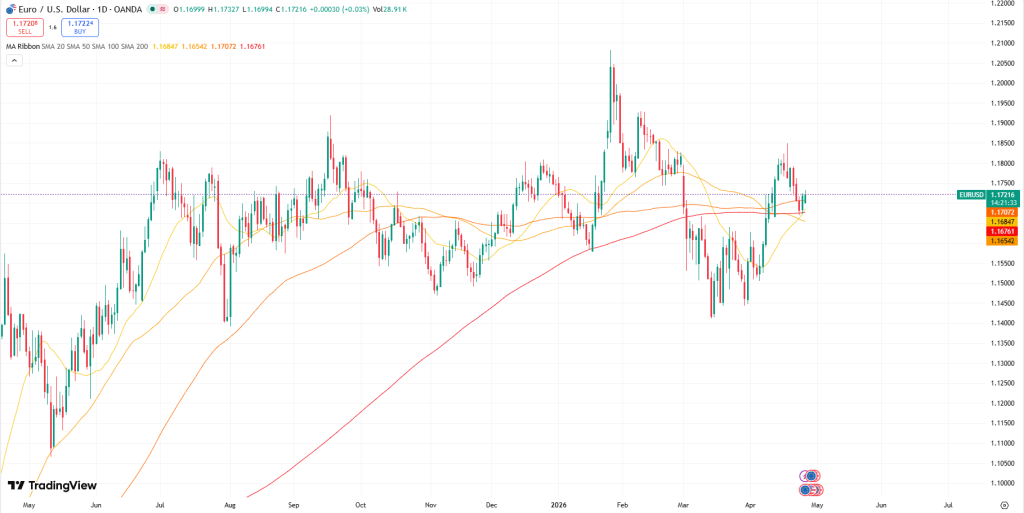

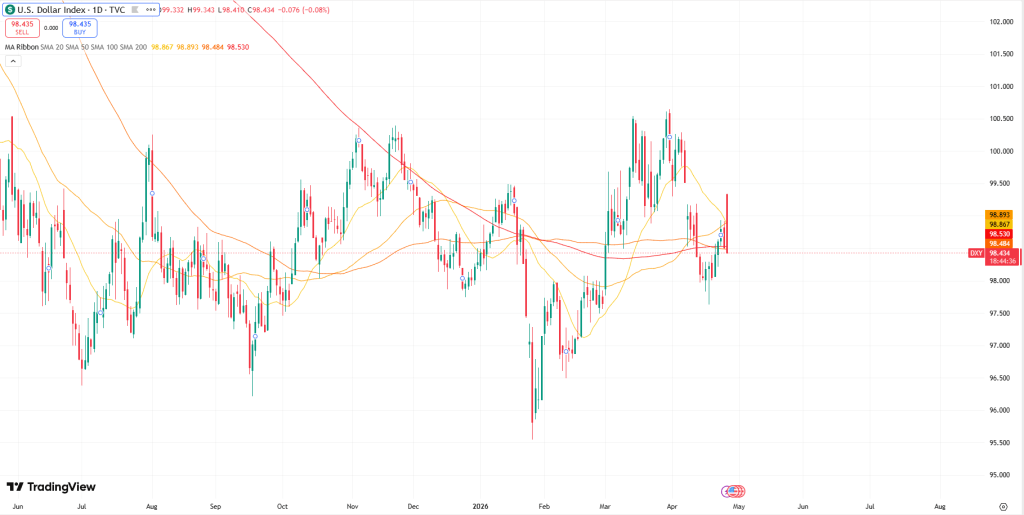

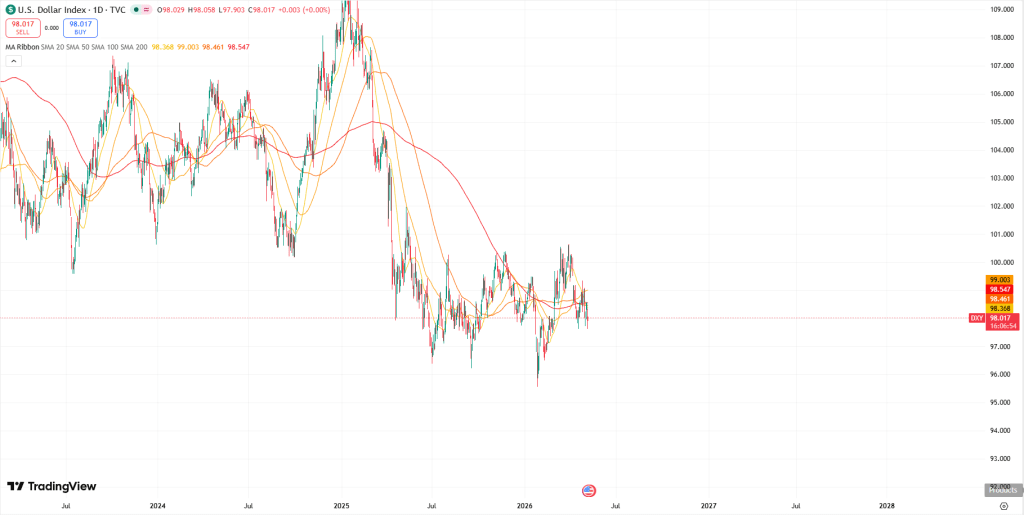

The US Dollar Index strengthened after April Retail Sales rose 0.5% month-over-month, surpassing market expectations. Meanwhile, Stephen Miran’s resignation from the Fed Board has paved the way for Kevin Warsh to take over as Federal Reserve Chair. At the same time, President Trump said US-China relations could become “better than ever,” while Chinese President Xi signaled a willingness to help ease tensions surrounding the Iran conflict.

The US Dollar Index (DXY), which tracks the US Dollar (USD) against a basket of six major currencies, extended its rally for a fifth straight session, trading near 99.10 during Friday’s Asian session.

The Greenback strengthened after the release of solid US Retail Sales data, which showed a 0.5% month-over-month increase in April, highlighting the resilience of US consumer spending despite persistently high borrowing costs.

Support for the US Dollar also came from developments within the Federal Reserve, as Stephen Miran’s resignation from the Board of Governors has opened the door for Kevin Warsh to become the next Fed Chair.

At the same time, rising inflationary pressures tied to escalating Middle East tensions have strengthened expectations that the Fed could keep interest rates elevated for longer or potentially raise them further.

Meanwhile, US President Donald Trump said on Thursday that he hopes relations with China will become “stronger and better than ever before,” adding that President Xi had offered support in helping ease tensions surrounding the Iran conflict. The improving diplomatic tone boosted market risk sentiment, which typically limits demand for the US Dollar’s safe-haven appeal.

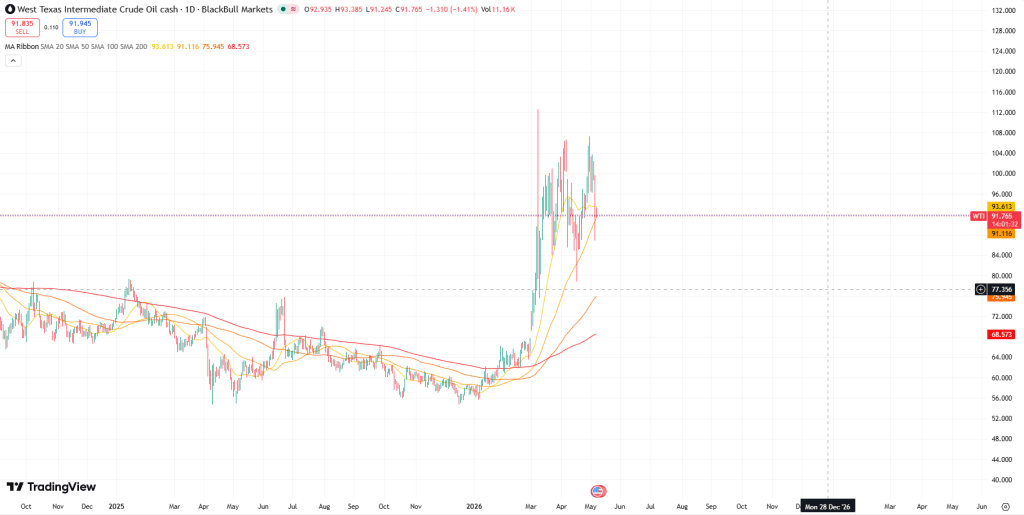

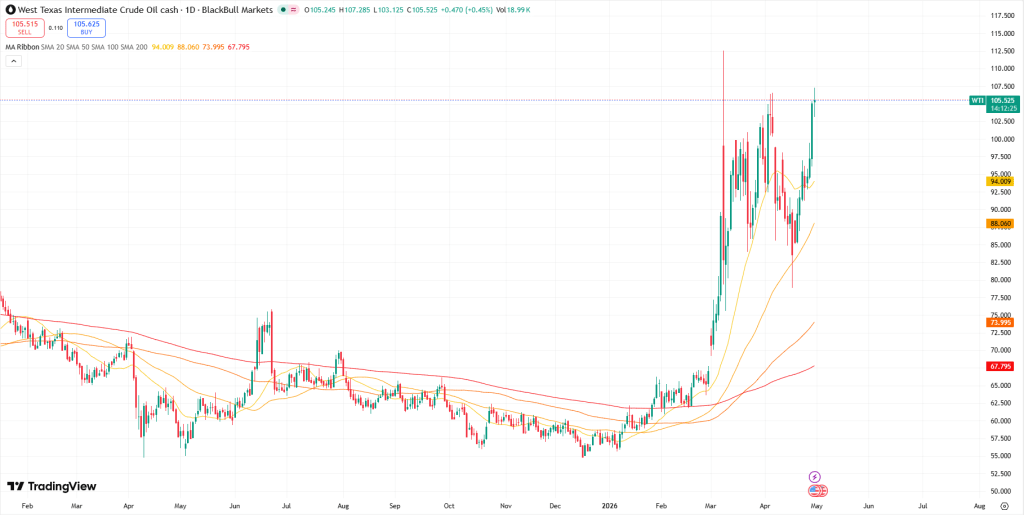

WTI edged lower after Iranian media reported that 30 vessels had successfully passed through the Strait of Hormuz. Still, crude remains on track for a weekly gain of more than 6% as stalled US-Iran negotiations continue to disrupt traffic through the key shipping route. Meanwhile, the White House noted that President Xi could increase purchases of US oil, potentially helping China reduce its dependence on the Strait of Hormuz.

West Texas Intermediate (WTI) crude remained under pressure on Friday during Asian trading, hovering near $97.60 per barrel after posting modest gains in the previous session. Despite the pullback, WTI is still set for a weekly increase of more than 6%, as diplomatic negotiations aimed at ending the conflict between the United States and Iran continue to stall, leaving the critical Strait of Hormuz effectively shut down.

Oil prices eased slightly after Iranian state media reported that 30 ships had successfully passed through the Hormuz Strait. Nevertheless, investor concerns remain elevated amid ongoing vessel seizures and attacks in the region.

The so-called “dual blockade” of the strategic waterway has become a major obstacle in peace discussions. US President Donald Trump recently described the ceasefire as being on “massive life support” after rejecting Tehran’s latest response to his proposed peace framework.

Meanwhile, a possible change in global energy trade dynamics emerged after a two-hour meeting in Beijing between Presidents Trump and Xi Jinping. According to the White House, Xi signaled interest in increasing Chinese purchases of US crude oil in an effort to diversify energy imports and reduce dependence on the unstable Strait of Hormuz route.

Still, the broader supply outlook remains concerning. The International Energy Agency (IEA) said oil and fuel shipments through the Strait fell by roughly 4 million barrels per day during March and April. The agency also cautioned that even if the conflict is resolved next month, global oil markets may continue facing significant supply shortages through October.

The market mood has shifted dramatically since late March. Back then, soaring oil prices, rising bond yields, and falling equities created a difficult environment for investors. Retail sentiment weakened, and Wall Street analysts faced growing pressure to reconsider their ambitious year-end targets for the S&P 500.

AI Reignites the Rally

Artificial intelligence once again became the market’s driving force. Semiconductor stocks rebounded sharply, with the VanEck Semiconductor ETF gaining more than 60% since its March 30 low. Volatility, as always, proved capable of moving markets in both directions.

