s ability to lower rates, as higher energy costs tend to fuel inflation. Rate cuts may only become more likely if oil prices rise to a point where they begin pushing the economy toward recession.

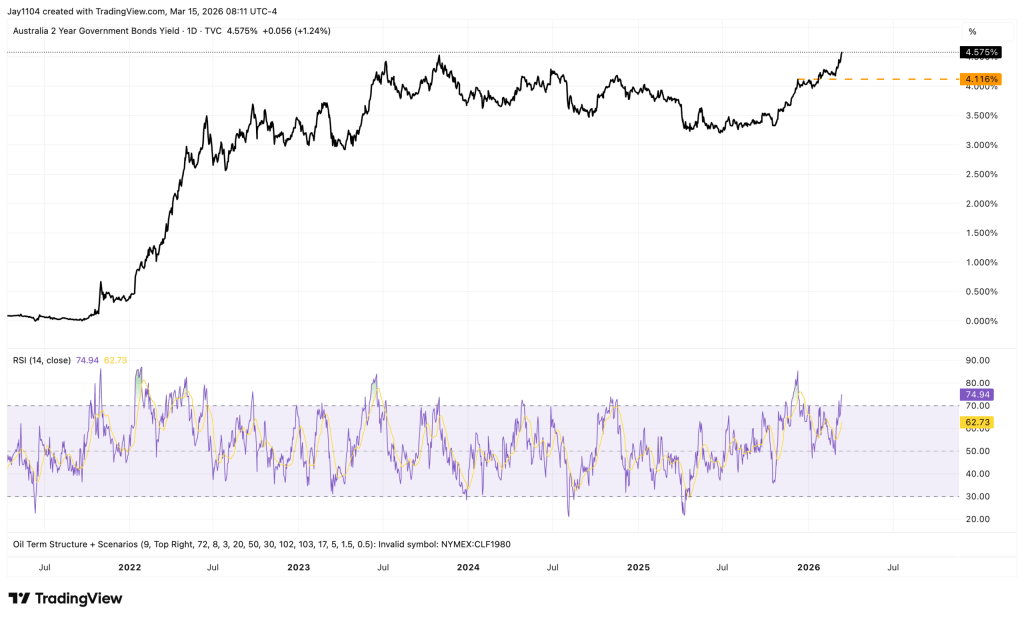

Rising rates are not limited to the U.S., as Australia’s 2-year bond yield has now moved above its October 2023 peak.

Rising global oil prices are likely to tighten liquidity and financial conditions worldwide. Tighter financial conditions typically place pressure on economic activity and risk markets. As long as oil prices remain elevated — or continue to climb — they are likely to further tighten global financial conditions and weigh on risk assets.

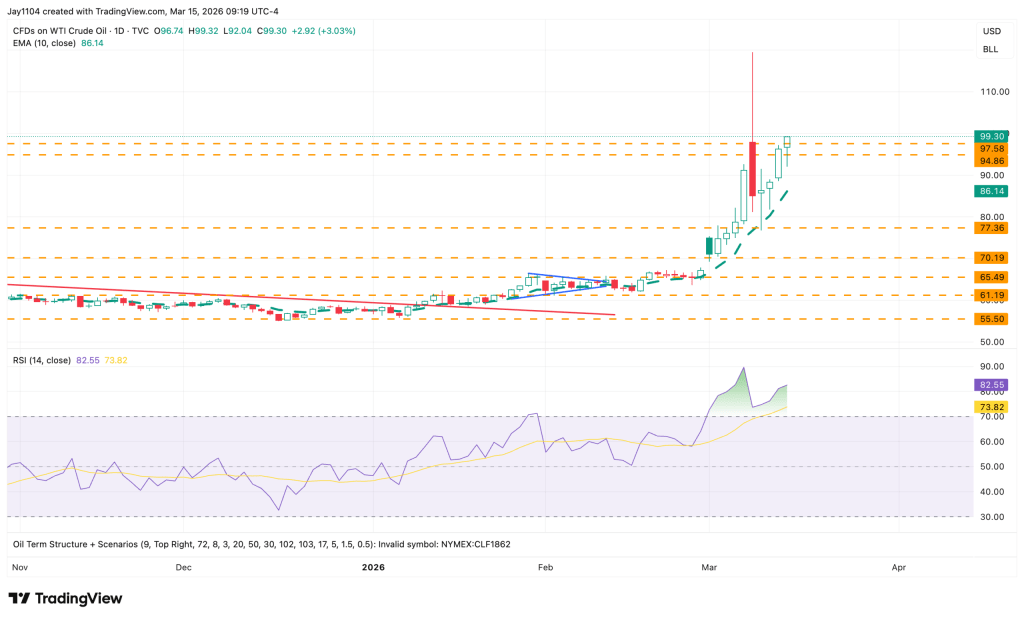

For investors trying to gauge the outlook for risk assets, the direction of oil prices has become increasingly important. However, predicting oil’s near-term path remains challenging. Weekend oil CFDs were trading about 3% higher and above $100 per barrel.

From a technical perspective, the trend remains upward for now, as long as oil continues to hold above its 10-day exponential moving average.

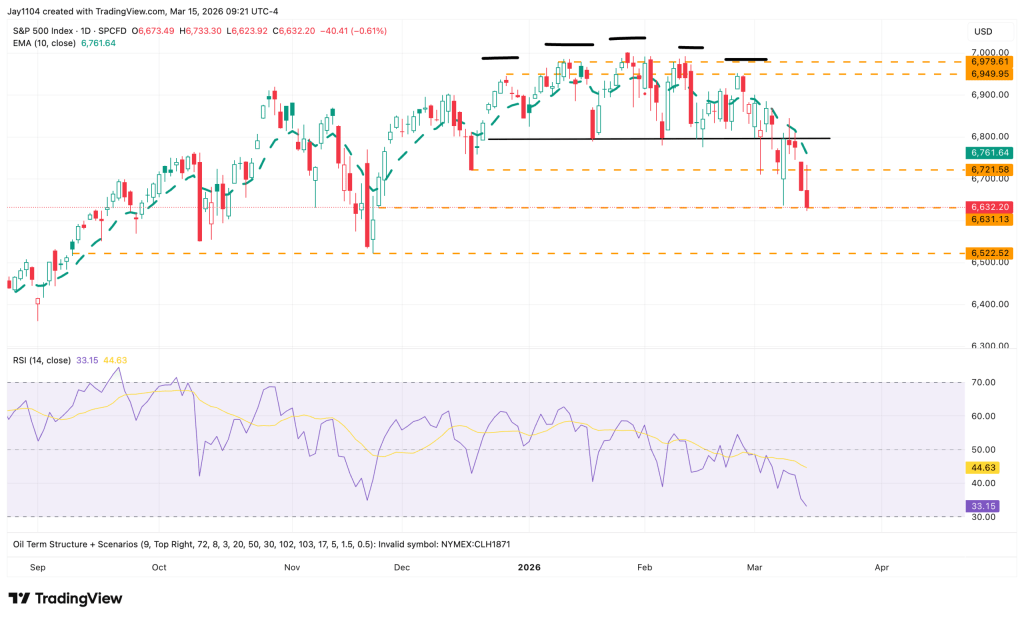

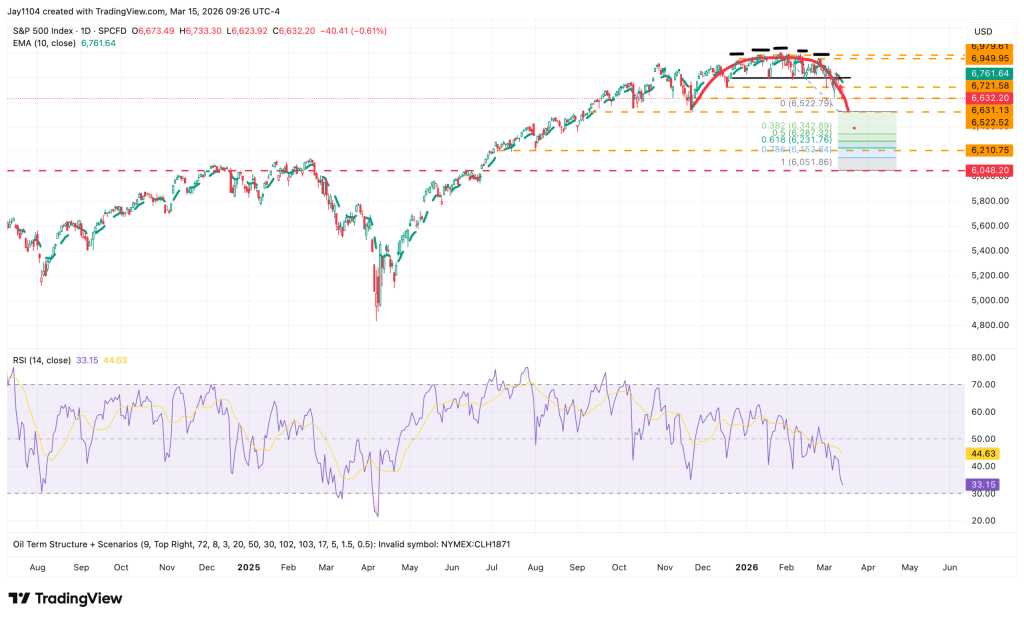

The situation is similar for the S&P 500—as long as the index stays below its 10-day exponential moving average, the short-term trend is likely to remain downward.

