- This week, markets will be closely watching developments in the Iran conflict, movements in oil prices, and changes in global government bond yields.

- Ondas is recommended as a buy for traders who are comfortable with high-risk, high-reward situations, especially with earnings approaching.

- PDD is suggested as a sell because its slowing growth and looming regulatory challenges likely outweigh any short-term upside, particularly ahead of its fourth‑quarter earnings release.

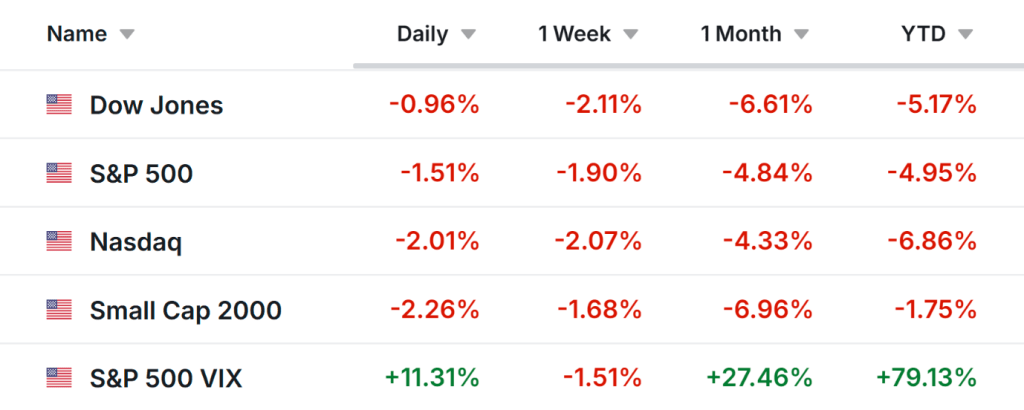

U.S. stocks fell sharply on Friday, with the S&P 500 ending at a six-month low, as tensions in the Middle East pushed oil prices higher, fueling concerns about inflation and the likelihood of rising interest rates.

The major U.S. stock indexes recorded their fourth consecutive week of losses. The Dow Jones Industrial Average fell 2.1%, the S&P 500 dropped 1.9%, the Nasdaq Composite slid 2.1%, and the Russell 2000 lost 1.7%.

Since the outbreak of the Iran conflict on February 28, the S&P 500 has declined 5.4%, the Nasdaq is down 4.5%, and the Dow has fallen nearly 7%. All three benchmarks are trading below their 200-day moving averages, highlighting the recent weakening of market sentiment.

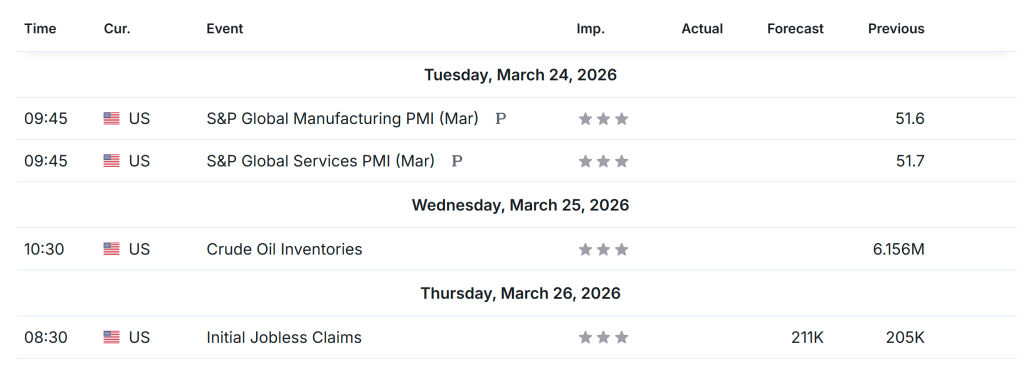

In the coming week, attention will continue to focus on oil prices, global bond yields, and developments in Iran.

U.S. economic releases are expected to be relatively light, with reports on manufacturing, services activity, and initial jobless claims scheduled for the week ahead.

Notable companies such as Carnival and Chewy are scheduled to release their earnings this week.

Additionally, a major energy conference in Houston, featuring leading executives from the global industry, may capture Wall Street’s focus.

Below, I outline one stock recommended for purchase and one to consider selling for the week of Monday, March 23, through Friday, March 27.