Interestingly, the rally has not been led solely by the market’s usual AI giants. While NVIDIA has surpassed its October 2025 highs, some of the strongest gains have come from more traditional chipmakers and memory producers. Micron Technology is approaching a trillion-dollar valuation, while Intel has delivered enormous gains tied to government-backed support. Meanwhile, Asian leaders such as Samsung Electronics and SK Hynix have reinforced the global nature of the AI boom.

Bubble Concerns Return

AI dominates conversations at investor and industry conferences across sectors. Themes such as automation, scalability, and productivity improvements are everywhere, but concerns are growing as well. Investors are increasingly debating workforce reductions, weaker free cash flow in parts of the tech sector, and whether current valuations resemble the speculative excesses of the late 1990s tech bubble.

Portfolio concentration has also become a major concern. With semiconductor stocks accounting for much of the market’s outperformance, generating broad-based alpha has become increasingly difficult.

Leadership Changes Across Corporate America

Beyond macro trends, executive turnover has emerged as another defining theme. Tim Cook recently announced plans to hand leadership of Apple to John Ternus, signaling the beginning of a new era for the company. At Adobe, Shantanu Narayen also indicated plans to step away from the CEO role.

Leadership changes have been especially visible in retail, with major transitions taking place at Walmart, Target, and Lululemon. Even the investment world felt the shift, as Berkshire Hathaway’s annual meeting — often called “Woodstock for Capitalists” — took place without Warren Buffett for the first time.

The Fed Enters a New Chapter

Another major transition is happening at the Federal Reserve. Jerome Powell is set to hand leadership to Kevin Warsh, marking a potentially important turning point for U.S. monetary policy. Markets currently expect the Federal Open Market Committee to remain cautious, with interest-rate cuts largely priced out for now.

This environment has weighed heavily on financial stocks, making Financials the weakest-performing sector in the S&P 500 so far in 2026. As a result, banking conferences may carry a more subdued tone compared with the enthusiasm surrounding technology, industrials, and communication services events.

A Strong Earnings Season

Despite these uncertainties, corporate America has delivered one of its strongest earnings seasons in years. First-quarter profit growth has been impressive, and upward earnings revisions have expanded well beyond the “Magnificent Seven” and leading AI firms. Investors will now closely watch how CEOs and CIOs revise their long-term outlooks as stronger estimates are incorporated into future guidance.

Key Investor Conferences Into Mid-Year

The coming weeks feature a packed calendar of investor conferences spanning technology, healthcare, consumer, financials, industrials, energy, materials, and regional markets. Notable events include:

Apple Worldwide Developers Conference

Morningstar Investment Conference

BloombergNEF Summit Amsterdam

JP Morgan Global Technology, Media, and Communications Conference

Goldman Sachs Utilities & Clean Energy Conference

Together, these events are expected to shape market narratives around AI, monetary policy, executive leadership changes, earnings momentum, and sector rotation through the middle of the year.

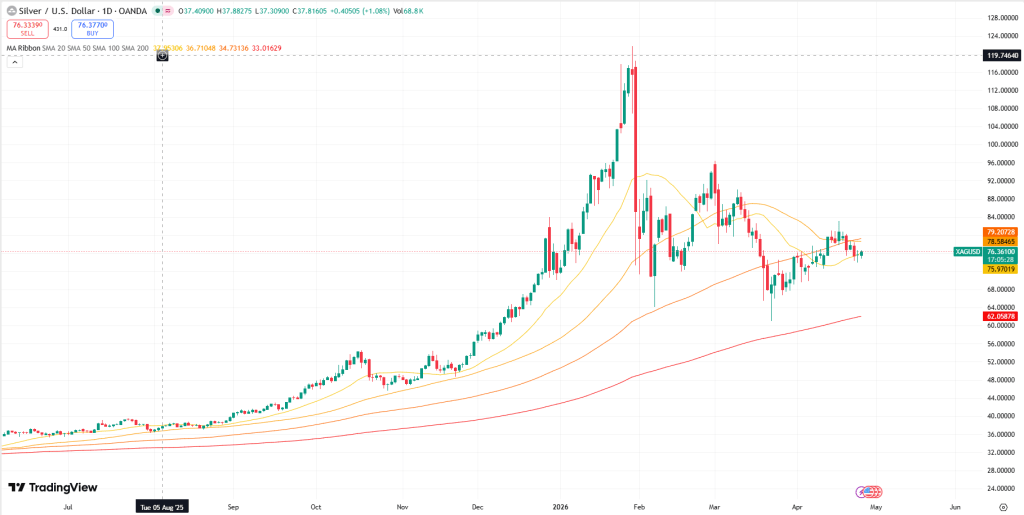

Silver surged above $85 this week after two separate single-session rallies of more than 6% — first on May 7 amid optimism surrounding Iran peace developments, and again on May 11 ahead of the anticipated Trump-Xi summit. The compression in the gold-silver ratio to 55.46, while gold itself remained relatively stable, makes the driver of the rally clear: markets were repricing industrial demand rather than reacting to fear. Around 60% of silver consumption comes from industrial use, much of it tied to supply chains dependent on US-China trade. Investors bid silver higher in anticipation that an extension of trade détente between Washington and Beijing would benefit industries with heavy silver demand.

Beneath the headline rally, however, a more important structural shift emerged on April 29 — one that could have greater implications for silver over the coming year than any individual price spike.

In the April 15 report, it was noted that March’s 3.3% CPI reading reinforced the stagflationary conditions this newsletter has been monitoring. April’s CPI, released on May 12, climbed further to 3.8% — the highest since May 2023 — confirming that the previous month’s inflation surge was not an isolated event. The Federal Reserve is now confronting a difficult combination of persistent inflation and a weakening labor market, and the events of April 29 highlighted how sharply divided policymakers have become over the appropriate response.

The Fed’s Deepest Division in 34 Years — and Why It Matters for Silver

On April 29, the Federal Open Market Committee voted 8-4 to keep interest rates unchanged at 3.50%–3.75%. The breakdown of votes was revealing: three governors argued rates should rise further, while one believed rates should already be cut. During what may be his final press conference as Fed Chair, Jerome Powell described policy as being “at the high end of neutral or perhaps mildly restrictive.” The statement reflected uncertainty rather than conviction — a central bank divided not only on policy direction, but on the broader outlook for the economy itself.

That same day, the Senate Banking Committee advanced Kevin Warsh’s nomination to replace Powell in a narrow 13-11 party-line vote, marking the first fully partisan committee vote for a Fed Chair nomination in modern history. Powell also announced he would remain on the Board of Governors after stepping down as Chair, positioning himself as a potential counterbalance to his successor. The combination of a fractured committee, a politicized leadership transition, and an outgoing Chair staying on the Board has little historical precedent.

A Federal Reserve unable to cut rates without risking higher inflation — yet unable to raise them without damaging growth — is effectively trapped. Historically, periods of monetary paralysis combined with political uncertainty at the central bank have often created favorable conditions for silver outperformance. The historical pattern is compelling enough to warrant close attention.

Three Periods of Fed Paralysis — and Three Major Silver Bull Runs

From 1978 through January 1980, the Federal Reserve repeatedly swung between tightening policy to combat inflation and easing to avoid recession, ultimately failing to fully address either problem. During that period, silver surged from $6.08 to $49.45 — a gain of more than 700% that cannot be explained solely by the Hunt Brothers’ speculative activity. Inflation exceeded 11% in 1974 and climbed above 14% by 1980, according to Federal Reserve data. The key dynamic, as documented by Fed historians, was that policymakers could not raise interest rates aggressively enough to contain inflation without severely damaging employment. Each delay further weakened confidence in the US dollar and pushed capital toward hard assets such as silver.

A similar pattern emerged between 2008 and 2011. The Fed maintained near-zero interest rates while inflation expectations increased and real yields fell into negative territory. Silver climbed from roughly $8.50 at the depths of the financial crisis to nearly $50 by April 2011, marking a gain of around 480%. Although the context differed — this time the Fed was attempting to stimulate a post-crisis economy rather than contain inflation — the underlying mechanism remained the same: a central bank unable to respond decisively contributed to dollar weakness and stronger silver prices.

The 2020–2022 period offered another example. Massive fiscal stimulus collided with a Federal Reserve that reacted slowly to accelerating inflation pressures. Silver rallied from approximately $12 in March 2020 to above $29 by August, more than doubling within five months. The Fed’s delayed tightening response allowed what was initially viewed as temporary inflation to become more persistent, while silver reflected both growing monetary instability and rising industrial demand.

Across all three episodes, the decisive factor was not simply the level of interest rates, but the Fed’s inability to commit firmly in either direction. During the stagflationary 1970s alone, silver gained roughly 1,546% over the decade as inflation averaged 7.4% annually and policymakers consistently lagged behind price pressures.

Today’s environment has not yet reached the extremes of 1979, but the structural similarities are increasingly difficult to ignore. Inflation remains elevated at 3.8%, wage growth has softened to 0.2% monthly, the US fiscal deficit has expanded to $2.065 trillion, and the Fed’s institutional independence is now openly being challenged.

The market reaction on May 8 underscored this shift. Despite a jobs report that exceeded expectations by 85%, the US dollar weakened rather than strengthened. Normally, stronger economic data supports a currency by attracting capital inflows. When a currency declines on positive economic news, markets may be signaling concern that the broader monetary framework is deteriorating faster than headline employment data suggests.

What This Could Mean for Silver

Even after climbing to $85, silver remains roughly 30% below its all-time high of $121.67 reached on January 29. While prices have risen sharply, the underlying structural backdrop remains largely intact. Metals Focus and the Silver Institute forecast a sixth consecutive annual silver market deficit of 46.3 million ounces. Meanwhile, COMEX registered inventories stand at 79.88 million ounces, with the coverage ratio holding at 13.4% — below the 15% stress threshold for a seventh straight month. The World Silver Survey 2026 also projects global silver supply to decline 2% in 2026 even as industrial demand remains above 650 million ounces annually.

The outcome of the Trump-Xi summit remains uncertain, and geopolitical tensions involving Iran are unresolved. After a nearly 13% rally in just two weeks, a short-term correction from the $85 level would not be unusual. Markets rarely move in straight lines.

However, the broader Federal Reserve dynamic described above appears less like a temporary trading catalyst and more like a structural shift in the monetary system — one that has historically created highly supportive conditions for silver. The April 29 FOMC split vote and the partisan confirmation battle surrounding Kevin Warsh did not immediately trigger a silver rally. Instead, they may have altered the long-term framework through which future market movements will be interpreted.

We are revisiting this chart due to its relevance to the current market rally. The upper panel displays the five-period Relative Strength Index (RSI), while the lower panel shows the daily chart of the SPDR S&P 500 ETF Trust (SPY). Historically, it has been viewed as a bullish signal when the RSI (5) climbs to +90 following a market low. With the indicator currently at 84.75, momentum remains strong and points to the potential for further gains. The green shaded areas highlight prior lows in the SPY, while the blue lines indicate previous instances when the RSI (5) reached the +90 level.

Over the past three years, and across the market’s last three major bottoms, the RSI (5) reached the +90 level at least twice during each recovery phase. In the current setup, the indicator has only recorded one such reading so far, though another could emerge in the near term. Historically, repeated RSI (5) readings above +90 have signaled that the rally may only be at the midpoint of a broader upward move.

The RSI (14) could climb toward the 80 level during the current advance, potentially paving the way for further upside. The indicator is currently at 76.85. As noted in yesterday’s commentary, the upper panel shows the 14-period RSI dating back to 2002, with blue dotted lines highlighting previous occasions when the RSI (14) reached 80. Historically, an RSI reading of 80 has reflected exceptionally strong market momentum and has never coincided with the final peak of a bull move.

Since 2002, the RSI (14) has touched 80 only eight times — roughly once every three years — making it a relatively rare event. Yesterday’s reading stood at 76.52, just 3.5 points below the 80 threshold. The significance of approaching 80 is that, in past cycles, it has often marked the midpoint rather than the end of a market advance. If the RSI does move up to 80 in the near term, it could provide a basis for projecting higher price targets for the ongoing rally. We will continue monitoring this chart closely going forward.

Yesterday, we highlighted the long-term outlook using the monthly RSI of the HUI/Gold ratio. A monthly RSI reading above 50 typically signals that HUI is in an uptrend, while a reading below 50 points to a downtrend. At present, the monthly RSI remains above 50, indicating that the longer-term trend for HUI — along with related indices such as GDX and XAU — remains bullish.