The distribution pattern in the S&P 500 appears relatively clear, with a key pivot level near 6,525, which coincides with the index’s November lows.

More significantly, measuring the decline from the recent high to this pivot level and projecting that move 100% lower points to a potential downside target near 6,050. Such a move would also fill the price gap from June 24 and allow the index to retest the breakout level from the pre-tariff highs, an area that could act as technical support.

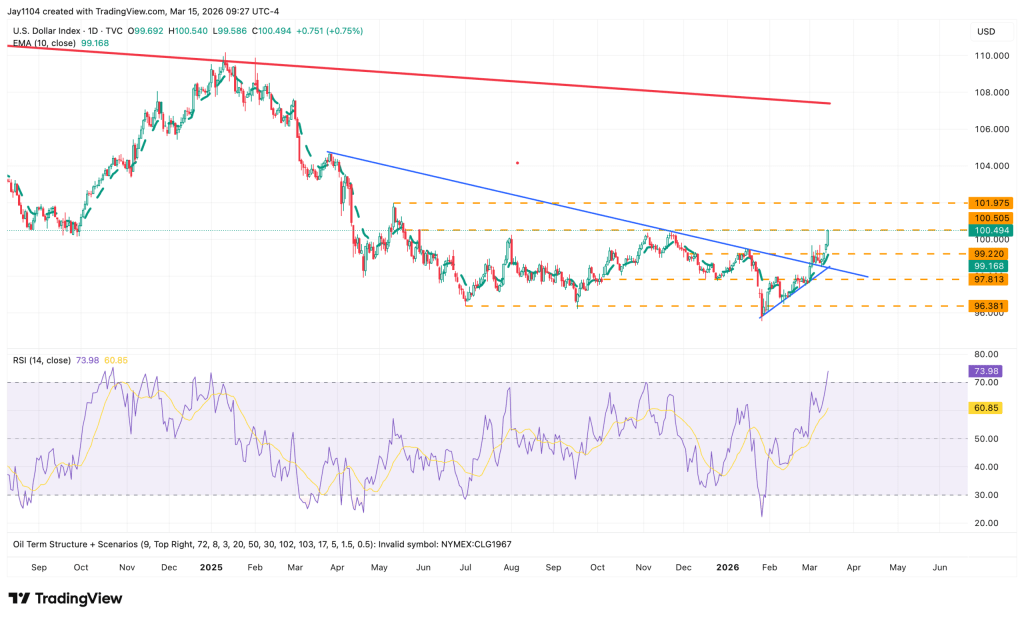

Such a scenario would likely require oil prices to stay elevated while interest rates and the U.S. dollar continue to strengthen. The U.S. Dollar Index could also extend its gains; a decisive break above 100.50 may open the door for a move toward 102.

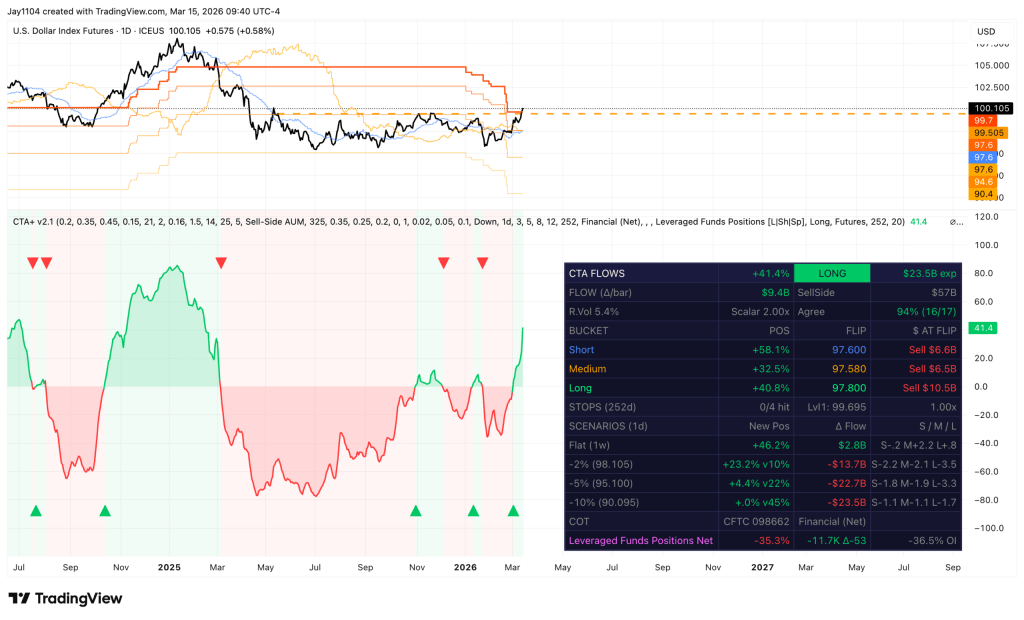

With momentum indicators turning positive, it appears likely that CTAs and leveraged funds may start adding long dollar positions while reducing their existing shorts.

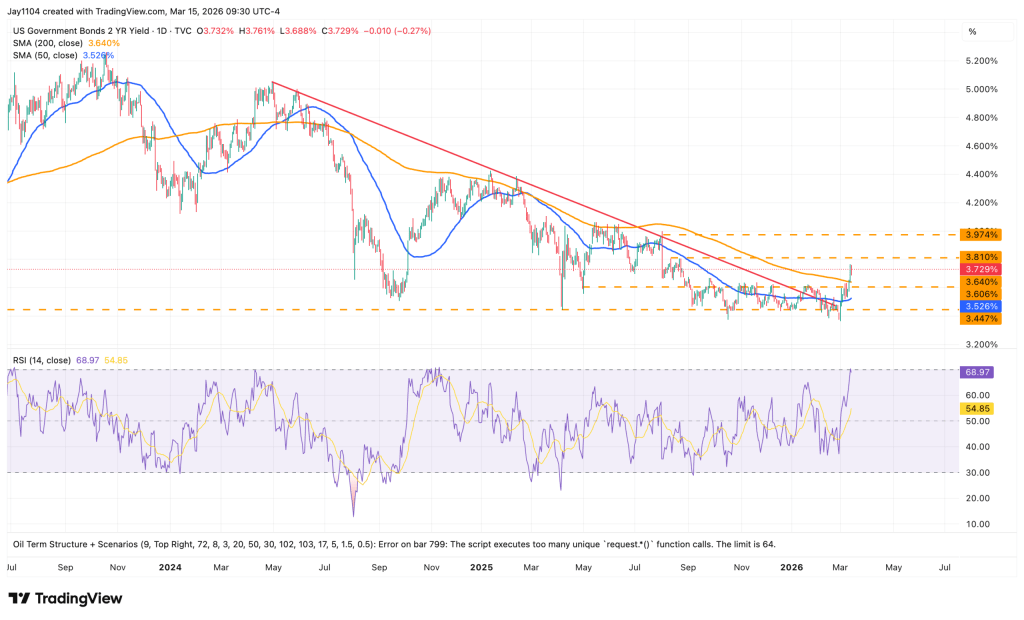

Meanwhile, the U.S. 2‑Year Treasury Yield may have room to extend higher, with the next resistance level seen near 3.80%, followed by a potential move toward 3.97%.