Recommended Buy: Ondas

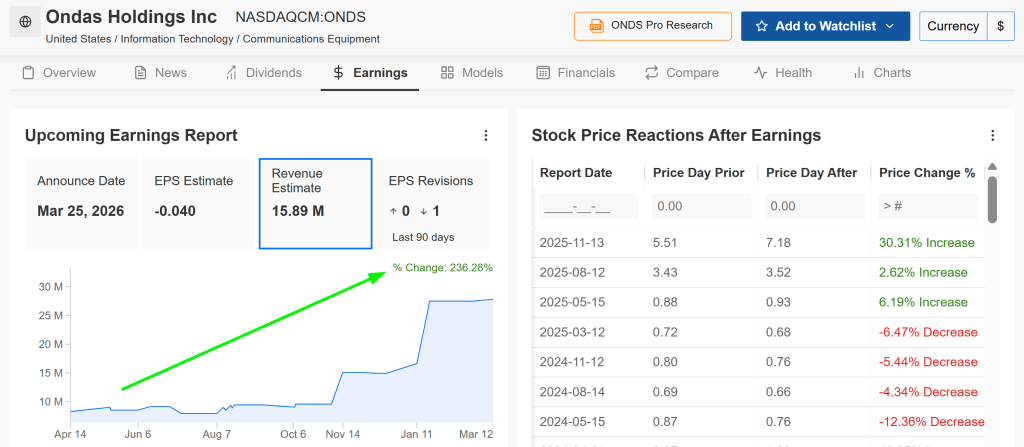

Ondas, a company specializing in private wireless networks and drone solutions, is scheduled to report its latest earnings this week. The firm is active in high-growth areas such as industrial automation and critical infrastructure, sectors that are rapidly embracing advanced wireless technologies.

Ondas will release its Q4 results on Wednesday, with a conference call set for 8:00 AM ET. Based on options market activity, investors are anticipating a potential move of roughly ±10% in ONDS shares following the announcement.

Ondas has already released updated preliminary results, reporting Q4 revenue of $29.1 million to $30.1 million—exceeding prior guidance of $27–$29 million—driven by strong demand in defense, homeland security, and critical infrastructure applications.

The company anticipates Q4 net income between $82.9 million and $83.4 million, with full-year net income projected at $50.4 million to $50.9 million, surpassing earlier estimates.

Management also reaffirmed its ambitious 2026 revenue target of $170–$180 million (excluding potential acquisitions), backed by a growing backlog and recent defense contract wins, including border protection systems and counter-drone solutions.

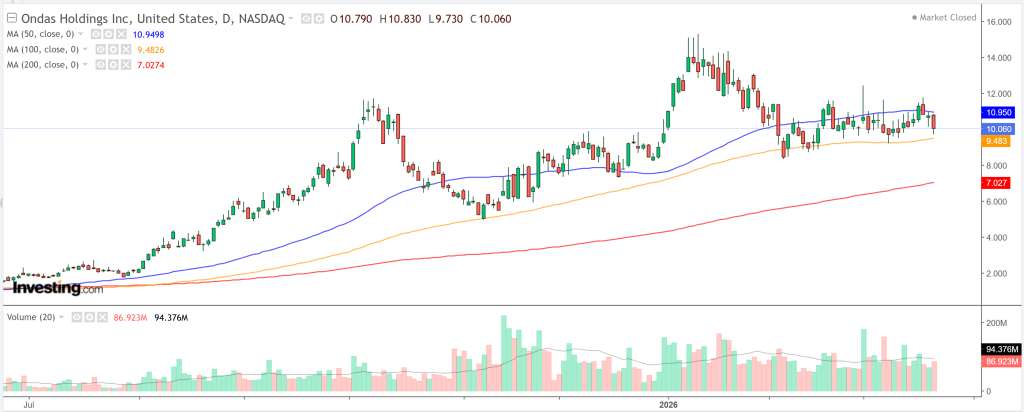

ONDS recently traded near $10, closing at $10.06 on Friday, following a pullback accompanied by strong trading volume. After an extraordinary one-year rally of roughly +1,300%, Ondas is now consolidating within a high-volatility symmetrical triangle. The stock is trading between $9.50 (rising support, aligned with the 50% Fibonacci retracement) and $11.50 (falling resistance), with the triangle nearly 80% complete.

This technical pattern indicates potential for a favorable earnings-driven move if the final results align with preliminary figures and guidance remains intact.

Trade Setup:

- Entry: $9.95 – $10.25

- Target: $12.00 (~20% potential gain)

- Stop-Loss: $9.35 (~6.5% risk)

Recommended Sell: PDD

In contrast, PDD Holdings, the parent company of Pinduoduo and Temu, heads into earnings week amid a pronounced downtrend. Despite strong growth in recent years, PDD faces increasing headwinds, including intensifying competition in China’s e-commerce market and rising global regulatory scrutiny, which could weigh on investor sentiment.