The chart above focuses on the intermediate-term outlook for GDX, which can weaken temporarily even within a broader long-term uptrend. The second panel from the bottom tracks the daily cumulative advance/decline line, while the panel above it shows the daily cumulative up/down volume, both for GDX. When both indicators trade above their mid Bollinger Bands, the intermediate-term trend is considered positive and is highlighted in green. Conversely, when both fall below their mid Bollinger Bands, the intermediate-term trend is viewed as negative and is shaded in pink.

Although the intermediate-term trend currently leans bearish — or more likely sideways in our view — we continue to focus on the longer-term picture, which remains constructive and bullish.

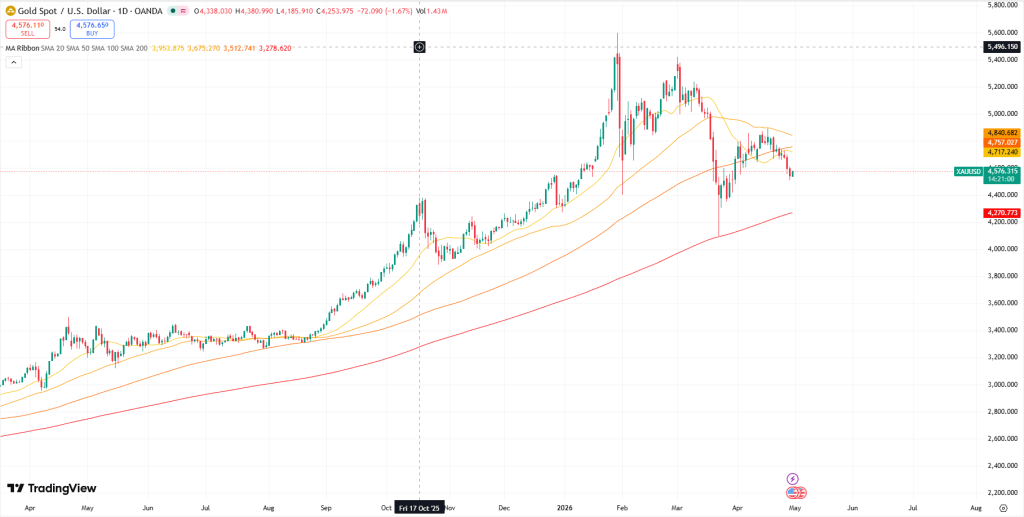

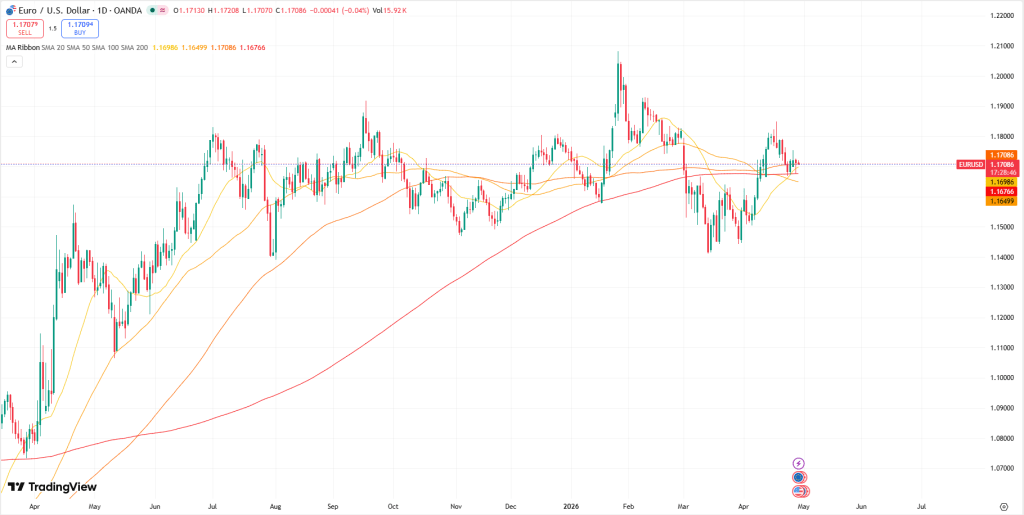

Gold prices traded sideways during Thursday’s Asian session as investors remained cautious ahead of the Trump–Xi summit in Beijing. US President Donald Trump arrived in China for talks with Xi Jinping, with trade tensions and the Iran conflict expected to dominate discussions. Meanwhile, US producer inflation surged at its fastest yearly pace in four years, lending support to the US Dollar.

Gold prices remained largely unchanged during Thursday’s Asian session as investors stayed cautious ahead of the summit between US President Donald Trump and Chinese President Xi Jinping in Beijing. Market attention is also turning to the upcoming US April Retail Sales data due later in the day.

According to Bloomberg, Trump arrived in Beijing on Wednesday for the first state visit to China by a US president in nine years. The meeting comes as Washington and Beijing attempt to stabilize relations amid ongoing geopolitical tensions linked to the Iran conflict.

The US and China are reportedly exploring a framework that would allow both countries to reduce tariffs on approximately $30 billion worth of goods without compromising national security concerns.

Meanwhile, US producer inflation rose at its fastest annual pace in four years, strengthening expectations that the Federal Reserve will keep interest rates elevated to contain persistent inflation pressures.

Data from the US Bureau of Labor Statistics released on Wednesday showed that the Producer Price Index (PPI) climbed 6.0% year-over-year in April, up from 4.3% in March and above market forecasts of 4.9%. On a monthly basis, PPI increased 1.4% after a 0.7% gain in March, significantly exceeding expectations of 0.5%.

Wholesale inflation reached its highest level since December 2022, largely driven by surging oil prices amid Middle East tensions. The stronger inflation data reinforced expectations that the Federal Reserve will maintain higher interest rates for longer, which could pressure Gold prices. Although Gold is often viewed as a safe-haven asset during geopolitical uncertainty, higher interest rates reduce its appeal because the metal does not offer yield.

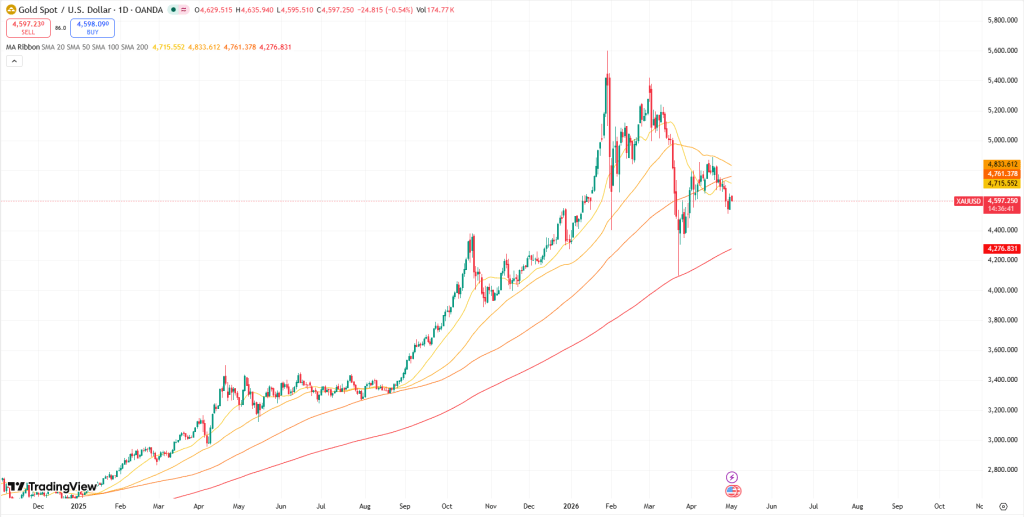

Gold Daily Chart

Technical Analysis

On the daily chart, XAU/USD is trading near $4,690 and continues to show a slightly bearish tone while remaining below the 100-day simple moving average (SMA). The metal is hovering just above the Bollinger Band midpoint, indicating short-term support within the current trading range. Meanwhile, the Relative Strength Index (RSI) stands at 49.65, reflecting neutral momentum and signaling consolidation rather than a strong directional move.

To the upside, the first resistance level is located near the 100-day SMA around $4,790. Additional gains could face resistance near the upper Bollinger Band at roughly $4,838 if bullish momentum strengthens further. On the downside, initial support is found around the Bollinger midpoint near $4,680, followed by a stronger support area close to the lower Bollinger Band around $4,518, where any deeper correction may begin to stabilize.

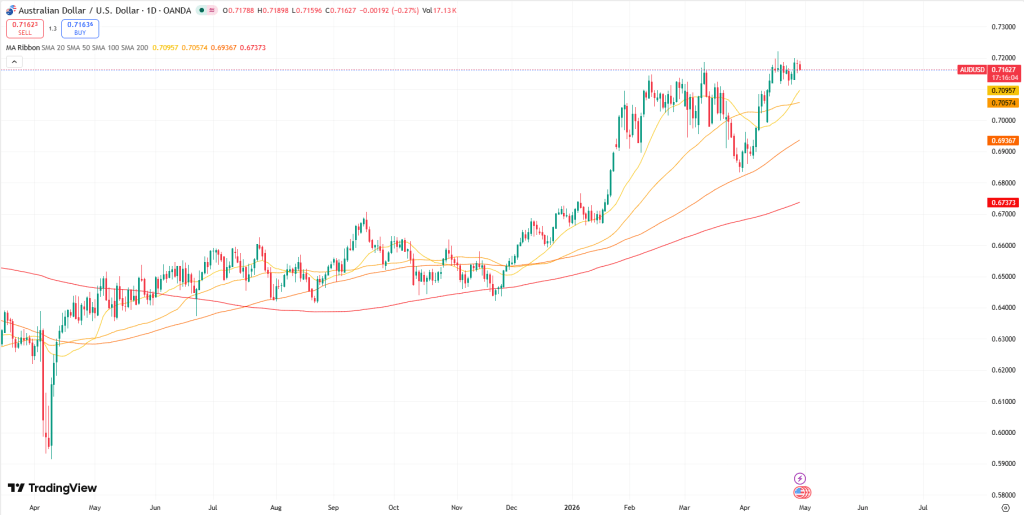

AUD/USD eases to near 0.7250 during Thursday’s Asian trading session.

US producer inflation unexpectedly posted its sharpest increase in four years.

Donald Trump is set to meet with Xi Jinping in China for a closely watched high-level discussion.

The AUD/USD pair declines toward 0.7250 during Thursday’s Asian session as stronger-than-expected US inflation figures lend support to the US Dollar against the Australian Dollar. Investors are also keeping a close eye on the summit between US President Donald Trump and Chinese President Xi Jinping in Beijing, along with the upcoming release of US April Retail Sales data later in the day.

US producer inflation recorded its strongest annual increase in four years in April, reinforcing demand for the Greenback. According to data published by the US Bureau of Labor Statistics on Wednesday, the Producer Price Index (PPI) climbed 6.0% year-over-year, up from 4.3% previously. On a monthly basis, PPI advanced 1.4% in April after rising 0.7% in March, significantly exceeding market expectations of 0.5%.

Market participants are now turning their attention to Thursday’s US Retail Sales report. Economists forecast retail sales growth of 0.5% month-over-month in April, following a 1.7% increase in March. Stronger-than-anticipated data could further strengthen the US Dollar and weigh on the AUD/USD pair.

Meanwhile, Bloomberg reported Wednesday that Trump arrived in Beijing for an official state visit, where he is expected to meet Xi Jinping to discuss trade relations and the conflict involving Iran. The trip marks the first state visit to China by a US president in nearly a decade. Any constructive outcomes from the US-China discussions may support the Australian Dollar, given Australia’s close trade ties with China.

A Bitcoin investor regained access to almost $400,000 worth of BTC after leveraging Claude AI to unlock a wallet that had remained inaccessible since 2015.

The recovery process involved AI-assisted analysis of legacy wallet files and mnemonic information to help identify the correct password.

Blockchain records later confirmed the transfer of the recovered funds, fueling broader conversations about the expanding role of artificial intelligence in cryptocurrency recovery efforts.

A Bitcoin (BTC) holder reportedly regained access to around 5 BTC — valued at nearly $400,000 — after recovering a forgotten wallet password, according to a viral post on X shared Wednesday.

The user, known on X as cprkrn, said the breakthrough came with the help of Claude AI after years of unsuccessful attempts to recover the wallet.