Technically, the outlook has strengthened as the yield has moved above its 200-day moving average, while the 50-day moving average is beginning to trend upward. In addition, the yield recently broke above a multi-year downtrend line that had been in place since April 2024, reinforcing the case for further upside momentum.

We’ll have to watch how the week develops. With options expiration (OPEX) taking place, market volatility could remain elevated. This is particularly true for the S&P 500, where put options currently dominate positioning, increasing the potential for sharp and erratic intraday price swings.

Bitcoin climbed above $74,000 on Monday, reaching its highest level in roughly six weeks as a wave of short liquidations supported the rally, although investors stayed cautious amid rising geopolitical tensions in the Middle East.

The largest cryptocurrency was last up 3.4% at $73,892.4 by 02:21 ET (06:21 GMT), after touching an intraday high of $74,336.9 earlier in the session.

Bitcoin gained about 6% last week even as global equity markets declined, with surging oil prices fueling concerns about inflation.

Crypto rallies on short liquidations

Cryptocurrency markets posted broad gains as traders who had bet on further price declines rushed to close their short positions.

Data from CoinGlass showed about $344 million in crypto liquidations over the past 24 hours, with short positions making up roughly 83% of the total.

Liquidations occur when leveraged traders are forced to close their positions after prices move against them, often intensifying price swings.

Despite the rebound, sentiment remained cautious as the conflict in the Middle East entered its third week, raising worries about global energy supply and inflation pressures.

Donald Trump, the U.S. president, has urged allies to help safeguard the Strait of Hormuz, a critical route for global oil shipments, as hostilities in the region continue.

Oil stays above $100 amid Iran war concerns

Reports indicated that despite repeated statements from U.S. officials claiming Iran’s military capabilities had been destroyed, drone attacks continued in Gulf states on Monday.

Oil prices remained supported above $100 per barrel amid fears of potential supply disruptions around the Strait of Hormuz, a key shipping route for global crude exports.

U.S. stock futures moved slightly higher in Asian trading on Monday as investors looked ahead to the upcoming policy meeting of the Federal Reserve, where policymakers are widely expected to keep interest rates unchanged while evaluating inflation risks.

Analysts noted that geopolitical uncertainty and broader macroeconomic risks could keep cryptocurrency markets volatile in the near term, even as short covering supports prices.

Oil prices increased on Monday as the ongoing conflict involving the United States, Israel, and Iran continued to disrupt oil production and transportation across the Middle East, despite a call from Donald Trump for international cooperation to protect the strategic Strait of Hormuz.

Brent crude futures climbed by $2.30, or 2.2%, reaching $105.44 per barrel at 0903 GMT, while U.S. West Texas Intermediate crude rose $1.29, or 1.3%, to $100 per barrel.

Both benchmarks have jumped more than 40% this month, reaching their highest levels since 2022. The surge followed U.S.–Israeli strikes on Iran, which led Tehran to halt shipments through the Strait of Hormuz—an essential route for global energy trade—disrupting roughly one-fifth of the world’s oil and LNG supplies.

On Monday, oil-loading activities were suspended at the UAE’s Fujairah port after a drone strike triggered a fire in the emirate’s petroleum industrial area, according to two sources who spoke to Reuters.

Fujairah, located outside the Strait of Hormuz, serves as an export hub for around 1 million barrels per day of the UAE’s flagship Murban crude oil, equivalent to roughly 1% of global oil demand.

The International Energy Agency warned on Thursday that the conflict in the Middle East is causing the most severe oil supply disruption on record, as major producers including Saudi Arabia, Iraq, and the United Arab Emirates have reduced output since the war began.

According to PVM analyst Tamas Varga, investors appear to understand that if just two weeks of disruption in the Strait of Hormuz have already caused significant damage to production, exports, and refining, a prolonged conflict could have far more serious consequences, particularly as global inventories continue to decline.

Analysts from ING said on Monday that recent U.S. strikes on Kharg Island over the weekend have heightened concerns about oil supply, as the majority of Iran’s crude exports are shipped through the island.

Although the attacks appeared to focus on military installations rather than energy infrastructure, ING noted that they still threaten supply stability. This is because Iranian crude is currently among the few oil flows still passing through the vital Strait of Hormuz.

During the weekend, Donald Trump warned that additional strikes could target Kharg Island—an export hub responsible for roughly 90% of Iran’s oil shipments—after U.S. forces hit military facilities there, prompting retaliatory actions from Tehran.

On Sunday, Trump called on other countries to assist in safeguarding this critical energy corridor and said that Washington was holding discussions with several nations about jointly monitoring and securing the strait.

Trump also stated that the United States remained in communication with Iran, though he expressed skepticism that Tehran was ready to engage in meaningful negotiations to bring the conflict to an end.

Meanwhile, the International Energy Agency announced on Sunday that more than 400 million barrels of strategic oil reserves would soon be released into the market—a record intervention intended to stabilize prices amid disruptions caused by the Middle East conflict.

According to the agency, reserves from countries in Asia and Oceania will be made available immediately, while supplies from Europe and the Americas are expected to enter the market by the end of March.

SEB analyst Meyersson said that as the conflict moves into its third week, the absence of a clear resolution is increasing global market anxiety about the possibility of an uncontrolled escalation.

However, U.S. Energy Secretary Chris Wright said on Sunday that he expected the war to end within the next few weeks, which could allow oil supplies to recover and energy prices to decline.

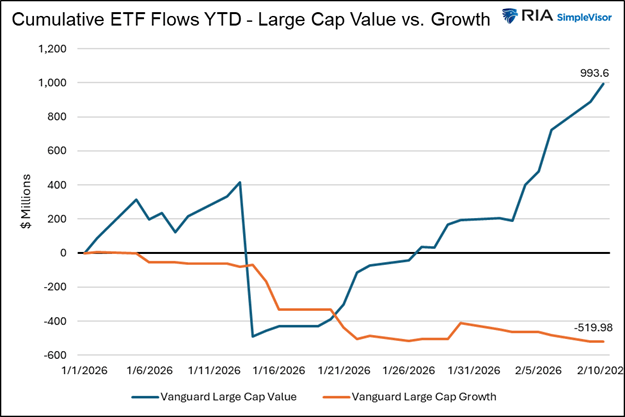

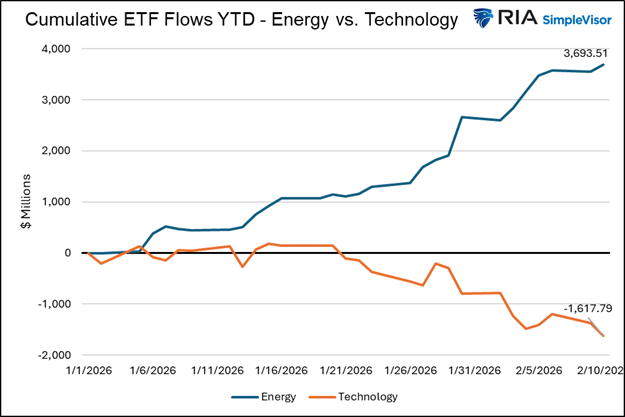

In a market dominated by passive strategies, investment decisions are often detached from traditional valuation metrics, which blurs the distinctions between classic styles such as value and growth.

Passive investors are commonly associated with broad market index funds tracking benchmarks like the S&P 500 or the Nasdaq. Yet passive capital also flows into sector- or factor-focused ETFs, including funds targeting areas such as consumer staples or large-cap growth.

While “passive” refers to not selecting individual stocks, it does not necessarily mean the investment behavior itself is passive. Increasingly, investors in passive vehicles actively trade themes and narratives, shifting capital between popular sectors and strategies.

For example, in recent months, stocks within large-value ETFs have gained popularity, while the once-favored mega-cap technology names have lost momentum. This rotation is clearly visible in the diverging performance of value and growth ETFs and sectors, as well as in the inflows and outflows among the largest exchange-traded funds.

The first chart below highlights the sharp contrast in capital flows between the Vanguard Value ETF and the iShares Russell 1000 Growth ETF.

The second chart illustrates an even wider divergence in flows between the Energy Select Sector SPDR Fund and the Technology Select Sector SPDR Fund.

All flow data presented in the charts is sourced from ETF.com.