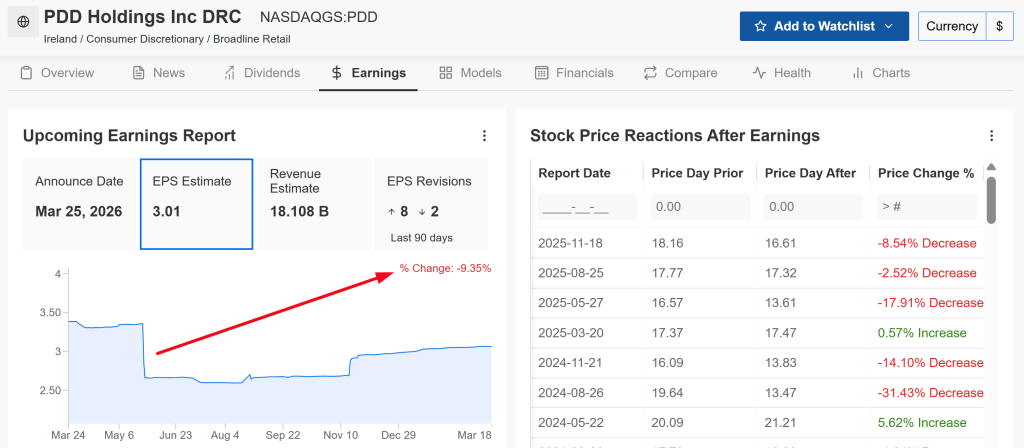

The company is scheduled to report its fourth-quarter results before the market opens on Wednesday. Options markets imply a potential ±6% move in the stock following the earnings release, highlighting the risk of an earnings miss.

Analysts expect year-over-year growth in both EPS and revenue, but recent quarters have fallen short, and the company faces broader challenges.

Temu’s rapid international expansion has driven up marketing expenses, potentially weighing on profitability. Additionally, PDD operates in a tightly regulated environment in both China and overseas, with recent scrutiny on data privacy and trade practices posing further risks.

Against this backdrop, even strong revenue results may not reassure investors if management provides cautious guidance or commentary, or if margins are pressured by ongoing subsidies and high marketing costs.

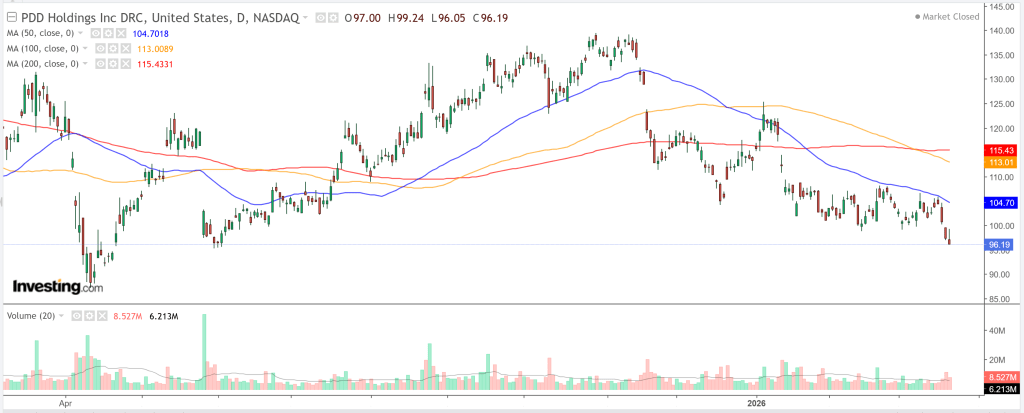

PDD has dropped nearly 25% over the past year, closing at $96.19 on Friday. The stock recently broke below key multi-month support at $97.00, signaling a textbook bearish breakdown.

Technical indicators reinforce the downtrend: the price is trading below all major moving averages (20-, 50-, and 200-day), the SuperTrend is red at $106.42, and the Ichimoku Cloud confirms a bearish outlook, with the next potential support zone around $90–$92.

Trade Setup:

- Entry: Near current levels (~$96)

- Target: $87 (~9.5% potential gain)

- Stop-Loss: $102 (~6.2% risk)

Disclaimer: This content is for informational purposes only and should not be considered financial advice. Always perform your own due diligence before making investment decisions.

Leave a comment