Crypto community reacts to AI-assisted wallet recovery

According to the post, the wallet became inaccessible after the owner changed the password and later forgot the updated credentials. Over the years, he allegedly tested countless password combinations, hired several recovery experts, and searched through old notes in an effort to regain access to the funds.

The turning point came when the user uploaded files from an old college computer into Claude AI. By combining the data with a recovered mnemonic seed phrase, he was ultimately able to decrypt the wallet and recover the Bitcoin.

“Tried ~3.5 trillion passwords + none worked, ended up matching an old seed phrase found in a college notebook with an old wallet file,” he wrote.

The user later publicly disclosed the forgotten password, triggering widespread reactions throughout the crypto community. In a follow-up post, he admitted he “would’ve been too dumb to figure it out” without the AI’s help.

Blockchain activity appears to support the claim. Wallet records linked to the address show BTC deposits dating back to April 2015, along with recent transactions consistent with a recovery and transfer of the funds to a new wallet, according to data from Blockchair.

The story quickly attracted attention from several notable figures in the crypto space, including Nic Carter, Laura Shin, and Jesse Pollak.

Importantly, the recovery depended on AI-assisted analysis of files and credentials already owned by the wallet holder, helping ease concerns about broader threats to Bitcoin wallet security.

The incident highlights an emerging use case for artificial intelligence in crypto recovery efforts. However, it does not suggest that AI can crack Bitcoin’s encryption, as the recovery relied on existing seed phrases and legacy wallet data rather than bypassing cryptographic protections.

The case also contrasts with other high-profile stories involving lost Bitcoin holdings, including the 2025 attempt by James Howells to recover a hard drive containing thousands of BTC from a landfill.

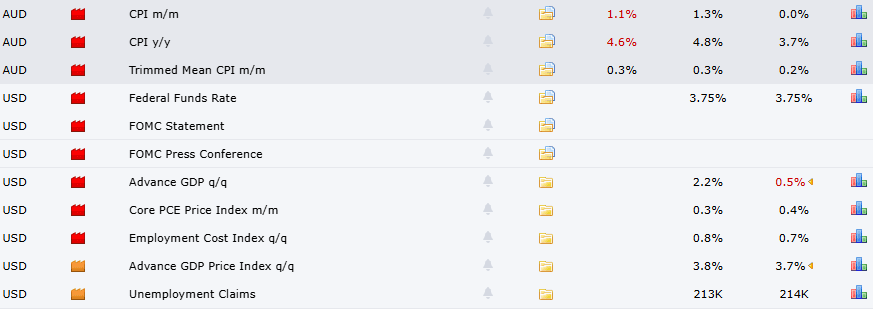

April’s CPI report delivered mixed signals. On Tuesday, the Labor Department reported that the Consumer Price Index (CPI) climbed 0.6% in April and 3.7% over the past year. Core CPI, which excludes food and energy, increased 0.4% for the month and 2.8% annually. Food prices rose 0.5%, while energy costs jumped 5.6%. Although core inflation came in slightly above expectations, Treasury yields remained relatively stable.

Shelter expenses, particularly owners’ equivalent rent, advanced 0.6% after easing in recent months. Analysts attribute much of this increase to disrupted data collection during the federal government shutdown, which may have distorted the figures.

Despite the uncertainty surrounding the report, inflation has continued to cool since the sharp rise seen in March, leading many investors to shift their attention back toward strong corporate earnings. Historically, equities have served as an effective hedge against inflation.

In periods of uncertainty, investors are often best served by focusing on fundamentally strong companies. Following an impressive earnings season, attention is now turning to upcoming results from NVIDIA and Micron Technology. Their performance could help drive first-quarter earnings growth for the S&P 500 above 20%. With demand continuing to rise for data centers and AI-related infrastructure, forecasts for the next quarter are becoming even more optimistic.

President Donald Trump is also set to begin a high-profile trip to China on Thursday, accompanied by senior officials including Treasury Secretary Scott Bessent and major business leaders such as Jensen Huang, Tim Cook, Elon Musk, and executives from ExxonMobil. The visit is widely viewed as an effort to strengthen commercial ties and reinforce U.S. economic influence amid shifting global power dynamics.

Many investors have compared today’s AI expansion to the dotcom boom of the late 1990s, when the infrastructure powering the internet was rapidly developed. The comparison makes sense given the enormous amount of capital now being invested to commercialize transformative, potentially world-changing technology. It also feels familiar because technology stocks fueled one of the strongest market rallies in history more than 25 years ago, and similar optimism is now surrounding AI, with investors aggressively raising valuations for companies expected to benefit from the trend.

The Strengths and Weaknesses of the Comparison

Although we don’t view the analogy as perfect — for several reasons discussed below — it is still useful to compare the trajectory of the tech-heavy Nasdaq-100 during the rise of AI with its performance during the early internet era, marked by the launch of Netscape, the first mainstream web browser.

As shown in the chart titled “Based on the Dotcom Era Comparison, the AI Bull Market Seems Fairly Reserved,” the recent climb in the Nasdaq-100 has been far more gradual than the explosive surge seen over a comparable four-year stretch in the late 1990s. From this perspective, the current AI-driven bull market — now approaching four years in duration — could still have significant upside ahead. Since the release of OpenAI’s ChatGPT, the Nasdaq-100 has gained more than 140%, whereas the index soared over 1,090% from Netscape’s debut to the peak of the dotcom bubble in March 2000.

We’re not suggesting history will repeat itself or that the Nasdaq-100 is destined to surge another 900% before collapsing. The broader point is that the market’s current trajectory may be more rational than many assume, and the present environment could resemble 1997 more than the euphoric conditions of late 1999 or early 2000.

Why This Cycle May Be Different

We recognize that “this time is different” can be dangerous language in investing. Still, every historical cycle has unique characteristics. While the AI boom shares some similarities with the dotcom era from a market perspective, the differences may be even more important.

Stronger market leaders.

Today’s dominant AI companies are largely financing the AI buildout through internal cash flow rather than speculative fundraising. Their business models are broader and more durable than the website-centric companies of the dotcom era, while their balance sheets are significantly healthier than those of the fiber-optic equipment firms that led the late 1990s rally. Certain AI niches may display speculative behavior, but those are not the primary drivers of the public markets.

More grounded valuations.

At the peak of the dotcom bubble in March 2000, the technology sector traded at roughly 58 times forward earnings estimates, versus about 25 times today. Back then, investors often focused on “clicks” and “eyeballs” instead of financial fundamentals. In contrast, today’s AI leaders are generally being valued based on revenue growth, earnings potential, and cash flow generation.

More mature IPOs.

Technology IPOs today tend to be larger, supported by established business models and meaningful revenue streams. Even companies that are not yet profitable often have a clearer and more believable path toward profitability than many internet startups did during the dotcom boom.

AI adoption is still in its early stages.

The current phase is centered on building AI infrastructure, while mass AI adoption has only just begun. During the late 1990s, speculative enthusiasm shifted heavily toward consumer internet companies that ultimately struggled to monetize their user bases, even after the infrastructure was built. Today, the eventual winners of the AI adoption phase remain uncertain. However, the financial strength of the infrastructure providers creates a stronger foundation for future AI-driven businesses to emerge.

Summary

There are undeniable parallels between the current AI-driven bull market and the dotcom boom of the late 1990s. Technology stocks are again leading the market, valuations are elevated, speculative pockets exist, and the underlying technological advances could reshape everyday life.

At the same time, there are key differences in the quality of market leadership, valuation discipline, the scale of speculation, and the stage of the technology cycle. Those distinctions suggest the current environment may be more sustainable than the final stages of the dotcom bubble.

Overall, the view remains constructive: this bull market may still have further room to run, with the technology sector continuing to lead. Industrials are also expected to benefit as AI infrastructure expands and adoption accelerates.

In the currency markets, Tuesdays have historically tended to favor government-issued fiat currencies over gold — though not consistently — and today happens to be Tuesday.

Fiat currencies may experience periods of strength — even lasting for years — but in the long run, they have consistently underperformed gold.

The weekly chart of gold versus fiat currencies continues to display a flag-like consolidation pattern, one that still appears to favor the bullish side.

The projected breakout target from this formation is estimated to be in the $8,000–$9,000 range.

Analysts across the gold market are debating both the origin of the flag pattern and the catalyst that could ignite the next major rally. The prevailing narrative from mainstream media and bank analysts has been that escalating US military involvement in Iran has pushed oil prices higher, increasing expectations that the Federal Reserve could raise interest rates. Because gold yields no interest while fiat currencies do, this dynamic has temporarily supported fiat over gold.

Some observers also argue that further downside pressure has come from the central banks of Iran and Russia, which may be selling gold reserves to offset declining fiat revenues and the financial strain caused by ongoing conflict.

Meanwhile, the Indian government has introduced additional taxes on bullion bank imports, encouraged citizens to reduce gold purchases, and is reportedly considering another increase in import duties.

Although the Federal Reserve has implemented some quantitative easing this year, the scale has been relatively limited.

It is worth noting that during 2010–2011, the Fed’s balance sheet expanded only modestly, yet gold prices surged sharply. In contrast, throughout 2024–2025, the Fed’s balance sheet actually contracted, but gold still dramatically outperformed fiat currencies. Why?

Commercial “QE” in the form of bank lending continues at an aggressive pace and far exceeds government-led quantitative easing. The expansion of private credit and money supply remains one of the key forces driving fiat currencies into a long-term decline against gold.

In the end, gold is an exceptionally complex form of money influenced by many different factors. Asian import duties, seasonal festivals, geopolitical conflicts, interest rates, and bank credit growth all play a role in determining gold’s fiat price.

A strong argument can be made that gold is not consistently predictable. Many analysts spend enormous effort trying to forecast movements that, in reality, may be inherently difficult — if not impossible — to predict accurately.

That uncertainty itself is one of the main reasons why millions of experienced gold investors across Asia and the West concentrate less on short-term forecasting and more on accumulating what they view as the “ultimate form of money” whenever prices weaken.

Maintaining focus on the broader macro picture is increasingly important as investors navigate persistent inflation, tariffs, the 2021–2025 geopolitical conflict cycle, elevated stock market valuations, debt ceiling concerns, and the ongoing shift in global economic power.

Although gold’s short-term direction is often unpredictable, key buying and selling zones can still be identified for both investors and traders. No one can know with certainty whether gold will reach a particular level, but if those zones are tested, market participants in the precious metals space are expected to accumulate aggressively. Historically, such phases have often led to dramatic outperformance by gold mining stocks relative to bullion itself.

I’m frequently asked, “When will mining stocks outperform gold?” My response is simple: “Whenever they enter a major buy zone. That’s where the strongest outperformance begins.”

Expecting long-term dominance from high-flying Nasdaq growth stocks over the Dow isn’t always realistic. However, when those stocks are purchased during pullbacks that bring the broader market into major support areas, they can generate remarkable gains within just a month or two — returns that the overall market might otherwise take years to produce.

The same principle applies to precious metals miners, often to an even greater degree. As a general rule, gold, silver, and copper mining stocks can deliver unleveraged fiat gains of 20% or more within one to two months after being bought at the right zones.

This year, the VanEck Gold Miners ETF has already experienced two strong periods of outperformance relative to gold bullion, and a third wave — potentially underway now — could produce even larger gains for gold-stock traders and investors.

Silver mining stock investors have also enjoyed exceptional gains this year, with the two major buy zones delivering rallies of 20% or more.

The rapid expansion of AI infrastructure and robotics is transforming copper into what some investors now call the “new oil.” The old slogan, “Drill, Baby, Drill!” may eventually evolve into, “Drill, Bonehead, Drill” — unless the drilling is for copper.

For copper stock investors, the key buy zones closely mirror those seen in gold and silver mining shares. The gold $4,400 support zone and the Dow 45,000 support zone were highlighted as attractive accumulation areas for miners before prices moved into those levels.

Historically, mining-stock ETFs and individual mining companies tend to stabilize around major support zones in both gold and the Dow. From those areas, they have often launched into powerful rallies.

The bottom line is straightforward: gold remains, in the eyes of many investors, the world’s premier form of money, while gold, silver, and copper mining stocks can become exceptional vehicles for outperformance — provided they are accumulated with patience, discipline, and careful timing.