The Value Rotation Narrative

Financial media has been heavily focused on the apparent shift from “expensive” growth stocks into supposedly “cheaper” value stocks. However, as discussed in Part One, investors are largely responding to a narrative. In many cases, market participants believe they are buying value when they are actually selling it.

The value-rotation story generally goes like this: high-beta, mega-cap growth stocks have already enjoyed strong gains and now appear overvalued and risky. As a result, investors assume the logical move is to rotate into the opposite segment of the market—smaller-cap, lower-priced, and traditionally “value” sectors.

Whether or not this reasoning is accurate, the narrative itself is influencing markets, sectors, and factor performance. Even if many so-called value ETFs do not truly represent value, capital flows continue to follow the story until investor sentiment eventually shifts.

When narratives diverge from underlying fundamentals, however, distortions can emerge. For that reason, active investors must recognize the influence of prevailing narratives while also identifying genuine value opportunities—because eventually the market tends to reward them.

Why Traditional Screens Often Miss True Value

Most value investors start their search with quantitative screens that filter for metrics such as low price-to-earnings ratios, high dividend yields, or low price-to-book multiples. While these indicators are helpful starting points, they should not be treated as definitive conclusions. Frequently, they only highlight companies that appear inexpensive on the surface.

In reality, “cheap” valuation metrics can sometimes reflect underlying problems rather than attractive opportunities. For example:

Earnings could be cyclical and currently near their peak.

The company’s business model may be weakening.

Management execution might be inconsistent.

Emerging legal, political, or structural challenges could be affecting the outlook.

Many screening models—particularly those that rely on historical data rather than forward-looking estimates—struggle to differentiate between companies that are truly undervalued and those that are simply in decline. As a result, investors often mistake statistical cheapness for genuine value.

A Forward-Looking Framework

To properly assess value, investors should evaluate companies through several valuation perspectives. Each perspective addresses a different aspect of a company’s fundamentals, and when all three point in the same direction, the likelihood of identifying genuine value opportunities increases.

These perspectives focus on the past, present, and future. Investors should ask: Does the company have a strong earnings history? Is it currently performing well? And does it have solid prospects for future growth? Just as important as earnings themselves is how the current share price compares with past results, current performance, and expected future earnings.

Past Earnings

The first step is determining whether the stock appears expensive based on its recent financial performance. Measures such as trailing price-to-earnings ratios, free cash flow yield, and profit margins help investors evaluate valuation relative to earnings and cash flow generated over the past year or two.

One-Year Forward Earnings

Forward-looking estimates are often more informative than historical metrics—but only when those projections are credible. As the legendary investor Benjamin Graham once advised, investors should limit forecasts to what can reasonably be anticipated.

Businesses with stable financial trends, durable competitive advantages, and consistent management execution generally deserve greater confidence than companies reliant on optimistic projections, uncertain economic scenarios, or speculative growth stories.

Growth-Adjusted Valuations

As discussed earlier, both trailing and forward P/E ratios can appear elevated if earnings growth is expected to accelerate. For that reason, investors often incorporate the PEG ratio, which compares valuation multiples with anticipated growth rates.

This third layer is frequently absent from many screening approaches. It is also the most challenging to evaluate, since small adjustments to growth expectations can significantly influence whether a stock qualifies as a genuine value opportunity.

Applying the Framework

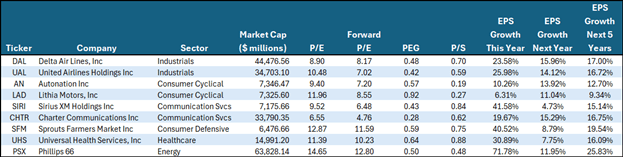

In Part One, we highlighted that companies such as Walmart and Costco—often perceived as classic value names—are not necessarily inexpensive.

Applying the three-tier framework shows that Walmart, for example, trades at a P/E ratio of 46, a forward P/E of 43, and a PEG ratio of 4.50, indicating a relatively high valuation across all three measures.

To help investors identify companies that may represent genuine value rather than merely appearing inexpensive, we developed a screening process. The companies that emerge from this screen combine relatively low valuations with solid earnings prospects and growth expectations that justify their current prices. While these stocks may better resemble true value opportunities in today’s market, they still carry risks.

The screen included the following criteria:

Market capitalization above $5 billion

U.S.-listed companies

P/E ratio

Forward P/E ratio

PEG ratio

Price-to-sales ratio

Quick ratio

Beyond the three primary valuation lenses, we also incorporated the price-to-sales ratio to reinforce the valuation assessment and the quick ratio to gauge a company’s short-term liquidity. Financial companies were excluded from the analysis because their earnings structures differ significantly from those of most other industries, making direct comparisons less meaningful.

Why True Value Often Gets Overlooked

Market outcomes are shaped not only by fundamentals but also by investor psychology and industry incentives. Many professional portfolio managers prefer to hold widely owned stocks because straying too far from benchmark indices can create career risk. Meanwhile, passive investment vehicles allocate capital according to index weightings that loosely align with their mandates, which naturally directs more money toward the largest and most established companies. Financial media narratives can further reinforce this dynamic by highlighting popular themes that attract even more capital to the same group of stocks.

These forces often create a self-reinforcing cycle: popular companies draw new inflows, rising prices follow, and the higher prices then attract additional investment. Companies that fall outside the spotlight frequently face the opposite pattern—even when their earnings and financial positions remain solid. As a result, the valuation gap between favored companies and overlooked ones can widen significantly.

For example, the companies identified in our screen generally represent only small positions in widely held ETFs. Phillips 66, the largest firm in the screen, represents just 3.78% of the Energy Select Sector SPDR Fund. Delta Air Lines and United Airlines—the next-largest companies—account for only 0.86% and 0.67% of the Industrial Select Sector SPDR Fund respectively. Their weights are even smaller in the large-cap value ETF Vanguard Value ETF.

The Value Trap

A common misconception in investing is that a stock that looks “cheap” automatically qualifies as a value investment. In reality, one of the riskiest situations is when a stock appears inexpensive but lacks the earnings strength, growth potential, or stability needed to justify its low valuation.

Take the airline sector as an example. Both Delta Air Lines and United Airlines appear in our screen as potential value candidates. However, their revenue prospects are highly sensitive to economic conditions and jet fuel prices. In addition, a meaningful share of their profits comes from airline credit card reward partnerships. If the economy slows, forecasts for strong double-digit earnings growth may prove unrealistic.

Rising jet fuel costs also pose an important question: can airlines pass those higher costs on to consumers? Another uncertainty is whether increasing competition from newer financial service providers could pull customers away from airline rewards cards tied to networks such as Visa and Mastercard.

Ultimately, genuine value investing requires both a reasonable price and credible earnings prospects. The stronger the investor’s confidence in a company’s future earnings growth, the higher the likelihood that a value investment will succeed.

Summary

Identifying true value has always been challenging, but the rise of passive investing has made the task even more difficult. Many investors today purchase “value” in name only, often through ETFs labeled with the term. These funds attract capital from investors seeking value exposure, yet fewer participants are actively searching for genuinely undervalued companies.

This dynamic can lead to a wide divergence between stocks perceived as value and those that truly offer value. Over time, such market distortions can create compelling opportunities—though investors must remain patient while waiting for those valuation gaps to eventually close.