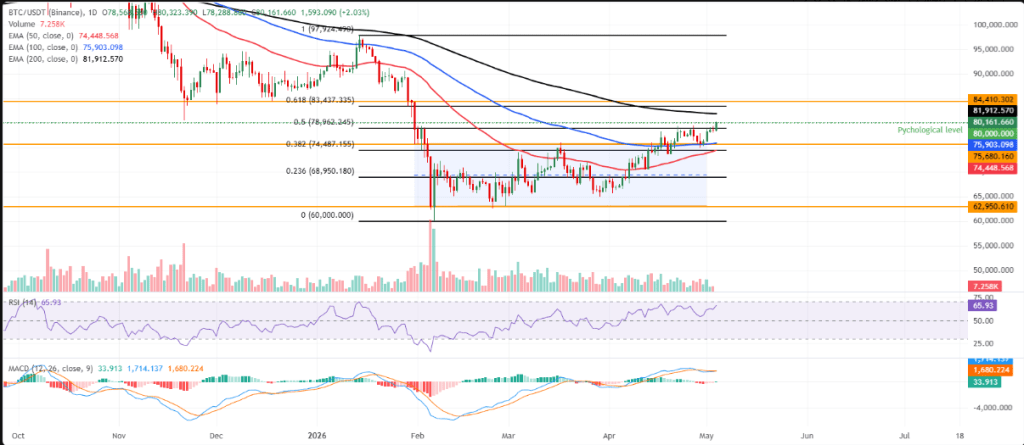

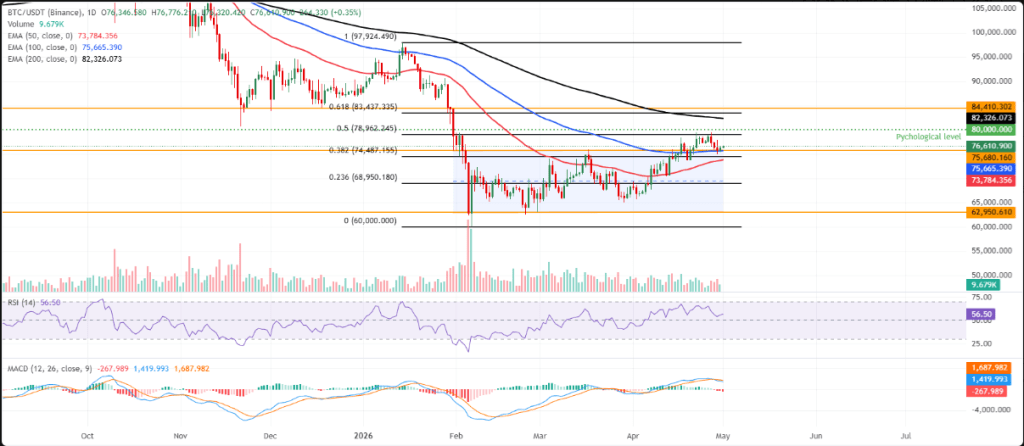

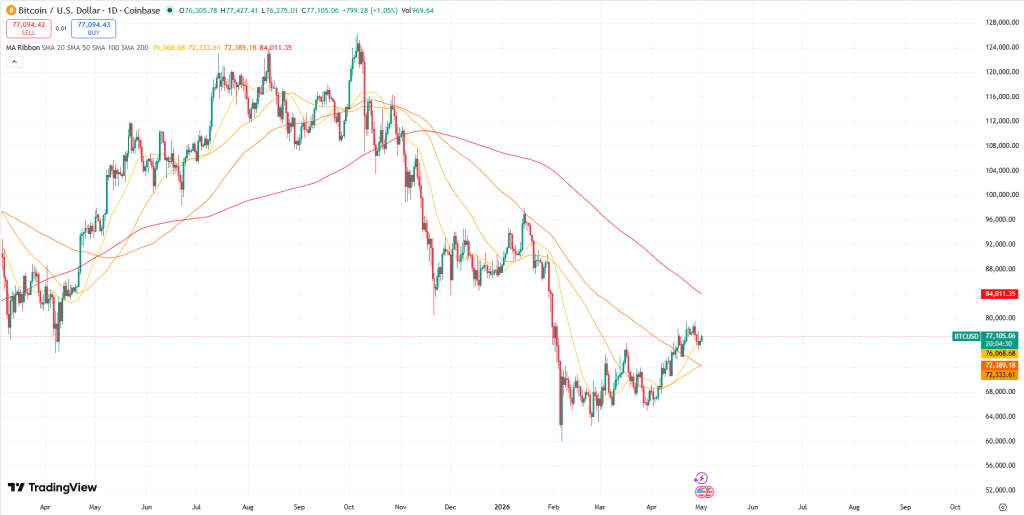

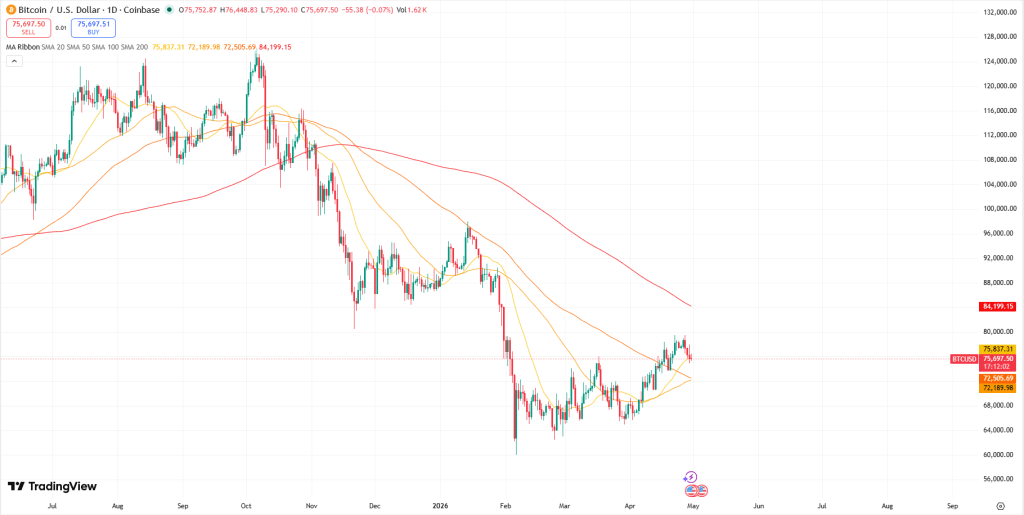

The BTC/USD pair has delivered several strong and technically reliable price swings in recent years, creating attractive trading opportunities for both investors and short-term traders.

As a result, market participants continue watching Bitcoin closely, anticipating another significant move ahead. However, Bitcoin’s recent climb to a fresh multi-month high lacked the strength and momentum seen in equities and other risk-sensitive assets during the same period. Combined with fading bullish momentum, this has raised questions about whether Bitcoin may be losing some of its long-standing market appeal, either temporarily or for a longer period.

One key reason traders are paying close attention now is that Bitcoin appears to be approaching a critical technical turning point. A closer examination of the chart shows bulls and bears are currently in near equilibrium. When price action compresses into a tightening consolidation phase like this, it often precedes a breakout that can trigger a stronger directional move, either continuing the existing trend or reversing it.

Additional factors adding to Bitcoin’s importance at the moment include:

Uncertain price action in the US Dollar, suggesting Bitcoin’s own dynamics may drive the next move;

Today’s US CPI inflation report, which could surprise markets and spark volatility.

The clearest sign that Bitcoin may be nearing a decisive move is the formation of a narrowing triangle pattern on the chart. The converging trend lines connecting recent highs and lows indicate increasing indecision and the possibility of a breakout in either direction.

That said, the pattern is not perfectly symmetrical, which slightly weakens its reliability. The ascending support trend line is noticeably steeper than the descending resistance line, making the setup less balanced than a classic triangle formation.

Another technical aspect worth noting is that, despite some softness in the broader long-term uptrend, Bitcoin still maintains a meaningful bullish structure after recently reaching fresh multi-month highs. This could strengthen the argument for an upside breakout, particularly if the price manages to break above the recent swing highs and establish itself beyond the $82,500 level.

AUD/USD Technical Analysis

One of the clearest signs that AUD/USD may be approaching a pivotal move is the formation of a tightening triangle pattern on the chart. The converging trend lines connecting recent highs and lows highlight growing market indecision and suggest that a breakout in either direction could soon emerge.

While the pair has remained confined within this narrowing structure for several sessions, the setup is not a perfectly symmetrical triangle. The ascending support line is steeper than the descending resistance line, making the formation slightly uneven and therefore somewhat less reliable as a classic consolidation signal.

Another technical factor worth monitoring is the broader trend structure. Although the longer-term bullish momentum remains relatively modest, AUD/USD has still managed to post fresh multi-month highs recently. This underlying strength may increase the probability of an upside breakout, particularly if buyers succeed in pushing the pair above nearby swing highs and sustaining momentum beyond key resistance levels.

At the same time, traders should remain cautious ahead of major macroeconomic catalysts, especially US inflation data and broader US Dollar movements, as these could determine whether the pair breaks higher or reverses lower from the current consolidation zone.

Watch Closely for US CPI Inflation Data

The primary risk for USD-related currency pairs today is the release of the US Consumer Price Index (CPI) data, widely regarded as one of the most influential monthly indicators in the Forex market.

This inflation report has the potential to trigger sharp volatility, particularly if the figures differ significantly from market expectations. Current forecasts suggest annual inflation could rise from 3.3% to 3.7%. Any meaningful deviation from that estimate is likely to have a direct impact on the US Dollar’s direction.

For instance, if inflation prints at 3.9% or higher, traders may anticipate a more hawkish Federal Reserve stance, which could strengthen the US Dollar and push this currency pair sharply lower. On the other hand, a softer reading of 3.5% or below could weaken the Dollar and fuel a strong upside move in the pair.

During major economic releases like this, market sentiment can shift rapidly, often overpowering existing technical setups and making chart patterns temporarily less reliable.

Could the Triangle Pattern Lose Its Importance?

Today’s analysis is largely based on the expectation that a breakout from the current triangle formation could trigger a decisive — or at least tradable — move in Bitcoin. However, there are several reasons why this pattern may ultimately prove less significant than expected.

First, the broader market trend still leans bullish. For traders who prefer to follow the prevailing trend, or at least avoid trading aggressively against it, a downside break from the triangle could turn into a false breakout that quickly reverses higher.

In addition, the triangle itself is not an especially convincing formation. As noted earlier, the structure lacks the balance and symmetry typically associated with stronger consolidation patterns, which reduces confidence in its predictive value.

There are also major macroeconomic and geopolitical risks that could easily overpower technical signals. Today’s US CPI inflation data has the potential to create sharp volatility across financial markets, while any unexpected developments involving tensions between the United States and Iran could rapidly shift investor sentiment.

In situations like these, strong fundamental catalysts can drive price action straight through technical levels and chart patterns, making formations such as the current triangle temporarily irrelevant.

Outlook on BTC/USD

The key focus for Bitcoin today is likely to be the direction of the eventual breakout from the tightening triangle formation. The first trend line tested could become the market’s main decision point for the session.

If price reacts positively from the ascending support trend line with a strong bullish rebound, it may present an attractive long opportunity — particularly if the nearby support level around $80,558 is also firmly defended. Such a move would suggest buyers are still in control despite recent consolidation.

On the other hand, a rejection from the upper resistance trend line could create a favorable short setup, especially if the psychologically important $82,000 level is rejected at the same time. That combination would reinforce the possibility that bullish momentum is fading near resistance.

As price action remains compressed within the triangle, traders will likely watch closely for confirmation signals before committing to a directional move.

Today’s BTC/USD Trading Signals

Risk per trade: 0.50%

Trade validity: Positions should be opened before 5:00 PM Tokyo time on Wednesday.

Long Trade Setups

Consider long positions after a bullish price action reversal on the H1 chart following a test of the following support levels:

$80,558

$79,440

$77,858

For risk management:

Place the stop loss $100 below the most recent swing low.

Once the trade gains $100 in profit, move the stop loss to breakeven.

Secure partial profits by closing 50% of the position after the first $100 gain, while allowing the remaining portion to continue running.

Short Trade Setup

Consider short positions after a bearish rejection or reversal signal on the H1 timeframe following a test of:

$81,343

Trade management guidelines:

Set the stop loss $100 above the latest swing high.

Move the stop loss to breakeven once the trade reaches $100 profit.

Take profit on half the position after a $100 favorable move and leave the rest open for a larger potential move.

Identifying Price Action Reversals

Common reversal confirmations on the hourly chart include:

Pin bars

Doji candles

Outside candles

Engulfing candles with a stronger close

These candlestick formations can help traders confirm whether support or resistance levels are being respected before entering a position.

Key Events to Watch

There are no major Bitcoin-specific events scheduled today. However, broader market volatility could increase due to important US economic developments, including:

US CPI inflation data release at 1:30 PM London time

Later remarks and developments involving the Federal Reserve Chair

These events could significantly influence US Dollar strength and indirectly impact Bitcoin price action.

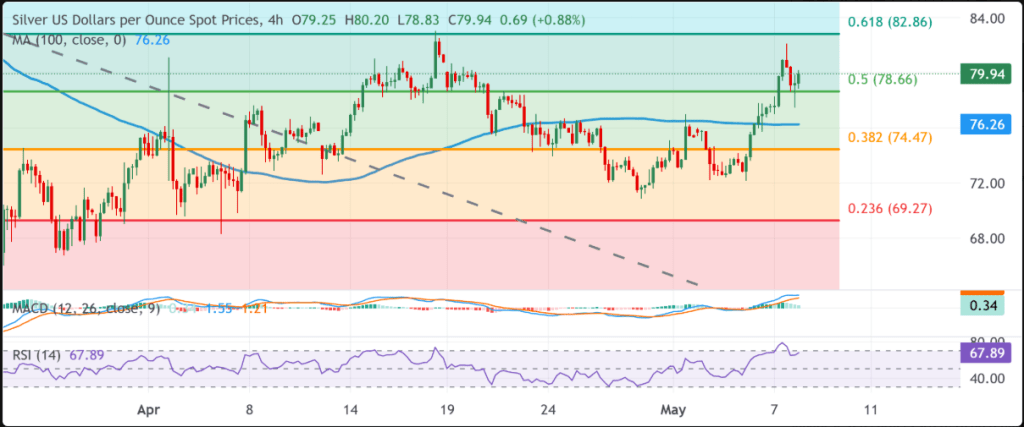

Silver gains support from its critical use in solar panels, electronics, and automotive manufacturing.

However, the precious metal could face pressure as escalating geopolitical tensions and possible disruptions in the Strait of Hormuz push oil prices and inflation higher.

Meanwhile, stronger-than-expected US inflation data has reinforced expectations that the Federal Reserve may keep interest rates elevated for longer to contain persistent inflationary pressures.

Silver prices (XAG/USD) extended their rally for a sixth consecutive session, trading near $86.80 per troy ounce during Wednesday’s Asian session. Growing industrial demand continues to support the metal, as Silver remains widely used in the manufacturing of solar panels, electronics, and automotive components.

Despite the strong upward momentum, geopolitical tensions could pose a major challenge to Silver’s advance. Concerns over a prolonged closure of the Strait of Hormuz may keep oil prices elevated, intensifying inflation pressures worldwide. This environment could encourage central banks to maintain higher interest rates for longer, reducing the attractiveness of non-yielding assets such as Silver as investors shift toward yield-bearing investments.

Tensions in the Middle East remain heightened after comments from US President Donald Trump, who stated that Iran is “under control” while warning that the situation could end either with a new agreement or complete “decimation.” Meanwhile, Iranian Deputy Foreign Minister Kazem Gharibabadi reiterated that any credible peace deal must involve compensation payments, recognition of Iran’s sovereignty over the Strait of Hormuz, and the removal of all US sanctions.

On the economic front, inflation concerns intensified after the US Bureau of Labor Statistics released stronger-than-expected April Consumer Price Index (CPI) data on Tuesday. Headline CPI rose 0.6% month-over-month, lifting annual inflation to 3.8%, the highest reading since May 2023. Core CPI, which excludes food and energy prices, also climbed 2.8% year-over-year. The data strengthened expectations that the Federal Reserve will likely keep interest rates elevated for an extended period in an effort to curb persistent inflation.

The US Dollar Index remained steady as President Trump’s remarks on the Middle East fueled geopolitical uncertainty and market volatility. Hotter-than-expected CPI figures reinforced expectations that the Federal Reserve may keep interest rates elevated for longer to contain persistent inflation pressures. Investors are now turning their attention to upcoming producer inflation data for further clues on how the conflict with Iran is affecting the broader US economy.

The US Dollar Index (DXY), which tracks the Greenback against a basket of six major currencies, held steady near 98.30 during Wednesday’s Asian session after posting gains over the previous two days. The US Dollar continued to draw support from escalating geopolitical tensions in the Middle East following recent remarks by President Donald Trump. Although Trump stated that Iran was “under control,” he warned that the situation would ultimately end either with a new agreement or with complete “decimation.” Meanwhile, Iranian Deputy Foreign Minister Kazem Gharibabadi reiterated that any acceptable peace deal must involve reparations, recognition of Iran’s sovereignty over the Strait of Hormuz, and the full removal of US sanctions.

Additional support for the Greenback came from stronger-than-expected US inflation data, which reinforced hawkish expectations for the Federal Reserve. Investors increasingly believe the Fed will keep interest rates elevated for longer in an effort to contain persistent inflationary pressures. According to data released by the Bureau of Labor Statistics on Tuesday, the US Consumer Price Index (CPI) rose 0.6% month-over-month in April, lifting annual inflation to 3.8%, the highest reading since May 2023. Core CPI, which excludes food and energy prices, also increased, posting a 2.8% annual gain.

With expectations for a Fed rate cut this year largely fading, markets are now pricing in the possibility of a quarter-point rate hike by December. Attention is now turning to upcoming producer inflation figures, which could offer further insight into how the ongoing conflict involving Iran is affecting the broader US economy.

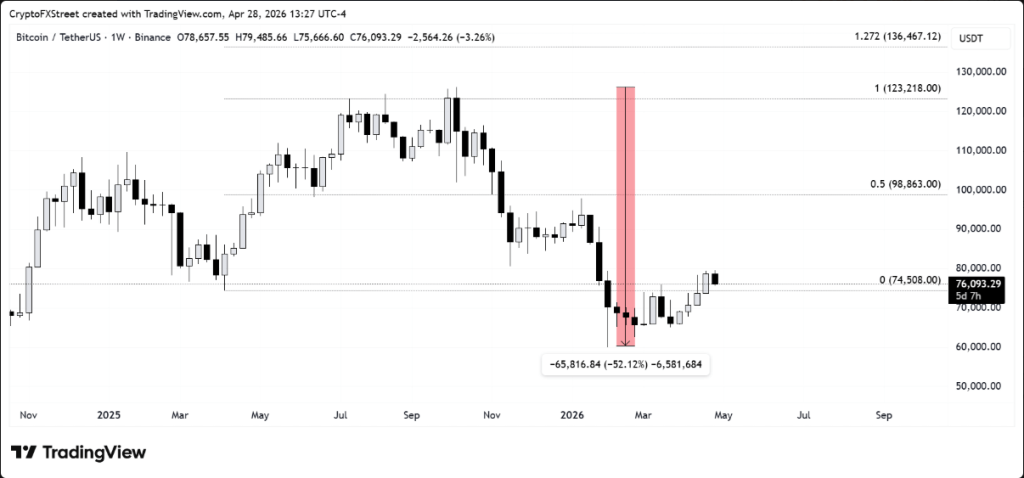

Bitcoin’s recovery pauses while the $80,000 support level remains intact, as optimism surrounding a final US-Iran peace deal begins to fade.

Market participants are also staying cautious ahead of key US economic data releases, particularly Tuesday’s CPI report.

Meanwhile, the US Senate Banking Committee is scheduled to conduct its markup hearing on the Clarity Act this Thursday.

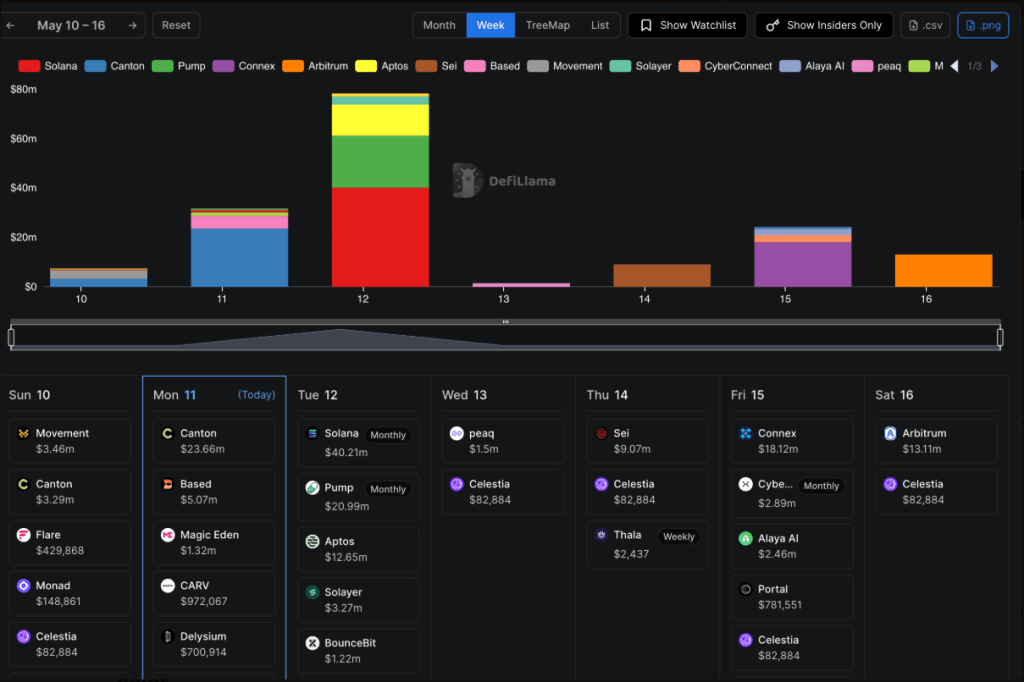

On the supply side, roughly $159 million worth of token unlocks — led by Solana’s $40 million and Pump.fun’s $21 million — may add further volatility to the crypto market.

The cryptocurrency market started the week on a subdued note, with Bitcoin (BTC) finding it difficult to maintain support above $80,000 as optimism over a final US-Iran peace agreement weakened due to growing complications in the negotiations.

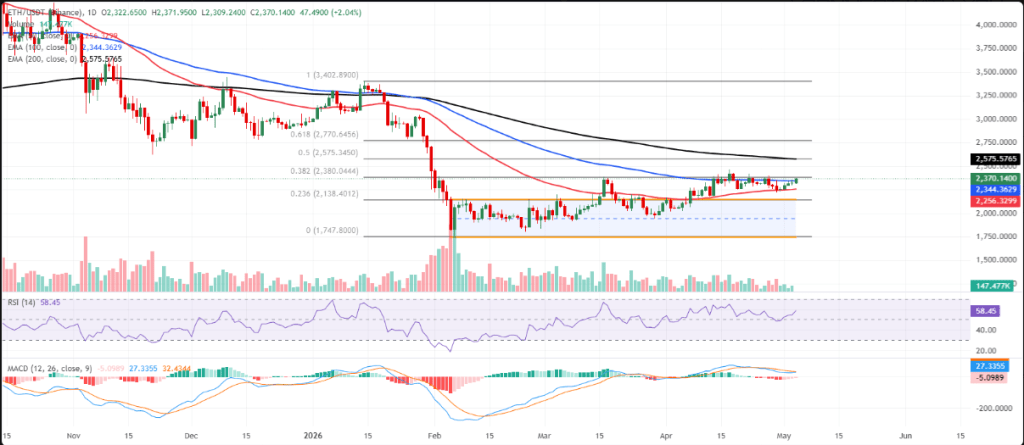

Altcoins also showed signs of fading momentum, with Ethereum (ETH) retreating from its weekly peak of $2,375, while Ripple (XRP) revisited support around $1.45 after facing rejection near the $1.50 resistance zone.

Trump rejects Iran’s peace proposal

US President Donald Trump has rejected Iran’s latest proposal to end the conflict, calling it “totally unacceptable.” The proposal, reportedly delivered to the White House through Pakistani mediators, was presented as a counteroffer to a one-page US memorandum outlining a phased framework for ending the war — a conflict that has severely disrupted the Strait of Hormuz, one of the world’s most strategically important shipping routes.