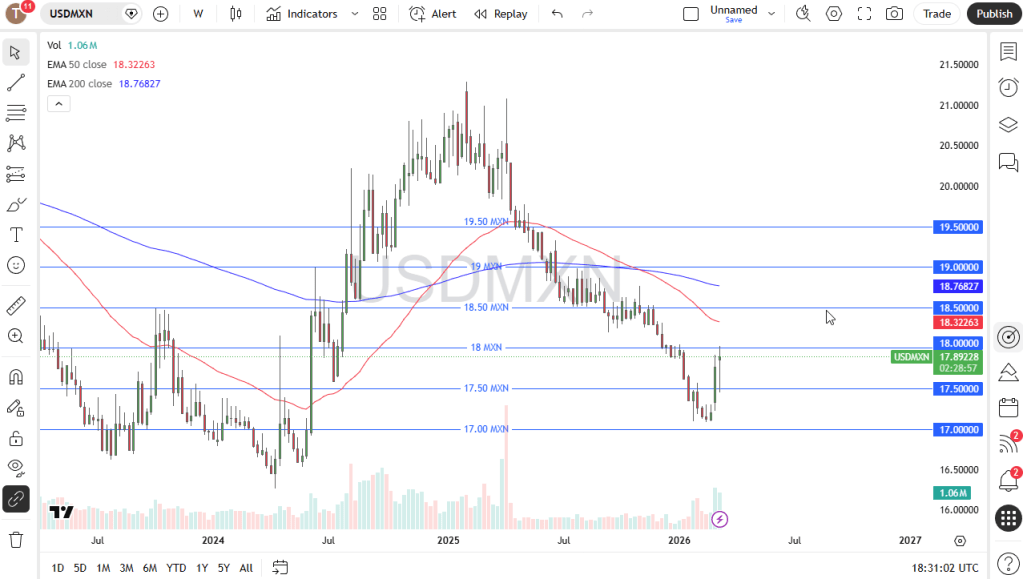

The U.S. dollar remained highly volatile over the past week as markets continued to assess the broader risk appetite outlook. The 18 MXN level still stands as a major resistance barrier, while the weekly candlestick formed a hammer pattern, signaling the potential for continued volatility. However, it is important to remember that holding long positions may carry costs due to interest rate differentials. A move lower would likely indicate a return of risk appetite in the market.

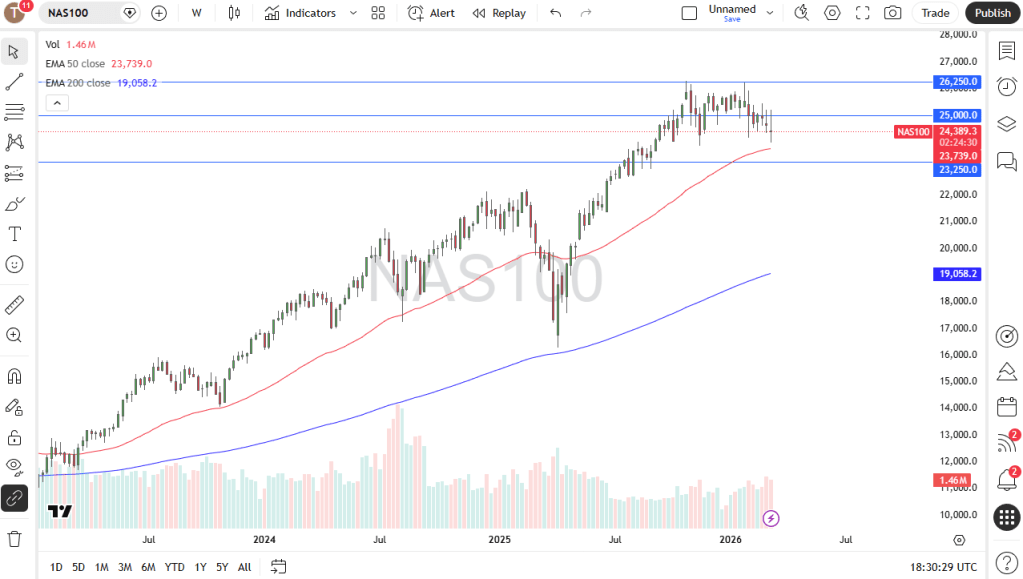

NASDAQ 100

The NASDAQ 100 experienced significant volatility over the past week, driven largely by rising U.S. interest rates and ongoing war-related headlines. Surging energy costs could also pose challenges for many AI-related companies, creating a lingering overhang that may weigh on the market. That said, a major sell-off does not appear likely at this stage. Instead, the market is likely to remain choppy, with pullbacks continuing to attract buyers.

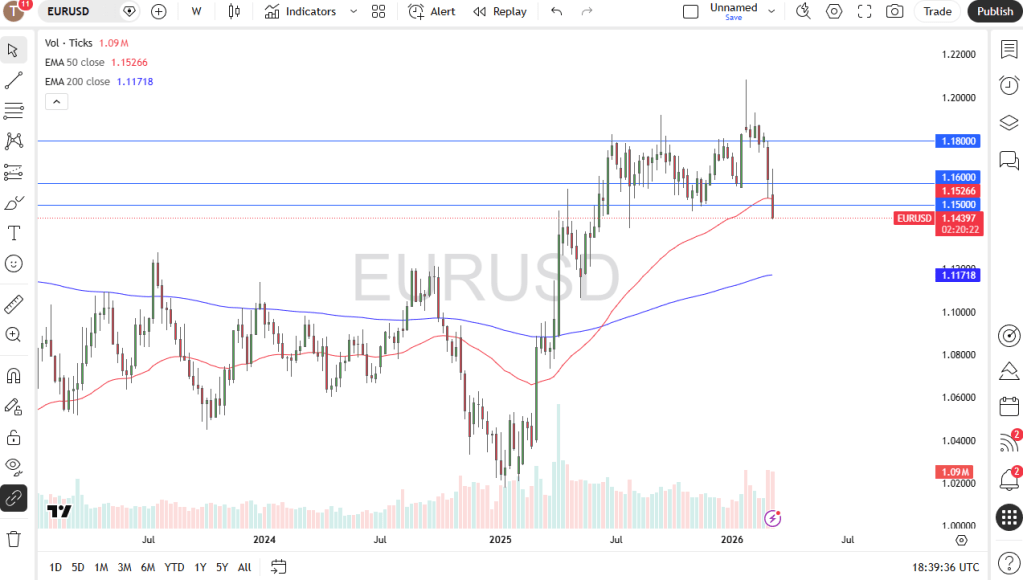

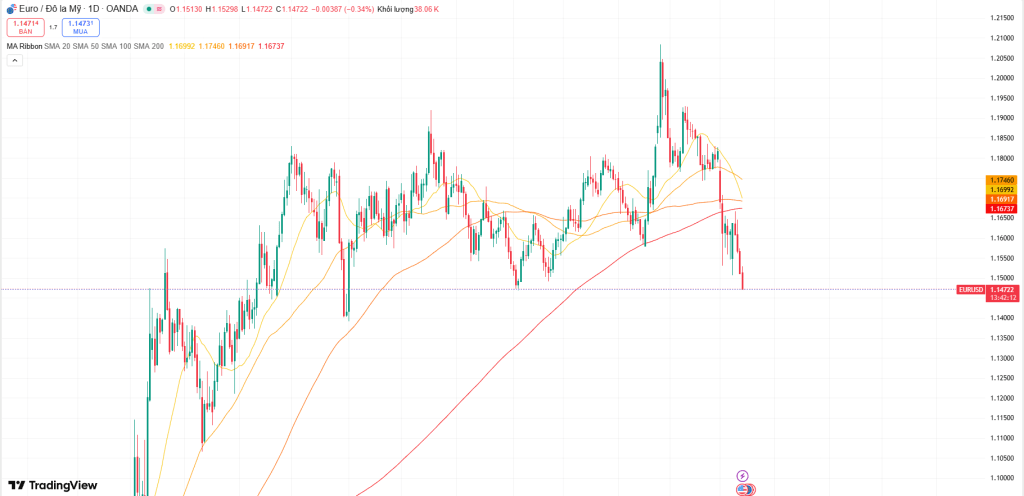

EUR/USD

The euro has declined sharply over the past week and has now slipped below the key 1.15 level, an area closely monitored by many traders. As a result, investors appear to be moving toward the US dollar in search of safety. At the same time, inflation in the United States remains persistent, leading traders to believe the Federal Reserve may have to keep interest rates higher for longer. Meanwhile, the European Central Bank must contend with potential energy shortages that could pose challenges for the continent.