Under the proposal, Iran demanded the complete removal of US sanctions, an immediate end to the military blockade around the Strait, and concessions related to its nuclear program, including a shorter moratorium on uranium enrichment. Tehran also sought sovereignty rights over the Strait of Hormuz, including authority to coordinate maritime traffic passing through the route.

Trump has continued to maintain a firm stance on Iran’s nuclear ambitions, insisting that the country’s nuclear program must be fully dismantled.

Meanwhile, global markets remain tense as hopes for a lasting peace agreement continue to weaken amid the fragile diplomatic environment. Oil prices also remain elevated, with West Texas Intermediate (WTI) crude holding near the $95.00 level.

Caution ahead of US macroeconomic data

The US Bureau of Labor Statistics (BLS) is scheduled to release the Consumer Price Index (CPI) report on Tuesday. The CPI is the US’s main inflation gauge, tracking changes in the average prices consumers pay for goods and services such as food, housing, and transportation over time.

For investors, CPI data plays a critical role in shaping expectations for interest rates. A stronger-than-expected inflation reading could further reduce hopes for Federal Reserve rate cuts in 2026, while softer inflation data may strengthen the bullish outlook for risk assets like Bitcoin, as markets anticipate a more accommodative monetary policy stance from the Federal Reserve.

March inflation data came in above expectations, with headline CPI rising to 3.3% year-over-year, compared to 2.4% in February. Core CPI — which excludes volatile food and energy prices — increased to 2.6% in March from 2.5% previously.

Markets are now forecasting April CPI to climb further to 3.7% YoY, while Core CPI is expected to edge up to 2.7%.

Investors will also closely monitor Wednesday’s Producer Price Index (PPI) release, which measures inflation from the producer side by tracking changes in the prices businesses receive for goods and services.

Clarity Act advances to US Senate markup hearing

The Senate Banking Committee is expected to hold its long-awaited markup hearing for the Digital Asset Market Clarity Act of 2025 — commonly known as the Clarity Act — on Thursday.

The legislation had remained largely stalled after Coinbase CEO Brian Armstrong announced in January that the exchange was withdrawing its support over concerns related to stablecoin yield provisions and other aspects of the bill.

However, momentum appears to have returned following the release of a compromise draft by Senators Thom Tillis and Angela Alsobrooks. The revised text reportedly proposes banning crypto firms from offering yield on static stablecoin reserve holdings, while still permitting rewards tied to stablecoin assets actively used in certain activities. The compromise helped move the legislation forward to the next stage of the process.

At the same time, banking industry groups indicated that several concerns with the compromise proposal remain unresolved. According to a report from CoinDesk, industry representatives said they would continue providing feedback in an effort to reach a framework that supports digital asset innovation while also strengthening consumer protections.

Large token unlocks could fuel market volatility

Several cryptocurrency projects are set to unlock additional token supply into the market this week, potentially increasing short-term volatility. The schedule began on Monday with a notable $5 million unlock from Based.

According to data from DefiLlama, Tuesday’s unlocks are expected to be significantly larger, led by Solana with roughly $40 million in tokens entering circulation, followed by Pump.fun at around $21 million and Aptos with nearly $13 million.

Additional sizable unlocks later in the week include approximately $9 million from Sei on Thursday, around $18 million from Connex on Friday, and roughly $13 million from Arbitrum on Saturday.

Token unlocks often increase selling pressure as newly released assets become available for trading, which can lead to heightened price swings, particularly during periods of cautious market sentiment.

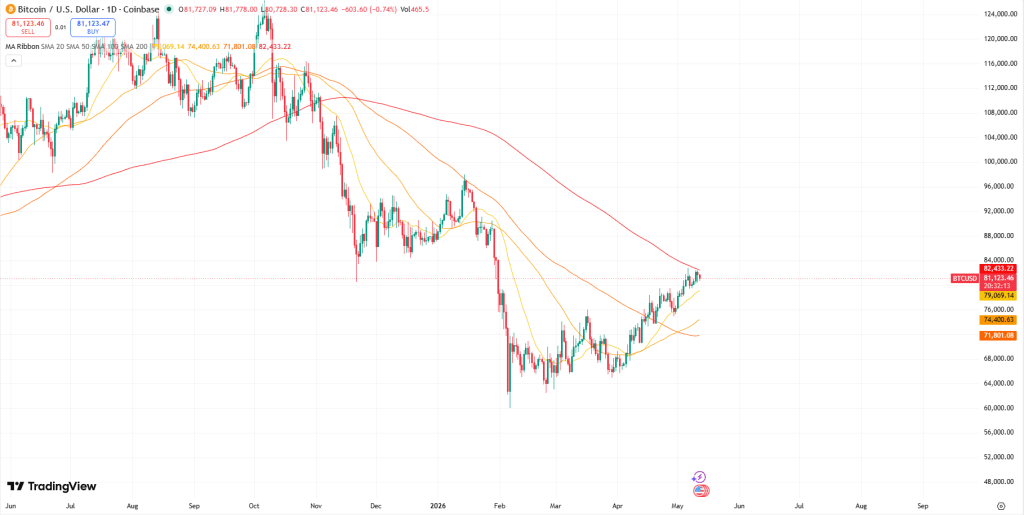

Technical outlook: Bitcoin rally loses momentum as support remains intact

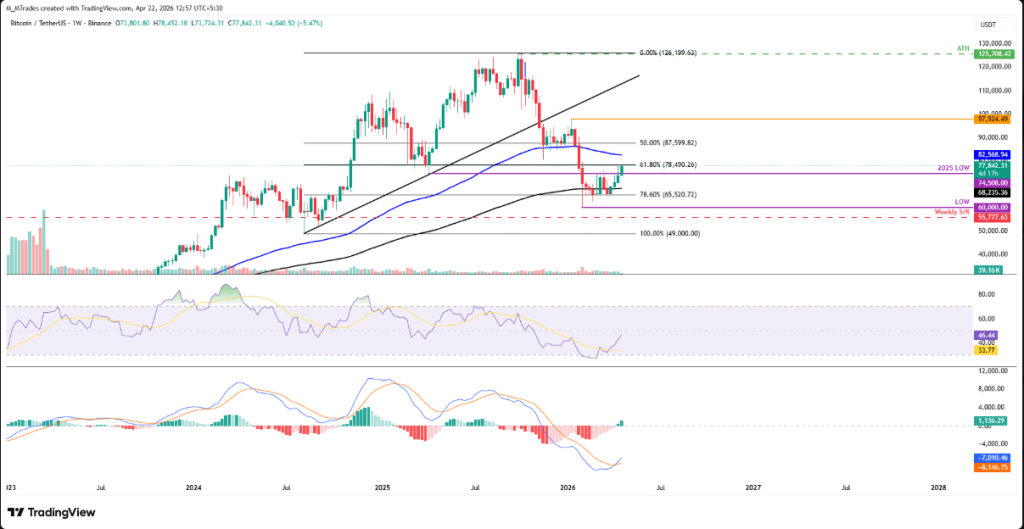

Bitcoin is trading around $81,246, maintaining a cautious tone as price action remains below the 50-week and 100-week Exponential Moving Averages (EMAs), as well as the weekly SuperTrend indicator.

Despite the near-term weakness, the 200-week EMA near $68,125 continues to support the broader bullish structure. Momentum indicators also point to consolidation rather than a sharp bearish reversal.

The Moving Average Convergence Divergence (MACD) histogram remains in positive territory, signaling that bullish momentum has not completely faded. Meanwhile, the Relative Strength Index (RSI) on the daily timeframe is hovering near the neutral 50 level, indicating that momentum is stabilizing instead of showing a decisive move higher at this stage.

On the upside, the first major resistance level appears near the 100-week EMA at $82,381, while the 50-week EMA around $85,634 strengthens a heavy supply zone overhead. A stronger bullish recovery would likely require a weekly close above the SuperTrend resistance at $91,753.

On the downside, the 200-week EMA near $68,125 remains the key structural support level for Bitcoin’s broader trend. A sustained move below this area would significantly weaken the medium-term technical outlook.

WTI prices climb toward $95.70 during Tuesday’s early Asian trading session, supported by rising US-Iran tensions and growing concerns over potential disruptions in the Strait of Hormuz. Meanwhile, markets are also watching as Trump is expected to arrive in Beijing later this week.

West Texas Intermediate (WTI), the US crude oil benchmark, is trading near $95.70 during Tuesday’s early Asian session, extending gains as renewed geopolitical tensions in the Middle East support oil prices.

According to CNN, US President Donald Trump has become increasingly dissatisfied with Iran’s approach to negotiations aimed at ending the conflict. Some of Trump’s advisers reportedly believe he is now more open to restarting major military operations than at any point in recent weeks.

At the same time, Iranian Parliament Speaker Mohammad Bagher Ghalibaf stated that Iran’s military is fully prepared to respond to any future attacks. The remarks followed Trump’s rejection of Tehran’s latest peace proposal over the weekend, describing it as “simply unacceptable.” Concerns over a potential prolonged disruption of the Strait of Hormuz — a key global energy shipping corridor — continue to provide support for WTI prices.

Meanwhile, Trump and Chinese President Xi Jinping are expected to meet on Thursday and Friday during Trump’s first visit to China since 2017. The two leaders are set to hold their first in-person talks in more than six months as both sides attempt to ease tensions linked to trade disputes, the US and Israeli conflict with Iran, and broader geopolitical disagreements.

Market participants are also awaiting the release of the American Petroleum Institute (API) crude oil inventory report later on Tuesday. A larger-than-expected decline in inventories could signal stronger demand and further support WTI prices, while a surprise increase in stockpiles may point to weaker demand or oversupply, potentially pressuring crude prices.

USD/CAD advances as escalating Middle East tensions strengthen the US Dollar’s appeal as a safe-haven currency.

President Trump has expressed growing frustration over the lack of progress in peace negotiations, raising concerns about a possible change in the region’s conflict approach.

Meanwhile, higher oil prices provide support for the Canadian Dollar, though they also create challenges for the Bank of Canada by adding to ongoing inflation pressures.

USD/CAD edges higher after closing nearly unchanged in the previous session, hovering around 1.3690 during Tuesday’s Asian trading hours. The pair is regaining upward momentum as the US Dollar strengthens amid escalating geopolitical tensions.

Investor sentiment has shifted toward safe-haven assets following reports of worsening diplomatic conditions in the Middle East. Markets are increasingly pricing in the risk of renewed large-scale military conflict, a development that typically drives demand for the Greenback against more risk-sensitive currencies.

A CNN report published Monday stated that US President Donald Trump has become increasingly dissatisfied with the lack of progress in negotiations aimed at ending regional hostilities. Sources close to the administration indicated that Washington is now giving more serious consideration to renewed military operations. Adding to market concerns, Iranian Parliament Speaker Mohammad Bagher Ghalibaf said, according to Reuters, that Iran’s armed forces are fully prepared to respond to any future attacks, placing the already fragile ceasefire under additional pressure.

Despite broad USD strength, the Canadian Dollar continues to receive support from rising oil prices. As Canada is the largest crude supplier to the United States, the CAD tends to benefit from gains in energy markets. Concerns that escalating regional tensions could disrupt global supply flows and reduce Middle Eastern exports have pushed crude prices sharply higher, helping cap further upside in USD/CAD.

At the same time, surging energy prices are reviving inflation concerns in Canada. March inflation data already reflected the impact of volatile oil prices, with annual CPI rising to 2.4%, the highest level seen in a year. While elevated crude prices generally strengthen the CAD, they also complicate the Bank of Canada’s policy outlook. Although the BoC recently kept interest rates unchanged and suggested that energy-related inflation may remain temporary, a prolonged geopolitical conflict could eventually force policymakers to reconsider their current stance.

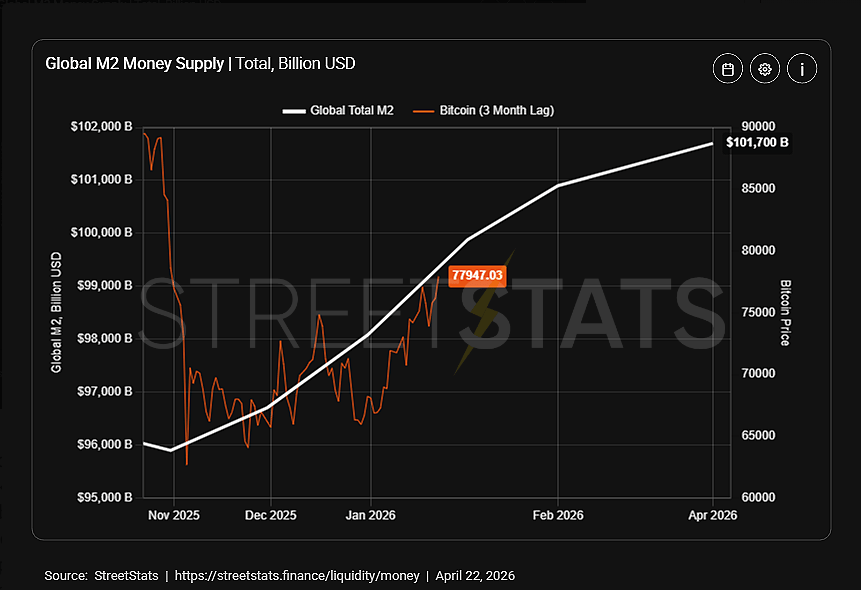

Gold advocates often argue that an expanding supply of dollars automatically weakens the currency: more money in circulation means each dollar buys less, prices rise, and gold serves as the ultimate hedge against this erosion of purchasing power. From this perspective, growth in the money supply is treated as inherently inflationary.

However, this view is overly simplistic for two main reasons. First, it strips away important context around how and why money supply expands. Second, it ignores a crucial driver of inflation that is just as important as supply itself: the velocity of money.

A recent commentary by Michael Oliver of Momentum Structural Analysis prompted a closer look at this debate. He points out that M2 has increased by roughly 45% since 2020, implying a steady erosion in the real value of cash “year by bloody year,” while reinforcing gold’s role as a preferred alternative store of value. While this is a persuasive narrative, the link between money supply expansion and inflation is not as direct or mechanical as often implied, and requires a more nuanced interpretation of M2 dynamics.

It is also worth noting that Oliver’s bullish stance on gold is not based solely on M2 growth. He also cites several additional factors, including the long-term debasement of fiat currencies by central banks, supportive technical structures, declining confidence in central bank credibility, geopolitical tensions increasing safe-haven demand, and persistent fiscal deficits that necessitate continued monetary accommodation.

Context Matters

Simply pointing to M2 growth in isolation is not meaningful without proper context. To clarify this point, we can refer back to a recent Commentary.

If inflation is the key reason for buying or selling gold, then what truly matters is how money supply growth compares to economic growth. On that basis, the picture changes significantly. During 2020 and 2021, M2 expanded far more rapidly than the real economy. However, in the years since, money supply growth has slowed considerably. Over the broader six-year period referenced by Oliver, GDP growth has actually modestly outpaced M2 expansion.

Assuming, for simplicity, that monetary velocity remains stable (a topic we address separately below), the implication is clear: M2 growth was strongly inflationary during 2020–2021, but in the current environment it is, at best, neutral—and may even be disinflationary or deflationary.

The intuition is straightforward. If an economy produces 10% more goods and services, but the money supply only expands by 5%, there is relatively more supply of goods than purchasing power. That imbalance forces either price reductions or rising unsold inventories. In both cases, the pressure on prices is downward rather than upward.

In that sense, if gold is being held primarily as a hedge against inflation, then relying on M2 growth alone may have been a reasonable argument during the pandemic-era monetary surge. But under current conditions, that same rationale is far less convincing without additional supporting factors.

Monetary Velocity Also Matters

Consider a simple thought experiment.

What if the government secretly printed an enormous amount of money, locked it away in a vault, and permanently lost the key? Would that sudden increase in the money supply drive prices of goods and services higher?

The answer is no—it would have virtually no impact.

Now imagine a different scenario: rumors of that hidden stockpile begin to circulate. Even though the money still isn’t being spent, expectations shift. People start to anticipate future spending, and that change in behavior alone could begin to influence prices.

The distinction here is important. Inflation is not determined solely by how much money exists “on paper.” It also depends on how actively that money is used—how quickly it circulates through the economy. This is what economists refer to as monetary velocity.

In other words, price levels are shaped not just by the supply of money, but by the willingness and ability of households, businesses, and institutions to spend it. When velocity is high, money changes hands quickly and exerts more upward pressure on prices. When velocity is low, even a large money supply may have limited inflationary impact.

This is why analyzing inflation through M2 alone can be misleading: without considering velocity, the picture is incomplete.

What Is Monetary Velocity

According to the Federal Reserve Bank of St. Louis, the velocity of money refers to the rate at which a single unit of currency is used to purchase domestically produced goods and services over a given period of time. In simpler terms, it measures how often each dollar is spent within the economy.

Put differently, it reflects how many times one dollar changes hands to facilitate transactions during a specific timeframe. When monetary velocity rises, it indicates that more economic transactions are taking place between individuals and businesses, signaling a more active flow of spending.

Velocity is therefore influenced by both economic activity and the money supply. A shrinking money supply does not necessarily imply lower prices if economic activity is strong and money is circulating rapidly—velocity can rise and still exert upward pressure on prices. Conversely, even if the money supply expands significantly, inflation may remain muted if that money is not actively being spent, meaning demand for goods and services stays weak and price pressures remain limited.

In short, monetary velocity helps explain why the relationship between money supply and inflation is not mechanical: it is the interaction between how much money exists and how quickly it is used that ultimately matters for price dynamics.

What Impacts Velocity?

Monetary velocity doesn’t move randomly—it reflects how people, businesses, and financial systems behave. A range of economic and psychological factors can either accelerate or slow the rate at which money changes hands.

Factors typically associated with higher velocity

These conditions encourage spending, investing, and faster circulation of money:

Lower interest rates — reduce the incentive to hold cash, encouraging spending and investment instead

Strong consumer and business confidence — optimism about the future leads to higher spending activity

Rising inflation expectations — if people expect prices to increase, they tend to spend sooner rather than later

Easy credit conditions — abundant lending increases effective purchasing power and transaction volume

Technological innovation — new products, services, and platforms create additional channels for spending

Income and wage growth — higher earnings support more frequent and larger transactions

Economic expansion — growing output naturally leads to more economic exchanges per unit of money

Factors typically associated with lower velocity

These conditions encourage saving, caution, or reduced spending:

Recessions or economic uncertainty — fear leads households and firms to defer spending

Expectations of falling prices (deflation) — consumers delay purchases in anticipation of cheaper goods later

Debt reduction (deleveraging) — paying down loans removes credit-driven money from active circulation

Aging populations — older demographics generally spend less and save more

Financial or banking stress — tighter credit conditions reduce lending and the “multiplier” effect of money

The key takeaway

Velocity is ultimately a behavioral and structural variable. It reflects confidence, incentives, credit conditions, and demographics—not just monetary policy or money supply figures. This is why two economies with similar M2 growth can experience very different inflation outcomes depending on how actively money is being used.

M2 and Core CPI

With a clearer understanding of monetary velocity, we can re-examine the common claim among gold advocates that M2 growth and inflation move closely together.

To test this more rigorously, a regression analysis is conducted using quarterly data on M2 and monetary velocity against Core CPI since 2010.

In this context, Core CPI is used instead of headline CPI because it excludes volatile food and energy components. These categories are often influenced by short-term shocks such as geopolitical events or weather conditions, which can obscure underlying inflation trends. By focusing on Core CPI, the analysis aims to capture a more stable and statistically meaningful relationship.

The first step of the analysis examines how M2 alone relates to Core CPI, allowing us to quantify the direct association between money supply growth and underlying inflation over time.

The results suggest that M2 growth, in isolation, has a very weak and statistically insignificant relationship with Core CPI. The R-squared value of 5.13% implies that changes in M2 explain only a small fraction of the variation in Core CPI over the sample period. In practical terms, most inflation dynamics are driven by other factors outside the money supply variable alone.

The negative t-statistic (-1.771) further indicates that the estimated relationship is not only weak but also inversely signed in this model specification—meaning that, within this dataset, higher M2 growth is associated with slightly lower Core CPI. However, this relationship is not statistically robust and should not be interpreted as causal.

Using the regression equation to forecast Core CPI from M2 alone therefore produces unreliable results. As expected from the low explanatory power of the model, the output has little predictive value and is effectively not useful for practical forecasting.

Overall, the takeaway is that M2 by itself is a poor standalone indicator of inflation dynamics, reinforcing the importance of incorporating additional variables—such as velocity, credit conditions, and broader economic activity—when analyzing price pressures.

M2, Velocity, and CPI

Next, we extend the analysis by incorporating monetary velocity into the multiple regression framework alongside M2.

The R-squared value indicates that the relationship becomes substantially stronger when both M2 and monetary velocity are included in the model, with the combined variables explaining more than half of the variation in Core CPI.

In addition, the F-statistic’s near-zero p-value suggests that the overall model is highly statistically significant, meaning there is a very low probability that these results are due to chance.

Finally, when the model’s implied Core CPI is plotted against actual Core CPI, the comparison shows that the combination of money supply and velocity tracks inflation much more closely than M2 alone. This supports the view that inflation dynamics are better understood as a function of both liquidity (M2) and its rate of circulation (velocity), rather than money supply in isolation.

Summary

There are valid reasons to buy and hold gold, but for short-term traders, it is important to understand the narratives that often drive gold price action.

The idea that rising money supply alone explains inflation—and therefore supports higher gold prices—can be misleading. As discussed, this relationship needs to be placed in proper context relative to economic growth. Equally important is not just the quantity of money in circulation, but the rate at which it circulates through the economy, or monetary velocity.

Many widely accepted macro narratives appear intuitive at first glance, but lose explanatory power once examined more closely. It is in these gaps between narrative and reality that investors can better understand the true drivers of asset prices—and reduce the risk of being caught offside when simplified stories fail to hold up in practice.

Most traders assume price moves are driven by news, indicators, or chart patterns.

But after spending enough time watching the market—especially in futures like NQ, ES, or Gold—you start to see a different driver at work:

Price moves because of liquidity.

Understanding liquidity isn’t just useful; it can be one of the strongest edges in trading. It helps explain why stops are often taken out before the real move begins, and why some breakouts fail while others accelerate aggressively.

Let’s break down two key concepts: liquidity sweeps and liquidity runs.

What Is Liquidity?

Before looking at specific setups, it’s important to understand this basic idea:

The market requires orders in order to move.

Large participants can’t simply enter huge positions at will—they need counterparties. They need liquidity on the other side of their trades.

So where does liquidity exist?

Above prior highs

Below prior lows

Around clear support and resistance levels

Near stop-loss clusters and breakout entry zones

These are exactly the areas where retail traders tend to place their orders. And these are also the zones that larger institutional players often target.

Liquidity Sweep: The Market Trap

A liquidity sweep occurs when price deliberately moves into areas where stop orders are concentrated, triggers them, and then sharply reverses.

This is often referred to as a “stop hunt.”

What it typically looks like:

Price pushes beyond a recent high or drops below a recent low Breakout traders get activated and stops are triggered Price quickly reverses in the opposite direction

Why it happens:

Large participants use this burst of liquidity to fill their own orders. Instead of chasing breakouts, they take advantage of the liquidity created by those breakout attempts.

Example (NQ or ES):

Price breaks above the morning high Retail traders enter long positions Shorts are stopped out as price moves higher Then price reverses sharply downward

That move above the high is the liquidity sweep.

How traders approach it:

Wait for price to take out a key level Watch for rejection signals (wicks, momentum shift) Enter in the opposite direction Target liquidity on the other side of the range

It’s essentially a reversal setup built around mean reversion after a liquidity grab.

Liquidity Run: The True Price Move

A liquidity run is the other side of the move.

Instead of reversing after grabbing liquidity, price continues in the same direction.

This is where strong trending moves form.

What it looks like:

Price breaks through a key level

Absorbs available liquidity

Then accelerates further in the same direction

Why it happens:

Once liquidity has been taken, there are fewer opposing orders left.

Stops are cleared

Resistance is weakened or gone

Momentum takes over

Example:

Price breaks out of a consolidation zone

Sweeps stops and triggers breakout entries

Then continues pushing in the same direction for an extended move

That’s a liquidity run.

How traders approach it:

Enter on breakout or retest setups

Confirm with momentum (volume, speed, market structure)

Trail stops as price expands