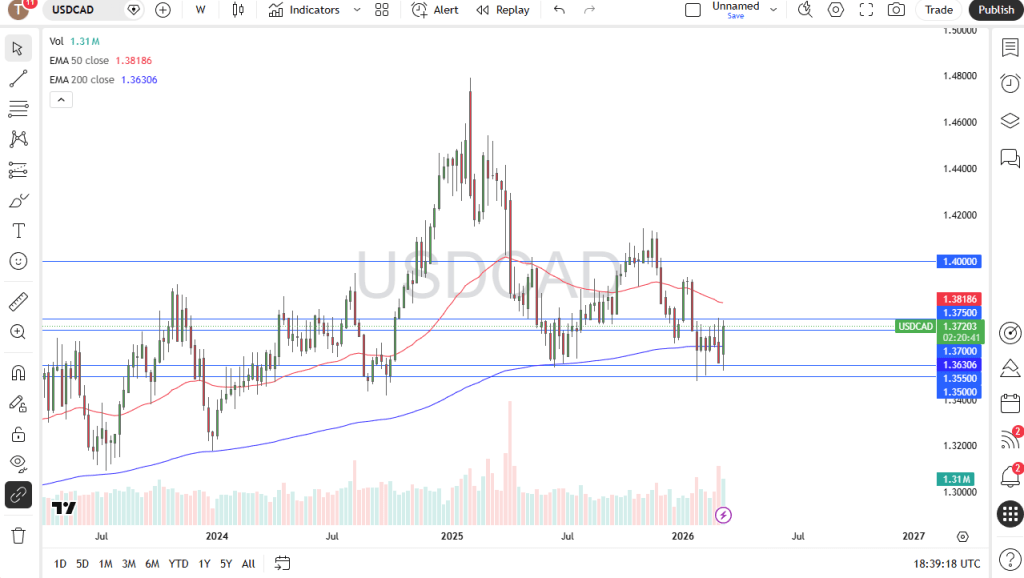

USD/CAD

The US dollar strengthened for most of the week, with the market continuing to encounter significant resistance around this area. The 1.3750 level remains a key obstacle, having acted as a strong barrier on several occasions. While higher oil prices typically support the Canadian dollar, this pair may behave differently as the United States keeps boosting its oil output, currently around 14 million barrels per day. As a result, the pair is likely to be driven largely by shifts in risk sentiment, with traders turning to the greenback during periods of uncertainty.

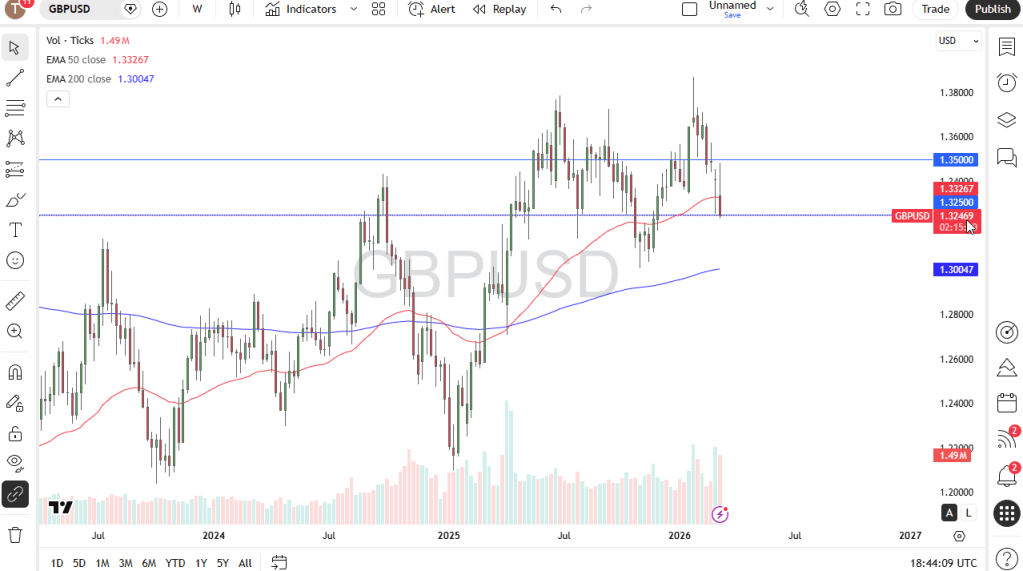

GBP/USD

The British pound attempted to rally over the past week but was sharply pushed lower as risk appetite deteriorated. GBP is now threatening a breakdown below the 1.3250 level. If it falls through that support, the next potential target could be around 1.30. Any rallies at this stage may present selling opportunities, as several factors continue to drive traders toward the US dollar. For now, buying interest remains limited, especially with ongoing war-related headlines that could continue to influence market sentiment.

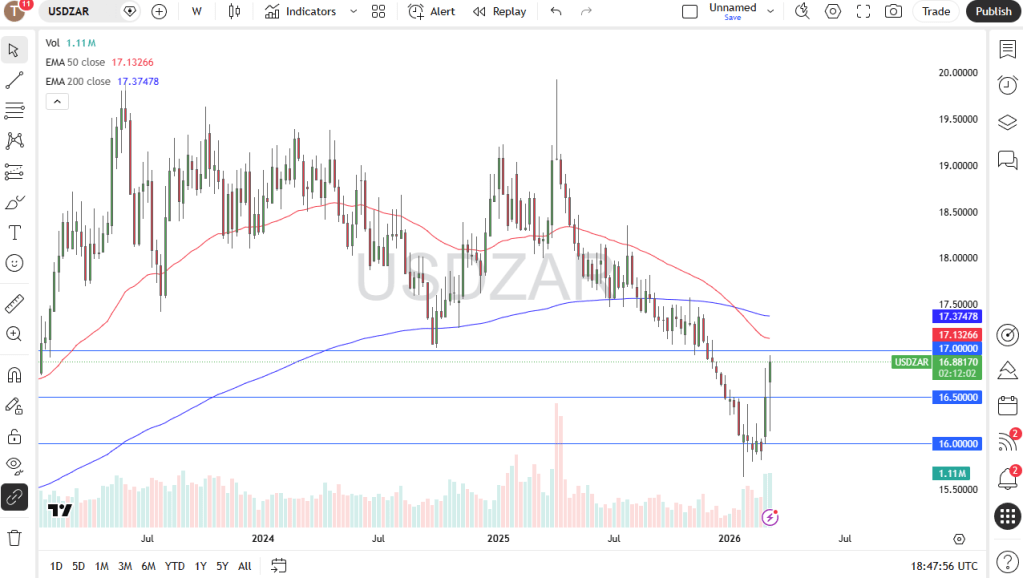

USD/ZAR

The US dollar started the week on the back foot but then rebounded sharply as traders navigated the ongoing risk aversion dominating the market. South Africa sits on the higher end of the risk spectrum, and concerns about the country’s ability to secure sufficient energy supplies are prompting capital outflows. As a result, the pair is now approaching the 17 ZAR level, a significant round and psychological threshold that many traders monitor closely. A break above this level could trigger a stronger move higher, suggesting the market is nearing a key turning point.

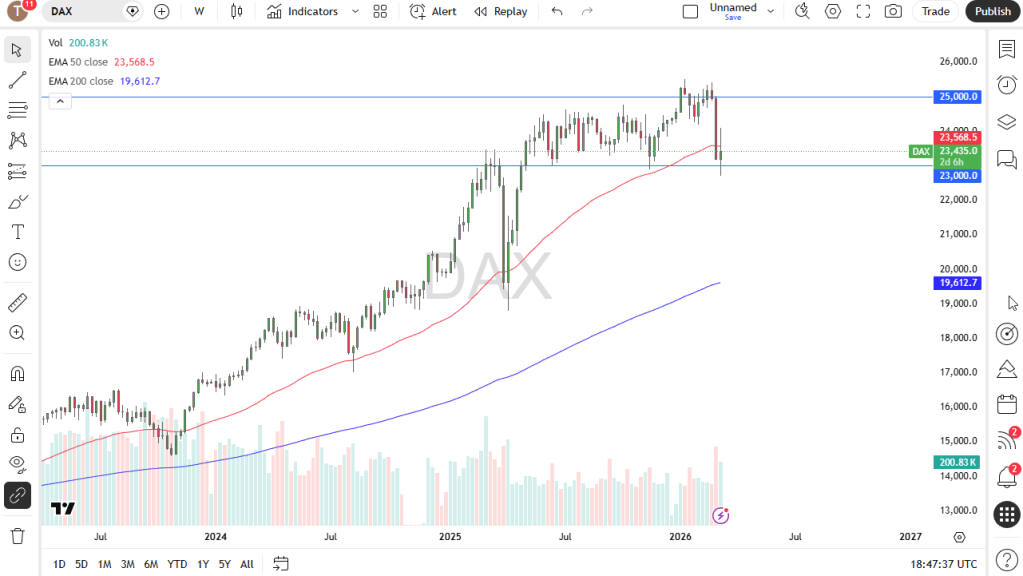

DAX

The German index has remained highly volatile, much like other markets, but it has so far managed to hold relatively steady, with the 23,000-euro level acting as a potential floor. From here, the market may attempt to recover. However, a closer look at the daily chart shows considerable choppiness, suggesting the index may be trying to form a base before any broader turnaround. If the market were to break below the 23,000-euro level, it could trigger a much sharper decline.

U.S. President Donald Trump has rejected Iranian proposals for a ceasefire, signaling that Washington intends to continue its “Operation Epic Fury” military campaign until Tehran agrees to tougher conditions, including the complete dismantling of its nuclear program.

With the conflict now entering its third week and the regional death toll approaching 3,750, the White House is reinforcing its “maximum pressure” strategy. At the same time, the effective shutdown of the Strait of Hormuz has helped keep global crude prices hovering close to $100 per barrel.

Hormuz tensions and Washington’s tougher demands

In a Saturday interview with NBC, Trump said Iran appears “ready to negotiate,” but emphasized that its current proposals do not meet U.S. strategic expectations. His refusal to scale back the offensive comes as Washington pushes for a multinational naval task force—including China, France, Japan, South Korea, and the United Kingdom—to reopen the world’s most critical maritime energy route.

The U.S. demands follow a wave of major strikes on Kharg Island, Iran’s main crude export terminal. Trump said military facilities there had been “obliterated,” though he claimed oil infrastructure was deliberately spared “out of decency.”

However, the president warned that restraint could end if Iran continues using mines and drones against commercial shipping. So far, at least 16 vessels have been targeted, prompting major oil exporters such as Saudi Arabia, Iraq, and Kuwait to scale back crude production.

Regional escalation and Fujairah’s role as a bypass

The conflict broadened overnight as Iran launched retaliatory attacks across the Persian Gulf, striking targets linked to Israel and several Arab energy hubs. The United Arab Emirates said its defenses have intercepted roughly 1,600 drones and 300 missiles since fighting began. Explosions were reported over Dubai as air defense systems engaged incoming threats.

Tensions intensified further after Tehran accused the UAE of allowing strikes on Iranian territory to be launched from its soil. Meanwhile, the port of Fujairah—a key export route that bypasses the Strait of Hormuz—resumed loading operations on Sunday after briefly suspending activity due to a drone-triggered fire.

Analysts view the stability of this alternative route as crucial to preventing a broader collapse in Gulf energy exports. Saudi Arabia also reported intercepting drones near Riyadh, while Qatar has suspended LNG shipments.

With the region’s defensive network under increasing strain, the prolonged confrontation risks turning into a sustained disruption to the global energy supply chain.

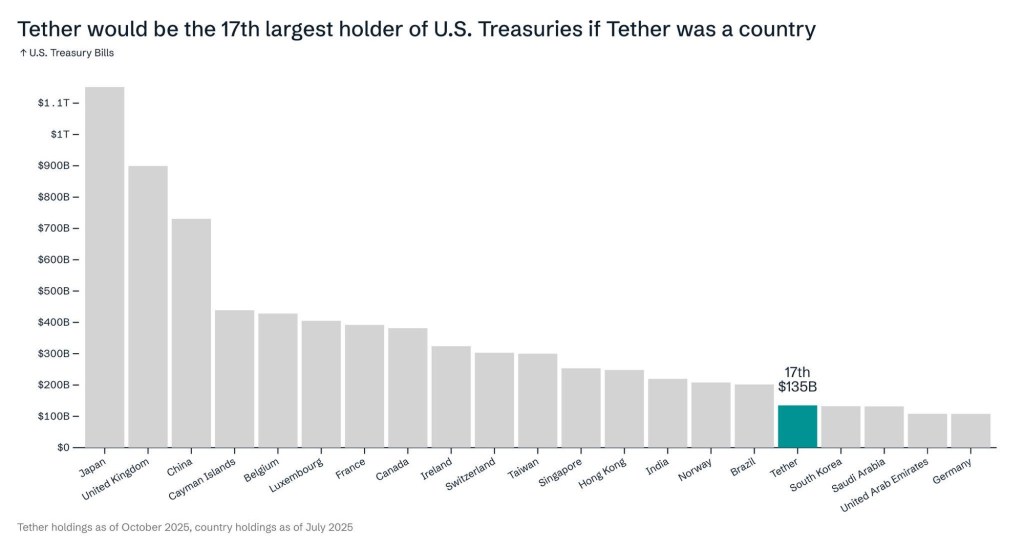

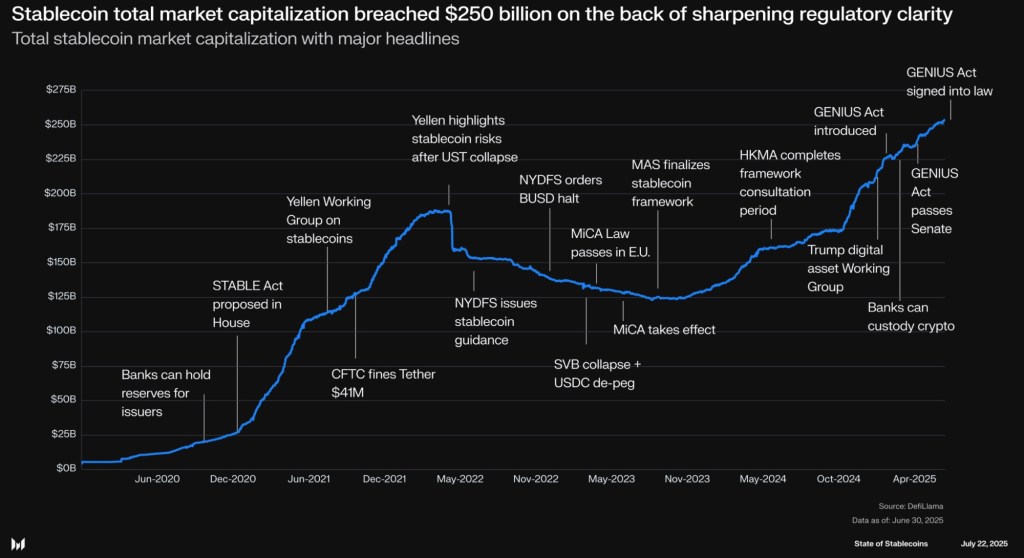

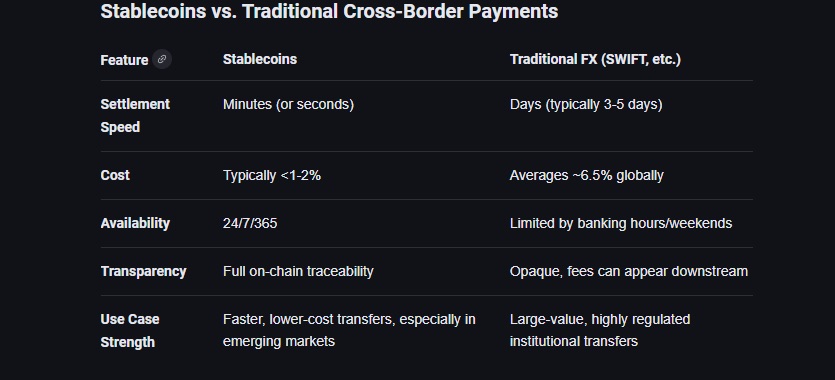

Stablecoins are transitioning from a niche cryptocurrency instrument into a macro-relevant component of the financial system, connecting global payment activity with U.S. dollar liquidity and short-term Treasury markets, according to a report from BCA Research.

The firm noted that the rapid growth of stablecoins could gradually alter parts of the global financial landscape as their use expands beyond crypto trading into areas such as payments, remittances, and tokenized assets.

Stablecoins are blockchain-based digital tokens designed to maintain a stable value by referencing another asset, most commonly the U.S. dollar. Their circulation has increased significantly in recent years, with total supply now exceeding $300 billion, compared with about $30 billion in 2020.

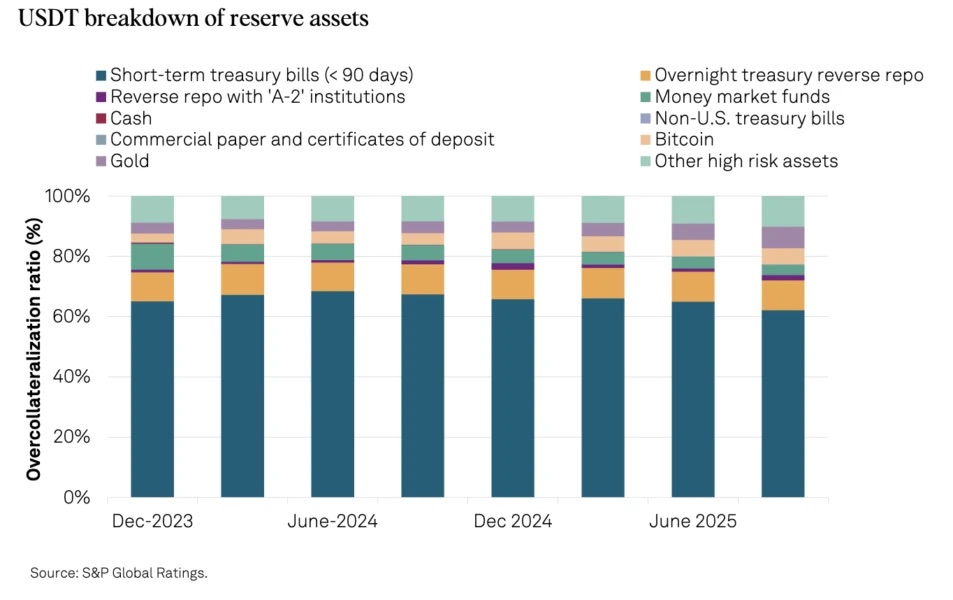

Because issuers must hold reserves to back the tokens they create, those funds are typically placed in highly liquid and low-risk assets such as U.S. Treasury bills, reverse repurchase agreements, and bank deposits. As the market expands, stablecoin issuers are becoming increasingly important marginal buyers of short-term U.S. government debt.

According to BCA, this development establishes a new channel linking worldwide payment demand to the U.S. Treasury market. Rising stablecoin issuance could boost demand for Treasury bills and potentially influence short-term interest rates, especially if new inflows represent additional capital rather than funds shifting from existing investors.

Adoption is also spreading geographically, particularly in emerging economies dealing with inflation, currency depreciation, or capital controls. In such environments, digital dollar tokens can function as a store of value and provide access to dollar-based financial services outside traditional banking channels.

This dynamic may further strengthen global demand for the U.S. dollar while creating policy challenges for governments where the growing use of digital dollars accelerates currency substitution and capital outflows.

Stablecoins may also pose competitive pressure for banks. The report highlighted that expanding digital dollar balances could divert funds from traditional bank deposits—especially non-interest-bearing transaction accounts—forcing banks to compete more aggressively to attract funding.

Despite their rapid growth, BCA emphasized that stablecoins still account for a relatively small portion of global payments and financial assets. However, continued expansion, clearer regulation, and broader institutional adoption could significantly increase their economic influence over the next decade.

Mid-tier and junior gold mining companies have largely completed reporting what has turned out to be the strongest quarter the industry has ever seen. These smaller producers—often considered the sector’s sweet spot for upside—once again broke numerous records and clearly outperformed the large major miners. In the latest quarter, mid-tier companies posted exceptional figures across the board, including revenue, net earnings, profit per ounce, operating cash flow, and cash reserves. Remarkably, early indicators suggest the current quarter could deliver even stronger results.

The main benchmark tracking mid-tier gold miners is the VanEck Junior Gold Miners ETF (GDXJ). With about $10.6 billion in assets under management as of midweek, it remains the second-largest gold-mining ETF after its counterpart, the VanEck Gold Miners ETF (GDX). While GDX is dominated by the largest mining companies, there is considerable overlap between the two funds. Despite its name, GDXJ today functions primarily as a mid-tier gold miner ETF, with true junior miners representing only a smaller share of the portfolio.

Gold mining companies are typically categorized by annual production levels measured in ounces. Junior miners generally produce less than 300,000 ounces per year, mid-tier producers generate between 300,000 and 1 million ounces, major miners exceed 1 million ounces, and the largest “super-major” companies produce more than 2 million ounces annually. On a quarterly basis, these thresholds translate to roughly under 75,000 ounces for juniors, 75,000–250,000 for mid-tiers, more than 250,000 for majors, and over 500,000 for super-majors. Among the 25 largest holdings of GDXJ, only four actually qualify as true juniors today.

In the referenced analysis table, quarterly production figures are highlighted in blue. Junior miners are defined not only by producing under 75,000 ounces per quarter but also by generating more than half of their revenue from gold production itself. This classification excludes streaming and royalty companies—firms that provide upfront capital for mine development in exchange for future production—as well as primary silver miners that produce gold as a byproduct. Even so, mid-tier miners often present more attractive investment opportunities than juniors.

The mid-tier companies dominating GDXJ offer a compelling combination of diversified production, strong growth potential, and relatively smaller market capitalizations, which create room for outsized gains. Compared with junior miners, they generally carry less operational risk, yet they tend to deliver greater upside during gold rallies than the large majors.

For many years, these mid-tier miners were largely overlooked by investors, but attention toward the group has grown recently. In 2025, leading up to gold’s mid-October peak, GDXJ surged an impressive 161.3% year-to-date. However, the sector experienced a sharp correction early in the fourth quarter as gold prices briefly retreated, sending GDXJ down 21.6% within just a few weeks. Once gold rebounded, the ETF quickly recovered, climbing another 38.9% by late December.

Interestingly, unlike GDX, GDXJ’s share price did not approach its historical highs during the quarter. The ETF originally peaked at $146.20 back in December 2010 and did not finally surpass that level until late January 2026, when gold reached an extremely overbought condition. The average price of GDXJ during Q4 2025 was about $103.33—still well below the $127.84 average recorded in Q4 2010. Even the strong rally earlier in the quarter did not push valuations to historic extremes.

At one point in early October, GDXJ traded 69.5% above its 200-day moving average, an unusually stretched level. However, this was still below the even more extreme 84.2% deviation reached in mid-2016. Over the course of gold’s massive 139.1% bull market from October 2023 to October 2025, GDXJ rose about 262.3%. That equates to only about 1.9 times leverage relative to gold’s gains, which is far below the historical pattern where smaller miners often amplify gold’s performance by three to four times.

Following a rapid correction, gold’s bull market resumed and continued climbing into late January 2026, ultimately reaching a total gain of roughly 196.4%. During that period, GDXJ increased about 387.9%, representing only around 2.0 times leverage to the metal. In other words, despite strong absolute returns, smaller gold miners have still underperformed relative to gold itself. This suggests that their share prices could still rise substantially as more investors begin to recognize the sector’s strong fundamentals.

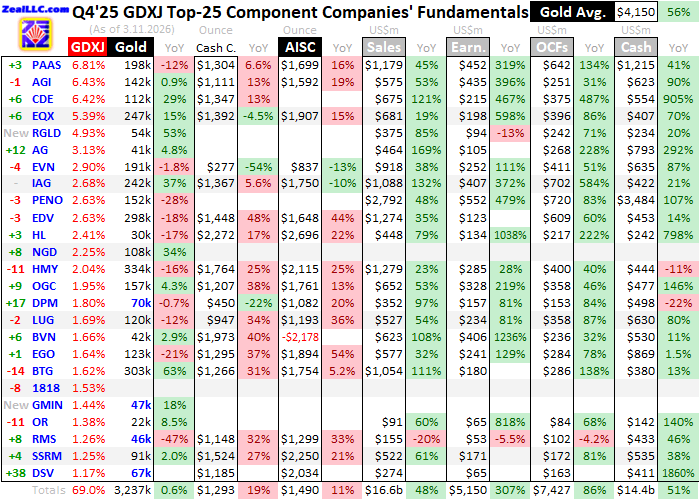

For 39 consecutive quarters, the analyst behind this research has examined the operational and financial results of the 25 largest companies within GDXJ. These firms—mostly mid-tier producers—now account for roughly 69% of the ETF’s total weighting. While reviewing quarterly reports requires extensive effort, it provides valuable insight into the underlying fundamentals of smaller gold miners and helps cut through the often misleading market sentiment surrounding the sector.

The accompanying table summarizes key operational and financial metrics for the top 25 GDXJ holdings in Q4 2025. The stock symbols listed are not all U.S. listings and are preceded by their ranking changes within the ETF over the past year. These shifts largely reflect changes in market capitalization, highlighting which companies have outperformed or lagged since Q4 2024. Each company’s current weighting within GDXJ is also provided.